It’s time to start thinking about what you want your Medicare coverage to look like next year. Did your current plan change? Did you develop a new health condition and need more coverage? Are you enrolling in Medicare for the first time?

No matter your situation, the Annual Enrollment Period (AEP) runs from October 15 through December 7. If you used AEP to enroll, your plan became effective on January 1, 2020.

By now, you may have realized that there are hundreds of Medicare plans out there, all offering slightly different benefits at different costs. So how do you choose?

The best Medicare plan for 2020 is the one that fulfills your needs. To figure out which Medicare plan is best for you, ask yourself the following questions:

What specific medical services do I need coverage for (ex: lab tests, blood work, surgery, chemotherapy, dental, etc.)

How much room do I have in my budget? Am I able to pay a little more to have more benefits?

Would I rather pay more on a monthly basis and pay very little when I visit the doctor, or is it better to pay a small amount every month but risk having higher copayments?

Who are the doctors and other providers who I want to be covered in my plan?

What prescriptions do I need coverage for?

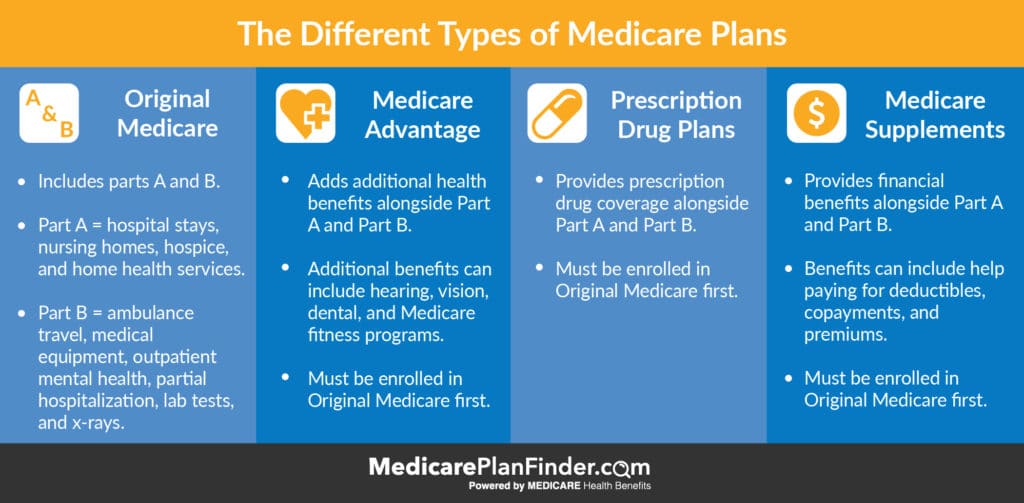

Start by Choosing a Type of Plan

There are four main types of Medicare plans to consider when you begin your Medicare plan search. Start by comparing Original Medicare, Medicare Advantage, Prescription Drug Plans, and Medicare Supplements.

Keep in mind that you cannot have Medicare Advantage and a Prescription Drug Plan at the same time. You also cannot have Medicare Advantage and a Medicare Supplement plan at the same time.

Which plan or combination of plans works best for you?

Medicare Advantage: A private plan that you can purchase once you have Original Medicare. Can add additional benefits such as hearing, vision, dental, fitness, etc. Can include a prescription benefit.

Prescription Drug Plans: Another type of private plan that you can purchase once you have Original Medicare. Usually only includes a prescription benefit.

Medicare Supplements (Medigap): Another type of private plan that you can have in addition to Original Medicare. Adds more financial coverage, like for copayments and deductibles.

You can choose from the following combinations:

Original Medicare only

Original Medicare and a Prescription Drug Plan

Medicare Advantage

Medicare Advantage with Prescription Drug Coverage

Medicare Supplement

Medicare Supplement AND standalone Prescription Drug Plan

Types of Medicare Plans

Original Medicare Only

Having Original Medicare only means you’ve enrolled in the government program, Medicare Part A and Part B, but you have not enrolled in an additional (private) plan. Parts A and B can cover some of your hospital and medical costs, but they do not cover prescription drugs and other additional benefits such as dental and vision.

