Hematologic Diseases & Common Blood Disorders in the Elderly

Blood has a number of important functions that include supplying your cells with oxygen and nutrients, fighting off infection, and removing waste such as carbon dioxide and lactic acid.

Hematologic diseases or blood disorders can impact your blood’s ability to function like it should. As you age, common blood disorders such as anemia and blood cancers may become more likely.

If you are age 65 and older, have ALS or ESRD, or have been receiving Social Security Disability Income for at least 25 months, you may be eligible for Medicare insurance. Medicare may cover some treatments and testing for common blood disorders.

List of Common Blood Disorders in the Elderly

As you age, you may become more susceptible to blood disorders. Common blood disorders in the elderly range from conditions that can be treated with diet and supplements to chronic diseases. The most common blood disorders include:

Anemia

Blood clots

Hemophilia

Leukemia

Lymphoma

Myeloma

Medicare Chronic Special Needs Plans for Blood Disorders

Original Medicare (Part A and Part B) may cover certain medical services for blood disorders. Medicare Part A is hospital insurance, and it can cover inpatient services such as surgeries that take place in the hospital. Medicare Part B is medical insurance, and it can cover outpatient services such as doctor visits and treatment, and emergency transportation.

For the most part, Original Medicare does not cover prescription drugs you take at home. Prescription drug coverage falls under Medicare Part D or certain Medicare Advantage plans.

Medicare Advantage plans are private health insurance plans that can offer supplemental benefits that Original Medicare does not such as prescription drug coverage, non-emergency medical transportation, and meal delivery.

Some chronic blood diseases may qualify you for a special type of Medicare Advantage plan called a Chronic Special Needs Plan (CSNP).

If you’re eligible for a CSNP, you may also qualify for a Special Enrollment Period (SEP) that allows you to make changes to your coverage as your medical needs change. Most people on Medicare have to wait for certain times of year to make changes.

With many CSNPs, you get coordination of care between multiple providers to ensure that your medical needs are met.. For example, a CSNP for leukemia, a type of blood cancer, may help pay for treatment by a blood specialist called a hematologist and/or a cancer specialist called an oncologist. Other team members may include surgeons and oncology nurses.

Another coverage option is a Medicare Supplement (Medigap) plan. Medigap plans can help cover certain fees associated with Original Medicare such as Part A and Part B coinsurance and copays, but they don’t usually include additional health benefits.

You cannot have both Medicare Advantage and Medicare Supplements. A licensed insurance agent can be an important resource for deciding which type of plan would best suit your needs.

Anemia in the Elderly

Anemia is a condition that happens when you have a lack of healthy red blood cells or a lack of hemoglobin (a main component of red blood cells). It can be caused by blood loss, decreased red blood cell production, and/or destruction of red blood cells. Symptoms include:

Dizziness

Fast or unusual heartbeat

Headache

Pain in your bones, chest, belly, and/or joints

Shortness of breath

Pale or yellow skin

Swollen or cold hands and feet

Feeling tired or weak

Vision problems

Medicare Coverage for Anemia

Medicare may cover a specific type of screening called a blood count for anemia if your doctor recommends one. The blood count can determine how much hemoglobin, white blood cells, and platelets your body has.

Medicare coverage for anemia treatment depends on the treatment. For example, a vitamin B12 deficiency can cause certain types of anemia, and they can be treated with oral vitamins and supplements. Neither Original Medicare nor Medicare Part D covers over-the-counter (OTC) vitamin supplements, however, some Medicare Advantage plans have an OTC benefit.

Original Medicare will help pay for vitamin B12 injections for certain types of anemia, as long as the injections are “reasonable and necessary to the treatment” of your hematologic disorder.

If your anemia is due to an iron deficiency, your doctor may recommend OTC supplements and/or changes to your diet.

If your body can’t produce enough red blood cells, your doctor may recommend blood transfusions as part of your anemia treatment. In that case, Medicare may help cover blood transfusions. You may have to pay coinsurance, copays, or deductibles depending on your plan and how your healthcare facility gets the blood.

Sometimes underlying chronic diseases such as cancer, kidney disease, and HIV/AIDS can cause anemia. In those cases, your treatment will depend on your condition and what your doctor recommends.

Blood Cancer

The most common types of blood cancer include leukemia, lymphoma, and myeloma.

Leukemia

Leukemia is cancer of the tissues that form blood, such as bone marrow and the lymphatic system. The cancer forms when mutated genes form in your DNA. According to the Mayo Clinic, symptoms include:

Fever or chills

Persistent fatigue, weakness

Frequent or severe infections

Losing weight without trying

Swollen lymph nodes, enlarged liver or spleen

Bleeding or bruising easily

Frequent nosebleeds

Tiny red spots on your skin

Excessive sweating, especially at night

Pain in your bones

Lymphoma

According to the Mayo Clinic, lymphoma is a blood cancer that occurs in the lymphatic system — part of the body’s “germ-fighting network.” Lymphoma has two main subtypes, which are Hodgkin’s and non-Hodgkin’s. Symptoms include:

Painless swelling of the lymph nodes in your neck, armpits, or groin

Chronic fatigue

Night sweats

Shortness of breath

Unintentional weight loss

Itchy skin

Myeloma

Myeloma is a cancer that forms in a type of white blood cell called a plasma cell. Your plasma cells help fight infection by making antibodies that attack germs. The cancer forms in your bone marrow, where the cancer cells can eventually outnumber healthy plasma cells. When that happens, your plasma cells can no longer produce antibodies. The cancer cells begin to produce proteins that can cause serious complications. Symptoms include:

Bone pain, especially in your spine or chest

Nausea

Constipation

Loss of appetite

Mental fogginess or confusion

Fatigue

Frequent infections

Unexplained weight loss

Weakness or numbness in your legs

Excessive thirst

Medicare Coverage for Blood Cancer

Your healthcare providers will create and execute your treatment plan depending on your type of blood cancer.

Medicare may cover diagnostic testing and screenings or blood cancer. Part B may cover treatments including outpatient radiation and intravenous chemotherapy. Medicare Part B may also cover CAR T-cell therapy for leukemia and lymphoma. Part A may cover hospital stays and inpatient surgeries as well as limited home healthcare services and skilled nursing care.

Medicare Part D may cover oral chemotherapy medications, painkillers, and/or anti-nausea drugs.

If you have blood cancer, you may qualify for a CSNP. After your initial diagnosis, you have 30 days to enroll in new coverage. If you need help selecting a CSNP*, talk to your agent. If you have a CSNP, your SEP will allow you to change your coverage as you need to. Your agent may be a valuable resource for finding the right plans.

*CSNPs may not be available in every location.

Hemophilia

Hemophilia is a hematologic disorder in which the blood can’t easily clot. If you have hemophilia, even a slight injury can cause severe bleeding. According to the Centers for Disease Control and Prevention (CDC), hemophilia is caused by a mutation in the gene that provides clotting instructions. The mutation can stop the “clotting protein from working properly.” Hemophilia can result in:

Bleeding in the joints that can lead to joint pain and disease

Bleeding in the brain which can cause long-term issues including paralysis and seizures

Bleeding in vital organs which can lead to death if the issue is severe

Medicare Coverage for Hemophilia

According to the National Hemophilia Foundation, Medicare Part B helps cover “clotting factors,” which are concentrated forms of clotting proteins. The CDC separates clotting factor products into two groups: plasma-derived and recombinant. Plasma-derived products come from donors. The clotting factors are separated from the blood plasma, tested for viruses, and freeze-dried. Recombinant products are genetically engineered in a laboratory. They do not contain any plasma or albumin.

