Does Medicare Cover Cataract Surgery in [mpf name="current_year"]?

Surgeons perform more than 3.8 million cataract procedures every year in the United States. As you age, your risk of developing cataracts increases. Approximately half of all Americans will develop cataracts by age 75.

Before factoring in health care coverage, cataract surgery can cost $3,700 to $7,000 per eye. If you have one of the millions of cases of cataracts, you may wonder, “Does Medicare cover cataract surgery and implants?” Yes. Medicare covers these costs for qualified Medicare beneficiaries.

How Much Does Medicare Pay for Cataract Surgery?

Original Medicare (Part A or Part B) generally* does not include vision coverage. However, cataract surgery is an exception. Medicare Part B covers basic lens implants and cataract removal.

If your provider recommends an advanced lens implant, you may need to pay some or all of the additional costs. It’s essential to talk with your doctor to get a clear understanding of the necessary procedure.

*Medicare Part A may cover emergency services in a hospital.

Medicare Part D, which is the prescription drug plan, may cover any prescription medications you need after you have had your cataract surgery.

Incidentally, any medications you need before surgery, such as prescription eye drops, will be covered by Medicare Part B. Part B will also cover eyeglasses or a set of contact lenses for cataract surgery that implants monofocal intraocular lenses (IOL).

Since Part D has no deductibles, you may be responsible for a specified copayment amount that you must pay when you get your prescription drugs.

What Type of Cataract Surgery Does Medicare Cover?

Medicare covers two types of surgery: manual blade surgery and laser surgery.

Medicare will also pay for an intraocular lens (IOL), which corrects presbyopia or astigmatism, but only if these lenses should be replaced because of cataracts.

Does Medicare Pay for Laser Cataract Surgery?

Medicare coverage for cataract surgery doesn’t depend on the surgical method. Medicare will cover 80% of the cataract removal and basic lens whether the procedure is conventional or bladeless with a computer-controlled laser. Similar to conventional surgery, laser surgery requires you to pay the additional costs if you require an advanced lens.

Does Medicare Pay for Cataract Surgery With Astigmatism?

Since you can correct astigmatism with glasses, Medicare will only cover a cataract surgery with astigmatism if the cataract surgery itself is considered necessary. If this is the case, Medicare will pay for the cataract surgery.

Does Medicare Cover Glasses or Contacts?

For the most part, Medicare does not cover routine vision care, glasses, or contact lenses. However, Medicare can make an exception

You may be wondering, “How much does Medicare pay for glasses after cataract surgery?” After your surgery, Medicare will cover 80% of the costs for prescription glasses or contacts, but you must purchase them through a provider who accepts Medicare assignment.

You will be responsible for the remaining 20%. Some beneficiaries have trouble getting Medicare to cover the pair of glasses or contacts.

If you are denied coverage, you can appeal the decision and request that they are covered. If you already paid for them out of your own pocket, you can request reimbursement.

You and your health provider can write a letter to add to your appeal, just be sure to state that you had met the requirements for cataract surgery, so your glasses or contacts must be covered.

What Is the Average Cost of Cataract Surgery?

Cataract surgery can range from $3,800 to $7,000 per eye without a health insurance plan. For standard cataract surgery, the average cost is $3,700.

However, the average cost of astigmatism-correcting surgery is $5,000, and presbyopia-correcting is about $7,000.

What does Medicare pay toward cataract surgery? It depends on the Medicare plan you are enrolled in. If you are only enrolled in Original Medicare, you will need to pay a 20% coinsurance and your Medicare Part B deductible, which is $185 in 2019.

You may be able to get even more coverage through a Medicare Supplement plan (Medigap) or Medicare Advantage plan. Additionally, because cataracts cloud the eye lens, eye surgery is classified as a medical condition.

This means that Medicaid could also pay some of your cataract surgery costs.

How to Find a Cataract Surgeon Who Accepts Medicare

Ophthalmologists are eye doctors who specialize in vision correction and care. Many times your ophthalmologist will perform your cataract surgery.

Since not every ophthalmologist will accept Medicare Advantage and you may not want to go through the trouble of finding another healthcare provider, then ask your health insurance provider to give you a Medicare eye doctor list.

However, it may be a little more difficult to find a cataract surgeon who accepts Medicare in 2020 because the physician fee schedule has changed since last year. Eye surgeons have had to take a 15% cut in reimbursement compared to Medicare coverage for cataract surgery in 2019.

So another option is to use the Medicare.gov’s physician compare tool to help you find an eye surgeon who accepts Medicare.

Click here to get started. First you’ll come to the physician finder tool. Enter your zip code in the search bar beside the red arrow. We used 37209, which is our corporate offices’ zip code in Nashville, TN.

Then type “ophthalmology” in the search bar above the green arrow. Then click “Search” beside the yellow arrow.

