Dementia is a decline in mental capacity that becomes severe enough to hinder a person’s ability to function. According to the Alzheimer’s Association, one-third of Americans die with some form of dementia.

Medicare Parts A and B (Original Medicare) will cover everything that’s medically necessary for dementia patients, but many other services won’t be covered.

Original Medicare dementia care may be limited, but certain Medicare Advantage plans offer coverage for more services that can include unexpected offerings like meal delivery.

Medicare Coverage for Dementia Patients Clarified

Doctor Explaining Medical Treatment for Dementia | Medicare Plan Finder

An Original Medicare plan will cover services that your doctor deems medically necessary. Medicare Part A covers inpatient hospital care, and Medicare Part B covers outpatient care and medical expenses such as doctors’ appointment costs.

Original Medicare will pay for the first 100 days of care in a skilled nursing facility (there may be some associated fees), and some Medicare Advantage (Part C) plans may include long-term care coverage as well as skilled nursing care.

Private insurance companies offer Medicare Advantage plans, so they have the freedom to cover benefits Original Medicare doesn’t. Medicare Part D or certain Medicare Part C plans cover prescription drugs such as cholinesterase inhibitors that can temporarily improve symptoms of dementia.

Medicare Advantage | Medicare Plan Finder

Medicare Supplements

Medicare Supplements (Medigap) plans can help cover the expenses that Original Medicare does not. Unlike Medicare Advantage plans, Medigap plans do not cover medical expenses, but they cover financial items such as Part A and B coinsurance and copayments. Even though Medigap and Medicare Advantage are two different types of plans, you cannot enroll in both at the same time.

Find Medicare Supplements | Medicare Plan Finder

Does Medicare Pay for Dementia Testing?

Medicare Part B covers cognitive testing for dementia during annual wellness visits. A doctor may decide to perform the test for patients who are experiencing memory loss.

The test consists of about 30 questions like, “What year is this?” to assess the patient’s memory and awareness. The test can be used as a baseline evaluation for future wellness visits and can be a valuable tool for catching dementia early.

Medicare Testing for Alzheimer’s

Dementia is a symptom that can result from many different diseases. Alzheimer’s disease is just one cause of dementia. The risk of developing Alzheimer’s increases with age and with a family history of Alzheimer’s.

There is a correlation between genes called apolipoprotein E (APOE) and Alzheimer’s, but those genes do not necessarily cause the disease. Medicare will not cover genetic testing for APOE genes.

Dementia as a SEP-Qualifying Condition

Medicare eligibles with dementia also qualify for specific Medicare Advantage plans called Chronic Special Needs Plans (CSNPs). These health insurance plans involve coordination and communication between the patient’s entire medical team to help ensure the patient gets the best possible care.

The best way to sort through the thousands of plans available and find the right CSNP for you is enlisting the help of a qualified professional by contacting us here.

If you’re diagnosed with dementia and already enrolled in Medicare Parts A and B, you will qualify for the Special Enrollment Period (SEP). The SEP allows you to enroll in new Medicare coverage or make changes to your existing CSNP whenever you need to instead of having to wait for certain times of the year.

Special Needs Plans | Medicare Plan Finder

Eligibility for Medicare Coverage for Dementia

If you meet the eligibility requirements for Medicare Parts A & B, you will also be eligible for the dementia coverage provided by Medicare. You can obtain Medicare coverage for dementia services if you are:

Age 65 or older

Any age and have a disability, or end-stage renal disease (ESRD)

Dementia patients are also eligible for other specific Medicare plans once they are officially diagnosed with the condition, like special needs plans (SNPs) and chronic care management services (CCMR.)

Medicare can also cover home health care that dementia patients often need. In order to receive this coverage, it must be certified as necessary by a doctor. The patient must also be classified as homebound, meaning they have trouble leaving the house without help.

Does Medicare Cover Memory Care?

Memory care is a specific type of long-term care for Alzheimer’s patients or people with dementia. Original Medicare will cover occupational therapy but does not cover assisted living facilities. However, certain Medicare Part C plans may include coverage for Medicare dementia care services such as adult day care or help to get dressed or to bathe.

Medicare dementia coverage is split between its component parts. Part A helps cover the cost of inpatient hospital stays, including the meals, nursing care, and medication that you need while you’re there. Meanwhile, Part B will cover the doctor’s services that you might receive during your stay in the hospital, such as testing or medical equipment.

Even more services can be covered by Part C, also called Medicare Advantage. In addition to everything covered by Parts A & B, these plans can also offer options for long-term and home care for dementia patients.

How Much Does Medicare pay for dementia care?

Each different part of Medicare will pay for its benefits in different ways. For example, Part A will cover the entire cost of your hospital or skilled nursing facility stay for the first 60 days. After this period, you will need to pay 20% coinsurance until day 90, when Part A will stop paying entirely.

Part B, on the other hand, will usually pay for 80% of all services that it covers. Medicare Supplement plans are often purchased to cover the remaining costs, and can also provide additional benefits to the patient.

Does Medicare cover long term care for dementia?

The long-term care insurance offered by Medicare depends on the nature of the service being provided to the patient. In many cases, the long-term care needed by dementia patients is classified as custodial care and won’t be covered by Medicare.

However, if your doctor prescribes a long-term care service as “medically necessary,” Medicare may help cover the costs. These exceptions can include services like hospice care, and part-time nursing care or occupational therapy provided in the home.

Does Medicare Pay for Home Health Care for Dementia Patients?

It is usually difficult to obtain coverage from Medicare for elderly care at home. However, it can completely cover some home health services that are deemed medically necessary by your doctor, including:

Physical and occupational therapies

Part-time skilled nursing care

Medicare social services

Most nursing home care is also classified as custodial care by Medicare, meaning it will not be covered. Medicare will cover custodial home health care for dementia patients only if it’s a part of hospice care.

Medicare Advantage plans, however, can offer many different home health benefits for those who suffer with dementia. Examples include personal care assistance, homemaker services, and meal delivery.

Does Medicare Cover Assisted Living for Dementia?

Original Medicare will not cover any services that are deemed custodial or personal care, including any that aid in typical activities of daily living, such as:

Eating

Getting Dressed

Bathing

Using the restroom

This rule also applies to assisted living and memory care facilities which provide these services. But depending on your state and the facility of choice, Medicaid may be able to help cover the cost of long-term custodial care provided in assisted living facilities.

Medicare Dementia Hospice Criteria

In order for Medicare to cover hospice care, your doctor must first document that you have less than six months to live. You or your durable power of attorney must sign documents indicating that you agree to accept care for comfort and that you waive other Medicare benefits.

What dementia services does Medicare not cover?

In almost all cases, Medicare will not cover any non-medical care services, such as:

Assisted-living or long-term care

Custodial services provided in a facility or in the home

Homemaker services

Meal delivery

There are exceptions to these rules, but the service in question must be recommended as medically necessary by your doctor. Medicare Advantage plans may offer coverage for these and other personal care services not covered by Medicare.

How to Cover the Gaps with Medicare and Dementia

Paying for dementia care can be daunting, even for Medicare beneficiaries. Both Parts A & B have deductibles you have to meet, and Part B only pays for 80% of its covered services. At the end of the day, a patient and their family may be left wondering how to pay for Alzheimer’s care.

The answer may come in the form of Medicare Part C, also called Advantage plans, which can pay for many of the custodial care costs not covered by Original Medicare. Another option may be a Medicare SNP, or special needs plan, which are geared toward patients with certain chronic conditions such as dementia.

Early Signs and Symptoms of Dementia

Dementia can have a variety of symptoms depending on the cause, as well as if the patient is in the early stages or late stages of the disease. However, some common signs symptoms include:

Cognitive changes

Loss of memory

Difficulty finding the right words during conversation

Getting lost while driving to and from familiar places

Difficulty with logical reasoning or solving problems

Difficulty with completing complex tasks

Difficulty with planning and organizing day-to-day activities

Difficulty with muscular coordination and motor functions

Being confused or disoriented

Psychological changes

Changes in personality

Depression

Anxiety

Inappropriate or irrational behavior

Paranoia

Agitation

Hallucinations

How to Find Memory Care

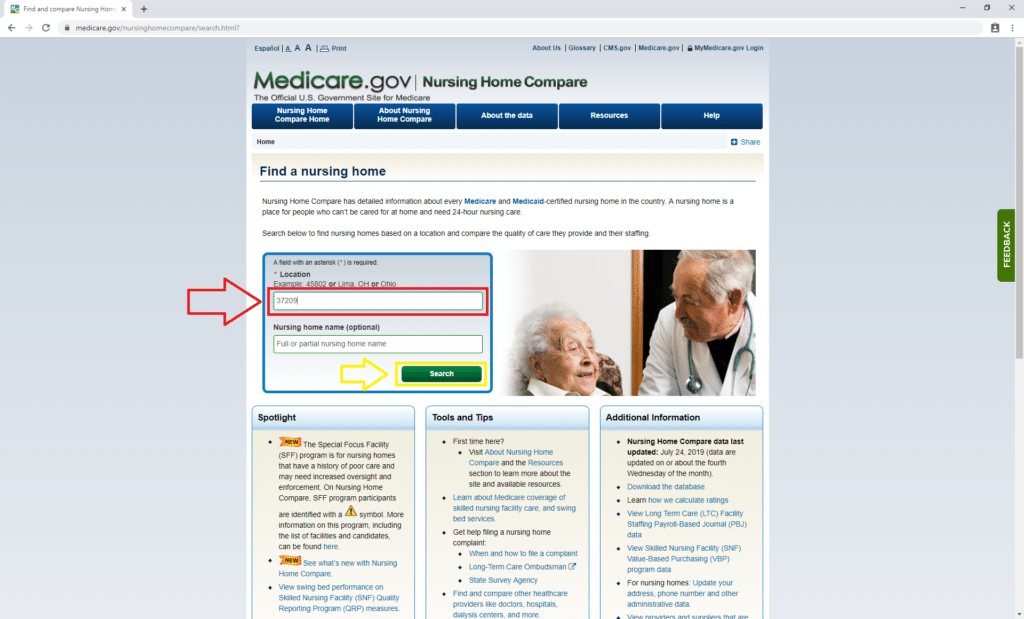

Medicare.gov has a tool to find nursing homes that accept Medicare for medical services. To get started, click here. Not all of these facilities have dedicated memory care teams, so you’ll need to contact them to verify their services.

