However, the Medicare AEP only lasts from 10/15 through 12/7 of each year. Some people may qualify for a Special Enrollment Period and may be able to change plans outside of the AEP, but for many, this will be the only time to change plans!

What you Should do During Medicare AEP

Even if you think you have the best Medicare plan in the world, here are a few things you should definitely do during or leading up to Medicare AEP. If you need help with this, we advise giving us a call.

Check Eligibility for Savings.

Apply for LIS (Extra Help) prescription drug savings program) and other Medicare Savings Programs to see if you could be saving money. If you have low income, you may even want to try applying for Medicaid! The results could influence what coverage you are eligible for this AEP.

Review Current Medicare Coverage.

Did you receive your ANOC (Annual Notice of Change), and is anything in your plan changing? These letters are usually sent and received every year at the beginning of September.

What insurance do you have now?

Do you have Original Medicare only, or do you have a private plan as well?

Do you have enough coverage?

Does your plan fit into your budget, or could you be saving more money?

Are all of your doctors and prescriptions covered by your current plan?

Ask yourself these questions and take notes, because there may be something better out there.

Notate your Life Changes.

Did you start seeing a new doctor this year, or do you have a problem with your current doctor? Not all plans accept the same doctors, so make sure you’re documenting your current physicians so you can easily confirm they are in network with any potential plans you’re considering for the new year.

Did you gain or lose a job, or suddenly develop financial stress? There are multiple ways to manage your Medicare based on a budget and a licensed agent can walk you through the options you may qualify for.

Were you diagnosed with a new health condition that requires expensive treatments? Some plans are specifically designed for certain chronic conditions.

Think about not only your past year but what you expect to happen over the next year. Think about what type of coverage you might need to get yourself through it all.

See What Medicare Plans are Available in 2026

Every year, new Medicare plans may come to the market, and old plans may change what they are offering. It’s important to look at the new information instead of just assuming that your old plan will stay the same. If your plan does change what they are offering, you will be notified – but it is important to look at other changes in your area as well.

Maybe there’s a great new doctor you’ve wanted to see, but she doesn’t accept your current plan! Or, maybe you suddenly have access to a plan with a five-star rating, when previously you only had access to four-star plans!

An important thing to note is that new benefits are not available to review and discuss each year until October 1st. You may need to speak with a licensed agent to ensure you’re reviewing the plans for the upcoming benefit year and not mistakenly comparing plan benefits that will ultimately be changing.

Meet with an Insurance Agent.

We know it’s nice to think that you can do it all yourself and that with the internet, you don’t need an insurance agent anymore! But, that’s not always true. The benefits of meeting with a licensed insurance agent are simple: it’s free, it’s easy, and it can’t hurt!

Our agents are licensed and represent a variety of different insurance companies, meaning they are not all biased towards one plan option.

Your plan won’t cost any more money whether you meet with an agent or not, so meeting an agent can only help you. A licensed agent can walk you through everything that is available in your local area and help you select the best option based on your needs. Plus, let us repeat – the meeting is free!

We’re here to help, so we don’t want to only talk about the positives. Here are some things that you should NOT do during the Medicare AEP:

Don’t Jump into a new Medicare Plan Too Fast.

Do you understand how to choose a Medicare plan? Sometimes good deals are tempting, and it’s easy to jump into a shiny new plan because the costs are lower or there’s an added benefit. Make sure you’ve considered everything before you switch because it might not be easy to switch back. Make sure that your doctors work with the new plan, it covers your prescriptions, and there aren’t any hidden costs. Also, make sure the new benefit is something that will actually be useful to you!

Misunderstand Medicare Supplements vs. Medicare Advantage Plans.

Medigap, or Medicare Supplements work differently from Medicare Advantage and other types of Medicare plans. Technically, Medigap enrollment is not limited to the AEP. However, that does not mean that you should just change back and forth between different Medigap plans any time.

If you enroll in Medigap outside of your Initial Enrollment Period (when you first become eligible for and enroll in Medicare), you may be put through an underwriting process and may have higher fees based on your age and any preexisting conditions. Medicare Advantage and Part D plans do NOT take age and preexisting conditions into account, but Medigap plans if you wait too long to enroll.

3. Don’t Avoid Researching Medicare Plan Options.

If you already know the name of a carrier, you might be tempted to go straight to their website and enroll in a plan that looks good online. However, there may be more than one carrier offering plans in your area. So, how do you look at all of them easily?

Start by using a plan comparison tool, like our free Medicare Plan Finder. Then, once you’ve compared a few options, consider taking that research to a licensed agent who can talk to you about what you’re looking at and why the differences matter.

Ready for AEP?