Blood Clots

If you get a cut or scrape, blood cells called platelets and certain clotting proteins in your plasma work together to create clot over the injury. Usually, your body will dissolve the blood clot after you’ve healed. According to the American Society of Hematology, sometimes clots do not dissolve naturally, or they form on the inside of blood vessels without an injury.

Blood clots may be extremely dangerous. For example, blood clots in the brain can lead to a stroke, clots in the coronary artery can cause a heart attack, and clots in the pulmonary artery can cause pulmonary embolisms.

According to Medical News Today, the legs are the most common place for a blood clot to develop. Symptoms of a clot in the leg may include:

Pain

Swelling

A feeling of warmth

Tenderness

Redness

Pain in your calf when you stretch your toes upward

Medicare Coverage for Blood Clots

Medicare covers medically necessary diagnostic tests such as pulmonary angiograms or ultrasounds to look for blood clots.

Treatment for blood clots may include prescription anticoagulants (blood thinners). Medicare Part D or certain Medicare Advantage plans may cover blood thinners such as Xarelto.

Get Coverage for Common Blood Disorders Today

If you need coverage for the most common blood disorders in the elderly, a licensed agent with Medicare Plan Finder may be able to help. Our agents can see what plans are available in your area and help you decide which one works best for your needs, whether you need a CSNP, Medicare Advantage plan, or a Medicare Part D plan. To arrange a meeting with an agent, call 1-844-431-1832 or contact us here now.

7 Fad Diets That Work for Seniors

It may seem like you hear about a different celebrity toting a new diet every time you turn the TV on. Some people say that eating lots of protein and cutting carbs is the way to go. Other people say to keep the bread and pasta in your diet and to not eat dietary fat.

The diets on this list may be considered fad diets, however, they are diets that work*. Experts in health and nutrition created and reviewed these diets, and they may offer overall health benefits along with additional support for specific health conditions such as dementia, heart disease, and diabetes.

*Always check with your doctor before starting any diet or exercise program.

1. Mediterranean Diet

According to US News, the Mediterranean Diet is the best diet for overall health, heart health, and diabetes management. The people who live around the Mediterranean Sea “live longer and suffer less than most Americans from cancer and cardiovascular ailments.”

The diet itself “is more of an eating pattern than a structured diet.” In other words, you’re “on your own to figure out how much to eat to lose or maintain weight.” With the Mediterranean Diet, you focus on fruits, vegetables, legumes, whole grains, and nuts.

You should also have fish “at least a couple of times a week,” and eat poultry, eggs, cheese, and yogurt “sparingly.” The diet does not prohibit sweets and red meat, but it does encourage you to eat them only on special occasions.

2. DASH Diet

DASH stands for Dietary Approaches to Stop Hypertension. The diet is promoted by the National Heart, Lung, and Blood Institute to stop or prevent high blood pressure. DASH ranks third in the “Best Heart-Healthy Diet” category.

The diet focuses on lean protein, fruits, vegetables, and low-fat dairy in an attempt to help manage blood pressure, because these foods contain nutrients such as potassium, calcium, fiber, and protein. All of these nutrients have been shown to “deflate blood pressure.”

DASH also recommends limiting sodium to 2300 mgs a day.

According to US News, the diet works because it’s easy to follow long-term.The DASH diet recommends making small changes such as:

Adding one vegetable or fruit serving to each meal

Introducing two or more meatless meals per week

Using herbs and spices rather than salt to flavor food

Snacking on almonds or pecans instead of chips

Swapping whole wheat flour for white flour whenever you can

Taking a 15-minute walk after lunch or dinner (or both)

DASH, according to US News, can be used as a weight loss diet if you burn more calories than you take in.

3. Flexitarian Diet

“Flexitarian” is a combination of two words — flexible and vegetarian. The term basically means that you’re a vegetarian most of the time, but you can eat meat when the urge hits. The diet is based on a book called The Flexitarian Diet: The Mostly Vegetarian Way to Lose Weight, Be Healthier, Prevent Disease and Add Years to Your Life, by Dawn Jackson Blatner, a registered dietician.

The idea is that if you consume more vegetables than meat, you can lose weight and improve your overall health. The US News panel of experts agree, because the Flexitarian Diet ranks third for the “Best Diets Overall,” “Best Diets for Weight Loss,” “Best Diets for Healthy Eating,” and “Best Weight Loss Diets.”

According to US News, the diet is easy to follow. The diet emphasizes plant-based protein (beans, peas, lentils), eggs, dairy, fruits, vegetables and whole grains. Blatner’s book offers a customizable meal plan that includes two snacks. If you follow the plan, you’ll consume about 1500 calories a day.

You can adjust your food intake as necessary for weight loss or maintenance. How much you consume depends on your age, weight, height, and activity level.

4. MIND Diet

The MIND Diet is designed to help promote brain health. Note: There is no guaranteed way to prevent Alzheimer’s, but eating leafy greens, nuts, and berries may lower your risk of developing the progressive brain disorder.

MIND stands for Mediterranean-DASH Intervention for Neurodegenerative Delay, and it’s a mixture of the DASH and Mediterranean diets. The diet was developed by Martha Clare Morris, a nutritional epidemiologist at Rush University Medical Center.

If you follow the MIND Diet, you’ll eat at least three servings of whole grains, a salad, and one more vegetable. You also get a glass of wine, which is good for brain health, according to Morris.

You’ll snack on nuts most days, and every other day you should eat half a cup of beans. You’re supposed to include poultry and blueberries twice a week, and fish once a week. When you cook at home, you should use olive oil instead of other cooking oils.

5. Volumetrics Diet

This diet was created by Barbara Rolls, a nutrition professor at Penn State University. Like the Mediterranean Diet, Volumetrics is an approach to eating, rather than a structured diet.

Volumetrics groups foods by energy density. Basically, the lower a food’s energy density, the more likely it is to fight off hunger.

For example, non-starchy fruits and vegetables, and broth-based soups have a very low energy density because they’re mostly water. Those foods are in Category One.

Low-density (Category Two) is the next step up. Those foods include starchy fruits and vegetables, whole grains, and low-fat meat.

Medium-density (Category Three) foods include meat, cheese, pizza, ice cream, pretzels, and cake.

High-density foods make up Category Four, and they include chips, chocolate candy, cookies, butter, and crackers.

To follow the diet, you’ll use Rolls’ book to categorize your food choices. You’re supposed to focus mainly on Category One and Two foods, keep Category Three portions small, and eat Category Four foods rarely.

Volumetrics can help you lose weight if you stay in a caloric deficit, which may be easy to do if you eat mainly filling, low-calorie foods.