Original Medicare and a Prescription Drug Plan

If you don’t think you need any other medical benefits aside from what parts A and B cover, but you do need prescription drug coverage, you can enroll in a standalone prescription drug plan in addition to your Original Medicare.

Medicare Advantage

With a Medicare Advantage (MA) plan, you’ll still have to pay your Part B premium, but you can get other benefits. MA plans can include additional health benefits such as fitness program memberships, dental care, vision, and more.

Choosing a Medicare Advantage Plan

So, did you decide to go with Medicare Advantage? Great! Now, there are a few types of Medicare Advantage plans that may be available for you. First, ask yourself whether or not you need a large network and whether the freedom to see any doctor is important to you. Then, read through these important differences:

HMO Plans (Health Maintenance Organization) – You’ll select one primary physician. In some cases, you may only receive coverage for that one doctor (unless he or she refers you to a specialist). Requirements may vary based on your plan.

HMO-POS Plans (Point-Of-Service) – You’ll select one primary physician, but you’ll have the freedom to visit any specialist in your network for your other needs. You will be charged a fee for visiting specialists.

PPO Plans (Preferred Provider Organization) – You can see any doctor, but your costs will usually be lower if you choose one that is in your network.

PFFS Plans (Private Fee-For-Service) – You will not need referrals or a primary physician, but you’ll have to pick a doctor that accepts your PFFS plan.

SNP (Special Needs Plans) – Designed for those who are eligible for both Medicare and Medicaid, live in a nursing home, or have a chronic illness or disability.

MSA (Medical Savings Account) – Works like a tax-free savings account for your medical bills. Medicare will deposit money into your HSA. You can use that account to pay for medical expenses.

Medicare Advantage with Prescription Drug Coverage

Some select Medicare Advantage plans come with a prescription drug benefit. This is important because you can’t have BOTH a Medicare Advantage plan and a standalone prescription drug plan. If you like the idea of Medicare Advantage but need prescription coverage, a “MAPD” or Medicare Advantage Prescription Drug Plan may be right for you.