Then you’ll come to a list of ophthalmologists who currently accept Medicare. Use the contact info to call different doctors to find the right fit.

Medicare Requirements for Cataract Surgery

Your vision must be 20/40 or worse to qualify for surgery. Your doctor will need to document that your vision is at this level or lower.

You also need to have difficulty completing daily living activities like reading, sewing, watching television, or driving.

It’s important to remember that the cloudiness in your eye is not directly correlated to the severeness of your cataracts. If you are unsure of your vision level or whether or not you qualify, visit your eye doctor.

Cataract Surgery and Medicare Supplements

Medicare Supplements work alongside Original Medicare and are a great way to add financial benefits to your current coverage. They can help cover your 20% coinsurance and your Medicare Part B deductible.

Plan F is currently the only plan that covers your Part B deductible.

However, Plan F was discontinued in 2020. If you enrolled in it before the start of 2020 you are locked into this plan and will maintain coverage. If you are interested in enrolling in Medicare Supplement Plans, fill out this form or give us a call at (833)-567-3163.

Cataract Surgery and Medicare Advantage

Medicare Advantage plans are required to cover, at a minimum, the same as Original Medicare. However, MA plans offer several additional benefits like prescription drug coverage, hearing and dental coverage, group fitness classes like SilverSneakers, and additional vision coverage.

Benefits will vary by plan but can include routine eye exams, eyeglasses, contacts, frames, and fittings. These benefits allow you to check your vision each year and update your prescription, lenses, and frames as needed.

If you are only enrolled in Original Medicare, you will need to pay for these expenses out of your own pocket.

What Are Cataracts?

Our eyes have a lens that works much like a camera. The lens bends light so you can see your surroundings.

A cataract makes that clear lens cloudy, and it can be more difficult to read or drive a car.

What Causes Cataracts?

Most of the time, cataracts develop with age, or when an injury changes your eye’s lens. As you age, the lens can become stiffer, thicker, and less transparent.

Sometimes genetic disorders, other eye conditions, medical conditions such as diabetes, or past eye surgery can contribute to cataract development. Other causes can be long-term steroid medication use.

Cataract Symptoms

According to the Mayo Clinic, signs and symptoms of cataracts can include:

Cloudy, blurry or dim vision

Increasing difficulty seeing at night

Sensitivity to light and glare

Need for brighter light for reading and other activities

Seeing “halos” around lights

Frequent changes in glasses or contact lens prescription

Fading or yellowing of colors

Double vision in one eye

How Do You Know If You Need Cataract Surgery?

Talk to your doctor if you experience any changes to your vision such as cloudiness or halos around lights. According to Harvard University, you should have an eye exam every year if you’re 65 or older.

Dr. Laura Fine, an ophthalmologist with Massachusetts General Hospital, says you don’t need cataract surgery until you think you need to see better.

Learn More About Medicare and Cataract Surgery

A licensed agent with Medicare Plan Finder may be able to find plans in your area that fit your budget and lifestyle needs.

Are you interested in learning about available plans in your area? Fill out this form or give us a call at (833)-567-3163 to schedule a no-cost, no obligation appointment with a licensed agent.

Assistive Devices for the Elderly: Feel Comfortable With Independent Living

As you age, simple tasks like buttoning your shirt, getting out of your chair, and putting on your shoes can become increasingly difficult. Assistive devices can help restore your confidence, improve mobility, and increase safety in your home.

The first step in making your day-to-day life easier is understanding assistive technology, durable medical equipment, and the role of Medicare.

What Is Assistive Technology?

Assistive technology (AT) covers a wide platform of devices for older adults who may need just a little bit of help. Assistive, adaptive, and rehabilitative devices all fall under the assistive technology umbrella.

Assistive devices help seniors maintain their functional independence. This, in turn, promotes their well-being. Communication aids, pill organizers, spectacles, memory aids, prostheses, or wheelchairs assist family members with cognitive decline or physical challenges with their daily activities.

Caregivers can improve an elderly person’s range of activities of daily living by carefully selecting the most appropriate assistive devices for safe, independent living.

For instance, encouraging the use of personal care products for good hygiene, grooming, and dressing can help older people maintain their dignity, raise their self-esteem, and improve their mobility by allowing them to take care of themselves.

Assistive technology can be used in various settings, such as living at home, in a nursing home, or in an assisted living facility.

Common Assistive Devices

High-tech mobility devices, such as walking canes, stairlifts, power wheelchairs, and scooters, can help seniors maintain their mobility. Mobility aids may also include low-tech assistive devices like transfer benches and bed rails because they reduce the risk of falls.

Meanwhile, adaptive devices are designed to make an available technology more accessible. For example, adaptive switches will allow an elderly person to activate switch-adapted electronics.

There are also assistive listening devices, called Frequency Modulation systems, that connect hearing aids to media such as tablets, smartphones, computers, and music players. Additionally, screen magnifiers are software products that interface with the graphical output of a computer to enlarge content on a screen.

