Finding an internal medicine doctor you really connect with can be difficult, and finding the right geriatric doctor, or geriatrician, can be even more difficult. You must have confidence in your provider’s ability to treat your conditions or to refer you to other providers with extensive experience working with older adults.. Your health is the most important thing you have, and you need a doctor you’re comfortable with.

What to Look for in Geriatric Doctors

All geriatric doctors specialize in the diagnosis, treatment, and prevention of disease and other medical or chronic conditions common to seniors. You want healthcare providers who know how to treat your population and provide quality care plans. However, a doctor’s area of focus is just one thing you should look for. You also want to find a doctor that you can feel comfortable with.

It’s important that you feel comfortable asking questions about personal health concerns and that you can trust that your doctor is listening. You should feel like your health is as important to your doctor as it is to you.

The right geriatrician will take pride in providing the best quality of care possible. You should feel like your doctor thinks of you as a whole person, not just a list of conditions and symptoms.

Your geriatrician should be capable of finding solutions to your health problems. For example, let’s say you get sick one day, so you go to the doctor. Your doctor diagnoses your health condition and prescribes a medication he or she thinks is best. You should have follow-up appointments to assess how the medication works, and your doctor should be committed to finding a prescription that works if the first one doesn’t.

A good place to start is to find out what other patients say about doctors in your area. Talk to friends, family, and caregiver if you have one to see if they like their geriatricians. Ask for recommendations from healthcare professionals you know and trust.

Look at doctor reviews on websites such as Healthgrades.com and read Google reviews. When you look for reviews on Google, also search for the doctor’s name and see if he or she is in the news. If his or her name pops up with a long history of legal trouble, you should move on.

How a Medicare Advantage Plan can Help

Look for a doctor who takes your insurance. If you have Medicare, you have a great resource to receive quality healthcare. However, Original Medicare doesn’t always approve every charge, and Medicare Parts A and B can be limited in what they cover.

That’s where Medicare Advantage (MA) plans come in. MA plans come from private insurance carriers and they can cover a lot of services Original Medicare does not. Medicare Advantage plans can cover a range of services including meal delivery, hearing, vision, and even fitness classes. Some plans even include prescription drug coverage!

There may be many MA plans to choose from in your area, and a great way to find out what’s available is to talk to a qualified professional who can help you find the right plan. You won’t lose your Original Medicare coverage if you enroll in a MA plan, and the “extras” your doctor recommends, like physical activity or home health devices, may be covered.

What if I’ve Already Found a Geriatric Medicine Doctor I Like?

Maybe you’ve found a doctor you like, and he or she decides to stop taking your insurance plan. If you have a Medicare Advantage plan, you may have to wait until the Annual Enrollment Period (AEP) to make changes to your plan unless you qualify for a Special Enrollment Period (SEP). If you want to stick with your doctor and are willing to wait until the AEP, which is every year from October 15 to December 7, find out what MA insurance plans your doctor accepts.

Usually, your doctor will give you a list of carriers he or she accepts, and Medicare Plan Finder benefits advisors have access to many different plans and carriers. Your benefits advisor will work with you to find a plan that will allow you to keep your geriatric doctor.

What is the Difference Between a Geriatric Doctor and a Regular Doctor?

Geriatricians provide primary care for seniors who have complicated medical issues. Age is not the only factor that causes people to need geriatricians. For example, an 80-year-old who is active and only takes a couple of medications doesn’t need to see a geriatrician, but a 65-year-old who has diabetes and heart disease does.

Your geriatric care will involve a team of medical professionals that will provide a comprehensive healthcare plan. You’ll work with your primary geriatric doctor, and often times a social worker, physical therapist, and/or a nutritionist depending on your needs.

If a doctor does not specify that they are a geriatric doctor, that does not necessarily mean that they do not work with older patients. However, doctors who do call themselves geriatric doctors typically have studied geriatrics and are more specialized in that area.

Geriatric Doctor

When You Should Find a New Doctor

If you feel like your doctor refuses to answer your questions, it may be time to find a new one. Your doctor has a responsibility to listen to you and answer your questions. If you say you’re concerned about a recommended procedure, your doctor should ask why. Your doctor should be able to ease your concerns and make sure you’re comfortable.

You should also find a new geriatrician if the office staff is unprofessional. If they don’t do their due diligence and provide you with all of the information you need, your health could be at serious risk. Your doctor and the office staff should have great communication skills. Look for a new doctor if your geriatrician doesn’t communicate with the rest of your care team, Your doctor should respond to you within a reasonable timeframe.

How to Find a New Doctor

The first step you should take when looking for a new doctor is to look for recommendations. Ask your friends and family members if they have a doctor that they like. Then, you can call that doctor’s office to verify that they accept your insurance.

If you don’t have any good recommendations, you may want to use an online search tool to find a doctor that accepts your plan.

Your plan might have a search tool of its own. That would be a great place to start because you know for sure that the information will be as up-to-date as possible. You can be sure that the doctors listed there will accept your plan (though it is always a good idea to call the doctor and ask before you set your first appointment).

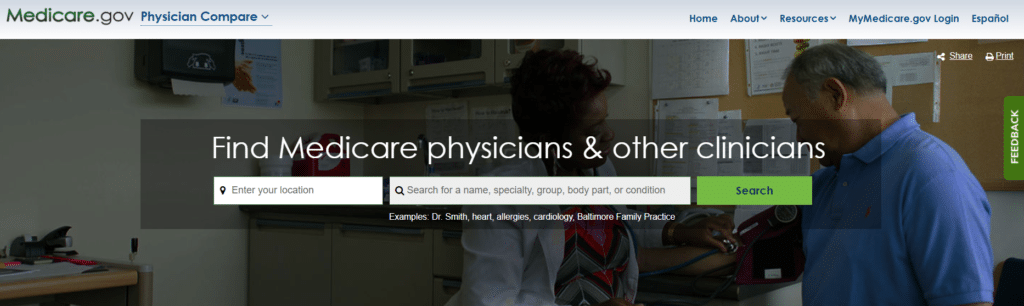

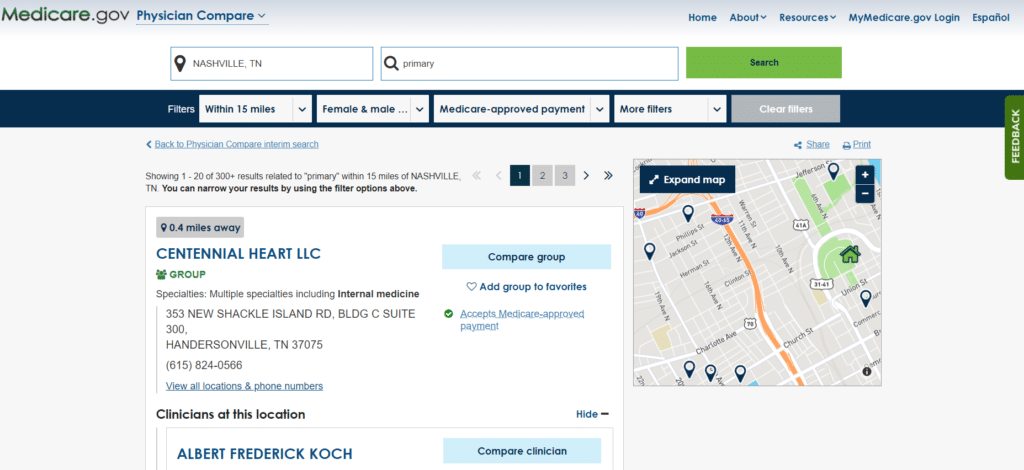

Medicare.Gov and ZocDoc are two other great tools you can use.

Medicare.Gov’s Physician Finder Tool

Medicare.Gov is a great place to start because it will tell you which doctors accept Original Medicare (Parts A and B). If you have a private plan like Medicare Advantage, be aware that just because a doctor accepts Medicare does not necessarily mean they will accept your private Medicare Advantage plan.

All you have to do is visit medicare.gov/physiciancompare and enter your location and the type of doctor you are looking for.

You may be asked to select exactly which type of doctor you are looking for. Then, you’ll see a list of doctors who accept Medicare near you. You can filter by board certification, group affiliation, male/female doctors, distance, and whether or not they accept Medicare-approved payment (meaning you won’t be billed for more than the Medicare deductible and coinsurance).

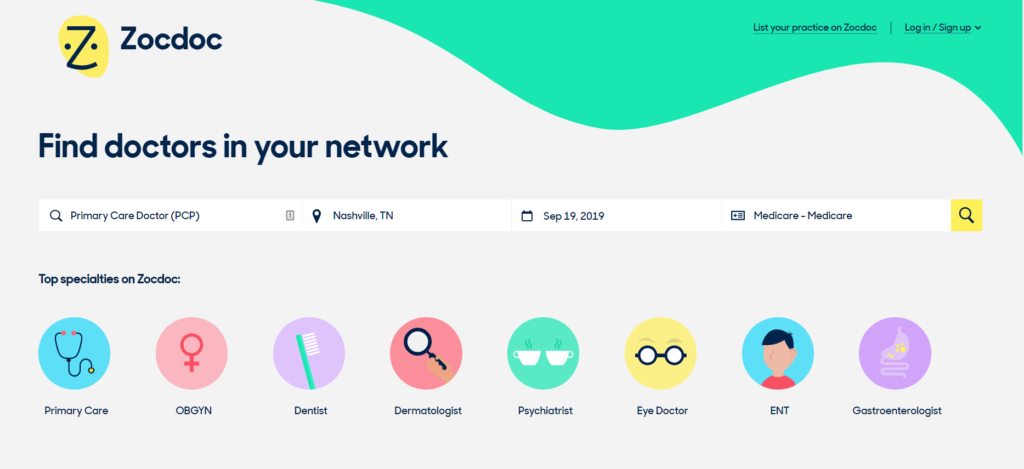

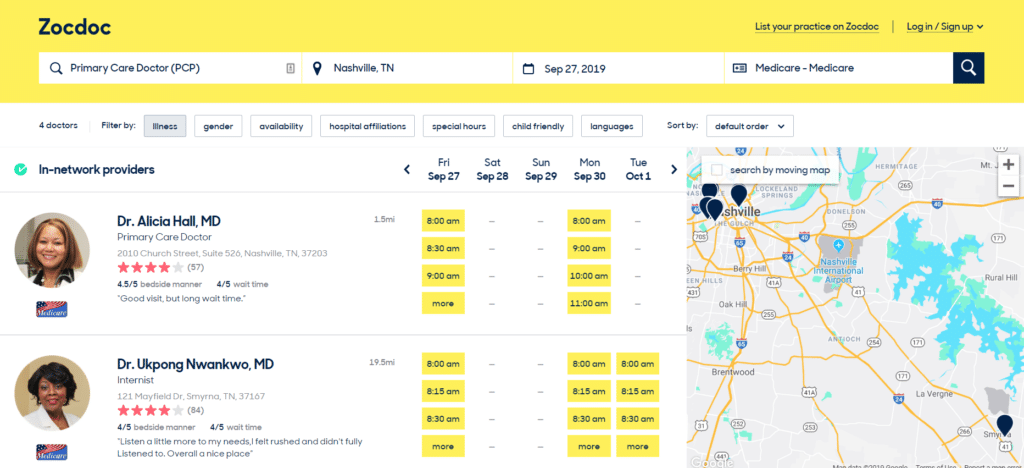

ZocDoc is another great online tool for finding doctors near you, and it includes reviews! There is also an appointment scheduling feature so that you can book an appointment without having to call the office.

You can filter your search by the procedure you need as well as by appointment time, languages, gender, hospital affiliations, etc.. To show you how that works, we used our home city of Nashville and “primary care” as an example. Notice how we selected “Medicare” as our form of insurance.

Having the right geriatric team and insurance plan is paramount to having the best overall health possible. The team at Medicare Plan Finder can help you navigate the Medicare plans out there and find the best fit. Call us at 800-691-0473 or contact us here today.

Contact Us | Medicare Plan Finder

This blog was originally written on May 17, 2019, by Troy Frink and updated on September 19, 2019, by Anastasia Iliou.

