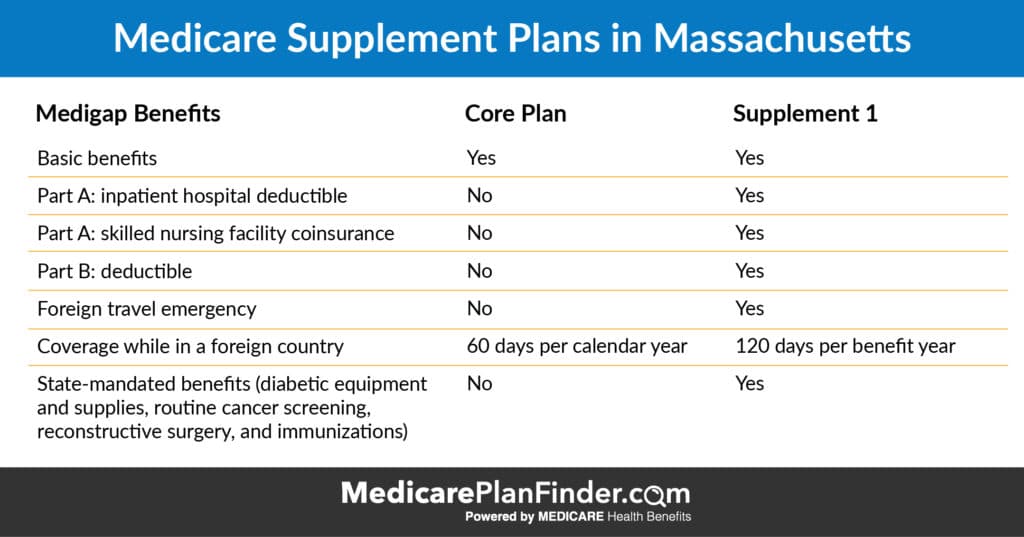

How Medigap is Unique in Minnesota, Wisconsin, and Massachusetts

In most of the United States, Medigap (also called Medicare Supplements) can be characterized by eight different types of plans (A, B, D, G, K, L, M, N). However, there are three states that work completely differently: Massachusetts, Minnesota, and Wisconsin.

A lot of the information you’ll see on the internet about Medicare Supplement plans talks about those eight plans, but we haven’t forgotten about you, Massachusetts, Minnesota, and Wisconsin! If you live in one of those three states, this guide is for you.

Psst…click below to read more about Medicare programs in each state:

If you already have a basic understanding of Medigap, you can skip ahead to the section about your state below.

Medigap is a type of private Medicare insurance that is not technically part of the government-sponsored Medicare program. Medigap plans are also called Medicare Supplements. The two terms can be used interchangeably. To enroll in Medigap, you have to enroll in Original Medicare first.

Additionally, you cannot have a Medicare Supplement plan and a Medicare Advantage plan at the same time. Click here to find out if Medicare Advantage is better for you than Medicare supplements.

What Does Medigap Cover?

Uniquely, Medicare Supplement plans do not typically provide additional health benefits. Instead, Medigap plans provide additional financial protection. For example, let’s say you get sick and have to go to the doctor at least once per month for treatment. Original Medicare may not cover the entire cost for you. You might have to pay your deductible first ($185 for Part B in 2019) and then 20% coinsurance on every visit.

If you have a Medicare Supplement plan that includes deductible and coinsurance coverage, you may not have to pay that $185 and 20%. Instead, you’ll only have to pay your Part B* premium and your Medigap premium.

You may have heard that you cannot be denied Medicare coverage based on your age or preexisting conditions. While that’s true, Medigap is a little different. If you enroll in a Medicare Supplement plan during your Initial Enrollment Period (the time when you first become eligible for Medicare), that holds true. However, if you wait too long to enroll, there is a chance that your plan will be put through underwriting and your prices may increase, or you may be denied coverage based on your age and preexisting conditions.

*Some people may have a Part A premium as well.

