Medicare Advantage and Medigap are similar in some ways but very different in others. If you’ve enrolled in a Medicare Advantage plan and you don’t like it, you may think switching Medicare plans and enrolling in Medigap is a great idea. It’s important to understand the differences between the two, so you can make the best choice.

What is Medicare Advantage?

Medicare Advantage, also called Medicare Part C, is a type of private Medicare plan. When you first enroll in Medicare, you’ll start with Medicare Part A (the part that covers hospital care), and then most people will enroll in Medicare Part B (the part that covers doctor’s appointments).

Medicare parts A and B are limited, so adding Part C can give you additional benefits like:

Long-term care

Specialized care

Dental

Vision

Hearing

Physical fitness

Prescription drugs

No two Medicare Advantage plans are the same. In fact, there are several different types. You’ll have to look at what you’re eligible for and decide which benefits you need most and how much you’re willing to spend.

Medicare Part C doesn’t always mean spending more money, though. Some plans might even have $0 premiums!*

*Even with a $0 Medicare Advantage premium, you’d have to continue paying your Part B premium.

What is a Medigap plan?

Medicare Advantage plans sound fantastic, but some people will find that Medigap plans work best for them. Medigap coverage is what can “fill the gap” between what Medicare covers and what you owe out of pocket. These plans are also called “Medicare Supplement” plans because they supplement your existing Medicare Part A and Medicare Part B coverage.

Some Medigap plans may provide a few extra “perks,” but generally speaking, they do not provide additional health benefits in the same way that Medicare Advantage plans do. Instead, supplemental insurance covers your Medicare Part A and Medicare Part B deductibles, copayments, coinsurance, etc.

You’re probably thinking, “great!” I’ll just go ahead and get Medigap and Medicare Advantage. However, you can’t have both. That decision can be tough, but it all comes down to how much you’re able to spend each month and whether or not you can afford a medical emergency. For example, Medigap premiums tend to be a bit higher than Medicare Advantage, but if you’re in the hospital all the time, it might pay off.

Can I switch from Medicare Advantage to Medigap?

If you enroll in a Medicare Advantage plan and decide that a Medigap plan might be better, you can switch – but there are a few things you’ll need to keep in mind.

Mainly, Medigap plans come with medical underwriting. In other words, you can be denied for pre-existing conditions. Meanwhile, you will never be denied or charged more for a Medicare Advantage plan based on your preexisting conditions. There are two times when your preexisting conditions won’t affect your Medigap enrollment: when you’re enrolling in Medicare for the first time, and if you are forced out of your current plan and need to find a new one quickly. That rule is called “guaranteed issue rights.”

You’ll also have to keep in mind that if you had a Medicare Advantage plan with prescription drug coverage and you want to switch to Medigap, you will lose your prescription drug coverage. The only way to have a prescription benefit with Medicare Supplements is to also invest in a Part D (prescription drug) plan.

One of the many benefits to Medicare Advantage is that most of your benefits will be rolled into one plan, whereas if you have Medigap, you may have to seek alternative plans for your prescription drugs, dental, vision, etc.

Can I switch from a Medigap plan to an Advantage plan?

Just like switching from Medicare Advantage to Medigap, switching from Medigap to Medicare Advantage is possible, but there are some things to be aware of.

One of the first things you’ll notice when you switch plans from Medigap to Medicare Advantage is that your copayments might rise. This will all depend on what plans you have. For example, if you had Medigap Plan G (which covers Part B copayments), and then you switched to a Medicare Advantage PPO plan that had a $20 copayment for doctor visits, you might feel like your costs are rising. However, your Medicare Advantage plan might have a lower premium than your Medigap plan did, making your overall costs lower.

Confused? Your insurance agent can walk through these numbers with you before you switch plans to help you decide which type of plan is truly best for you.

Is it better to have Medicare Advantage or Medigap?

The question should read, “Is it better for ME to have Medicare Advantage or Medigap?” That may not be the answer you were looking for, but it is different for every person. What you may see as disadvantages of Medicare Advantage might be great for someone else. Common Medicare Advantage disenrollment reasons, like trouble finding a doctor in-network or the lack of one very specific benefit, may not apply to you.

While Medicare Advantage usually provides more covered benefits, Medigap can result in lower hospital bills and lower overall out-of-pocket costs.

Your decision should be based on your health history, your budget, and the quality of plans available in your area. Try sitting down and writing a pros/cons list for Medicare Advantage vs. Medigap, like this:

Medicare Advantage:

Pros: Prescription drug coverage can be included

Cons: Stricter network

Medicare Supplements:

Pros: Copayments can be covered

Cons: Higher premiums

Add in any items specific to you, like a specific benefit that you need or a specific cost that you are worried about. Then, circle the items that are most important to you. Whichever column has the most circled items is likely the best option for you.

Why should I switch Medicare plans?

There are plenty of reasons to switch Medicare plans. Everything from network size to costs and benefits can be a factor.

You may want to switch Medicare plans if:

Your plan doesn’t cover all of your healthcare needs.

The premiums are too high.

Your favorite doctors are not in-network.

The costs are not worth the benefits you’re receiving.

A better plan becomes available in your area.

You become eligible for a cheaper or more specialized plan.

When can I switch from Medicare Advantage to Medicare Supplement?

Unfortunately, switching Medicare plans is not always easy. If you have a Medigap plan, you can switch to another Medigap plan at any time. However, if you already have Medicare Advantage and want a new Medicare Advantage plan, or if you have Medigap but want to switch to Medicare Advantage, you’ll have to wait for one of three* Medicare Advantage enrollment periods:

Annual Enrollment Period: October 15 – December 7 of every year, applies to all Medicare beneficiaries, any change is allowed

Special Enrollment Period: Applies only to those with specific circumstances, such as a special medical or financial need, and allows enrollments at specific times outside of AEP and OEP

Open Enrollment Period: January 1 – March 31 of every year, allows those with Medicare Advantage to make one switch to a different Medicare Advantage plan or drop coverage

*The fourth Medicare Advantage enrollment period is when you first become eligible for Medicare and is called the Initial Enrollment Period. This is when you would enroll in Medicare Part A and Part B for the first time and can choose to also enroll in Medicare Advantage (or Medicare Supplements and Part D).

When can I switch from Medicare Advantage to Medigap without losing guaranteed issue rights?

When you lose your current coverage for reasons beyond your control

Additionally, Medicare.gov identifies a few specific circumstances that can grant you guaranteed issue rights, including:

Your Medicare Advantage plan leaves your service area, or you move out of the plan’s service area.

You have Part A and Part B, and now your employer coverage is ending.

You joined either a Medicare Advantage plan of PACE (Programs of All-Inclusive Care for the Elderly) upon turning 65 and decided to switch within the first year.

You switched from Medigap to Medicare Advantage and want to switch back within less than one year.

Your policy’s company mislead you or broke a rule.

When You Can Change Medicare Advantage Plans

If you don’t want to switch between Medigap and Medicare Advantage and you simply want to disenroll from a Medicare Advantage plan or switch to another, you can do that during one of the Medicare Advantage enrollment periods.

CMS added the Medicare Advantage disenrollment period in 2020 to give beneficiaries another chance to switch without having to wait a full calendar year. This Medicare disenrollment period is actually the “Open Enrollment Period” lasting from January 1 through March 31. You are only eligible if you already have Medicare Advantage.

If you’d prefer to switch from Medigap to Medicare Advantage or make any other types of changes, you can do that during the annual election period in the fall, which is sometimes referred to as “Medicare open enrollment,” though it should not be confused with the Open Enrollment Period.

If you qualify for a Special Enrollment Period (SEP), you can make changes outside of the traditional enrollment periods. Common reasons that you might qualify are if you moved to a new plan service area (or your plan leaves your service area, you move into or out of a long-term care facility, you are also eligible for Medicaid, or you have a medical condition that qualifies you for a Special Needs Plan.

Can I Change my Medicare Advantage Plan If I Move?

You can (and may have to) change your Medicare Advantage plan if you move. Medicare Advantage plans are confined to specific service areas. Some are confined to specific counties or zip codes, while others are state-wide. If you leave that service area, you will need to change plans.

Additionally, moving to a new service area grants you a Special Enrollment Period. That means that from the date that you are officially living in the new area, you will have 60 days to switch Medicare Advantage plans. If you wait too long, you will have to wait until the Annual Enrollment Period rolls around again.

Switching Medicare Advantage Plans with Pre-existing Conditions

If you have preexisting conditions and want to switch into a new Medicare Advantage plan, you do not have to worry about medical underwriting. Medicare Supplement (Medigap) plans are the only type of Medicare plan that may require medical underwriting. Original Medicare (parts A and B), Prescription Drug Plans (Part D), and Medicare Advantage plans (Part C) all cannot deny you coverage based on your health history.

How to Switch Medicare Plans: Step by Step

When you think you’re ready to switch Medicare plans, follow these steps to ensure a successful switch:

Review your current benefits and make notes about what you like and what you don’t like about your current plan.

Meet with an insurance agent who can help you fill out your application correctly and answer all your questions (for no additional fees).

Tips for choosing a Medicare plan

Choosing a Medicare plan is a very personal process. Your Medicare coverage goes beyond copayments and deductibles. It can determine how prepared you are for emergencies, it can affect the quality of care you receive, and it can alter your lifestyle based on the benefits included.

Some people might find that traditional Medicare (parts A and B alone) is all they need, but most people will likely want to look for a prescription drug plan or some other benefits as well. No two health plans are the same. Some are very simple, covering basic needs and prevention, and others are complex, offering unique benefits like gym memberships and meal delivery.

When choosing your Medicare coverage, keep the following tips in mind:

What works for your spouse or friend may not work for you.

Always make sure your favorite doctors are in the plan network before you enroll.

Before selecting a prescription drug plan, verify that the prescriptions you need are covered.

Remember to look at all costs: premiums, copayments, deductibles, and coinsurance. It’s easy to get excited when you see one low number, but everything together can add up.

It doesn’t cost you anything to meet with an insurance agent who already understands the plans. They might even be able to help you save money.

We Can Help You Decide Which Coverage You Need

Changing your Medicare plan from Medicare Advantage to a Medicare Supplement is a big decision. Our licensed agents are highly trained, and they can help you find the plans available in your area. Your agent can discuss the pros and cons of MA and Medigap and help you make the decision that best fits your needs. To set up a no-cost, no-obligation meeting with an agent, call 1-844-431-1832 or contact us here today.

Home Health Tests Seniors Should Try

We’re all aware we should make an effort to regularly see our physicians. But we also know that life tends to get in the way.

Especially for seniors, transportation and cost can often prevent routine doctor visits. However, just because you can’t get to your doctor’s office, doesn’t mean you have to stay in the dark about your health. There are quite a number of tests that you can perform without ever leaving home!

Tests You Can Do At Home Today

The range of at-home tests and testing methods varies widely. Some require expensive medical equipment only available through a supplier and with a prescription, while others require only a pen and paper. Here are some tests that you can do today with little to no supplies

SAGE Test for Dementia

The Self-Administered Gerocognitive Exam, or SAGE, was devised by researchers from the Wexner Medical Center at Ohio State University. SAGE can help detect early warning signs of cognitive impairment and memory loss in less than 15 minutes.

The test has several components and several forms, all of which can be viewed and downloaded at the Wexner Medical Center’s website. These include sections on orientation, language, memory and visuospatial awareness.

The most well-known element of the SAGE is known as the clock drawing test. All you need to do is get out a pen and paper and draw a picture of a clock, with the hands reading 3:40. Then compare your drawing to a real clock to see how you scored.

If your circle is closed, give yourself a point. If all twelve numbers are accounted for and in the right place, you get two more points. If your hands are in the correct position as well, you passed with flying colors. A score of any less than three points, however, might be an indication that you should see your physician for further screening. This test is sometimes performed without the rest of the exam, though it is usually recommended to perform the entire SAGE test for dementia detection.

Free Medicare 101 Course

Window Test for Vision Loss

Our eyes take a lot of abuse these days from the onslaught of screens and artificial lighting. It’s even more severe as we get older and the natural, age-related loss of vision begins to take effect. If you experience some trouble reading, give yourself this informal at-home eye exam to judge whether or not you should seek an eye care professional.