6. Mayo Clinic Diet

The Mayo Clinic Diet is designed to promote “weight loss and a healthy lifestyle.” The diet uses the Mayo Clinic’s “unique food pyramid” that emphasizes fruits, vegetables, and whole grains.

The diet works on some of the same principles as the Volumetrics Diet by focusing on foods with low energy densities. For example, two cups of broccoli has the same amount of calories as one quarter of a Snickers bar.

The Mayo Clinic Diet is effective for weight loss. According to the Mayo Clinic, you can lose “6-10 pounds in two weeks, and continue losing 1-2 pounds each week until you hit your goal weight.” You do this by adding a healthy breakfast, fruits, vegetables, whole grains, healthy fats, and at least 30 minutes of physical activity every day.

7. TLC Diet

In the diet’s case, “TLC” stands for Therapeutic Lifestyle Changes. The National Institute of Health’s National Cholesterol Education Program created the diet with the goal of cutting cholesterol for heart health. It focuses on vegetables, fruits, bread, whole grains, pasta, and lean meat.

If you want to lower your LDL (bad cholesterol) level, men are supposed to eat 2,500 calories a day, and women are to eat 1,800. If you also want to lose weight, men are to eat 1,600 calories a day, and women are supposed to aim for 1,200 calories a day.*

Then you’re supposed to limit saturated fat to less than seven percent of your daily calories. If you do that and our LDL level hasn’t dropped by 8-10 percent, then add “two grams of plant stanols or sterols and 10-25 grams of soluble fiber every day.” You can find stanols and sterols in vegetable oils.

Other daily guidelines include:

Keeping meat to a maximum of five ounces per day, and sticking to skinless poultry and fish

Eating 2-3 servings of low-fat or nonfat dairy products

Loading up on fruits and vegetables — up to four servings of fruit and 3-5 servings of vegetables daily

Eating 11 servings of bread, cereal, rice, pasta, or other grains

*The exact appropriate number of calories to eat may differ for each individual person. Speak to a doctor before beginning a new diet.

Healthy Choices for Your Overall Health

The above diets may be a great starting point for getting or staying healthy. Go to your doctor with specific questions about diet and exercise, and check out our blog for information about Medicare. To learn more about Medicare Advantage and/or Medicare Supplements, call 844-431-1832 or contact us here to arrange a meeting with a licensed agent.

Ultimate Guide to Railroad Retirement Medicare Benefits

According to the US Railroad Retirement Board, more than 500 thousand people receive railroad retirement benefits, which include “retirement, survivor, unemployment, and sickness insurance benefits for railroad workers and their families.”

Many railroad retirees can also receive Medicare health insurance benefits. Railroad Retirement Medicare benefits work much the same way as regular Medicare benefits. The difference lies in what organization administers the benefits. The Railroad Retirement board administers railroad Medicare benefits for most eligible people, and the Social Security Administration administers regular Medicare benefits.

Who Is Eligible for Railroad Retirement Benefits and Medicare?

Railroad Retirement benefits do not include health insurance, but many retirees are also eligible for Medicare. Each program has different eligibility requirements.

According to Union Pacific, one of the major railroad companies in the United States, the earliest that Railroad Retirement benefits begin is “either age 60 with 30 years of qualifying service, or age 62.”

If you have less than 30 years of service, you must wait until full retirement age to receive full benefits. You may be eligible for reduced benefits if you’re at least 62, but haven’t reached full retirement age, which ranges from 65-67 depending on when you were born. For example, full retirement age is 67 for anyone born after 1960.A

Another way you can qualify for Railroad Retirement Board benefits is through disability insurance. You must have at least 10 years of service to qualify for RRB disability insurance.

Medicare Eligibility Requirements

Many people are eligible for Railroad Retirement Board Medicare benefits when they turn 65. You can also qualify if you have ALS, ESRD*, or SSDI**.

If you are already receiving Railroad Retirement or Social Security benefits when you turn 65, you’ll automatically be enrolled. You’ll receive information about it a few months before your birthday. You will “have the option of turning Part B coverage down” because you have to pay a monthly premium for Part B.

*The Social Security Administration handles benefits for enrollees with ESRD.

**Must have had SSDI for at least 24 months to qualify.

What Does Medicare Cover?

Original Medicare (Parts A and B) covers many medical expenses, but it doesn’t cover everything. Here’s a breakdown of what Medicare covers:

Medicare Part A

Medicare Part A covers inpatient care, skilled nursing facility care, hospice, and home health services. You may be responsible for copays, coinsurance, and/or deductibles.

Medicare Part B

Medicare Part B helps pay for outpatient care including doctor’s appointments and preventive services. Part B also helps pay for emergency medical transportation, durable medical equipment (DME), mental health services, and partial hospitalization. You may be responsible for paying deductibles, copays, coinsurance, and/or monthly premiums.

Medicare Part C (Medicare Advantage)

Medicare Part C, or Medicare Advantage plans are private insurance policies that can offer additional benefits to Original Medicare. Those supplemental benefits can include hearing, vision, dental, meal delivery, and even fitness classes. Some Medicare Advantage plans offer prescription drug benefits.

Medicare Part D

Another way to get prescription drug coverage is through a standalone Medicare Part D plan. You may be responsible for premiums, copays, coinsurance, and/or deductibles with a Part D plan.

What Is a Railroad Retirement Medicare Supplement?

It’s important to understand the difference between Medigap and Medicare Advantage because you can’t have both types of plans. While Medicare Advantage plans cover additional health benefits, Medicare Supplement (Medigap) plans cover financial items such as copays and coinsurance.

Medigap plans offer eight different levels of coverage in 2020, and each level is assigned a letter. Note: People who enrolled prior to 2020 might have Plan C or Plan F. Plans that cover the Part B deductible (like Plan C and Plan F) will not be available to anyone newly eligible for Medicare in 2020.

Learn More About Railroad Medicare Benefits

If you need help finding the right Medicare plan, a licensed agent with Medicare Plan Finder may be able to help. Every location has different plans, and it may be difficult to determine what plan would work best. Our agents are highly trained and they can help you determine what kind of plan you need for additional coverage — Part D, Medicare Advantage, or Medigap. Call 844-431-1832 or contact us here to set up a no-cost, no-obligation appointment today.

A Guide to Medicare Insulin Coverage

According to the Kaiser Family Foundation (KFF), a non profit healthcare organization, Medicare Part D (prescription drug) spending increased from $1.4 billion to $13.3 billion from 2007 to 2017.

The huge increase in drug costs ultimately gets passed to the consumer. KFF also said that insulin out-of-pocket costs have “quadrupled.” That may be the case, but Medicare insulin coverage may help lower costs if you qualify.

How Does Medicare Insulin Coverage Work?

Original Medicare is the public health insurance that helps beneficiaries pay for medical expenses. It does not cover prescription drugs, with one exception — insulin.

However, Medicare insulin coverage is limited. Medicare Part B (medical insurance) only covers insulin if it’s administered with an insulin pump. The pump is considered to be durable medical equipment (DME), which Medicare helps cover when medically necessary.

That means that while Original Medicare may help pay for insulin pumps, diabetes screening/treatment, and even orthotics for diabetics, Original Medicare does not cover insulin by itself.