Senior couple speaking with a doctor

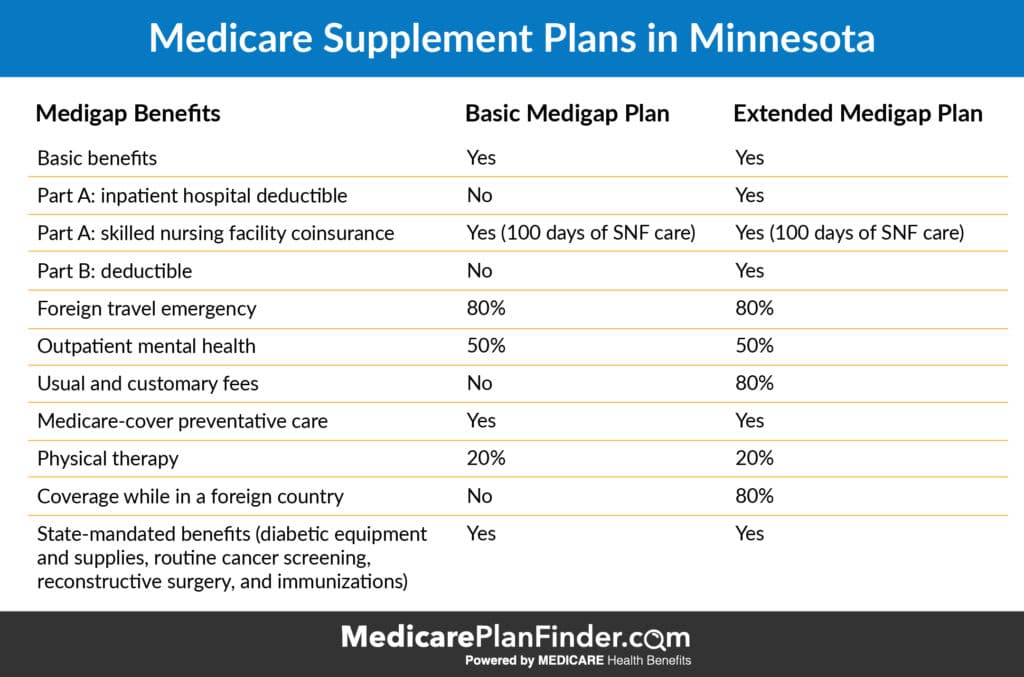

Minnesota Medicare Supplement Plans

While you can’t get the same eight plans (A, B, D, G, K, L, M, N) in Minnesota that are offered in other states, there are technically modified versions of plans K, L, M, and N available.

Additionally, Minnesota offers two unique plans: The “Basic Plan,” and the “Extended Basic Plan.”

The preexisting conditions underwriting may apply. However, you’ll get a 6-month Medigap enrollment period (where age and preexisting conditions do not apply) if you return to work or if you drop Part B in favor of your employer’s health plan.

80% of foreign travel emergency, then 100% after you spend $1,000 per year out-of-pocket

80% of “usual and customary fees,” then 100% after you spend $1,000 per year out-of-pocket

Minnesota Medicare Supplement Plans

So you’re probably wondering, if the Minnesota Medigap Basic Plan and the Extended Basic Plan both always offer the same benefits, why would you choose one Basic Plan over another?

The answer is that costs can vary and plans are allowed to add some extra benefits. There are four additional benefits that plans are permitted to add to the Basic and Extended Basic plans: Part A inpatient deductible, Part B deductible (no longer available in 2020), usual and customary fees, and non-Medicare preventive care.

At least $30,000 for kidney disease treatment (dialysis, transplants, etc.)

Insulin pumps, self-management training, and other diabetes care

50% and 25% cost-sharing plans are also available, which are similar to Medigap Plan K and Medigap Plan L (which would be available in other states).

So, you might be wondering why you have multiple options to choose from for Wisconsin Medigap plans if they are all supposed to be the same “basic” plan. The answer to that is that plans ARE allowed to add additional benefits other than what is in the basic plan, and the costs can vary. Companies are allowed to add the following benefits:

Why Can’t I get Part B Deductible Coverage in 2020?

When MACRA (The Medicare Access and CHIP Reauthorization Act) passed in 2015, a couple of changes were made that didn’t take effect right away; Losing Part B deductible coverage was one of them.

Congress made the decision to not allow plans to cover the Part B deductible starting in 2020. This decision saves money for the Medicare program and doesn’t have an astronomical effect on you. The Part B deductible was only $185 in 2019. All this means is that you will have to pay $185 out-of-pocket before the rest of your coverage kicks in.

It also means that if you are already enrolled in one of the plans listed above that includes the Part B deductible, you won’t lose that coverage. However, if you decide to switch plans or drop that coverage at any time, you won’t be able to get back into it starting in 2020.