First, sit across the room from a large window or door so that you can see all the lines of the frame around it. Cover one eye and focus on the window or door frame with your open one for 30 seconds. Then repeat with the opposite eye. The horizontal and vertical lines of the frame should be clearly visible with no missing or hazy areas. If the edges of the frame seem distorted or warped, this may indicate macular degeneration, a disease that is currently the leading cause of irreversible vision loss in people over 60.

Cushion Test for Peripheral Arterial Disease

The cushion test can be performed without even getting out of bed! It can help detect blocked arteries in your legs and feet, a condition known as PAD, or peripheral arterial disease. Those with high blood pressure or diabetes, both common among seniors, are especially at-risk for this disease.

To perform this test, lie on a bed and elevate your legs with pillows or cushions until they are resting at a comfortable 45-degree angle. Keep them there for one minute, then sit up and swing your legs over the side of the bed so that they hang at an angle of 90 degrees. If either or both of your legs turn pale when elevated and take several minutes to return to their normal shade after sitting up, you may need to consult your physician with the results from this peripheral artery disease test.

Phalen’s Maneuver for Carpal Tunnel

We are an increasingly computer-savvy society and people of all ages are typing more than they used to. Extended periods of typing are strongly associated with carpal tunnel syndrome, a painful condition caused by a pinched median nerve in the wrist, but many other activities like driving can bring on these symptoms as well. Furthermore, people over 55 years old are at a much higher risk and those over 65 are more likely to have cases that are severe.

Phalen’s maneuver is a test devised to diagnose carpal tunnel at home and has been shown to be surprisingly effective. To see for yourself, press the tops of your hands together with your fingers pointing toward the floor and your elbows extended. If you can, hold this position for a full minute. If you feel an unpleasant sensation, such as prickling, tingling, or burning, you may likely have carpal tunnel and should consider preventive measures.

Check out this video from Physiotutors on YouTube that explains how to perform the Phalen test:

Testing With Medical Equipment

Some at-home health tests will require special instruments to fully gauge the results. While many of these items can be freely obtained from online and brick-and-mortar retailers, some require ordering through a medical supplier with a doctor’s prescription. Below, we will detail some of the testing you can do at home with the help of specially-designed medical equipment.

Blood Sugar Test

For the 12 million seniors living with diabetes* (about 25% of those over the age of 65), monitoring blood sugar levels is an near-constant concern. Luckily, this is something that can be checked at home or on-the-go using a blood glucose monitor, or glucometer. These can be found online or in pharmacies in the form of kits, which include testing strips, needles (called lancets), and the glucometer itself.

To test blood sugar at home, you will need to insert a test strip into the electronic monitor and prick the side of your finger with the provided lancet. Gently apply pressure to that finger until you see a drop of blood form, then touch it to the edge of the test strip. In just a few seconds, you will have an accurate metering of your current blood sugar levels, no matter where you are.

Blood Pressure Test

Along with heart rate, breathing rate, and body temperature, blood pressure is one of the four most significant vital signs that our bodies produce. High blood pressure can be caused by countless factors like high cholesterol, stress, and even fear, and affects almost 70% of adults between the ages of 65 to 74. Monitoring blood pressure accurately is vitally important, as symptoms may not manifest until these levels are dangerously high. Doctors maintain accuracy by using large, costly machines but there are ways to test blood pressure at home with minimal equipment.

The quickest and most accurate results will come from automated, electronic blood pressure monitors that come with an upper arm cuff. Many different brands of at-home blood pressure cuff exist and can be found at pharmacies or similar retailers. The directions for use may change from model to model but there are certain rules that apply no matter what brand you use, including placing the cuff directly on the skin, placing the feet flat on the floor, elevating the arm to chest height, and avoiding smoking or drinking for 30 minutes before testing.

At-Home Lab Tests

Another popular method of in-home health testing comes in the form of test kits that can be ordered right to your door. These vary widely, not only in terms of what is being tested, but also in the method of sample collection. Some services will send a team of professionals to administer and retrieve your test, while others will only send instructions and require you to send your samples back in the mail for results. These can be purchased to test for a wide range of conditions, including food sensitivity, hormone testing, DNA testing, and other at-home blood tests.

Medicare DME Coverage

Medical equipment may be needed for certain tests.

Durable medical equipment, or DME, is a designation that Medicare uses to classify coverable medical equipment that can be used in the home. This benefit might be used to cover the cost of equipment to aid in the at-home testing we have already covered. The covered equipment can range from crutches and canes to CPAP devices and hospital beds, though it all must come from a Medicare-approved medical supplier.

Medicare-Approved Glucose Meters

Blood sugar monitors and test strips are usually covered under Medicare Part B as durable medical equipment for home use with a doctor’s prescription. You may be able to rent or buy a glucometer but Medicare will only provide coverage if both your physician and the supplier are both enrolled and participating in Medicare. Be sure to clarify this with your doctor and equipment supplier, as some may be enrolled but not “participating” and may not accept the cost of assignment.

Medicare Part B may cover the cost of a blood pressure monitor or ambulatory blood pressure monitoring (ABPM) device but only under very specific circumstances. Part B will cover a blood pressure monitor and stethoscope for those who receive blood dialysis treatment in their home and will pay for the rental of an ABPM device for patients who have exhibited “white coat hypertension,” a phenomenon where nervousness in clinical settings causes artificially high blood pressure readings.

For those with Medicare Part C, or Medicare Advantage, all the benefits of Parts A & B will be covered but may also include additional benefits and expanded coverage. Contact your insurance company to find out if your Part C plan covers blood pressure monitors or glucometers.

If you don’t have a Medicare Advantage plan, give us a call at 844-431-1832 or contact us online to speak with a licensed agent and find a plan that can address your healthcare needs!

2020 Medicare Plan Finder: How to Find the Best Medicare Plan in 2020

It’s time to start thinking about what you want your Medicare coverage to look like next year. Did your current plan change? Did you develop a new health condition and need more coverage? Are you enrolling in Medicare for the first time?

No matter your situation, the Annual Enrollment Period (AEP) runs from October 15 through December 7. If you used AEP to enroll, your plan became effective on January 1, 2020.

By now, you may have realized that there are hundreds of Medicare plans out there, all offering slightly different benefits at different costs. So how do you choose?

The best Medicare plan for 2020 is the one that fulfills your needs. To figure out which Medicare plan is best for you, ask yourself the following questions:

What specific medical services do I need coverage for (ex: lab tests, blood work, surgery, chemotherapy, dental, etc.)

How much room do I have in my budget? Am I able to pay a little more to have more benefits?

Would I rather pay more on a monthly basis and pay very little when I visit the doctor, or is it better to pay a small amount every month but risk having higher copayments?

Who are the doctors and other providers who I want to be covered in my plan?

What prescriptions do I need coverage for?

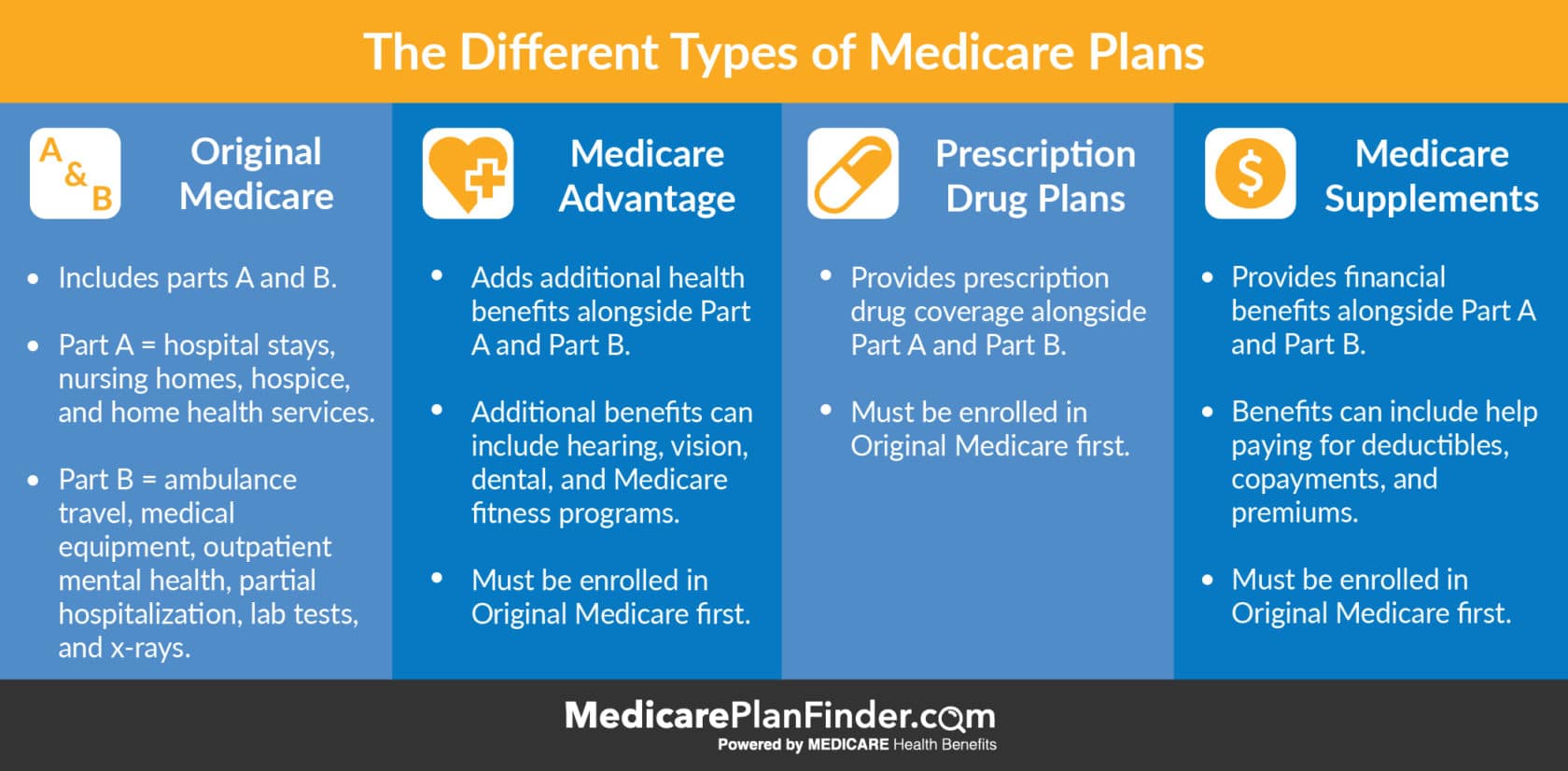

Start by Choosing a Type of Plan

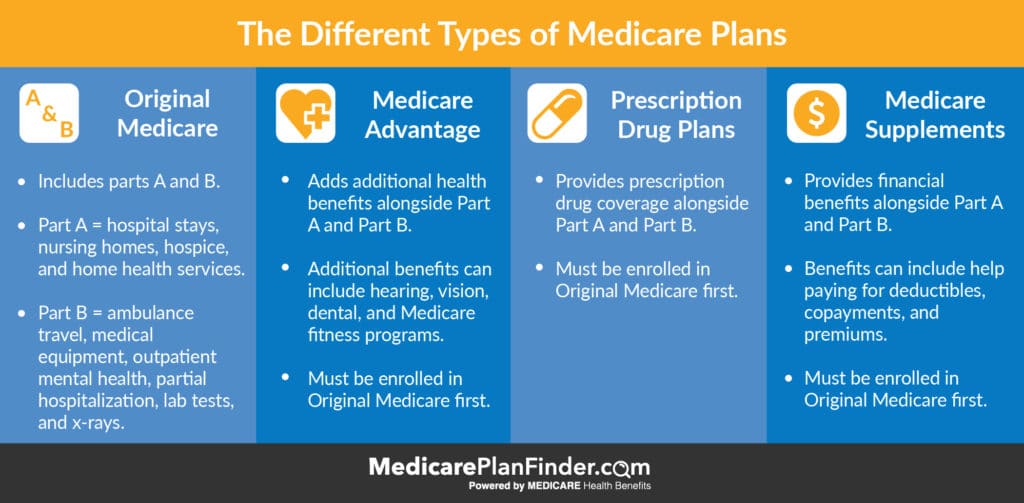

There are four main types of Medicare plans to consider when you begin your Medicare plan search. Start by comparing Original Medicare, Medicare Advantage, Prescription Drug Plans, and Medicare Supplements.