If you’re eligible for Medicare and want insulin coverage, you have two options. One option is through a Medicare Part D plan that only helps cover drugs. The other option is through a private insurance plan called a Medicare Advantage Prescription Drug (MAPD) plan.

Many Part D and MAPD plans use a formulary to determine how much you pay at the pharmacy. A formulary is a list of the drugs your plan covers. The list divides prescriptions into tiers. Each tier has a different copay or coinsurance amount. According to GoodRx, Lantus, the most popular insulin has “a copay of $37.50-$67.50.” That’s a significant savings when you consider that the estimated Walmart pharmacy retail price is $507.

How Can I Get Insulin at a Lower Price?

If you have a limited income, you may be able to receive help for Part D premiums and drug costs with a Low Income Subsidy (LIS), also called Extra Help. LIS eligibility is based on your income, assets, and the Federal Poverty Level. According to the Social Security Administration (SSA), Extra Help can save you almost $5 thousand per year. If you’re eligible for LIS, you won’t pay more than $8.50 for covered name brand drugs or $3.40 for covered generic prescription drugs.

If you qualify for LIS, you may also qualify for Medicaid. If you qualify for both Medicare and Medicaid, you may qualify for a Medicare Advantage plan called a Dual Special Needs Plan (DSNP). Many DSNPs offer prescription drug coverage with low copays. DSNPs may also offer additional benefits such as fitness classes, vision coverage, and meal delivery.

If you have LIS or a DSNP, you are eligible for a Special Enrollment Period (SEP), which allows you to enroll in new coverage or change existing plans at different parts of the year.

Many people have to wait until the Annual Enrollment Period (AEP), which is from October 15 to December 7 to make changes. With a LIS or DSNP SEP, you can make one change per quarter from January to September. Those changes will take effect on the first of the month following your change. You can make changes during AEP as well, however, those changes won’t take effect until January 1 the following year.

SEPs can be long-term or temporary. For example, in the case of a DSNP, you have a SEP for as long as you qualify for both Medicare and Medicaid. If you gain or lose Medicaid coverage, you have a temporary SEP, which allows you 30 days to enroll in a new plan.

To illustrate how a DSNP SEP works, let’s take the hypothetical example of a 70-year-old man who’s recently qualified for Medicaid. In this example, it’s January 12 and the man qualified on the 10th. The man has until February 9 to enroll in a DSNP. Let’s say he enrolls on February 9. The new coverage will take effect on March 1.

If the man decides he’s not satisfied with his new plan, he can make one change on April 1, which is the start of the second quarter of the year. The man won’t be allowed to make any more changes until July 1. He won’t be allowed to make any changes after September 30 with his DSNP SEP.

Why Is Insulin So Expensive?

According to NPR, many different factors affect insulin’s price. The most important factor is that there’s no generic equivalent to insulin.

With many drugs, other manufacturers cannot legally create generic versions because of patent laws

Once a patent expires, manufacturers have license to create generic versions of brand-name drugs. Generic drugs are often much cheaper than their name brand counterparts. According to the World Health Organization, current insulin patents won’t expire until 2030.

What Is Insulin?

Insulin is a hormone produced in the pancreas that regulates blood sugar. Your body will store glucose in your liver if there’s more sugar than it needs. Insulin will trigger your body to release that sugar when you need it.

If your blood sugar is too high, you can develop diabetes, which is when your body can’t use insulin efficiently or make its own insulin. Type 1 diabetes is when the pancreas can’t make insulin. Type 2 diabetes is when the pancreas makes insulin, but the body doesn’t respond well to it.

The drug insulin dates back to the early 1920s. Researchers conducted a clinical trial with diabetes patients. The trial used insulin from cattle pancreases, and “most patients recovered.” After the trial, insulin was “produced and sold on a massive scale around the world.” Both type 1 and type 2 diabetes need insulin shots to use glucose from food.

Types of Insulin

According to the American Diabetes Association, there are different types of insulin. The type of insulin your doctor prescribes depends on how quickly it works and how long it lasts. Insulin may have a peak blood-sugar lowering capacity and length of total time it works. Injectable insulin is the most common, and it can be divided into five types:

Rapid-acting insulin: Starts to work about 15 minutes after injection, peaks in about one hour, and continues to work for two to four hours.

Regular or short-acting insulin: Typically reaches the bloodstream within half an hour of injection, peaks anywhere from two to three hours after injection, and is effective for approximately three to six hours.

Intermediate-acting insulin: Usually reaches the bloodstream about two to four hours after injection, peaks four to 12 hours later, and is effective for about 12 to 18 hours.

Long-acting insulin: Reaches the bloodstream several hours after injection and can lower glucose levels for 24 hours or longer.

Ultra long-acting insulin: Reaches the bloodstream in six hours, does not peak, and lasts about 36 hours.

Another way to take insulin is inhaled insulin. According to the American Diabetes Association, it begins working in 12-15 minutes, peaks by about 30 minutes, and leaves the body in about three hours.

No matter what type of insulin your doctor prescribes, be sure to follow the instructions for taking and storing the insulin. For example, all insulin comes in liquid form. You may have to refrigerate insulin so it doesn’t expire too soon.

Get Medicare Coverage for Insulin

If you need insulin coverage, a licensed agent with Medicare Plan Finder may be able to help. Our agents are highly trained. They can find what Part D and/or Medicare Advantage plans are in your area, and they can even help you apply for LIS. To set up a no-cost, no-obligation appointment call 844-431-1832 or contact us here today.

Medicare Coverage for Diagnostic Colonoscopy

A colonoscopy is a test that uses a small camera to scan your entire colon to detect disease before it becomes a catastrophic health issue.

Colorectal cancer, also called colon cancer, is the third most common cancer among adults in the United States, according to the Centers for Disease Control.

Does Medicare Cover Colonoscopy?

Medicare can cover some or all of the costs surrounding your colonoscopy. How much you pay depends on what the test finds and whether the test is considered to be a screening colonoscopy or a diagnostic colonoscopy.

Screening Colonoscopies

Medicare Part B covers preventive screenings, tests, and x-rays, including screening colonoscopies. Original Medicare covers screening colonoscopies in full if your doctor or health care provider agrees to perform the test. The coverage you get depends on your risk for developing cancer.

If you have a high risk for developing colon cancer, you get coverage for:

One screening colonoscopy every two years

If you have an average risk of developing colon cancer, you get coverage for:

One screening colonoscopy every 10 years

Or one screening colonoscopy four years after a flexible sigmoidoscopy (a similar test to a colonoscopy, however, it only examines the lower part of the colon

Diagnostic Colonoscopies

If the screening colonoscopy reveals a polyp or other cancer tissue and your doctor removes it, then the test becomes a diagnostic colonoscopy.

Medicare coverage for a diagnostic colonoscopy differs from a screening colonoscopy. You might be responsible for paying 20 percent of the Medicare-approved total cost of the procedure along with the Medicare Part B deductible, which is $185 in 2019.

Does Medicare Pay for Colonoscopy Anesthesia?