We’ll split assistive technologies into health, home, and comfort categories. You can purchase these products online and in-store from companies like Amazon, Walmart, and Target. Some health devices can be priced as low as five dollars.

Health Devices

Health devices act as an extra layer of protection and are a great way to prevent falls and accidents. For example, grab bars in the bathroom can help you get in and out of the shower and keep you stabilized and balanced. Consider purchasing:

Activator poles to keep you stabilized and balanced.

Grab bars to keep your balance in hallways, stairwells, bathrooms, etc.

A bed cane to help you get in and out of bed.

A shower bench so you can sit and avoid falling in the shower.

Toilet rails to help you sit down and keep your balance.

Stairlifts so you can go up or down stairs with ease.

Wheelchair ramps so you can easily get into and out of your home.

Slip-free stair strips to keep you from slipping on slick surfaces.

Home Devices

Home devices are a fantastic way to increase independence and confidence in your home and make it easier for you to be home alone. For example, if you need a walker or cane to get around comfortably, an automatic swing door opener allows you to open the door hands-free. Common home devices include:

Video doorbells so you can see who’s at the door before you get up.

Fall detectors to alert your friends and family if you take a tumble.

A power failure alarm to alert you of lost power and provide emergency lighting.

An automatic swing door opener so you can open doors hands-free.

A talking thermostat so you can hear the temperature settings.

Voice-activated lights to turn your lights on and off without getting up.

Comfort Devices

Sometimes the smallest tasks can cause the largest frustrations. For example, you may be easily annoyed if you can’t button your shirt yourself or hear the television well. Common comfort devices include:

A buttoning hook to help you button shirts and pants.

A zipper pull so you don’t have to fumble with small zippers.

A modified keyboard so you can see the letters on the keys more clearly.

Robotic vacuums so you can have clean floors without lifting a finger.

A table tray so you can eat anywhere in your home.

A mattress lift so you can get in and out of your bed with ease.

A sound amplifier to help you hear conversations, television shows, etc.

Assistive Technology Devices

Georgia Tech describes high-tech assistive technology gadgets for seniors who want to remain independent as complex devices with digital or electronic parts that can be computerized.

They point out that these devices are often expensive, usually require training, and take some effort to learn. Some examples of helpful things for elderly people that have a small learning curve are power wheelchairs, digital hearing aids, and voice-activated telephones.

Durable Medical Equipment

Durable Medical Equipment (DME) includes equipment like hospital beds, oxygen equipment, sleep apnea devices, glucose monitors, and some of the assistive devices mentioned above. DME devices are covered under Medicare Part B. You will be responsible for 20%.

The equipment must be durable, used for a medical reason in your home, and have an expected lifetime of at least three years for Part B to cover it.

Medicare Advantage (MA) plans can also cover DME and assistive devices. The difference is that MA plans are able to offer additional benefits that Original Medicare does not. This includes benefits like hearing, dental, and vision coverage.

Some MA plans even offer group fitness classes like Silver Sneakers or an over-the-counter monthly allowance. If you’re looking for additional coverage and benefits beyond Original Medicare, a Medicare Advantage plan may be perfect for you!

How to Choose an Assistive Device

With so many products for elderly people living alone, it can often be difficult for a caregiver or senior to make a decision on what to buy. For instance, a senior who asks, “How do I choose a walking aid?” has to select between wheeled frames, walking frames without wheels, folding frames, indoor trolleys, and outdoor trolleys.

Consequently, the right decision requires a clear assessment of needs and then matching those needs with available features.

If deciding on a walking aid is complex, imagine how much more bewildering it must be for caregivers to select the best smart device for elderly patients? For instance, when it comes to smartphones, GreatCall offers a variety of options, such as the Jitterbug Smart 2 and the Jitterbug Flip.

Again, it’s about matching needs with features. Some expert advice from someone familiar with technology is helpful.

What to Consider Before Purchasing

A family caregiver helping a loved one decide what assistive device to purchase must consider factors like independence, specific needs, personal goals, simplicity, and so on. Before making a purchase, it’s useful to talk to a professional or people who have purchased the device, consider the cost, and ask if a trial is available.

Implementing assistive technology in the home may require some structural modifications to a room. When considering interior home modifications, such as relocating switches, installing emergency alarms, or lowering bench heights, it’s usually practical and cost-effective to only modify necessary areas in an apartment or house.

Assistive technology devices for elderly people can be classified into two broad groups, high-tech AT, such as smartphone systems and sensors, and low-tech AT, such as pill organizers and canes. Usually, people who need assistive devices require both kinds.

In addition to mobility AT, personal care AT, and communication AT, there are a number of assistive technology devices for seniors with cognitive decline. For instance, seniors with Alzheimer’s or Parkinson’s disease with significant memory loss can benefit from wearable timers that have set and forget features for managing things like turning off the stove after cooking or running water in a bath.