How do I Decide Which Medigap Plan is Right For Me?

Regardless of which state you live in, we have a plan finder tool that can help you compare your options.

We also have licensed agents available to answer your questions and help you make your final decision. To find out if there is an agent near you that you can meet with, call 844-431-1832 or send us a message by clicking the “let’s chat” button in the bottom right corner.

How to Choose the Best Type of Medicare Plan for You

When it’s time to choose a Medicare plan, it’s easy to get overwhelmed. There are quite a few different types of Medicare plans to choose from. Once you choose what type you want – you still have to choose a plan! Making the right choice is important because it may not be easy to change plans if you change your mind.

The Annual Enrollment Period (October 15 through December 7) is when anyone can make changes, and for some people, it’s the only time. If you make the wrong choice, you might have to wait a whole year before you can change again (unless you qualify for the OEP or have a SEP).

Which Types of Medicare Plans are Best for Me?

To figure out which Medicare plan is best for you, ask yourself the following questions:

What specific medical services do I need coverage for (ex: lab tests, blood work, surgery, chemotherapy, dental, etc.)?

How much room do I have in my budget? Am I able to pay a little more to have more benefits?

Would I rather pay more on a monthly basis and pay very little when I visit the doctor, or is it better to pay a small amount every month but risk having higher copayments?

Who are the doctors and other providers who I want to be covered in my plan?