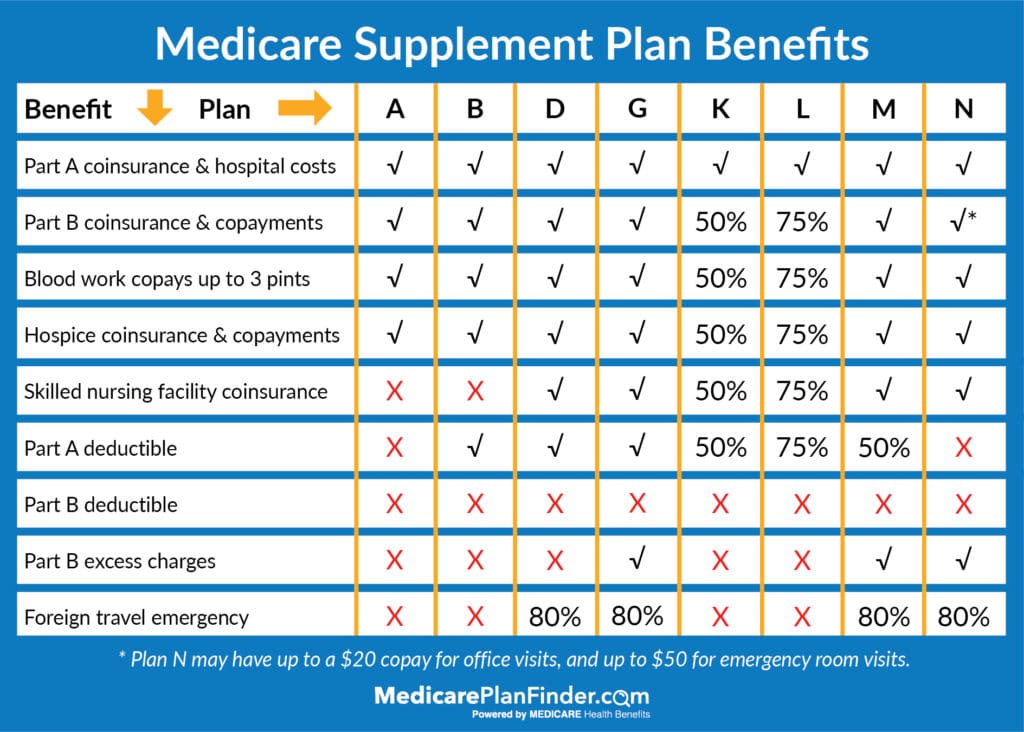

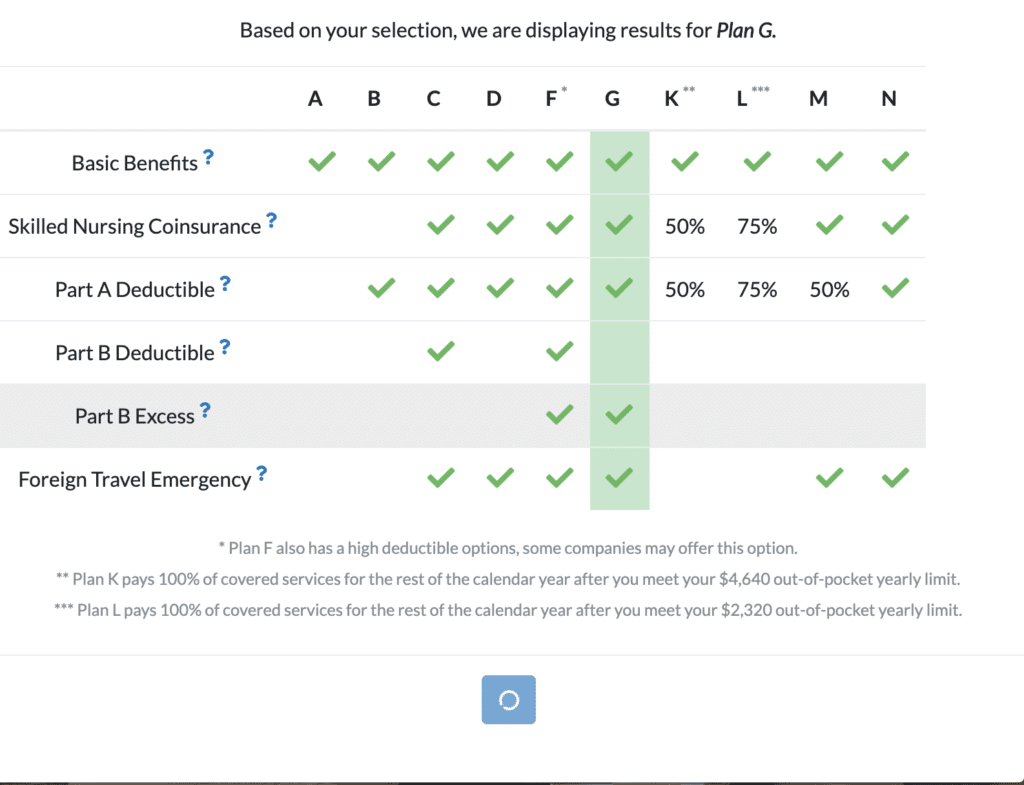

Medicare Supplement

Sometimes called “Medigap,” Medicare Supplement plans bridge the gap between your Part A and B costs and your out of pocket costs. For example, Medigap Plan A covers Part A* coinsurance and hospital costs, Part B coinsurance and copayments, up to three pints of blood, and hospice coinsurance and copayments. It does not offer additional health benefits, but it eliminates many of the costs that come with Part A and B.