They will also benefit from smartphone apps that remind them of to-do lists or appointments.

Where to Buy Assistive Devices

A caregiver or senior can buy assistive technology from online tech stores. In 5 Assistive Technology Stores for your Techie with Special Needs, author Lauren Lewis recommends five top online stores that sell assistive devices: EnablingDevices.com, Boundless Assistive Technology, Enable Mart, Infogrip, and Able Net. Her article covers each store’s specialty.

Assistive Technology and Devices Coverage

Assistive technology and devices can improve your life in several areas. If you are interested in learning more about things to help at home, such as increasing your independence, improving your quality of life, supporting your health, and restoring your confidence, let us help you!

We have licensed agents across 50 states that are contracted with all of the major insurance companies and can help you find a plan that makes it easier for you to afford assistive devices for elderly parents or patients. To get started, call (833)-567-3163 or click here.

Alzheimer’s Care Guide: Symptoms, Stages, Prevention, and Treatment

There are more than 5.7 million Americans living with Alzheimer’s. This number is expected to reach 14 million by 2050.

The complications from this disease make Alzheimer’s the sixth leading cause of death in the United States, so it’s important to educate yourself on the symptoms, signs, stages, prevention, and treatment.

Difference Between Alzheimer’s and Dementia

Dementia is a syndrome and used to describe symptoms that include memory loss, difficulty problem solving, and struggling with thoughts and language. Alzheimer’s is a disease and is a type of dementia.

In fact, there are over 100 types of dementia. Some forms of dementia can be temporary, reversed, or cured, however, Alzheimer’s disease cannot.

Alzheimer’s Symptoms and Stages

Alzheimer’s can cause changes in the brain long before any symptoms or signs start to show. Understanding the symptoms can help you detect Alzheimer’s early on and increase your chance of benefiting from treatment.

The risk of developing Alzheimer’s will vary per individual, but the following are the largest risk factors.

Age: Alzheimer’s is not a normal part of aging, however, your risk increases with age. Most people with Alzheimer’s are diagnosed after the age of 65. After 65, your risk doubles every five years.

Family History: If your parent or sibling was diagnosed with Alzheimer’s, you are more likely to develop the disease. This risk increases with the number of diagnosed family members.

Other Risks: There is a strong connection between our hearts and our brain. If you have heart disease, are overweight, or lack regular exercise, you’re at a higher risk of developing Alzheimer’s.

What Are the Very First Signs of Alzheimer’s?

Alzheimer’s is a slow progressing brain disease. If you notice any of the following warning signs, contact your doctor:

Forgetting recently learned information (dates, appointments, events, etc.)

Trouble following a recipe

Difficulty driving to a familiar location

Losing track of dates, seasons, and times

Difficulty reading

Trouble judging distances

Struggling with vocabulary

Misplacing things around the home

Paying less attention to hygiene needs

Avoiding social activities

Changing personality

What Are the 7 Stages of Alzheimer’s?

There are three general stages of Alzheimer’s – mild (early stage), moderate (middle stage), and severe (late stage). However, these stages can be broken down into seven more specific stages.

Keep in mind that the seven stages can overlap, and placing someone into a specific stage can be difficult.

Stage 1 – No Impairment: Alzheimer’s is not detectable in this stage. There are no signs of memory problems or other symptoms.

Stage 2 – Very Mild Decline: Minor memory problems may begin to surface. You would still perform well on memory tests, and Alzheimer’s will be difficult to detect.

Stage 3 – Mild Decline: At this stage, you or family members may start to notice small symptoms. Memory tests may be affected and doctors can detect impaired function. Someone in this stage may be unable to find the right words in conversation or remember new names.

Stage 4 – Moderate Decline: This stage is much more clear-cut. Someone in this stage may have difficulty with basic math problems, have short-term memory loss, be unable to manage bills, and may forget details of the past.

Stage 5 – Moderately Severe Decline: Those in this stage may begin to require assistance in day-to-day life. They may be unable to get dressed appropriately, be unable to recall details like their phone number, and demonstrate significant confusion.

Stage 6 – Severe Decline: People in this stage need constant supervision and may require professional care. They may be unaware of their environment, unable to recognize faces, and unable to remember most of their personal history. Loss of bladder control, personality changes, and wandering are also common in this stage.

Stage 7 – Very Severe Decline: This is the final stage of Alzheimer’s. People at this stage are unable to communicate and respond to their environment. Their speech may be limited to less than six words and they are unable to sit up independently.

How Quickly Does Alzheimer’s Progress?

The rate that Alzheimer’s symptoms progress can vary, but the average person lives four to eight years after diagnosis. However, early detection and a healthy lifestyle can help someone with Alzheimer’s live 20+ years after diagnosis.