How to Get Help Paying Medicare Premiums

The National Council on Aging (NCOA) says that over 25 million Americans age 60 and older “struggle with rising … healthcare bills.” Thankfully, federal and state governments have assistance programs for people who need help paying Medicare premiums and other costs.

What Are Medicare Premiums?

A premium is an amount you pay every month for insurance coverage. Original Medicare is health insurance that provides coverage for specific services.

You can qualify for Medicare either by turning 65, or sooner if you have ALS, ESRD, or you’ve received SSDI for at least 25 months.

Medicare premiums can seem expensive, especially if you have a limited income. For example, many people don’t have to pay a Medicare Part A (hospital insurance) premium, but they might still have to pay the Medicare Part B (medical insurance) monthly premium (standard is $144.60 in 2020).

You might not have to pay a Part A premium if you or your spouse has worked 40 or more quarters and paid Medicare taxes or you otherwise qualify for premium-free Part A. You could pay up to $458 per month in 2020 if you don’t qualify for premium-free Part A.

On top of that, Original Medicare (Part A and Part B) doesn’t cover everything. If you want extra benefits such as prescription drug coverage, you’ll need to enroll in Medicare Part D, or a Medicare Advantage plan with a prescription drug benefit. Either option may come with a separate premium. Luckily, you may be able to receive help paying Medicare premiums.

What Should I Do If I Need Help Paying My Medicare Premiums?

How to Get Help Paying Medicare Premiums | Medicare Plan Finder

If you need help paying Medicare premiums, you can apply for several assistance programs called Medicare Savings Programs (MSPs). You may need to provide certain legal documents such as a Social Security card, Medicare Card, and proof of income and address to apply. You may even qualify for several different benefit programs at the same time!

Medicare Savings Programs

There are four types of Medicare Savings Programs (MSP). Each one has its own set of income limits. Your state may have different limits for annual income, too.

In 2019, the total asset limits for most MSPs are $7,730 for an individual, and $11,600 for a couple. These limits are only federal guidelines. Your state may have different limits.

Qualified Medicare Beneficiary Program (QMB). Can help pay premiums for Part A and Part B, as well as copays, deductibles, and coinsurance. An individual may qualify in 2019 with an income up to $1,061 per month or $1,430 per month for a couple. If you qualify for QMB, you may also be eligible for Extra Help (LIS) paying for Part D prescription coverage.

Specified Low Income Medicare Beneficiary Program (SLMB). Can help pay premiums for Part B. A single person may qualify in 2019 with an income up to $1,269 per month or $1,711 per month for a couple. If you qualify as a SLMB, you’re may be eligible for LIS paying for Part D prescription coverage.

Qualified Disabled and Working Individuals Program (QDWI). Can help to pay Part A premiums. This MSP is for disabled people who lost their premium-free Medicare Part A when they went back to work. The income limits for QDWI are $4,249 per month for an individual, and $5,722 for a couple in 2019. The asset limit is $4,000 for an individual and $6,000 for a couple.

Medicare Savings Program Application and Eligibility

The best way to find out if you qualify for MSPs is to apply and let your state determine eligibility. However, Benefits.gov has a tool that uses multiple choice questions to find out if you may be eligible.*

Your state’s Medicaid office can provide information about how to apply and where to send your application.

After you apply, you should receive a “Notice of Action” within 45 days detailing what programs you qualify for, and you should be automatically enrolled in the program that most aligns with your qualifications.

Low Income Subsidy (LIS)

Low Income Subsidy (LIS) or Extra Help is a federally-funded program that helps Medicare beneficiaries save on prescription drugs. LIS can help cover your Part D premium, deductibles, coinsurance, and copays.

The program can provide huge savings! For example, you won’t pay more than $3.40 for generic drugs or $8.50 for brand-name drugs in 2019 according to the Social Security Administration (SSA).

To qualify for LIS, you must have a monthly income of less than $1,405 for an individual or less than $1902 for a couple in 2019. You must also

Have Original Medicare (Part A and Part B) coverage

Have prescription drug coverage (either a Medicare Part D plan or a Medicare Advantage plan with prescription drug benefits)

Have American citizenship

Not have savings, investments, and real estate valuing more than $28,150 if you are married or $14,100 if you are single

You may also qualify for Extra Help if you have Supplemental Security Income (SSI) or if you have both Medicare and Medicaid insurance. If you think you meet the eligibility requirements, click here to apply for LIS or ask your insurance agent to help you.

If you qualify for a DSNP, you may also qualify for a Special Enrollment Period (SEP), which can give you the freedom to make one change per quarter to your plan*. This is a huge cost-saving benefit to DSNP enrollees because it means you can enroll in a plan that best suits your needs.

For example, if your doctor stops accepting your insurance plan, but he accepts another DSNP in your area, you can switch plans to stay with your doctor. You won’t have to enroll in a different plan with a potentially higher premium.

*For the first three quarters of the year as long as you qualify for both Medicare and Medicaid.

How to Save Money on Premiums With Private Medicare Insurance Plans

Some people may not qualify for Medicaid, MSPs or LIS. However, you may still be able to save some money. If you have Original Medicare, you can enroll in private plans such as Medicare Advantage or Medicare Supplements. Note: You must choose one because you cannot be enrolled in both at the same time.

Medicare Advantage Plans

Medicare Advantage (MA) plans help cover medical services. These plans can offer additional benefits such as prescription drugs, vision, hearing, dental, and even fitness classes! Most MA plans have monthly premiums (the average is $23 in 2019) and some MA plans have $0 monthly premiums*.

*You must continue to pay the Part B premium in addition to a Medicare Advantage premium.

If you stick with Original Medicare, you could end up spending more money in premiums and other monthly dues. For example, if you have a gym membership, you likely have to pay dues. That’s one expense. If you have private dental insurance to cover routine cleanings, that’s another. Add vision insurance to that, and that’s three monthly expenses.

Alternatively, you might be eligible for a Medicare Advantage plan that includes dental, vision, and fitness supplemental benefits!

Medicare Supplement Plans

Medicare Supplement (Medigap) plans help pay for financial items such as coinsurance. In 2020, there eight different Medigap plans that offer different levels of coverage. Basically, the more services the plan covers, the higher the premium. Depending on your needs, you can save money on premiums by selecting a plan that covers fewer services.

2020 Medigap Comparison Chart

Find Help Paying Medicare Premiums

If you’re struggling to pay your monthly Medicare premiums, a licensed agent with Medicare Plan Finder may be able to help. Our agents are highly trained and can help you find a plan that suits your budget needs. To set up a no-cost, no-obligation appointment call 844-431-1832 or contact us here to learn more today.

Find Medicare Plans | Medicare Plan Finder

MOOP meaning in healthcare? What is it and Why Does It Matter?

Medicare is a resource that many people use to help with healthcare costs, but like any health insurance, it can be expensive. Depending on your condition or what procedures you need, you could spend thousands of dollars on healthcare costs throughout the course of a year.

However, there are safeguards built into these plans designed to protect how much you’ll ultimately be required to spend out-of-pocket on medical costs in a specific calendar year. This is called the maximum out-of-pocket, also known as the MOOP. But that’s only part of the equation, when you bring your prescriptions into the equation, you have what’s now called a TROOP, also known as True-out-of-pocket.

Yes it’s confusing.

But, the good news is both MOOP and TrOOP are means of patient protection that limit your spending on medical services through various health insurance plans such as a Medicare Advantage plan, and/or a Medicare Part D plan.

Important note, Individuals only utilizing Original Medicare (Part a and Part b only) do not have the same protections, which is why most people take advantage of either Medicare advantage plan or a Medicare supplement paired with a Part D drug plan.

Medicare MOOP

Maximum out-of-Pocket Medicare Advantage Costs

The Centers for Medicare and Medicaid (CMS) regulates Medicare Advantage plans. In many cases, the Medicare Advantage MOOP is as much as $6,700 for in-network services. And, various health insurance companies plan MOOPs can be higher or lower.

If you combine costs for health care services for both in- and out-of-network limits, maximum out-of-pocket limits for some plans can be up to $10,000.

Be aware that not every cost you receive counts toward your MOOP limit.

For example, if you have a Part D plan, your monthly premiums and prescription costs may not count toward your MOOP. Also, your plan may not cover out-of-network services even after you reach the out-of-pocket spending limit.

What Happens When You Hit Your Limit?

Once you hit your max out-of-pocket spending limit, your Medicare Advantage plan should pay for the rest of your out-of-pocket expenses for qualifying services for the remainder of the year. This includes hospital stays, medical equipment and other medical expenses that come along when you use your insurance coverage.

Note: Look at your plan’s Evidence of Coverage (EOC) document for specific details about qualifying covered services.

Let’s look at a real-world example of this. Let’s say your doctor recommends a hip replacement and your Medicare Advantage plan has a $6,700 MOOP. The average hip replacement surgery is $39,000, which is much more than your MOOP.

In this example, you haven’t had any MOOP-qualifying costs, so your total out-of-pocket expenses will be $6,700. That means that your insurance carrier will pay more than $32,000.

Medicare TrOOP

TrOOP stands for True Out-Of-Pocket costs. While it may sound similar to MOOP, it is not the same thing.

While MOOP applies to Original Medicare-covered services with Medicare Advantage Plans, TrOOP applies to prescription drug coverage, whether that’s from Medicare Advantage Prescription Drug plans or stand-alone Medicare Part D plans.

How Does the TrOOP Work?

TThe TrOOP starts when you reach the annual out-of-pocket threshold after you’ve left the donut hole. In order for your costs to count, they must meet the following conditions:

Your generic or brand-name prescriptions are on your Medicare Part D plan’s formulary or list of prescription drugs.

One exception to the “formulary rule” is if Medicare and your plan approves your drugs even if the prescription drugs aren’t on your plan’s formulary. In this case, your medications will still count toward TrOOP because both Medicare and your plan approved the formulary exception.

You purchased your approved medications at one of your Medicare plan’s in-network pharmacies.

Note: Medicare Part D plans vary by location and coverage policies can depend on the individual plan.

Other Costs That Count Toward TrOOP

Other Medicare Part D costs can count toward TrOOP including:

Your Annual Initial Deductible: If your plan has an initial deductible, this is the amount you’ll pay before your Medicare Part D coverage “kicks in.” This means that you’ll pay 100 percent of your prescription costs until you reach that initial deductible*.

Cost-Sharing Costs After You’ve Met the Initial Deductible: If your plan requires you to pay a copay or coinsurance, those costs will go toward your TrOOP. For example, if your plan requires a $10 copay for a medication, that money will go toward your out-of-pocket limit.

Payments While You’re in the Donut Hole: This is where things may get a little confusing. According to CMS, the manufacturer discount on “applicable drugs” is 70 percent, your cost is 25 percent, and your plan pays the remaining five percent. The five percent your plan pays does not count toward TrOOP, meaning that only 95 percent of the total drug cost counts*.

State Pharmaceutical Assistance Programs (SPAPs): Some, but not all states have assistance programs called SPAPs that work with your Medicare Part D plan. In qualifying cases, the SPAP program may help pay for your Part D premiums, deductible and copays. If the SPAP program assists with your plan costs, those payments may count toward TrOOP.

*If you receive income-based subsidies or other assistance, you may pay a different amount depending on your needs-based program.

What Is the Medicare Donut Hole?

The “donut hole” is a gap in coverage that some Medicare enrollees will see in their prescription drug coverage. It works like this: In 2019, Medicare Part D has a $415 deductible (some plans may be less) and a $3,820 initial coverage limit for total out-of-pocket costs. The donut hole is the gap between the initial coverage limit and the annual out-of-pocket-threshold ($5,100 ).

The donut hole will effectively be going away in 2020. This means that you’ll pay 25 percent of both generic and prescription drug costs after you reach the initial coverage limit.

According to CMS, the 2020 Part D deductible will be $435, the initial coverage limit will be $4020, and the out-of-pocket threshold will be $6,350.

What Doesn’t Count Toward TrOOP?

Not all the money you spend on your prescriptions counts toward your out-of-pocket limit. For example, the amount your plan covers does not count.