The best Medicare Supplement plan is the one that fits your needs at the time. For example, you might not need skilled nursing care when you first sign up for Medicare, so Plan A might work best for you. Eventually, your health condition may require more inpatient services and skilled nursing services, so Plan D may be a better fit.

*Be careful not to confuse Part A with Plan A

2020 Medicare Supplement Comparison Chart

Medicare Supplement AND a Prescription Drug Plan

Medicare supplements do not offer any prescription coverage, but you are able to enroll in both a Medicare Supplement plan and a standalone Prescription Drug Plan at the same time.

What is the Best Medicare Plan in 2020?

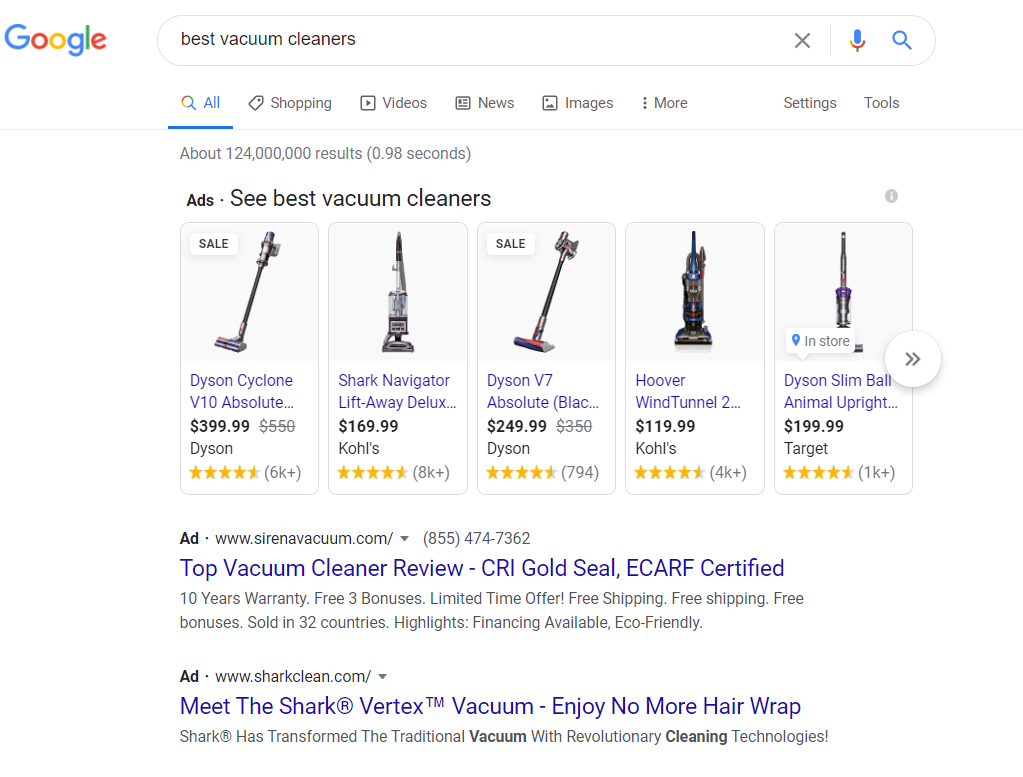

Everyone wants to know what the “best” Medicare plan is, but just like shopping for anything else, “best” can be subjective. If you were shopping for a vacuum cleaner, you’d probably search “best vacuum cleaners,” too, but what would you find?

We did that part for you, and we got about 228,000,000 results. You’re never going to sort through all those options, right?

Google search results for “Best Vacuum Cleaners”

When you really want to narrow down the best vacuum for your needs, you’re probably going to filter your search by price, capabilities, maybe even the size of the vacuum…any number of things that are going to narrow down your choices to what you really want to purchase.

