Save Money on Prescription Drugs with Discount Cards

Do you have a high deductible or copayment for prescription drugs? Or maybe you’ve been prescribed a medication that isn’t covered by your insurance? Don’t worry, prescription discount cards could be the budget-friendly solution you need to cut down on costs.

What Are Prescription Discount Cards?

Prescription discount cards are offered through networks designed to help consumers save on medications. These cards are free, easy to use, and widely accepted at thousands of pharmacies nationwide. They can provide significant discounts on both brand-name and generic drugs, even for those without insurance.

Many of the top-rated prescription discount cards can be sent directly to your email or phone for immediate use.

By comparing available options and learning how these programs work, you can maximize your savings and make informed decisions about your prescription costs.

Why Consider Prescription Discount Cards?

Here are some key reasons why prescription discount cards are worth exploring:

Immediate Savings: You could save up to 80% or more on the retail price of prescription medications.

Ease of Use: Present your card at participating pharmacies and instantly access discounts.

Accessibility: These cards are free, require little to no personal information, and are available to everyone.

Versatility: Many programs also offer discounts on pet medications.

How Do They Work?

When you use a prescription discount card, the savings come from negotiated rates between pharmacies and pharmacy benefit managers (PBMs). PBMs act as middlemen, working to secure lower prices on drugs for consumers. This process often results in significant cost differences for the same medication at different pharmacies, so it’s essential to compare prices.

The Truth About Prescription Discount Cards

It’s normal to feel cautious about something that sounds too good to be true, especially when Medicare scams and other healthcare-related frauds are on the rise. Here’s how to identify legitimate prescription discount cards:

Clear Pricing Tools: Legitimate programs let you compare drug prices for both brand-name and generic medications online.

Pharmacy Acceptance: Ensure the card is accepted at your preferred pharmacies.

No Strings Attached: Reliable programs don’t require you to provide sensitive personal information.

Transparency: Discounts are consistent and comparable to other trusted programs.

Best Prescription Discount Cards in 2026

Not all prescription discount cards are created equal. Some may offer greater savings on specific medications or have more participating pharmacies in their network. Here are some of the top options to consider:

1. GoodRx

GoodRx is one of the most popular discount programs, allowing you to compare prices across 70,000+ pharmacies in real-time. The app provides coupons that can save you up to 80% on medications. Simply print, email, or text the coupon to yourself and present it at the pharmacy.

2. SingleCare

SingleCare offers a free prescription discount card that works at major pharmacies like CVS, Walmart, and Walgreens. Discounts can be as high as 80%. The program is user-friendly and doesn’t require personal information.

3. US Pharmacy Card

This free card is accepted at more than 59,000 pharmacies nationwide. It’s especially versatile, offering discounts on pet medications too. Cards can be printed, emailed, or texted directly to you.

4. Discount Drug Network

With potential savings of up to 85%, this card is another great option. It requires minimal information to sign up and offers a robust pricing tool for easy comparisons.

How to Use a Prescription Discount Card

Find a Participating Pharmacy: Popular options like Walmart, Walgreens, CVS, and Rite Aid often honor prescription discount cards.

Present Your Card: Show your card or coupon to the pharmacist when you pick up your prescription.

Compare Prices: Use online tools or mobile apps to compare prices before you head to the pharmacy.

Real-World Example: How Much Can You Save?

Let’s take the example of rosuvastatin (Crestor), one of the most commonly prescribed medications in the U.S.

Retail Price: $161.64 for a 30-day supply of 20 mg tablets (without insurance).

Discounted Price: With GoodRx, you could pay as little as $8.44 at Walmart.

That’s a massive saving of over $150 — just by using a free prescription discount card!

Prescription Discount Cards and Medicare

Navigating Medicare and prescription drug coverage can feel overwhelming. Fortunately, a licensed agent can help you understand your options, whether you’re looking at Part D plans, Medicare Advantage, or supplement plans.

If you’re interested in learning more, schedule a no-cost, no-obligation appointment with one of our licensed agents today. Call us at (833)-567-3163 or fill out our online form.

Final Thoughts

Prescription discount cards can be a game-changer for anyone looking to reduce their medication costs. Whether you’re uninsured, underinsured, or simply looking for a way to save, these programs provide an easy and effective solution.

Take the first step toward savings today. Explore your options, download a card, and start comparing prices at your local pharmacies.

How do I get a New Medicare Card?

When you first enroll a Medicare, you’ll receive a “Welcome to Medicare” packet in the mail with your Medicare card.

If your Medicare card is lost, stolen, or damaged, you’ll need to request a replacement card immediately through Social Security. Be sure to request a new card quickly so that you don’t have to wait for coverage at your next doctor’s appointment.

Your doctor might be able to look up your Medicare number, but it will be easier and faster if you can present your card.

When you use the online service, you should receive your Medicare card in the mail within 30 days. It will be automatically shipped to the address on file with Social Security, so make sure the address in your account is correct.

If you get your Medicare benefits through the Railroad Retirement Board, you’ll want to contact them directly:

1-877-772-5772 (TTY 1-312-751-4701, M-F, 9 AM to 3:30 PM)

Your local RRB office

What to do if you Lose Your Medicare Card

Have you lost or misplaced your Medicare card? A lost Medicare card can be very dangerous as it contains your social security number. Losing your Medicare card is similar to losing your social security card. That’s why starting this year, new Medicare cards will be slightly different. We’ll discuss that and show you a new Medicare card image in a bit.

If you need to order a new Medicare card because of a lost Medicare card or changed information (like if you change your name or address), your first step should be to contact Social Security and let them know. You can also print a copy of your Medicare card by signing into My.Medicare.gov (you may need to create an account). If you still have your old Medicare card or if you find your lost Medicare card, be sure to cut it up and throw it away so that no one can steal your information.

What is a Medicare Card

When you enroll in Medicare for the first time, you’ll receive a red, white, and blue Medicare card in the mail. If you are automatically enrolled in Medicare Part A, you will receive your plastic Medicare card about three months before your 65th birthday so that you will already have it when your plan becomes active.

Your plastic Medicare card proves that you have Medicare health insurance and will tell providers (doctors, pharmacists, hospitals, etc.) what type of coverage you have and what day your coverage begins. You should keep your plastic Medicare card with you at all times so that if you have to see a doctor for any reason, you can prove that you have Medicare coverage and avoid being overcharged.

New Medicare Cards 2018

In 2017, CMS (Centers for Medicare and Medicaid Services) decided to launch a new version of the red, white, and blue Medicare card. The big change is that instead of having your Social Security number plastered on your card, you’ll be assigned a Medicare number.

You should treat your “MBI” or Medicare beneficiary identifier number the same way you treat your Social Security number – don’t give it out unless you know it’s necessary and you trust the person you’re giving it to. However, it is much safer to carry a card with your Medicare number than your Social Security number!

Everyone should have received a new Medicare card by early 2019. The last batch was reportedly shipped in October 2018. If you never received one, be sure to contact Social Security right away (or ask your insurance agent for help).

The new plastic Medicare cards will not affect your benefits – it will only protect your security.

Unlike the old plastic Medicare card you may have, new Medicare cards will not be plastic. They will be made of paper to make it easier for providers to use and make copies. We recommend purchasing a cheap plastic cover for your Medicare card. You can buy a pack of card covers (like these) in bulk on Amazon or stop by your favorite local office supplies store, like Staples or Officemax.

If you have questions about your Medicare plan or these new Medicare cards, call your agent! If you don’t yet have an agent, call us at (833)-567-3163.

Avoiding Medicare Card Scams

Scammers might try to get your Medicare number from you. Remember that Medicare will never call and ask you to verify your number – they already have that information. If someone calls you and asks for your Medicare number, and you weren’t expecting them to call, do not give it to them. The only people that should need your Medicare number are your doctors, your insurance agents, and your private health plan (if you have one).

Here are some tips for protecting your identity in regards to your new Medicare card:

A Medicare employee will never call and ask for your social security number or banking information. If someone does call you asking for that information, it may be a scam. Do NOT give out your social security number to someone who claims to be calling from Medicare unless you know you can trust the person on the line.

If someone asks you to pay for a Medicare card, it is a scam. Medicare cards are always free and you should receive one automatically when you enroll.

If someone tells you that your benefits will be revoked if you do not give information or money, it may be a scam. The only people that should ask you for money are your doctors or your plan’s billing department. Be sure to always know who you are talking to.

In fact, click through to our guide on Medicare scams to learn how to block unknown scam callers on your phone. Read about common scams to look out for so you can be as prepared as possible.