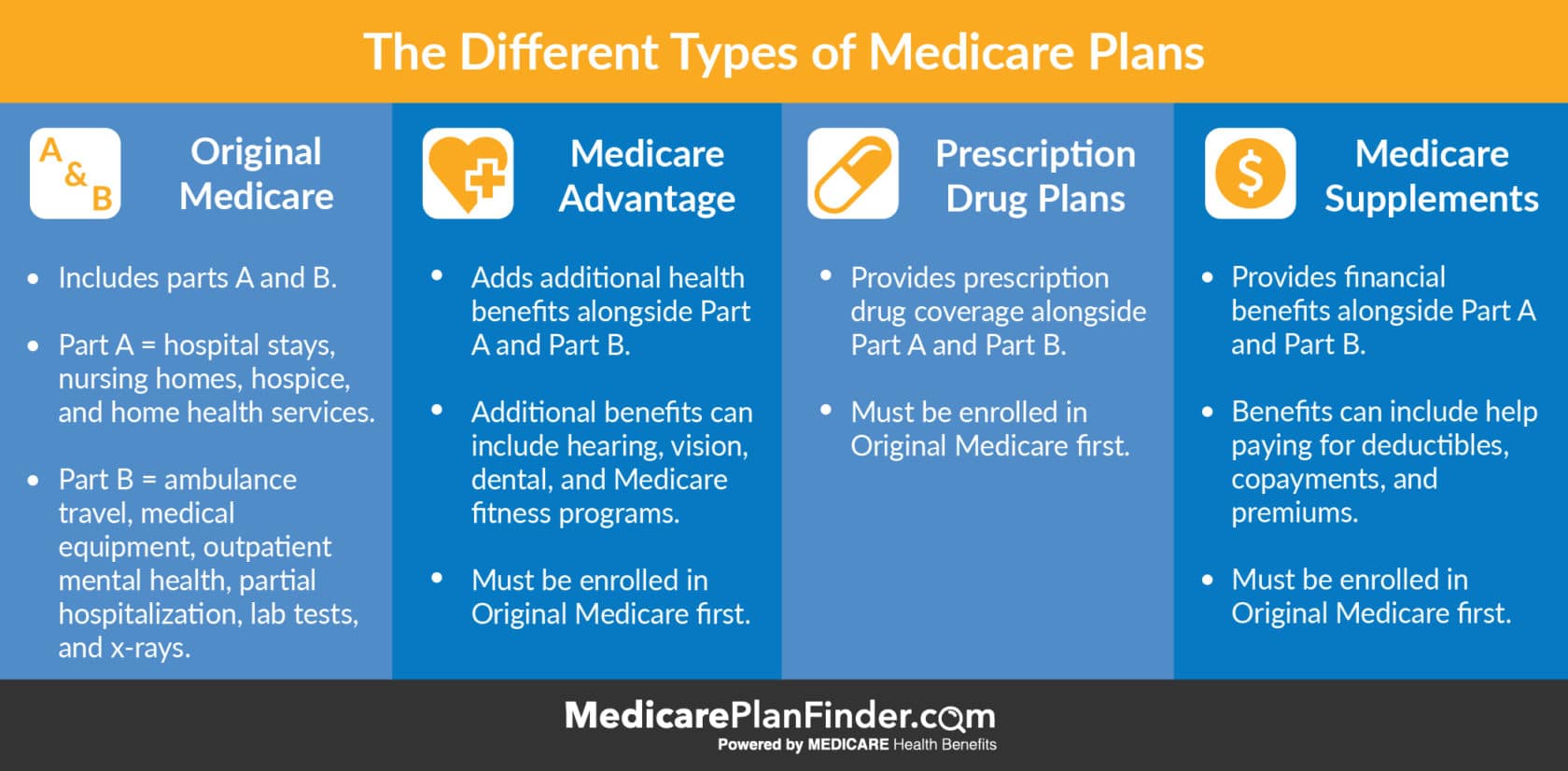

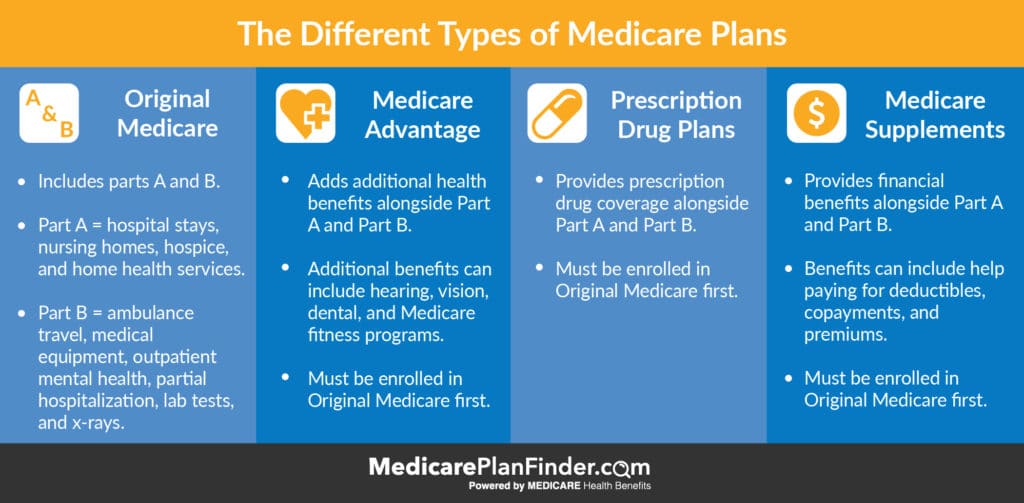

There are four main types of Medicare plans to consider when you begin your Medicare plan search. Start by comparing Original Medicare, Medicare Advantage, Prescription Drug Plans, and Medicare Supplements.

Keep in mind that you cannot have Medicare Advantage and a Prescription Drug Plan at the same time. You also cannot have Medicare Advantage and a Medicare Supplement plan at the same time.

Which plan or combination of plans works best for you?

Medicare Advantage: A private plan that you can purchase once you have Original Medicare. Can add additional benefits such as hearing, vision, dental, fitness, etc. Can include a prescription benefit.

Prescription Drug Plans: Another type of private plan that you can purchase once you have Original Medicare. Usually only includes a prescription benefit.

Medicare Supplements (Medigap): Another type of private plan that you can have in addition to Original Medicare. Adds more financial coverage, like for copayments and deductibles. This type of plan would also require you to have a stand alone part D drug plan.

Different Types of Medicare Plans

Choosing a Medicare Advantage Plan

So, did you decide to go with Medicare Advantage? Great! Now, there are a few types of Medicare Advantage plans that may be available for you. First, ask yourself whether or not you need a large network and whether the freedom to see any doctor is important to you. Then, read through these important differences:

HMO Plans (Health Maintenance Organization) – You’ll select one primary physician. In some cases, you may only receive coverage for that one doctor (unless he or she refers you to a specialist). Requirements may vary based on your plan.

HMO-POS Plans (Point-Of-Service) – You’ll select one primary physician, but you’ll have the freedom to visit any specialist in your network for your other needs. You will be charged a fee for visiting specialists.

PPO Plans (Preferred Provider Organization) – You can see any doctor, but your costs will usually be lower if you choose one that is in your network.