Keep in mind that you cannot have Medicare Advantage and a Prescription Drug Plan at the same time. You also cannot have Medicare Advantage and a Medicare Supplement plan at the same time.

Which plan or combination of plans works best for you?

Medicare Advantage: A private plan that you can purchase once you have Original Medicare. Can add additional benefits such as hearing, vision, dental, fitness, etc. Can include a prescription benefit.

Prescription Drug Plans: Another type of private plan that you can purchase once you have Original Medicare. Usually only includes a prescription benefit.

Medicare Supplements (Medigap): Another type of private plan that you can have in addition to Original Medicare. Adds more financial coverage, like for copayments and deductibles.

You can choose from the following combinations:

Original Medicare only

Original Medicare and a Prescription Drug Plan

Medicare Advantage

Medicare Advantage with Prescription Drug Coverage

Medicare Supplement

Medicare Supplement AND standalone Prescription Drug Plan

Types of Medicare Plans

Original Medicare Only

Having Original Medicare only means you’ve enrolled in the government program, Medicare Part A and Part B, but you have not enrolled in an additional (private) plan. Parts A and B can cover some of your hospital and medical costs, but they do not cover prescription drugs and other additional benefits such as dental and vision.

Original Medicare and a Prescription Drug Plan

If you don’t think you need any other medical benefits aside from what parts A and B cover, but you do need prescription drug coverage, you can enroll in a standalone prescription drug plan in addition to your Original Medicare.

Medicare Advantage

With a Medicare Advantage (MA) plan, you’ll still have to pay your Part B premium, but you can get other benefits. MA plans can include additional health benefits such as fitness program memberships, dental care, vision, and more.

Choosing a Medicare Advantage Plan

So, did you decide to go with Medicare Advantage? Great! Now, there are a few types of Medicare Advantage plans that may be available for you. First, ask yourself whether or not you need a large network and whether the freedom to see any doctor is important to you. Then, read through these important differences:

HMO Plans (Health Maintenance Organization) – You’ll select one primary physician. In some cases, you may only receive coverage for that one doctor (unless he or she refers you to a specialist). Requirements may vary based on your plan.

HMO-POS Plans (Point-Of-Service) – You’ll select one primary physician, but you’ll have the freedom to visit any specialist in your network for your other needs. You will be charged a fee for visiting specialists.

PPO Plans (Preferred Provider Organization) – You can see any doctor, but your costs will usually be lower if you choose one that is in your network.

PFFS Plans (Private Fee-For-Service) – You will not need referrals or a primary physician, but you’ll have to pick a doctor that accepts your PFFS plan.

SNP (Special Needs Plans) – Designed for those who are eligible for both Medicare and Medicaid, live in a nursing home, or have a chronic illness or disability.

MSA (Medical Savings Account) – Works like a tax-free savings account for your medical bills. Medicare will deposit money into your HSA. You can use that account to pay for medical expenses.

Medicare Advantage with Prescription Drug Coverage

Some select Medicare Advantage plans come with a prescription drug benefit. This is important because you can’t have BOTH a Medicare Advantage plan and a standalone prescription drug plan. If you like the idea of Medicare Advantage but need prescription coverage, a “MAPD” or Medicare Advantage Prescription Drug Plan may be right for you.