How much you’ll pay for anesthesia depends on whether your colonoscopy is for screening or diagnostic purposes. Medicare coverage for diagnostic colonoscopy anesthesia comes with both a 20 percent coinsurance fee and the Part B deductible. S

ince a screening colonoscopy is considered preventive care, Medicare waives any coinsurance fees and the Part B deductible that normally goes with anesthesia.

Does Medicare Cover Virtual Colonoscopy?

A virtual colonoscopy (CT colonoscopy) uses a computer rather than a camera to scan the large intestine. According to the American Cancer Society, Medicare “does not cover virtual colonoscopies at this time.”

What Other Colon Cancer Tests Does Medicare Cover?

Sometimes people will use other tests to screen for colon cancer. Medicare will cover the following preventive screening tests if you’re 50 or older:

Cologuard (stool DNA test): Once every three years for people ages 50 to 85 who do not display colon cancer symptoms and who have an average risk of colorectal cancer. A stool DNA test can show altered DNA and/or blood in the sample, and those results may mean you have cancer.

Fecal Occult Blood Test (FOBT) or Fecal Immunochemical Test (FIT): For people 50 and older once per year. The FOBT or FIT is a lab test that checks stool samples for occult (hidden) blood. The hidden blood may signify that the colon has polyps or cancer.

Screening Barium Enema: An X-ray that involves using a white liquid called barium to enhanced photos of the colon.

Your doctor may order a diagnostic colonoscopy if any of the above tests yield abnormal results. The diagnostic colonoscopy costs will apply.

Medicare Genetic Testing for Colon Cancer

Some people are more likely to develop cancer than others. The BRCA1 and BRCA2 gene mutations indicate a higher likelihood of developing cancer and passing the disease on to your children.

Medicare will pay for genetic testing for colon cancer if the test is medically necessary. In order for Medicare to pay for your genetic testing, you must have a high risk for developing the disease and have a personal history of cancer.

What Does Medicare Consider High Risk for Colon Cancer?

The Centers for Medicare and Medicaid Services (CMS) consider people to be high-risk if they have or have had any of the following:

A personal or family history of colon cancer

A personal history of inflammatory bowel disease such as Crohn’s Disease

A sibling, parent or child who’s had colon cancer or an adenomatous polyp

A personal or family history of adenomatous polyposis

A colon cancer diagnosis qualifies you for the Special Enrollment Period (SEP), which means you won’t have to wait for certain times of the year to change your coverage or enroll in new coverage. The SEP allows you to add or remove coverage as your needs change.

Find Medicare Coverage for Diagnostic Colonoscopy

Getting Medicare coverage for a screening or diagnostic colonoscopy might be a huge factor in finding colon cancer before it’s too late. If you need quality health insurance, Medicare Plan Finder can help. Call us at 844-431-1832 or fill out this form today.

Contact Us | Medicare Plan Finder

This post was originally published on May 2, 2019, and updated on October 28, 2019.

Does Medicare Pay for Assisted Living or Nursing Homes?

Aging can bring up concerns about long-term care for many people, especially if there’s nobody at home to help out. You may wonder about nursing homes or assisted living facilities and how you’ll pay for it when the time comes. If you have Medicare, you may want to know, “Does Medicare pay for assisted living or nursing homes?”

How Much Does Medicare Pay for Assisted Living or Nursing Homes?

Nursing home care can be extremely expensive. According to Genworth, a private room in a nursing home costs an average of $8,517 a month, and assisted living facilities cost an average of $4,051 a month.

Original Medicare –– the public health insurance created in 1965 for retirees –– helps pay for a variety of healthcare costs, but nursing home care itself is not one of them. Custodial care doesn’t fall under Medicare’s guidelines for medical coverage. However, Medicare can help pay for medical expenses during a nursing home stay.

Medicare Part A (hospital insurance) covers up to 100 days at a skilled nursing facility. According to the Medicare Rights Center, “Medicare will not cover the cost of your stay if you need additional days,” or if you need long-term care in an assisted living facility. Part A also covers hospice care. Medicare does not cover room and board at nursing homes or hospice facilities with the exception of short-term stays or respite care.

Original Medicare is divided into two parts: Part A and Part B. Medicare Part A covers inpatient hospital stays. Medicare Part B (medical insurance) helps pay for emergency ambulance transportation. Part B also helps cover doctor appointments.

Original Medicare does not cover prescription drugs. However, you have a couple of different options if you want coverage for prescription medications. You can purchase a Medicare Part D plan, which is only prescription drug coverage, or a Medicare Advantage Prescription Drug (MAPD) plan.

Medicare Advantage plans are private insurance policies that can offer additional benefits to Original Medicare such as meal delivery, non-emergency medical transportation, dental, hearing, and vision coverage.

If you’re at a nursing home for 90 days and have a medical need to stay longer, you may qualify for a Medicare Advantage plan called an Institutionalized Special Needs Plan (ISNP). These plans are designed to cover the specific healthcare needs of someone who requires institutional care including prescription drugs. If you qualify for an ISNP, you may have a Special Enrollment Period (SEP) which allows you to enroll in new coverage or make changes to your insurance plan much more often than those who do not qualify for a SEP.

Click here to read about SEPs and when you can make changes.

What’s the Difference Between a Nursing Home and Assisted Living?

Nursing homes and assisted living centers both provide personal care. The difference is the type of setting. Nursing homes provide medical and personal care in a clinical setting. Assisted living centers offer a more home-like, social setting.

Some people need the clinical setting of a nursing home because of their health condition. For example, someone who cannot walk on his own and requires daily medical care may fair better in a nursing home. Someone who is fully mobile and only requires intermittent medical care and a watchful eye may be better off in an assisted living center.

How Can I Pay for a Nursing Home?

Medicare does not help pay for room & board in nursing homes or assisted living facilities.

Medicare Supplements are private plans that can help pay for Medicare coinsurance or copays, but they only help pay for what you owe Medicare. Since Medicare doesn’t cover nursing home resident fees, Medicare Supplements don’t help with those costs either.

Some Medicare Advantage plans may offer additional coverage for nursing home or assisted living residences. Plans are different in every county and zip code, so we can’t promise that one is available in your area. However, we can get you in touch with a local licensed agent who can give you that information. Call 844-431-1832 or submit your contact information to have someone call you.

Another option to pay for nursing homes or assisted living facilities is life insurance or long-term care insurance. Some whole life insurance policies allow you to draw from them when you need long-term care at a nursing home.

Does Medicaid Cover Nursing Homes?

Medicaid is a state and federal program that helps people with limited incomes receive healthcare. If you qualify for Medicaid and meet your state’s need requirements for nursing home care, your stay may be covered.

Every state has different criteria for determining eligibility for nursing home care. You must also meet your state’s income standard to qualify for Medicaid. According to the Medicare Rights Center, “Your state may have higher Medicaid income guidelines if you need nursing care, or a spend-down program to help you qualify.”

If you qualify for both Medicare and Medicaid, you may also qualify for a Medicare Advantage plan called a Dual Special Needs Plan (DSNP). With a DSNP, you get coverage for all of the Original Medicare program’s benefits, and you also can get some of the supplemental benefits Medicare Advantage plans can provide, such as prescription drugs, dental, and vision. Some plans may even offer additional nursing home coverage. DSNPs often offer low-cost premiums, copays, and coinsurance.