*This post was originally published on 9/7/17. It was last updated on 1/15/2025.

Winter Wellness Tips for Seniors and Medicare Eligibles

Winter often consists of lower temperatures, less sunlight, and more time indoors. The same weather that is bothersome to most can prove to be dangerous for others.

Winter Safety Tips for the Elderly

love, winter holidays and people concept – happy senior couple with takeaway coffee at christmas market on town hall square in tallinn, estonia

Seniors and Medicare eligibles face several dangers including falling on ice or snow, frostbite, and hypothermia. Use these winter wellness tips to help ensure you are healthy, safe, and able to enjoy the holidays with your friends and family.

Falling on Ice or Snow

According to the Centers for Disease Control and Prevention, falls are the leading cause of injury and death in older adults. Fall prevention is important outside and in your home, but snow and ice can easily blindside you. Tips to protect yourself from falling on ice or snow include:

Understand the side effects of your medications. Some medicines can cause dizziness or vision issues, so be cautious when leaving your home.

Wear weather-appropriate shoes. Make sure your shoes are the right size and have good traction.

Allow extra time when commuting to your destination. Don’t rush when you’re walking and take small deliberate steps.

Use sand or cat litter on sidewalks or walkways.

When going inside, wipe your feet off before you enter. Wet shoes can cause you to slip on dry surfaces.

Keep your hands free whenever possible. If you are carrying bags, take several trips so you do not overload yourself. Always ask for help if possible.

Have emergency numbers stored in your phone. Take your phone whenever you leave the house, even on short trips to your car or mailbox. If you fall, you can easily access your phone and call for help.

Frostbite and Hypothermia in the Elderly

As temperatures drop, there is an increased risk of frostbite and hypothermia in the elderly. Frostbite and hypothermia are a result of cold weather and can be difficult to notice. Understanding the differences, warning signs, and symptoms are important when practicing winter wellness.

Frostbite occurs when your skin is exposed during extreme winter conditions. The cold weather causes your tissues underneath your skin to freeze. Frostbite causes you to lose feeling in the exposed area, which is commonly your fingers, toes, nose, ears, cheeks, and chin. If your skin turns white or a grayish-yellow color, or feels firm or waxy, seek medical care immediately.

Hypothermia occurs when your body’s core temperature becomes abnormally low. Hypothermia in the elderly is more likely due to a decreased production of body heat.

Warning signs of hypothermia include shivering, exhaustion, confusion, memory loss, slurred speech, and drowsiness. If you are experiencing these warning signs, take your temperature if possible. If your temperature is below 95 degrees, seek medical health immediately.

Prevention is key to protect yourself from frostbite and hypothermia. Make sure your home is well heated and insulated and be sure to eat healthy foods to fuel your body.

If you need to go outside or travel for any given reason, check the weather, and if possible, avoid extremely low temperatures. However, if you must venture out, wear plenty of weather-appropriate clothing.

Senior Isolation in the Winter

Many seniors and Medicare eligibles may be unable to leave their home in the winter. This can lead to a lack of social interaction. Feeling isolated can disrupt sleep, raise blood pressure, increase the risk of depression, and lower your overall well-being. Tips to prevent isolation include:

Call, email, or FaceTime friends and family regularly.

Consider getting your meals delivered to encourage a healthy diet. Programs like Meals on Wheels are great options.

Reach out to friends, family, and neighbors.

If you really struggle with isolation, consider moving into an assisted living facility.

Fire Hazards

Home fires can start at any time but are more common in the colder months. It’s important to practice fire safety and have an emergency action plan in place. Here’s what you should remember:

Make sure you have smoke alarms in the appropriate areas of your home, especially near any sleeping areas. Test alarms regularly and have spare batteries on hand.

Never walk away from a room when cooking. Plus, you should always have a fire extinguisher handy.

Keep curtains and drapes away from any heat source.

Never leave a burning candle unattended.

If you have a fireplace, get it inspected annually.

Place space heaters in an area that is open and clear.

If you smoke, avoid smoking indoors and around oxygen tanks.

Seasonal Affective Disorder (SAD)

Seasonal affective disorder (SAD) is a type of depression that’s associated with changes in seasons. The disorder begins and ends at about the same time every year, with symptoms starting in autumn and continuing until spring.

Symptoms of SAD

SAD symptoms may include:

Feeling depressed most of the day almost every day

Loss of interest in activities you’d normally enjoy

Low energy

Having problems falling or staying sleeping asleep (or sleeping too much)

Changes in your appetite or weight

Feeling sluggish or irritable

Difficulty concentrating

Feeling hopeless, worthless or guilty

Frequent thoughts of death or suicide*

*If you or someone you love experiences thoughts of suicide, please call the National Suicide Prevention Lifeline at 1-800-273-8255.

Combat SAD With a Winter Fitness Plan for Retirees

Retirees and Medicare eligibles can fight SAD with a great fitness plan. According to Harvard Medical School, fitness is as effective as antidepressants in some cases. Although a gym membership with fitness classes may help, you can get a great workout at home. All you need is some dumbbells, resistance bands, or even a chair.

In some locations, going for a walk outside isn’t an option due to weather concerns. Have you considered going for a walk at the mall? Many indoor shopping centers open their doors to “mall walkers” before the stores open.

Winter Wellness and Medicare

Winter wellness is important in maintaining a healthy lifestyle through the holidays and into spring. However, it’s important to focus on your wellness year around. Medicare Advantage plans have additional benefits and coverage that can help you become the healthiest version of you!

Many plans offer hearing, dental, and vision coverage. Plus, some even offer fitness classes like through SilverSneakers®! If you’re interested in hearing more about these additional benefits or have any questions regarding your Medicare coverage, call us at 844-431-1832 or fill out this form to get in contact with a licensed agent.

This post was originally published on December 11, 2018, and updated on November 22, 2019.

Yoga for Seniors and Medicare Eligibles

Yoga for seniors and Medicare eligibles is an effective way to improve your mental and physical wellness. When some people think of yoga, they may picture complex poses with intricate twists. That image of an unattainable exercise may make the ancient practice seem intimidating.

However, yoga doesn’t have to be intimidating or unattainable. Yoga has many health benefits, and it can even be included in certain Medicare plans.

Health Benefits of Yoga for Seniors

Yoga combines physical movements, breathing, and meditation into one exercise. If you struggle with joint pain, balance issues, body stiffness, sleep issues, stress, or anxiety, yoga may be able to help! The health benefits of yoga for seniors and Medicare eligibles are as follows:

Balance and Stability

As you age, your risk of falling increases. Yoga focuses on slow and measured movements and the strengthening of your muscles. These exercises can help keep you upright and strong to avoid tripping or falling. Your focus, strength, and body alignment can all improve with yoga and increase your balance and stability.

Flexibility

At any age, stretching is important. Simple tasks, like tying your shoes, can quickly become difficult without proper daily stretching. Yoga allows you to increase your flexibility through each exercise.

Breathing

Respiratory limitations can be developed when our oxygen level begins to deplete. Studies have shown that after twelve weeks of yoga, many seniors and Medicare eligibles have seen significant respiratory improvement. Plus, the deep breathing exercises that encompass basic yoga sequences and poses can improve overall lung function in a low-impact environment.

Stress and Anxiety

Yoga for seniors and Medicare beneficiaries can help reduce stress and promotes mental clarity. Yoga is so much more than just “stretching.” It is a practice that requires both the mind and body. Meditation and relaxation are heavily incorporated. These exercises can help you be more mindful and aware of the present moment in time.

Yoga for Obese Seniors

According to the Mayo Clinic, yoga may be a “useful addition to an overall weight-loss plan.” You may not burn as many calories with yoga as you do with aerobic exercise, but it can help improve your self-esteem and overall mood.

Obesity can put excess stress on your joints, and yoga may be a safe form of exercise that may not cause additional pain.

If you want to do yoga, it may be a great addition to a comprehensive fitness program that includes aerobic activity such as cycling or walking.

Beginning Yoga for Seniors and Medicare Eligibles

Yoga doesn’t have to be intimidating. There are gentle yoga poses for seniors and Medicare eligibles and some poses incorporate chairs to help aid any balance or stability issues.

Gentle Yoga Poses for Seniors and Medicare Eligibles

Simple yoga for seniors and Medicare eligibles is generally low-impact and great for beginners. There are numerous gentle yoga poses for seniors and Medicare eligibles that are available, but the most popular are as follows:

Seated Forward Bend: Sit on the floor and keep your legs straight in front of you. Inhale and lean forward as far as you can. To avoid potential injuries, never force or push your body. This pose can calm the brain and help relieve stress. It stretches the spine, shoulders, and hamstrings and stimulates your liver and kidneys.