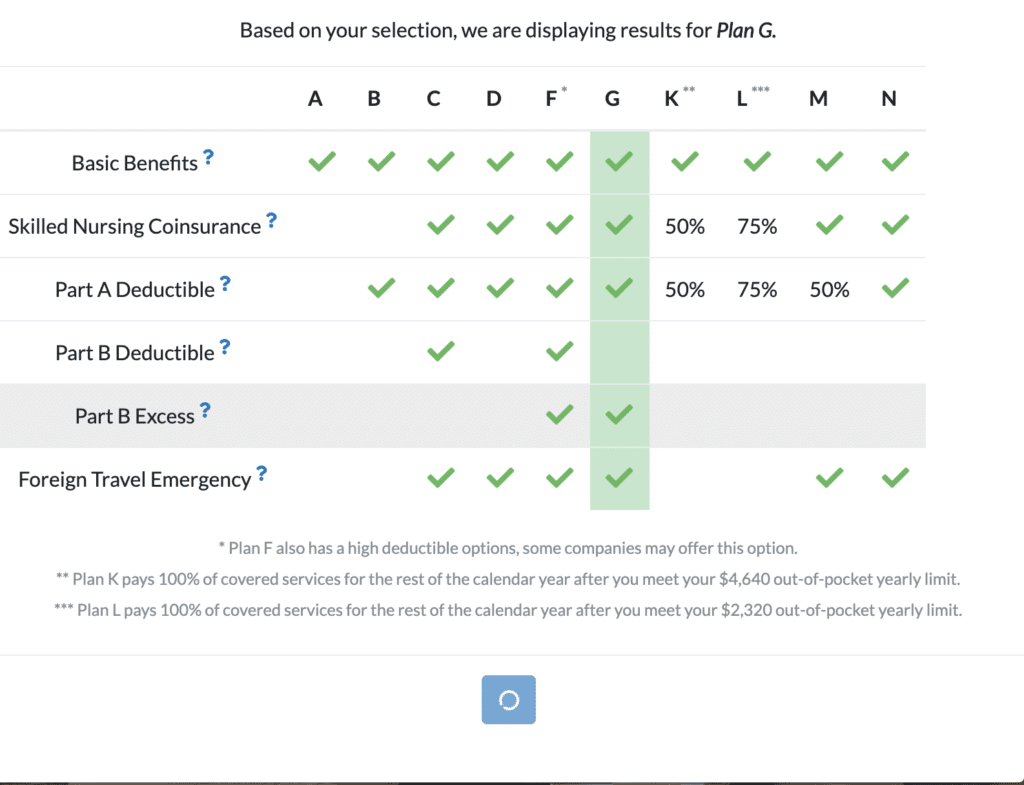

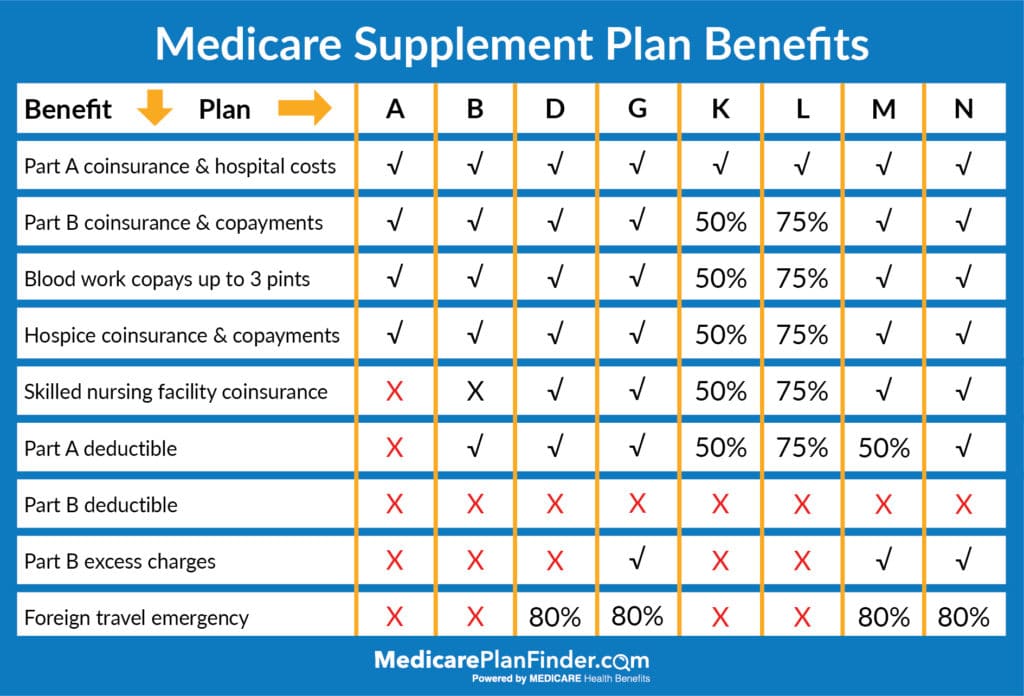

Medicare Supplement

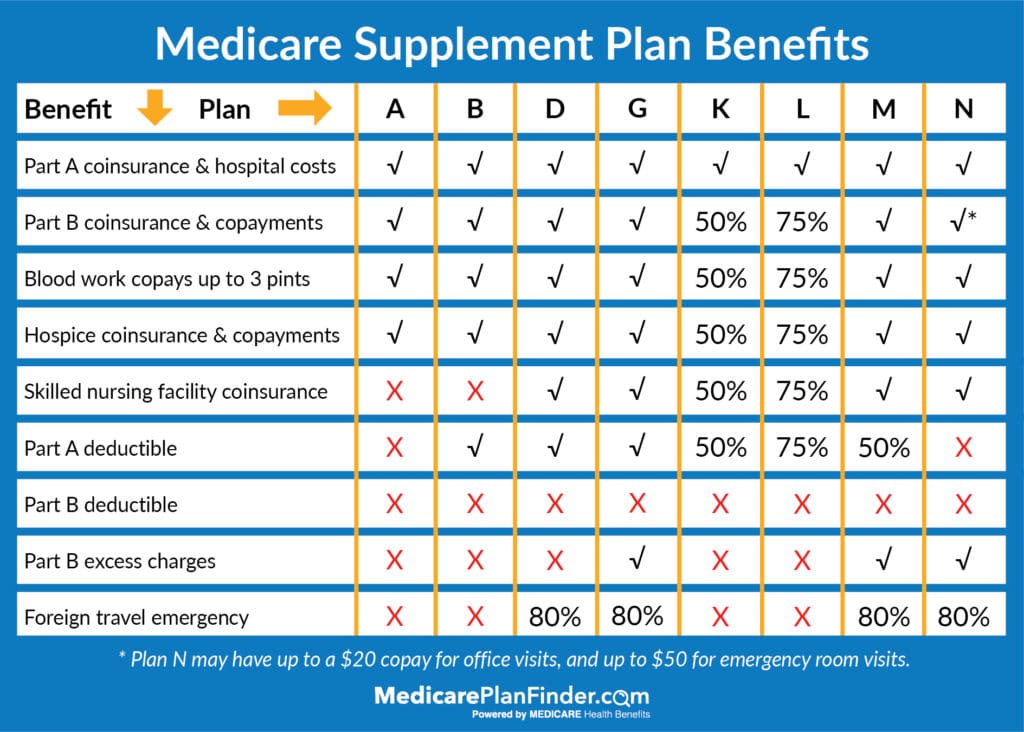

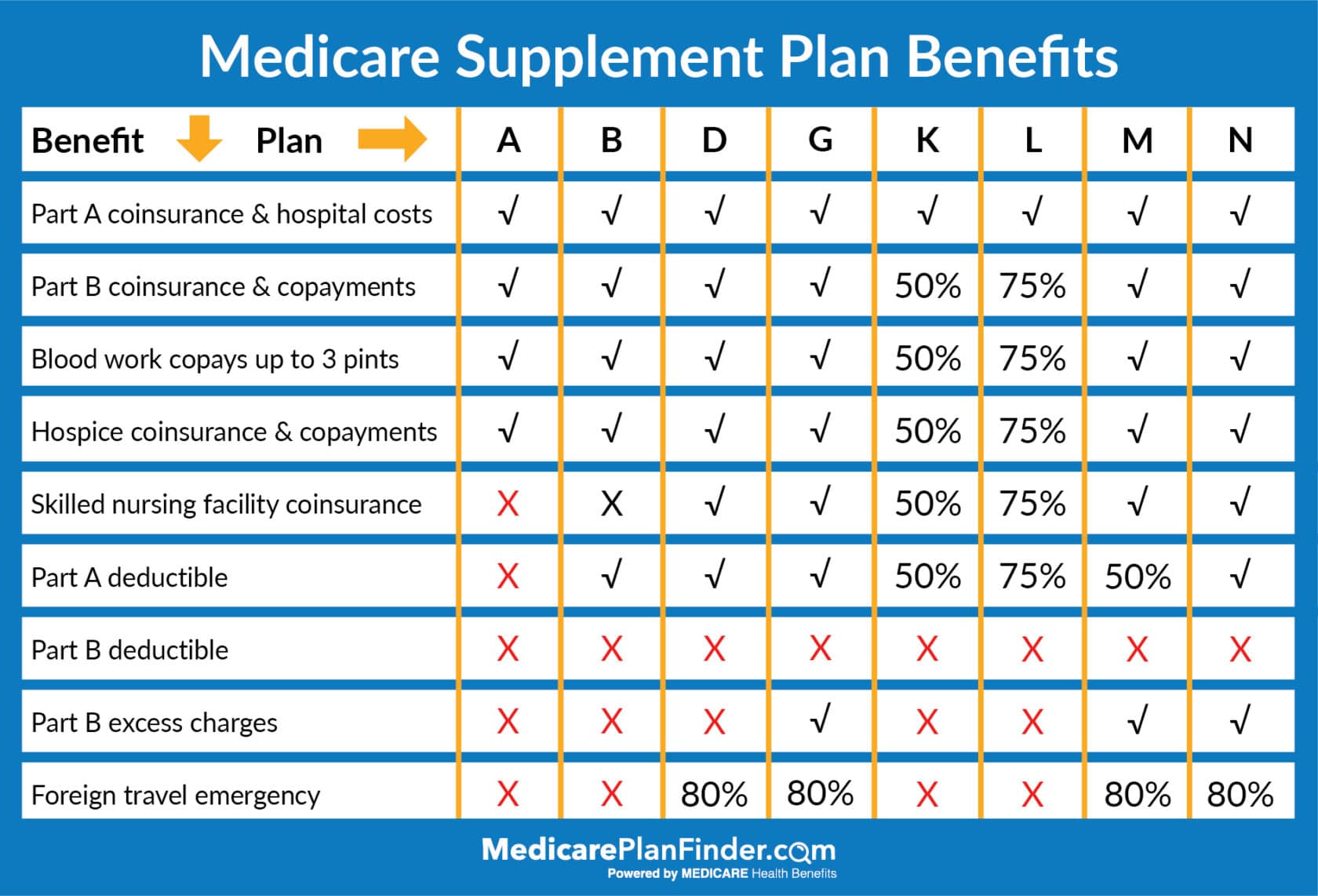

Sometimes called “Medigap,” Medicare Supplement plans bridge the gap between your Part A and B costs and your out of pocket costs. For example, Medigap Plan A covers Part A* coinsurance and hospital costs, Part B coinsurance and copayments, up to three pints of blood, and hospice coinsurance and copayments. It does not offer additional health benefits, but it eliminates many of the costs that come with Part A and B.

The best Medicare Supplement plan is the one that fits your needs at the time. For example, you might not need skilled nursing care when you first sign up for Medicare, so Plan A might work best for you. Eventually, your health condition may require more inpatient services and skilled nursing services, so Plan D may be a better fit.

*Be careful not to confuse Part A with Plan A

2020 Medicare Supplement Comparison Chart

Medicare Supplement AND a Prescription Drug Plan

Medicare supplements do not offer any prescription coverage, but you are able to enroll in both a Medicare Supplement plan and a standalone Prescription Drug Plan at the same time.

What is the Best Medicare Plan in 2020?

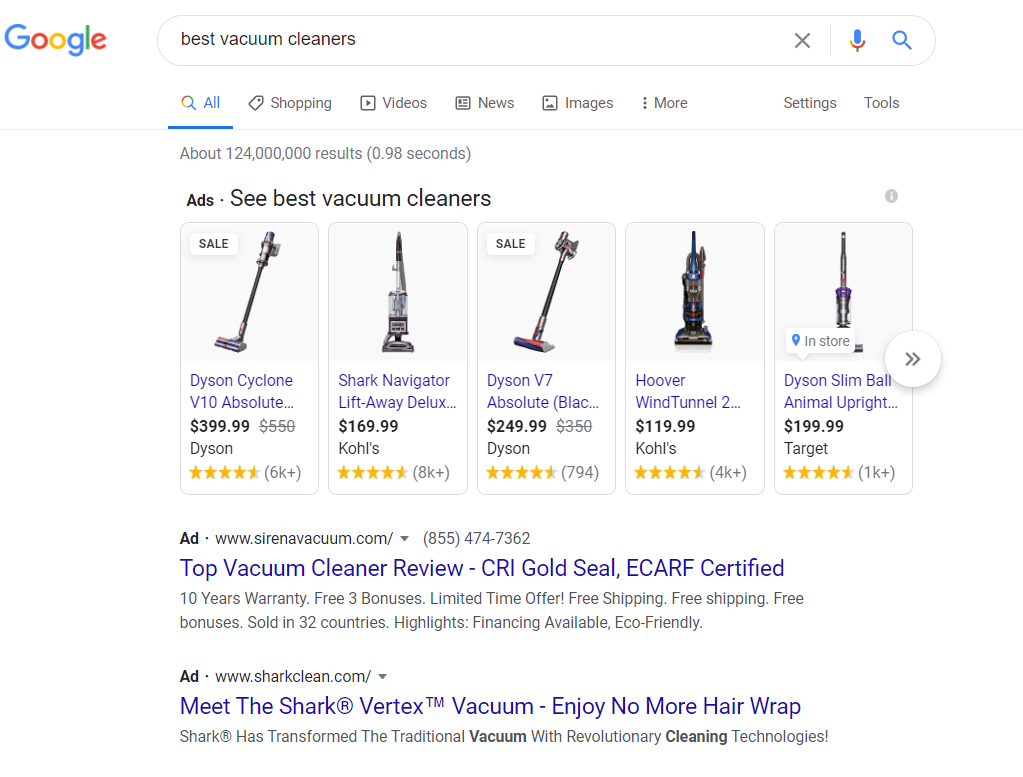

Everyone wants to know what the “best” Medicare plan is, but just like shopping for anything else, “best” can be subjective. If you were shopping for a vacuum cleaner, you’d probably search “best vacuum cleaners,” too, but what would you find?

We did that part for you, and we got about 228,000,000 results. You’re never going to sort through all those options, right?

Google search results for “Best Vacuum Cleaners”

When you really want to narrow down the best vacuum for your needs, you’re probably going to filter your search by price, capabilities, maybe even the size of the vacuum…any number of things that are going to narrow down your choices to what you really want to purchase.

While there probably aren’t 124,000,000 Medicare plans available to you, there are far too many for this to be a quick Google search! Like choosing the “best” vacuum, choosing the “best” Medicare plan for you requires some research.

Medicare Plan Finder Tool

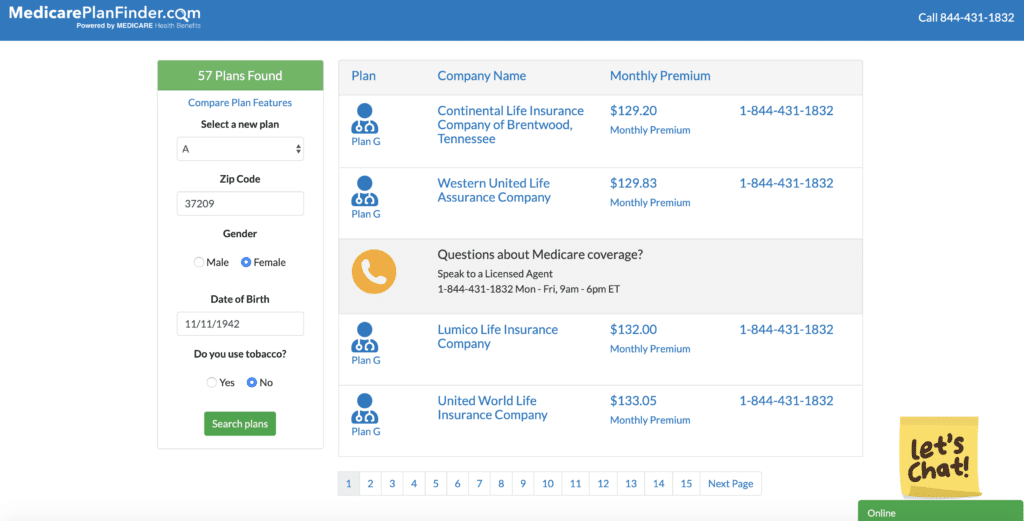

Our Medicare Plan Finder tool compares plans from carriers in your area. You’ll have to tell us your birthdate and a few other things so that we can determine what you’re eligible for.

Once you’ve entered your information, you’ll see a graph showing you the names of the plans and the potential premiums you might owe for those plans. This is a great place to start your research.

We ran a sample search for a 76-year-old non-smoking woman in Nashville who wanted a low premium to show you what the results look like. Your online Medicare Plan Finder results may not look the same.

2020 Medicare Plan Finder Tool Search ResultsMedicare Plan Finder Tool (These search results may not be an accurate representation of your search results)

New Medicare.gov Tool

You may have heard the buzz about Medicare.gov’s new plan finder tool. They’re offering a “new and improved” experience after getting complaints about their old tool.

To use Medicare.gov’s tool, you’ll need to enter your Medicare number and some other information. Then, you’ll see a graph of the plans available in your area.

Scour the Internet

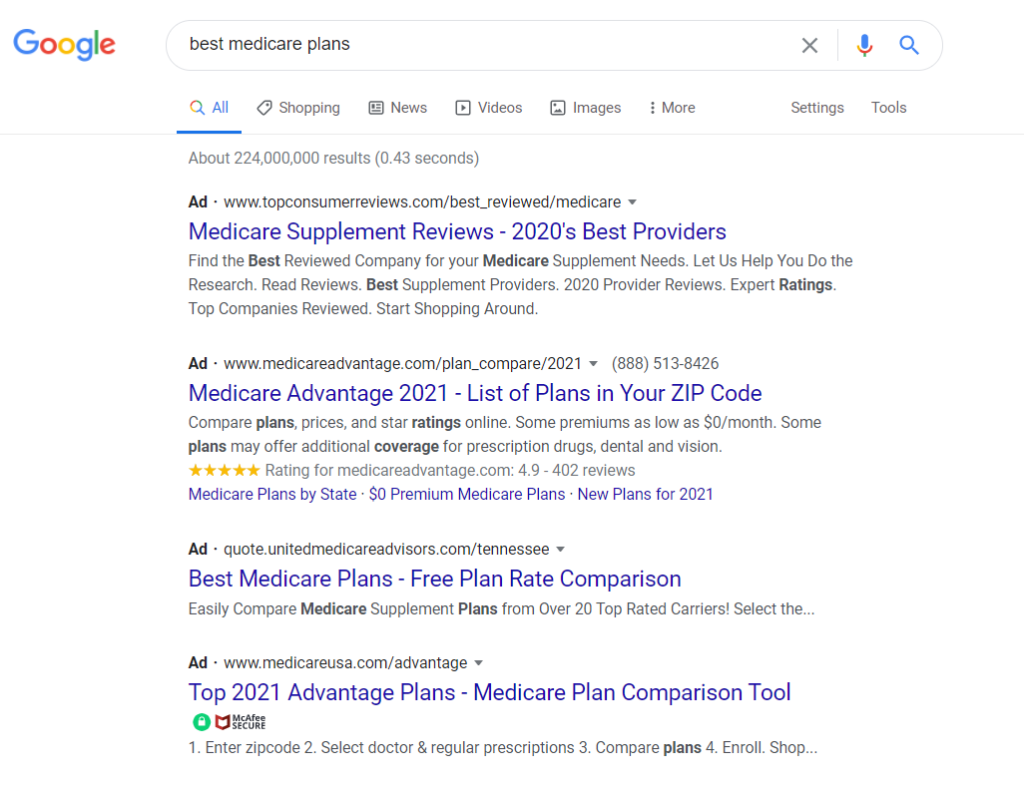

We don’t recommend this option, but you could start your Medicare plan shopping experience with a quick Google search. However, watch what happened when we Googled “best medicare plan.” The first four search results are ads.

Best Medicare Plans

The other thing you can try is going directly to the carrier websites, if you already know the name of a company you’d like to purchase from. However, keep in mind that those websites are only going to show you a select group of plans that they alone offer. You could be missing out on better plans from different carriers.