Once you’re on the nursing home finder tool page, enter your zip code as shown below in red. We used 37209, which is our corporate headquarters’ zip code in Nashville, Tennessee. Then click “Search,” shown in yellow.

How to Find Memory Care Step 1 | Medicare Plan Finder

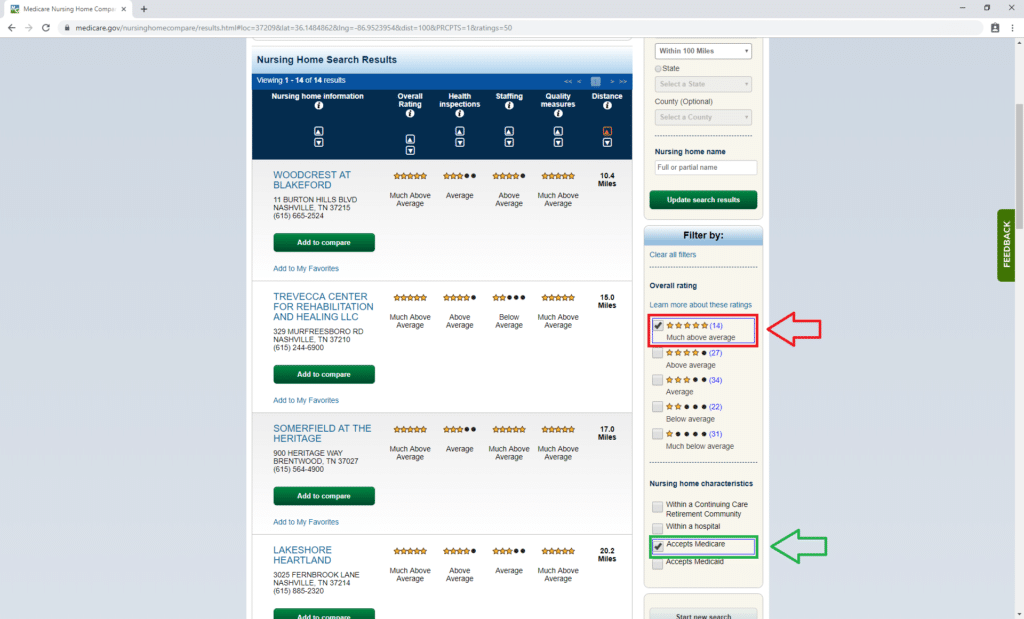

Then you’ll reach a list of nursing homes in your area. The nursing home finder tool lets you sort facilities by star rating, which is based on a scale of one to five.

Basically, the higher the rating, the better the care the facility provides. For demonstration purposes, we only chose to see homes that have a five-star rating (shown below in red) and that take Medicare insurance (in green.)

How to Find Memory Care Step 2 | Medicare Plan Finder

You may have to contact more than one facility to find the right one for you. Ask about costs and how they help patients with dementia. If one seems like it may be a good fit, ask to tour the home to really get a feel for it.

Resources for Families

Family members of dementia patients have access to a wide variety of resources to help them cope. The first step for helping your loved ones is to educate yourself about the disease and to learn how you can be the most supportive.

You should also look into support groups for your family so they can find like-minded people who are having similar experiences. Dementia should not be dealt with alone.

If you are a caregiver for a parent with dementia, you should consider important things such as who will have the power of attorney and make financial decisions for the patient at the end of his or her life. If you haven’t enrolled in a life or a final expense insurance policy, you should consider doing so now.

We Can Help You Find Medicare Coverage for Dementia

Dementia is difficult for everyone involved. If you or a loved one has dementia, we can help you navigate Medicare dementia care and find a Chronic Special Needs Plan that’s right for you. Set up a no-obligation appointment with a licensed agent by calling 844-431-1832 or contacting us here today.

Contact Us | Medicare Plan Finder

How to Find Medicare-Approved Mobility Scooters in my Area

According to the University of California’s Disability Statistics Center, about 6.8 million people rely on mobility scooters to get around their homes. Electric scooters may help give people independence and freedom who might otherwise be left in bed. If you’re looking for a Medicare-approved mobility scooter, first you have to qualify to receive one.

Your doctor must submit a written order stating that you have a medical need for a scooter to use at home.

You have a health condition that causes extreme difficulty moving around your house.

You can’t engage in daily living activities such as bathing, dressing, getting in or out of bed or a chair, or using the bathroom, even with an assistive device.

You’re able to safely operate the scooter including getting on and off the device, or you have a caregiver with you at all times to help you use the device safely.

You can use the equipment in your home (for example, it’s small enough to fit through your doors).

Both your doctor and the equipment supplier are Medicare-approved.

If Medicare approves the device, you may pay 20 percent of the Medicare-approved amount after you pay your Part B deductible for the year. Medicare may pay the other 80 percent.

Medigap Coverage for Scooters

A Medigap (Medicare Supplement) plan is a type of private insurance policy that can help pay for financial items such as Medicare coinsurance (like the 20 percent you’d pay for a scooter) and copays. In 2025, Medigap plans have 8 different coverage levels and each one is assigned a letter.

Medicare Advantage Scooter Coverage

Medicare Advantage plans are private insurance policies that can provide coverage for more services than Original Medicare. Even though Medicare Supplement and Medicare Advantage sounds similar, they are actually very different.

Medigap plans help pay for Original Medicare-related fees. Medicare Advantage plans offer coverage for the same services as Original Medicare, but they can also offer additional benefits such as hearing, dental, vision, and fitness classes. You cannot have both a Medicare Supplement and a Medicare Advantage plan, so it’s best to meet with an agent to learn what’s right for you.

A Medicare Advantage plan may offer reduced fees for mobility scooters, however, your exact cost depends on your plan.

How to Get a Medicare-Approved Mobility Scooter

In order to get a prescription for a mobility scooter, you must first have a face-to-face visit with your doctor. Your doctor must document your condition and ability to move around your home. Your documentation needs to say that you can’t use other mobility aids, and a scooter is your only option.

The mobility device supplier must receive the order within 45 days of your in-person evaluation.

How to Find a Medicare-Approved Electric Scooter Supplier

Medicare.gov has a DME directory so you can find a Medicare-approved electric scooter supplier. Click here to get started. Enter your zip code in the search bar. We used our home office’s zip code in Nashville, TN for demonstration purposes. Then click “Go” beside the green arrow.

Other Types of Mobility Equipment Medicare Covers

The Centers for Medicare and Medicaid (CMS) categorizes some other mobility aids as Durable Medical Equipment. You may qualify for a manual or power wheelchair instead of a mobility scooter.

Manual Wheelchair

If you can’t use a cane or walker, but you have enough upper body strength to use a manual wheelchair, you may qualify for one instead of a powered scooter. You may have to rent a wheelchair first, even if you plan on buying it eventually.

Power Wheelchair

You may qualify for a power wheelchair if you can’t use a manual wheelchair or electric Hoscooter safely. If you aren’t strong enough to operate the scooter, your doctor may recommend a power wheelchair instead.

Does Medicare Cover Stair Lifts?

Stair lifts are a mobility aid many people use to travel up and down stairs in their homes. Medicare considers stair lifts to be home modifications rather than DME, therefore, Original Medicare doesn’t cover them.

However, some Medicare Advantage plans may cover some of the costs of buying and installing a stair lift chair.

Medicare Scooter Fraud and How You Can Help Stop It

Medicare fraud can happen in a variety of ways. For example, in 2018, an equipment supplier found a woman’s Medicare number and claimed they sold her an electric wheelchair. The supplier did not sell the woman anything. In fact, the 85-year-old “refused the hand of a deputy and climbed into the witness chair” according to the Associated Press (AP).

Possible signs of scooter fraud are a supplier offering you a “free” scooter, offering to pay you in cash or to waive your copay, or having a doctor you don’t know order a scooter for you.

If you suspect fraud, call 1-800-MEDICARE (1-800-633-4227) to report the incident. Be sure to write down all of the details of your incident such as the company’s name and who you talked to.

Get Coverage for Medicare-Approved Mobility Scooters

A licensed agent with Medicare Plan Finder may be able to help the best coverage to suit your needs, whether it’s a Medicare Supplement or Medicare Advantage plan.

There may be many plans available in your area, and your agent may be able to find a plan that fits your budget, lifestyle, and one that offers important benefits such as scooter coverage.

For more questions, you can email us or call directly at (833)-567-3163.

Contact Us | Medicare Plan Finder

A Guide to Osteoporosis Medicare Coverage

Osteoporosis literally means “porous bone”. It’s characterized by low bone mass and deteriorating bone tissue and it leads to fragile bones and an increased risk of hip, spine, and wrist fractures.

According to the International Osteoporosis Foundation (IOF), more than 61 million people will be affected by osteoporosis or low bone density by 2020. If you’re one of those millions of people and you have Medicare, you may wonder about osteoporosis Medicare coverage and what you can do to help your bone health.

Osteoporosis Medicare Treatment and Testing Coverage

Osteoporosis Screening Medicare | Medicare Plan Finder

Original Medicare covers certain preventive services and treatments for osteoporosis.

Does Medicare Cover Bone Density Tests?

As part of Medicare’spreventive care program, Medicare Part B may cover one bone density test every two years—more often if the tests are medically necessary—if you meet one or more of the following conditions:

You’re a woman whose doctor determines you’re at risk for osteoporosis, based on estrogen deficiency, your medical history, and other risk factors

Your X-rays show possible osteoporosis, osteopenia, or spine fractures

You take prednisone or steroid-type drugs or you plan to start

You have primary hyperparathyroidism

You’re monitored to see if your osteoporosis drug treatment is working

Does Medicare Cover Prolia Injections and Other Osteoporosis Drugs?

Original Medicare (Part A and Part B) may help pay for an injectible drug for osteoporosis (Prolia, Reclast, or other drugs) and visits by a home health nurse to inject the drug if you meet the following conditions:

You’re a woman.

You’re eligible for Part B and qualify for Medicare home health services.

You have a bone fracture that a doctor certifies is related to postmenopausal osteoporosis.