Legs Up The Wall: Find a sturdy wall and bring your tailbone as close as possible and raise your legs. Stay in this position for 10-15 minutes and focus on your breathing. This pose reduces gravity on your body and helps calm the nervous system.

Easy Pose: This yoga pose has been depicted as far as 2,000 years ago. Keep your back straight and cross your legs. This pose is great for meditation and breathing exercises. This pose comes naturally to children, but as you age, it may become more difficult. With practice, you can open your hips and help your spine return to proper alignment.

Corpse Pose: Lie flat on your back with your feet spread shoulder-width apart. Have your palms facing upwards. This pose is usually done at the end of your yoga practice and is more than just laying down. It relaxes your whole body and can release any stress, fatigue, or tension you may have.

Gentle Yoga Poses for Seniors and Medicare Eligibles | Medicare Plan Finder

Chair Yoga Poses for Seniors and Medicare Eligibles

If the balancing aspect of yoga intimidates you – good news, a chair can help! Many yoga poses can be modified to incorporate a chair. There are still significant benefits to this type of yoga, and it is very popular among people who have balancing issues. The following are chair yoga poses for seniors and Medicare eligibles:

Forward Fold: Sit in a chair and bend forward. When you inhale, raise your arms over your head and reach as far as possible. This yoga pose stretches your hips, hamstrings, and calves. This pose calms the brain and relieves stress. Plus, it stimulates your livers and kidneys and improves digestion.

Spinal Twist: When you are sitting on a chair, reach back as far as you can and twist your torso. It’s important to keep a good posture while twisting. This can lengthen, relax, and align your spine. Plus, it stretches your entire upper body. This can prevent your spine from becoming stiff and can help you maintain a normal spinal rotation.

Pigeon: The normal Pigeon pose can be quite difficult for seniors to do, so a chair can help tremendously! Sit up straight in your chair and keep your feet shoulder-width apart. Bring your right or left leg onto the other knee. Push the knee downward, and if possible, pull your foot up slightly. Repeat this 3-5 times and then switch to the other leg. Pigeon pose helps open your hip joints and helps lengthen your hip flexors. It can also help prevent or relieve sciatica pain.

Cat and Cow: Keep your feet flat on the floor and keep your back straight. When you inhale, arch your spine and roll your shoulders back. When you exhale, arch your spine the other way and drop your chin to your chest. This is great for breathing exercises. This stretches the lungs and chest, which makes breathing easier. This also stretches the hips, back, and abdomen.

Chest Expansion: Sit as straight as possible and reach your hands to the back of your chair. Lift your chest and take a deep breath. Do this for 3-5 breaths and then repeat. This strengthens your hand, arm, shoulder, and back muscles.

Chair Yoga for Seniors | Medicare Plan Finder

For more yoga poses for seniors, check out this video “Yoga for Seniors” by Yoga With Adriene:

Does Medicare Cover Yoga?

Original Medicare does not cover yoga or any other fitness classes. However, certain private insurance plans called Medicare Advantage cover the same benefits as Original Medicare (Part A and B) and can cover additional benefits such as vision, dental, and hearing coverage along with coverage for fitness classes.

These plans are growing in popularity. According to the Henry J Kaiser Family Foundation, enrollment has tripled to 19 million beneficiaries since 2003.

SilverSneakers ® Yoga Classes

Medicare SilverSneakers® is a fitness benefit found in many Medicare Advantage plans. SilverSneakers® hosts fitness programs for seniors that focus on general fitness, strength, flexibility, and walking ability for seniors and Medicare eligibles just like you. Medicare SilverSneakers® fitness events can also help seniors find new friends who also want to pursue an active lifestyle.

SilverSneakers® yoga classes provide a unique opportunity for seniors and Medicare eligibles to practice yoga in a judgment-free, inclusive group. These classes often incorporate chair yoga poses for seniors and Medicare eligibles.

More than 65% of leading Medicare Advantage plans include Medicare SilverSneakers.® This is generally provided at no cost.

Plus, there are over 11,000 locations across the US that offer SilverSneakers® yoga classes. Once you are enrolled in a Medicare Advantage plan that includes SilverSneakers® yoga, you will have access to any participating facility.

How to Find SilverSneakers ® Yoga Classes Near You

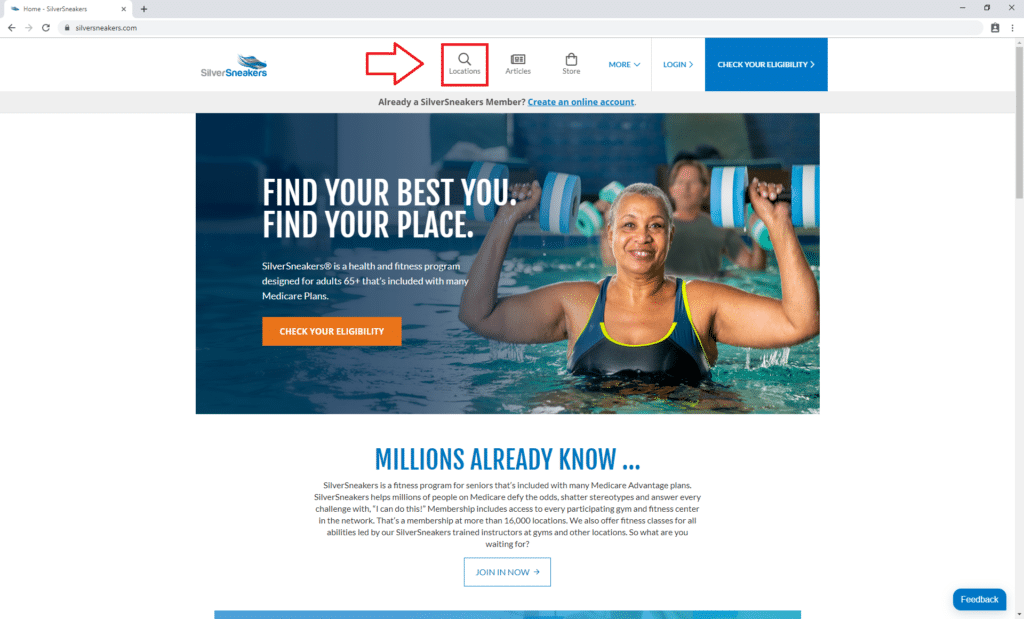

The SilverSneakers® website has a location finder so you can find participating gyms with classes near you. To get started, click here. You’ll come to the SilverSneakers® homepage, which looks like this. Click on the magnifying glass with the word “Locations” under it.

How to Find SilverSneakers ® Yoga Near You Step 1 | Medicare Plan Finder

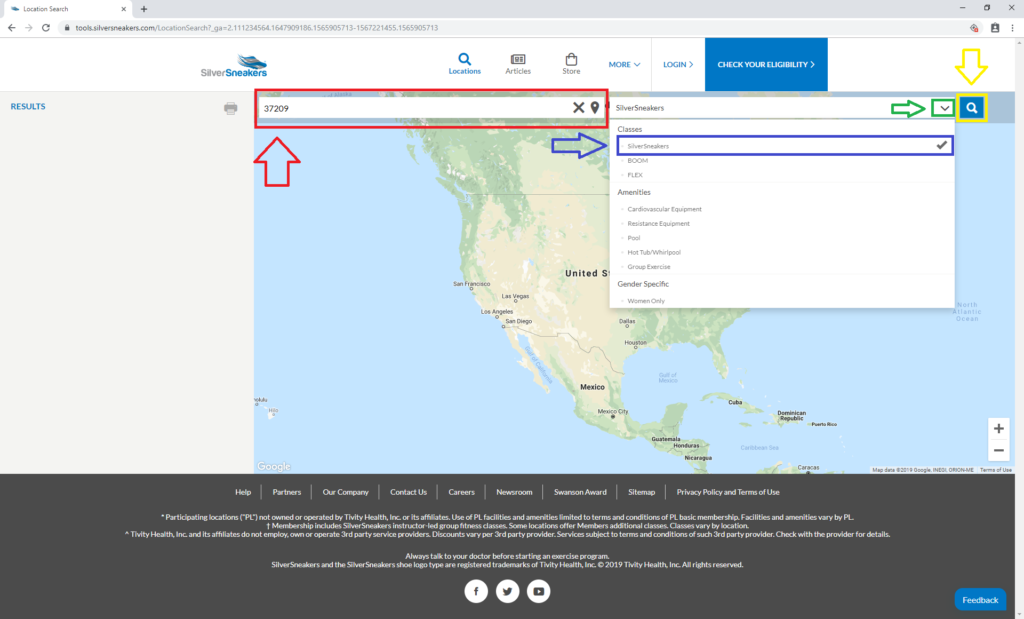

That will lead you to the location finder tool. Enter your zip code in the search bar as shown in red. We chose 37209, which is the zip code for our corporate offices in Nashville, TN. Then click the carrot shown in green. After you do that, select SilverSneakers® as shown in blue. The final part of this step is clicking the magnifying glass shown in yellow.