Meet With a Licensed Agent

Another option for Medicare plan research is to let a licensed agent do the work for you.

Let’s go back to our vacuum cleaner example. Imagine if you had someone do all the vacuum research for you and then present you with only one or two options that meet your needs. Imagine if that service was free, and all you had to do was talk to the agent for a few minutes to hear about all the benefits. What if the vacuum didn’t cost anything different just because you bought it from the agent instead of Amazon. Wouldn’t you take that deal?

At MedicarePlanFinder.com, we have agents across 38 states that can help you sort through your Medicare options and narrow it down for you. The appointments are free and easy, and you won’t pay any more for your Medicare plan whether you buy it from a licensed agent or online by yourself.

The difference is that our agents are experienced and can tell you all the ins and outs of your plan options (maybe even more than what is advertised online)!

Ready to get started? Give us a call at 844-431-1832 or click here to have an agent call you.

When Can You Enroll in Medicare in 2020?

Your enrollment periods will depend on a few factors, such as:

What type of coverage are you hoping to enroll in?

Are you over the age of 65?

Do you have a chronic condition or low income that qualifies you for a Special Enrollment Period?

Do you have a qualifying life event such as moving to a new state where different plans are available?

Medicare Enrollment Periods | Medicare Plan Finder

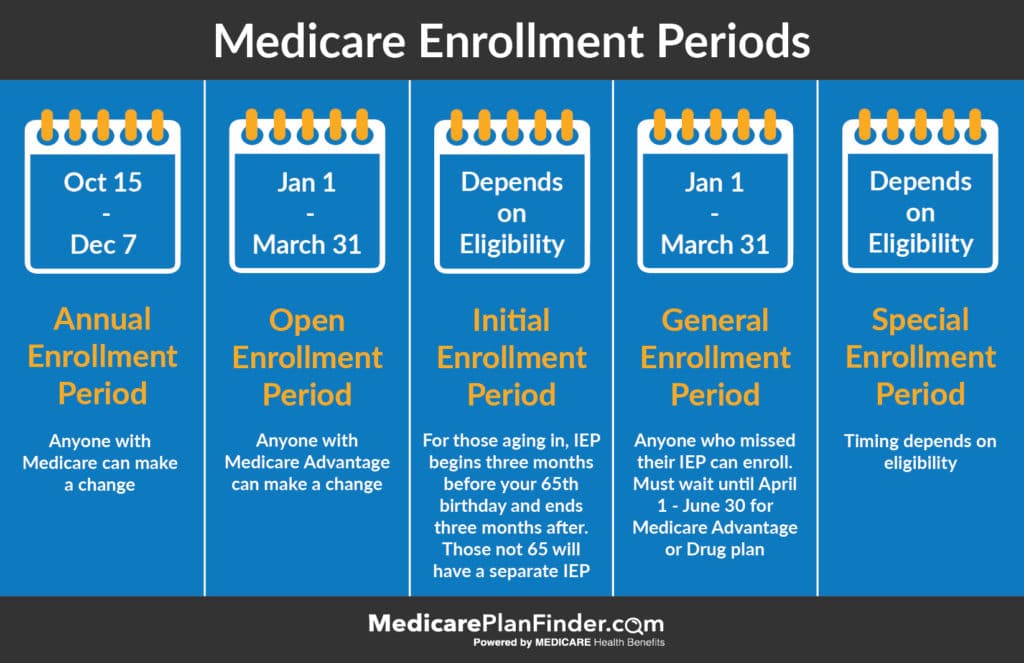

Initial Enrollment Period

Your Initial Enrollment Period is the time you get started with Medicare coverage.

If you are eligible for Medicare due to age (you are over 65 or about to turn 65), your Initial Enrollment Period will last from three months before your 65th birthday through three months after.

Initial Enrollment Period Medicare

If you qualify for Medicare for another reason, such as having a disability or chronic illness, your Initial Enrollment Period will be the month of your diagnosis.

Annual Enrollment Period

Once you’ve enrolled in Original Medicare (Parts A and B), you’re eligible for the Annual Enrollment Period. The AEP runs from October 15 through December 7 of each year. During this time, you can enroll in Medicare Advantage or Part D (prescription drug coverage).

Special Enrollment Period

There are two types of Special Enrollment Periods: Immediate/consequential and “long-term”. If you qualify for an immediate Special Enrollment Period, you typically have 90 days to make a change following a major life event. If you qualify for a “long-term” special enrollment period, you are able to change plans once per quarter for the first three quarters of the year (and during AEP, which falls during the fourth quarter of the year). Keep in mind that a SEP is never truly permanent, as you could lose your eligibility at any time due to a major life change.

To qualify for an “immediate” SEP, you must incur a major life change such as moving to a new service area that has different plans available (a different zip code), moving into or out of a medical facility, gaining or losing Medicaid eligibility, etc. You can also gain a SEP if your plan decides to leave the Medicare program

To qualify for a “long-term” SEP, you must be:

Eligible for Medicaid,

Eligible for a Medicare Savings Program,

Eligible for a Special Needs Plan, or

Eligible for LIS (Extra Help)

Other Enrollment Periods

Technically, there are two other Medicare enrollment periods as well.

The General Enrollment Period runs from January 1 through March 31 and is a time when people who missed their Initial Enrollment Period can sign up for Medicare parts A and B. The Open Enrollment Period also runs from January 1 through March 31 and is for those who selected a Medicare Advantage plan during AEP and changed their mind.

It’s important to make note of all the Medicare enrollment periods and which ones you are eligible for so that you don’t miss your chance to enroll!

Ready to get started? Give us a call at 844-431-1832 or click here to have an agent call you during your enrollment period.

This post was originally published on October 16, 2019, and was last updated on November 13, 2020.

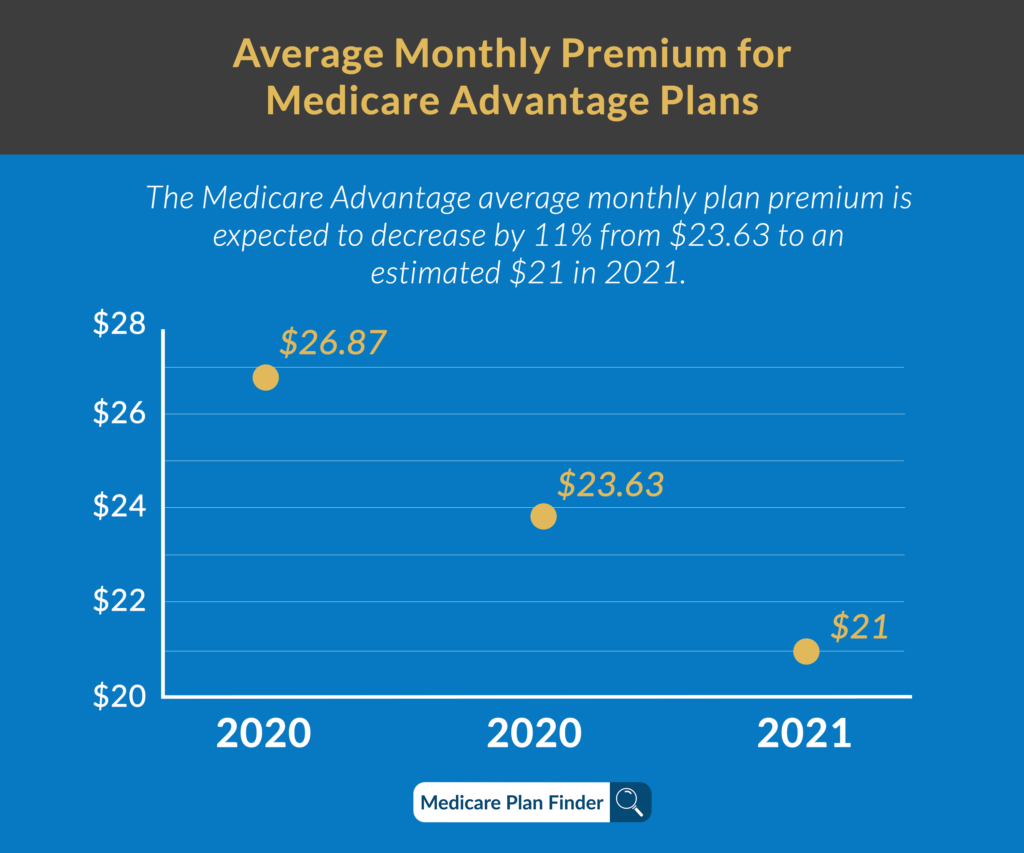

Good News: 2021 Medicare Advantage Plans Have Higher Ratings and Lower Premiums

It’s time to start making decisions for your healthcare coverage in 2021. The Annual Enrollment Period for Medicare beneficiaries is going on NOW and only lasts through December 7.

As you’re looking through your Medicare Advantage and Part D plan options for next year, you may notice that monthly premiums are shrinking and benefits are expanding!

CMS (The Centers for Medicare & Medicaid Services) released a statement earlier this fall that said the average monthly premium for a Medicare Advantage plan in 2021 will be the lowest it’s been in 14 years (since 2007!)

In fact, the average Medicare Advantage (MA) premium will see a decrease of 34.2% from 2017, while plan choice and benefits continue to expand. In some states like Alabama, Nevada, and Kentucky, the average premium decrease since 2017 will be closer to 50%.

Medicare Part D prescription drug plans (PDPs) will also have low premiums in 2021, with standard plans averaging around $30.50 a month. This marks a 12% decrease in PDP premiums since 2017.

Average monthly Medicare Advantage premiums

Average star ratings increasing

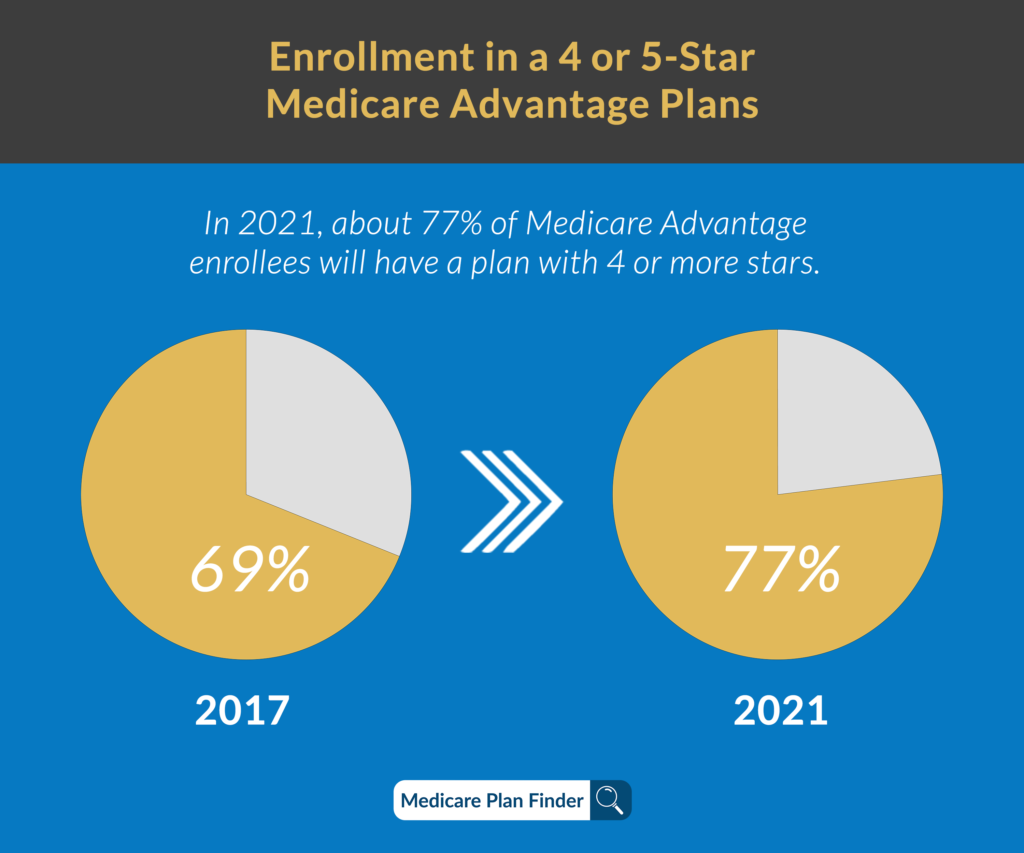

The average star ratings for Medicare Advantage and prescription drug plans in 2021 are set to increase significantly. About 77% of Medicare Advantage enrollees will have a plan with 4 or more stars, and 98% of those in a standalone PDP plan will have a rating of more than 3.5 stars.