Like an ISNP, a DSNP means you may have a Special Enrollment Period (SEP), however, with this SEP, you can only make one change per quarter from January to September. Any changes you make within those first three quarters will become effective on the first of the month after you make the change.

You can also make a change during the Annual Enrollment Period (AEP), which is from October 15 to December 7, but your new coverage won’t take effect until January 1 of the following year.

What to Look for in a Nursing Home

Entering a nursing home is a big decision. Write down your medical and budgetary needs. For example, you may need a facility that offers memory care. Your nursing home should be capable of handling your medical needs. You should also feel safe and comfortable in your nursing home.

The Centers for Medicare and Medicaid (CMS) has a five-star quality rating system for nursing homes. The rating system is based on health inspection scores, staff-to-resident ratio, and other quality measures. Be sure to check out a nursing home’s rating before you consider moving in. A one-star facility may not provide the quality of care you deserve, but a four or five-star facility might.

Be sure to ask about the nursing home’s costs. Find out how much you’ll pay every month, and if there are any additional items you may have to pay for such as salon services.

If you’re unsure of what to look for in a nursing home, download our nursing home checklist. The list covers items such as questions you should ask and what you should compare when you look at different facilities.

How to Find Medicare-Certified Nursing Homes

Once you’ve determined your budget and medical needs, you can start looking for nursing homes in your area. Use Medicare.gov’s Nursing Home Compare tool to find local Medicare-certified facilities. Click here to get started.

Enter your zip code in the search bar and click “Search.” We used our home office’s zip code of 37209.

The next page you see will be a list of nursing homes in your area. You can sort the list by different criteria. For demonstration purposes, we’re only sorting the facilities by overall rating from highest to lowest. To do this, click on the down arrow under “Overall Rating.”

After you sort the list by your most important criteria, call different facilities to get an idea of price and bed availability. If a nursing home sounds like a good fit, schedule an appointment to tour the facility with your nursing home checklist in hand. You may want to visit the facility more than once before you commit to it.

List of Medicare/Medicaid-Certified Nursing Homes Near Me

We are working on expanding our research for you. We’ve started putting together lists of nursing homes in certain cities. Don’t see your city yet? Send us a message to request a list of nursing homes available in your city.

If nursing home care isn’t feasible, you may have other options for long-term care. Talk to your family, healthcare provider, a counselor, or a social worker to see what’s available in your area.

According to Medicare.gov, you may have several options including:

Home and community-based services

Accessory Dwelling Units (in-law apartments)

Subsidized senior housing

Continuing Care Retirement Communities (CCRCs)

Group living arrangements

Hospice and respite care

*PACE (Program of All-inclusive Care for the Elderly)

If you need coverage for long-term care, a licensed agent with Medicare Plan Finder may be able to help you find it. Your agent may be able to find long-term care, life insurance, or Medicare Advantage plans that cover nursing home and/or assisted living facilities. To arrange a no-cost, no-obligation appointment, call 844-431-1832or contact us here today.

Halloween Safety Tips: Take the Grandkids Trick or Treating

Kids love Halloween because it means they get to dress up as their favorite characters and eat candy. Grandparents love Halloween because they get to see their grandchildren have the time of their lives — it also means your grandkids might share their peanut butter cups.

Halloween can be a lot of fun, but it can also be dangerous. For example, kids are twice as likely to be hit by a car as they are on any other night of the year. With a little planning and supervision, you and your grandkids can safely enjoy Halloween. Follow these Halloween safety tips for maximum fun and peace of mind.

Safe Trick or Treating Tips

Before you take your grandchildren trick or treating, do the following things to ensure safety:

Explore Familiar Territory: As you age, it can become more difficult to see at night. Set a curfew for your grandkids and plan a route you’re familiar with. Make sure the route is well-lit and that you stay on the sidewalk. Always bring a flashlight with batteries and your cell phone. Walking around the neighborhood with your grandkids to get candy doesn’t only benefit them, it’s also a great way for you to get some exercise in!

Inspect Treats Before You Indulge: It may be hard for your grandchildren to wait until they get home to eat their candy, but they should. Look at their candy before they eat it, and throw away anything that’s already been opened, looks tampered with, or otherwise looks suspicious. If your grandkids are very young, remove any choking hazards such as gum, peanuts, and/or hard candy. If your grandkids have food allergies, carefully read the labels to make sure they’re safe.

Have a Plan in Case You Get Separated: You should try to stay with your grandchildren at all times, of course, but if you do happen to get separated, make sure you have a plan. Give your grandchild a piece of paper with your name and phone number and agree on a meeting spot in case you get separated .

Make Sure Costumes are Safe: Your grandkids should wear bright colors and flame-retardant materials. If it’s dark, add reflective tape to your grandkids’ trick or treat bags or costume. Masks can obstruct your grandchildren’s vision, so nontoxic makeup may be a better choice. Props with points such as swords and wands might pose safety hazards. If it’s chilly, make sure the costume is warm, or, at the very least, loose enough to wear warm clothing underneath (but not lose enough to create a tripping hazard).

Attend Trunk or Treat Events: If your area has them, trunk or treat events are a great way for your grandkids to get candy and for everyone to remain safe. In a trunk or treat event, people park their cars in parking lots, decorate open trunks,, and pass out candy to trick or treaters. These events can be a safer alternative to walking from door to door in neighborhoods.

Pumpkin Carving Safety

Carving jack-o’-lanterns may be a time-honored tradition, but it can lead to injuries if you don’t use safe practices.

Consider Carving Alternatives: Instead of taking a knife to a pumpkin, consider drawing with permanent markers or using puff paint. This tip is especially useful for young children. If you must actually carve a jack-o’-lantern, have an adult handle the knife — no matter how many times your grandkids ask.

Use Caution With Candles: Put candle-lit jack-o’-lanterns away from curtains or anything else that could catch on fire. Never leave pumpkins with candles unattended and be sure to blow out the flame before you leave. Or, instead of using candles, use battery-powered flameless candles, flashlights, or glow sticks.

Safe Trick or Treating at Home

Part of the fun in Halloween trick or treating is passing out candy at your own home. With a little preparation, you can make your home a safe place for trick or treaters to visit.

Remove Clutter: Put away tripping hazards such as garden hoses and bicycles. Be sure to clear leaves, snow, or other debris from your sidewalk.

Light the Area: Not only will lighting your porch, sidewalk, and/or driveway let trick or treaters know that you’re open for business, but good lighting also makes your property safer. Replace any burnt-out lightbulbs to ensure visibility.

Make Sure Your Pets Are Under Control: Don’t take any chances on a scared pet biting or chasing a trick or treater. Make sure your pets are well-behaved or that they’re in another part of the house.

Have a Safe and Happy Halloween!

We hope the above safety tips are useful and that Halloween is great for you and your grandkids. Check out our blog for more safety tips and information about Medicare. If you want to learn more about Medigap and/or Medicare Advantage, you can arrange an appointment with one of our highly trained, licensed agents by calling 844-431-1832 or contacting us here.