Your doctor certifies that you’re unable to learn to give yourself the drug by injection and your family members and/or caregivers are unable and unwilling to give you the drug by injection.

You may owe coinsurance and/or deductibles. You may be responsible for paying other services in full if Medicare doesn’t approve them.

Prolia Finder

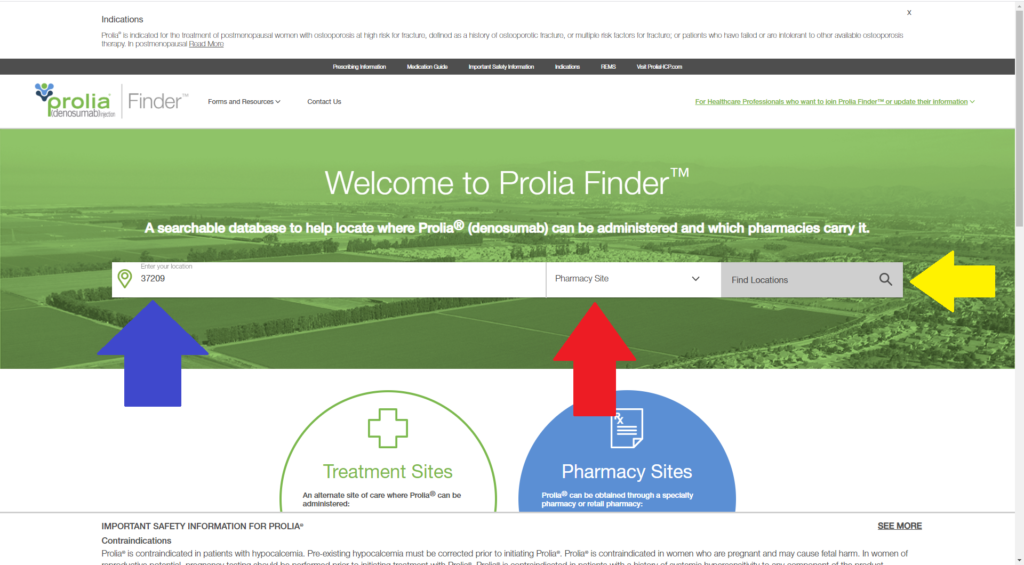

If you don’t know where to get started looking for Prolia, click here. That will lead you to the Prolia finder tool. Enter your zip code in the box above the blue arrow. We used our home office in Nashville, Tennessee’s zip code, which is 37209.

Then select “Pharmacy Site” in the drop-down menu above the red arrow. Then click “Find Locations” beside the yellow arrow. That will lead you to a list of pharmacies where you can find Prolia. You may have to contact more than one to find the right facility for you.

The next step is going to your pharmacy and picking up your medication. You may owe Part D or Medicare Advantage drug fees. Once you obtain the medication, make an injection appointment with your healthcare provider.

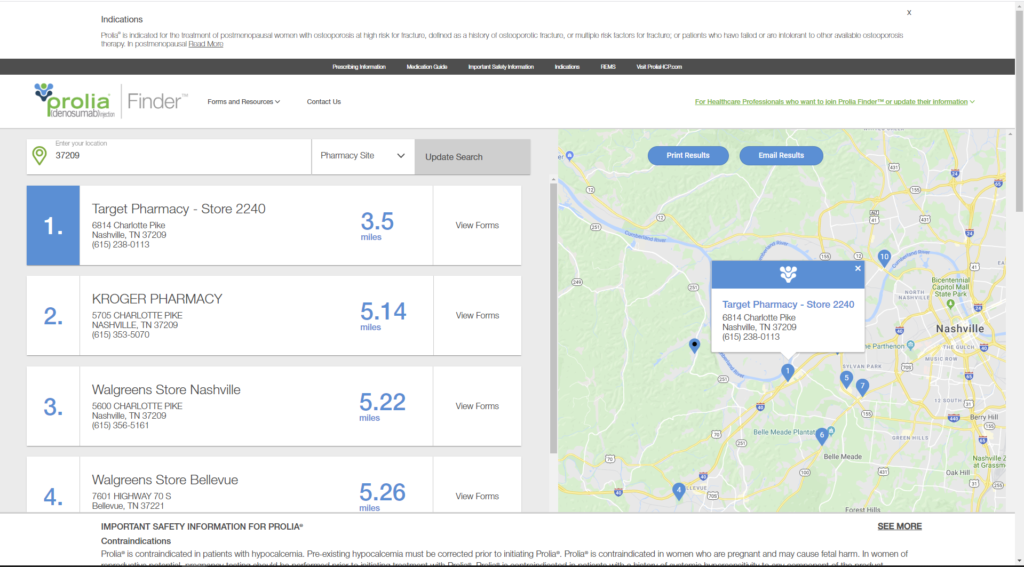

You can also receive an injection at a Prolia treatment site, which you can find using the same Prolia finder tool.

To find a treatment location, go through the same steps to find a pharmacy site, except select “Treatment Site” from the drop-down menu above the red arrow. After you click “Find Locations” you’ll reach a list of Prolia treatment sites and contact information. Again, you may have to call more than one to find the best fit.

Medicare Coverage for Other Osteoporosis Drugs

In most cases, Original Medicare doesn’t include prescription drug coverage. If your doctor prescribes ibandronate (Boniva), alendronate (Fosamax), and/or risedronate (Actonel, Atelvia) and you want Medicare coverage, you’ll need to enroll in either a Medicare Part D plan or a Medicare Advantage plan with a prescription drug benefit.

How to Increase Bone Density at Home

Along with taking your prescribed medications, there are many things you can do to help increase your bone density at home. According to the National Osteoporosis Foundation (NOF), you can protect your bones by exercising, eating right, avoiding tobacco, and limiting alcohol.

Exercises for Osteoporosis

The two most important types of osteoporosis are weight-bearing and muscle-strengthening exercises. Both types of exercises can help build and maintain bone density. As always, you should check with your healthcare provider before starting any exercise program.

Weight-Bearing Exercises

Weight-bearing exercises include activities that make you move against gravity while staying upright. Weight-bearing exercises can be high-impact or low-impact.

High-impact weight-bearing exercises help build bones and keep them strong. However, you may need to avoid high-impact exercises if you have a broken bone.

Some examples of high-impact weight-bearing exercises:

Dancing

High-impact aerobics

Hiking

Jogging/running

Jumping Rope

Stair climbing

Tennis

Low-impact weight-bearing exercises are also effective at keeping bones strong. They’re also a safe alternative if you can’t do high-impact exercises.

Some examples of low-impact weight-bearing exercises:

Using elliptical machines

Doing low-impact aerobics

Using stair climbers

Brisk walking on a treadmill or outside

Muscle-Strengthening Exercises

Muscle-strengthening exercises use a weight or some other resistance to push or pull against gravity. They are also known as resistance exercises and include:

Lifting free weights

Using weight machines

Using elastic exercise bands (resistance bands)

Lifting your own body weight (pull-ups, pushups, etc.)

Functional movements that you use in daily life, such as standing from a sitting position

Yoga and pilates can also help improve strength, balance, and flexibility. However, certain positions may not be safe for people with osteoporosis or low bone density. If you have questions about the safety of an exercise, consult your doctor or physical therapist.

Medicare Fitness Coverage

Medicare Fitness Coverage | Medicare Plan Finder

Original Medicare does not cover gym memberships or fitness classes. However, certain Medicare Advantage plans offer coverage for fitness classes along with other supplemental benefits such as dental, hearing, and vision coverage.

A licensed agent with Medicare Plan Finder may be able to help you find a plan that suits your needs. Plans vary by zip code, but some Medicare Advantage with fitness benefits have $0 premiums. To set up a no-cost, no-obligation appointment, call 844-431-1832 or contact us here.

Diet for Osteoporosis

Diet for Osteoporosis | Medicare Plan Finder

According to NOF, a “balanced diet that’s rich in calcium and Vitamin D” is important for your bone health.

NOF says the following foods are good for your bones because they may contain nutrients such as magnesium, potassium, Vitamin C, and Vitamin K along with Vitamin D and calcium:

Dairy Products

Low-fat milk, yogurt, and cheese

Non-fat milk, yogurt, and cheese

Fish

Canned sardines and salmon (with bones)

Fatty varieties such as salmon, mackerel, tuna and sardines

Fruits and Vegetables

Artichokes

Bananas

Beet greens

Broccoli

Brussels sprouts

Chinese cabbage

Collard greens

Dandelion greens

Kale

Mustard greens

Okra

Oranges

Papaya

Pineapple

Plantains

Plantains

Potatoes including sweet potatoes

Red peppers, green peppers,

Spinach

Tomato products

Turnip greens

Fortified Foods

Some food manufacturers add Vitamin D and calcium to products such as cereal, juice, and bread. Always check the product’s label to see exactly what’s in the container.

Find Osteoporosis Medicare Coverage Today!

Talk to one of our agents if you want to learn more about Medicare’s coverage for osteoporosis. Our licensed agents are highly trained and they may be able to help you find a plan that fits your budget and lifestyle.

If you’ve been diagnosed with low bone density or osteoporosis, you may need treatment as quickly as possible. One of our agents can show you what’s available in your location. Call 844-431-1832 or contact us here to arrange a meeting now.

Contact Us | Medicare Plan Finder

Medicare Meal Delivery Services & Meals on Wheels

According to a report from the non-profit organization Feeding America, 5.5 million adults 60 and older are “food insecure,” meaning they lack access to enough quality foods. Many seniors and Medicare eligibles may be homebound due to medical conditions or income level, and they simply can’t get out to buy the food they need.

Meals on Wheels or Medicare meal delivery services may be able to help if you meet certain conditions.

What Is Meals on Wheels?

Medicare Food Delivery | Medicare Plan Finder

Meals on Wheels is best known as a food delivery service for homebound people who don’t otherwise have access to healthy food. Meals on Wheels has more than five thousand programs that operate across the entire United States. Those programs feed more than 2.4 million people every year.

Meals on Wheels programs may operate on a sliding payment scale, meaning that you won’t necessarily be turned away if you can’t afford the meals. Some local programs accept SNAP (food stamps). Every local Meals on Wheels program has a different set of payment guidelines, so it’s best to reach out your local program if you have questions.

