Final Expense (Burial) Insurance

One of the ways you show that you love your family members is by creating an estate plan that protects their financial health when you pass away. You save and invest on a regular basis, you have acquired several assets you hope to pass on, and you’ve made sure those assets are protected by buying various types of life insurance.

If you’re like many people, you have auto, home, health, and life insurance. Those are fairly standard and can provide a high level of protection when your family needs it most.

But there is another type of insurance that is sometimes overlooked but that also provides protection in times of need. Setting aside dedicated funds for your funeral and related expenses can be a smart move to preserve other types of assets. Dedicated funds can be set aside in the form of final expense insurance, also often referred to as burial insurance.

What is Final Expense Insurance and Why Do I Need It?

What does Final Expense Insurance Cover?

The Differences Between Pre-need Funeral Plans and Final Expense Life Insurance

Are There Different Types of Final Expense Insurance Policies?

Policy Features and Eligibility Requirements

Working With the Best Final Expense Insurance Companies in 2020

Does Medicare Cover Funeral Expenses?

Can You Have More Than One Final Expense Insurance Policy?

How Much Does Final Expense Cost?

Other Ways to Pay for Final Expenses

Pros and Cons: Is Final Expense Insurance a Good Deal?

How Do I Buy Final Expense Insurance?

What is Final Expense Insurance and Why Do I Need It?

Final expense insurance is exactly what it sounds like. A dedicated life insurance policy specifically issued to use for costs associated with a person’s death.

Many insurers use the term “final expense insurance” and “burial insurance” interchangeably. However, some do not. Depending on the company, burial insurance may have more restricted uses of funds the final expense insurance, so it’s best to check on this small but important fact when you begin looking at policies.

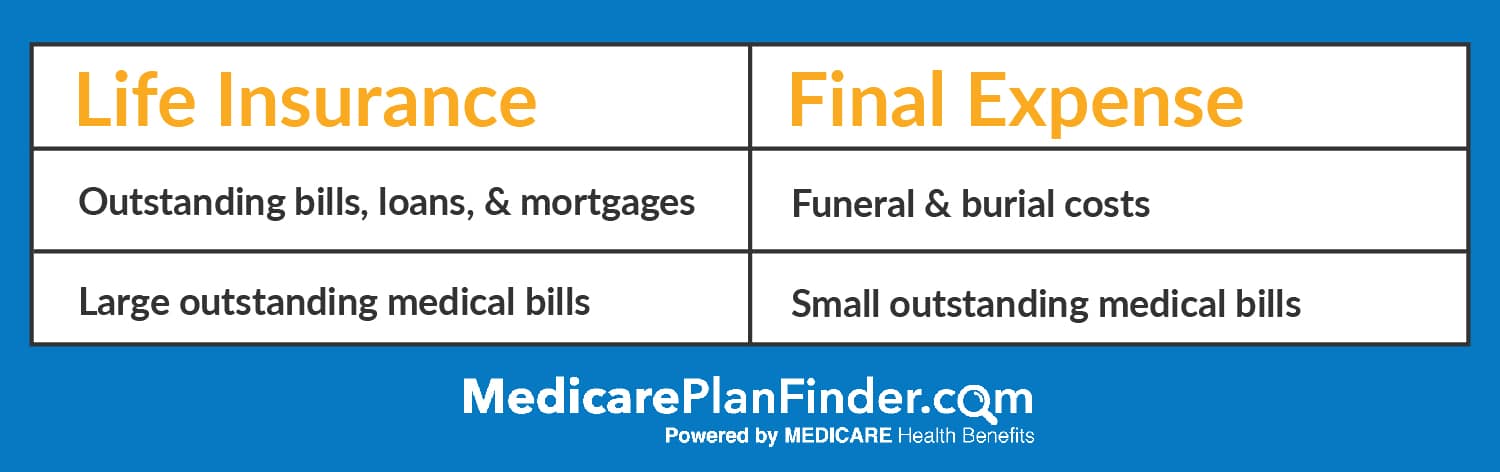

You might not think or know too much about these costs, but a funeral alone can run $10,000 or more, and that can be a heavy financial burden for family members to bear at a difficult time. Final expense insurance protects against sticker shock and having to dip into other resources when a family member passes away.

It’s less than ideal if you have to shave expenses off the top of a traditional life insurance death benefit or pull thousands of dollars out of an estate to cover costs before heirs see any proceeds.

Policies are different and for smaller amounts than regular life insurance, so the premiums are more affordable. The exact amount you need can be decided by how you want to plan your “exit” strategy. That way you can try to match the amount of your final expense death benefit to the estimated costs for your funeral and related expenses.

What does Final Expense Insurance Cover?

Typically, a policy will cover a variety of expenses, including:

- Casket

- Headstone

- Cemetery plot

- Cremation services

- Urns

- Funeral home services

- Funeral procession and hearse

- Memorial services

- Outstanding medical and legal bills

- Last wishes, such as burial in a remote location, or spreading ashes at sea, etc.

After these expenses have been paid, any remaining funds left in the policy can be spent whatever way the beneficiary chooses.