For example, let’s say your prescription costs $50. Your copay is $15 and your insurance policy pays $35. Only the $15 you pay for your prescription goes toward your limit. Other items that don’t count include monthly premiums and excluded drugs.

CMS considers excluded drugs to be optional, and are therefore not covered. According to the Center for Medicare Advocacy, excluded drugs include:

Drugs to promote weight loss or weight gain, even if they cosmetic use, such as to treat morbid obesity. One exception is that that drugs to treat AIDS wasting are not considered to be for cosmetic purposes and are therefore NOT excluded.

Fertility medications

Erectile dysfunction drugs, except when medically necessary and when they aren’t used to treat sexual dysfunction

Hair growth and other cosmetic drugs. Note that drugs to treat acne, psoriasis, rosacea and vitiligo are not considered cosmetic drugs.

Foreign drug purposes

Vitamins and minerals, except niacin, Vitamin D supplements (when used for a documented medical reason), prenatal vitamins and fluoride

Consult your formulary if you have more questions about what medications are included in your plan.

Let Us Help You Navigate MOOP Medicare and TrOOP

Medicare may seem complicated, and Medicare Plan Finder is here to help. Our licensed agents are highly trained and can help you determine what plan will save you the most money. Contact us here to set up a no-cost, no-obligation appointment to learn more or call us at (833) 567-3163.

5 Ways to Boost Brain Health for Seniors

It’s perfectly natural to lose some mental “processing speed” as we age. This process is called cognitive aging and usually starts as soon as we reach adulthood. While certain brain functions like vocabulary might even improve as we get older, others will gradually decline. A common list of cognitive changes in elderly people typically includes slower problem solving, diminished spatial awareness, and a decline in perceptual speed and memory.

Most of these aging brain symptoms are entirely normal but the rate of this decline may increase, leading to MCI (mild cognitive impairment) or even dementia. However, scientific research has uncovered several methods proven to help maintain elderly brain health and most of them are simple things you can do in your day-to-day life!

Staying Active At Any Age

The connection between exercise and brain health for seniors has long been established. But new studies are suggesting that staying active may be the best way to prevent memory loss in old age! While it might be most effective before severe memory loss begins, it also appears to benefit those with advanced conditions like Alzheimer’s or vascular dementia.

Seniors who exercise regularly can experience reduced inflammation, improved blood flow, and even increased growth of new blood vessels in the brain. An active lifestyle can also improve the quality of sleep, which we will see later is another crucial factor in maintaining brain health. In fact, sustaining a moderate regimen of low impact exercises from six months to a year has even been associated with increased volume in the prefrontal and medial temporal cortices, the parts of the brain responsible for memory and critical thinking!

Medicare Fitness Programs

Unfortunately, the research also indicates that exercise must be a regular commitment in order to see some of these amazing benefits. But dedicating at least three hours a week can be difficult for seniors who don’t have access to a gym. This is where Medicare plans that include fitness programs can help. Plans can include Medicare fitness programs Programs like SilverSneakers® and Silver&Fit® that are designed specifically for seniors and can provide access to fitness and exercise centers. Some may supply their less mobile members with home fitness kits.

Many of us probably remember our mothers extolling the virtues of “brain food.” Turns out she was right! A diet consisting of mostly fruits, vegetables, nuts, beans, and fish has been closely linked to brain health and a lower risk of dementia. This “Mediterranean diet” is also often touted for its positive effects on heart health and cardiovascular risk factors, which can indirectly influence the health of the brain.

In addition to a more healthy diet, many seniors take supplements to get a higher dose of these crucial ingredients than can be found in the foods themselves. Some of the most popular include fish oils like omega-3 fatty acids, antioxidants such as resveratrol, as well as creatine and even caffeine.

Companies have begun producing memory supplements targeted at seniors. Some of these include:

Brainol (includes 19 ingredients for improved cognition, like B-Vitamins, Huperzine A, L-Theanine, and DMAE.

Neurofuse (includes B-Vitamins, L-Theanine, DMAE Bitartrate, and Huperzine A.)

Irwin Naturals Brain Awake (includes Vitamin B6 and L-Theanine)

BriteSmart (includes Huperzine A)

While memory supplements are not typically covered by Medicare, some Medicare Advantage plans might have an OTC (over the counter) allowance benefit which would allow you to purchase supplements. Click here to read more about OTC benefits in Medicare.

One of the easiest methods for seniors to maintain mental acuity is daily brain training. This interactive practice can take on many forms, from crossword puzzles to arts and crafts. And now more than ever, there are services and applications specifically designed to give you your daily dose of critical thinking.

Activities for Alzheimer’s Patients at Home

There are countless ways for seniors to get their brains engaged on a daily basis. Many are things you might already enjoy, including puzzles or card games. In the technological age, of course, many of these activities can be done on a computer or smartphone.

In addition to these traditional games, there are many apps that are designed specifically as activities for seniors with dementia and Alzheimer’s. Apps like Lumosity are great for challenging your brain on a daily basis and some, such as Mindmate, even include exercise and nutrition tips. A cursory Google search may also help you find other free brain games for seniors.

Some doctors suggest that one of the best ways to retain memory and cognitive functioning is to remain engaged with a social group. Many seniors use social media to stay in touch with family and friends and there are even apps like Timeless that are designed to help people with dementia or Alzheimer’s stay social.

Clear Your Mind (And The Rest Will Follow)

The importance of everyday factors like stress and sleep on brain health for seniors shouldn’t be overlooked, especially for the elderly. A good night’s sleep will clear the brain of toxins that accumulate throughout the day like beta-amyloid, a protein which is also commonly found in Alzheimer’s patients. Stress can also play a huge role in how the brain functions by introducing high levels of cortisol and even possibly reducing the size of the prefrontal cortex, the part of your brain that governs memory and learning.

Meditation and Aging

Meditation has been shown to increase the thickness of the hippocampus and decrease the volume of the amygdala, which is responsible for stress and anxiety. Research into mindfulness meditation has even indicated an effect on the process of aging itself. A 2017 UCLA study showed that the brains of people who meditate regularly actually declined at a slower rate than those who did not.

Natural Sleep Remedies For The Elderly

We know that sleep is essential for overall brain health for seniors, but many older adults experience trouble sleeping. Some practices for getting better sleep include turning off screens and lights, regular exercise, reducing sugar intake, and keeping a consistent sleep schedule with naps no longer than 20 minutes. If something more serious is causing you to lose sleep, you might need to consult a physician to test for sleep apnea or to evaluate any medications you might be taking.

Medicare Annual Wellness Visit

If the decline in cognitive functions persists or accelerates, you may need to seek professional help as a preventive measure. As part of your Medicare benefits, you may be entitled to a paid Annual Wellness Visit with your primary care provider to develop a personalized prevention plan that takes into account your lifestyle and risk factors.

In addition to checking physical factors like height, weight, and blood pressure, they can perform a cognitive assessment and screen for various forms of dementia or cognitive impairment. Additionally, a Special Needs Plan might be used to supplement your Medicare benefits. These plans are Medicare Advantage products specifically focused on providing care and coverage for patients with dementia.

Prescription Drug Plans for Alzheimer’s

If your condition or that of a loved one develops into Alzheimer’s or another form of dementia, Medicare Part D may cover the cost of prescription drugs to treat the symptoms. These medications include brands like Aricept and Exelon. Though they are not cures for the disease itself, they are effective at temporarily improving common symptoms of dementia, such as confusion or aggression.

Memory Care Through Medicare

Some severe cases of dementia and Alzheimer’s can make it nearly impossible to handle all the daily duties that come with living alone. In these cases, Medicare may help pay for nursing home care for a period of up to 100 days but will not cover such a solution in the long-term. However, some Medicare Part C plans may help cover the high costs of a nursing home or memory care facility.

For help enrolling in a Medicare plan that covers memory care and other brain health services, call us at 844-431-1832 or click here.

How to Choose the Best Type of Medicare Plan for You

When it’s time to choose a Medicare plan, it’s easy to get overwhelmed. There are quite a few different types of Medicare plans to choose from. Once you choose what type you want – you still have to choose a plan! Making the right choice is important because it may not be easy to change plans if you change your mind.

The Annual Enrollment Period (October 15 through December 7) is when anyone can make changes, and for some people, it’s the only time. If you make the wrong choice, you might have to wait a whole year before you can change again (unless you qualify for the OEP or have a SEP).

Which Types of Medicare Plans are Best for Me?

To figure out which Medicare plan is best for you, ask yourself the following questions:

What specific medical services do I need coverage for (ex: lab tests, blood work, surgery, chemotherapy, dental, etc.)?

How much room do I have in my budget? Am I able to pay a little more to have more benefits?

Would I rather pay more on a monthly basis and pay very little when I visit the doctor, or is it better to pay a small amount every month but risk having higher copayments?

Who are the doctors and other providers who I want to be covered in my plan?