Typically, program members receive one meal per business day. You may not be able to receive meals on weekends, holidays, or during inclement weather.

Meals on Wheels may provide additional benefits along with food delivery. The volunteers who deliver the meals can talk to the program members, which can provide an additional social benefit.

Meals on Wheels Food Delivery Finder

Meals on Wheels’ network of independently-operated programs provides 218 million meals all over the US. While each local program may provide different services based on your community’s needs, every program is dedicated to encouraging healthier lifestyles.

If you have questions about the services your local Meals on Wheels program provides, check out the Meals on Wheels America directory. Once you’re on the page, enter your zip code and hit “enter.”

Medicare Food Delivery | Medicare Plan Finder

That leads you to a page that lists contact information for the programs in your area.

Who Qualifies for Meals on Wheels?

Each local program may have different eligibility requirements, however, most homebound people who are 60 and older will qualify. People younger than 60 may also qualify if they are homebound, disabled, and they meet certain income requirements.

Most Meals on Wheels programs use CMS guidelines for determining whether you’re homebound. The Centers for Medicare and Medicaid (CMS) defines homebound as, “confined to the home due to illness or injury.”

You don’t necessarily have to be incapable of leaving; if it is difficult for you to leave, that counts. For example, if you can’t leave the house without a walker, and it’s extremely physically taxing when you leave, CMS may consider you to be homebound.

Is Meals on Wheels Covered by Medicare?

Original Medicare (Part A and Part B) does not cover Meals on Wheels or any other home meal delivery service. However, certain private insurance plans called Medicare Advantage plans can offer meal delivery services if you meet certain qualifications.

Along with meal delivery, Medicare Advantage plans can cover benefits including non-emergency transportation to medical appointments, vision, dental, and hearing services.

How Do I Get Meals on Wheels With My Medicare Advantage Plan?

Most Medicare Advantage plans that offer Medicare meal delivery usually offer the service for a limited time. For example, if you’re discharged from a hospital or a skilled nursing facility, you may receive 10 pre-packaged frozen meals. Your plan may have limits on how many times per year you can receive the post-discharge Medicare food delivery service.

Another way Medicare Advantage plans can offer meal delivery services is if you have a chronic condition. Your plan may offer a set number of pre-packaged meals annually if you have special dietary needs.

Some plans will offer the meal delivery benefit more than once per year to people who have multiple conditions. Some Medicare Advantage plans may allow doctors to order more meals depending on your needs, too.

The licensed agents with Medicare Plan Finder can help you find a Medicare Advantage plan in your area that offers meal delivery services. We are dedicated to helping you find the best plan for your lifestyle and budget.

Medicare Advantage | Medicare Plan Finder

Does Medicaid Cover Meals on Wheels?

If you are homebound and eligible for Medicaid, your state may provide a waiver that pays for home-delivered meals. Medicaid will only cover Medicaid-approved meal delivery services such as Mom’s Meals and Homestyle Direct.

For example, some states require nutrition counseling for Medicaid beneficiaries. Other states do not. If you have questions about your state’s requirements for Medicaid meal delivery services, click here to contact your state’s Medicaid office.

Each state has different policies regarding how you pay for home meal delivery. Some states pay as little as $3.00 per meal, and some pay as much as $8.00 per meal.

How Do I Get Meals on Wheels for My Mother/Relative?

Every local program has different rules about how to apply for Meals on Wheels, and who can apply. Contact your local program’s office to learn about specific requirements.

Some Meals on Wheels programs can cost about $7 per meal, but they accept contributions based on what the recipient can afford.

Even though your loved one’s local Meals on Wheels program may operate on a sliding payment scale or accept SNAP, a Medicare Advantage plan with meal delivery may be the best option for your relative to get vital nutrients after a hospital stay. You can only make Medicare decision’s on your relative’s behalf if you have durable power of attorney (POA).

Agents cannot legally discuss your loved one’s protected health information (PHI) without durable POA. Talk to your agent about your loved one’s needs. Your agent can help you determine if a Medicare Advantage plan with meal delivery is right for your relative.

What Is a Typical Meals on Wheels Menu?

Medicare Meal Delivery | Medicare Plan Finder

Many Meals on Wheels programs provide one meal per day that meets ⅓ of the Food and Drug Administration’s (FDA) recommended daily nutritional value. Meals may contain a protein, a starch, a vegetable, and a dessert.

Many local programs vary the menu every month so you aren’t getting the same thing every day. For example, one day’s meal might be:

Protein: Barbecue pork

Starch: Red potatoes

Vegetable: Spinach salad with French dressing

Dessert: Banana bread

Can I Choose What I Get?

Some local Meals on Wheels programs give their recipients options for meals, such as a diabetes-friendly dessert or a vegetarian option. However, because each program is different, the Meals on Wheels program near you may not let you choose what you get.

How We Can Help With Medicare Meal Delivery

The right Medicare Advantage plan can help provide you with the nutrition you need after a hospital stay or if you have a chronic illness. Our licensed agents can help you find the best health insurance plan that fits your needs. Call 844-431-1832 or contact us here to learn more today.

Contact Us | Medicare Plan Finder

This post was originally published on July 25, 2019, and updated on September 30, 2019.

Does Medicare Cover Knee Replacements?

More than 600 thousand people need knee replacements every year, according to the American Academy of Orthopaeidic Surgeons (AAOS). If you’re one of those people and you have Medicare, you may wonder, “Does Medicare cover knee replacements?” Yes, but only in certain circumstances.

Medicare Criteria for Total Knee Replacement

Does Medicare Cover Knee Replacements? | Medicare Plan Finder

In order for your Medicare plan to cover a knee replacement procedure, the surgery must be medically necessary. For example, the Centers for Medicare and Medicaid (CMS) lists the following conditions that can lead to joint replacement:

Osteoarthritis (mild, moderate, severe)

Inflammatory arthritis (for example, rheumatoid arthritis, psoriatic arthritis)

Malignancy of the distal femur, proximal tibia, knee joint, and/or soft tissues

Previous knee replacement failure

Fractures

Osteonecrosis (a disease caused when the joints receive less blood than normal)

*This list is not exhaustive. You may have different conditions that lead to a knee replacement.

Your doctor will perform a physical exam before recommending surgery. During the exam, your doctor will assess your range of motion, look at how you walk, and look for deformities and/or tenderness. Your doctor will likely order blood work and other lab tests to determine the best possible treatment plan.

Medicare Knee Replacement Age Limit

There is no age limit for a Medicare knee replacement. However, you may still be responsible for some out-of-pocket costs.

What Is the Cost of a Total Knee Replacement if You Are on Medicare?

The exact cost of a knee replacement surgery is hard to pinpoint. Many different factors go into the total cost of the procedure including:

How long you spend in the operating room

The type of anesthesia and the amount the doctor uses

X-rays during and after the operation

Post-surgery medications to manage pain, prevent infection, and help prevent blood clots

How many days you spend recovering in the hospital

Post-surgery physical therapy to help exercise your knee

With Original Medicare, Part A may cover your hospital stay after you meet the Part A deductible. AAHKS says that most people stay in the hospital for 1-3 days “depending on your rehabilitation protocol and how fast you progress with physical therapy.”

If your surgeon recommends an outpatient TJA, Medicare Part B may cover the procedure. If Part B covers the procedure, you may owe 20 percent of all Medicare-approved charges, Part B may pay the remaining 80 percent.

Does Medicare Cover Knee Replacement Surgery Recovery?

Medicare Part A will cover a temporary stay in a skilled nursing facility. Original Medicare may also cover medications, testing, and other clinical services.

Medicare Part B covers postoperative follow-up appointments. Original Medicare may not cover prescription drugs to fight pain or prevent infection, but a Medicare Part D or Medicare Advantage plan with a prescription benefit can cover those medications.

Free Prescription Discount Card

Knee Replacement Cost With Medicare Advantage

If you qualify for Medicare, you can get a Medicare Advantage (MA) plan, which is a private insurance plan that can cover the same services as Original Medicare. The difference is that a MA plan can cover additional benefits such as grab bars and meal delivery for when you return home from a hospital stay.

Each MA plan may require a different deductible, copay, coinsurance payment, or out-of-pocket maximum*, so what you actually pay depends on your plan.

Some Medicare Advantage plans offer a prescription drug benefit, which Original Medicare does not. You may owe a copay or coinsurance for your postoperative medications, and those payments vary by plan.

Knee Replacement Cost With a Medicare Supplement Plan

While Medicare Advantage plans cover Original Medicare services plus additional benefits, Medicare Supplement (Medigap) plans cover financial items such as deductibles and coinsurance. You must choose one because you cannot have both a MA plan and a Medigap plan.

A Medicare Supplement plan can pay some or all of your out-of-pocket costs. Note: You may still owe at premium.

If you’re unsure if a Medicare Advantage or Medicare Supplement plan is right for you, a licensed agent with Medicare Plan Finder Can help. There may be many plans to choose from in your area. Our agents are highly trained and may be able to help you find a plan that suits your needs.

Contact Us | Medicare Plan Finder

What’s Involved in a Knee Replacement Surgery?

Discussing a Knee Replacement Procedure With a Surgeon | Medicare Plan Finder

Your surgery may be a total knee replacement or a partial knee replacement depending on how damaged your joint is.

Regardless if your procedure is a partial or total knee replacement, the surgery will require anesthesia. Your surgical team may use general anesthesia, which makes you sleep during the surgery, or spinal anesthesia, which makes you numb from the waste down, but you’re still awake.

During the procedure, your surgeon will bend your knee to see the entire surface of the joint. Then your surgeon will make an incision 6-10 inches long and then cut out any damaged joint surfaces.

After the joint is prepared, then your surgeon will attach the artificial joint and close the incision after making sure the new joint works properly. According to the Mayo Clinic, the procedure lasts about two hours.

Get Medicare Coverage for Knee Replacement Surgery Today

If you need a knee replacement and want to find the right Medicare plan to cover the procedure, one of our licensed agents may be able to help. There may be many plans available in your area, but how do you know which one is right for you? Your agent will assess your needs, show you the available options, and then help you determine the best path to take. To set up a no-cost, no-obligation appointment, call 844-431-1832 or contact us here today.

Find Medicare Plans | Medicare Plan Finder

Does Medicare Cover Life Alert?