PFFS Plans (Private Fee-For-Service) – You will not need referrals or a primary physician, but you’ll have to pick a doctor that accepts your PFFS plan.

SNP (Special Needs Plans) – Designed for those who are eligible for both Medicare and Medicaid, live in a nursing home, or have a chronic illness or disability.

MSA (Medical Savings Account) – Works like a tax-free savings account for your medical bills. Medicare will deposit money into your HSA. You can use that account to pay for medical expenses.

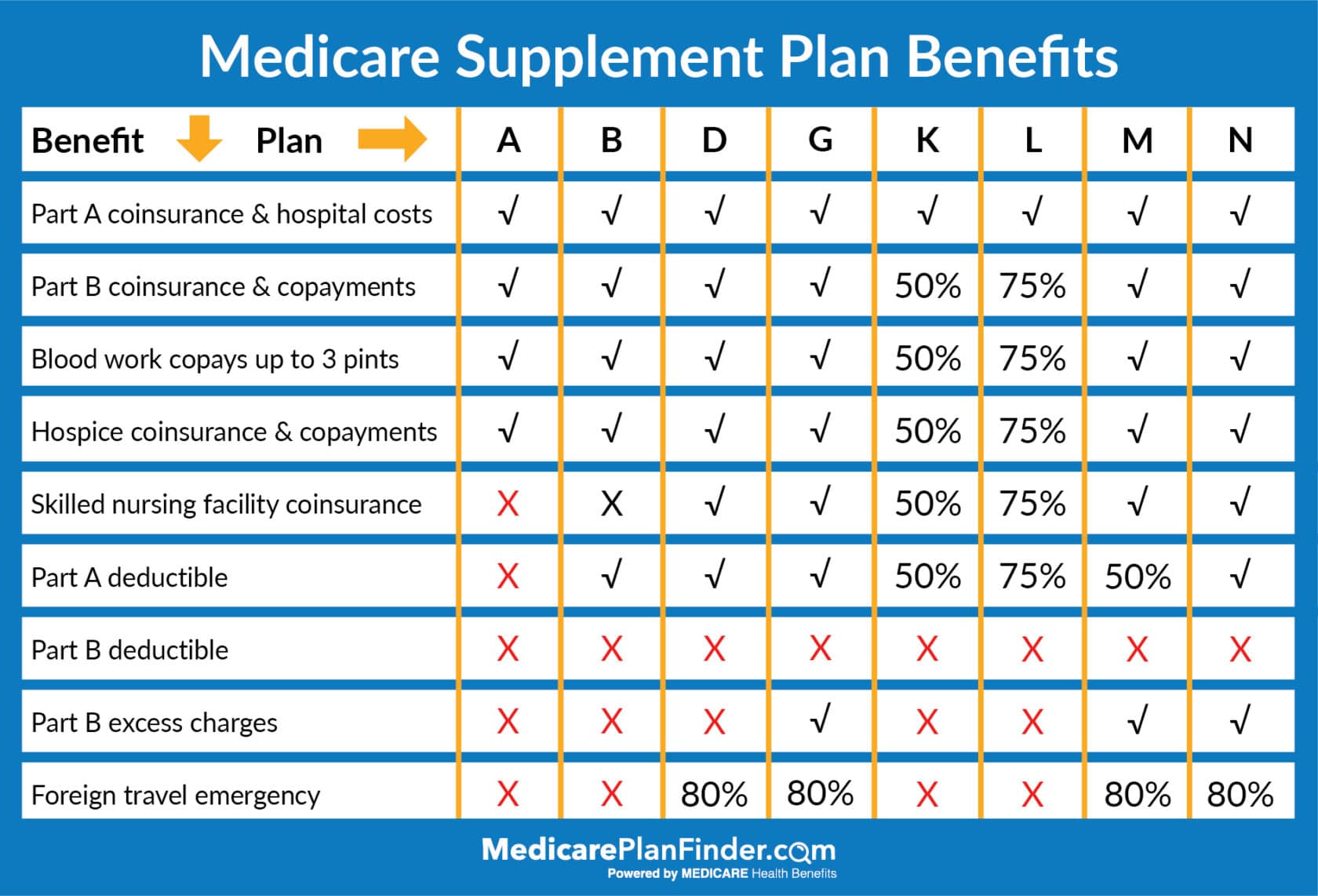

How do I Pick a Medicare Supplement Plan?