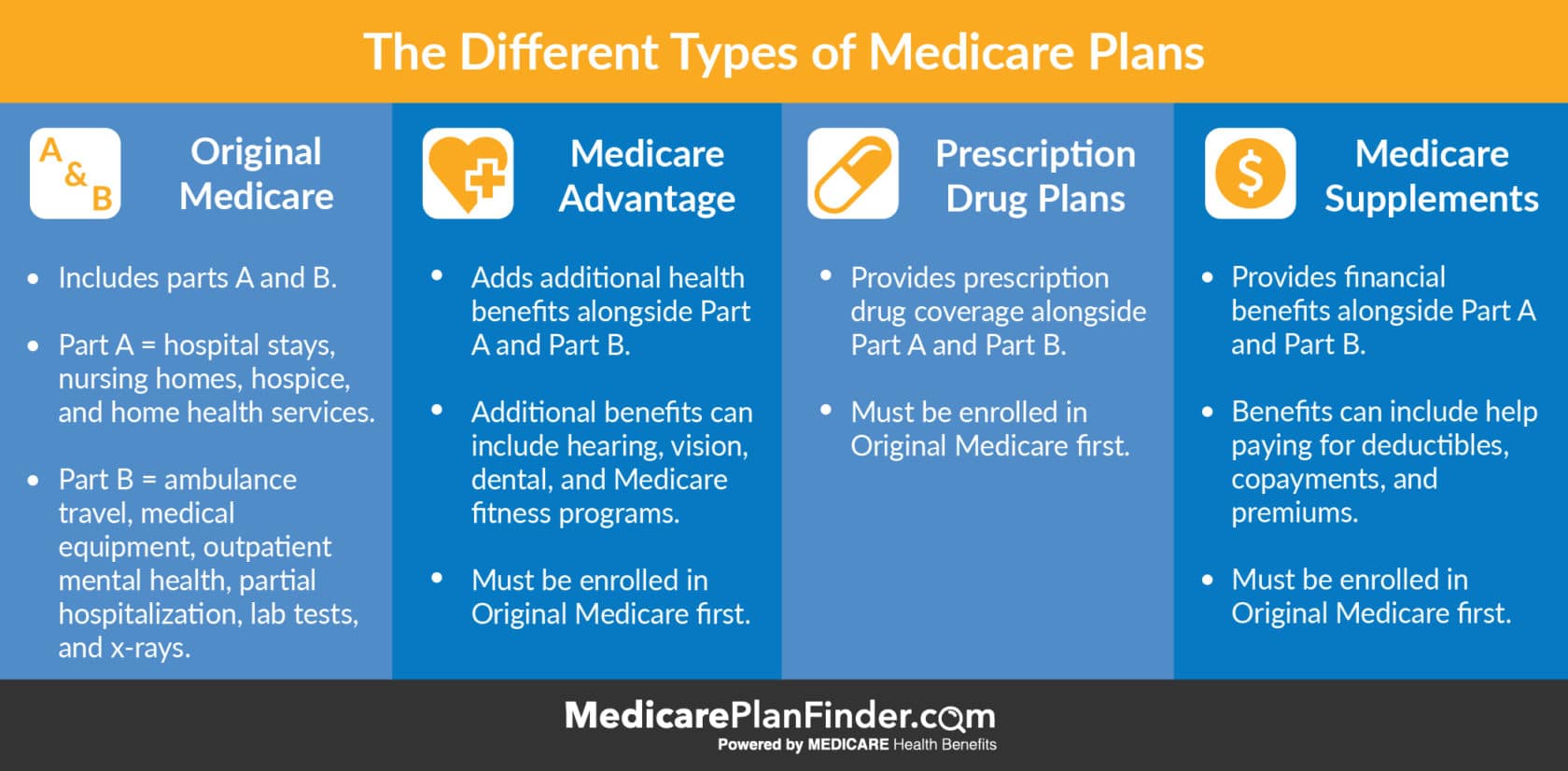

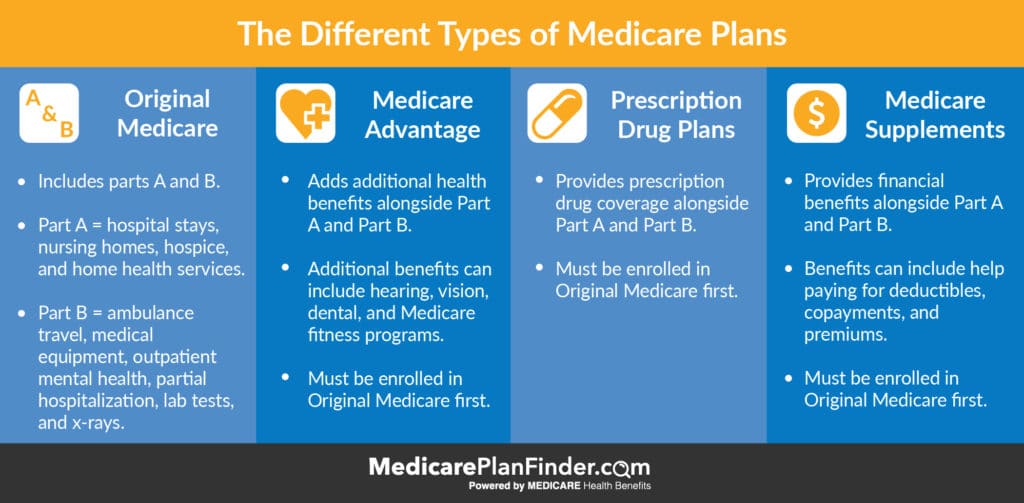

There are four main types of Medicare plans to consider when you begin your Medicare plan search. Start by comparing Original Medicare, Medicare Advantage, Prescription Drug Plans, and Medicare Supplements.

Keep in mind that you cannot have Medicare Advantage and a Prescription Drug Plan at the same time. You also cannot have Medicare Advantage and a Medicare Supplement plan at the same time.

Which plan or combination of plans works best for you?

Medicare Advantage: A private plan that you can purchase once you have Original Medicare. Can add additional benefits such as hearing, vision, dental, fitness, etc. Can include a prescription benefit.

Prescription Drug Plans: Another type of private plan that you can purchase once you have Original Medicare. Usually only includes a prescription benefit.

Medicare Supplements (Medigap): Another type of private plan that you can have in addition to Original Medicare. Adds more financial coverage, like for copayments and deductibles. This type of plan would also require you to have a stand alone part D drug plan.

Different Types of Medicare Plans

Choosing a Medicare Advantage Plan

So, did you decide to go with Medicare Advantage? Great! Now, there are a few types of Medicare Advantage plans that may be available for you. First, ask yourself whether or not you need a large network and whether the freedom to see any doctor is important to you. Then, read through these important differences:

HMO Plans (Health Maintenance Organization) – You’ll select one primary physician. In some cases, you may only receive coverage for that one doctor (unless he or she refers you to a specialist). Requirements may vary based on your plan.

HMO-POS Plans (Point-Of-Service) – You’ll select one primary physician, but you’ll have the freedom to visit any specialist in your network for your other needs. You will be charged a fee for visiting specialists.

PPO Plans (Preferred Provider Organization) – You can see any doctor, but your costs will usually be lower if you choose one that is in your network.

PFFS Plans (Private Fee-For-Service) – You will not need referrals or a primary physician, but you’ll have to pick a doctor that accepts your PFFS plan.

SNP (Special Needs Plans) – Designed for those who are eligible for both Medicare and Medicaid, live in a nursing home, or have a chronic illness or disability.

MSA (Medical Savings Account) – Works like a tax-free savings account for your medical bills. Medicare will deposit money into your HSA. You can use that account to pay for medical expenses.

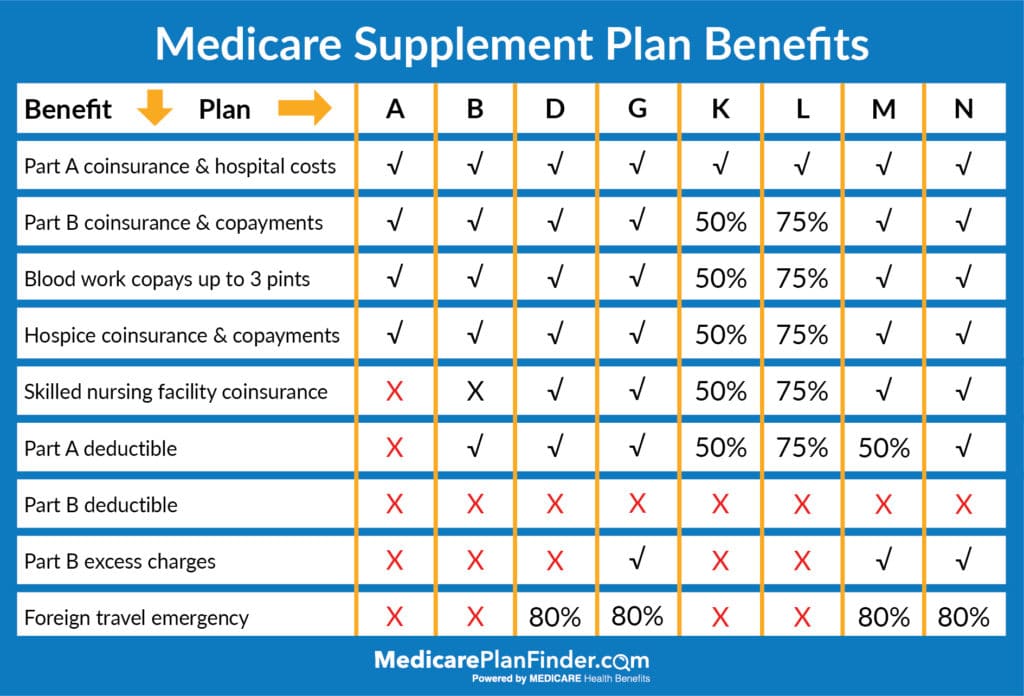

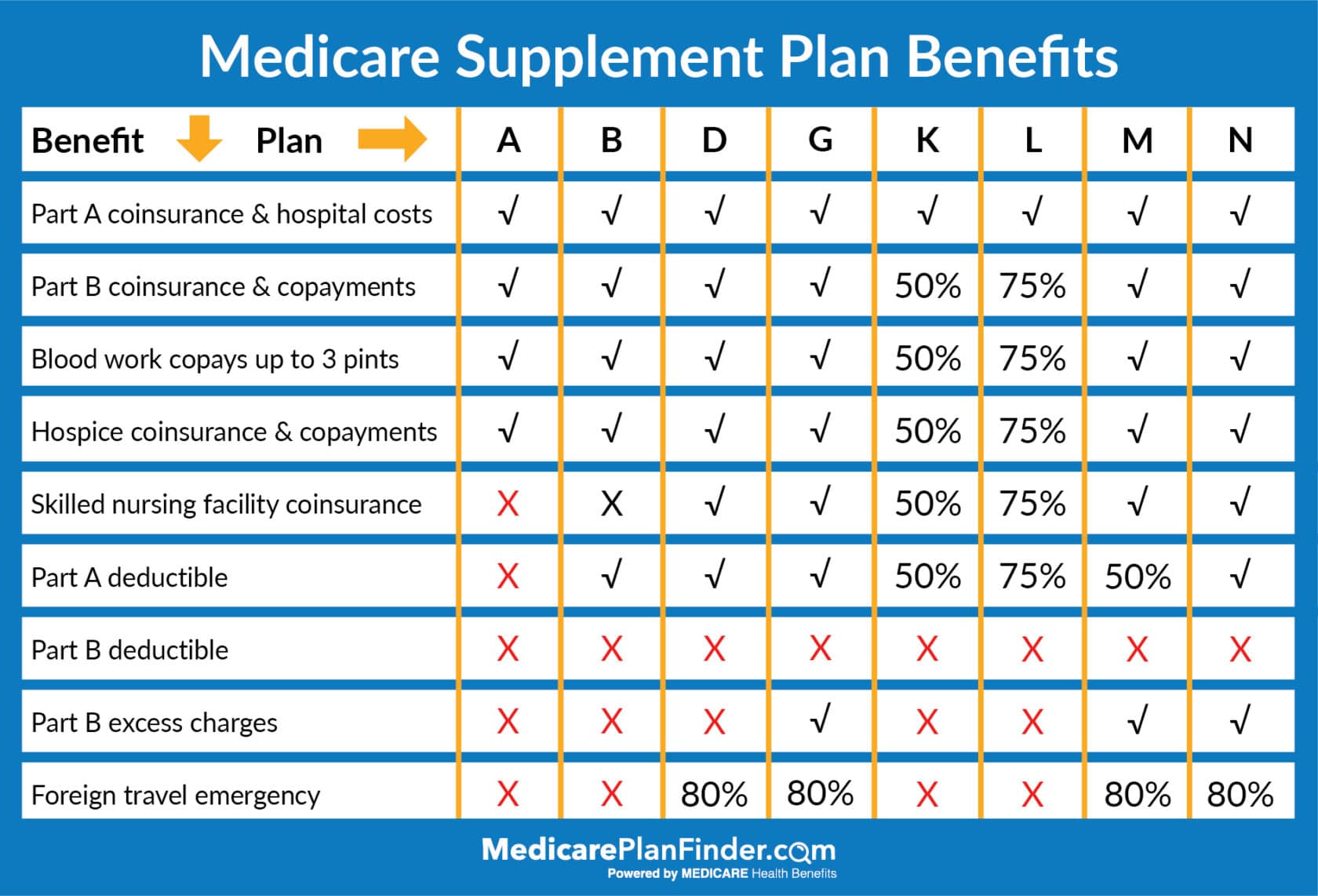

How do I Pick a Medicare Supplement Plan?

If you’ve decided that you want a Medicare Supplement plan, you’ll want to start by selecting the plan letter that corresponds with the coverage you need. Use the chart below for reference.

Once you’ve made that decision, you may have a few different carriers available in your area to choose from (some smaller cities may not have several options available).

Finding Medicare Plans in your area just got easier. Our Medicare Plan Finder tool can help you not only see what is available, but see which options may be best for your unique needs.

You can enroll by yourself, or you can meet with a licensed agent (for free) who can walk you through the process to make sure you don’t make any mistakes. The licensed agent can also talk to you about a variety of different types of plans in your area and answer all your questions.

This unbiased approach is a great way to get the help you need when selecting a Medicare plan.

To set up your free meeting with a Medicare Plan Finder licensed agent, call 833-567-3163 or click here.