How to Find SilverSneakers Yoga Near You Step 2 | Medicare Plan Finder

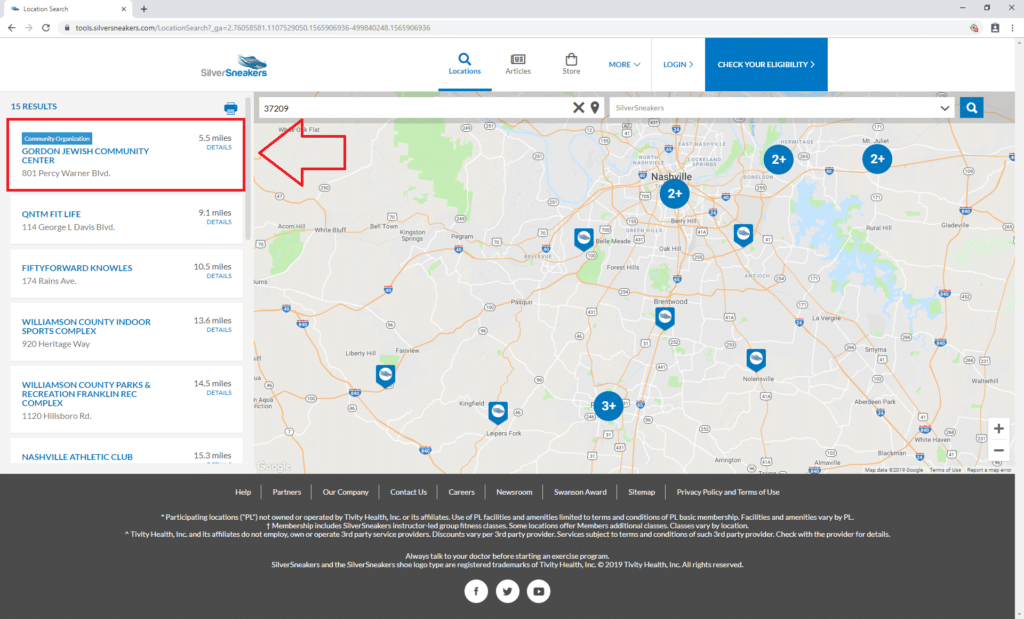

The next page lists the SilverSneakers® partners in your area. Clicking the listed gym names will show you the amenities at each location. We only clicked on the first location for demonstration purposes.

How to Find SilverSneakers ® Yoga Near You Step 3| Medicare Plan Finder

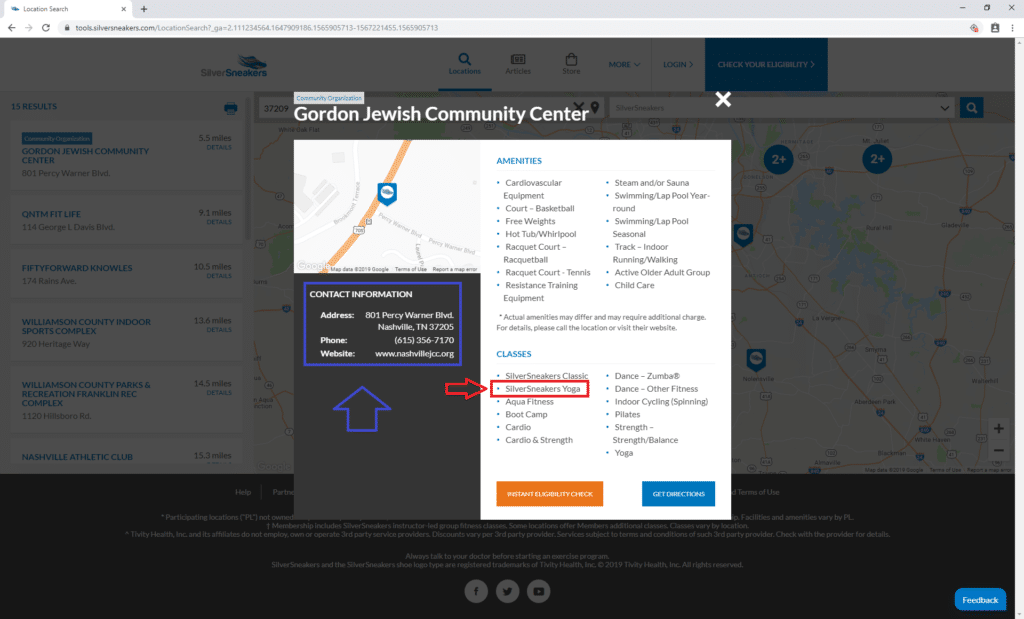

Here, you can see that the Gordon Jewish Community Center offers SilverSneakers® yoga classes in red. Use the contact information shown in blue to learn how to get started.

How to Find SilverSneakers Yoga Near You Step 4| Medicare Plan Finder

Enroll in Medicare Advantage

If SilverSneakers® yoga is something you’re interested in, then you should consider enrolling in a Medicare Advantage plan.

If you interested in enrolling in the best MA plan for your needs and budget, fill out this form or call us at 844-431-1832 to speak with a licensed agent. These appointments are no-cost to you and obligation-free. Our licensed agents can answer any questions you may have, and best of all, make sure you get SilverSneakers® yoga.

This post was originally published on October 25, 2018, by Kelsey Davis and was updated on November 18, 2019, by Troy Frink.

Fall Prevention: Tips, Tricks, and Exercises

According to the Centers for Disease Control and Prevention, falls are the leading cause of injury and death in older adults. Falls can occur at any time and can range in severity.

Seniors and Medicare eligibles can suffer from significant injuries or pain. The average hospital cost for a fall injury can exceed $30,000. Fall prevention is important to help lower the risk of falling and potential injuries.

Preventing Falls at Home

According to the Department of Health and Human Services (HHS), the majority of falls (60 percent!) occur in the home. Something as minor as a slippery spot on the floor or an electrical cord out of place can have devastating consequences.

Thankfully, there are several steps you can take to help reduce the risk of falling. The following are quick and easy suggestions that can give you a greater sense of security in your home:

Eliminate Clutter

If you have clutter in narrow or close areas, like hallways or staircases, you can easily trip or lose your balance. One of the easiest steps you can take is keeping your home clean and tidy by eliminating clutter and keeping your pathways clear.

Remove Hazards

Every room in your home should be free of tripping hazards. These hazards can include loose carpet, slippery rugs, damaged wood floorboards, etc. You should examine your home for these hazards and if you find one, remove or repair it. It is better to opt for carpet over hardwoods if possible.

Install Handrails

Woman Using Grab Bar

Grab bars and handrails can help to lower your risk of falling, especially in the bathroom. Install handrails near the toilet and bathtub and in hallways and stairwells. If you are unable to install these yourself, contact a handyman or a family member.

Wear Properly Fitting Clothes

Everyone wants to be comfortable and able to relax in their home, but did you know that baggy clothes can make you more likely to fall? Wear clothes that are the proper length, and avoid wearing anything that drags on the floor.

Wear shoes or non-slip slippers when possible. Socks can be slippery and increase your risk of falling. Non-slip socks are great alternatives that help maintain comfort and lower your risk of falling.

Create Light

It’s important that your home is well lit so you can see where you are walking. Install brighter light bulbs in dark, high-risk falling areas like hallways or stairwells. Plus, night-lights in bathrooms or hallways can help you see during any time of the night.

Preventing Falls in Hospitals

If you are in a hospital for any given reason, there is a risk of falling, especially if you are staying long-term. If you need to get up or go to the bathroom, use the call light or ask the nurse for help.

Some medicines can make you feel sleepy or dizzy, so when you are getting up, move slowly. Be sure to wear your glasses or hearing aids when you are up and moving around.

Plus, use a walker or cane because bedside tables, IV poles, and other objects cannot provide the proper support. Lastly, if you have any concerns about your safety, be sure to alert the nursing staff.

How Can Seniors Prevent Falls?