Alzheimer’s Test

There is no single test that can diagnose someone with Alzheimer’s. Doctors use a combination of medical history, physical exams, neurological exams, mental status tests, and brain imaging when diagnosing.

Neurological exams address reflexes, coordination, eye movement, speech, and sensation. Mental status tests give an overall sense if a person is able to understand dates, times, locations, and simple instructions or calculations.

The Main Cause of Alzheimer’s

Although scientists don’t fully understand all the causes of Alzheimer’s, research suggests that this progressive disease is related to aging, genetics, and underlying health conditions.

Environmental and lifestyle factors may also contribute. Often the disease could be a combination of these factors.

Alzheimer’s Prevention

Complex factors like age, genetics, environment, lifestyle, and existing medical conditions play a role in developing Alzheimer’s. However, while you can’t change your genes or your age, there are plenty of steps you can take to help prevent Alzheimer’s.

Can Alzheimer’s Be Prevented?

There is strong evidence that shows changing your lifestyle promotes a healthy heart and lowers your risk of Alzheimer’s.

Prevention tips include:

Healthy Heart: There are several connections between our heart and brain. Studies have shown that about 80% of people with Alzheimer’s also have some form of heart disease. Manage your blood pressure, diabetes, and cholesterol levels to lower the risk of developing any heart conditions.

Exercise and Diet: Regular exercise and a healthy diet directly benefit your brain cells. Exercise increases blood flow and oxygen to the brain and a healthy diet limits your intake of sugars and saturated fats.

Social Activities: Staying social helps build and maintain strong connections. This can keep you mentally active. Researchers believe these connections can lower your risk of Alzheimer’s by increasing mental stimulation and reinforcing connections between nerve cells and your brain.

Alzheimer’s Disease Treatment

There is no cure for Alzheimer’s and no way to stop its progression. However, there are drug and non-drug options to help treat the symptoms. These include:

Medications for Memory: Cholinesterase inhibitors and memantine are common drugs used to treat memory loss and confusion. A doctor can prescribe these medications, so be sure to contact your health care provider.

Behavior Treatments: Some doctors may prescribe antidepressants, anxiolytics, or antipsychotic medications for people who demonstrate drastic behavior.

Alternative Treatments: Researchers believe that herbal remedies, dietary supplements, and certain foods can enhance memory and prevent Alzheimer’s. Some examples include coconut oil, coral calcium, and omega-3 fatty acids. To see an extended list, click here.

Alzheimer’s Care

Are you a caregiver? There are several options available to help a loved one diagnosed with Alzheimer’s. These options include:

Minor Assistance: You can help your loved one with simple tasks like removing objects that could cause injury, maintaining smoke alarms and fire extinguishers, and keeping dark areas, like stairwells, well lit.

Home Care: Home health services and adult day centers are two options that can help with more intensive health and well-being tasks, while the patient is still living in the home.

Residential Care: Residential care is common in the later stages of Alzheimer’s. Residential care can include assisted living, nursing homes, and Alzheimer’s special care units. These options can help with tasks like meal preparation, dressing, bathing, and other everyday tasks.

Alzheimer’s, like other forms of dementia, will often require long-term care. The type of care someone will need will change as the disease progresses; so, at some point, outside care will probably be necessary.

Outside care options include nursing home care, assisted living, adult care services, and respite care. Caring for Alzheimer’s patients in a nursing home is necessary when caring for your loved one at home has become overwhelming.

Alzheimer’s and Dementia Care: Tips for Daily Tasks

The Mayo Clinic organizes tips for caring for some with Alzheimer’s into two groups: things to do to reduce frustration and guidelines to follow to ensure a safe environment.

A care plan to reduce frustration could include the following:

Creating a daily routine for the patient.

Allowing the patient to take their time.

Doing tasks that involve the patient.

Offering the patient choices, such as offering finger foods if it’s time to eat but they are not hungry.

Providing instructions that are easy to understand and simple to follow. Establish eye contact to make sure the patient understands what has been said.

Reducing napping time so that the patient remains aware of whether it is day or night.

Reducing distractions when they are eating, such as turning off the television during mealtime to make it easier to focus on eating.

Some safety tips on dealing with Alzheimer’s patients could include the following:

Preventing falls by avoiding things that could trip a patient up, like extension cords, and installing handrails in places like bathrooms.

Putting locks on all cabinets that could contain dangerous equipment or materials, such as guns, power tools, utensils, cleaning detergents, and so on.

Checking water temperature before showers or baths to avoid scalding.

Avoid accidental fires by supervising smoking.

Making sure all carbon monoxide detectors and smoke alarms have charged batteries.

When applying these dementia caregiver tips, the caregiver needs to be patient and flexible and be open to changing routines as the symptoms of the disease progress.

