Welcome to the Medicare Plan Finder Healthy Living Challenge. As you age, it can become easier and easier to form unhealthy habits. We’re here to help you break those habits and live your best life!

In this 28 day health challenge, you can turn your life around and start a new healthy lifestyle. Making healthy choices should not be one-time decisions. Start by making small changes (like following this calendar), then look for other ways to live healthier.

The Challenge

28-Day Healthy Living Challenge | Calendar | MedicarePlanFinder.com

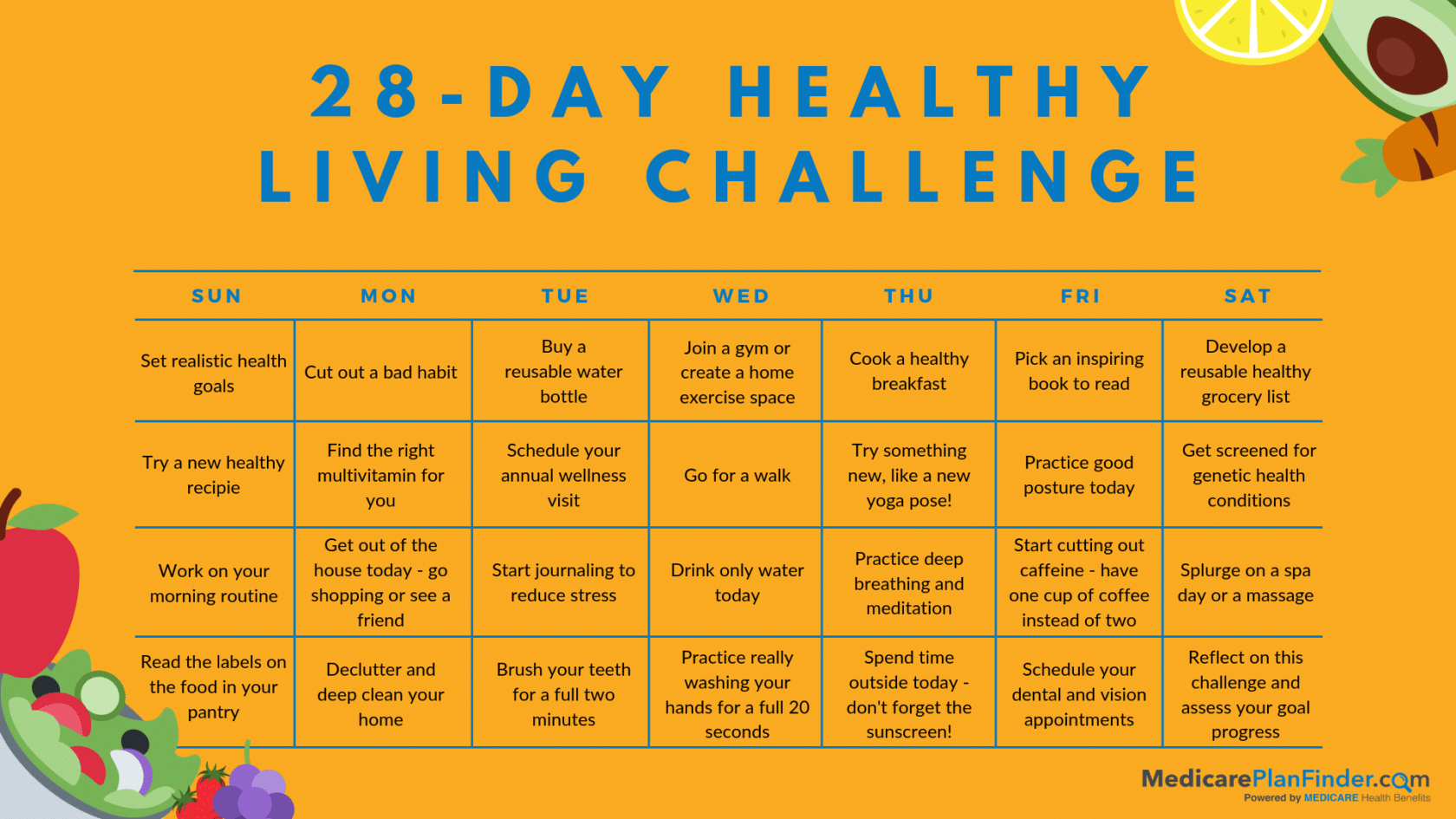

Set your health goals

Cut out a bad habit

Invest in a reusable water bottle

Join a gym or create a workout space in your home

Eat a healthy breakfast

Pick an inspiring book to read

Develop a healthy eating shopping list

Try a new healthy recipe

Invest in a multivitamin

Schedule your annual wellness visit

Go for a walk

Try something new

Practice good posture

Get screened for genetic health conditions

Work on your morning routine

Get out of the house

Start journaling to reduce stress

Drink only water

Practice deep breathing and meditation

Start cutting out caffeine

Splurge on a spa day or massage

Read the labels on the food in your pantry

Declutter and deep clean your home

Brush your teeth for a full two minutes, and make it a habit

Wash your hands for a full 20 seconds, and make it a habit

Spend time outside, but don’t forget the sunscreen

Schedule your regular dental and vision appointments

Reflect on the Healthy Living Challenge and assess your health goal progress

Day One: Set Realistic Health Goals

Start the Healthy Living Challenge by talking to your doctor or taking the time to sit and think about your health. What can you improve on? What needs to change? Think about your weight, your diet, your blood test results, your daily habits, etc.

Remember that to start a new healthy lifestyle is to do more than eat your vegetables and exercise – you also have to keep a rounded diet, exercise safely, engage in social activities, reduce stress, drink plenty of water, and more. Set goals like getting your cholesterol back to a healthy level, losing a few pounds, or drinking eight glasses of water per day.

Day Two: Cut out a bad Habit

On the second day, think about your daily routine, and cut out a bad habit. It can take a full 28 days to break a habit, so it’s a good idea to think about this early.

The habit could be anything from sitting on the couch for too long to overworking yourself. Or, it could be something like eating too much sugar or staying up too late.

Cutting out your bad habit can be one of your S.M.A.R.T health goals. Take day two of this Healthy Living Challenge to really focus in on that one bad habit and think about how you can put an end to it.

Everyone’s water needs can be different, so be sure to check with your doctor before taking our medical advice. The amount of water you need each day can depend on your individual healthcare needs.

Day Four: Join a gym or Create a Home Exercise Space

Creating a home exercise space can be as simple as buying a yoga mat and a few ten-pound weights, or as complicated as investing in equipment such as a treadmill. Alternatively, join a gym! If you have a Medicare Advantage or Medicare Supplement plan, you may be eligible for a Medicare fitness program, such as SilverSneakers® or Silver and Fit®.

Day Five: Cook a Healthy Breakfast

Too many of us eat unhealthy breakfasts or skip the meal altogether. It’s easy to eat unhealthy, especially in the morning, when you’re tired and rushing to get on with your day. However, sometimes preparing a healthy meal is just as easy as pouring a bowl of sugary cereal.

Consider focusing on superfoods in the morning, like a handful of blueberries coupled with a kale and tomato omelet. Or, start by making small changes like reaching for less sugary cereals in the grocery aisle and replacing your white bread toast with whole wheat.

Day Six: Pick an Inspiring Book to Read

Sometimes all that you need to take charge and start a new healthy lifestyle is a motivating book. We found the following healthy aging books available on Amazon:

Build a grocery list that you can take with you every time you visit the grocery store. This grocery list can help you stay on track and prevent you from grabbing unnecessary items like sugary desserts. Add items like 2% milk instead of whole milk, lean chicken breasts instead of fatty steaks, and wheat bread instead of white bread.

Day Eight: Try a new Healthy Recipe

Now that you have a start to your grocery list, take a look at some healthy recipes that you can make with your healthy ingredients (you may need to add a few items to your list). We found these cookbooks on Amazon:

If you’ve had a blood test recently, talk to your doctor about your results and find out if you lack any crucial vitamins. Then, ask your doctor if you should be taking any supplements or multivitamins. You can usually get multivitamins over the counter at any pharmacy or grocery store. Taking a multivitamin is an easy positive step you can take towards better health.