Fall Prevention Exercise – Medicare Plan Finder

Exercising is a great way to increase your balance and help lower your risk of falling. These exercises can help strengthen your muscles, and when completed regularly, improve your muscles and joints. The following are great exercises that help prevent falls:

Chair Sit to Stand

Find a sturdy chair with arms. Practice getting in and out of the chair and focus on utilizing your leg muscles. Use the arms of the chair to help you get up, but as you improve, try using only one hand. Aim for 10 repetitions.

Marching in Place

Have a chair nearby in case you lose your balance. Practice marching in place, but bring your knees as high as you can. Use your muscles instead of your momentum. Aim for 10 knee raises on each leg.

Balance on One Leg

Find a sturdy surface like a chair or countertop. Use these surfaces for support. Raise one leg and try to find your balance while standing on the other. Aim for 10-15 seconds per leg.

Toe to Heel

Hold onto a chair or countertop. Raise up onto the balls of your feet and hold for a few seconds, then relax into a normal stance. Next, rock back on your heels and hold for a few seconds. Aim for ten repetitions.

Injuries and Complications

As we mentioned above, falls are the leading cause of injury and death in older adults. Did you know one out of five falls will result in a serious injury such as a broken bone or head injury?

These injuries can make living your day-to-day life difficult. Plus, if you have vitamin d deficiency or take certain medications like sedatives or antidepressants, your risk of falling increases. Common injuries from falling include:

Head injuries

Hip fractures

Back and spinal injuries

Shoulder injuries

Torn ligaments, tendons, and muscles

Neck injuries

What to Do If You Fall

In the unfortunate incident you do fall and you live alone, you may consider buying a medical alert system to contact emergency personnel. A medical alert system is a device that you wear that features a button you can push to call for help. The systems usually come with monthly fees, but Life Alert and other medical alert devices can help provide peace of mind.

You can also keep a cordless phone or smartphone with you at all times, so you can call for help if you fall.

Another option is wearing a smartwatch. According to NPR, the Apple Watch can detect when a user has fallen, and the device will generate a notification to emergency personnel. If you don’t respond for more than a minute after the alert, the watch can automatically call for help and send “a message with location to emergency contacts.”

Does Medicare Cover Fall Injuries?

Medicare generally covers most expenses if you have a fall. If you are admitted to a hospital from your injuries, Part A may cover this expense or any necessary treatments.

Your Part A deductible and coinsurance may apply after 60 days. If you go to an emergency room, doctor’s office, or clinic due to a fall, Part B generally covers these expenses. Similar to Part A, your deductible, coinsurance, or copay payment amounts may apply.

Fall prevention is one of many ways to remain proactive and practice a healthy lifestyle. Medicare Advantage plans can offer even more benefits and coverage that help you become the healthiest version of you. Many MA plans offer hearing, dental, and vision coverage, and some even offer group fitness classes like SilverSneakers®.

If you are interested in arranging a free, no-obligation appointment with a top agent, call us at 844-431-1832 or fill out this form.

*This post was originally published on November 13, 2018. Last Updated on October 18, 2019.

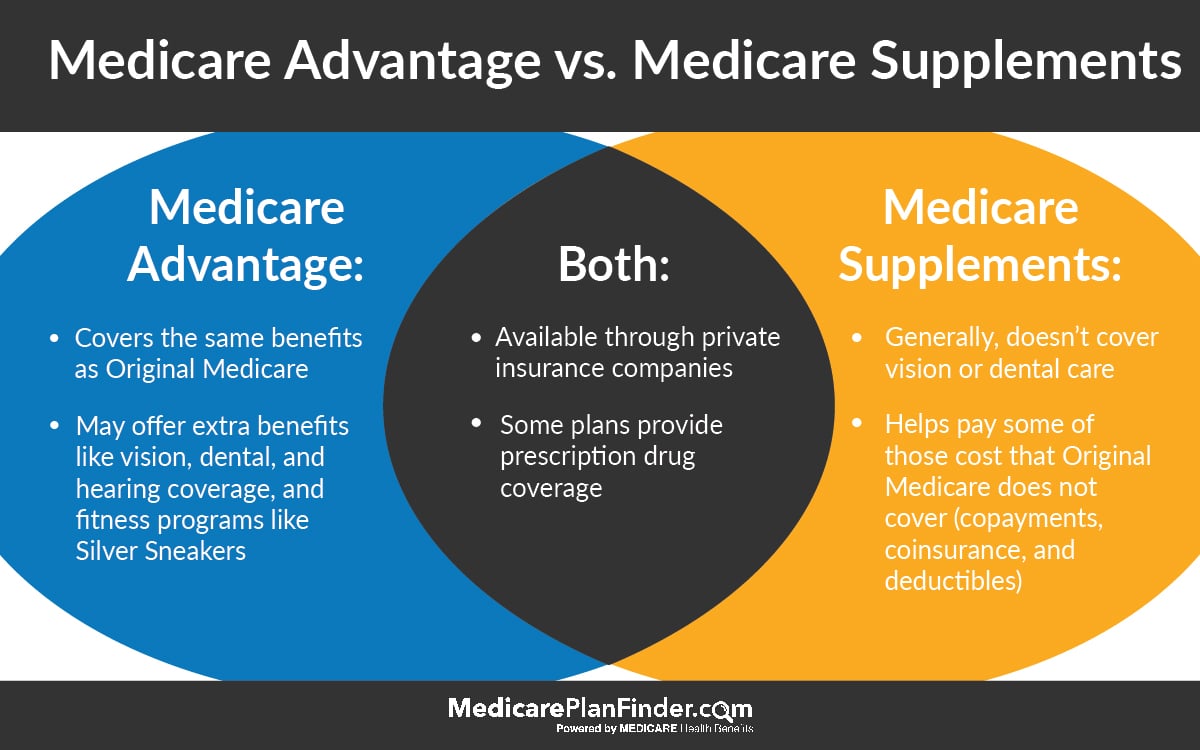

Medicare Advantage vs. Medicare Supplement

Medicare Advantage and Medicare Supplements (also called Medigap) are very different insurance plans with distinct benefits. The answer to the question “is Medicare Advantage better than Medigap?” depends on your circumstances and needs.

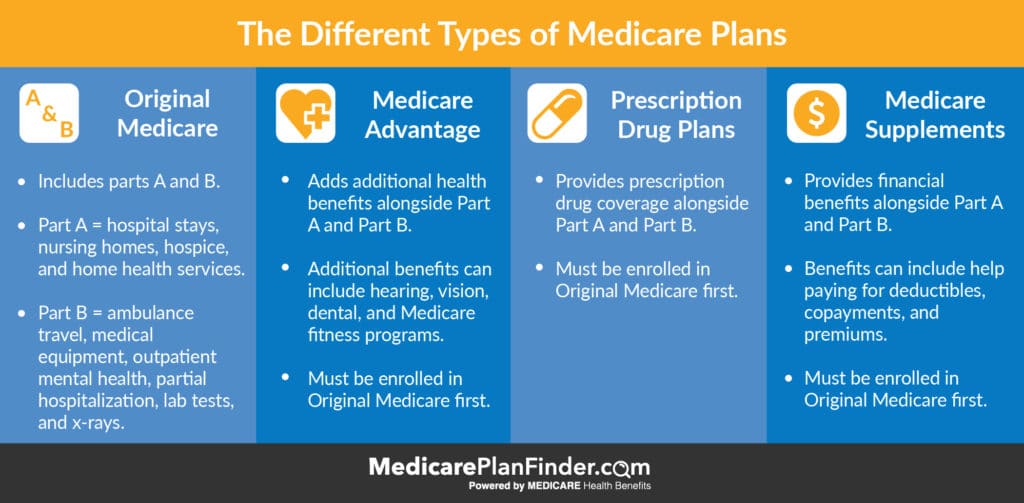

What is Medicare Advantage?

Medicare Advantage plans are private plans (not owned by the federal government) that can offer additional health benefits. To have Medicare Advantage, you have to enroll in Original Medicare first. You may have to continue to pay your Medicare Part B premium even if you have Medicare Advantage (MA), but MA premiums can be as little as $0.

Medicare Advantage plans are not all the same, but they can provide benefits like (click on the links to learn more about each one):

There are many different types of Medicare Advantage plans, although not every plan type may be available in your area.

A health maintenance organization (HMO) is a network of health-care providers and facilities where you choose a primary care physician to coordinate your care.

A preferred provider organization (PPO) is also a network of health-care providers and facilities but typically you do not need to select a primary care physician, and you have more flexible options regarding out-of-network care.