Caring for the Caregiver

Family caregivers, such as a son or daughter caring for an Alzheimer’s parent, must prepare for a series of distressing experiences as they watch their mother or father forget favorite family memories and lose practical self-care skills.

It’s often challenging dealing with an Alzheimer’s parent because of the overwhelming emotions, the fatigue, the isolation, and the financial complications. Still, it’s rewarding to bond with a parent by providing them with care and service and solving their problems.

There are also new relationships with others they meet in a similar situation through support groups.

Getting Help With Caregiving

Initially, family caregivers can reduce stress by sharing their caregiving challenges with their support groups.

However, caregiver stress will increase as the disease progresses. While medications used for Alzheimer’s will control some symptoms, they can only provide a limited amount of memory care support before a patient experiences significant memory loss.

Eventually, it will become necessary to consider outside care options, such as respite care, senior care, or moving the patient to a skilled nursing senior center.

For information or support on what to do when caregiving for an Alzheimer patient becomes difficult, visit the Alzheimer’s Association at www.alz.org.

Coping With the Last Stages of Alzheimer’s

Alzheimer’s disease and related dementias affecting older adults get severe during the last stages of the disease. Patients will need considerable support because they will lose touch with what is going on around them.

It can be difficult to figure out how to talk to someone with Alzheimer’s when they don’t respond to what is happening in their environment, can’t communicate any discomfort or pain, and have difficulty controlling their movements.

Legal and Financial Planning

Legal and financial planning for someone with Alzheimer’s requires a specialized lawyer because any general powers of attorney will not work for asset protection planning. A skilled and experienced lawyer is also necessary if the patient needs a health care power of attorney document.

Role of Medicare and Alzheimer’s

Original Medicare (Parts A and B) cover inpatient hospital care and some doctor’s fees associated with Alzheimer’s. Plus, Medicare will pay up to 100 days of skilled nursing home care in certain circumstances.

Long-term custodial care, like a nursing home, is not covered. Medicare will pay for hospice care in-home or at a hospice facility.

Medicare Advantage plans are great options for coverage beyond Original Medicare.

Some people with Alzheimer’s may be eligible for a Medicare Special Needs Plan. SNPs are a different type of Medicare Advantage plan and generally provide coverage for doctor visits, hospital services, and prescription drugs. Some of these plans can coordinate care services to help you better understand your condition and your doctor’s plan.

If you qualify for a Medicare Special Needs Plan, you may also qualify for a Special Enrollment Period. This means you can enroll or change Medicare plans throughout the year!

If you have any questions about Medicare Special Needs Plans or Special Enrollment Periods do not hesitate to contact us. Our licensed agents are contracted with all the major carriers across 50 states and can help you enroll in a plan that fits your needs and budget.

To schedule a no-cost, no-obligation appointment, click here or call us at (833)-567-3163.

Does Medicare Cover Hospice Care?

More than 1.7 million Americans use hospice each year to maintain or improve their quality of life due to a terminal illness. Hospice care plans address physical, emotional, and spiritual pain and offer support to caregivers during the grieving process.

Hospice decisions can take an emotional and financial toll on you and your family, so you may be asking… “Does Medicare cover hospice?”

How does Medicare cover hospice care?

If you are enrolled in Medicare Part A (hospital insurance), you may qualify for hospice care. However, you must meet the following criteria:

Your doctor certifies that you are terminally ill (with a life expectancy of less than 6 months)

You accept palliative care (for comfort) rather than try to cure your condition

You sign an agreement choosing hospice care over other Medicare-covered benefits to treat your illness

You are not eligible if you had already made a hospice election or have not previously received pre-election hospice services (evaluation of your need for pain and symptom management).

If you meet the above criteria, the following services may be part of your hospice care plan and are covered in part by Medicare:

Other services focused on pain and symptom management

There may be a co-payment of $5 for your prescription drugs or other pain relief. You may also need to pay five percent of the Medicare-approved amount for respite care. However, the following services are not covered by Medicare:

Hospice is intended for people who have six months or less to live. To receive hospice care, you can not receive curative treatment.

If you decide to receive treatment, your hospice care is no longer covered. However, you can withdraw from your hospice care at any given point, and you can resume treatment as long as you are still eligible.

Prescription Drugs Intended to Cure

Just like you can’t pursue curative treatment, you can not take prescription drugs that are intended to cure your illness when receiving hospice care. Hospice only covers drugs that are intended for pain relief and control.

Care for Any Hospice Provider That Wasn’t Arranged by the Hospice Team

You are only eligible to receive care from the hospice team that you initially select.

You cannot get hospice coverage from a different provider unless you go through the switching process. However, you can still visit your regular doctor if they have been appointed to supervise your hospice care plan.

You can only switch to a different hospice provider once per benefit period. If you are interested in switching, be sure to do your research and pick a hospice team you feel comfortable with.