There will also be more plans with a 5-star rating than were available in 2020, including UnitedHealthcare, Cigna, and Anthem BCBS. Even the lowest-rated plans have improved to at least 2.5 stars.

CMS uses this Medicare star rating system for Medicare Advantage and Part D plans to determine whether or not a plan is doing its job, and whether or not it can stay on the market. Plans that consistently receive poor ratings (one or two stars) will eventually be removed from the market.

Plans are given a star rating between one and five, with one being “poor” and five being “excellent.”

Medicare Advantage plans are rated on the following factors:

Level of access to preventive services (including annual physical exams and screenings)

Care coordination

How often members receive treatment for long-term conditions

Current member satisfaction

Plan performance in comparison to the previous year

Customer service quality

Part D plans are rated on the following:

Number of member issues with the plan

How many people left over one year

Patient safety while using prescriptions in the plan

Accuracy of pricing

Quality of care

Customer service quality

More and more Medicare Advantage and Part D plan carriers are entering the market every year, meaning there is more competition. More competition means that more plans are trying to be the most valuable to be able to compete. That’s why even though costs may be going down, plan ratings are still increasing.

If you plan on meeting with a licensed agent during this year’s Annual Enrollment Period, be sure to ask about four and five-star plans in your area!

3300Medicare Advantage star ratings increasing

Remind me: What is Medicare Advantage?

You can enroll in Medicare Advantage as an addition to your Original Medicare coverage. Since Medicare Advantage plans are owned and operated by private insurance companies and are not the same as the government Medicare program, the coverage is a bit different.

Medicare Advantage plans are able to cover things that Original Medicare is not, such as fitness programs, dental, vision, and prescription drugs.

Medicare Advantage plans might come with copayments, coinsurance, and deductibles, but the average premium for 2021 is expected to be $21/month.

If you can afford to add a Medicare Advantage premium, the benefits may save you from thousands of dollars in healthcare costs later on.

Expanded benefits for 2021

Earlier this year, CMS released the 2021 benefit and cost sharing information on Medicare.gov. In large part due to the coronavirus pandemic, they are offering expanded benefits in several key areas, and many health care providers are taking advantage of this flexibility.

There will be over 4,800 Medicare Advantage plans in 2021 for enrollees to choose from, a 76.6% increase since 2017. The number of MA plans per country is also growing in the new calendar year.

In response to the COVID-19 pandemic, 94% of all MA plans will provide added telehealth benefits. The current health crisis also drove CMS to develop the Part D Savings Model, which sets a $35 monthly copay rate for insulin. Over 1,750 MA and PDP plans are participating in this new model in 2021.Many health plans are also expanding their benefits for enrollees with chronic conditions. About 500 Medicare Advantage plans will feature either supplemental benefits or lower copays to those with specific chronic diseases or other conditions.

$0 Premiums and Special Needs Plans

Some people may even be eligible for a $0 premium Medicare Advantage plan. Others still may be eligible for low-cost Medicare Advantage Special Needs Plans.

CSNPs are Chronic Special Needs Plans and are for people who have certain chronic conditions and need additional coverage. ISNPs are Institutional Special Needs Plans and are for people who have been living in an institution such as an inpatient medical facility for 90 days or more. DSNPs are Dual Eligible Special Needs Plans and are for people who are dual-eligible for both Medicare and Medicaid.

How to Get a Low-Cost, Five-Star Medicare Advantage Plan in 2020

Our licensed agents across the nation are contracted and certified to sell a number of Medicare Advantage plans. An agent can sit down with you and show you all of the top-rated plans available in your area and help you select which one is best for you.

To get in touch with a licensed agent, call 844-431-1832 or click here.

A Guide to Medicare Coverage for Dementia

A Guide to Medicare Coverage for Dementia

Dementia is a decline in mental capacity that becomes severe enough to hinder a person’s ability to function. According to the Alzheimer’s Association, one-third of Americans die with some form of dementia.

Medicare Parts A and B (Original Medicare) will cover everything that’s medically necessary for dementia patients, but many other services won’t be covered.

Original Medicare dementia care may be limited, but certain Medicare Advantage plans offer coverage for more services that can include unexpected offerings like meal delivery.

Medicare Coverage for Dementia Patients Clarified

Doctor Explaining Medical Treatment for Dementia | Medicare Plan Finder

An Original Medicare plan will cover services that your doctor deems medically necessary. Medicare Part A covers inpatient hospital care, and Medicare Part B covers outpatient care and medical expenses such as doctors’ appointment costs.

Original Medicare will pay for the first 100 days of care in a skilled nursing facility (there may be some associated fees), and some Medicare Advantage (Part C) plans may include long-term care coverage as well as skilled nursing care.

Private insurance companies offer Medicare Advantage plans, so they have the freedom to cover benefits Original Medicare doesn’t. Medicare Part D or certain Medicare Part C plans cover prescription drugs such as cholinesterase inhibitors that can temporarily improve symptoms of dementia.

Medicare Advantage | Medicare Plan Finder

Medicare Supplements

Medicare Supplements (Medigap) plans can help cover the expenses that Original Medicare does not. Unlike Medicare Advantage plans, Medigap plans do not cover medical expenses, but they cover financial items such as Part A and B coinsurance and copayments. Even though Medigap and Medicare Advantage are two different types of plans, you cannot enroll in both at the same time.

Find Medicare Supplements | Medicare Plan Finder

Does Medicare Pay for Dementia Testing?

Medicare Part B covers cognitive testing for dementia during annual wellness visits. A doctor may decide to perform the test for patients who are experiencing memory loss.

The test consists of about 30 questions like, “What year is this?” to assess the patient’s memory and awareness. The test can be used as a baseline evaluation for future wellness visits and can be a valuable tool for catching dementia early.

Medicare Testing for Alzheimer’s

Dementia is a symptom that can result from many different diseases. Alzheimer’s disease is just one cause of dementia. The risk of developing Alzheimer’s increases with age and with a family history of Alzheimer’s.

There is a correlation between genes called apolipoprotein E (APOE) and Alzheimer’s, but those genes do not necessarily cause the disease. Medicare will not cover genetic testing for APOE genes.

Dementia as a SEP-Qualifying Condition

Medicare eligibles with dementia also qualify for specific Medicare Advantage plans called Chronic Special Needs Plans (CSNPs). These health insurance plans involve coordination and communication between the patient’s entire medical team to help ensure the patient gets the best possible care.

The best way to sort through the thousands of plans available and find the right CSNP for you is enlisting the help of a qualified professional by contacting us here.

If you’re diagnosed with dementia and already enrolled in Medicare Parts A and B, you will qualify for the Special Enrollment Period (SEP). The SEP allows you to enroll in new Medicare coverage or make changes to your existing CSNP whenever you need to instead of having to wait for certain times of the year.

Special Needs Plans | Medicare Plan Finder

Eligibility for Medicare Coverage for Dementia

If you meet the eligibility requirements for Medicare Parts A & B, you will also be eligible for the dementia coverage provided by Medicare. You can obtain Medicare coverage for dementia services if you are:

Age 65 or older

Any age and have a disability, or end-stage renal disease (ESRD)

Dementia patients are also eligible for other specific Medicare plans once they are officially diagnosed with the condition, like special needs plans (SNPs) and chronic care management services (CCMR.)

Medicare can also cover home health care that dementia patients often need. In order to receive this coverage, it must be certified as necessary by a doctor. The patient must also be classified as homebound, meaning they have trouble leaving the house without help.

Does Medicare Cover Memory Care?

Memory care is a specific type of long-term care for Alzheimer’s patients or people with dementia. Original Medicare will cover occupational therapy but does not cover assisted living facilities. However, certain Medicare Part C plans may include coverage for Medicare dementia care services such as adult day care or help to get dressed or to bathe.

Medicare dementia coverage is split between its component parts. Part A helps cover the cost of inpatient hospital stays, including the meals, nursing care, and medication that you need while you’re there. Meanwhile, Part B will cover the doctor’s services that you might receive during your stay in the hospital, such as testing or medical equipment.

Even more services can be covered by Part C, also called Medicare Advantage. In addition to everything covered by Parts A & B, these plans can also offer options for long-term and home care for dementia patients.

How Much Does Medicare pay for dementia care?

Each different part of Medicare will pay for its benefits in different ways. For example, Part A will cover the entire cost of your hospital or skilled nursing facility stay for the first 60 days. After this period, you will need to pay 20% coinsurance until day 90, when Part A will stop paying entirely.

Part B, on the other hand, will usually pay for 80% of all services that it covers. Medicare Supplement plans are often purchased to cover the remaining costs, and can also provide additional benefits to the patient.

Does Medicare cover long term care for dementia?

The long-term care insurance offered by Medicare depends on the nature of the service being provided to the patient. In many cases, the long-term care needed by dementia patients is classified as custodial care and won’t be covered by Medicare.

However, if your doctor prescribes a long-term care service as “medically necessary,” Medicare may help cover the costs. These exceptions can include services like hospice care, and part-time nursing care or occupational therapy provided in the home.

Does Medicare Pay for Home Health Care for Dementia Patients?

It is usually difficult to obtain coverage from Medicare for elderly care at home. However, it can completely cover some home health services that are deemed medically necessary by your doctor, including:

Physical and occupational therapies

Part-time skilled nursing care

Medicare social services

Most nursing home care is also classified as custodial care by Medicare, meaning it will not be covered. Medicare will cover custodial home health care for dementia patients only if it’s a part of hospice care.

Medicare Advantage plans, however, can offer many different home health benefits for those who suffer with dementia. Examples include personal care assistance, homemaker services, and meal delivery.

Does Medicare Cover Assisted Living for Dementia?

Original Medicare will not cover any services that are deemed custodial or personal care, including any that aid in typical activities of daily living, such as:

Eating

Getting Dressed

Bathing

Using the restroom

This rule also applies to assisted living and memory care facilities which provide these services. But depending on your state and the facility of choice, Medicaid may be able to help cover the cost of long-term custodial care provided in assisted living facilities.

Medicare Dementia Hospice Criteria

In order for Medicare to cover hospice care, your doctor must first document that you have less than six months to live. You or your durable power of attorney must sign documents indicating that you agree to accept care for comfort and that you waive other Medicare benefits.

What dementia services does Medicare not cover?

In almost all cases, Medicare will not cover any non-medical care services, such as:

Assisted-living or long-term care

Custodial services provided in a facility or in the home

Homemaker services

Meal delivery

There are exceptions to these rules, but the service in question must be recommended as medically necessary by your doctor. Medicare Advantage plans may offer coverage for these and other personal care services not covered by Medicare.

How to Cover the Gaps with Medicare and Dementia

Paying for dementia care can be daunting, even for Medicare beneficiaries. Both Parts A & B have deductibles you have to meet, and Part B only pays for 80% of its covered services. At the end of the day, a patient and their family may be left wondering how to pay for Alzheimer’s care.

The answer may come in the form of Medicare Part C, also called Advantage plans, which can pay for many of the custodial care costs not covered by Original Medicare. Another option may be a Medicare SNP, or special needs plan, which are geared toward patients with certain chronic conditions such as dementia.