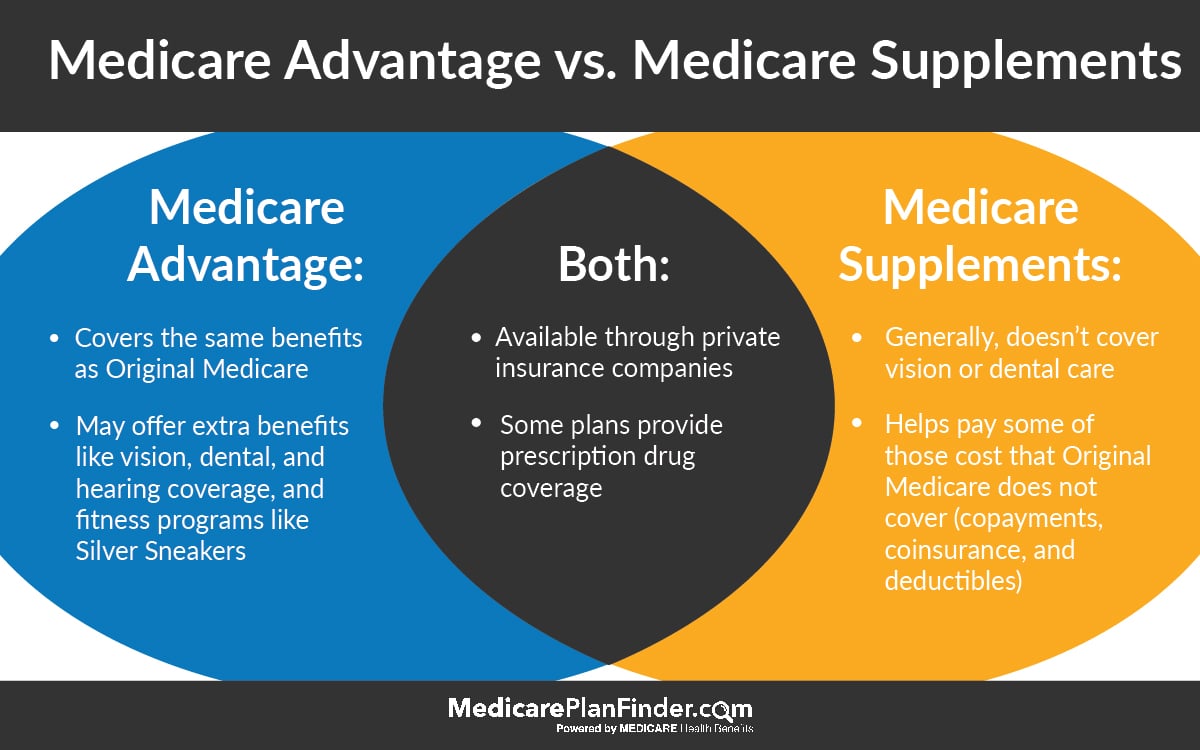

Medicare Advantage vs. Medicare Supplement

Medicare Advantage and Medicare Supplements (also called Medigap) are very different insurance plans with distinct benefits. The answer to the question “is Medicare Advantage better than Medigap?” depends on your circumstances and needs.

What is Medicare Advantage?

Medicare Advantage plans are private plans (not owned by the federal government) that can offer additional health benefits. To have Medicare Advantage, you have to enroll in Original Medicare first. You may have to continue to pay your Medicare Part B premium even if you have Medicare Advantage (MA), but MA premiums can be as little as $0.

Medicare Advantage plans are not all the same, but they can provide benefits like (click on the links to learn more about each one):

There are many different types of Medicare Advantage plans, although not every plan type may be available in your area.

A health maintenance organization (HMO) is a network of health-care providers and facilities where you choose a primary care physician to coordinate your care.

A preferred provider organization (PPO) is also a network of health-care providers and facilities but typically you do not need to select a primary care physician, and you have more flexible options regarding out-of-network care.

A private fee-for-service (PFFS) plan is a mode of benefit delivery where you are not limited to a network. However, there are no guarantees that your doctor or hospital will accept the plan. If you choose to receive your Medicare health coverage through a private Medicare Advantage plan, you must continue paying your Part B premium regardless, because you remain enrolled in Original Medicare (Part A and Part B), even after joining a Part C plan.

What is Medigap?

Medigap is more different from Medicare Advantage than you might think. While Medicare Advantage plans are able to offer health benefits, Medicare Supplement plans (also called Medigap) offer financial benefits. For example, some Medigap plans can cover your Part B premium.

The chart below explains the differences between available Medigap plans in 2020. You can also use our Medicare Plan Finder search tool to compare plans in your area.

2020 Medicare Supplement Comparison Chart

Comparing Medicare Advantage vs. Medicare Supplement plans

Let’s look at Medicare Advantage vs. Medigap. In short, the difference between Medicare Advantage and Medicare Supplement plans is that one can supply health benefits while the other can supply financial coverage.

Medicare Supplement Insurance is a policy that’s added to Original Medicare, Part A and Part B, to provide additional financial coverage. Medicare Advantage is a private plan option that may provide you with other health benefits that Original Medicare does not cover (like dental, vision, fitness programs, etc.).

You cannot have both Medicare Advantage and Medigap at the same time.

Medicare Advantage vs Medicare Supplements | Medicare Plan Finder

A given plan type (e.g., Plan F) has the same benefits regardless of the insurance company that provides the policy, or the state in which you reside. This is not true of Medicare Advantage plans, however, because coverage details may vary by plan.

Excluding prescription drug coverage, any standard Medigap plan with Part A and B will have more benefits than a standard Medicare Advantage plan. However, as mentioned above, some Medicare Advantage plans offer benefits beyond those found in Part A and Part B.

Some Medicare Advantage plans offer prescription drug coverage (often for an additional monthly cost). With a Medigap plan, in contrast, you would need to enroll in a separate prescription drug plan. When comparing plan options, consider your costs for drug coverage. In some cases, Medigap with a stand-alone prescription drug plan has lower total costs than a Medicare Advantage plan with drug coverage. In other cases, the reverse might be true.

[Tweet “Do your research! Comparing #Medicare Advantage vs Medicare Supplement”]

Real-Life Examples: Medicare Advantage vs. Medicare Supplements

Let’s take a look at some real-life examples to help you decide whether Medicare Advantage or Medicare Supplements are right for you.

If you have Medicare Parts A (hospital coverage), B (medical coverage), and D (prescription coverage) and you are hospitalized for cancer treatments for 90 days, you may have out of pocket costs. The Part A deductible means you would pay well over $1,000 first. Once you meet your deductible, your costs will go down. However, after day 60, you’ll be responsible for a portion of every day that you stay there.

If you have Medigap Plan B, your deductible and many of your other hospital costs will be covered. This plan would be in addition to your Part B coverage, so it would all work together to provide extra coverage.

If you have Medicare Advantage, you may have additional health benefits. You’d still likely be responsible for some of those out-of-pocket hospital costs, but your plan might provide a home healthcare benefit, meaning you can get a private in-home nurse when you are released from the hospital. You might also have coverage for medical equipment, such as bathroom safety equipment or a walker.

Comparison is key: Medicare Advantage vs. Medicare Supplements

When choosing between a Medigap plan and a Medicare Advantage plan, take the time to do your research. Read the benefit descriptions of every Medigap and Medicare Advantage plan you are considering. Be certain to look at:

Monthly premium

Deductibles

Doctor and healthcare facility restrictions

Benefits

Anticipated plan costs given your typical use of health-care and hospitalization services

Prescription drug coverage cost sharing as it relates to your medication usage

In the end, your decision is going to be the one that you feel the most comfortable with. The challenge is often wading through all the material to get to the bottom line. Want to make that a little easier? Give us a call at 844-431-1832.

This post was originally published on October 23, 2018, and was last updated on August 29, 2019.

What Can You Do During the Medicare Annual Enrollment Period?

Medicare Enrollment Periods

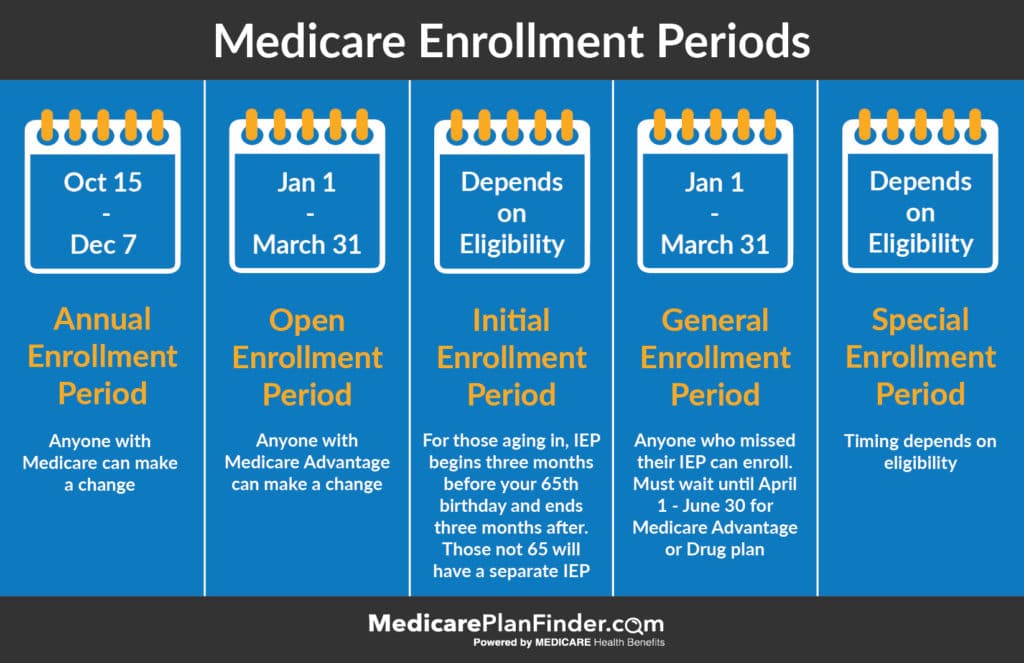

Did you know that there are five different Medicare enrollment periods throughout the year? Not everyone will be eligible for every period, but everyone who has Medicare is eligible for the Annual Enrollment Period.

Be sure to keep track of each enrollment period so that you know when it’s your turn to make changes. Don’t go months with a bad plan just because you missed your enrollment period!

What/When is the Annual Enrollment Period?

The Annual Enrollment Period runs from 10/15 through 12/7 of each year. This is the time when all Medicare beneficiaries are eligible to make changes, which will go into effect on January 1 of the following year. It does not apply to people who have not yet enrolled in any form of Medicare coverage. If you’re enrolling for the first time, you’ll have an “Initial Enrollment Period.” You can use the AEP later to make changes if you don’t like the choices you made during your IEP.

Changing Medicare Plans After the Annual Enrollment Period

There are a few other times throughout the year when you may be eligible to make changes.

The Initial Enrollment Period (IEP) is for those enrolling in Medicare for the first time. If you are aging into the program, this will begin three months before your 65th birthday and end three months after. If you become eligible due to disability, your IEP will depend on your disability status or diagnosis.

The General Enrollment Period (GEP) is for those who missed their IEP. It runs from January 1 through March 31. If you enroll during the GEP, your coverage will begin on July 1. You may face a late enrollment penalty fee for not enrolling during your IEP. If you want to enroll in Medicare Advantage during the OEP, you can do that between April 1 and June 30, or you can wait for the AEP.

The Special Enrollment Period (SEP) is not one specific time frame. You may qualify for a “temporary” SEP if you have a special circumstance that results in a loss of coverage, such as losing a job with coverage or moving to an area where different plans are available. You will likely have 30 days following the event to make a change. Some circumstances, like having a disability, can make you eligible for a different type of SEP. If you are disabled or have low-income and have a special needs plan, you can change plans once per quarter for the first three quarters of the year.

How can I get a SEP for Medicare?

To qualify to change plans once every quarter for the first three quarters of the year, you must:

Be a member of a Medicare Savings Program or Medicaid

Be part of SPAP (State Pharmaceutical Assistance Program)

Be in a Medicare Savings Program or LIS (Extra Help)

To qualify for to change plans once following an event, you must:

Move to a new service area that has different plan options available

Involuntarily lose your coverage

Find a contract violation with your plan

Lose or gain a job where you are enrolled in employer benefits

Move into or out of a medical facility

Leave imprisonment

Suddenly gain or lose Medicaid eligibility

Suddenly gain or lose Medicare Savings Program or LIS eligibility

Have been automatically enrolled in Part D

OEP vs. AEP

OEP is not the same as AEP. During AEP, you can make a lot of different changes to your coverage. During OEP, you can only do one of the following:

Switch from one Medicare Advantage plan to another

Change from a Medicare Advantage plan with prescription drug coverage to Original Medicare + Part D

Switch from Medicare Advantage to Original Medicare (can also add Part D)

What can I do During the AEP?