The Differences Between Pre-need Funeral Plans and Final Expense Life Insurance

Do not confuse final expense life insurance with pre-need funeral plans. They are different.

Pre-need funeral plans are sold by funeral homes and pay specifically for funeral expenses. They are also sometimes referred to burial insurance or final expense insurance but don’t be fooled by the differences.

There are a few drawbacks when a funeral home sells a plan like this.

Because the plan is sold by a funeral home and not an insurance provider, there is a lot less oversight. Insurance plans sold by insurance companies have much more regulatory oversight, meaning you get a much higher level of protection.

Even if they are well-intentioned, a funeral home could mishandle or mismanage your funds after you pay them, or they could go out of business, leaving you completely out of luck. The result is that you could be out thousands of dollars and may not even discover it for several years.

Although the federal government did pass the Funeral Rule of 1984 to provide more oversight of the funeral industry, this law does not apply to many of the features in pre-need plans. Pre-need plans are governed by individual states, and that means protections could vary widely depending on where you live.

When you shop for a final expense policy, make sure it is one that is offered by a life insurance provider to give you the added level of protection you deserve.

Are There Different Types of Final Expense Insurance Policies?

There are several kinds of final expense life insurance policies to meet a variety of needs.

The policies you qualify for are based on a health history assessment in most cases. The only exception is when you buy a guaranteed issue policy, where no assessment is required. Otherwise, you’ll answer several questions and have urine and/or blood sample analyzed.

Different types of funeral insurance policies can include:

Level Benefit Funeral Insurance. This pays the full policy amount when you die and is in force as soon as you are approved. Generally, these policies are available for people who have no disqualifying health issues, so not everyone will qualify. They also tend to have the lowest comparable premiums.

Graded Benefit Funeral Insurance. This type of policy can be offered if pre-existing health issues are discovered during the health assessment. Graded plans ramp up and pay full benefits over time. The ramp-up period will vary from provider to provider.

Modified Benefit Funeral Insurance. This is another graded benefit plan, but the ramp-up and payout schedule is different due to higher risks

Guaranteed Issue Funeral Insurance. This type of policy requires no health assessment. Everyone is approved. Payouts and more restricted than other types of policies. This is typically seen as a last resort for people who can’t get other forms of funeral insurance, such as people in hospice or with a terminal illness.

Policy Features and Eligibility Requirements

In addition to covering several types of final expenses, a funeral insurance policy is attractive for other reasons as well.

Policies are often written for coverage amounts that range from $5,000 to $25,000 in coverage. You can decide on the benefit amount based on what your personal projected final costs will be. The differs quite a bit from traditional life insurance, where policies are often written for $250,000, $500,000 and more.

The purposes of each are different as well. Final expense insurance is dedicated primarily to the funeral and related expenses. Life insurance protects surviving family members with expenses going forward, such as long-term mortgage, car payments, health insurance, college expenses, and other ongoing “quality of life” costs.

Because funeral insurance policies are whole life policies, a cash value can accumulate over time. That cash value gives you added flexibility in case you want to tap into those funds.

You can designate anyone you want to be a beneficiary of the policy. Be sure they are comfortable handling the financial aspects of the policy when you pass away. They will need to be a gatekeeper for the funds during a difficult period, so choose wisely.

Also, funeral insurance premiums do not change. Once you start paying a certain premium amount, you are locked in for that cost, instead of worrying about an escalating premium as you get older, as you would pay with a term insurance policy. The price of your initial premium will be higher the older you are.

Additional benefits may be awarded in the case of accidental death. Be sure to ask your insurer about this provision when shopping for a policy.

In some cases, insurance providers will also offer policies to people with terminal illnesses. It may be difficult, but not impossible, to find a provider who will offer you a guaranteed issue funeral insurance policy. Many providers also offer same day approval.

These types of policies often come with a two-year graded death benefit and you may not be covered for anything but an accidental death during this initial period. If you pass away during the waiting period, your heirs will only get back what you paid into the policy, plus a small additional amount in interest.

Working With the Best Final Expense Insurance Companies in 2020

At Medicare Plan Finder, our agents are able to help you with your final expense, life insurance, and many other protection needs. We offer final expense plans from top carriers, like:

- Aetna

- AIG

- American Amicable

- Cigna

- Foresters

- Gerber

- Great Western

- Mutual of Omaha

- Prosperity Life

- Renaissance Life

- TransAmerica

We are independent final expense agents and we don’t work for a specific company. Using our considerable resources, we’re able to shop around to many companies and save you as much money as possible due to that flexibility.

Some agents are captive agents. This means they work for one company, and only sell products offered by that company. People often choose to work with a captive agent mainly because they already have a level of trust and a relationship in place because they bought other types of policies (i.e, life, auto, health).

A licensed funeral director may also sell final expense insurance, but most of the time, that’s not the case. Instead, they sell pre-need plans that let you pay for a funeral in advance. This locks you in and assumes you will have the funeral at their facility. It tends to benefit the funeral home more than it benefits you as the consumer.

Does Medicare Cover Funeral Expenses?