Day Ten: Schedule Your Annual Wellness Visit

Have you been attending your annual wellness visits with your doctor? Medicare covers an annual wellness visit for all beneficiaries. This visit is your chance to ask your doctor about any possible health concerns you have, and to request tests and screenings for various illnesses that you’re worried about. Remember, it’s always best to get ahead of your health and start healing before your symptoms worsen.

Day Eleven: Go for a Walk

Getting your daily exercise does not necessarily have to mean an intense cardio workout. Especially as you’re getting older, you have to be careful about over-exerting yourself and getting hurt. Today, go for a walk around your neighborhood or at a local park. Even a one-mile leisurely walk can lift your spirits and boost your metabolism. Consider taking your grandkids to the park for even more fun!

Day 11: Go for a walk!

Day Twelve: Try Something new!

Trying something new, no matter what it is, can positively alter your mood and motivate you to make the most of your days. While there is certainly value in having a daily routine, think about new things that you’ve always wanted to try. It can be a physical, mental, emotional, or social task! Consider trying yoga for the first time, taking yourself out to a new restaurant, or taking a painting class.

Day Thirteen: Practice Good Posture Today

You could be hurting your back every day without even knowing it. Pay extra attention today to the way you sit, stand, and bend over to pick things up. Practice always bending with your knees instead of your whole back, and practice straightening your shoulders as you sit and stand.

If you notice pain or discomfort, consider visiting a chiropractor. Medicare covers spinal manipulation when necessary, and some Medicare Advantage plans may cover other chiropractic services.

Day Fourteen: Get Screened for Genetic Health Conditions

If you didn’t already talk to your doctor about this, think about getting some genetic tests for familial health conditions. About one in every three people develop some form of cancer, and some of those cases are hereditary. The best way to beat cancer is to stop it before it develops and spreads.

A genetic test is the first step in determining whether or not you might need to prepare. The new myPath melanoma test is a popular one that your Medicare plan may cover.

Day Fifteen: Work on your Morning Routine

While it may seem small, your morning routine can impact your entire day. If you’re someone who has “bad” morning habits like sleeping in too late or skipping breakfast, use today to come up with a plan to adjust your routine and develop healthy habits. Try things like starting a morning workout regimen or opening the blinds before you go to bed so that the sun gets you out of bed earlier.

Day 15: Work on Your Morning Routine

Day Sixteen: Get out of the House Today – Go Shopping or see a Friend

A lot of adults can get into the habit of getting home from work and sitting on the couch for hours. Retired adults sometimes go a full day or longer without even leaving the house!

If that sounds like you, make an extra effort today to leave your house and do something. Your effort can be as small as going to the grocery store and running errands, or as large as spending all day with a friend. Figure out what works for you and make it happen today.

Day Seventeen: Start Journaling to Reduce Stress

If you’ve been feeling stressed or depressed lately, one great way to lift your spirits is to start journaling regularly. If you don’t have one, buy a journal or a notebook today and jot down notes about how you’re feeling, why you’re feeling that way, and what you’re going to do to try to fix it. Some people find happiness in just writing about what they did throughout the day!

If journaling is not helping or if you have a more serious mental health issue, please know that you CAN get the care you need. If you have Medicare, many of your treatments and appointments may be covered.

If this is an emergency, please call the Suicide Prevention Hotline at 1-800-273-8255.

Day 17: Start journaling

Day Eighteen: Drink Only Water Today

Did you buy that water bottle on day three? Today, focus not only on drinking at least eight glasses of water but also not drinking anything else. That means no juices, no alcoholic beverages, no coffee – none of it.

If you’re worried about cutting out caffeine, you may be surprised to find that the effects of drinking all that water can eliminate your caffeine withdrawal. Sticking to only water can also help you lose weight, reduce your appetite, and even increase your focus.

Day Nineteen: Practice Deep Breathing and Meditation

In this crazy world, it’s easy to get caught up in the stressful moments and forget to sit back and breathe. Spend some time today sitting and reflecting. Turn off your phone and the TV, find a comfortable place in your home, and allow yourself to reflect on whatever is stressing you out.

Practice deep breathing exercises and meditation. If you don’t care for yourself emotionally, you run the risk of your health declining physically.

Day Twenty: Start Cutting out Caffeine

Whether coffee, tea, soda, or something else is your caffeinated guilty pleasure, it might be time to cut back. Coffee and tea are healthy in small doses, but too much can lead to anxiety, insomnia, digestive problems, and high blood pressure.

If you drink more than one cup of a caffeinated beverage per day, or even if you only drink one but want to cut back, make today your first step. Drink one cup instead of two, or switch to decaf in the afternoon.

Day Twenty-one: Splurge on a spa day or a Massage

You may have learned from day 13 that posture is incredibly important, and you might not even realize that you hurt your posture. Use day 21 of this Healthy Living Challenge as an excuse to treat yourself to a nice massage or a day at the spa. Alternatively, schedule an appointment with your chiropractor!

Day Twenty-two: Read the Labels on the Food in Your Pantry

Common pantry items like canned soup and vegetables and pastas are often diet staples, but they could be doing more harm than you think. Canned soups are a great example. On the basic level, they are healthy…but they contain more sodium than you could even imagine! Use today to read the labels on the food items in your pantry and recognize what you could be putting into your body. You may decide to think twice the next time you’re shopping for those items!

Day Twenty-three: Declutter and Deep Clean Your Home

Whether you’re too busy, too tired, or just don’t feel like doing it, chances are there is at least one room in your home that could use some tidying. You probably haven’t thought of cleaning as a health-conscious activity, but decluttering and cleaning can prevent trips and falls, can improve the air quality in your home, and might even uncover some items you can sell for extra cash. If you can’t do it yourself, ask family for help or pay a cleaning service to come in and help you out.

Day 23: Deep Clean Your Home

Day Twenty-four: Brush your Teeth for a Full two Minutes

Dentists recommend that you brush your teeth for a full two minutes, twice per day. How long do you brush your teeth, and are you reaching every tooth? Some electric toothbrushes come with built-in timers, or you can put a kitchen timer in your bathroom to keep yourself honest. Healthy teeth lead to improved overall health, so this is crucial.

Day Twenty-five: Practice Really Washing your Hands for a Full 20 Seconds

People make the same mistake with hand washing as with teeth brushing. Every time you wash your hands – whether it’s after using the bathroom or before you eat – the CDC recommends that you wash thoroughly for at least 20 seconds. Be sure to lather every part of your hands with antibacterial soap before you rinse.

Day 25: Wash your hands for 20 seconds

Day Twenty-six: Spend Time Outside Today – Don’t forget the Sunscreen!

Spending time outside increases your Vitamin D intake, elevates your mood, improves your concentration, and can even help you sleep at night. However, even if it’s winter and you don’t feel the sun, you are still exposed to it and should wear sunscreen. Wearing sunscreen isn’t only about protection from burns; it also protects you from general sun exposure that leads to wrinkles and discoloration.

Plus, sunburn does more than just make your skin red and itchy – it can lead to skin cancer! Protecting your skin from the sun is more than just a good idea, it’s necessary for your health. Be sure to apply sunscreen every time you expect to be outside for more than a few minutes.

Day Twenty-seven: Schedule your Dental and Vision Appointments

Dental and vision appointments tend to feel less important than general doctor visits, because you may not notice that you are developing cavities or that your eyesight is worsening. Be sure to keep up with your annual (or bi-annual) dental and vision appointments.

Day Twenty-eight: Reflect on the Healthy Living Challenge and Assess your Goal Progress

Congratulations! You’ve made it through our 28-day Healthy Living Challenge. Moving forward, your goal should be to turn everything you did this past month into long-term habits. Drink eight glasses of water every day, get outside as much as possible, go for walks, and eat healthily. Find creative ways to reduce stress, declutter, and socialize with your friends, family, and neighbors.

For day 28, think about the S.M.A.R.T goals that you started with. Did you meet your goals, or at least make progress? What do you need to do next? If you need to follow up with a doctor, but you don’t have the coverage you need, maybe your next step needs to be reaching out to an insurance agent.

Do you qualify for Medicare? You can try to get a Medicare plan by yourself, but it doesn’t cost anything to meet with an agent, and there is never any obligation to buy.

Your agent can help you assess your needs and pick the plan that works best out of all your available options. Just call833-567-3163 to schedule your appointment.