If you’ve decided that you want a Medicare Supplement plan, you’ll want to start by selecting the plan letter that corresponds with the coverage you need. Use the chart below for reference.

Once you’ve made that decision, you may have a few different carriers available in your area to choose from (some smaller cities may not have several options available).

Finding Medicare Plans in your area just got easier. Our Medicare Plan Finder tool can help you not only see what is available, but see which options may be best for your unique needs.

You can enroll by yourself, or you can meet with a licensed agent (for free) who can walk you through the process to make sure you don’t make any mistakes. The licensed agent can also talk to you about a variety of different types of plans in your area and answer all your questions.

This unbiased approach is a great way to get the help you need when selecting a Medicare plan.

To set up your free meeting with a Medicare Plan Finder licensed agent, call 833-567-3163 or click here.

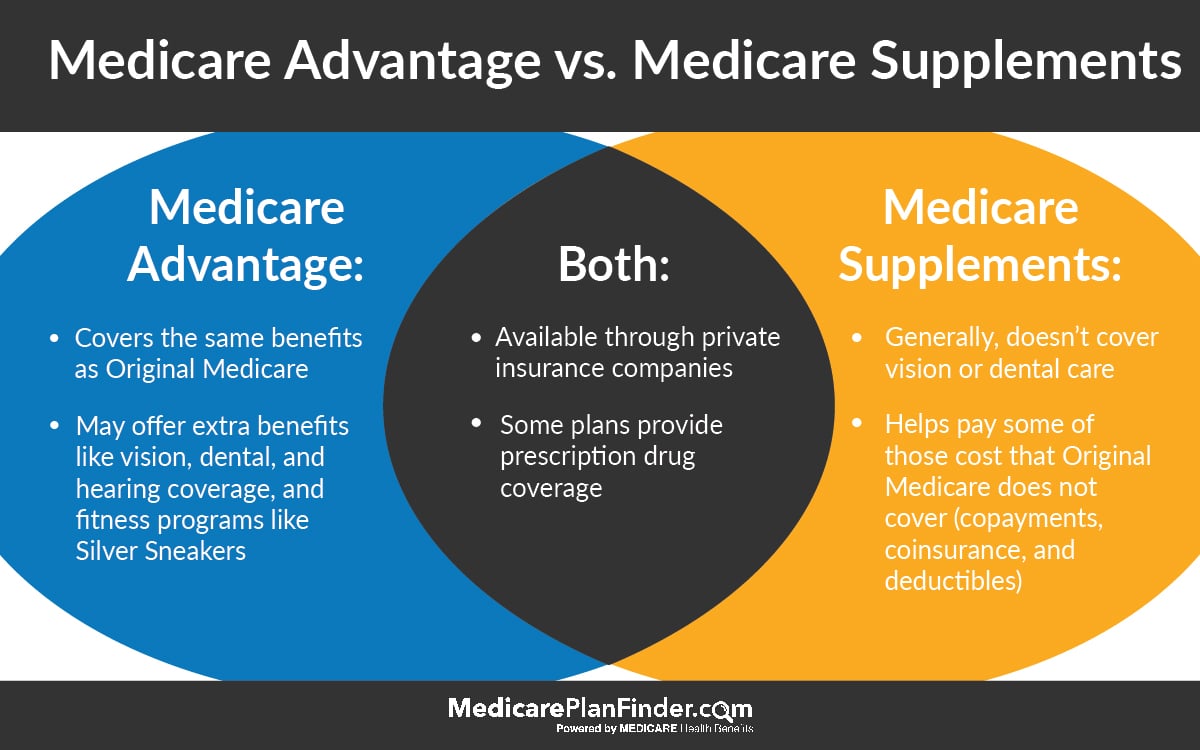

Medicare Advantage vs. Medicare Supplement

Medicare Advantage and Medicare Supplements (also called Medigap) are very different insurance plans with distinct benefits. The answer to the question “is Medicare Advantage better than Medigap?” depends on your circumstances and needs.

What is Medicare Advantage?

Medicare Advantage plans are private plans (not owned by the federal government) that can offer additional health benefits. To have Medicare Advantage, you have to enroll in Original Medicare first. You may have to continue to pay your Medicare Part B premium even if you have Medicare Advantage (MA), but MA premiums can be as little as $0.

Medicare Advantage plans are not all the same, but they can provide benefits like (click on the links to learn more about each one):

There are many different types of Medicare Advantage plans, although not every plan type may be available in your area.