A private fee-for-service (PFFS) plan is a mode of benefit delivery where you are not limited to a network. However, there are no guarantees that your doctor or hospital will accept the plan. If you choose to receive your Medicare health coverage through a private Medicare Advantage plan, you must continue paying your Part B premium regardless, because you remain enrolled in Original Medicare (Part A and Part B), even after joining a Part C plan.

What is Medigap?

Medigap is more different from Medicare Advantage than you might think. While Medicare Advantage plans are able to offer health benefits, Medicare Supplement plans (also called Medigap) offer financial benefits. For example, some Medigap plans can cover your Part B premium.

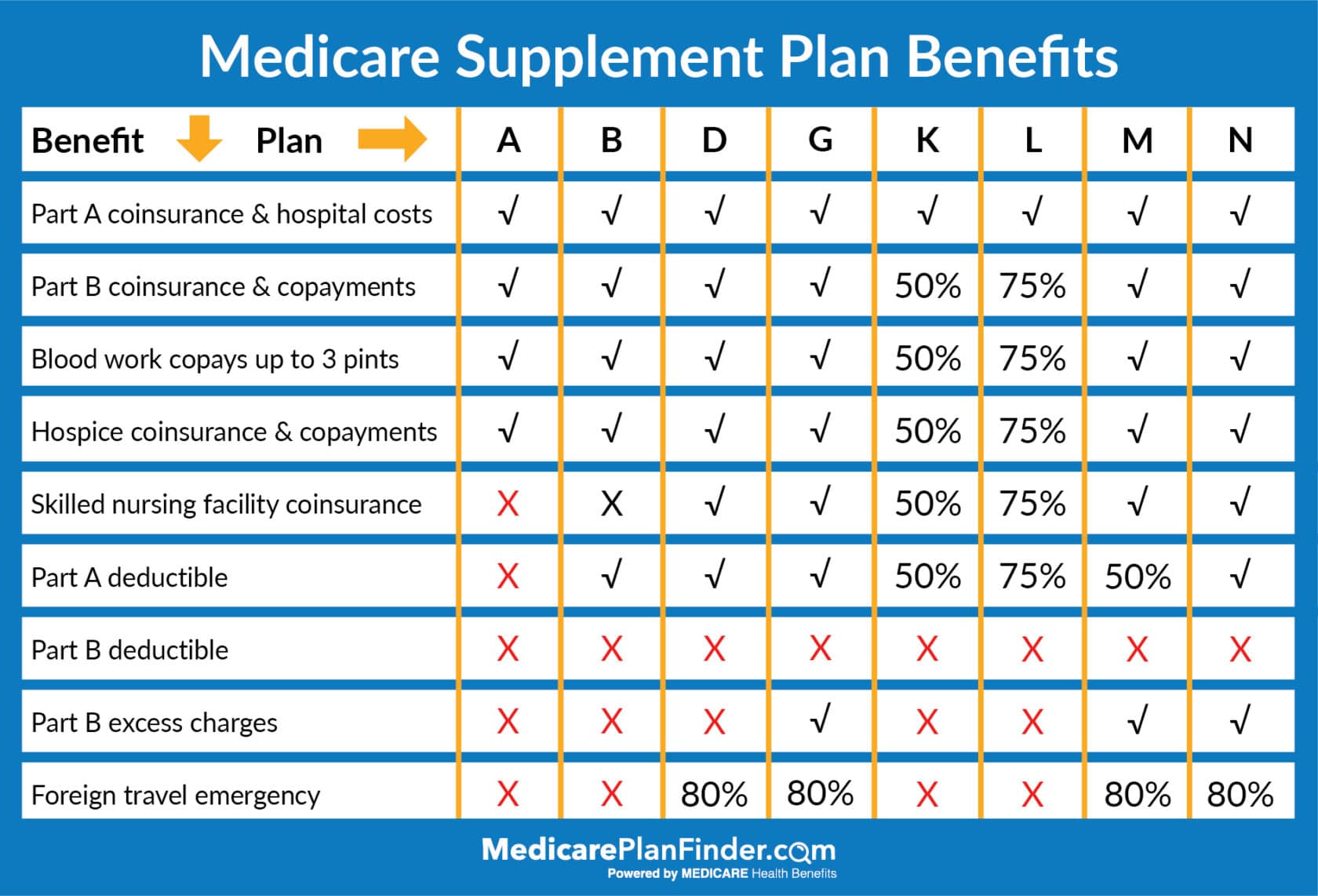

The chart below explains the differences between available Medigap plans in 2020. You can also use our Medicare Plan Finder search tool to compare plans in your area.

2020 Medicare Supplement Comparison Chart

Comparing Medicare Advantage vs. Medicare Supplement plans

Let’s look at Medicare Advantage vs. Medigap. In short, the difference between Medicare Advantage and Medicare Supplement plans is that one can supply health benefits while the other can supply financial coverage.

Medicare Supplement Insurance is a policy that’s added to Original Medicare, Part A and Part B, to provide additional financial coverage. Medicare Advantage is a private plan option that may provide you with other health benefits that Original Medicare does not cover (like dental, vision, fitness programs, etc.).

You cannot have both Medicare Advantage and Medigap at the same time.

Medicare Advantage vs Medicare Supplements | Medicare Plan Finder

A given plan type (e.g., Plan F) has the same benefits regardless of the insurance company that provides the policy, or the state in which you reside. This is not true of Medicare Advantage plans, however, because coverage details may vary by plan.

Excluding prescription drug coverage, any standard Medigap plan with Part A and B will have more benefits than a standard Medicare Advantage plan. However, as mentioned above, some Medicare Advantage plans offer benefits beyond those found in Part A and Part B.

Some Medicare Advantage plans offer prescription drug coverage (often for an additional monthly cost). With a Medigap plan, in contrast, you would need to enroll in a separate prescription drug plan. When comparing plan options, consider your costs for drug coverage. In some cases, Medigap with a stand-alone prescription drug plan has lower total costs than a Medicare Advantage plan with drug coverage. In other cases, the reverse might be true.

[Tweet “Do your research! Comparing #Medicare Advantage vs Medicare Supplement”]

Real-Life Examples: Medicare Advantage vs. Medicare Supplements

Let’s take a look at some real-life examples to help you decide whether Medicare Advantage or Medicare Supplements are right for you.

If you have Medicare Parts A (hospital coverage), B (medical coverage), and D (prescription coverage) and you are hospitalized for cancer treatments for 90 days, you may have out of pocket costs. The Part A deductible means you would pay well over $1,000 first. Once you meet your deductible, your costs will go down. However, after day 60, you’ll be responsible for a portion of every day that you stay there.

If you have Medigap Plan B, your deductible and many of your other hospital costs will be covered. This plan would be in addition to your Part B coverage, so it would all work together to provide extra coverage.

If you have Medicare Advantage, you may have additional health benefits. You’d still likely be responsible for some of those out-of-pocket hospital costs, but your plan might provide a home healthcare benefit, meaning you can get a private in-home nurse when you are released from the hospital. You might also have coverage for medical equipment, such as bathroom safety equipment or a walker.

Comparison is key: Medicare Advantage vs. Medicare Supplements

When choosing between a Medigap plan and a Medicare Advantage plan, take the time to do your research. Read the benefit descriptions of every Medigap and Medicare Advantage plan you are considering. Be certain to look at:

Monthly premium

Deductibles

Doctor and healthcare facility restrictions

Benefits

Anticipated plan costs given your typical use of health-care and hospitalization services

Prescription drug coverage cost sharing as it relates to your medication usage

In the end, your decision is going to be the one that you feel the most comfortable with. The challenge is often wading through all the material to get to the bottom line. Want to make that a little easier? Give us a call at 844-431-1832.

This post was originally published on October 23, 2018, and was last updated on August 29, 2019.

5 Medicare Enrollment Periods & What You Can Do During Each One

Did you know there are five different Medicare enrollment periods? You may qualify to enroll or make changes to your current coverage and have no idea! AEP is just a few months away, so we’d like to share with you what you can do during the various enrollment periods so you are properly prepared.

Initial Enrollment Period

Your Initial Enrollment Period (IEP) is typically your first opportunity to enroll in Medicare. Your IEP is three months before your 65th birthday and three months after. This gives you a seven-month window to enroll in your preferred coverage.

In most cases, if you do not enroll in Part A and Part B (Original Medicare) during your IEP, you will be charged a late enrollment penalty fee that will be added to your monthly Part B premium. If you do not have prescription drug coverage, you should also consider enrolling in a Part D plan to avoid other penalties down the road. You are not required to enroll in a Medicare Advantage or Medicare Supplement plan, but you should consider enrolling to optimize your coverage.