No. Medicare only covers health costs. It provides no coverage for a funeral or related expenses.

Some people assume that if they have a Medical Savings Account (MSA), their funeral costs will be covered. That’s not the case, either.

Although an MSA functions much like a bank account, funds can only be used for medical expenses, and funeral expenses are not considered a medical expense.

If a loved one passes away and you are responsible for closing their MSA, you’ll need to contact Medicare. To do so, call Social Security to report the death at 1-800-772-1213 (TTY 1-800-325-0778), Monday-Friday, from 7 am to 7 pm. If you’re eligible, you may qualify for a small Social Security death benefit.

If your loved one worked for the railroad, call the Railroad Retirement Board at 1-877-772-5772, Monday-Friday, from 9 am to 3:30 pm.

Also, if your loved one had a Medicare Advantage plan, you’ll need to call their plan’s carrier as well.

Can You Have More Than One Final Expense Insurance Policy?

Yes. As long as you pay your premiums on time, there’s no reason why you can’t get more than one final expense policy.

It may be wise to discuss this strategy with your insurance agent. He or she may have some other more economical ways that could provide better coverage for you.

How Much Does Final Expense Cost?

As you can guess, the answer is, it depends.

There are several variables to consider before a policy is issued.

An agent will need to know how much coverage you want, what type of policy you want, if you have pre-existing health conditions, your age, and other essential information.

You can expect to pay anywhere from $20 to $80 per month depending on your variables.

Funeral Costs: What to Expect

Let’s be clear. One of the reasons final expense insurance is available is because funerals are not cheap. Average funerals now cost more than $10,000, with costs more than double that amount in many cases.

Where you live does have some impact on costs.

The National Funeral Directors Association released a General Price List Study in 2019 that shows the median cost for a funeral has increased by 6.4% over the past five years. A median cost for cremation has also increased by 7.3% over the same period.

Because funeral costs were the subject of complaints about unfair and predatory business practices a few years back, Congress passed The Funeral Rule of 1984, which is now administered by the Federal Trade Commission.

Under this law, consumers have a right to transparency of costs and the right to buy separate goods (casket, memorial service, etc.) without being pressured to buy a package deal. You also have the right to see an itemized list of services, the right to use an alternative container for cremation, and the right to provide the funeral home with a casket or urn you purchased elsewhere, among many other protections.

Other Ways to Pay for Final Expenses

If you’re undecided about a final expense policy, or money is tight and you’re exploring options, consider some of these other ways to offset funeral expenses:

- Military Death Benefit. If the decedent was currently serving or is an honorably discharged veteran, there are some limited benefits available through the Veterans Administration, such as burial flags and headstones or grave markers. The VA will pay up to $2,000 for a service-related death for burial expenses on or after September 11, 2001, or $1,500 for deaths before that date. For a non-service-related death, the VA will pay $796 toward funeral expenses on or after October 1, 2019, as well as other monetary benefits if you qualify. You will need to meet several eligibility requirements and supply evidence of the death and expense costs to collect the benefit.

- Direct cremation. A simple, no-frills form of cremation that can cost as little as $400.

- Medicaid. If you are covered by Medicaid, see if any funds are available in your state for funeral expenses.

- Supplemental Security Income. Funeral expense coverage may be available if you are a low-income SSI recipient.

- Indigent burial programs. Check with your county’s department of social services to see if they offer this service.

- Body donation. Made to a local university medical school or private organization to support research and education.

- Burial on the family property. Some states allow this. Check local zoning laws and health regulations.

Pros and Cons: Is Final Expense Insurance a Good Deal?

Final expense insurance makes sense for some people more than others. Here are the pros and cons to decide if it’s the right kind of coverage for you.

Pros

- Easy to qualify, and in some cases, you’re guaranteed coverage.

- The application process is fairly short and simple.

- You have several different types of policies to choose from.

- Approval is generally quick, sometimes within 24 hours.

- Many different companies sell final expense insurance, giving you several options for coverage.

- You can get coverage even if you’re terminally ill.

- You’re covered if you die through an accidental cause.

- Coverage is affordable.

- Coverage is flexible, depending on your personal preferences.

- Benefits can be used for a variety of expenses.

- You can name anyone as a beneficiary.

- Premium costs remain level throughout the life of the policy

- You can’t be canceled, even if your health deteriorates.

- Your death benefit does not ever decrease.

- Your policy has cash value accumulation.

Cons

- Some policies have a graded two-year ramp-up period before benefits are paid.

- If you pass away during the graded period, your beneficiaries will only get your premium payments back, plus a little interest.

- This type of insurance tends to be more expensive, dollar-for-dollar, than life insurance with medical underwriting.

- The amount of the death benefit is relatively small. You’re limited to $25,000 per policy in most cases.

- Pre-existing medical conditions can make it more difficult to find coverage.

How Do I Buy Final Expense Insurance?

If you’re ready to purchase a final expense policy (or need other insurance assistance), one of our licensed and experienced agents in your area can help you out. All you have to do is give us a call and we can send someone your way.

Request a call or call us NOW for your free appointment at 833-GET-ENROLLED.