This is only the beginning. Congrats on starting the path to a healthier you!

5 Medicare Enrollment Periods & What You Can Do During Each One

Did you know there are five different Medicare enrollment periods? You may qualify to enroll or make changes to your current coverage and have no idea! AEP is just a few months away, so we’d like to share with you what you can do during the various enrollment periods so you are properly prepared.

Initial Enrollment Period

Your Initial Enrollment Period (IEP) is typically your first opportunity to enroll in Medicare. Your IEP is three months before your 65th birthday and three months after. This gives you a seven-month window to enroll in your preferred coverage.

In most cases, if you do not enroll in Part A and Part B (Original Medicare) during your IEP, you will be charged a late enrollment penalty fee that will be added to your monthly Part B premium. If you do not have prescription drug coverage, you should also consider enrolling in a Part D plan to avoid other penalties down the road. You are not required to enroll in a Medicare Advantage or Medicare Supplement plan, but you should consider enrolling to optimize your coverage.

The General Enrollment Period (GEP) is for those who are enrolling in Medicare for the first time but missed their IEP. The GEP runs from January 1 to March 31 each year, and coverage will begin in July.

During the GEP, you can:

Enroll in Original Medicare if you missed your IEP

*If you enroll for the first time during the GEP, you can follow up by enrolling in a Medicare Advantage plan during a period from April 1 through June 30.

Annual Enrollment Period

The Annual Enrollment Period (AEP) runs from October 15 to December 7 each year. During this time, all Medicare beneficiaries can make changes to their plans. You may not need to do anything during AEP. However, major insurance carriers can change the benefits that they offer every year. It’s possible that a change in your plan benefits or your provider network will change how you feel about your plan. Ultimately, it’s always a good idea to speak with an agent. Any changes you make during AEP become effective on January 1 of the following year.

Most people can only make changes to their plans once a year (during AEP), but if you qualify for a Special Enrollment Period you can make those changes during different times of the year or even all year long. Lifelong SEPs allow you to change plans once every quarter for the first three quarters of the year. Circumstantial SEPS allow you to change plans once following a particular event.

Starting in 2019, there will be a new “Medicare Open Enrollment Period” that will run from January 1 through March 30. OEP was created for anyone who signs up for a Medicare Advantage plan during AEP to enroll in a different plan, without having to wait until the following fall. You do not have to do anything during OEP unless you are unhappy with the coverage you enrolled in during AEP.

Change from Medicare Advantage to Original Medicare only, with the option to add a prescription drug plan

Contact Medicare Plan Finder

Are you looking to enroll in Medicare Advantage, Medicare Supplements, or Part D? Are you still confused on which Medicare enrollment periods you qualify for?

Our agents at Medicare Plan Finder can answer any of your questions and simplify the enrollment process. They are contracted with most of the major carriers in your state so the agent should not show bias when enrolling. To speak with a licensed agent and to learn about plans in your area, click here or call 844-431-1832.

This blog was originally published on 10/23/18 and was updated on 7/15/19.

Silver and Fit® vs Silver Sneakers® Medicare Fitness Programs

Wishing you could afford a gym membership or a yoga class? You might be able to get the coverage you need with a Medicare fitness program.

As you age, regular exercise and healthy habits become more and more important. In fact, a regular exercise program can help prevent everything from falls around the home to diabetes!

Thousands of gyms across the country offer a Silver & Fit® or SilverSneakers® Medicare fitness program, and several Medicare Advantage plans actually include those programs as benefits (at no extra cost)! Maintaining a healthy lifestyle just got that much easier!

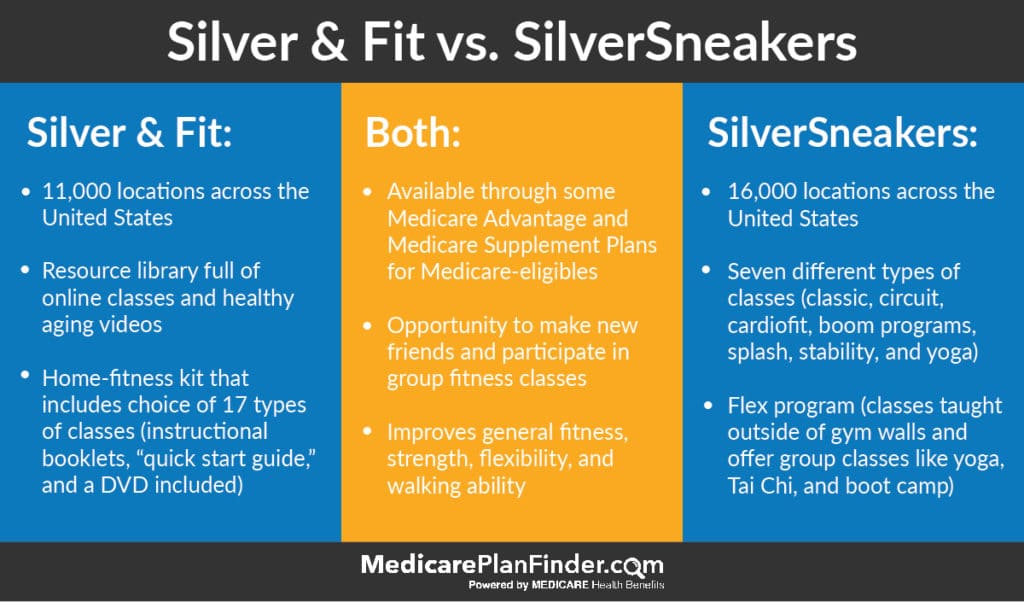

Are SilverSneakers ® and Silver and Fit ® the Same?

SilverSneakers® and Silver and Fit® are both Medicare fitness programs, but they are not the same. They are two separate companies offering similar benefits.

Both companies offer group fitness classes and exercise opportunities, and both companies partner with Medicare Advantage and Medicare Supplement plans to provide their benefit.

SilverSneakers ® vs Silver and Fit ®

Silver and Fit ® vs. SilverSneakers ® | Infographic | Medicare Plan Finder

The main differences between the two programs are the locations, the types of classes, and the availability of home fitness. Silver and Fit® eligibility and SilverSneakers® eligibility are generally the same.

Each program partners with a number of different gyms and wellness centers across the country. It is possible that you may have access to more gyms with one program than the other, so it’s a good idea to check for locations in your area before making a decision (scroll down to see our location lists for each program).

Silver and Fit® offers “home fitness kits” for people who do not have a gym in their area or are not able to get to a gym for any reason. On the other hand, SilverSneakers® offers a broader range of group fitness classes.

If you have access to both programs, picking the best one for you may require that you decide if you prefer group fitness classes or home fitness kits. Read on for a more in-depth view of each program.

SilverSneakers ® Medicare Fitness

In a nutshell, SilverSneakers® is a fun exercise program for seniors. It is a fitness benefit found in many leading Medicare insurance plans that help provide guidance and convenient group exercises to improve general fitness, strength, flexibility, and walking ability. These classes can also help seniors and Medicare eligibles find new friends who also want to pursue an active lifestyle.

How do you get a Medicare Fitness Program like SilverSneakers ®?

This fitness service is not covered by Original Medicare (Part A and B). If you are interested in enrolling in a Medicare fitness program, you will need to be enrolled in a Medicare Advantage or Medicare Supplement plan that supports it.

Fitness programs are not included in every Medicare Advantage or Medicare Supplement plan, so it’s important to discuss your coverage options with a licensed agent. They can help you purchase a plan that fits your needs and budget and includes a fitness program.

SilverSneakers ® and Silver and Fit ® Insurance Providers

While we can’t list out the current SilverSneakers® and Silver and Fit® insurance providers (they are always changing), we can tell you that many of the “major” carriers that you’ve heard of offer these programs as a part of their Medicare Advantage plans.

If you’re interested, we can set you up to chat with a licensed agent who knows everything about what plans are available in your area today. Just call 800-531-3748 or click here.

SilverSneakers ® Eligibility

To meet SilverSneakers® eligibility requirements, you must be at least 65 years old and enrolled in a Medicare plan that includes the SilverSneakers® benefit.

Many leading Medicare Advantage plans, as well as a few Medigap plans, include automatic Silver Sneakers® eligibility. The best part is that this is available to you – if you qualify – at no cost! How do you figure that part out? Well, fill out this form or call us at 800-531-3748!