During AEP, you can make a number of different changes to your coverage, like:

Enroll in a Medicare Advantage plan

Switch to a different Medicare Advantage plan from what you had

Drop your Medicare Advantage plan and have only Part A and Part B

Add a Part D prescription drug plan

Change to a Medicare Advantage plan with a prescription drug benefit

Change from a MAPD (Medicare Advantage Prescription Drug Plan) to a Medicare Advantage plan without prescription coverage

Change from one Part D plan to another

Drop your prescription drug coverage and return to Original Medicare only

You can also add or remove Medicare Supplement (Medigap) coverage, but keep in mind that you can enroll in Medicare Supplements during any time of year. Enrollment periods to not apply to Medicare Supplement plans. However, if you enroll in Medigap any time past your Initial Enrollment Period, underwriting may apply, leaving you with higher costs than you could have had if you enrolled sooner.

Why the AEP is so Important for Medicare

The ability to make these changes every year is more important than you may realize.

Even if you think you’re happy with your plan, plans are allowed to change their benefits and costs every year. Your plan can add or remove benefits and make cost adjustments as they need to. At the same time, new plans are continually entering (and leaving) the market. It’s a good idea to take a look and see if there is a better plan for you each year.

Licensed agents are required to go through a training and certification process before they can sell to you. They are usually trained on what’s going on in the area that they sell in. They may be able to tell you about plans that you haven’t even heard about before, and they can help you sort through your options. It does not cost anything to meet with a Medicare Plan Finder licensed agent.

Can you Auto-Renew Medicare?

In most cases, you do not have to renew your plan each year. Your Medicare coverage will automatically continue as long as that plan is still available for the current year. The only reason your plan wouldn’t renew is if that specific plan itself leaves your service area or leaves Medicare.

However, that does not mean that you shouldn’t review your coverage each year. Have your finances or your healthcare needs changed? Has your plan changed its benefits or costs? Ask these questions every year to make sure you’re still getting the coverage you need.

New to Medicare

How to Make Medicare Plan Changes

You can enroll in a new Medicare Advantage plan by getting help from a licensed agent. If you haven’t enrolled in Original Medicare yet, be sure to do that first by contacting Social Security either online or at 1-800-772-1213. You can also visit your local Social Security office.

To get in touch with a licensed agent in your area, click here or call us at (833)-567-3163.

7 Common Medicare Mistakes to Avoid

Choosing the right Medicare plan for you can seem daunting. You may be confused about what plan to buy or frustrated that you can’t find the information you need to make a sound choice.

You don’t want to potentially be stuck paying huge penalties or have a plan that doesn’t work for you. However, if you have the right knowledge, you can steer clear of the hassle that comes with these seven common Medicare mistakes to avoid.

1. Waiting Until It’s too Late to Sign up for Medicare

Medicare Late Enrollment Penalty | Medicare Plan Finder

If “timing is everything,” that goes double for Medicare enrollment. One of the most common Medicare mistakes to avoid is putting off enrollment until it’s too late. Many people know that you can enroll in Medicare when you’re 65, but what they might not know is that you can actually start the process when you’re 64. The three months before your 65th birthday, the three months after your birthday, and your birthday month is what’s called the Initial Enrollment Period (IEP).

You can avoid costly penalties if you sign up during your IEP. If you sign up to late your Medicare Part B premium may go up 10 percent for each year that you could have been covered but didn’t enroll.

The IEP doesn’t apply to everyone. For example, people with certain chronic conditions or people who’ve received SSDI benefits for at least 25 months may be eligible for a lifelong Special Enrollment Period (SEP). If you qualify, your lifelong SEP will allow you to make changes to your coverage once per quarter for the first three quarters of the year.

People who go through certain life changes such as losing coverage upon retirement or losing a spouse’s coverage can sign up for Medicare during a temporary SEP, which allows you to enroll late without paying a penalty. However, a circumstantial SEP is only for eight months after you stop receiving employer coverage, so it’s crucial that you enroll during that time frame.

3. Thinking You’re Covered Just Because Your Spouse Has Coverage

Employer insurance plans usually come with an option that covers you and your spouse. Medicare does not work that way. You and your spouse each need an individual plan.

This is actually a good thing. When you were younger, it probably made more sense to not deal with multiple insurance carriers. However, as you age, you become more susceptible to certain illnesses, and you may have different needs than your spouse. You may need more or less covered services.

For example, you might only need to visit your doctor every once in a while for wellness exams or the occasional sickness. However, your spouse may need to look into enrolling in a special type of plan called a Chronic Special Needs Plan (C-SNP) because of a chronic illness.

4. Not Using the AEP to Make Changes or Enroll in New Plans

If you don’t take advantage of the Annual Enrollment Period (AEP), which is October 15 – December 7, you could be stuck with a plan that doesn’t fit your needs for another year.

For example, if you only have Original Medicare and you want to capitalize on the supplemental benefits Medicare Advantage plans can offer, AEP is your window of opportunity.

5. Assuming Medicare Is Unaffordable

Some people may put off enrolling in Medicare because they think they can’t afford it.

While Medicare isn’t free, many people can get premium-free Medicare Part A. You will not owe a Part A premium if you or your spouse has worked and paid Medicare taxes for more than 40 quarters.

Even though you may have to pay premiums for Part B and other Medicare coverage, there is help available. If you have a limited income, you may be able to find assistance through certain Medicare programs such as Medicare Savings Programs, Low Income Subsidy Extra Help, and state Medicaid programs.

Medicare Savings Programs (MSPs): These programs can help pay the Part B monthly premium and help out with coinsurance fees, depending on the program. (There are currently three types of MSPs).

Low Income Subsidy (LIS) Extra Help: This federal program can help pay for the costs associated with Medicare Part D prescription drug coverage.

State Medicaid Programs: This program is funded by both federal and state resources. Medicaid provides medical assistance for people with low incomes and few assets. All Medicaid programs provide certain coverages such as prescription drugs.

Free Prescription Discount Card

People who qualify for MSPs or LIS may also qualify for Medicaid. If you’re eligible for both Medicare and Medicaid, you can enroll in what’s called a Dual Special Needs Plan (DSNP). A DSNP may help pay for most or all of your healthcare costs.

6. Thinking Medicare Covers Everything

Common Medicare Mistakes to Avoid | Medicare Plan Finder

Original Medicare (Part A and Part B) is a great resource for helping out with healthcare costs, but it doesn’t cover everything. Medicare Part A covers inpatient services at hospitals. Medicare Part B covers outpatient services such as doctor’s appointments. Even with those services, you’ll still owe your monthly premium and coinsurance if you see your doctor. For example, the fee for Part B services is usually 20 percent of Medicare-approved costs.

Original Medicare doesn’t cover many services people need such as vision, hearing, and dental care. The Centers for Medicare and Medicaid (CMS) allows private insurance plans called Medicare Advantage (MA) plans to provide those services.

Not every plan in every location offers those extra services, so it’s a good idea to talk to someone who can help you find the plans available in your area if those services are important to you. A licensed agent with Medicare Plan Finder can help you determine what type of Medicare plan is right for you.

For some people, Medicare Advantage plans may not make sense, but they still need more coverage than Original Medicare provides. Some people may only need help with financial items such as coinsurance fees. Those people might benefit most from a Medicare Supplement (Medigap) plan. While MA plans help cover healthcare services, Medigap plans only cover costs.

Find Medicare Plans | Medicare Plan Finder

7. Not Understanding What You Have to Pay out of Pocket

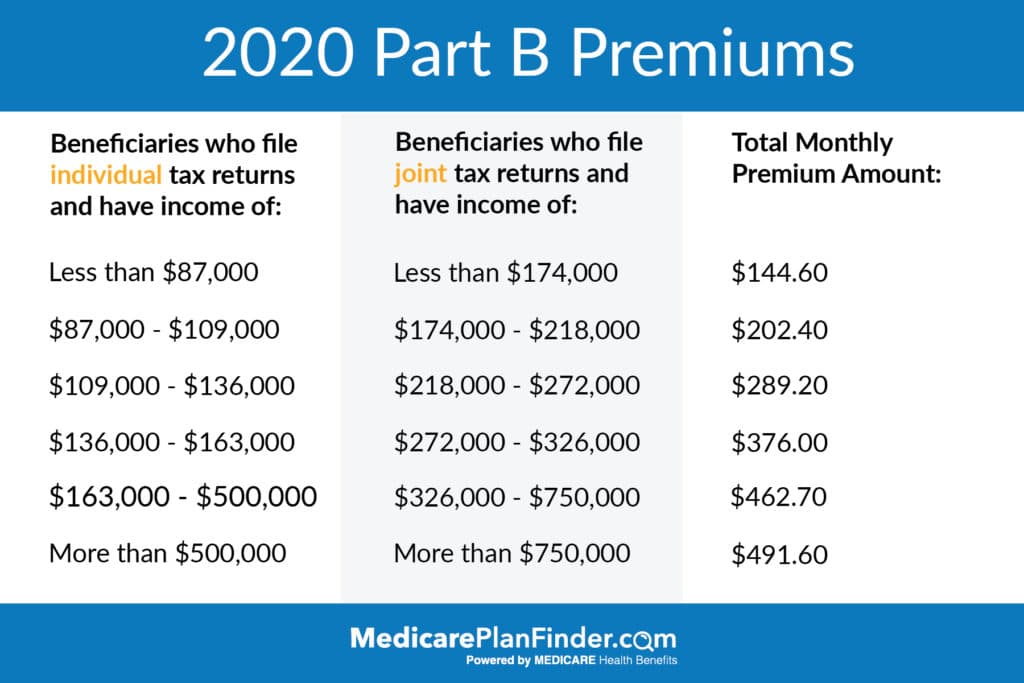

Even if you enroll in a Medicare Advantage or Medigap plan, you may still owe monthly premiums. That means that even though your Medicare Advantage plan may have a $0 premium, you may also have to pay the Part B premium, which is $144.60 in 2020 (unless you have high income).

2020 Medicare Part B Premiums

You may also have to pay a deductible before your coverage starts. The Part B deductible in 2020 is $198. Your MA or Part D plan may also require you to pay a deductible.

You may also have to pay copays or coinsurance. You may owe a copay, which is a fixed amount you pay for services such as doctor’s appointments with many MA plans. Coinsurance is a percentage of covered services. Original Medicare pays about 80 percent of approved costs and you are responsible for the other 20 percent. Your cost sharing for covered services may be different if you’re enrolled in a MA or Medicare Supplement plan.

Let Us Help You Avoid Common Medicare Mistakes

Medicare can be confusing. You might not know what coverage you need or what type of plan fits your budget and lifestyle. A licensed agent with Medicare Plan Finder can show you what’s available in your area and help you choose the best plan for you. Your agent is familiar with the common Medicare mistakes to avoid and help you take the right steps. To schedule an appointment, call 844-431-1832or contact us here today.

Contact Us | Medicare Plan Finder

How to Protect Yourself from Medicare Scams, Fraud, and Abuse

The Annual Enrollment Period (AEP) will be here before you know it. AEP is the most popular time of year for beneficiaries to change or enroll in a new plan. However, this means Medicare scams, fraud, and abuse are at all all-time high. Medicare Plan Finder makes understanding these risks easy, so you feel protected year-around.

Medicare Fraud and Abuse

The government loses millions of dollars each year due to Medicare fraud and abuse. This causes Medicare prices to increase. The government has created laws to protect all parties involved in Medicare and Medicaid.

These laws promote healthy relationships between agents, carriers, and clients to prevent the insurance industry from becoming profit-based, instead of care-based. Your coverage should be more important than profits.

Medicare fraud includes:

Knowingly making false claims or misrepresenting data

Intentionally giving or receiving rewards for goods and services

Promoting one health service over another

Billing Medicare for appointments that never happened or for more than what actually happened

Medicare abuse includes:

Billing for unnecessary services

Excessive supply purchases

Misusing codes

Learning about Medicare Scams | Medicare Plan Finder

Medicare Fraud and Abuse Laws

The government has implemented the following:

False Claims Act (FCA) – Protects the government from being overcharged on goods or services. No proof of intent is required.

Anti-Kickback Statute (AKS) – Agents cannot knowingly reward referrals for health care programs.

Physician Self-Referral Law (Stark Law) – Doctors cannot make referrals to health care companies in which they have an interest.