What Is a Medicare SELECT Plan?

Medicare is a giant healthcare system that helps eligible people receive medical services. However, it doesn’t cover everything health-related. One tool that people use to afford healthcare is called a Medicare SELECT plan.

What Is Medicare SELECT?

A Medicare SELECT plan is a type of Medicare Supplement (Medigap) plan. Medigap plans are private insurance policies that can help close the gap between your coverage and what you pay. Medicare SELECT plans require you to use a specific network of medical facilities and healthcare providers.

How Does a Medicare SELECT Plan Work?

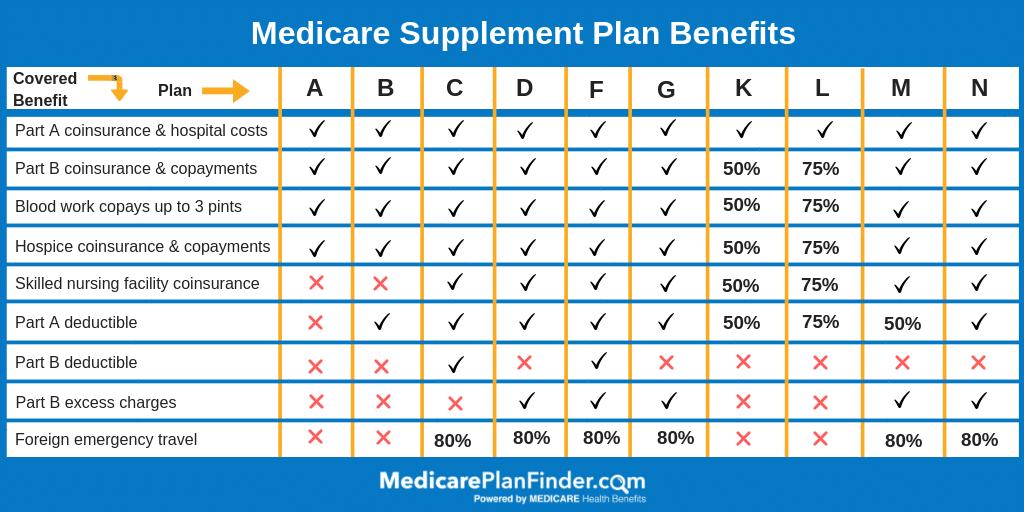

A regular Medicare Supplement plan provides coverage anywhere that accepts Medicare. In 2019, there are 10 standardized Medigap plans you can enroll in. Covered services depend on which “letter” you buy, but each letter offers the same coverage in every state.

Medicare Supplement Plans Comparison Chart

Plans that cover the Medicare Part B deductible (Plan C and Plan F) will not be available to anyone newly eligible for Medicare after January 1, 2020. If you qualify for Medicare and want coverage for those items now, talk to an agent today!

Medicare SELECT policies are different from other Medigap plans because they aren’t accepted everywhere that takes Medicare. Also, Medicare SELECT is different because not all 50 states have plans available.

Medicare SELECT premiums depend on a variety of factors, but because they feature smaller networks than normal Medigap plans, Medicare SELECT premiums may be less.

Is Medicare SELECT Different Than Medicare Advantage?

Medicare SELECT is different than Medicare Advantage because of what the plans cover. Because Medicare SELECT is a type of Medicare Supplement policy, it only covers financial items such as deductibles, coinsurance, and copays.

Like Medigap policies, Medicare Advantage plans are private insurance policies. However, Medicare Advantage plans cover medical services, and they can offer supplemental benefits such as vision, hearing, dental, and fitness classes. You must choose either a Medigap plan or a Medicare Advantage plan. You cannot have both.

Certain Medicare Advantage plans called HMOs are a lot like Medicare SELECT, because they can feature smaller networks of providers than Medicare Advantage PPOs or regular Medigap plans.

When Can I Buy Medicare SELECT?

According to the Medicare Rights Center, the best time to enroll in a Medigap plan is during your Open Enrollment Period (OEP), which is the six months after you’ve enrolled in Medicare Part B.

If you miss your Open Enrollment Period, you can buy a Medigap plan when you have a guaranteed issue right. For example, you have guaranteed issue within “63 days of losing or ending certain kinds of health coverage.”

You may also have a guaranteed issue right if you enrolled in a Medicare Advantage plan when you were first eligible for Medicare and disenrolled within one year. Other circumstances that may allow you to have guaranteed issue are if your private Medicare plan ends coverage or you move out of the plan’s service area.

If you decide a Medicare SELECT or any Medicare Supplement policy isn’t for you, you can cancel within 30 days of starting coverage. However, you should cancel with caution, because you may not be able to buy another policy depending on where you live, and you might get charged more because of your health.

If you buy a Medicare SELECT policy and you don’t like it, you can switch to a standard Medicare Supplement plan within 12 months of your Medicare SELECT policy taking effect.

Learn More About Medicare SELECT

Medicare SELECT plans aren’t available in every state. A licensed agent with Medicare Plan Finder can show you what’s available in your area and help you make a decision. Our agents are highly trained and may be able to find a plan that fits your budget and lifestyle. Call 844-431-1832 or contact us here to set up a no-cost, no-obligation appointment today.

Find Medicare Plans | Medicare Plan Finder

Ultimate Guide to NIA’s Go4Life® Program

According to the US Department of Health and Human Services (HHS), “only 28-34 percent of adults ages 65-74 are physically active.” In an effort to get seniors moving, the National Institute of Aging (NIA) launched the Go4Life® campaign.

What Is Go4Life®?

Go4Life® is exercise and physical activity campaign from the National Institute of Aging at NIH (National Institutes of Health) that’s designed to help people include exercise and physical activity in their daily lives.

According to NIA, the campaign’s “essential elements are motivating older adults to become physically active for the first time, return to exercise after a break in their routines, or build more exercise and physical activity into weekly routines.”

The campaign offers exercise guides, motivational tips, and other free resources such as tracking tools to help you get started with and keep at physical activity.

Go4Life ® Types of Exercise

Go4Life®’s goal is to have people focus on more than one type of exercise. The campaign recommends doing four types of exercise for comprehensive physical fitness*:

Endurance

Strength

Balance

Flexibility

*Always check with your doctor before starting any exercise program.

Endurance

Endurance activities are also called aerobic or cardiovascular exercise.

Benefits of Endurance Training

According to the Mayo Clinic, cardiovascular exercise has many benefits including:

Strengthening your heart and muscles

Burning calories

Helping control your appetite

Boosting your mood through endorphins (feel-good chemicals)

Helping you sleep better at night

Reducing arthritis pain and joint stiffness

Helping prevent or manage high blood pressure, heart disease and diabetes

Endurance Training Exercises

Go4Life® recommends the following endurance exercises:

Mall Walking: Malls provide a safe space for walking that’s free from bad weather and traffic.

Walking or Rolling Exercise: Brisk walking or rolling in a wheelchair around your neighborhood or other outdoor areas can increase your heart rate and breathing.

Exercise Around the House: You don’t even need to leave your home to be active! For example, gardening, sweeping, raking, and shoveling snow are great ways to get your heart rate up.