Many people remember the “I’ve fallen and I can’t get up,” commercials from the ‘80s and ‘90s and laugh, but those ads actually sold a useful product called a medical alert system or personal emergency response system (PERS).

Life Alert, who currently owns the trademark to the phrase, is just one medical alert system on the market today. With the press of a button, you can call for help when you need it most!

If you have Medicare insurance you may want to know, “Does Medicare cover Life Alert or any other medical alert system?” The answer may be complicated.

Does Medicare Cover Life Alert Wristbands?

Does Medicare Cover Life Alert? | Medicare Plan Finder

Usually, a medical alert system comes in the form of a pendant button that’s worn around the neck. The system has a base station that communicates with the pendant to call emergency medical staff. The systems can also be wristbands or speakerphones.

Original Medicare does not cover Life Alert wristbands or any other medical alert system, but there may be other ways to receive private Medicare insurance coverage or discounts on personal emergency response systems.

If your Medicare plan doesn’t cover PERS, Medicaid as well as specific long-term care insurance policies may cover certain personal emergency response system costs in some states.

Medicare Advantage | Medicare Plan Finder

Life Alert Systems for Seniors and Medicare Eligibles

A medical alert system may provide peace of mind to someone who lives alone. For example, your caregiver may not be with you 24 hours a day. If you fall, you might not be able to reach a phone to ask for help. Some medical alert systems have a fall detection feature so the system can call for help if you take a tumble.

Medical Alert System Features

Every medical alert system can call for emergency services, but some offer additional features including:

Fall detection and/or prevention: According to the CDC, falls are the leading cause of “injury and death in older Americans.” Some medical alert systems offer a fall detection feature for an additional fee.

Health monitoring: Along with alerting emergency help, some personal emergency response systems can monitor health vitals, such as blood pressure and pulse, and can even send medication reminders.

GPS tracking: This service can be extremely helpful if you or your loved one is on-the-go. With a Global Positioning System (GPS), emergency responders can find the person who wears it no matter where they end up.

Activity tracking: Much like a Fitbit, some medical alert devices can track your activity inside or outside the home. Some include a built-in step counter and health challenges to keep you moving.

Daily check-in services: Some devices offer a check-in feature either with a live person or electronically.

Home security monitoring: Falls aren’t the only type of emergency. Some medical alert devices can alert emergency services in the event of fire, smoke and/or carbon monoxide.

Specific Medical Alert Systems and Their Features

To give you a better idea of what devices have certain features, here are five popular medical alert systems and their features:

Bay Alarm Medical:This device features 24-hour monitoring, a one thousand foot range for home devices, a waterproof pendant with 36-hour battery life, and offers landline, cellular, and GPS options with automatic fall detection.

Life Alert:This medical alert system offers options for landline, cellular, and GPS service, 24-hour monitoring, and batteries that last up to 10 years and do not need charging.

Medical Alert:This personal emergency response device features automatic fall detection with all systems, 24-hour monitoring, landline or cellular systems, a GPS option, and a lockbox option.

Medical Guardian:This PERS features a lockbox, 24-hour monitoring, a 1,300 foot range, and waterproof pendants with a 72-hour backup battery.

MobileHelp:This device features 24-hour monitoring, waterproof help buttons, a GPS option, and two-way voice communication. MobileHelp does not require a landline to use its product.

What to Consider When Looking for a Medical Alert System

Consider your lifestyle and your needs when you look for a personal emergency response system. Ask yourself the following questions:

How do I wear the device, and is it comfortable? If your device has sharp edges or it can irritate your skin, you may want to find a different option.

How far can I go with the device? Some devices are only meant for the home. If you go outside the device’s range, say one thousand feet, it may not work. Other devices can connect to a smartphone so you can contact emergency support if you leave your house and can’t reach your phone.

How durable is the device? You want a device that can handle the demands of your day-to-day life. You want a device that won’t break when you need it most.

How long does the battery last? Consider the device’s battery life and how you charge the device. Find out how long it takes to charge and how to know when the battery is low.

How easy is it to set up? If your device is too complicated to set up and use effectively, then it’s not providing a useful service. Also, find out if the device will require technology updates, and if those updates happen automatically or if you’ll have to manage them.

Does it come with a lockbox? Some companies install a lockbox so emergency responders can enter your home if you’re incapacitated. The lockbox can help keep your home safe while letting emergency personnel do their jobs.

Can my caregiver or family members connect to the device? Some medical alert systems allow your caregivers and/or family members to connect to the device. Ask yourself if that’s something you need.

How long does it take for someone to respond? In an emergency, someone should respond in a matter of seconds. Sometimes waiting longer than that can make a huge difference in your recovery.

Does the company have good customer service? Find out if the response center staff receive adequate training and if they can talk to your loved one in their preferred language. Also, you may have to speak to someone if it’s not an emergency. Learn about the company’s tech support and how to ask questions about their service and the device itself.

How Much Is Life Alert?

Looking at Life Alert Costs | Medicare Plan Finder

Medical alert systems aren’t free. With most systems, you’ll pay a monthly fee of about $25-$50 a month, plus an initial installation fee.

Be sure to read the fine print. If you do have to sign a contract, find out what it takes to leave the contract. For example, some companies will void the contract if you enter a nursing home.

Find Personal Emergency Response System Coverage

Even though Original Medicare does not cover Life Alert or any other medical alert system, a licensed agent with Medicare Plan Finder may be able to help you find coverage. Our agents are highly trained and they can help you see what plans are available in your area, and they can help you select the best one for you. Call 844-431-1832 or contact us here today.

Contact Us | Medicare Plan Finder

How to Find the Right Geriatric Doctor

Finding an internal medicine doctor you really connect with can be difficult, and finding the right geriatric doctor, or geriatrician, can be even more difficult. You must have confidence in your provider’s ability to treat your conditions or to refer you to other providers with extensive experience working with older adults.. Your health is the most important thing you have, and you need a doctor you’re comfortable with.

What to Look for in Geriatric Doctors

All geriatric doctors specialize in the diagnosis, treatment, and prevention of disease and other medical or chronic conditions common to seniors. You want healthcare providers who know how to treat your population and provide quality care plans. However, a doctor’s area of focus is just one thing you should look for. You also want to find a doctor that you can feel comfortable with.

It’s important that you feel comfortable asking questions about personal health concerns and that you can trust that your doctor is listening. You should feel like your health is as important to your doctor as it is to you.

The right geriatrician will take pride in providing the best quality of care possible. You should feel like your doctor thinks of you as a whole person, not just a list of conditions and symptoms.

Your geriatrician should be capable of finding solutions to your health problems. For example, let’s say you get sick one day, so you go to the doctor. Your doctor diagnoses your health condition and prescribes a medication he or she thinks is best. You should have follow-up appointments to assess how the medication works, and your doctor should be committed to finding a prescription that works if the first one doesn’t.

A good place to start is to find out what other patients say about doctors in your area. Talk to friends, family, and caregiver if you have one to see if they like their geriatricians. Ask for recommendations from healthcare professionals you know and trust.

Look at doctor reviews on websites such as Healthgrades.com and read Google reviews. When you look for reviews on Google, also search for the doctor’s name and see if he or she is in the news. If his or her name pops up with a long history of legal trouble, you should move on.

How a Medicare Advantage Plan can Help

Look for a doctor who takes your insurance. If you have Medicare, you have a great resource to receive quality healthcare. However, Original Medicare doesn’t always approve every charge, and Medicare Parts A and B can be limited in what they cover.

That’s where Medicare Advantage (MA) plans come in. MA plans come from private insurance carriers and they can cover a lot of services Original Medicare does not. Medicare Advantage plans can cover a range of services including meal delivery, hearing, vision, and even fitness classes. Some plans even include prescription drug coverage!

There may be many MA plans to choose from in your area, and a great way to find out what’s available is to talk to a qualified professional who can help you find the right plan. You won’t lose your Original Medicare coverage if you enroll in a MA plan, and the “extras” your doctor recommends, like physical activity or home health devices, may be covered.

What if I’ve Already Found a Geriatric Medicine Doctor I Like?

Maybe you’ve found a doctor you like, and he or she decides to stop taking your insurance plan. If you have a Medicare Advantage plan, you may have to wait until the Annual Enrollment Period (AEP) to make changes to your plan unless you qualify for a Special Enrollment Period (SEP). If you want to stick with your doctor and are willing to wait until the AEP, which is every year from October 15 to December 7, find out what MA insurance plans your doctor accepts.

Usually, your doctor will give you a list of carriers he or she accepts, and Medicare Plan Finder benefits advisors have access to many different plans and carriers. Your benefits advisor will work with you to find a plan that will allow you to keep your geriatric doctor.

What is the Difference Between a Geriatric Doctor and a Regular Doctor?

Geriatricians provide primary care for seniors who have complicated medical issues. Age is not the only factor that causes people to need geriatricians. For example, an 80-year-old who is active and only takes a couple of medications doesn’t need to see a geriatrician, but a 65-year-old who has diabetes and heart disease does.

Your geriatric care will involve a team of medical professionals that will provide a comprehensive healthcare plan. You’ll work with your primary geriatric doctor, and often times a social worker, physical therapist, and/or a nutritionist depending on your needs.

If a doctor does not specify that they are a geriatric doctor, that does not necessarily mean that they do not work with older patients. However, doctors who do call themselves geriatric doctors typically have studied geriatrics and are more specialized in that area.

Geriatric Doctor

When You Should Find a New Doctor

If you feel like your doctor refuses to answer your questions, it may be time to find a new one. Your doctor has a responsibility to listen to you and answer your questions. If you say you’re concerned about a recommended procedure, your doctor should ask why. Your doctor should be able to ease your concerns and make sure you’re comfortable.

You should also find a new geriatrician if the office staff is unprofessional. If they don’t do their due diligence and provide you with all of the information you need, your health could be at serious risk. Your doctor and the office staff should have great communication skills. Look for a new doctor if your geriatrician doesn’t communicate with the rest of your care team, Your doctor should respond to you within a reasonable timeframe.

How to Find a New Doctor

The first step you should take when looking for a new doctor is to look for recommendations. Ask your friends and family members if they have a doctor that they like. Then, you can call that doctor’s office to verify that they accept your insurance.