Medicare Workout Programs

There are numerous workouts you can choose from. These include classic, circuit, cardio-fit, yoga, splash, stability, etc. A workout is typically 45 to 60 minutes, twice a week. These classes are total body conditioning workouts and often involve hand-held weights, elastic tubing for resistance exercises, and small exercise balls. In some classes, participants may use chairs for additional support and balance.

The classic workout focuses on low-impact training that is suitable for all fitness levels. This workout is designed to increase your muscle strength and range of movement. There is typically a chair that incorporates seated exercises and offers a great start to living a healthy lifestyle.

They also offer indoor and outdoor exercise opportunities. Some locations have yoga on the beach, exercises in a neighborhood park, or other fun outdoor exercise opportunities!

Medicare Fitness Programs | Medicare Plan Finder

SilverSneakers ® Go

In early 2019, SilverSneakers® released an app just in time for New Year’s resolutions. The app allows you to access your member ID and digital card. It can track and schedule the various classes and activities available to members. Plus, it even shows locations and classes near you, which is great if you are traveling in a new area.

Senior Yoga Classes

Many of the gyms that accept SilverSneakers® and Silver & Fit® include classes, like aerobics, yoga, etc.

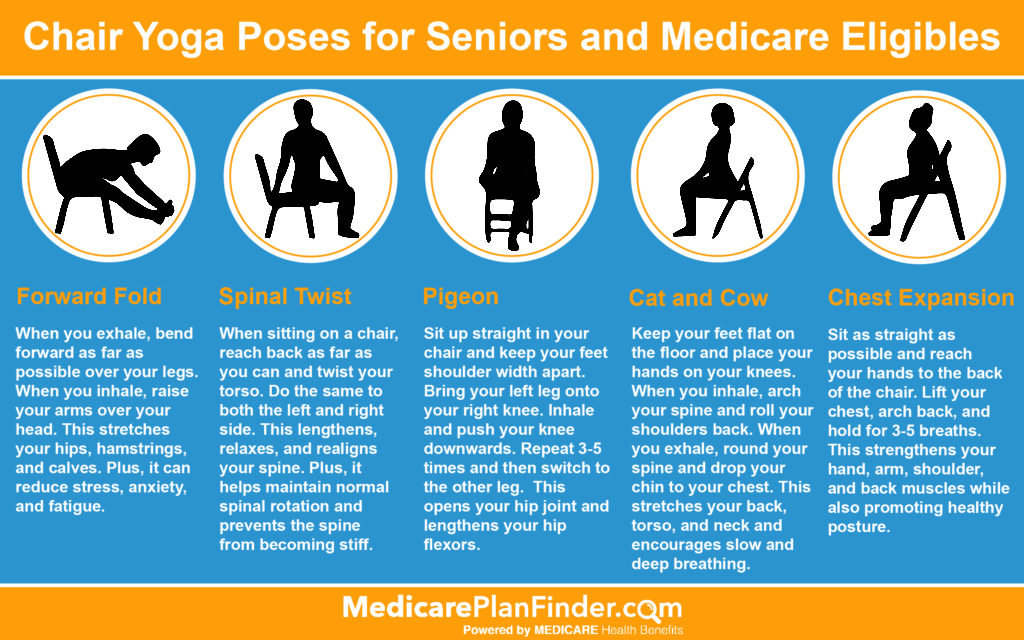

SilverSneakers® yoga classes provide a unique opportunity for seniors and Medicare eligibles to practice yoga in a judgment-free, inclusive group. These classes may incorporate chair yoga poses for seniors and Medicare eligibles.

Senior Yoga Poses | Medicare Plan Finder

SilverSneakers ® Eligible Gyms and Locations

There are over 16,000 SilverSneakers® locations across the United States. These locations include gyms, wellness centers, and YMCAs. Additionally, each location can provide equipment demonstrations.

Are you in Tennessee? Read this: YMCAs in Tennessee will no longer be accepting SilverSneakers®.

Once enrolled, you have access to any of these participating facilities. Enrollees receive a list of local participating facilities, including addresses and phone numbers.

We’ve compiled lists of SilverSneakers® locations based on where most of our audience is located. If your location is not listed, click here.

Did you mean SilverSneakers®? If you’re searching for Silver Slippers, you may be getting confusing it for SilverSneakers®. If you are genuinely looking for silver slippers, we found a great pair that can be purchased here. Otherwise, if you have any other questions regarding SilverSneakers®, fill out this form and we will get in touch with you!

Have more questions specific to SilverSneakers®? The SilverSneakers® phone number is 866-584-7389.

Medicare Fitness Programs | Medicare Plan Finder

Silver & Fit ® Programs

This program includes multiple benefits that are available to seniors and Medicare eligibles like you. These benefits include a fitness facility program, home fitness program, a resource library, fitness challenges, rewards program, and more! Depending on your coverage, there may be no additional fees to join. This is great if you are on a budget and looking to live a healthy lifestyle.

The body conditioning classes that are designed to increase your strength, endurance, stamina, flexibility, balance, and more. A class is typically an hour in length and is offered several times a week. The program incorporates weights, elastics, and balls into the workouts.

One of the many perks of Silver and Fit is the balance between fitness facility programs and home fitness programs. Home fitness programs offer various kits including walking, yoga, chair Pilates, stress management, Tai Chi, and aquatic exercise. This is a great option for seniors and Medicare eligibles who need focused exercise in their home.

Other program benefits include gender-specific gyms and exercise centers beyond the average fitness facility. These facilities can include yoga and lap pools.

Silver and Fit Eligibility and Age Requirements

To be eligible for Silver & Fit®, you must be age 65 or older and enrolled in Medicare.

Original Medicare (Parts A and B) does not cover this fitness program. Certain Medicare Advantage and Medicare Supplement plans offer this program.

To find out if your current Medicare Advantage or Medicare Supplement plan includes Silver and Fit eligibility, click here or call us to speak with a licensed agent at (833) 567-3163.

What is the Annual Fee for Silver & Fit ® ?

Fees for Silver & Fit® can vary based on your Medicare plan. You may be asked to pay an annual Silver & Fit® membership fee, or your Silver & Fit® benefit might be rolled into your Medicare plan premium.

SilverSneakers | Medicare Plan Finder

Silver and Fit Locations (Fitness Centers and Gyms)

If you choose to enroll in this program, you will have access to over 11,000 Silver and Fit gyms and locations nationwide. These locations can include gyms, wellness centers, and YMCAs. Once you have your Silver & Fit® membership info, you can select a gym. Just be sure to call the gym and verify that they are participating in the Silver & Fit® program.

We’ve put together a few quick lists based on where the majority of our audience lives. If your location isn’t listed, go to silverandfit.com to find locations near you.

Have more questions specific to Silver & Fit®? The Silver and Fit phone number is 1-877-427-4788.

Get Medicare Fitness Benefits NOW!

It’s never too late to start exercising. Active lifestyles are important for maintaining your health and quality of life. Exercise can benefit older adults mentally and physically. Moderate exercise can help alleviate stress and potentially reduce feelings of depression. Plus, regular exercise may be able to improve mental function.

Participation in a Medicare fitness program can help improve your strength, balance, and endurance. Participating in a healthy lifestyle encourages independence.

If you have any questions or are interested in exploring Medicare coverage, complete this form or call us at (833) 567-3163.

This blog was originally published on 10/1/18 by Kelsey Davis was most recently updated on 11/13/19by Anastsia Iliou.

The Shocking Truth About Medicare and Dermatology

Does Medicare cover dermatology?

Medicare coverage for dermatology can be quite limited. If you or your loved one needs treatment NOW, take a look at your coverage before it’s too late and you’re stuck with a big bill!

Medicare Part B can cover some dermatology services. If your condition is medically necessary, Part B will cover doctor services relating to evaluating, diagnosing, or treating skin conditions. Medicare will not cover cosmetic treatments, and it will only cover skin cancer screenings if you are showing symptoms.

How Does Medicare Cover Dermatologist Visits?

Dermatologist and Patient | Medicare Plan Finder

For dermatology-related services, you will have to meet your Part B deductible first. For most people in 2019, the deductible will be $185.