Early Signs and Symptoms of Dementia

Dementia can have a variety of symptoms depending on the cause, as well as if the patient is in the early stages or late stages of the disease. However, some common signs symptoms include:

Cognitive changes

Loss of memory

Difficulty finding the right words during conversation

Getting lost while driving to and from familiar places

Difficulty with logical reasoning or solving problems

Difficulty with completing complex tasks

Difficulty with planning and organizing day-to-day activities

Difficulty with muscular coordination and motor functions

Being confused or disoriented

Psychological changes

Changes in personality

Depression

Anxiety

Inappropriate or irrational behavior

Paranoia

Agitation

Hallucinations

How to Find Memory Care

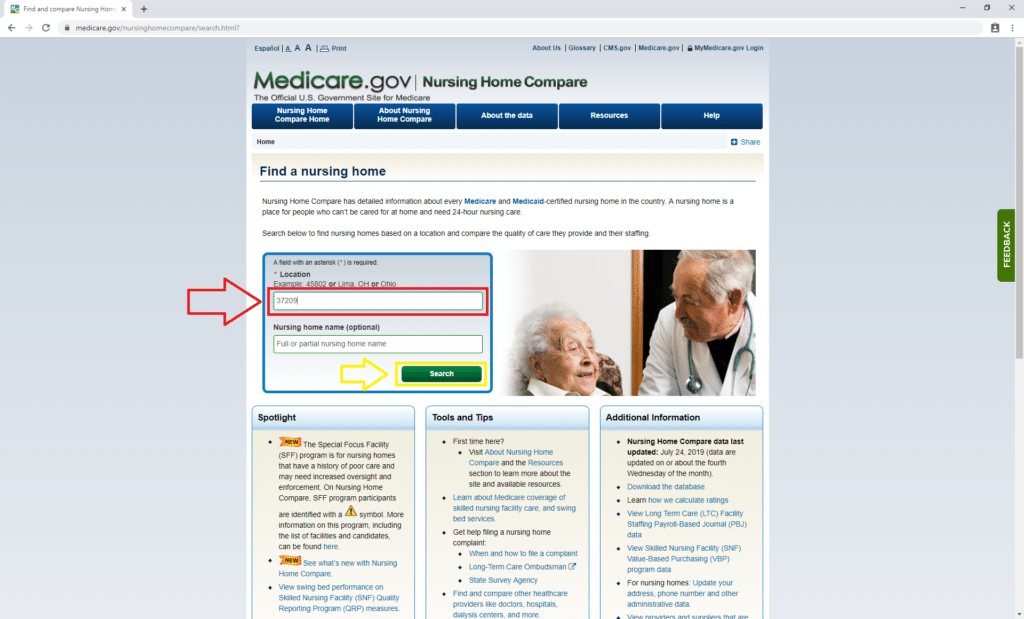

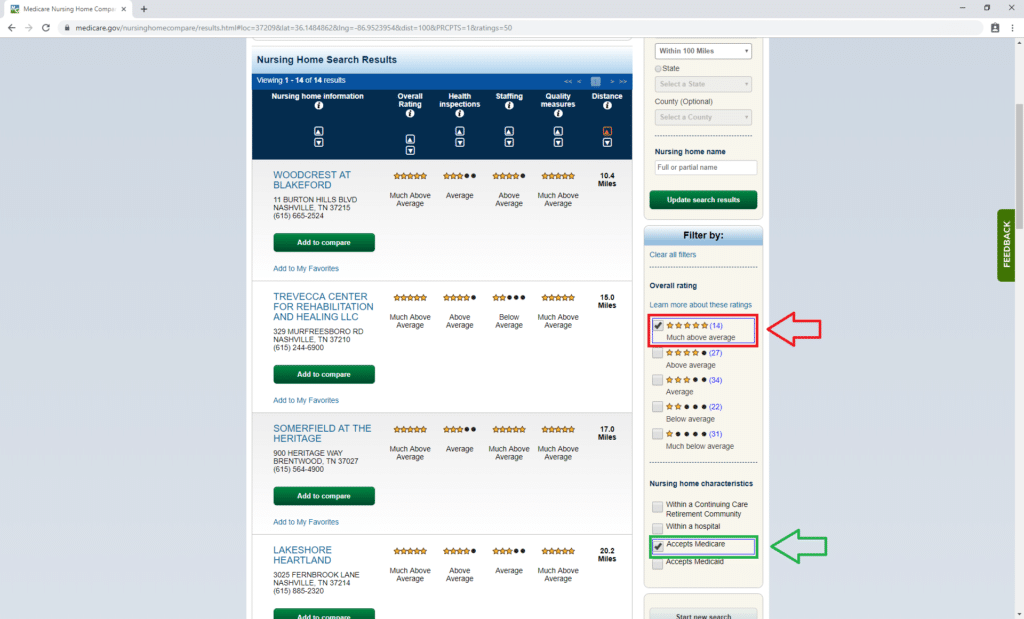

Medicare.gov has a tool to find nursing homes that accept Medicare for medical services. To get started, click here. Not all of these facilities have dedicated memory care teams, so you’ll need to contact them to verify their services.

Once you’re on the nursing home finder tool page, enter your zip code as shown below in red. We used 37209, which is our corporate headquarters’ zip code in Nashville, Tennessee. Then click “Search,” shown in yellow.

How to Find Memory Care Step 1 | Medicare Plan Finder

Then you’ll reach a list of nursing homes in your area. The nursing home finder tool lets you sort facilities by star rating, which is based on a scale of one to five.

Basically, the higher the rating, the better the care the facility provides. For demonstration purposes, we only chose to see homes that have a five-star rating (shown below in red) and that take Medicare insurance (in green.)

How to Find Memory Care Step 2 | Medicare Plan Finder

You may have to contact more than one facility to find the right one for you. Ask about costs and how they help patients with dementia. If one seems like it may be a good fit, ask to tour the home to really get a feel for it.

Resources for Families

Family members of dementia patients have access to a wide variety of resources to help them cope. The first step for helping your loved ones is to educate yourself about the disease and to learn how you can be the most supportive.

You should also look into support groups for your family so they can find like-minded people who are having similar experiences. Dementia should not be dealt with alone.

If you are a caregiver for a parent with dementia, you should consider important things such as who will have the power of attorney and make financial decisions for the patient at the end of his or her life. If you haven’t enrolled in a life or a final expense insurance policy, you should consider doing so now.

We Can Help You Find Medicare Coverage for Dementia

Dementia is difficult for everyone involved. If you or a loved one has dementia, we can help you navigate Medicare dementia care and find a Chronic Special Needs Plan that’s right for you. Set up a no-obligation appointment with a licensed agent by calling 844-431-1832 or contacting us here today.

Contact Us | Medicare Plan Finder

2020 Medicare Changes & Trump’s Executive Order

Every year, CMS (Centers for Medicare and Medicaid Services) reserves the right to make changes to the Medicare program. Rules and regulations around enrollment periods, penalty fees, marketing, and plan benefits are released in late summer and early fall for the following year. Costs can rise, and brand new plans can enter or leave the market.

Medicare is confusing as it is. When you add these yearly changes into the mix, choosing the right plan can be stressful. Our goal is to make all of this less stressful for you. Our website is a great educational tool, and our licensed agents can provide free assistance!

Here are the changes you need to know about for Medicare in 2020.

On October 3, 2019, President Donald Trump signed an executive order “protecting” the Medicare program. What does this mean?

Alex Azar, Health and Human Services (HHS) Secretary, said that Trump told HHS to take “specific, significant steps” towards improving Medicare funding and improving healthcare for American seniors. These steps include lowering Medicare Advantage costs, allowing savings accounts, and improving access to new medical technology. It also leaves room for more plan options, more telehealth, more wellness benefits, and a stronger financial model.

In his post-executive order speech given in Florida yesterday morning, Trump stated, “In my campaign for president, I made you a sacred pledge that I would strengthen, protect and defend Medicare for all of our senior citizens.” That was the intent of the executive order.

Is Medicare Going Up in 2020?

New 2020 Medicare premiums and costs for 2020 have not been released yet. The new numbers are usually released in early fall of the year prior, so we are expecting to see them over the coming months. The Wall Street Journal reported in April that 2020 Medicare Part B premiums are likely to increase by $8.80/month to a total of $144.30, but this is not final.

We will continue to update this post with new 2020 costs as they are released. Thank you for your patience!

2020 Medigap Changes

Just like the Original Medicare program, private plans like Medicare Advantage, Medicare Supplements, and standalone benefit plans can change every year.

Plan availability may not be the same for everyone. Medigap eligibility, in particular, can depend on your age when you enroll, preexisting conditions, and where you live. Plans can be different not only in every state but also in every county and zip code.

Use our plan finder tool to find out what Medigap plans are available in your area for 2020.

Is Medicare Supplement Plan F Going Away in 2020?

Starting in 2020, you will no longer be able to purchase Medigap Plan F or Medigap Plan C. Plan F was one of the most popular plans, and Plan C was fairly similar. The plans are going away because they include coverage for the Part B deductible (only $185 in 2019).

You might here plans C and F referred to as “first-dollar” plans because they virtually eliminate out-of-pocket costs. CMS decided that taking away the Part B deductible coverage was a smart move to discourage people from overusing their primary physician offices and costing the Medicare program a lot of money for unnecessary doctor’s visits.

If you already have Medigap Plan F or Medigap Plan C, you can be grandfathered in. That means that you will not lose your coverage in 2020. However, if you leave your Plan F or Plan C in favor of a different Medigap plan, you won’t be able to re-enroll in F or C.

Will Plan F Premiums Rise After 2020?

As Plan F sees less and less enrollees, Plan F premiums will likely begin to rise. We can’t say this for sure and we will certainly have to wait and see what happens, but generally less enrollees means higher costs for the companies, resulting in higher premiums.

Will There be a High Deductible Plan G in 2020?

Since people will not be able to purchase Plan F or Plan C in 2020, CMS did want there to be another option with similar benefits. Plan G was already that option, given that the only difference is that Plan G does not cover the Part B deductible.

The other difference is that previously, Plan G was not offered with a high-deductible. If you typically have low medical costs, you may prefer a high-deductible option. Having a high deductible often means that your premiums will be lower. This way, you don’t have to pay as much until you start experiencing health concerns. The high deductible Plan G option can replace the high deductible F option.

Donut Hole Closing in 2020

In addition to all of these plan changes, the infamous “Donut Hole” will be effectively closing in 2020. The Bipartisan Budget Act of 2019 closed the coverage gap for brand-name drugs in 2019, and the generic drug coverage gap will be eliminated in 2020. This basically means that, if you have a Medicare Part D plan, you will only be responsible for 25% of your covered prescription drug costs instead of 44%.

2020 Medicare Advantage Changes

There may be more Medicare Advantage plan changes to come in 2020, but we wanted to make sure you had heard about the changes from last year.

On October 12, 2018, the Centers for Medicare and Medicaid (CMS) announced the 2019 Original Medicare premium and deductible increase, but what about Medicare Advantage (MA) plans? Unlike Medicare Part A and B, beneficiaries enrolled in MA plans may see a decrease in their premiums in 2019 and 2020 compared to 2018.

2020Medicare Advantage Cost Changes and 2020 Premiums

In September of 2018, CMS announced that on average, Medicare Advantage premiums will decrease by 6%. This is great for beneficiaries interested in affordable vision, dental, and hearing coverage or even fitness classes like SilverSneakers®!

CMS estimated that 83% of beneficiaries would have equal or lower premiums for 2019 and 46% will have a $0 premium! Premiums for MA plans have steadily declined, and this is the lowest premium we’ve seen in three years. This is a perfect example of a private and public collaboration that allows beneficiaries to drive and define the value. The 2019 Medicare Advantage changes are a quick glance of what you can expect to continue in the future.

2020 cost changes for Part A and B premiums and deductibles have not officially been released yet but are not expected to increase by very much. We will continue to monitor this information and will update as soon as the cost changes are officially announced.

Early in 2018, CMS (Centers for Medicare and Medicaid Services) released new rules that allow Medicare Advantage plans to offer a few benefits, like “daily maintenance,” transportation, telehealth, and durable medical equipment.

Some plans in 2020* are really going above and beyond, offering benefits like new air conditioners and pest control!

*These benefits are not included in all MA plans. Your agent may be able to help you find a plan that includes more.

Daily Maintenance

The addition of the “daily maintenance” benefit means that Medicare Advantage plans are now able to offer at-home care items, such as wheelchair ramps and other home modifications. Tied in with that benefit are other forms of durable medical equipment, like hospital beds, oxygen equipment, blood sugar monitors, etc, as well as “non-skilled” services. Non-skilled refers to items that do not require a licensed doctor or nurse, such as aides who can assist with bathing and dressing or homemakers who can help with cleaning and cooking.