While there probably aren’t 124,000,000 Medicare plans available to you, there are far too many for this to be a quick Google search! Like choosing the “best” vacuum, choosing the “best” Medicare plan for you requires some research.

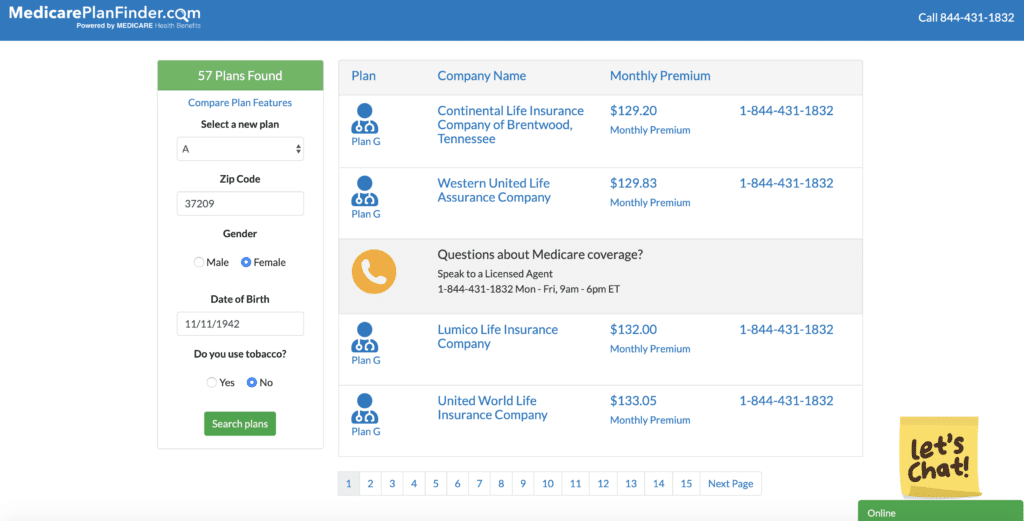

Medicare Plan Finder Tool

Our Medicare Plan Finder tool compares plans from carriers in your area. You’ll have to tell us your birthdate and a few other things so that we can determine what you’re eligible for.

Once you’ve entered your information, you’ll see a graph showing you the names of the plans and the potential premiums you might owe for those plans. This is a great place to start your research.

We ran a sample search for a 76-year-old non-smoking woman in Nashville who wanted a low premium to show you what the results look like. Your online Medicare Plan Finder results may not look the same.

2020 Medicare Plan Finder Tool Search ResultsMedicare Plan Finder Tool (These search results may not be an accurate representation of your search results)

New Medicare.gov Tool

You may have heard the buzz about Medicare.gov’s new plan finder tool. They’re offering a “new and improved” experience after getting complaints about their old tool.

To use Medicare.gov’s tool, you’ll need to enter your Medicare number and some other information. Then, you’ll see a graph of the plans available in your area.