Does Medicare cover hospice room and board?

Medicare does not cover room and board regardless if you live at home, in a nursing home or inpatient assisted living facility, or inpatient hospice office. The only exception is during short-term inpatient or respite care stays in which Medicare will help cover the costs.

Emergency Care

Emergency transportation is not covered by Medicare’s hospice benefits. Medicare will not cover emergency inpatient hospital care unless they are arranged by your hospice team or unrelated to your terminal illness.

Does Medicare cover hospice in a nursing home or at home?

If you are eligible, Medicare will cover hospice care regardless if you receive the care in your home, nursing home, or inpatient facility. Some nursing homes work directly with a hospice team. In a nursing home setting, your hospice team can help with the following:

Regular visits to the nursing home

Consultations by specialized hospice physician as needed

Pain and medication management

Educating staff on symptoms, medications, and care

Emotional and spiritual support

Coordinating care across all patient’s medical providers including doctors, hospice team, and nursing home staff

How long will Medicare pay for hospice care?

Hospice care is intended for people who have less than an estimated six months to live. If you still require hospice care after six months, you can continue to receive benefits if a hospice doctor recertifies your terminal illness in a face-to-face meeting.

You can get hospice care for two 90-day benefit periods followed by an unlimited number of 60-day benefit periods.

Level One: This level includes basic care under Medicare’s hospice benefit. Services include nursing services, medical equipment & supplies, and medications.

Level Two: Medicare designates people who need continuous care such as home health care. The home health aide stays in the patient’s home for eight to 24 hours a day, but it’s short-term care. The patient’s needs are re-evaluated once every 24 hours.

Level Three: The third level of Medicare hospice coverage is general inpatient care. Some people have short-term symptoms that are so severe that they can’t get adequate treatment at home. With level three care, the patient has 24-hour care available.

Level Four: This level of care is more for the family than the patient. If the patient doesn’t meet the criteria for inpatient care and the family needs a break from daily care duties, respite care may be an option. Respite care provides caregivers temporary relief by admitting the patient to a hospital.

Medicare Palliative Care vs. Medicare Hospice Care Coverage

Medicare can cover palliative care for helping relieve symptoms in accordance with curative care. Some organizations define palliative care as “specialized medical care for people living with a serious illness” with the focus of care being symptom relief rather than to find a cure.

The difference between palliative care and hospice care is that palliative care can occur in conjunction with curative care.

Medicare may cover palliative care, but not under the Medicare hospice benefit.

Hospice and Medicare Supplements

Medicare Supplements can help cover the gaps in hospice care that Original Medicare may not, like prescription drugs for pain relief and respite care. After your Medicare coverage, you will likely be responsible for five percent of your total respite care costs and a $5 copay per prescription drug. Medicare Supplements can cover some, or all, of these gaps.

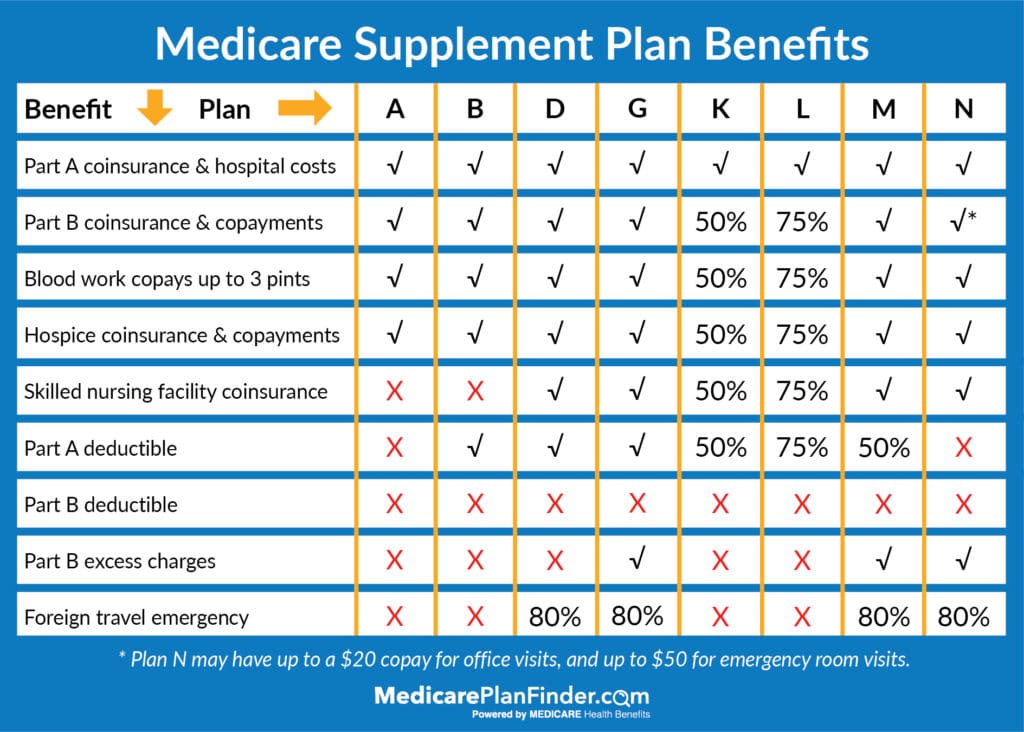

Medicare Supplement Plans A, B, D, G, M, N cover 100 percent of hospice coinsurance and copayments. Medigap Plan K covers 50 percent and Plan L covers 75 percent.