Then, Medicare will usually pay 80% of the service cost. You will be responsible for the remaining 20%. For Medicare to cover that 80%, your dermatologist or physician must accept Medicare assignment. Your doctor should be able to tell you whether or not they accept assignment, but if you’re not sure, your insurance carrier or insurance agent can help you.

Some Medicare Supplement (otherwise known as Medigap) plans can cover the rest of your costs, like your deductible and the remaining 20%. If you’re interested in investing in a Medigap policy, one of our agents can help. Click here to get started on setting up your free Medicare Plan Finder appointment.

Uniquely, Medicare plans are now able to cover MyPath, a genetic test for malignant melanoma.

How Much Does It Cost to Go to a Dermatologist With Medicare?

Dermatology costs vary based on what insurance you have, where you live, and what services you need. If you have Medicare (demonstrated above), you will likely be responsible for 20% of services. Some dermatologists accept Medicaid as well.

Keep in mind that in the cases of Medicare and Medicaid, your care will most likely not be covered unless it is determined to be medically necessary. For example, acne care is not generally considered a medically necessary treatment plan, but skin cancer removal is.

Thankfully, dermatology visits are not typically wallet-breaking. Depending on what doctor you see, where you live, and what services you require, The Law Dictionary says you may only need to pay between $100 and $200, which is a low cost compared to other health services, like hospital stays.

Do You Need a Dermatologist?

We’re not doctors, but chances are that if you’re asking this question, you should go and see a dermatologist.

Some skin conditions that you may start to notice as you age are dry and itchy skin, benign growths, loose skin (especially around the eyes, cheeks, and jawline), transparent or thin skin, spotting, wrinkles, and easy bruising.

While those are all certainly typical signs of aging, there are steps you can take to keep your skin healthy and prevent further damage, like:

Don’t stay in direct sunlight for long periods of time.

Always use a sunscreen with SPF 30 or higher when spending time outdoors.

Stay away from tanning beds.

Check your skin or have a loved one check your skin for new growths or moles that appear to be changing in color or size.

See a dermatologist whenever you face a new concern!

Questions to Ask Your Dermatologist

Patient Asking Dermatologist Questions | Medicare Plan Finder

Knowing what questions to ask your doctor can be a challenge, especially if you are really unsure of what’s wrong. We searched the internet and compiled this list of questions you may want to ask your dermatologist:

What foods should I avoid for my skin health? What should I be eating more of?

How can I slow down signs of aging, like wrinkles and dark spots?

How can I check my own moles and how do I know when to call you?

What lotions and sunscreens do you recommend?

These are the skin products I use now (list sunscreens, lotions, exfoliators, makeup, etc.). Are they damaging?

How to Find a Dermatologist

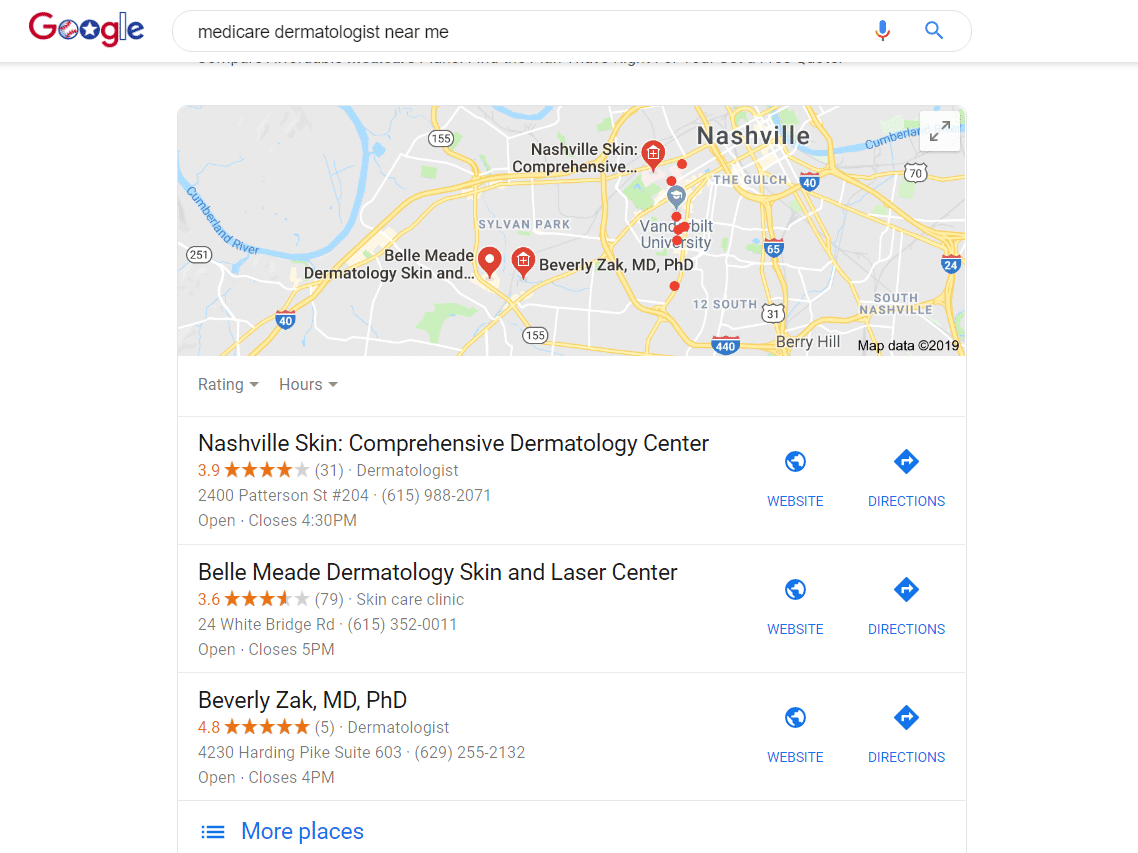

To find a dermatologist near you, you can visit a site like “doctor.com” or perform a Google search. Usually, searching for “dermatologist near me” pulls up reasonable results. For example, these are the results when we searched from our office in Nashville.

Once you’ve looked at reviews and found some good dermatologists in your area, make sure they accept Medicare. If you have another plan that you’re using, like Medicare Advantage, make sure the dermatologist is in your plan network.

Dermatologists are specialists. If you have an HMO (Health Maintenance Organization) plan, you may need a referral from your primary physician before you can see a dermatologist. If you aren’t sure whether or not you need a referral or if you need help finding a dermatologist that is in your network, call your insurance agent!

A highly trained, licensed insurance agent can help you walk through the process of finding providers in your network and can help you make sure you have all the coverage you need. Don’t have an insurance agent? To set up an appointment with your new agent, give us a call at 844-431-1832.

Contact Us | Medicare Plan Finder

*This post was originally published on June 28, 2018, and updated on July 3, 2019.

Get Middle Tennessee Dental Care with Medicare and Interfaith Dental

Nashville and Middle Tennessee residents don’t have to suffer from a lack of affordable dental coverage. In 1994, Dr. Tom Underwood founded Interfaith Dental with the help of the Nashville Dental Society and the Outreach Commission of West End United Methodist Church.

Interfaith Dental makes it possible for low-income families to access the dental care they need without having to pay full price.

Low Income Dental Clinics in Middle Tennessee

Middle Tennessee has quite a few public health clinics, and many specialize in dental care for low-income families and individuals. We work closely with Interfaith Dental, located both in the Fesslers Lane/Elm Hill Pike area of Nashville and near the St. Thomas Rutherford Hospital campus in Murfreesboro. Below are some of the low-income dental clinic options you have in Middle Tennessee.

Not located in Middle TN? That’s ok – there are plenty of low income dentists throughout the country. This government website is operated by the Bureau of Primary Health Care, a part of the Health Resources and Services Administration. You can use their tool to find a federally-funded community health center that offers dental services.

Additionally, you can search through the American Dental Association or the American Dental Hygienists’ Association to find supervised, low-cost care that is part of the training program for dental students. Your care will be supervised by licensed and experienced dentists. If you have Medicare, we can help you make sure you have the best Medicare plan to get you the dental services you need and help you find the best dentist that accepts Medicare.

Who is Interfaith Dental (IFD)?