A health maintenance organization (HMO) is a network of health-care providers and facilities where you choose a primary care physician to coordinate your care.

A preferred provider organization (PPO) is also a network of health-care providers and facilities but typically you do not need to select a primary care physician, and you have more flexible options regarding out-of-network care.

A private fee-for-service (PFFS) plan is a mode of benefit delivery where you are not limited to a network. However, there are no guarantees that your doctor or hospital will accept the plan. If you choose to receive your Medicare health coverage through a private Medicare Advantage plan, you must continue paying your Part B premium regardless, because you remain enrolled in Original Medicare (Part A and Part B), even after joining a Part C plan.

What is Medigap?

Medigap is more different from Medicare Advantage than you might think. While Medicare Advantage plans are able to offer health benefits, Medicare Supplement plans (also called Medigap) offer financial benefits. For example, some Medigap plans can cover your Part B premium.

The chart below explains the differences between available Medigap plans in 2020. You can also use our Medicare Plan Finder search tool to compare plans in your area.

2020 Medicare Supplement Comparison Chart

Comparing Medicare Advantage vs. Medicare Supplement plans

Let’s look at Medicare Advantage vs. Medigap. In short, the difference between Medicare Advantage and Medicare Supplement plans is that one can supply health benefits while the other can supply financial coverage.

Medicare Supplement Insurance is a policy that’s added to Original Medicare, Part A and Part B, to provide additional financial coverage. Medicare Advantage is a private plan option that may provide you with other health benefits that Original Medicare does not cover (like dental, vision, fitness programs, etc.).

You cannot have both Medicare Advantage and Medigap at the same time.

Medicare Advantage vs Medicare Supplements | Medicare Plan Finder

A given plan type (e.g., Plan F) has the same benefits regardless of the insurance company that provides the policy, or the state in which you reside. This is not true of Medicare Advantage plans, however, because coverage details may vary by plan.

Excluding prescription drug coverage, any standard Medigap plan with Part A and B will have more benefits than a standard Medicare Advantage plan. However, as mentioned above, some Medicare Advantage plans offer benefits beyond those found in Part A and Part B.

Some Medicare Advantage plans offer prescription drug coverage (often for an additional monthly cost). With a Medigap plan, in contrast, you would need to enroll in a separate prescription drug plan. When comparing plan options, consider your costs for drug coverage. In some cases, Medigap with a stand-alone prescription drug plan has lower total costs than a Medicare Advantage plan with drug coverage. In other cases, the reverse might be true.

[Tweet “Do your research! Comparing #Medicare Advantage vs Medicare Supplement”]

Real-Life Examples: Medicare Advantage vs. Medicare Supplements

Let’s take a look at some real-life examples to help you decide whether Medicare Advantage or Medicare Supplements are right for you.

If you have Medicare Parts A (hospital coverage), B (medical coverage), and D (prescription coverage) and you are hospitalized for cancer treatments for 90 days, you may have out of pocket costs. The Part A deductible means you would pay well over $1,000 first. Once you meet your deductible, your costs will go down. However, after day 60, you’ll be responsible for a portion of every day that you stay there.

If you have Medigap Plan B, your deductible and many of your other hospital costs will be covered. This plan would be in addition to your Part B coverage, so it would all work together to provide extra coverage.

If you have Medicare Advantage, you may have additional health benefits. You’d still likely be responsible for some of those out-of-pocket hospital costs, but your plan might provide a home healthcare benefit, meaning you can get a private in-home nurse when you are released from the hospital. You might also have coverage for medical equipment, such as bathroom safety equipment or a walker.

Comparison is key: Medicare Advantage vs. Medicare Supplements

When choosing between a Medigap plan and a Medicare Advantage plan, take the time to do your research. Read the benefit descriptions of every Medigap and Medicare Advantage plan you are considering. Be certain to look at:

Monthly premium

Deductibles

Doctor and healthcare facility restrictions

Benefits

Anticipated plan costs given your typical use of health-care and hospitalization services

Prescription drug coverage cost sharing as it relates to your medication usage

In the end, your decision is going to be the one that you feel the most comfortable with. The challenge is often wading through all the material to get to the bottom line. Want to make that a little easier? Give us a call at 844-431-1832.

This post was originally published on October 23, 2018, and was last updated on August 29, 2019.