7 Common Medicare Mistakes to Avoid

Choosing the right Medicare plan for you can seem daunting. You may be confused about what plan to buy or frustrated that you can’t find the information you need to make a sound choice.

You don’t want to potentially be stuck paying huge penalties or have a plan that doesn’t work for you. However, if you have the right knowledge, you can steer clear of the hassle that comes with these seven common Medicare mistakes to avoid.

1. Waiting Until It’s too Late to Sign up for Medicare

If “timing is everything,” that goes double for Medicare enrollment. One of the most common Medicare mistakes to avoid is putting off enrollment until it’s too late. Many people know that you can enroll in Medicare when you’re 65, but what they might not know is that you can actually start the process when you’re 64. The three months before your 65th birthday, the three months after your birthday, and your birthday month is what’s called the Initial Enrollment Period (IEP).

You can avoid costly penalties if you sign up during your IEP. If you sign up to late your Medicare Part B premium may go up 10 percent for each year that you could have been covered but didn’t enroll.

Note: There are some exceptions to late enrollment penalties, but it’s much easier to enroll during your window of opportunity.

2. Being Confused About the SEP

The IEP doesn’t apply to everyone. For example, people with certain chronic conditions or people who’ve received SSDI benefits for at least 25 months may be eligible for a lifelong Special Enrollment Period (SEP). If you qualify, your lifelong SEP will allow you to make changes to your coverage once per quarter for the first three quarters of the year.

People who go through certain life changes such as losing coverage upon retirement or losing a spouse’s coverage can sign up for Medicare during a temporary SEP, which allows you to enroll late without paying a penalty. However, a circumstantial SEP is only for eight months after you stop receiving employer coverage, so it’s crucial that you enroll during that time frame.

3. Thinking You’re Covered Just Because Your Spouse Has Coverage

Employer insurance plans usually come with an option that covers you and your spouse. Medicare does not work that way. You and your spouse each need an individual plan.

This is actually a good thing. When you were younger, it probably made more sense to not deal with multiple insurance carriers. However, as you age, you become more susceptible to certain illnesses, and you may have different needs than your spouse. You may need more or less covered services.

For example, you might only need to visit your doctor every once in a while for wellness exams or the occasional sickness. However, your spouse may need to look into enrolling in a special type of plan called a Chronic Special Needs Plan (C-SNP) because of a chronic illness.

4. Not Using the AEP to Make Changes or Enroll in New Plans

If you don’t take advantage of the Annual Enrollment Period (AEP), which is October 15 – December 7, you could be stuck with a plan that doesn’t fit your needs for another year.

For example, if you only have Original Medicare and you want to capitalize on the supplemental benefits Medicare Advantage plans can offer, AEP is your window of opportunity.

5. Assuming Medicare Is Unaffordable

Some people may put off enrolling in Medicare because they think they can’t afford it.

While Medicare isn’t free, many people can get premium-free Medicare Part A. You will not owe a Part A premium if you or your spouse has worked and paid Medicare taxes for more than 40 quarters.

Even though you may have to pay premiums for Part B and other Medicare coverage, there is help available. If you have a limited income, you may be able to find assistance through certain Medicare programs such as Medicare Savings Programs, Low Income Subsidy Extra Help, and state Medicaid programs.

- Medicare Savings Programs (MSPs): These programs can help pay the Part B monthly premium and help out with coinsurance fees, depending on the program. (There are currently three types of MSPs).

- Low Income Subsidy (LIS) Extra Help: This federal program can help pay for the costs associated with Medicare Part D prescription drug coverage.

- State Medicaid Programs: This program is funded by both federal and state resources. Medicaid provides medical assistance for people with low incomes and few assets. All Medicaid programs provide certain coverages such as prescription drugs.

People who qualify for MSPs or LIS may also qualify for Medicaid. If you’re eligible for both Medicare and Medicaid, you can enroll in what’s called a Dual Special Needs Plan (DSNP). A DSNP may help pay for most or all of your healthcare costs.

6. Thinking Medicare Covers Everything

Original Medicare (Part A and Part B) is a great resource for helping out with healthcare costs, but it doesn’t cover everything. Medicare Part A covers inpatient services at hospitals. Medicare Part B covers outpatient services such as doctor’s appointments. Even with those services, you’ll still owe your monthly premium and coinsurance if you see your doctor. For example, the fee for Part B services is usually 20 percent of Medicare-approved costs.