Outdoor Activities: These activities include cycling, horseback riding, sailing, jogging, skating, snorkeling, and swimming.

Indoor Activities: These activities include indoor lap swimming, using cardio equipment at your local gym, dancing, water aerobics, martial arts, and/or bowling.

Sports: Competition and teamwork can be extremely motivating. Sports such as tennis, pickleball, volleyball, and hockey can be great ways to raise your heart rate and help keep you healthy.

Strength

When many people think of strength training, they think of lifting weights at the gym. While that is one way, you can also get valuable strength training in the comfort of your own home with dumbbells and/or resistance bands.

Benefits of Weight Lifting

According to RunRepeat.com, “long-term lifting is the best way to prevent age-related muscle loss,” and lifting is “even prescribed for the prevention of diseases like osteoporosis.” Other benefits include:

Weight Lifting Routines for Seniors and Medicare Eligibles

Go4Life® suggests gradually increasing the weight you use to build strength. Start with a weight you can lift eight times maximum. Use the same weight until you can easily do 10-15 repetitions.

When you can do two sets of 10-15 repetitions, add more weight. You should only be able to lift the new weight eight times. Then repeat that cycle until you reach your goal. Go4Life® recommends the following strength exercises. You can find exercise instructions here.

Upper Body Exercises

Seated rows with resistance bands

Chair dips

Bicep curls with resistance bands

Wall pushups

Dumbbell bicep curls

Lateral raises with dumbbells

Front raises with dumbbells

Overhead presses with dumbbells

Dumbbell wrist curls

Grip exercise with a tennis ball

Tricep extensions with a dumbbell

Lower Body Exercises

Calf raises using a chair for balance

Standing from a chair

Leg extensions

Leg curls

Lateral leg raises

Back leg raises

Balance

As we age, our sense of balance can change. According to Harvard University, we lose our sense of balance if we aren’t physically active.

Benefits of Balance Training

According to the National Council on Aging (NCOA), about 25 percent of adults over 65 fall every year, and the right exercise program can help seniors prevent falls. It makes sense, too. NIA says that having good balance will help you carry out daily activities such as walking up and down stairs and navigating around objects on the floor.

Balance Exercises to Try at Home

Follow the instructions here to start Go4life®’s balance training routine.

Go4Life recommends doing the following stretches three to five times whenever you exercise. You can do all of these exercises at home using a chair, supporting yourself with a wall, or lying on the floor.

Partner stretch

Standing calf stretch

Lying lower back stretch

Lying hip stretch

Standing thigh stretch

Lying thigh stretch

Seated back of leg stretch

Lying back of leg stretch

Seated ankle stretch

Various seated back stretches

Getting up from a lying position on the floor

Lying down from a seated position

Go4Life® also recommends yoga to help improve your flexibility.

Medicare Fitness Coverage

If you’re eligible for Medicare, you may be able to find coverage for gym memberships and fitness classes. Original Medicare, the public health insurance does not offer a fitness benefit. However, certain private insurance policies called Medicare Advantage plans can cover gym memberships and fitness classes.

Programs such as Silver & Fit® and SilverSneakers® partner with insurance carriers and local gyms to offer beneficiaries discounted memberships. Some insurance carriers even offer their own fitness benefits.

Some Medicare Advantage plans that offer fitness benefits even have $0 monthly premiums*! Plan benefits and availability vary by location, so check with your agent if you have questions about Medicare fitness coverage.

*Even if your Medicare Advantage plan has a $0 premium, you may still owe the Part B premium.

Find Coverage for Medicare Fitness Programs

Go4Life® provides exercise guidance so seniors can get active. If you want to learn about Medicare Advantage fitness coverage, a licensed agent with Medicare Plan Finder can help. Our agents are highly trained and they may be able to help you find a plan that fits your lifestyle and budget. To set up a no-cost, no-obligation appointment, call 844-431-1832 or contact us here today.

Find Medicare Plans | Medicare Plan Finder

Medicare SEP Changes 2020: When You Can Enroll If You’re Eligible for a DSNP or LIS

DSNPs (Dual Special Needs Plans) are Medicare Advantage plans for people who are eligible for both Medicare and Medicaid. LIS (Low Income Subsidy), or Medicare Extra Help is a federal program that helps Medicare beneficiaries save money on prescription drugs.

If you are eligible for either DSNPs or LIS, your enrollment periods might be a bit different from others.

Am I Eligible for LIS?

If you’re eligible for Medicare and you make less than 150 percent of the Federal Poverty Level, you may qualify for LIS. You can also automatically qualify for Extra Help if you’re already on SSI or you qualify for a DSNP.

What Does LIS Cover?

LIS helps qualifying people pay for prescription drugs and it covers items such as Part D premiums, deductibles, and the “Donut Hole”.

LIS coverage is offered on a sliding scale. That means the subsidy provides more or less help depending on your qualifications.

For example, if you’re single and you qualify for full LIS and Medicare only, you’ll pay no more than $3.40 for covered generic drugs and $8.50 for covered brand-name drugs. You will have no copay once you spend $5,000 out-of-pocket for covered prescription drugs.

What are Medicare DSNPs (Dual-Eligible Special Needs Plans)?

DSNPs cover your Original Medicare premiums and services, and, since they’re Medicare Advantage plans, they can offer additional benefits* such as:

Many DSNPs have $0 monthly premiums, and if you see healthcare providers in your plan’s network, you shouldn’t have to pay Medicare deductibles and copays.

*Plan benefits and availability depend on many different factors such as location and carrier. Talk to your licensed agent to learn about available plans and covered services.

What Are the Changes to My SEP?

In the past, if you qualified for a lifelong SEP, you could enroll in a new DSNP, Medicare Advantage, or Part D plan up to once a month for the entire year.

In 2019 and 2020, if you’re eligible for a DSNP, LIS, or you only qualify for Medicare Savings Programs (MSPs) such as the Qualified Medicare Beneficiary (QMB) program or the Specified Low-Income Medicare Beneficiary (SLMB) program, the 2019-2020 CMS guidelines state that you can enroll in a new plan or drop coverage once per quarter for the first three quarters of the year (January – September).

Any changes you make during this time will become effective on the first of the month following the date you made the change. For example, if you enroll in a new DSNP plan on February 10, that change will become effective on March 1. You would not be able to make another change until the next quarter.

Q1: January – March

Q2: April – June

Q3: July – September

Q4: October – December

So, what does that mean for the rest of the year? Well, it means that you’ll fall into the AEP like everyone else.

The Annual Enrollment Period (AEP), which is October 15 to December 7, is a time when anyone can make changes to their existing Medicare coverage. Any AEP changes will take effect on January 1 of the following year. For example, if you make a change during AEP on November 15, that change will become effective on January 1.

Get the Medicare Health Insurance You Need Today

A licensed agent with Medicare Plan Finder may be able to help you find the coverage you need to stay in optimal health. Our agents are highly trained and they can find out what’s available in your area and help you make the right decision.

Our agents focus on the individual and offer an unbiased approach to helping you enroll in Medicare plans. To schedule a no-cost, no-obligation appointment, call 833-431-1832 or contact us here now.