If you don’t have any good recommendations, you may want to use an online search tool to find a doctor that accepts your plan.

Your plan might have a search tool of its own. That would be a great place to start because you know for sure that the information will be as up-to-date as possible. You can be sure that the doctors listed there will accept your plan (though it is always a good idea to call the doctor and ask before you set your first appointment).

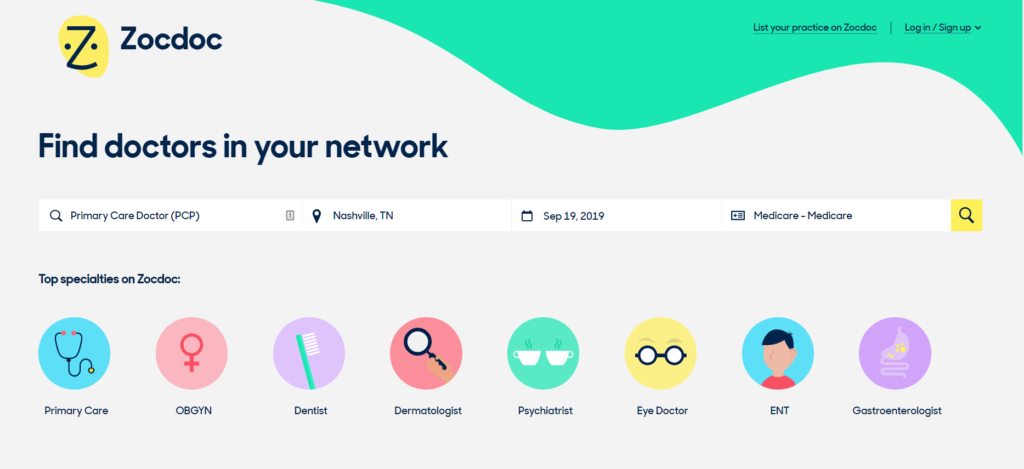

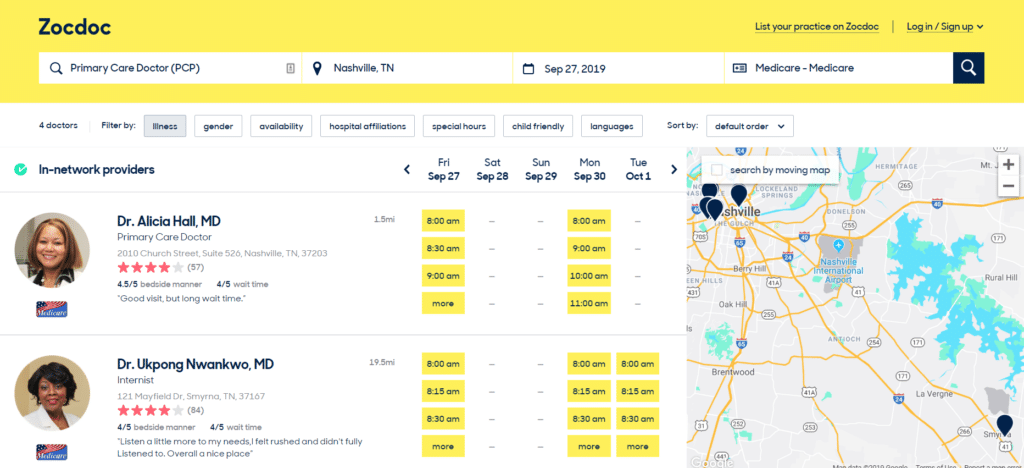

Medicare.Gov and ZocDoc are two other great tools you can use.

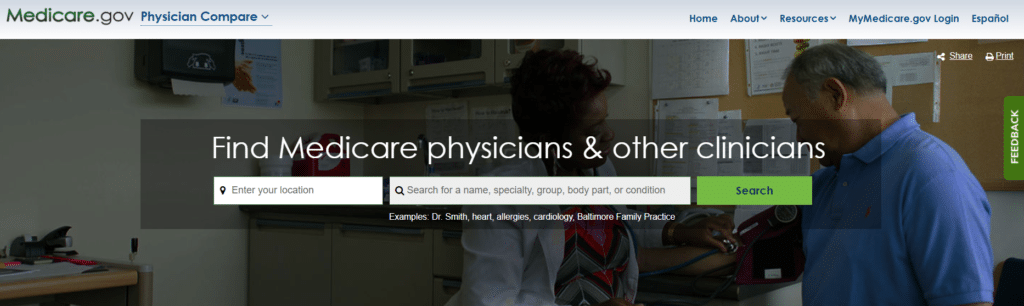

Medicare.Gov’s Physician Finder Tool

Medicare.Gov is a great place to start because it will tell you which doctors accept Original Medicare (Parts A and B). If you have a private plan like Medicare Advantage, be aware that just because a doctor accepts Medicare does not necessarily mean they will accept your private Medicare Advantage plan.

All you have to do is visit medicare.gov/physiciancompare and enter your location and the type of doctor you are looking for.

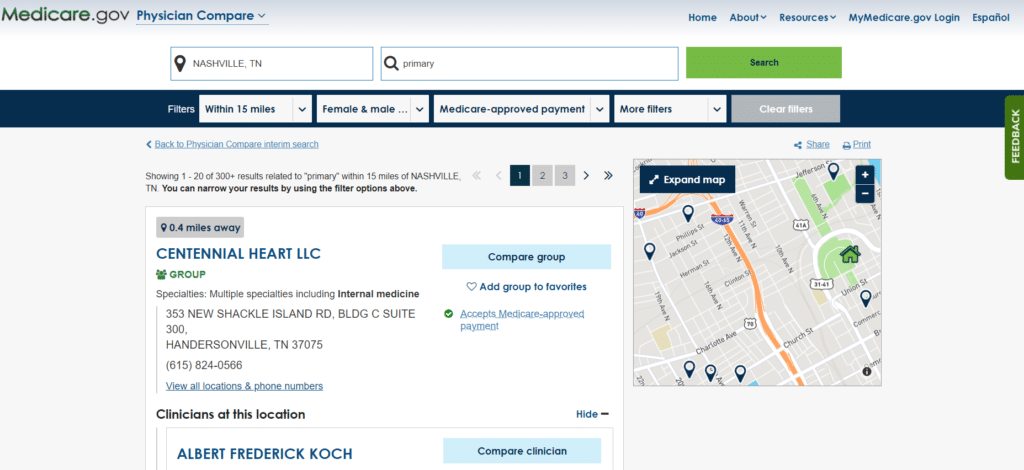

You may be asked to select exactly which type of doctor you are looking for. Then, you’ll see a list of doctors who accept Medicare near you. You can filter by board certification, group affiliation, male/female doctors, distance, and whether or not they accept Medicare-approved payment (meaning you won’t be billed for more than the Medicare deductible and coinsurance).

ZocDoc is another great online tool for finding doctors near you, and it includes reviews! There is also an appointment scheduling feature so that you can book an appointment without having to call the office.

You can filter your search by the procedure you need as well as by appointment time, languages, gender, hospital affiliations, etc.. To show you how that works, we used our home city of Nashville and “primary care” as an example. Notice how we selected “Medicare” as our form of insurance.

Having the right geriatric team and insurance plan is paramount to having the best overall health possible. The team at Medicare Plan Finder can help you navigate the Medicare plans out there and find the best fit. Call us at 800-691-0473 or contact us here today.

Contact Us | Medicare Plan Finder

This blog was originally written on May 17, 2019, by Troy Frink and updated on September 19, 2019, by Anastasia Iliou.

How to Get Help Paying Medicare Premiums

The National Council on Aging (NCOA) says that over 25 million Americans age 60 and older “struggle with rising … healthcare bills.” Thankfully, federal and state governments have assistance programs for people who need help paying Medicare premiums and other costs.

What Are Medicare Premiums?

A premium is an amount you pay every month for insurance coverage. Original Medicare is health insurance that provides coverage for specific services.

You can qualify for Medicare either by turning 65, or sooner if you have ALS, ESRD, or you’ve received SSDI for at least 25 months.

Medicare premiums can seem expensive, especially if you have a limited income. For example, many people don’t have to pay a Medicare Part A (hospital insurance) premium, but they might still have to pay the Medicare Part B (medical insurance) monthly premium (standard is $144.60 in 2020).

You might not have to pay a Part A premium if you or your spouse has worked 40 or more quarters and paid Medicare taxes or you otherwise qualify for premium-free Part A. You could pay up to $458 per month in 2020 if you don’t qualify for premium-free Part A.

On top of that, Original Medicare (Part A and Part B) doesn’t cover everything. If you want extra benefits such as prescription drug coverage, you’ll need to enroll in Medicare Part D, or a Medicare Advantage plan with a prescription drug benefit. Either option may come with a separate premium. Luckily, you may be able to receive help paying Medicare premiums.

What Should I Do If I Need Help Paying My Medicare Premiums?

How to Get Help Paying Medicare Premiums | Medicare Plan Finder

If you need help paying Medicare premiums, you can apply for several assistance programs called Medicare Savings Programs (MSPs). You may need to provide certain legal documents such as a Social Security card, Medicare Card, and proof of income and address to apply. You may even qualify for several different benefit programs at the same time!

Medicare Savings Programs

There are four types of Medicare Savings Programs (MSP). Each one has its own set of income limits. Your state may have different limits for annual income, too.

In 2019, the total asset limits for most MSPs are $7,730 for an individual, and $11,600 for a couple. These limits are only federal guidelines. Your state may have different limits.

Qualified Medicare Beneficiary Program (QMB). Can help pay premiums for Part A and Part B, as well as copays, deductibles, and coinsurance. An individual may qualify in 2019 with an income up to $1,061 per month or $1,430 per month for a couple. If you qualify for QMB, you may also be eligible for Extra Help (LIS) paying for Part D prescription coverage.

Specified Low Income Medicare Beneficiary Program (SLMB). Can help pay premiums for Part B. A single person may qualify in 2019 with an income up to $1,269 per month or $1,711 per month for a couple. If you qualify as a SLMB, you’re may be eligible for LIS paying for Part D prescription coverage.