Non-Emergency Medical Transportation Coverage

CMS has also added the ability for MA plans to provide non-emergency transportation coverage, a service that several Medicaid plans provide. This benefit (if your plan covers it) will allow you to receive free or low-cost rides to medical appointments and pharmacies. In most cases, you can only qualify for this benefit if you do not have another adequate means of transportation. The appointment that you are requesting a ride to must be for a Medicare-covered service.

Telemedicine and Telehealth

MA plans can now provide coverage for telehealth. That means you can have live video interaction with your doctor through digital clinics like HealthTap, Teladoc, and MDLive. Telehealth can also include health alerts delivered to your phone, health education apps, electronic medical data transfers, mail-order prescriptions, digital appointment scheduling and exam reminders, and more.

New Enrollment Period (OEP)

Before 2019, most people were only able to switch into new Medicare Advantage plans during the Annual Enrollment Period in the fall. Now, if you already have a Medicare Advantage plan, you may be eligible to make a change during OEP. OEP, or the Open Enrollment Period, takes place from January 1 through March 31. During this time, you can switch from one Medicare Advantage plan to another or drop your Medicare Advantage plan in favor of Original Medicare (Part A and Part B only).

Future of Medicare Advantage Plans

According to the Henry J Kaiser Family Foundation, enrollment has tripled to 19 million beneficiaries since 2003 and continues to grow each year. CMS estimates that MA enrollment will hit an all-time high of 22.6 million beneficiaries in 2019 (an 11.5% increase)!

As enrollment continues to increase, plan selection and variety increase too, with approximately 600 new plans offered in 2019! 99% of seniors and Medicare-eligibles have access to a MA plan – and 91% can choose from 10 or more plan options. Beneficiaries will not only see more plans to choose from, but also new supplemental Medicare benefits!

Enroll in a Medicare Advantage Plan in 2020

Are you interested in getting coverage beyond Original Medicare? Along with the new benefits, many Medicare Advantage plans offer dental, hearing, and vision coverage.

Our agents at Medicare Plan Finder can contract with nearly every carrier in your state! This means that you can enroll in the MA plan that best fits your needs and budget.

The Annual Enrollment Period runs from October 15 through December 7. Start looking over your plan benefits now so that you’re ready to enroll before December 7!

Ready to learn more? Call us at 844-431-1832 or fill out this form to arrange a no-cost, no-obligation appointment with an agent in your area.

*This post was originally posted on November 8, 2018, and was last updated on October 4, 2019.

Medicare Meal Delivery Services & Meals on Wheels

According to a report from the non-profit organization Feeding America, 5.5 million adults 60 and older are “food insecure,” meaning they lack access to enough quality foods. Many seniors and Medicare eligibles may be homebound due to medical conditions or income level, and they simply can’t get out to buy the food they need.

Meals on Wheels or Medicare meal delivery services may be able to help if you meet certain conditions.

What Is Meals on Wheels?

Medicare Food Delivery | Medicare Plan Finder

Meals on Wheels is best known as a food delivery service for homebound people who don’t otherwise have access to healthy food. Meals on Wheels has more than five thousand programs that operate across the entire United States. Those programs feed more than 2.4 million people every year.

Meals on Wheels programs may operate on a sliding payment scale, meaning that you won’t necessarily be turned away if you can’t afford the meals. Some local programs accept SNAP (food stamps). Every local Meals on Wheels program has a different set of payment guidelines, so it’s best to reach out your local program if you have questions.

Typically, program members receive one meal per business day. You may not be able to receive meals on weekends, holidays, or during inclement weather.

Meals on Wheels may provide additional benefits along with food delivery. The volunteers who deliver the meals can talk to the program members, which can provide an additional social benefit.

Meals on Wheels Food Delivery Finder

Meals on Wheels’ network of independently-operated programs provides 218 million meals all over the US. While each local program may provide different services based on your community’s needs, every program is dedicated to encouraging healthier lifestyles.

If you have questions about the services your local Meals on Wheels program provides, check out the Meals on Wheels America directory. Once you’re on the page, enter your zip code and hit “enter.”

Medicare Food Delivery | Medicare Plan Finder

That leads you to a page that lists contact information for the programs in your area.

Who Qualifies for Meals on Wheels?

Each local program may have different eligibility requirements, however, most homebound people who are 60 and older will qualify. People younger than 60 may also qualify if they are homebound, disabled, and they meet certain income requirements.

Most Meals on Wheels programs use CMS guidelines for determining whether you’re homebound. The Centers for Medicare and Medicaid (CMS) defines homebound as, “confined to the home due to illness or injury.”

You don’t necessarily have to be incapable of leaving; if it is difficult for you to leave, that counts. For example, if you can’t leave the house without a walker, and it’s extremely physically taxing when you leave, CMS may consider you to be homebound.

Is Meals on Wheels Covered by Medicare?

Original Medicare (Part A and Part B) does not cover Meals on Wheels or any other home meal delivery service. However, certain private insurance plans called Medicare Advantage plans can offer meal delivery services if you meet certain qualifications.

Along with meal delivery, Medicare Advantage plans can cover benefits including non-emergency transportation to medical appointments, vision, dental, and hearing services.

How Do I Get Meals on Wheels With My Medicare Advantage Plan?

Most Medicare Advantage plans that offer Medicare meal delivery usually offer the service for a limited time. For example, if you’re discharged from a hospital or a skilled nursing facility, you may receive 10 pre-packaged frozen meals. Your plan may have limits on how many times per year you can receive the post-discharge Medicare food delivery service.

Another way Medicare Advantage plans can offer meal delivery services is if you have a chronic condition. Your plan may offer a set number of pre-packaged meals annually if you have special dietary needs.

Some plans will offer the meal delivery benefit more than once per year to people who have multiple conditions. Some Medicare Advantage plans may allow doctors to order more meals depending on your needs, too.

The licensed agents with Medicare Plan Finder can help you find a Medicare Advantage plan in your area that offers meal delivery services. We are dedicated to helping you find the best plan for your lifestyle and budget.

Medicare Advantage | Medicare Plan Finder

Does Medicaid Cover Meals on Wheels?

If you are homebound and eligible for Medicaid, your state may provide a waiver that pays for home-delivered meals. Medicaid will only cover Medicaid-approved meal delivery services such as Mom’s Meals and Homestyle Direct.

For example, some states require nutrition counseling for Medicaid beneficiaries. Other states do not. If you have questions about your state’s requirements for Medicaid meal delivery services, click here to contact your state’s Medicaid office.

Each state has different policies regarding how you pay for home meal delivery. Some states pay as little as $3.00 per meal, and some pay as much as $8.00 per meal.

How Do I Get Meals on Wheels for My Mother/Relative?

Every local program has different rules about how to apply for Meals on Wheels, and who can apply. Contact your local program’s office to learn about specific requirements.

Some Meals on Wheels programs can cost about $7 per meal, but they accept contributions based on what the recipient can afford.

Even though your loved one’s local Meals on Wheels program may operate on a sliding payment scale or accept SNAP, a Medicare Advantage plan with meal delivery may be the best option for your relative to get vital nutrients after a hospital stay. You can only make Medicare decision’s on your relative’s behalf if you have durable power of attorney (POA).

Agents cannot legally discuss your loved one’s protected health information (PHI) without durable POA. Talk to your agent about your loved one’s needs. Your agent can help you determine if a Medicare Advantage plan with meal delivery is right for your relative.

What Is a Typical Meals on Wheels Menu?

Medicare Meal Delivery | Medicare Plan Finder

Many Meals on Wheels programs provide one meal per day that meets ⅓ of the Food and Drug Administration’s (FDA) recommended daily nutritional value. Meals may contain a protein, a starch, a vegetable, and a dessert.

Many local programs vary the menu every month so you aren’t getting the same thing every day. For example, one day’s meal might be:

Protein: Barbecue pork

Starch: Red potatoes

Vegetable: Spinach salad with French dressing

Dessert: Banana bread

Can I Choose What I Get?

Some local Meals on Wheels programs give their recipients options for meals, such as a diabetes-friendly dessert or a vegetarian option. However, because each program is different, the Meals on Wheels program near you may not let you choose what you get.

How We Can Help With Medicare Meal Delivery

The right Medicare Advantage plan can help provide you with the nutrition you need after a hospital stay or if you have a chronic illness. Our licensed agents can help you find the best health insurance plan that fits your needs. Call 844-431-1832 or contact us here to learn more today.

Contact Us | Medicare Plan Finder

This post was originally published on July 25, 2019, and updated on September 30, 2019.

How to Find the Right Geriatric Doctor

Finding an internal medicine doctor you really connect with can be difficult, and finding the right geriatric doctor, or geriatrician, can be even more difficult. You must have confidence in your provider’s ability to treat your conditions or to refer you to other providers with extensive experience working with older adults.. Your health is the most important thing you have, and you need a doctor you’re comfortable with.

What to Look for in Geriatric Doctors

All geriatric doctors specialize in the diagnosis, treatment, and prevention of disease and other medical or chronic conditions common to seniors. You want healthcare providers who know how to treat your population and provide quality care plans. However, a doctor’s area of focus is just one thing you should look for. You also want to find a doctor that you can feel comfortable with.

It’s important that you feel comfortable asking questions about personal health concerns and that you can trust that your doctor is listening. You should feel like your health is as important to your doctor as it is to you.

The right geriatrician will take pride in providing the best quality of care possible. You should feel like your doctor thinks of you as a whole person, not just a list of conditions and symptoms.

Your geriatrician should be capable of finding solutions to your health problems. For example, let’s say you get sick one day, so you go to the doctor. Your doctor diagnoses your health condition and prescribes a medication he or she thinks is best. You should have follow-up appointments to assess how the medication works, and your doctor should be committed to finding a prescription that works if the first one doesn’t.

A good place to start is to find out what other patients say about doctors in your area. Talk to friends, family, and caregiver if you have one to see if they like their geriatricians. Ask for recommendations from healthcare professionals you know and trust.

Look at doctor reviews on websites such as Healthgrades.com and read Google reviews. When you look for reviews on Google, also search for the doctor’s name and see if he or she is in the news. If his or her name pops up with a long history of legal trouble, you should move on.

How a Medicare Advantage Plan can Help

Look for a doctor who takes your insurance. If you have Medicare, you have a great resource to receive quality healthcare. However, Original Medicare doesn’t always approve every charge, and Medicare Parts A and B can be limited in what they cover.

That’s where Medicare Advantage (MA) plans come in. MA plans come from private insurance carriers and they can cover a lot of services Original Medicare does not. Medicare Advantage plans can cover a range of services including meal delivery, hearing, vision, and even fitness classes. Some plans even include prescription drug coverage!

There may be many MA plans to choose from in your area, and a great way to find out what’s available is to talk to a qualified professional who can help you find the right plan. You won’t lose your Original Medicare coverage if you enroll in a MA plan, and the “extras” your doctor recommends, like physical activity or home health devices, may be covered.

What if I’ve Already Found a Geriatric Medicine Doctor I Like?

Maybe you’ve found a doctor you like, and he or she decides to stop taking your insurance plan. If you have a Medicare Advantage plan, you may have to wait until the Annual Enrollment Period (AEP) to make changes to your plan unless you qualify for a Special Enrollment Period (SEP). If you want to stick with your doctor and are willing to wait until the AEP, which is every year from October 15 to December 7, find out what MA insurance plans your doctor accepts.

Usually, your doctor will give you a list of carriers he or she accepts, and Medicare Plan Finder benefits advisors have access to many different plans and carriers. Your benefits advisor will work with you to find a plan that will allow you to keep your geriatric doctor.

What is the Difference Between a Geriatric Doctor and a Regular Doctor?

Geriatricians provide primary care for seniors who have complicated medical issues. Age is not the only factor that causes people to need geriatricians. For example, an 80-year-old who is active and only takes a couple of medications doesn’t need to see a geriatrician, but a 65-year-old who has diabetes and heart disease does.

Your geriatric care will involve a team of medical professionals that will provide a comprehensive healthcare plan. You’ll work with your primary geriatric doctor, and often times a social worker, physical therapist, and/or a nutritionist depending on your needs.

If a doctor does not specify that they are a geriatric doctor, that does not necessarily mean that they do not work with older patients. However, doctors who do call themselves geriatric doctors typically have studied geriatrics and are more specialized in that area.

Geriatric Doctor

When You Should Find a New Doctor