Criminal Health Care Fraud Statute – Cannot defraud; bill for unnecessary medical goods and services (like drugs that are not needed or wheelchairs for those who are not impaired).

What Can You Do?

Don’t become a victim! If you aren’t sure about a health agent’s validity, ask for licensing information or work with Medicare Plan Finder. To help fight Medicare fraud and abuse, report any suspicious activity to 1-800-HHS-TIPS (1-800-447-8477). You can also report the activity online.

Plan Finder Tool | Medicare Plan Finder

Common Medicare Scams

A licensed Medicare agent is required to abide by strict rules when contacting seniors and Medicare beneficiaries. It is illegal for anyone (including an authorized Medicare agent) to show up at your front door without permission.

Also, keep in mind that no one associated with Medicare will ever call you to update your information. The following are common Medicare scams you need to look out for:

Grandparent Scam

One recent scam involves adults calling the elderly and pretending to be their grandchildren asking for money. They’ll say that they are in some form of trouble and need money.

To avoid this grandparent scam, be sure to ask for a personal detail that only your real grandchild would know the answer to. It is easy to assume you would recognize their voice, but if someone calls in a panic, your adrenaline may kick in, and their voice is the last thing you’re worried about.

Medicare Coverage Helpline Scam

In recent years, there has been a television commercial targeting current Medicare beneficiaries. The advertisement is from the “Medicare Coverage Helpline” and claims that if you have parts A and B, you are eligible for vision, dental, and prescription drug plans due to a recent Medicare health reform.

The commercial will provide a 1-800 number. Do not call that number. If you are interested in vision, dental, or prescription drug coverage, one of our licensed agents can discuss plans that are specific to your area. To get started, click here.

Medicareplans.com Scam

Medicareplans.com is an out-dated link that was a fake marketplace for those searching for a Medicare plan. While this link is no longer active, it is important to be careful when reviewing different companies and websites.

Look for websites that start with “https” instead of “http.” The “s” indicates a secure website. If you have doubts, a simple google search like “[Insert Company Name Here] Scam” can show any potential scam information.

Medicare Phone Scams

Medicare phone scams are probably the most common way that seniors and other Medicare beneficiaries are taken advantage of. In some cases, a scammer may call you and pretend to be from Medicare and offer you free services if you provide your Medicare number or Social Security number.

In other cases, a scammer who claims to be from Medicare may say that they need to validate your information to keep you from losing your benefits. The real Medicare program will never ask for this information. Never give these numbers away over the phone.

One phone scam in particular, the “can you hear me” scam, is easy to fall victim to. The scammers use this question to get a “yes” answer from people, which they would then edit to make it seem as though they were agreeing to purchase a product or submit information. If you answer the phone and someone you don’t know asks, “Can you hear me?” hang up right away.

Medicare Refunds

Scammers will often try to catch your attention by saying you have Medicare refunds. The scammer’s goal is to get your bank information. Common reasons for Medicare refunds include changes or enhancements to Medicare or lawsuits with private insurance companies.

If for some reason you are entitled to a Medicare refund, a check will be mailed to you directly. No one will ever call asking for your bank information.

How to Avoid Medicare Scams

Medicare scams can be easily avoided. CMS (Centers for Medicare and Medicaid Services) suggests the following tips for avoiding scams and fraud:

Treat your Medicare card like a credit card. Keep it in a safe spot and never give out your number to anyone other than your doctors.

Do not accept an offer for free gifts or money in exchange for your Medicare information.

Don’t accept services that aren’t usually covered by Medicare unless a doctor that you trust tells you that it is necessary.

Will Medicare Ever Call You?

Medicare will never call you randomly and ask personal questions. If you are already covered by Medicare, they have all the information they need. If someone from Medicare needs to contact you, they will find a more official communication route.

If you have any additional questions about Medicare communication, or if who is contacting you is legitimate, contact a Medicare customer service representative at 1-800-MEDICARE (1-800-633-4227).

Medicare Scams | Medicare Plan Finder

Free Stuff for Seniors From the Government

Seniors and Medicare beneficiaries can fall into specific categories that scammers will use to their benefit. Scammers will sometimes call pretending to be from the government and offer free health checkups or free medical supplies.

During these fake calls, they will use common senior health conditions to act like they know specific details about your health. The scammer has no idea you have diabetes or high blood pressure; all they know is that a handful of seniors have those conditions. Scammers are hoping you will also fall into that category.

Some scammers have been known to give names and addresses of your doctor. It is unknown how they receive this information. Even if the caller ID looks reputable, don’t trust them so quickly.

Technology has continued to evolve and faking caller ID has become easier and easier. Don’t trust if someone says they are providing free products or services from the government. Scammers will say all you have to pay for is shipping costs, then get access to your credit card information.

How to Stop Medicare Phone Calls

As we mentioned, Medicare will not call you without your permission. If you receive a phone call about your Medicare plan, but did not consent to a call, it is likely a scam.

To help prevent calls from unknown numbers, don’t answer unknown numbers unless you’re expecting a call from a legitimate company (like us!). You will receive a voicemail if the call is legitimate.

If you have a smartphone, you can download apps that detect scam calls and block the calls instantly. You can also put your number on the National Do Not Call Registry.

How to Block Specific Numbers

Both iPhone and Android users can block specific numbers from calling. This is a useful tool because many scam callers will cycle through phone numbers. Once you block a number, you will not receive calls from that number unless you unblock it.

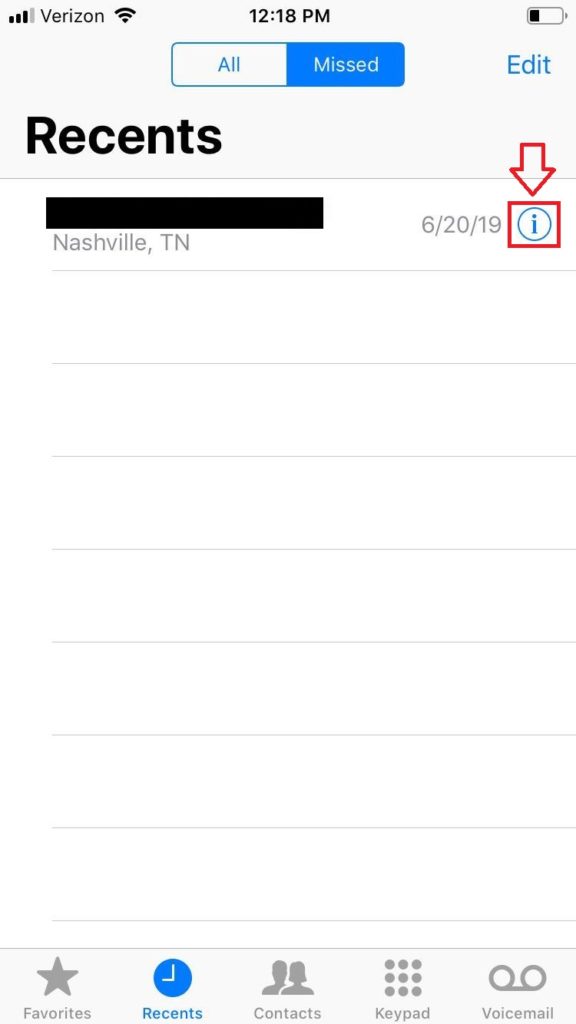

How to Block Phone Numbers on an iPhone

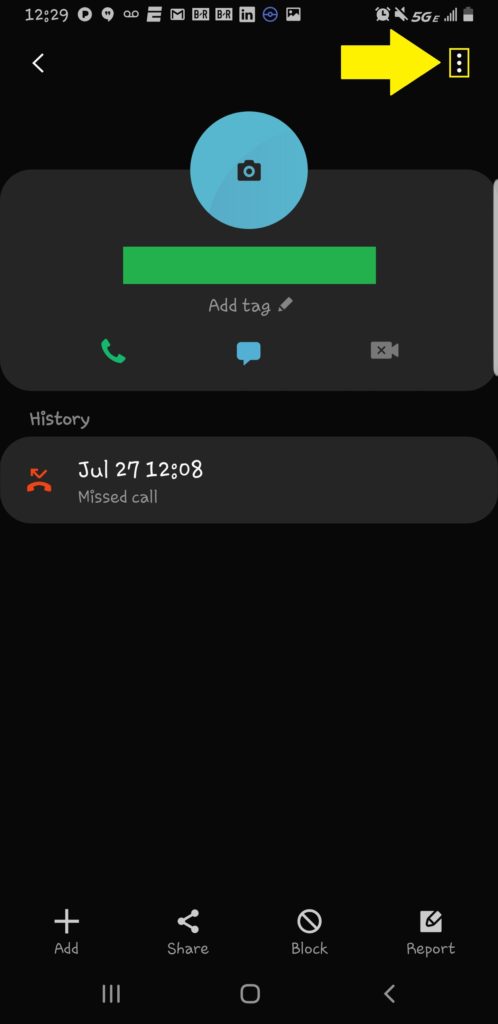

First go to you to your most recent calls. Then find the number you want to block and tap the “i” icon. That will lead you to the contact information associated with that phone number.

That will lead you to your most recent calls. Then find the number you want to block and tap the “i” icon. That will lead you to the contact information associated with that phone number.

How to Block Phone Numbers on an iPhone Step 1 | Medicare Plan Finder

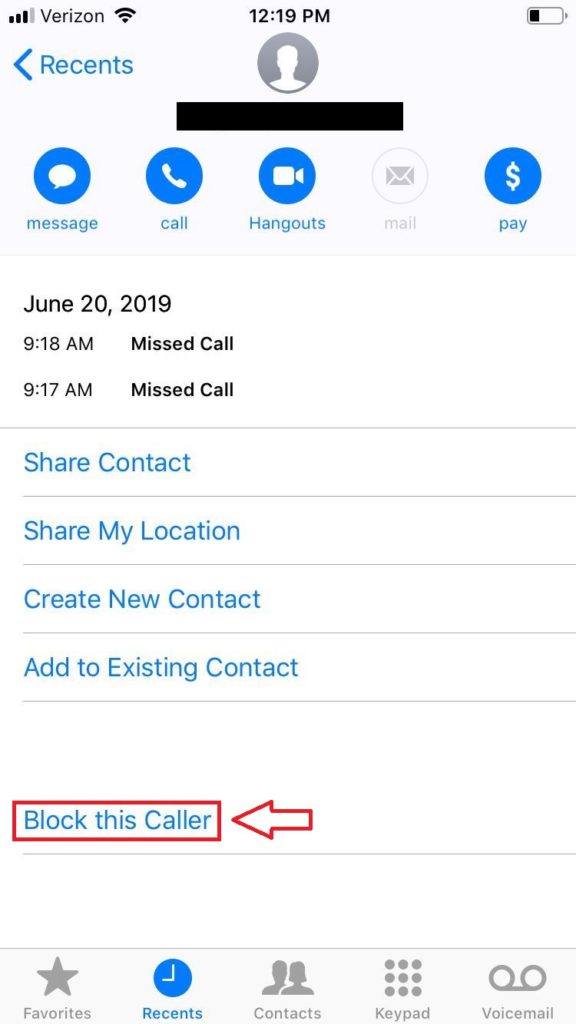

Then scroll down to where you see “Block this Caller” and tap on the words.