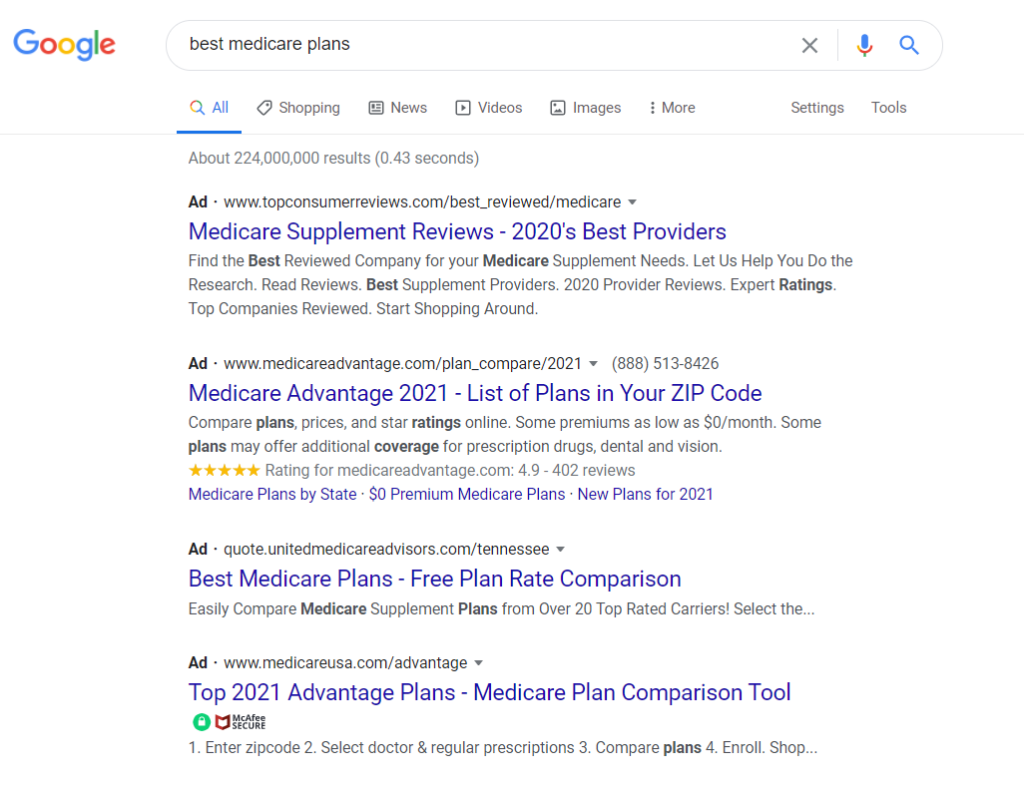

Scour the Internet

We don’t recommend this option, but you could start your Medicare plan shopping experience with a quick Google search. However, watch what happened when we Googled “best medicare plan.” The first four search results are ads.

Best Medicare Plans

The other thing you can try is going directly to the carrier websites, if you already know the name of a company you’d like to purchase from. However, keep in mind that those websites are only going to show you a select group of plans that they alone offer. You could be missing out on better plans from different carriers.

Meet With a Licensed Agent

Another option for Medicare plan research is to let a licensed agent do the work for you.

Let’s go back to our vacuum cleaner example. Imagine if you had someone do all the vacuum research for you and then present you with only one or two options that meet your needs. Imagine if that service was free, and all you had to do was talk to the agent for a few minutes to hear about all the benefits. What if the vacuum didn’t cost anything different just because you bought it from the agent instead of Amazon. Wouldn’t you take that deal?

At MedicarePlanFinder.com, we have agents across 38 states that can help you sort through your Medicare options and narrow it down for you. The appointments are free and easy, and you won’t pay any more for your Medicare plan whether you buy it from a licensed agent or online by yourself.

The difference is that our agents are experienced and can tell you all the ins and outs of your plan options (maybe even more than what is advertised online)!

Ready to get started? Give us a call at 844-431-1832 or click here to have an agent call you.