Interfaith Dental is a low income dental clinic with a mission to “create a healthier community by providing transformational oral health care for those experiencing poverty.” They envision a Middle Tennessee community where every resident “has the opportunity to achieve and sustain a healthy smile,” regardless of income status.

When it began in 1994, IFD only had two chairs and one employee, operating out of the West End United Methodist Church basement. By 1998, they were able to move their operation to 1721 Patterson Street (just off West End, near the St. Thomas Midtown campus).

In 2012, they opened another clinic in Murfreesboro, expanding their reach into Rutherford County. In even bigger news, this past year (2019), the clinic was able to expand into a new office at 600 Hill Avenue (near the Fesslers Lane/Elm Hill Pike intersection).

They’ve come along way from their two-chair operation, now owning 26 state-of-the-art dental operatories.

How to Become an Interfaith Dental Patient

Since the Interfaith Dental Clinic offers such low-cost dental care, there is an application process before you become eligible for services. To be eligible, you must be legally considered low-income (living below the poverty line), uninsured, and suffering from a devastating dental disease.

To get more information or to schedule your first appointment, call 615-329-4790 for the Nashville office, or 615-225-4141 for the Murfreesboro office.

Your Interfaith Dental journey will begin with a phone questionnaire. You’ll be asked for some basic information which will determine if you are eligible for Interfaith Dental Clinic services and what services you need.

Next, the Patient Care Coordinator that you speak with will tell you when the next “Application Day” is. On that day, you’ll come into the office to complete your application. Both the Nashville and Murfreesboro locations have the same office hours in 2019, which are:

Monday through Wednesday, 8 AM to 4 PM

Thursdays, 1 PM to 7:30 PM

Fridays, 8 AM to 12 PM

Be sure to bring the following items with you on “Application Day”:

Current Year Tax Return

Two current pay stubs for anyone working in your household.

If you are paid in cash, provide written documentation from your employer on a business letterhead that contains the business name, address, phone number, and owner information as well as your hire date, hours worked per week, pay rate, and hourly income.

College students, bring your class schedule

Work training program participants, bring proof of enrollment.

65+, provide social security/pension/retirement proof of income.

Proof of address (utility bill, bank statement, etc.)

TN driver license

Referral from medical professional, social worker, or employer (if you have one)

Due to high demand, there may be a waiting period for your services. There are a limited amount of applications that are handed out on a first-come, first-serve basis every month.

While walk-ins are generally not accepted, please call Interfaith Dental if you have a dental emergency. Some emergency services are offered on a first-come, first-serve basis.

What to Expect from Your First Interfaith Dental Appointment

At your first Interfaith Dental Clinic appointment, you’ll begin by meeting the team members. Then, someone will sit with you to review your medical and dental history and discuss all of your dental concerns.

Interfaith Dental care is comprehensive – they want to know how your dental health has affected your career, your family, and even your self-confidence. Is your goal to have a beautiful smile again, or to eliminate pain? Your care providers will hear all of your concerns and follow up with the best possible care.

The next step of your first appointment is a series of full diagnostic X-rays and oral exams that will help the doctors determine a treatment plan. Phase one will usually include fillings, cleanings, and extractions, and phase two will include crowns, root canals, and even partial dentures, if necessary.

If that sounds like a lot, it’s because it is. Your first appointment with Interfaith Dental can take up to two hours, in some cases – so be sure to allow that much time out of your day.

Original Medicare only covers dental services when they are part of a hospital stay.

For example, if you go to the St. Thomas emergency room with a fractured jaw and need emergency dental care in the hospital, those services may be covered by Medicare Part A. However, common dental services and treatments such as annual exams, cleanings, root canals, dentures, implants, etc. are not covered by Original Medicare.

To get Medicare dental coverage, you’ll need to either enroll in a private, individual dental plan or a Medicare Advantage (Part C) plan. Medicare Advantage plans, even though they are Medicare health plans, are operated by private insurance companies, which allow them to add benefits that the Original Medicare program does not cover. This can include not only dental benefits but also benefits like fitness programs, vision, meal delivery, etc.

Medicare Plan Finder and Interfaith Dental, Bringing Change Together

Medicare Plan Finder works with Interfaith Dental by helping their patients fill the gaps in their dental coverage. Interfaith Dental is not always able to provide free or very low-cost care. For example, there may be times where a $10,000 dental procedure costs $5,000 at Interfaith Dental. You’d still be paying $5,000 less than if you went to a regular dentist, but that $5,000 may be more than you can handle. At Medicare Plan Finder, we try to match you up with a low-cost insurance plan that can cover those extra out-of-pocket costs.

Start by scheduling your appointment at the Interfaith Dental Clinic located nearest to you. Call 615-329-4790 for the Nashville office, or 615-225-4141 for the Murfreesboro office.

Then, if your doctor determines that you need a series of procedures that you can’t afford (even with Interfaith Dental’s help), give us a call at 844-431-1832. We can help you determine whether or not you are eligible for Medicare (did you know you don’t have to be 65?). If you’re eligible, we’ll help you find low-cost coverage so that you can go back to Interfaith Dental to get the services you need.

Father’s Day 2019: Healthy Gifts for the dad who Wants Nothing

Are you one of the millions of people looking for gifts for the dad who wants “nothing?” Maybe this is the year that you can finally give him something other than a new tie. As dad ages, consider gifting him the education, care, and technology he needs to stay healthy.

Sometimes the best gift is not a physical object. Consider gifting your dad with:

Bringing him healthy meals or taking him out to healthy lunches

Fitness Gifts for Dad

One of the easiest ways to get dad a gift that encourages him to practice healthy habits is by looking at the fitness industry. These gifts not only say, “I love you,” but also allow you to be proactive for his health:

A gym membership (if he qualifies for Medicare, you can get him a gym membership by helping him sign up for certain Medicare Advantage plans).

List of Male-Specific Diseases

The best gift you can give your aging father is education and readiness for what life may throw at him next. Even if dad is healthy now, help him learn about diseases that he may be susceptible to. Is he nearing or over age 65? Help him also learn about different insurance options that he may not have heard about yet!

These are some male-specific diseases and diseases that are more likely to affect aging men than women. Remind your dad to look for the signs.

According to the Centers of Disease Control and Prevention (CDC), cancer is the 2nd leading cause of death for people over the age of 65. It’s extremely important for seniors and Medicare eligibles to remain proactive when it comes to their health. If cancer is caught early enough through screenings, it may be treatable. The most common cancers found in men are:

Prostate cancer

This type of cancer generally grows slowly and is initially found in the prostate gland where it may not cause extreme harm. However, prostate cancer can grow quickly and create bigger issues. If your dad is over 50 years old, African American, or if prostate cancer runs in your family, he has a higher risk of developing prostate cancer.

Colorectal cancer

Did you know colorectal cancer is the second leading cause of cancer-related deaths in the US? Colorectal cancer develops from abnormal growths called precancerous polyps. These growths can be removed before they turn cancerous, so it is vital to stay alert and proactive.

Medicare Coverage for Men

If your dad is eligible for Medicare, Medicare covers a digital rectal exam and a prostate-specific antigen (PSA) test once a year. In addition to these tests, Medicare covers numerous colorectal screenings like the fecal occult blood test, flexible sigmoidoscopy, and colonoscopies. Screenings are extremely important. The CDC says that close to 1,000 colorectal cancer deaths could be prevented each year if even 70.5% of people attended regular screenings.

Are you interested in exploring Medicare insurance available for you? Our agents can explain your coverage options and help you find a plan that best fits your needs and budget. If you are interested in arranging a no-cost, no-obligation appointment with an agent, complete this form or give us a call today at 844-431-1832.

*Originally published on August 16, 2018, and updated on June 13, 2019.

3 Heart Health Resources you Should use

It’s never too late to start making good decisions regarding your heart health. As you age, your risk of developing heart disease dramatically increases.

You can help manage the risk by taking an active role in maintaining your heart health, and using the free resources you have at your disposal, including:

1. Medicare Preventive Services for a Healthy Heart

Man at Medicare Wellness Visit | Medicare Plan Finder

Your doctor may be your best resource for keeping your heart healthy. Did you know you can get a free wellness exam every year if you have Medicare insurance?