How to Block Phone Numbers on an iPhone Step 2 | Medicare Plan Finder

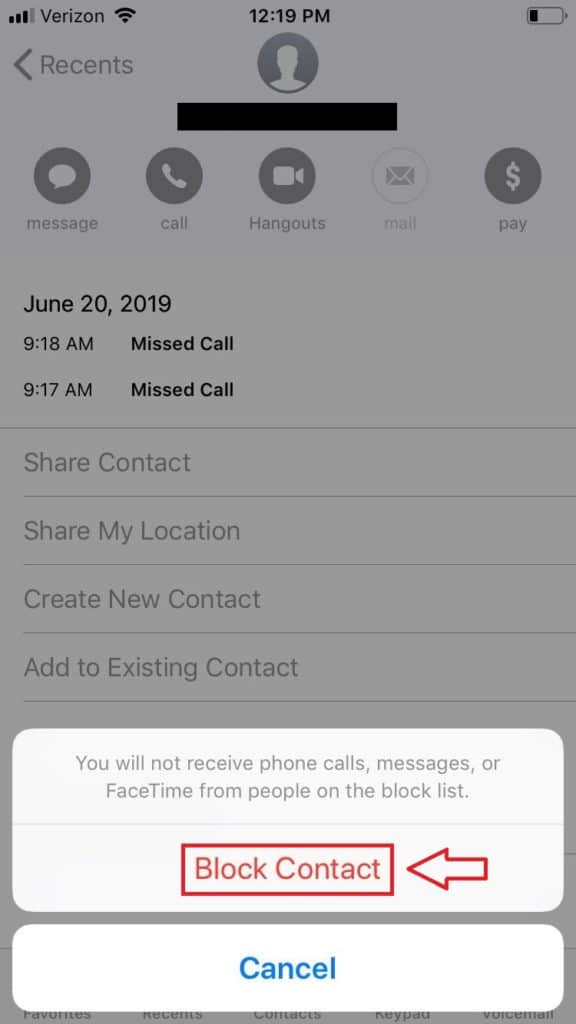

The final step is verifying that you want to block the caller.

How to Block Phone Numbers on an iPhone Step 3 | Medicare Plan Finder

How to Block Phone Numbers on an Android

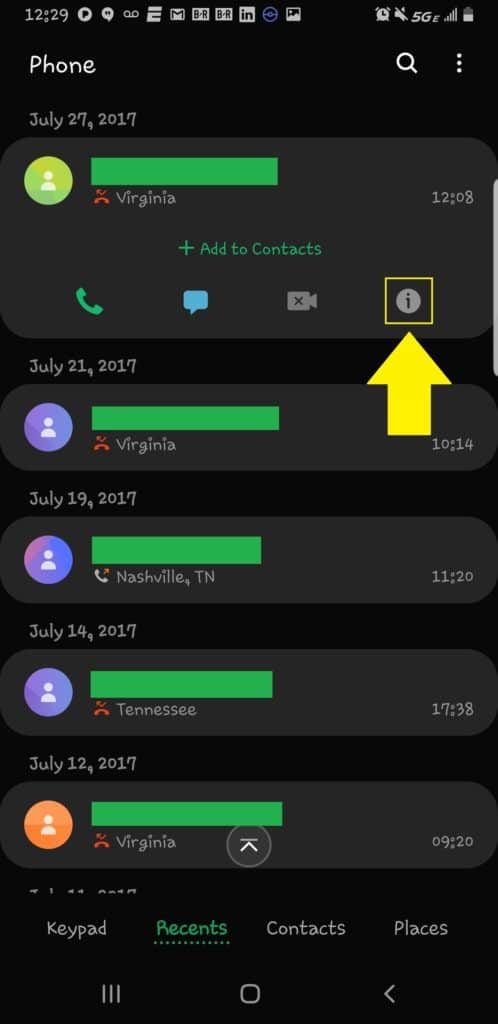

First, go to your most recent calls. Then tap the “i” icon under the phone number you want to block.

How to Block Phone Numbers on an Android Step 1 | Medicare Plan Finder

Then tap the three dots as shown below.

How to Block Phone Numbers on an Android Step 2 | Medicare Plan Finder

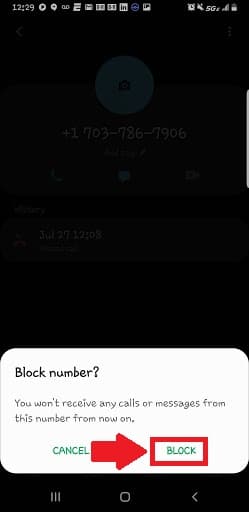

Then select “Block.”

How to Block Phone Numbers on an Android Step 3 | Medicare Plan Finder

Medicare Helpline

Protecting yourself from Medicare scams may seem like an impossible task. Now that you understand the common Medicare scams you will know what to watch out for.

If you are ever suspicious or have questions regarding Medicare fraud, call the Medicare Helpline. They can answer any questions you may have. The Medicare Helpline is a 24-hour toll-free line and can be reached at 1-800-MEDICARE.

Also, you can help eliminate Medicare fraud by reporting suspicious activity. Call the Medicare fraud line at 1-800-447-8477 or report the incident online.

Enroll in Medicare

The risks of Medicare scams does not lower the importance of proper Medicare coverage. We are dedicated to helping you choose the best plan from all of the options available in your area. Why do we need your information?

Zip Code: We need this because Medicare plans are different in every zip code.

County: We ask for your county because sometimes zip codes fall into more than one county.

Email and Phone Number: We ask for your contact information because we want to have a conversation with you about helping you find a great health plan.

Birthday: Sometimes we’ll ask for your birthday to help us ensure that you qualify for Medicare benefits.

Medicare Plan Finder and other legitimate resources will not ask for your Social Security Number or Medicare number before speaking with you. If someone who you do not know asks for your SSN or Medicare number, do not give out that information until you know that it is safe to do so.

We are here to discuss the best Medicare coverage for your needs and budget. If you’re interested in speaking with a licensed Medicare agent or scheduling a free no-obligation appointment, fill out this form or call us at 844-431-1832.

This blog was originally published on 10/1/18, and was updated on 8/21/19.

A Guide to Medicare Chronic Lung Disease Coverage

Chronic lung diseases affect millions of people in the United States. It falls under the fourth leading cause of death. Thankfully, the Centers for Medicare & Medicaid Services (CMS) considers chronic lung disorders to be one of the qualifications for a Medicare Special Needs Plan.

As you age, it’s easy to brush off symptoms as “part of the aging process.” You might even purposely ignore certain symptoms because they “aren’t that bad,” and you don’t want to pay for treatment – but your symptoms could be indicative of a bigger problem and should not be taken lightly.

If you are diagnosed with chronic lung disease, you may qualify for a Medicare Special Needs Plan that can save you thousands of dollars in doctor visits and treatment costs. Qualifying for a Special Needs Plan means you will also qualify for a Special Enrollment Period, which allows you to change plans more often.

Let’s take a look at what all of this might mean for you.

What Is Chronic Lung Disease?

Doctor and Nurse Discussing Chronic Lung Disease With Patient | Medicare Plan Finder

Chronic lung disease refers to any condition that causes long-term obstructions to a person’s airways. They can cause the following symptoms:

Shortness of breath after little or no physical exertion, or shortness of breath after normal exercise plus a brief rest period

A persistent cough – one that lasts longer than a month

Mucus or sputum production lasting a month or longer

Labored breathing

Swollen feet, ankles or legs

Blue lips

If you experience any of these symptoms, you should talk to your doctor immediately. Chronic lung disease can severely impact your quality of life and shorten your lifespan considerably. The faster you get started on treatment, the better.

SEP-Qualifying Disabilities

To qualify for a SEP (Special Enrollment Period) due to a disability or disease, your condition must be “severe or disabling.” The list of chronic lung diseases below would automatically qualify you for a SEP because you would be eligible for a Medicare Special Needs Plan, or SNP.

Once you qualify for a Special Enrollment Period, you won’t be restricted to the Annual Enrollment Period (AEP) anymore.

Usually, AEP is the only time of year that Medicare beneficiaries can switch Medicare Advantage plans. It only lasts from October 15 through December 7. Those with a SEP are eligible to make one change per quarter (January – March, April – June, July – September). The fourth quarter is excluded because you’ll be able to switch like everyone else from October 15 through December 7 (the Annual Enrollment Period).

Chronic Lung Diseases List

The Centers for Medicare & Medicaid Services (CMS) specifically defines the following lung disorders as chronic lung diseases that could make you eligible for a Medicare Special Needs Plan:

Asthma

Chronic bronchitis

Emphysema

Pulmonary fibrosis (PF)

Pulmonary hypertension

Lung cancer is a qualifier as well (though it is listed in the “cancer” category instead of “chronic lung disorders.”

Severe COPD as a Qualifying Disease

You might be wondering, “what about severe COPD? Does Medicare cover COPD?” Medicare Part B can cover COPD diagnosis and treatment.

To begin, Medicare Part B covers your doctor’s visits at 80%. Start by asking your doctor about COPD and getting tested. Then, Part B also will cover a comprehensive pulmonary rehabilitation program for moderate to severe COPD (chronic obstructive pulmonary disease). If your doctor offers this treatment, you will only owe 20% of the Medicare-approved amount with Part B (after the Part B deductible). If you are hospitalized, your treatment will fall under Part A, and you may owe a hospital copayment.

Emphysema and bronchitis are forms of COPD, so a COPD diagnosis may mean that you also qualify for a Special Needs Plan (SNP) and a Special Enrollment Period. In that case, you may be able to get even more coverage.

SNP plans often come with care coordination. That means no more confusing phone calls and mixed messages between all your different doctors!f

What Chronic Lung Disease Treatments Will Medicare Cover for COPD?

Two main diseases fall under the term COPD: chronic bronchitis and emphysema. There currently is no cure for COPD. Early detection can help you manage your symptoms and continue to live a “normal” life with COPD.

One of the main things to keep in mind when living with COPD is that seemingly small things like seasonal allergies or air pollution can cause serious exacerbations. It’s important to take every small infection or symptom seriously.

COPD Oxygen Therapy

People with COPD may have low blood oxygen levels, which is called hypoxia. Supplemental oxygen, or oxygen therapy, can help prevent heart failure and improve quality of life in COPD patients.

Some people may need long-term oxygen therapy 24 hours per day. Others may only need supplemental oxygen during exercise, sleep, or air travel.

You can get oxygen therapy in three ways:

Oxygen concentrators

Oxygen-gas cylinders

Liquid-oxygen devices

Remember that you cannot smoke or stay near an open flame while using any of these devices.

Medicare Part B will cover your device as well as any accessories (like mouthpieces or tubing), maintenance, repairs, and the oxygen itself. You will only be responsible for 20% of the costs with Part B.

Uniquely, Medicare requires a five-year obligation with whichever company you use to rent your oxygen equipment. After five years, you will be able to rent new oxygen equipment from a separate provider.

COPD Prescription Drugs with Medicare Health Insurance

While no prescription can cure COPD, there are several that can help you manage your discomfort. Some examples may include:

Bronchodilators (in an inhaler; relaxes the airway muscles)

Inhaled steroids (reduce inflammation)

Phosphodiesterase-4 inhibitors (reduces inflammation and relaxes the airway muscles)

Sometimes, when patients have severe emphysema or severe COPD, doctors may recommend surgery. There are three COPD surgeries:

Lung Volume Reduction: Small portions of damaged tissue are removed from the upper lungs, creating extra space so that your diaphragm is more productive. The procedure is minimally invasive. A small valve is placed in the lung.

Bullectomy: Bullae (large air spaces) are removed from the lungs to improve airflow.

Lung Transplant: A lung transplant comes with huge risks, but can also have huge rewards. This procedure requires that you meet specific criteria outlined by your doctor. After a lung transplant, you’ll need to take immune-suppressing medications for the rest of your life.

Medicare coverage for your surgery would fall under Part A, but you’ll still have copayments and a deductible. Some Medicare Advantage plans might provide more coverage.

COPD and Medicare Supplement

A Medicare Supplement (also called Medigap) plan can be a great way to cover the extra costs associated with COPD. However, most people will find that a Medicare Advantage plan is better for COPD than a Medicare Supplement. That’s because you cannot be denied for Medicare Advantage based on preexisting conditions. However, you can be denied Medicare Supplement coverage.

There are two times when you can get a Medicare Supplement plan without medical underwriting. One is when you’re signing up for Medicare health insurance for the first time, and the other is if you lose your current coverage due to no fault of your own and need a new plan.

Lung Cancer Screenings

If you’ve been diagnosed with COPD, your doctor may recommend annual lung cancer screenings, because about one percent of COPD patients develop lung cancer. Medicare Part B covers yearly lung cancer screenings with Low-Dose Computed Tomography (LDCT) if you meet one or more of the following conditions:

You’re 55-77 years old

You don’t display any lung cancer symptoms

You smoke currently or quit smoking within the past 15 years

In the past, you smoked at least one pack per day for 30 years

A doctor orders the screening

Inhalers Medicare Will Cover