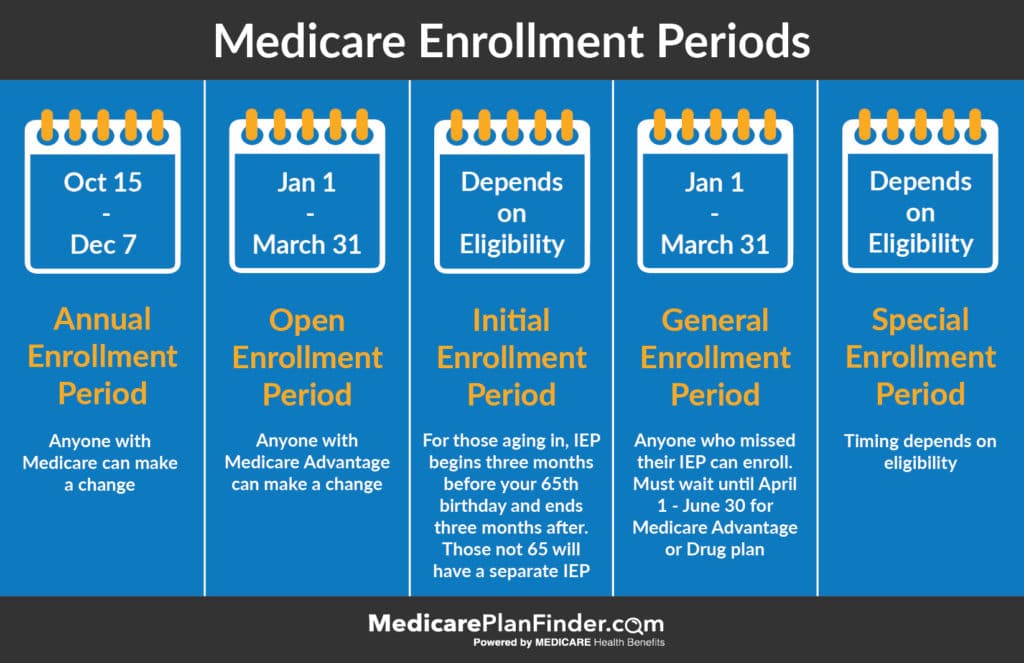

When Can You Enroll in Medicare in 2020?

Your enrollment periods will depend on a few factors, such as:

What type of coverage are you hoping to enroll in?

Are you over the age of 65?

Do you have a chronic condition or low income that qualifies you for a Special Enrollment Period?

Do you have a qualifying life event such as moving to a new state where different plans are available?

Medicare Enrollment Periods | Medicare Plan Finder

Initial Enrollment Period

Your Initial Enrollment Period is the time you get started with Medicare coverage.

If you are eligible for Medicare due to age (you are over 65 or about to turn 65), your Initial Enrollment Period will last from three months before your 65th birthday through three months after.

Initial Enrollment Period Medicare

If you qualify for Medicare for another reason, such as having a disability or chronic illness, your Initial Enrollment Period will be the month of your diagnosis.

Annual Enrollment Period

Once you’ve enrolled in Original Medicare (Parts A and B), you’re eligible for the Annual Enrollment Period. The AEP runs from October 15 through December 7 of each year. During this time, you can enroll in Medicare Advantage or Part D (prescription drug coverage).

Special Enrollment Period

There are two types of Special Enrollment Periods: Immediate/consequential and “long-term”. If you qualify for an immediate Special Enrollment Period, you typically have 90 days to make a change following a major life event. If you qualify for a “long-term” special enrollment period, you are able to change plans once per quarter for the first three quarters of the year (and during AEP, which falls during the fourth quarter of the year). Keep in mind that a SEP is never truly permanent, as you could lose your eligibility at any time due to a major life change.

To qualify for an “immediate” SEP, you must incur a major life change such as moving to a new service area that has different plans available (a different zip code), moving into or out of a medical facility, gaining or losing Medicaid eligibility, etc. You can also gain a SEP if your plan decides to leave the Medicare program

To qualify for a “long-term” SEP, you must be:

Eligible for Medicaid,

Eligible for a Medicare Savings Program,

Eligible for a Special Needs Plan, or

Eligible for LIS (Extra Help)

Other Enrollment Periods

Technically, there are two other Medicare enrollment periods as well.

The General Enrollment Period runs from January 1 through March 31 and is a time when people who missed their Initial Enrollment Period can sign up for Medicare parts A and B. The Open Enrollment Period also runs from January 1 through March 31 and is for those who selected a Medicare Advantage plan during AEP and changed their mind.

It’s important to make note of all the Medicare enrollment periods and which ones you are eligible for so that you don’t miss your chance to enroll!

Ready to get started? Give us a call at 844-431-1832 or click here to have an agent call you during your enrollment period.

This post was originally published on October 16, 2019, and was last updated on November 13, 2020.