The General Enrollment Period (GEP) is for those who are enrolling in Medicare for the first time but missed their IEP. The GEP runs from January 1 to March 31 each year, and coverage will begin in July.

During the GEP, you can:

Enroll in Original Medicare if you missed your IEP

*If you enroll for the first time during the GEP, you can follow up by enrolling in a Medicare Advantage plan during a period from April 1 through June 30.

Annual Enrollment Period

The Annual Enrollment Period (AEP) runs from October 15 to December 7 each year. During this time, all Medicare beneficiaries can make changes to their plans. You may not need to do anything during AEP. However, major insurance carriers can change the benefits that they offer every year. It’s possible that a change in your plan benefits or your provider network will change how you feel about your plan. Ultimately, it’s always a good idea to speak with an agent. Any changes you make during AEP become effective on January 1 of the following year.

Most people can only make changes to their plans once a year (during AEP), but if you qualify for a Special Enrollment Period you can make those changes during different times of the year or even all year long. Lifelong SEPs allow you to change plans once every quarter for the first three quarters of the year. Circumstantial SEPS allow you to change plans once following a particular event.

Starting in 2019, there will be a new “Medicare Open Enrollment Period” that will run from January 1 through March 30. OEP was created for anyone who signs up for a Medicare Advantage plan during AEP to enroll in a different plan, without having to wait until the following fall. You do not have to do anything during OEP unless you are unhappy with the coverage you enrolled in during AEP.

Change from Medicare Advantage to Original Medicare only, with the option to add a prescription drug plan

Contact Medicare Plan Finder

Are you looking to enroll in Medicare Advantage, Medicare Supplements, or Part D? Are you still confused on which Medicare enrollment periods you qualify for?

Our agents at Medicare Plan Finder can answer any of your questions and simplify the enrollment process. They are contracted with most of the major carriers in your state so the agent should not show bias when enrolling. To speak with a licensed agent and to learn about plans in your area, click here or call 844-431-1832.

This blog was originally published on 10/23/18 and was updated on 7/15/19.

Mother’s Day Health Tips to Share with Your Senior Mother

Your mother has dedicated her life to caring for you, and as she ages, it’s time for the roles to reverse. The best gift any mother could ask for is for her children to be wonderful, caring adults! As you plan to celebrate this Mother’s Day with your mother, consider giving the gift of your support throughout the rest of her life.

Healthy Ways to Celebrate Mother’s Day

Whether your mom is at home, in a living facility, or a hospital, you can still enjoy a beautiful Mother’s Day with her. If the weather is nice and she is able, take her for a walk! Sunshine strengthens the bones and the immune system and reduces stress while inducing feelings of happiness. You can also take her to a healthy brunch. Skip the sugary, syrupy pancakes and take your mom to a place where she can enjoy some fresh fruit with oatmeal or yogurt or opt for eggs and toast.

Top Women’s Health Concerns

Even if you don’t want to think about your mother’s aging and her health on Mother’s Day, think about selecting a day to discuss these topics with her. The top concerns that aging women face are:

Look for symptoms of these ailments in your mother, and educate her on what to look out for. Certain things, like breast swelling, brittle bones, muscle pain, and memory loss can be easy to spot. Depression is one of the ailments that is hardest to notice, especially when you don’t see a person often. Some people are really good at hiding their depression symptoms. When you don’t see your mother for a few weeks or even months, she might act like her normal self around you and then go home and sleep all day because she’s mentally exhausted. Keep your mother’s spirits up and help her fight depression by ensuring that she is engaging in hobbies and activities, keeping some sort of a social life, and keeping some sort of responsibility, like keeping a garden or a pet, or even just keeping the house clean.

Top Aging Women’s Health Tips

The best things your mother can do (and you, too!) as she ages are:

Eat healthy

Stay smart about medications

Manage existing health conditions

Get screened

Stay active

Eating healthy is always easier said than done as we are tempted by the snack aisle in the grocery store and the beautiful pastry display at Starbucks. Remind your mother to enjoy everything in moderation and keep superfoods like leafy greens, berries, and avocados in her diet.

Pay close attention to her doctor’s or pharmacist’s instructions regarding medications. Help your mother avoid being one of the statistics for senior opioid abuse. On the same token, make sure your mother is taking her medications and properly managing her preexisting health conditions. Help her out by purchasing vitamins and supplements that she can take, making sure she is comfortable at home, and watching her sugar intake.

Seniors are likely to avoid trips to the doctor because they don’t have an easy way to get there or they simply forget to book their yearly appointment. Some don’t want to pay for it – but guess what? Medicare covers one yearly wellness exam at no cost to the patient. This is a good time for your mother to ask questions and a good time for her doctor to perform or schedule screenings for common ailments. Those screenings are usually covered, too, so there’s no excuse!

Lastly, make sure your mother is regularly taking walks and engaging in household chores to stay active.

Get Support While you Take Care of Mom

Providing care for a loved one is no easy task, but you are not alone. Caregiver support groups throughout the country can answer your questions, give you advice, and allow you to interact with other caregivers just like you. Consider reaching out to the Family Caregiver Alliance, a group that has worked since the late ’70s to support people like you. You can also reach out to the Caregiver Action Network. They are located in D.C. and spend a lot of time advocating for caregiver rights and laws.

We’ve put together information on caregiver networks and some of our own advice for taking care of your loved ones, here. We specialize in Medicare plans, so if your mother or someone else you know needs help finding a plan, don’t hesitate to reach out to Medicare Plan Finder. We work with all of the major plans so there is no bias and you are never obligated to buy. If you are the “Power of Attorney” for your mother, we can speak directly to you about her healthcare plans.

We hope you enjoy a beautiful Mother’s Day this year and we hope to speak with you soon regarding your or your mother’s care.

Understanding Your Best Cancer Insurance, Heart Attack Insurance, and Stroke Insurance Options

Medicare is designed to provide coverage for the most basic healthcare that everybody needs. Therefore, it does not include extensive cancer, heart attack, or stroke coverage. That’s why many Medicare beneficiaries enroll in secondary health insurance plans to supplement their current coverage gaps.

Original Medicare Part A covers hospital costs, and Original Medicare Part B covers doctor visits. Medicare Advantage adds on prescription drug coverage as well as other benefits like fitness incentives, dental, vision, and hearing.

Medicare Supplement plans add on extra coverage for your deductibles, copayments, and coinsurance (and sometimes cover prescriptions as well). While those Medicare options are certainly useful for both your wallet and your health, they simply won’t cover all of your health care needs. That’s where ancillary plans, (also known as secondary health insurance plans) come in.

Do you Need Supplemental Insurance?

Supplemental insurance plans provide coverage for medical procedures and needs that Medicare won’t. You might wonder, “why doesn’t Medicare just cover everything in one plan?” Well, Medicare is a government program, and everyone’s healthcare needs are different. It is not lucrative for Medicare to cover everything. That’s why people who need extra financial help can add on ancillary coverage to help cover their extra healthcare costs.

If you have a medical history that includes cancer, heart disease, or stroke symptoms, you may benefit from an ancillary plan that specifically covers your symptoms or can give you extra cash. That’s why you should always disclose all your healthcare and financial information to your agent – they can’t help you get the right amount of coverage if they don’t know how much coverage you need!

Most ancillary plans work by sending reimbursement checks (usually upon diagnosis). You’ll tell your plan when you are diagnosed with a disease, and they will send you a check based on your policy value (sometimes all at once, sometimes annually, etc.). Since your money will come in the form of a reimbursement, you can technically use it for whatever you need – loss of income, childcare, travel to facilities, home health care, rehabilitation/therapy, and any other out-of-pocket costs that Medicare does not touch.

What Does Cancer Insurance Cover?

Cancer insurance plans can vary greatly. In general, you’ll find policies that cover services like:

Blood and plasma

Breast reconstruction

Chemotherapy

Child/pet care expenses

Extended care facility stays

Hospice

Hospitalization

Initial diagnosis

Medical imaging

Organ transplants

Prosthetics

Radiation

Rehabilitative therapy

Surgery

Transportation and lodging related to hospital stays

What are the Best Cancer Insurance Plans?

No other disease statistics come close to cancer. Men have about a 50% chance of developing cancer, while women have about a 33.3% chance. Cancer kills about 1,600 Americans every day and includes about 10% of American healthcare expenses.