To schedule an appointment with one of our licensed agents, call (833)-567-3163 or click here. We can’t wait to help you get the coverage you deserve!

Good News: 2021 Medicare Advantage Plans Have Higher Ratings and Lower Premiums

It’s time to start making decisions for your healthcare coverage in 2021. The Annual Enrollment Period for Medicare beneficiaries is going on NOW and only lasts through December 7.

As you’re looking through your Medicare Advantage and Part D plan options for next year, you may notice that monthly premiums are shrinking and benefits are expanding!

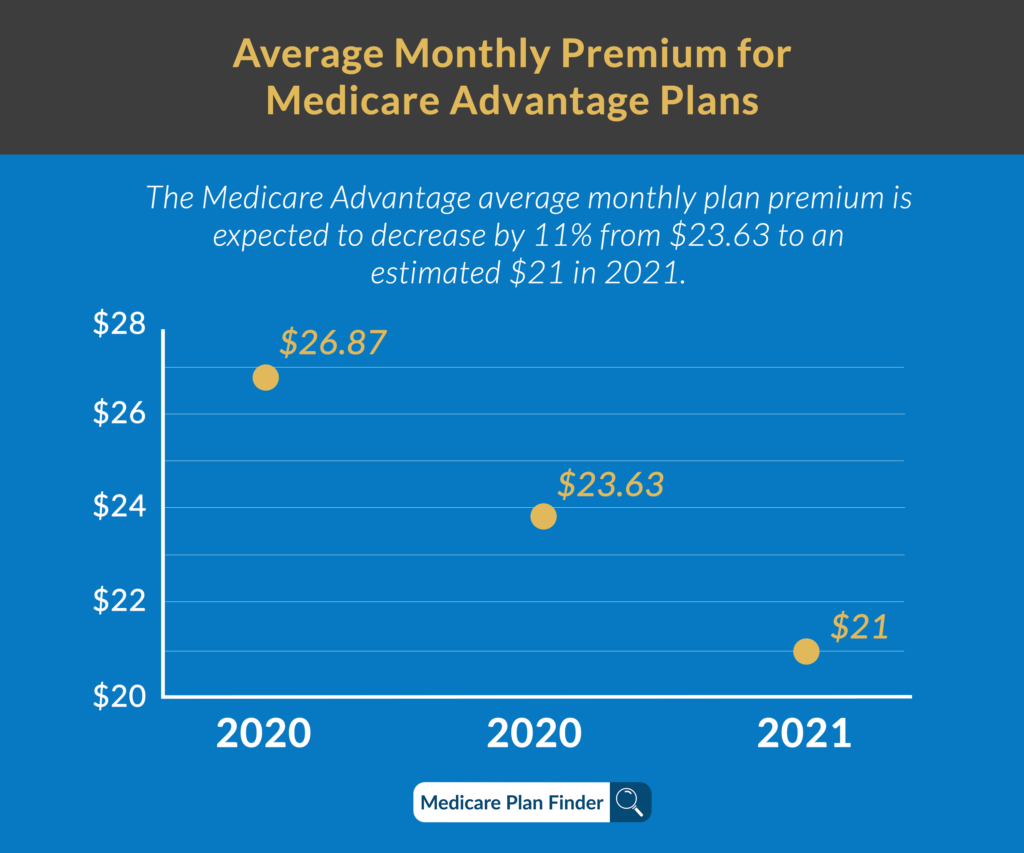

CMS (The Centers for Medicare & Medicaid Services) released a statement earlier this fall that said the average monthly premium for a Medicare Advantage plan in 2021 will be the lowest it’s been in 14 years (since 2007!)

In fact, the average Medicare Advantage (MA) premium will see a decrease of 34.2% from 2017, while plan choice and benefits continue to expand. In some states like Alabama, Nevada, and Kentucky, the average premium decrease since 2017 will be closer to 50%.

Medicare Part D prescription drug plans (PDPs) will also have low premiums in 2021, with standard plans averaging around $30.50 a month. This marks a 12% decrease in PDP premiums since 2017.