The Medicare Annual Wellness Visit (AWV) may include measurements of your height, weight, BMI and blood pressure, which can help identify your risk of developing heart disease. During your AWV, your doctor can discuss action plans for your diet and exercise in order to help minimize your risk of developing a heart condition.

Medicare will also cover blood tests for cholesterol once every five years. The heart screening will measure your cholesterol, triglyceride and lipid levels. An electrocardiogram (EKG or ECG) will give your doctor a picture of your heartbeat. EKGs fall under medically necessary diagnostic testing. Medicare will pay for an EKG if your doctor orders one.

Work with your doctor to develop a diet and exercise plan. Medicare will cover medically necessary obesity screenings and nutrition counseling.

Some private health insurance policies called Medicare Advantage plans will cover fitness classes along with all of the wellness services Original Medicare covers. Talk to an agent about finding a Medicare Advantage plan that will allow you to keep your doctor and access every service you need.

2. Risk Tracking for an Accurate Picture of Heart Health

The American College of Cardiology offers CardioSmart for free. The website features a BMI calculator, a Heart Disease Risk Assesment, and a Cholesterol Calculator online (as well as a “Med Reminder” app to remind you to take your medication).

As you age, it becomes more important to track your weight, your cholesterol levels, and your overall diet. Additionally, you should look at your family medical history. Find out what kind of genetic risk you have for developing heart disease. If you have immediate family members with a history of heart conditions, that may indicate that you have a greater risk of developing cardiovascular disease.

3. Take Control of Your Diet and Exercise

Heart-Healthy Foods and Exercise Equipment | Medicare Plan Finder

Your risk for heart disease is closely linked to your weight. If you’re overweight or obese, you have a much greater chance of developing heart disease, and losing weight is one of the most effective ways to help prevent heart disease.

A 10 percent weight loss significantly reduces your heart disease risk. Consistent calorie tracking is one of the most important steps in losing weight successfully. It may seem difficult to track what you eat, but there are hundreds of tools out there that can help you. If you are at risk for heart disease, you’ll want to focus on eating lean proteins while cutting down on fats and sodium and increasing your fiber intake (whole grains, fruits and vegetables).

You can create your own tracking system by writing down what you eat every day, or you can try using an app that will store your information and help you figure out your caloric intake. MyFitnessPal is one example of a free app that is easy to use.

All you have to do is enter the foods you eat and any exercise you complete throughout the day. It’ll track your nutrition and your calories and tell you if you’re eating too much or not eating enough of any specific food group. The MyFitnessPal mobile app even has a feature that allows you to scan a package’s barcode and upload the food’s nutritional information.

Let us Help

A comprehensive health insurance plan is a great resource to help you stay healthy. Medicare Plan Finder agents can help you find a plan that covers the services you need while fitting your budget and lifestyle. Call us at 844-431-1832or contact us here to learn more.

Contact Us | Medicare Plan Finder

This post was originally published on October 12, 2017, by Anastasia Iliou and was updated on June 13, 2019, by Troy Frink.

A Guide to Hospital Indemnity Insurance

Medicare is a great resource for covering your healthcare costs, but it doesn’t cover everything. Are you spending more on hospital visits than you can afford? Are you or a loved one going to need assisted living or nursing home care soon?

Those services can be extremely expensive, and additional insurance coverage can provide the safeguard you need. Consider discussing ancillary products for short-term care and hospital indemnity insurance with your licensed agents

What Is Short-term Care Coverage?

Short-Term Care in Hospital | Medicare Plan Finder

Short-term care insurance is designed to provide hospital coverage for one year or less. Short-term plans are recommended for people who may become severely ill or injured or for anyone over 80.

These policies are especially beneficial for anyone staying in a nursing home or using an assisted living program. It can also help if you missed open enrollment and have to wait another year to apply for Medicare.

Pre-existing conditions will usually not affect your short-term care insurance. Premiums will rise with your age, so it’s important to get coverage early. Short-term coverage works fast; you can start receiving benefits as soon as the day after purchase.

Make sure to speak with an agent about your health conditions and your current coverage to determine if you need the extra coverage that short-term care insurance provides.

What Is Hospital Indemnity Coverage?

The word indemnity means protection from financial liability such as hospital expenses. Ancillary hospital indemnity policies are the best, cheapest way to save your piggy bank in the event of a hospital stay.

The average cost for one night in the hospital is between $1500-$3000 before any additional drugs or procedures that may be a part of your stay. The average hospital stay for seniors is 5.5 days.

Hospital indemnity plans can help make up for hundreds of dollars that you may be charged in the hospital. Your plan will have a set limit on the length of time you can spend in the hospital.

Hospital indemnity coverage can cost you as little as $12 per month depending on your financial needs and your potential for lengthy hospital stays. If you have or are eligible for a $0-premium Medicare Advantage plan with a high deductible, hospital indemnity insurance will help you cover those deductibles.

Everyone is eligible for hospital indemnity coverage, and your pre-existing conditions will not affect your ability to extend your coverage. One important note about hospital indemnity insurance is that you may have to wait for benefits used towards illnesses, but you most likely will not have to wait for accidental injury coverage.

How Does Hospital Indemnity Coverage Work?

To receive your benefits, you will need to make a claim immediately following your hospital stay, stating your expenses. You will receive a check directly in the mail from your carrier for a predetermined cash value (per hospital day).

For example, if your hospital copay is $400, you will need to pay $400 directly to the hospital. Your insurance carrier will then reimburse up to a certain amount, say, $250 depending on the specifics of your plan.

Since your reimbursement comes in the form of a check, you can use your hospital indemnity coverage for any services that you may need. Hospital costs are not limited to what shows up on your overnight bill. Consider the following additional costs:

Laboratory and radiology tests

Ambulance transportation

Emergency room costs

Outpatient surgeries

Hospital parking for you and any visitors

Post-hospital skilled nursing facilities

You can purchase hospital indemnity coverage at any time, but the closer you are to your Initial Enrollment Period (within the seven months surrounding 65th birthday), the lower your costs will be.

Start by setting up an appointment with your agent to discuss your options for ancillary insurance products that your Medicare plan does not cover.

Hospital Indemnity Insurance for Medicare Advantage

Private insurance carriers offer Medicare Advantage (MA) plans to cover many services Original Medicare does not. MA plans can offer coverage for services such as vision, dental and hearing in addition to hospital coverage and doctor’s appointments.

Hospital services, however, can still come with expensive copayments. You can use an indemnity policy to help relieve your out-of-pocket expenses and stay within your budget. Hospital indemnity coverage gives you a safety net to use in the event of a medical emergency.

Indemnity plans are different from PPOs because indemnity plans are not primary health insurance. For example, your PPO or HMO will often come with preventive services such as an annual wellness visit. Hospital indemnity insurance plans only reimburse all or part of your costs related to short-term care.

We Can Help You Find Hospital Indemnity Insurance Coverage

Hospital insurance can mean the difference between having huge hospital bills or paying a manageable premium and a deductible if you use hospital services.

A licensed agent with Medicare Plan Finder can help you find the policy you need to cover your healthcare needs. Call 844-431-1832or contact us here to arrange a meeting today.

This post was originally published on April 06, 2017, by Anastasia Iliou and was updated on May 30, 2019, by Troy Frink.

Prescription Help for Medicare Beneficiaries

For many people, prescription drugs are the most expensive part of health care. Some medications are so expensive that many people stop taking their prescriptions, and their health problems get worse. Thankfully, there are options for prescription help for Medicare beneficiaries.

Apply for LIS

You might be qualified for Extra Help, or Low Income Subsidy (LIS). Extra Help is a Medicare savings program based on income level. If your yearly income and total assets are at or below 150 percent of the federal poverty level, you may qualify for LIS. Some beneficiaries have saved nearly $4,000 per year by enrolling in LIS. If you’re not sure if you’re qualified, speak to your agent! We can help you look over the qualifications and go through the application process.

If you qualify for LIS, you might also qualify for Medicaid. If you’re eligible for both Medicare and Medicaid, you qualify for Dual Special Needs Plans (DSNP), which are a type of Medicare Advantage plan. DSNPs typically provide coverage for doctor appointments, hospital services and prescription medications.

If you have a DSNP, you will also qualify for a Special Enrollment Period (SEP), which allows you to enroll in new plans or make changes to your existing coverage at any time throughout the year, rather than having to wait for certain times.