There really isn’t one best cancer insurance policy, because everyone’s financial and healthcare needs are different. However, one of the “best” and most common options is a lump sum policy. For a monthly payment of even as little as $20 per month, you can invest in a policy worth anywhere from a couple thousand to a hundred thousand dollars. If you are then diagnosed with cancer, you will receive the lump sum of your policy’s cash value to help you cover your cancer costs.

Lump sum cancer insurance is a good idea if you have a family history of cancer or if you meet any risk factors, such as a history of tobacco use, increased sun exposure, or obesity. If you already have a cancer diagnosis, you may not be able to enroll in this type of cancer insurance. A Medicare Advantage or Medicare Supplement plan might be a better option, as pre-existing conditions will not prevent you from enrolling. Plus, you can choose a Medicare Advantage plan or Medicare Supplement plan with great prescription drug benefits.

Cancer Insurance Pros and Cons

Cancer Insurance Pros:

Financial Relief – While you’re worrying about your health, you don’t want to have to worry about your finances. Not only is cancer treatment expensive, but you may have to leave your job to adequately receive the treatment you need! Not only can cancer policies help you pay for your care, but they can also help you recover from lost income.

Extra Medical Coverage – Original Medicare covers basic hospital and doctor costs, and you might have a prescription drug plan, but Medicare alone does not cover all cancer-related costs. A cancer plan will help you pay for extra prescriptions and procedures.

Peace-of-Mind – If you have a family history of cancer or if you’ve shown signs, having a cancer policy can give you the peace-of-mind to know that you’re covered in the event of a diagnosis.

Cancer Insurance Cons:

Availability – Cancer insurance can be harder to find than other health insurance options. However, our licensed agents are able to sell plans from most cancer insurers in your area. A MedicarePlanFinder agent can help you find what you need.

Pre-existing Conditions – If you’ve had any cancer symptoms in the past, it may be hard for you to find a cancer policy. It is really designed for those who have a family history of cancer and want to make a smart decision early on. That’s why you should buy now, BEFORE your diagnosis.

Types of Cancer Insurance

Lump Sum Cancer Insurance

A lump sum cancer insurance plan is meant to provide extra cash when you need it most: while you’re undergoing treatment. You will receive a payment for the value of your policy (usually between $5,000 and $100,000), at the time of your diagnosis.

Indemnity Cancer Plans

Indemnity plans are designed to help you pay for the costs of staying in a hospital for an extended period of time. Instead of paying out your benefits all at once in a lump sum, an indemnity cancer plan can pay you per day. For example, it might pay out $300 for each day you spend in the hospital.

Top Cancer Insurance Plans

While there are seemingly endless possibilities for getting cancer coverage, these are some of the top cancer insurance plans that Medicare Plan Finder agents currently offer (subject to change):

Aetna Cancer Insurance

Aetna offers a cancer, heart attack, and stroke insurance policy for seniors and Medicare eligibles. You or a person that you designate will receive a lump sum based on your policy value upon your cancer diagnosis. The policy can be valued at anywhere from $5,000 to $75,000.

Aetna cancer policies give you a 30-day “look” period. That means that if you decide within 30 days of your purchase that you do not like the plan you chose, you can back out.

Cigna Cancer Insurance

Cigna’s cancer policies can cost you as little as $19 per month and can cover you for as little as $5,000 or as much as $100,000. Cigna cancer coverage is available to anyone ages 18-99. For an added premium, you can also receive coverage for cancer recurrence, heart attacks, and strokes.

Mutual of Omaha Cancer Insurance

Mutual of Omaha offers both a cancer only insurance plan and a cancer, heart attack, and stroke insurance plan. Since the policy pays out as a lump sum at the time of diagnosis, you can use it however you want, regardless of who your doctors are.

GTL Cancer Insurance

Guarantee Trust Life (GTL) cancer insurance is wrapped into one policy including cancer, heart attack, and stroke coverage. They pay a lump-sum upon diagnosis regardless of what other health insurance you may have. GTL benefits are flexible but range up to $75,000.

Medico Cancer Insurance

Medico will pay a lump sum benefit upon your internal cancer or malignant melanoma diagnosis. It is a one-time benefit paid directly to you – you can use it in any way you see fit!

Frequently Asked Questions About Cancer Insurance

Can I get cancer insurance after diagnosis?

It can be a challenge to get a good cancer insurance policy after you’ve already been diagnosed. That’s why we recommend that you look at your cancer insurance options NOW, to avoid any financial surprises later.

Is Cancer Insurance Worth it?

In short, yes! Wouldn’t you rather pay a small fee every month now instead of paying thousands upon thousands later? Investing in your health now allows you to plan for the finer things in life, like a beautiful retirement!

Can I buy cancer insurance online?

We don’t recommend buying without speaking to a licensed agent. Medicare Plan Finder agents are licensed with multiple insurance carriers, which means they can help you find quotes for several different plans and help you choose the best one for your needs.

How much does cancer insurance cost?

This really is going to depend on what you need. All carriers offer different types of plans that offer different amounts of coverage. If you do not have a personal history of cancer, you can get $5,000 of coverage for about $16/month! Of course, the more coverage you want, the higher your monthly costs will be.

Who sells the cheapest cancer insurance?

Cigna offers one of the cheapest plans at as little as $19 per month, and Mutual of Omaha boasts of rates as low as $10 per month! Your choice will depend on your healthcare needs, how much coverage you want, and your geographic area. Remember, not all plans are available in every state or county. It’s more important to look at the coverage that you’re getting first, THEN consider the cost. Our agents can help you find the best balance.

What other types of coverage are included in cancer insurance?

Cancer, stroke, and heart attacks are three of the most common ailments in America. Some cancer insurance policies are wrapped into one policy that includes stroke and heart attack coverage. This means that if you develop a heart condition now and develop cancer symptoms later, your one cancer, heart attack, and stroke policy will likely cover all or most of your conditions.

What Does Stroke Insurance Cover?

According to stroke.org, a stroke occurs every 40 seconds and is the 5th leading cause of death in the United States. A stroke happens when blood flow is cut off from an area of the brain, resulting in brain cells losing oxygen and dying. The dying cells lead to memory and muscle control loss. Small strokes may only result in temporary weakness, while large strokes can permanently paralyze a person.

Shockingly, nearly 80% of strokes are preventable. You can help prevent strokes by keeping a healthy weight and blood pressure, exercising regularly, avoiding excess alcohol consumption, and not smoking.

When looking for stroke insurance, Medicare Advantage and Medicare Supplement plans are great places to start. Having extra Medicare coverage will most likely give you access to more affordable healthcare through your doctors and pharmacies.

If that is not enough coverage, you can invest in a stroke policy. Most stroke policies are combined with heart attack policies. Stroke insurance is usually paid out as a lump sum (ranging from as low as $5,000 to as much as $100,000), which means it can cover anything from relevant surgeries to income replacement, instead of covering individual benefits.

Heart Attack Insurance

The CDC states that about 610,000 Americans die of heart disease every year. As common as heart disease is, it’s not cheap to handle. It can cost upwards of $20,000 for a hospital stay alone, not including the costs of any surgeries and prescriptions that follow.

While your Medicare plan may cover your hospital stay costs, it may not completely cover the surgeries and prescriptions you need. In fact, Original Medicare does not cover prescriptions at all. You will need to enroll in either a separate prescription drug plan (otherwise known as Part D) or either a Medicare Advantage or Medicare Supplement plan that includes prescription drug coverage. That’s why a heart attack/stroke plan is a great option. After a heart attack, you can receive a lump sum based on your policy value to help you pay for care or replace lost income.

Cancer, Heart Attack, and Stroke Insurance

Some cancer, heart attack, and stroke insurance policies are looped into one policy. The same policy can cover heart transplants, physical therapy, patient and family member transportation and lodging, bypass surgeries, anesthesia, replacement of lost income, and help with home expenses.

Costs for cancer, heart attack, and stroke policies will vary based on your needs and how much coverage you want to pay for. If you prefer, you can pay as little as $20 per month (but will have less coverage than if you paid a higher monthly premium).

Help Us Help You

If your family medical history includes strokes or heart attacks, be sure to disclose that information to your Medicare agent. They can help you pick a plan that best encompasses your needs, and then help you decide whether or not you need to add an ancillary policy.

Do you have an agent? Our agents are able to sell countless different plans, so they can help you find the one that truly works best for you. Submit your contact information on Medicare Plan Finder so we can have one of our licensed agents reach out to you. If you’d prefer, give us a call today at 844-431-1832.

This post was originally published on March 23, 2017. It was updated on October 23, 2018, and again on July 18th, 2019.