Average monthly Medicare Advantage premiums

Average star ratings increasing

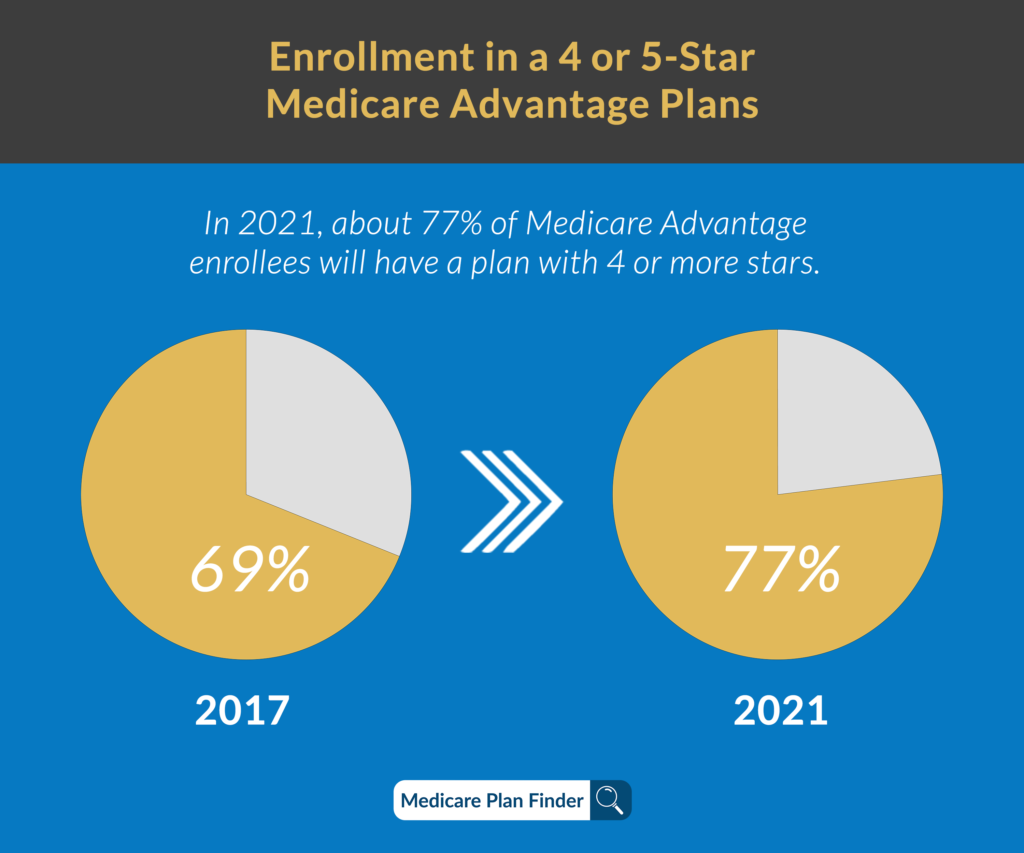

The average star ratings for Medicare Advantage and prescription drug plans in 2021 are set to increase significantly. About 77% of Medicare Advantage enrollees will have a plan with 4 or more stars, and 98% of those in a standalone PDP plan will have a rating of more than 3.5 stars.

There will also be more plans with a 5-star rating than were available in 2020, including UnitedHealthcare, Cigna, and Anthem BCBS. Even the lowest-rated plans have improved to at least 2.5 stars.

CMS uses this Medicare star rating system for Medicare Advantage and Part D plans to determine whether or not a plan is doing its job, and whether or not it can stay on the market. Plans that consistently receive poor ratings (one or two stars) will eventually be removed from the market.

Plans are given a star rating between one and five, with one being “poor” and five being “excellent.”

Medicare Advantage plans are rated on the following factors:

Level of access to preventive services (including annual physical exams and screenings)

Care coordination

How often members receive treatment for long-term conditions

Current member satisfaction

Plan performance in comparison to the previous year

Customer service quality

Part D plans are rated on the following:

Number of member issues with the plan

How many people left over one year

Patient safety while using prescriptions in the plan

Accuracy of pricing

Quality of care

Customer service quality

More and more Medicare Advantage and Part D plan carriers are entering the market every year, meaning there is more competition. More competition means that more plans are trying to be the most valuable to be able to compete. That’s why even though costs may be going down, plan ratings are still increasing.

If you plan on meeting with a licensed agent during this year’s Annual Enrollment Period, be sure to ask about four and five-star plans in your area!

3300Medicare Advantage star ratings increasing

Remind me: What is Medicare Advantage?

You can enroll in Medicare Advantage as an addition to your Original Medicare coverage. Since Medicare Advantage plans are owned and operated by private insurance companies and are not the same as the government Medicare program, the coverage is a bit different.

Medicare Advantage plans are able to cover things that Original Medicare is not, such as fitness programs, dental, vision, and prescription drugs.

Medicare Advantage plans might come with copayments, coinsurance, and deductibles, but the average premium for 2021 is expected to be $21/month.

If you can afford to add a Medicare Advantage premium, the benefits may save you from thousands of dollars in healthcare costs later on.