Original Medicare doesn’t cover many services people need such as vision, hearing, and dental care. The Centers for Medicare and Medicaid (CMS) allows private insurance plans called Medicare Advantage (MA) plans to provide those services.

Not every plan in every location offers those extra services, so it’s a good idea to talk to someone who can help you find the plans available in your area if those services are important to you. A licensed agent with Medicare Plan Finder can help you determine what type of Medicare plan is right for you.

For some people, Medicare Advantage plans may not make sense, but they still need more coverage than Original Medicare provides. Some people may only need help with financial items such as coinsurance fees. Those people might benefit most from a Medicare Supplement (Medigap) plan. While MA plans help cover healthcare services, Medigap plans only cover costs.

7. Not Understanding What You Have to Pay out of Pocket

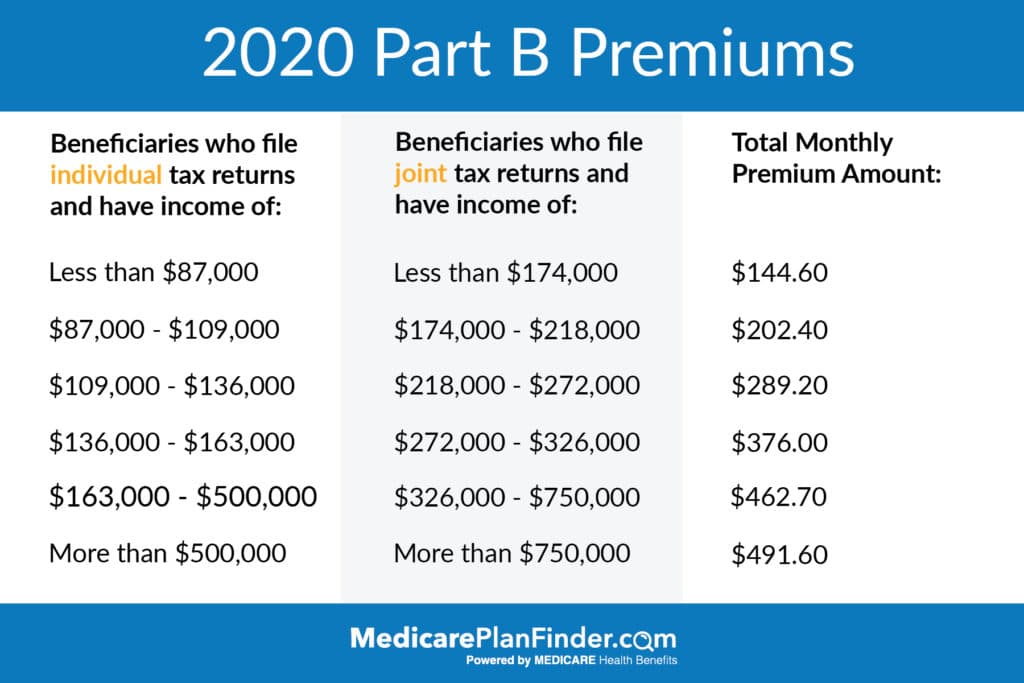

Even if you enroll in a Medicare Advantage or Medigap plan, you may still owe monthly premiums. That means that even though your Medicare Advantage plan may have a $0 premium, you may also have to pay the Part B premium, which is $144.60 in 2020 (unless you have high income).

You may also have to pay a deductible before your coverage starts. The Part B deductible in 2020 is $198. Your MA or Part D plan may also require you to pay a deductible.

You may also have to pay copays or coinsurance. You may owe a copay, which is a fixed amount you pay for services such as doctor’s appointments with many MA plans. Coinsurance is a percentage of covered services. Original Medicare pays about 80 percent of approved costs and you are responsible for the other 20 percent. Your cost sharing for covered services may be different if you’re enrolled in a MA or Medicare Supplement plan.

Let Us Help You Avoid Common Medicare Mistakes

Medicare can be confusing. You might not know what coverage you need or what type of plan fits your budget and lifestyle. A licensed agent with Medicare Plan Finder can show you what’s available in your area and help you choose the best plan for you. Your agent is familiar with the common Medicare mistakes to avoid and help you take the right steps. To schedule an appointment, call 844-431-1832 or contact us here today.