Qualified Disabled and Working Individuals Program (QDWI). Can help to pay Part A premiums. This MSP is for disabled people who lost their premium-free Medicare Part A when they went back to work. The income limits for QDWI are $4,249 per month for an individual, and $5,722 for a couple in 2019. The asset limit is $4,000 for an individual and $6,000 for a couple.

Medicare Savings Program Application and Eligibility

The best way to find out if you qualify for MSPs is to apply and let your state determine eligibility. However, Benefits.gov has a tool that uses multiple choice questions to find out if you may be eligible.*

Your state’s Medicaid office can provide information about how to apply and where to send your application.

After you apply, you should receive a “Notice of Action” within 45 days detailing what programs you qualify for, and you should be automatically enrolled in the program that most aligns with your qualifications.

Low Income Subsidy (LIS)

Low Income Subsidy (LIS) or Extra Help is a federally-funded program that helps Medicare beneficiaries save on prescription drugs. LIS can help cover your Part D premium, deductibles, coinsurance, and copays.

The program can provide huge savings! For example, you won’t pay more than $3.40 for generic drugs or $8.50 for brand-name drugs in 2019 according to the Social Security Administration (SSA).

To qualify for LIS, you must have a monthly income of less than $1,405 for an individual or less than $1902 for a couple in 2019. You must also

Have Original Medicare (Part A and Part B) coverage

Have prescription drug coverage (either a Medicare Part D plan or a Medicare Advantage plan with prescription drug benefits)

Have American citizenship

Not have savings, investments, and real estate valuing more than $28,150 if you are married or $14,100 if you are single

You may also qualify for Extra Help if you have Supplemental Security Income (SSI) or if you have both Medicare and Medicaid insurance. If you think you meet the eligibility requirements, click here to apply for LIS or ask your insurance agent to help you.

If you qualify for a DSNP, you may also qualify for a Special Enrollment Period (SEP), which can give you the freedom to make one change per quarter to your plan*. This is a huge cost-saving benefit to DSNP enrollees because it means you can enroll in a plan that best suits your needs.

For example, if your doctor stops accepting your insurance plan, but he accepts another DSNP in your area, you can switch plans to stay with your doctor. You won’t have to enroll in a different plan with a potentially higher premium.

*For the first three quarters of the year as long as you qualify for both Medicare and Medicaid.

How to Save Money on Premiums With Private Medicare Insurance Plans

Some people may not qualify for Medicaid, MSPs or LIS. However, you may still be able to save some money. If you have Original Medicare, you can enroll in private plans such as Medicare Advantage or Medicare Supplements. Note: You must choose one because you cannot be enrolled in both at the same time.

Medicare Advantage Plans

Medicare Advantage (MA) plans help cover medical services. These plans can offer additional benefits such as prescription drugs, vision, hearing, dental, and even fitness classes! Most MA plans have monthly premiums (the average is $23 in 2019) and some MA plans have $0 monthly premiums*.

*You must continue to pay the Part B premium in addition to a Medicare Advantage premium.

If you stick with Original Medicare, you could end up spending more money in premiums and other monthly dues. For example, if you have a gym membership, you likely have to pay dues. That’s one expense. If you have private dental insurance to cover routine cleanings, that’s another. Add vision insurance to that, and that’s three monthly expenses.

Alternatively, you might be eligible for a Medicare Advantage plan that includes dental, vision, and fitness supplemental benefits!

Medicare Supplement Plans

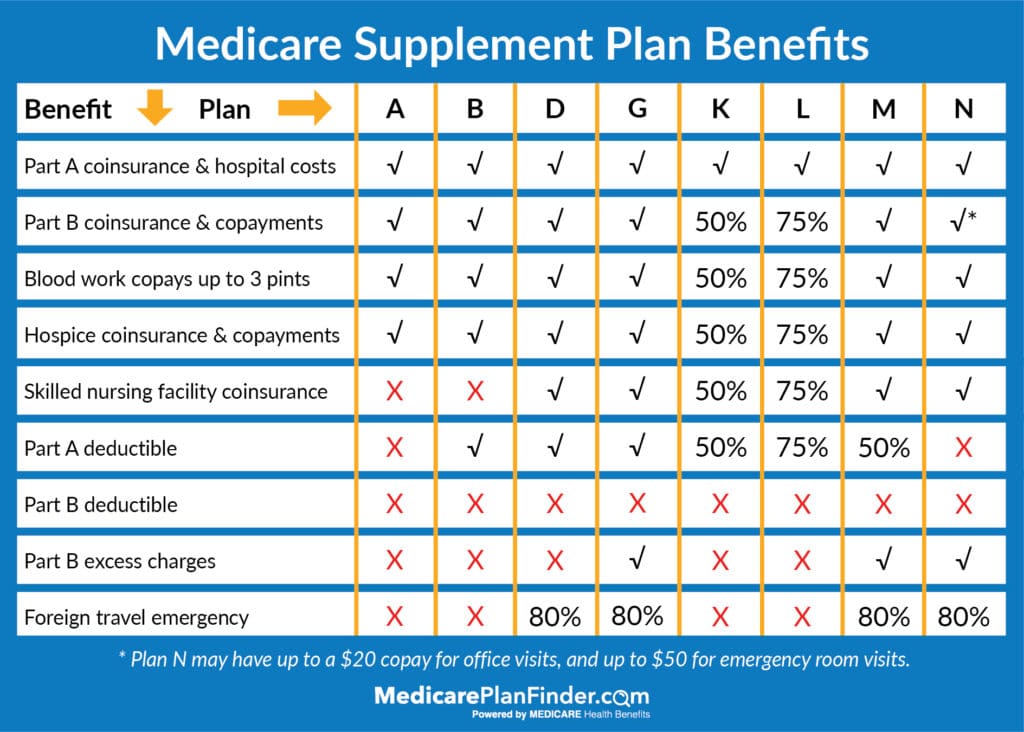

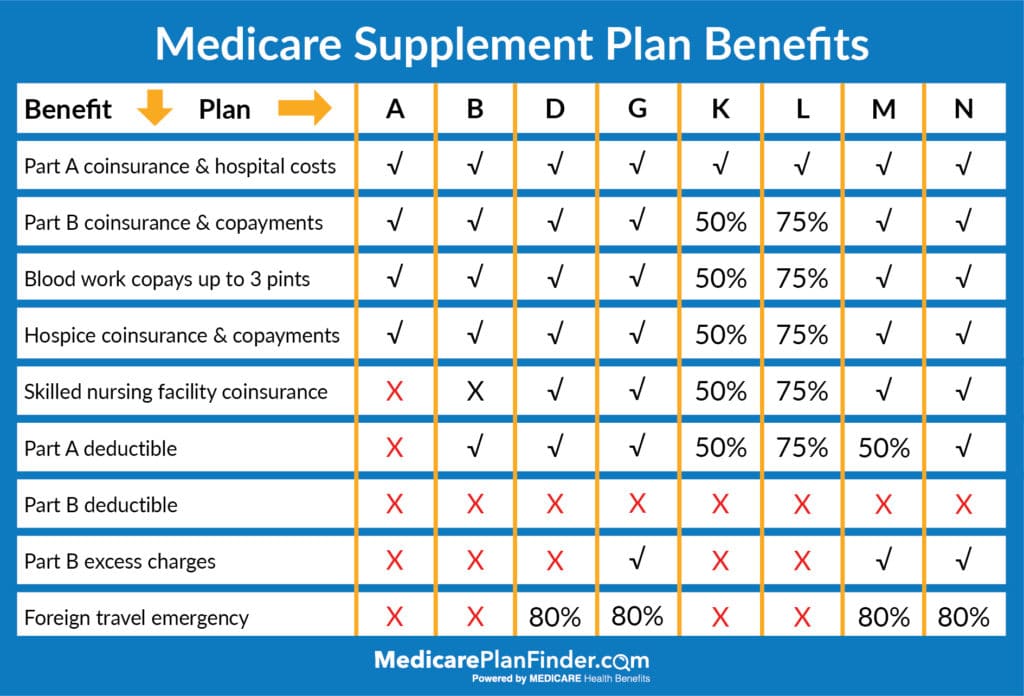

Medicare Supplement (Medigap) plans help pay for financial items such as coinsurance. In 2020, there eight different Medigap plans that offer different levels of coverage. Basically, the more services the plan covers, the higher the premium. Depending on your needs, you can save money on premiums by selecting a plan that covers fewer services.

2020 Medigap Comparison Chart

Find Help Paying Medicare Premiums

If you’re struggling to pay your monthly Medicare premiums, a licensed agent with Medicare Plan Finder may be able to help. Our agents are highly trained and can help you find a plan that suits your budget needs. To set up a no-cost, no-obligation appointment call 844-431-1832 or contact us here to learn more today.

Find Medicare Plans | Medicare Plan Finder

MOOP meaning in healthcare? What is it and Why Does It Matter?

Medicare is a resource that many people use to help with healthcare costs, but like any health insurance, it can be expensive. Depending on your condition or what procedures you need, you could spend thousands of dollars on healthcare costs throughout the course of a year.

However, there are safeguards built into these plans designed to protect how much you’ll ultimately be required to spend out-of-pocket on medical costs in a specific calendar year. This is called the maximum out-of-pocket, also known as the MOOP. But that’s only part of the equation, when you bring your prescriptions into the equation, you have what’s now called a TROOP, also known as True-out-of-pocket.

Yes it’s confusing.

But, the good news is both MOOP and TrOOP are means of patient protection that limit your spending on medical services through various health insurance plans such as a Medicare Advantage plan, and/or a Medicare Part D plan.

Important note, Individuals only utilizing Original Medicare (Part a and Part b only) do not have the same protections, which is why most people take advantage of either Medicare advantage plan or a Medicare supplement paired with a Part D drug plan.

Medicare MOOP

Maximum out-of-Pocket Medicare Advantage Costs

The Centers for Medicare and Medicaid (CMS) regulates Medicare Advantage plans. In many cases, the Medicare Advantage MOOP is as much as $6,700 for in-network services. And, various health insurance companies plan MOOPs can be higher or lower.

If you combine costs for health care services for both in- and out-of-network limits, maximum out-of-pocket limits for some plans can be up to $10,000.

Be aware that not every cost you receive counts toward your MOOP limit.