Expanded benefits for 2021

Earlier this year, CMS released the 2021 benefit and cost sharing information on Medicare.gov. In large part due to the coronavirus pandemic, they are offering expanded benefits in several key areas, and many health care providers are taking advantage of this flexibility.

There will be over 4,800 Medicare Advantage plans in 2021 for enrollees to choose from, a 76.6% increase since 2017. The number of MA plans per country is also growing in the new calendar year.

In response to the COVID-19 pandemic, 94% of all MA plans will provide added telehealth benefits. The current health crisis also drove CMS to develop the Part D Savings Model, which sets a $35 monthly copay rate for insulin. Over 1,750 MA and PDP plans are participating in this new model in 2021.Many health plans are also expanding their benefits for enrollees with chronic conditions. About 500 Medicare Advantage plans will feature either supplemental benefits or lower copays to those with specific chronic diseases or other conditions.

$0 Premiums and Special Needs Plans

Some people may even be eligible for a $0 premium Medicare Advantage plan. Others still may be eligible for low-cost Medicare Advantage Special Needs Plans.

CSNPs are Chronic Special Needs Plans and are for people who have certain chronic conditions and need additional coverage. ISNPs are Institutional Special Needs Plans and are for people who have been living in an institution such as an inpatient medical facility for 90 days or more. DSNPs are Dual Eligible Special Needs Plans and are for people who are dual-eligible for both Medicare and Medicaid.

How to Get a Low-Cost, Five-Star Medicare Advantage Plan in 2020

Our licensed agents across the nation are contracted and certified to sell a number of Medicare Advantage plans. An agent can sit down with you and show you all of the top-rated plans available in your area and help you select which one is best for you.

To get in touch with a licensed agent, call 844-431-1832 or click here.

What Can You Do During the Medicare Annual Enrollment Period?

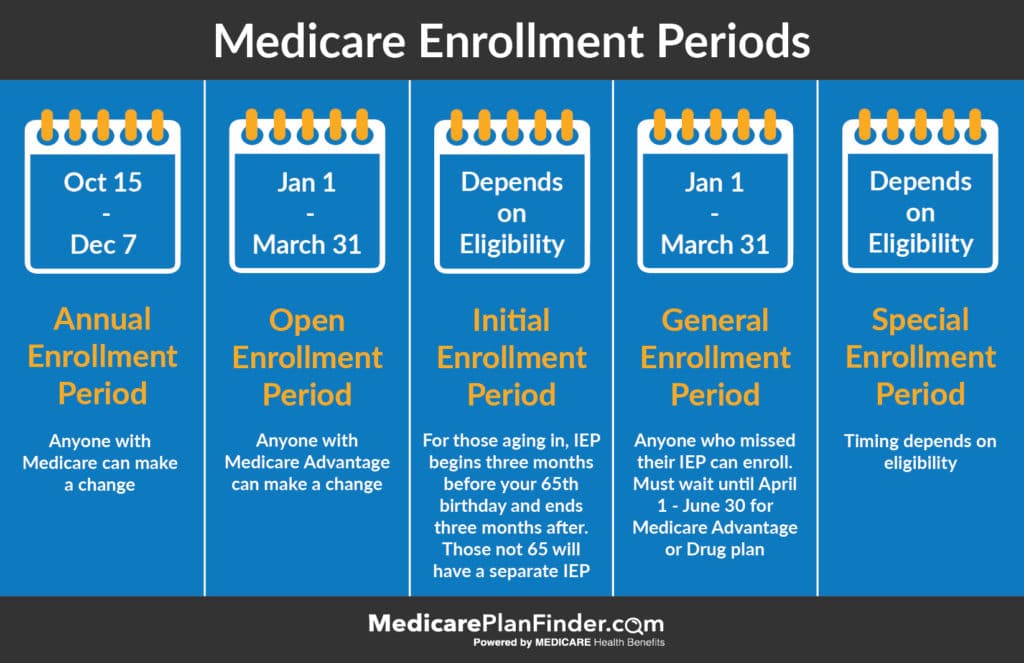

Medicare Enrollment Periods

Did you know that there are five different Medicare enrollment periods throughout the year? Not everyone will be eligible for every period, but everyone who has Medicare is eligible for the Annual Enrollment Period.

Be sure to keep track of each enrollment period so that you know when it’s your turn to make changes. Don’t go months with a bad plan just because you missed your enrollment period!

What/When is the Annual Enrollment Period?

The Annual Enrollment Period runs from 10/15 through 12/7 of each year. This is the time when all Medicare beneficiaries are eligible to make changes, which will go into effect on January 1 of the following year. It does not apply to people who have not yet enrolled in any form of Medicare coverage. If you’re enrolling for the first time, you’ll have an “Initial Enrollment Period.” You can use the AEP later to make changes if you don’t like the choices you made during your IEP.