Special Needs Plans | Medicare Plan Finder

Change Your Medicare Plan

If you don’t qualify for a SEP, you will have to wait for the Annual Enrollment Period (AEP) to make changes to your coverage or enroll in a new plan. Original Medicare does not provide prescription drug coverage. However, Medicare Part D or certain private insurance policies called Medicare Advantage plans cover medications and provide prescription help for seniors on Medicare.

Private insurance carriers offer Medicare Advantage (MA) plans to pick up where Original Medicare falls short. Along with prescription drugs, some MA plans can provide coverage for vision, dental, transportation and even fitness classes. Talk to your licensed agent to find a plan that fits your budget and lifestyle.

Medicare Advantage | Medicare Plan Finder

Consider a Plan With Gap Insurance

The donut hole is a limit on what your prescription drug plan will cover, and it applies to all Medicare clients who don’t have Extra Help. The donut hole will be going away in 2020, but for now, here’s a cost breakdown for 2019:

You will pay for 100 percent of your drug costs until you hit your deductible, which is $435 in 2020. Once you meet your deductible, you will only pay a small percentage of your drug costs until you’ve spent $4,020. At that point, you enter the you will pay up to 25 percent for brand-name drugs and up to 25 percent of generic drugs until you reach $6,350. At that point, you will only be responsible for five percent of your drug costs for the rest of the year.

Some Medicare plans offer additional coverage to protect you from the donut hole. That’s something you can ask your agent about when you meet to discuss your coverage options!

Rx Discount Card | Medicare Plan Finder

Request Generic Drugs

Most drugs that your doctor prescribes will have a generic counterpart that works just as well. In fact, the FDA requires that generic drugs have the same level of quality and performance as their brand name counterparts. Brand name drugs are more expensive because the companies that manufacture them had to pay for research and development. They pass those costs onto the consumer.

Ask your doctor if he or she prescribed a name-brand or a generic drug. If your doctor is willing to switch from a brand name to a generic, you might be able to save hundreds of dollars every year!

Let Us Help

Prescription help for seniors on Medicare can come from changing your Medicare Plan, Extra Help or from buying cheaper prescriptions. A highly trained licensed agent with Medicare Plan Finder can help you find a plan that’s right for you. To set up an appointment, call us at 844-431-1832 or contact us here today.

Find Medicare Plans | Medicare Plan Finder

This post was originally published on October 26, 2017, by Anastasia Iliouand was updated on May 23, 2019, by Troy Frink.

Can you get Medicare Overseas Coverage?

Are you planning a summer trip to Europe? Finally going on an African safari now that you’re retired? We hope you have some great vacation time planned, but we really hope you stay safe while you’re out there enjoying yourself! For the most part, Original Medicare will only cover your care that occurs within the United States (including Puerto Rico, The U.S. Virgin Islands, American Samoa, Guam, and The Northern Marina Islands), so it’s important to think about your healthcare options before you head abroad.

Original Medicare overseas coverage is extremely limited, but you will be covered if:

If you are in the U.S. during a medical emergency but a foreign hospital is closer

If you are in Canada on a direct route to Alaska (and far from an American hospital)

If you’re on a cruise ship and less than six hours from an American port

If you have a Medicare Advantage plan with foreign coverage

If you have a Medicare Supplement with foreign travel insurance

Do you have the coverage you need in case you get sick or injured while you’re out of the United States?

Medicare Advantage Foreign Travel Coverage

Private insurance carriers offer Medicare Advantage (MA) plans to add additional benefits to your Medicare coverage (and may include coverage abroad). Original Medicare only covers hospital and limited medical expenses, but MA plans can include dental, vision, meal delivery, fitness classes, and even foreign travel coverage.

There are thousands of MA plans to choose from, but not all of them include Medicare overseas coverage. MA plans are different in every state, county, and zip code. Reach out to us for more information on what’s available in your area.

Medicare Advantage | Medicare Plan Finder

Medicare Supplements Foreign Travel Insurance

Like MA plans, Medicare Supplement (Medigap) plans also offer coverage beyond Original Medicare. The difference is that MA plans cover medical expenses, but Medigap plans cover expenses such as deductibles and coinsurance. You cannot have a Medicare Supplement plan if you have a MA plan, so it’s smart to talk to a licensed agent to find out which type of plan is best for your budget and lifestyle.

Find Medicare Supplements | Medicare Plan Finder

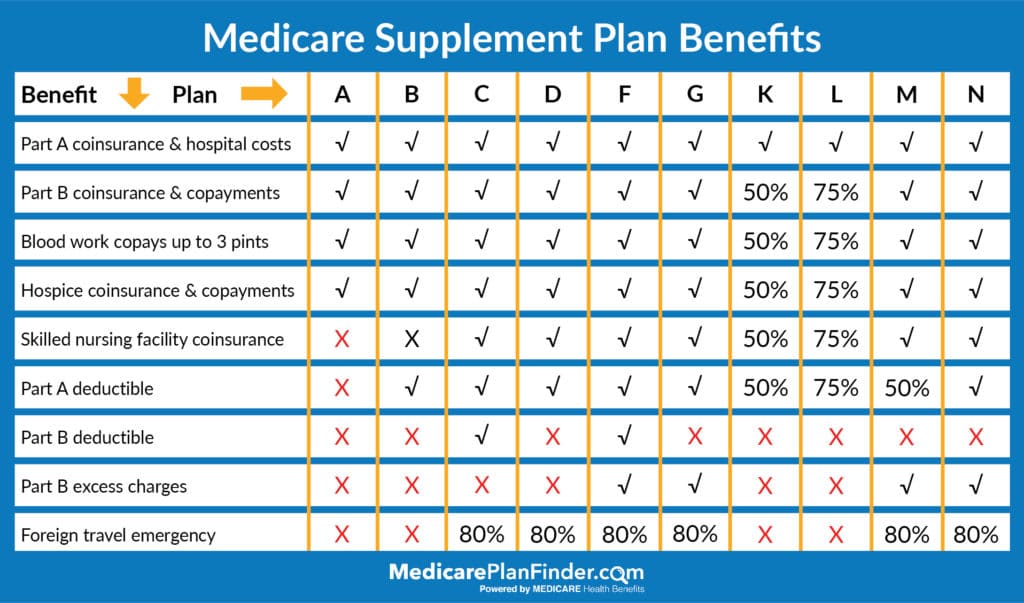

Medigap plans D, E, G, H, I, J, M, and N may cover up to 80 percent of your overseas costs if you meet the plan’s foreign travel deductible (plans C and F include this benefit as well but will be removed from the market in 2020). The expenses will only be covered if they occur within the first two months of your stay overseas, provided Original Medicare doesn’t already cover them. These Medigap plans come with a $50,000 lifetime limit on overseas travel insurance benefits.

Medicare Supplement Plans Comparison Chart | Medicare Plan Finder

How to Prepare for Traveling Abroad

Unfortunately, our planet is covered in bacteria and viruses that can harm our bodies. Those bacteria and viruses don’t live everywhere, though, which means our immune systems haven’t been exposed to them. Therefore, our bodies don’t know how to fight foreign diseases. That’s why you need vaccinations for foreign diseases before you leave the country.

Visit your primary care physician and tell them where you’re going and how long you’ll be there. Medicare will cover your pre-vacation doctor visit where he or she will give you a list of vaccinations to consider.

Along with getting the proper vaccinations before you travel, your doctor may recommend you bring medications for common illnesses you may find at your destination, or for other things that may ail you during your trip. For example, let’s say you’re going on a tropical cruise. Your doctor may recommend you bring mosquito repellant, sunscreen, and motion sickness medicine.

If you have concerns about serious injuries or illnesses during your vacation, consider purchasing a Medicare Advantage or Medigap plan that has coverage for foreign healthcare. You’ll have peace of mind knowing your treatment will be covered.

We Can Help

If you’re planning on traveling to an area where Original Medicare won’t cover your medical treatment, you might want to consider purchasing a plan with foreign travel insurance. If you have questions about Medicare overseas coverage, call an agent at 844-431-1832 or contact us here. We hope you stay safe and enjoy your travels!

Contact Us | Medicare Plan Finder

This post was originally published on June 01, 2017, and was updated by Troy Frink on May 20, 2019.