For example, if you have a Part D plan, your monthly premiums and prescription costs may not count toward your MOOP. Also, your plan may not cover out-of-network services even after you reach the out-of-pocket spending limit.

What Happens When You Hit Your Limit?

Once you hit your max out-of-pocket spending limit, your Medicare Advantage plan should pay for the rest of your out-of-pocket expenses for qualifying services for the remainder of the year. This includes hospital stays, medical equipment and other medical expenses that come along when you use your insurance coverage.

Note: Look at your plan’s Evidence of Coverage (EOC) document for specific details about qualifying covered services.

Let’s look at a real-world example of this. Let’s say your doctor recommends a hip replacement and your Medicare Advantage plan has a $6,700 MOOP. The average hip replacement surgery is $39,000, which is much more than your MOOP.

In this example, you haven’t had any MOOP-qualifying costs, so your total out-of-pocket expenses will be $6,700. That means that your insurance carrier will pay more than $32,000.

Medicare TrOOP

TrOOP stands for True Out-Of-Pocket costs. While it may sound similar to MOOP, it is not the same thing.

While MOOP applies to Original Medicare-covered services with Medicare Advantage Plans, TrOOP applies to prescription drug coverage, whether that’s from Medicare Advantage Prescription Drug plans or stand-alone Medicare Part D plans.

How Does the TrOOP Work?

TThe TrOOP starts when you reach the annual out-of-pocket threshold after you’ve left the donut hole. In order for your costs to count, they must meet the following conditions:

Your generic or brand-name prescriptions are on your Medicare Part D plan’s formulary or list of prescription drugs.

One exception to the “formulary rule” is if Medicare and your plan approves your drugs even if the prescription drugs aren’t on your plan’s formulary. In this case, your medications will still count toward TrOOP because both Medicare and your plan approved the formulary exception.

You purchased your approved medications at one of your Medicare plan’s in-network pharmacies.

Note: Medicare Part D plans vary by location and coverage policies can depend on the individual plan.

Other Costs That Count Toward TrOOP

Other Medicare Part D costs can count toward TrOOP including:

Your Annual Initial Deductible: If your plan has an initial deductible, this is the amount you’ll pay before your Medicare Part D coverage “kicks in.” This means that you’ll pay 100 percent of your prescription costs until you reach that initial deductible*.

Cost-Sharing Costs After You’ve Met the Initial Deductible: If your plan requires you to pay a copay or coinsurance, those costs will go toward your TrOOP. For example, if your plan requires a $10 copay for a medication, that money will go toward your out-of-pocket limit.

Payments While You’re in the Donut Hole: This is where things may get a little confusing. According to CMS, the manufacturer discount on “applicable drugs” is 70 percent, your cost is 25 percent, and your plan pays the remaining five percent. The five percent your plan pays does not count toward TrOOP, meaning that only 95 percent of the total drug cost counts*.

State Pharmaceutical Assistance Programs (SPAPs): Some, but not all states have assistance programs called SPAPs that work with your Medicare Part D plan. In qualifying cases, the SPAP program may help pay for your Part D premiums, deductible and copays. If the SPAP program assists with your plan costs, those payments may count toward TrOOP.

*If you receive income-based subsidies or other assistance, you may pay a different amount depending on your needs-based program.

What Is the Medicare Donut Hole?

The “donut hole” is a gap in coverage that some Medicare enrollees will see in their prescription drug coverage. It works like this: In 2019, Medicare Part D has a $415 deductible (some plans may be less) and a $3,820 initial coverage limit for total out-of-pocket costs. The donut hole is the gap between the initial coverage limit and the annual out-of-pocket-threshold ($5,100 ).

The donut hole will effectively be going away in 2020. This means that you’ll pay 25 percent of both generic and prescription drug costs after you reach the initial coverage limit.

According to CMS, the 2020 Part D deductible will be $435, the initial coverage limit will be $4020, and the out-of-pocket threshold will be $6,350.

What Doesn’t Count Toward TrOOP?

Not all the money you spend on your prescriptions counts toward your out-of-pocket limit. For example, the amount your plan covers does not count.

For example, let’s say your prescription costs $50. Your copay is $15 and your insurance policy pays $35. Only the $15 you pay for your prescription goes toward your limit. Other items that don’t count include monthly premiums and excluded drugs.

CMS considers excluded drugs to be optional, and are therefore not covered. According to the Center for Medicare Advocacy, excluded drugs include:

Drugs to promote weight loss or weight gain, even if they cosmetic use, such as to treat morbid obesity. One exception is that that drugs to treat AIDS wasting are not considered to be for cosmetic purposes and are therefore NOT excluded.

Fertility medications

Erectile dysfunction drugs, except when medically necessary and when they aren’t used to treat sexual dysfunction

Hair growth and other cosmetic drugs. Note that drugs to treat acne, psoriasis, rosacea and vitiligo are not considered cosmetic drugs.

Foreign drug purposes

Vitamins and minerals, except niacin, Vitamin D supplements (when used for a documented medical reason), prenatal vitamins and fluoride

Consult your formulary if you have more questions about what medications are included in your plan.

Let Us Help You Navigate MOOP Medicare and TrOOP

Medicare may seem complicated, and Medicare Plan Finder is here to help. Our licensed agents are highly trained and can help you determine what plan will save you the most money. Contact us here to set up a no-cost, no-obligation appointment to learn more or call us at (833) 567-3163.

4 Things to Do on Your 65th Birthday to Save Money

Turning 65 is a huge milestone for many people. Not only can you qualify for Medicare, but you also may be eligible for lots of senior discounts!

You also have a lot of decisions to make. For example, the full retirement age to receive Social Security benefits used to be 65, but that’s changed to 66 ½ for people turning 65 in 2019. You must decide if you want to retire or continue working to receive full benefits. If you don’t make a decision, you could be missing out on a lot of money. Use this list of four things to do on your 65th birthday to save money now.

Turning 65 Checklist

1. Enroll in a Medicare Plan.

You can potentially save thousands of dollars if you enroll in the right kind of Medicare plan on time.

When You Can Enroll in Medicare

Many people are eligible to enroll in Medicare during their Initial Enrollment Period (IEP), which is the three months before your 65th birthday, your birthday month, and the three months after your 65th birthday. Note: That IEP is only for people who qualify for Medicare because of their age. If you qualify for Medicare because you’ve been diagnosed with ALS, ESRD or you’ve received SSDI for at least 25 months, your IEP will begin when you become eligible.

If you don’t enroll during your IEP, you may face up to 10 percent of your premium costs in late enrollment penalties. However, you may be able to delay Medicare Part B enrollment if you receive coverage through your or your spouse’s employer.

If you lose employer coverage you may be eligible for a Special Enrollment Period (SEP), which will allow you to enroll in a new plan.

That covers when you may be eligible to enroll in Medicare insurance, but you may not know what kind of policy you need. Original Medicare helps pay for many hospital and outpatient services, but it doesn’t cover everything. Many Medicare enrollees choose to add private insurance coverage to Original Medicare in order to cover the services they need.

Should I Choose Medicare Advantage or Medigap?

You may have the option of choosing a Medicare Advantage or a Medigap (Medicare Supplement) plan. Both options can help pay for items that Original Medicare does not. You cannot have both a Medicare Advantage (MA) plan and a Medicare Supplement plan, so it’s important to understand the distinction between the two:

Medicare Advantage can add additional benefits such as prescription drugs, hearing, dental, vision, and even fitness classes! MA plans help pay for healthcare services.

Medicare Supplement plans cover financial items such as coinsurance and deductibles.

It’s ultimately up to you to decide which type of plan you need, and it might be confusing. If you want help deciding which plan is right for you, a licensed agent with Medicare Plan Finder can help. Your agent will discuss your needs and can help you find a plan that fits your budget and lifestyle. Call (833)-567-3163 or contact us here to set up a no-cost, no-obligation appointment.

2. Consider Purchasing Long-Term Care, Life, and Final Expense Insurance.

Even though it may seem uncomfortable, considering long-term care, life, and final expense insurance may be one of the most important things to do on your 65th birthday. Planning ahead can help you and your loved ones save a lot of money in the long-run.

Long-Term Care Insurance

Many people will need long-term care at some point in their lives, and it can be expensive. You may be able to save money by purchasing an insurance plan to help pay for your needs.

Original Medicare doesn’t cover long-term care unless it follows a hospital stay or it’s medically necessary. While you can use a Medicare Supplement plan to help pay for copays, some Medicare Advantage plans may offer a long-term care benefit.

Life Insurance

A life insurance policy can help your loved ones financially after you pass away. You can save money in monthly premiums the earlier you enroll depending on your type of policy.

Final Expense Insurance

While long-term care insurance can help cover medical expenses and life insurance can help your loved ones after you die, final expense insurance helps cover funeral and burial costs. A final expense policy can help your loved ones carry out your last wishes after you pass away.

3. Sort out Your Legal Affairs.

If you haven’t already, getting your legal affairs in order is a crucial thing to do on your 65th birthday. Even though the average life expectancy in the United States is over 79 years old in 2019, accidents and chronic illnesses can happen at any moment, unfortunately. Now is the time to get your wishes sorted out regarding healthcare and your estate.

Think about what choices you have and how they will affect your and your loved ones’ future. Then organize your personal and medical files.

Power of Attorney

Find an elder law attorney and meet about drafting a legal will and designating your power of attorney, which is a document that allows a person of your choosing to make legal decisions on your behalf. There are different types of power of attorney that take effect in different circumstances. Your lawyer will help you assign the right kind of power of attorney to the person you choose.

You may also want to discuss a living will (medical directive), which is a document that ensures your medical wishes are carried out, with your lawyer.

4. Take Advantage of Senior Discounts!

Many companies offer discounts to people just for turning 65. You can receive discounts on items ranging from restaurant meals to plane tickets. According to SeniorLiving.org, Southwest Airlines offers reduced fares for anyone 65 and older.

You can also get discounts on prescription drugs from many pharmacies! Download this prescription drug discount card to receive huge savings on the prescriptions you use every day.

You’re Turning 65 and Medicare Plan Finder Can Help.

If you’re turning 65, Medicare Plan Finder can help you get the insurance coverage you need. Our agents can help you determine what plan will help you save the most money. Want to learn more? Call (833)-567-3163 or contact us here to arrange an appointment today.