Changing Medicare Plans After the Annual Enrollment Period

There are a few other times throughout the year when you may be eligible to make changes.

The Initial Enrollment Period (IEP) is for those enrolling in Medicare for the first time. If you are aging into the program, this will begin three months before your 65th birthday and end three months after. If you become eligible due to disability, your IEP will depend on your disability status or diagnosis.

The General Enrollment Period (GEP) is for those who missed their IEP. It runs from January 1 through March 31. If you enroll during the GEP, your coverage will begin on July 1. You may face a late enrollment penalty fee for not enrolling during your IEP. If you want to enroll in Medicare Advantage during the OEP, you can do that between April 1 and June 30, or you can wait for the AEP.

The Special Enrollment Period (SEP) is not one specific time frame. You may qualify for a “temporary” SEP if you have a special circumstance that results in a loss of coverage, such as losing a job with coverage or moving to an area where different plans are available. You will likely have 30 days following the event to make a change. Some circumstances, like having a disability, can make you eligible for a different type of SEP. If you are disabled or have low-income and have a special needs plan, you can change plans once per quarter for the first three quarters of the year.

How can I get a SEP for Medicare?

To qualify to change plans once every quarter for the first three quarters of the year, you must:

Be a member of a Medicare Savings Program or Medicaid

Be part of SPAP (State Pharmaceutical Assistance Program)

Be in a Medicare Savings Program or LIS (Extra Help)

To qualify for to change plans once following an event, you must:

Move to a new service area that has different plan options available

Involuntarily lose your coverage

Find a contract violation with your plan

Lose or gain a job where you are enrolled in employer benefits

Move into or out of a medical facility

Leave imprisonment

Suddenly gain or lose Medicaid eligibility

Suddenly gain or lose Medicare Savings Program or LIS eligibility

Have been automatically enrolled in Part D

OEP vs. AEP

OEP is not the same as AEP. During AEP, you can make a lot of different changes to your coverage. During OEP, you can only do one of the following:

Switch from one Medicare Advantage plan to another

Change from a Medicare Advantage plan with prescription drug coverage to Original Medicare + Part D

Switch from Medicare Advantage to Original Medicare (can also add Part D)

What can I do During the AEP?

During AEP, you can make a number of different changes to your coverage, like:

Enroll in a Medicare Advantage plan

Switch to a different Medicare Advantage plan from what you had

Drop your Medicare Advantage plan and have only Part A and Part B

Add a Part D prescription drug plan

Change to a Medicare Advantage plan with a prescription drug benefit

Change from a MAPD (Medicare Advantage Prescription Drug Plan) to a Medicare Advantage plan without prescription coverage

Change from one Part D plan to another

Drop your prescription drug coverage and return to Original Medicare only

You can also add or remove Medicare Supplement (Medigap) coverage, but keep in mind that you can enroll in Medicare Supplements during any time of year. Enrollment periods to not apply to Medicare Supplement plans. However, if you enroll in Medigap any time past your Initial Enrollment Period, underwriting may apply, leaving you with higher costs than you could have had if you enrolled sooner.

Why the AEP is so Important for Medicare

The ability to make these changes every year is more important than you may realize.

Even if you think you’re happy with your plan, plans are allowed to change their benefits and costs every year. Your plan can add or remove benefits and make cost adjustments as they need to. At the same time, new plans are continually entering (and leaving) the market. It’s a good idea to take a look and see if there is a better plan for you each year.

Licensed agents are required to go through a training and certification process before they can sell to you. They are usually trained on what’s going on in the area that they sell in. They may be able to tell you about plans that you haven’t even heard about before, and they can help you sort through your options. It does not cost anything to meet with a Medicare Plan Finder licensed agent.

Can you Auto-Renew Medicare?

In most cases, you do not have to renew your plan each year. Your Medicare coverage will automatically continue as long as that plan is still available for the current year. The only reason your plan wouldn’t renew is if that specific plan itself leaves your service area or leaves Medicare.

However, that does not mean that you shouldn’t review your coverage each year. Have your finances or your healthcare needs changed? Has your plan changed its benefits or costs? Ask these questions every year to make sure you’re still getting the coverage you need.

New to Medicare

How to Make Medicare Plan Changes

You can enroll in a new Medicare Advantage plan by getting help from a licensed agent. If you haven’t enrolled in Original Medicare yet, be sure to do that first by contacting Social Security either online or at 1-800-772-1213. You can also visit your local Social Security office.

To get in touch with a licensed agent in your area, click here or call us at (833)-567-3163.