If you are interested in enrolling in a Medicare Supplement plan, or have questions on how these plans work with your correct coverage, click here to get in contact with a licensed agent.

2020 Medicare Supplement Comparison Chart

Hospice and Medicare Advantage

If you enroll in a Medicare Advantage plan, you will have the same hospice care coverage as with Original Medicare. However, Medicare Advantage plans can offer extra benefits like vision, hearing, and dental coverage. They may also offer fitness programs like SilverSneakers®.

If you are interested in enrolling in a Medicare Advantage plan, fill out this form, or give us a call at 844-431-1832. There is no cost to you to meet with one of our agents and there is never an obligation to enroll.

This post was originally published on April 16, 2019, and updated on November 18, 2019.

$0 Premium Humana Honor Plans for Veterans

Humana is one of the biggest Medicare Advantage carriers, with over 8.4 million members across all 50 states (plus D.C. and Puerto Rico). They’ve been active for over three decades! New this year, Humana is providing a “Humana Honor” Medicare Advantage plan.

Uniquely, though it is “available to anyone eligible for Medicare” who lives in the service area, this Medicare Advantage plan is designed to complement VA (Veteran’s Affairs) coverage. Many veterans think they have no use for Medicare Advantage (or even Medicare at all) due to their VA coverage, but a plan like this could be a game-changer.

Do you Need Medicare if you have VA Coverage?

For some people, the VA may provide all the coverage you need. But, if you can get additional coverage at no extra cost, why not take it?

Plus, even though there are 1,921 VA facilities across the country, wait times can be a problem. You can use this tool to find out what your local wait times are, but you might not need to if you have additional coverage. If you also have Medicare (and if you have Medicare Advantage), your network can be expanded to many more local doctors and other medical facilities, where you may have an easier time getting an appointment.

Plus, the VA does not automatically provide dental coverage to all veterans. You can purchase it through the VADIP (VA Dental Insurance Program), but you might not need to. If it makes sense for you and if it is available in your area, you can instead enroll in a Humana Honor or other Medicare Advantage plan that includes a dental benefit.

Humana Honor is available as 17 different plans available in 28 states:

Alabama

Arizona

Arkansas

California

Colorado

Delaware

Florida

Georgia

Idaho

Illinois

Indiana

Kansas

Louisiana

Maryland

Michigan

Mississippi

Missouri

Nevada

New Mexico

New York

Ohio

Oklahoma

Oregon

Pennsylvania

South Carolina

Tennessee

Utah

Washington

How to get Humana Honor Medicare Advantage

There are a few ways you can enroll in Humana plans, but we recommend speaking with a licensed agent. An agent can help you sort through all your options and make sure that the plan you like is truly the best plan for you. It is free to speak with a licensed agent regarding your healthcare, so it can only help!

You can speak to a MedicarePlanFinder.com agent by calling 844-431-1832 during business hours or clicking here.

Humana Taking Care of Veterans

Humana has strong relationships with (and is the national Medicare plan carrier for) the VFW (Veterans of Foreign Wars) and AMVETS (American Veterans). Infact, Humana partnered with the VWF’s “Uniting to Combat Hunger” campaign and helped raise money for over 500,000 veteran meals.

Humana has also contributed over one million dollars to the Entrepreneurship Bootcamp for Veterans with Disabilities, an organization that serves post-9/11 veterans. They also sponsor the Washington, D.C. Rolling Thunder Motorcycle Run during Memorial Day weekend, as well as the Wounded Warrior’s “Warrior Games.”

Additionally, Humana’s administration has hired over 4,500 veterans and veteran spouses since 2011.

Whether you like Humana’s Medicare Advantage plans or not, you have to give them props for their work with veterans and veteran families!

We’re proud to offer Humana plans through our insurance brokers and are excited to be a part of providing veterans with the care they deserve.

Good News: 2021 Medicare Advantage Plans Have Higher Ratings and Lower Premiums

It’s time to start making decisions for your healthcare coverage in 2021. The Annual Enrollment Period for Medicare beneficiaries is going on NOW and only lasts through December 7.

As you’re looking through your Medicare Advantage and Part D plan options for next year, you may notice that monthly premiums are shrinking and benefits are expanding!

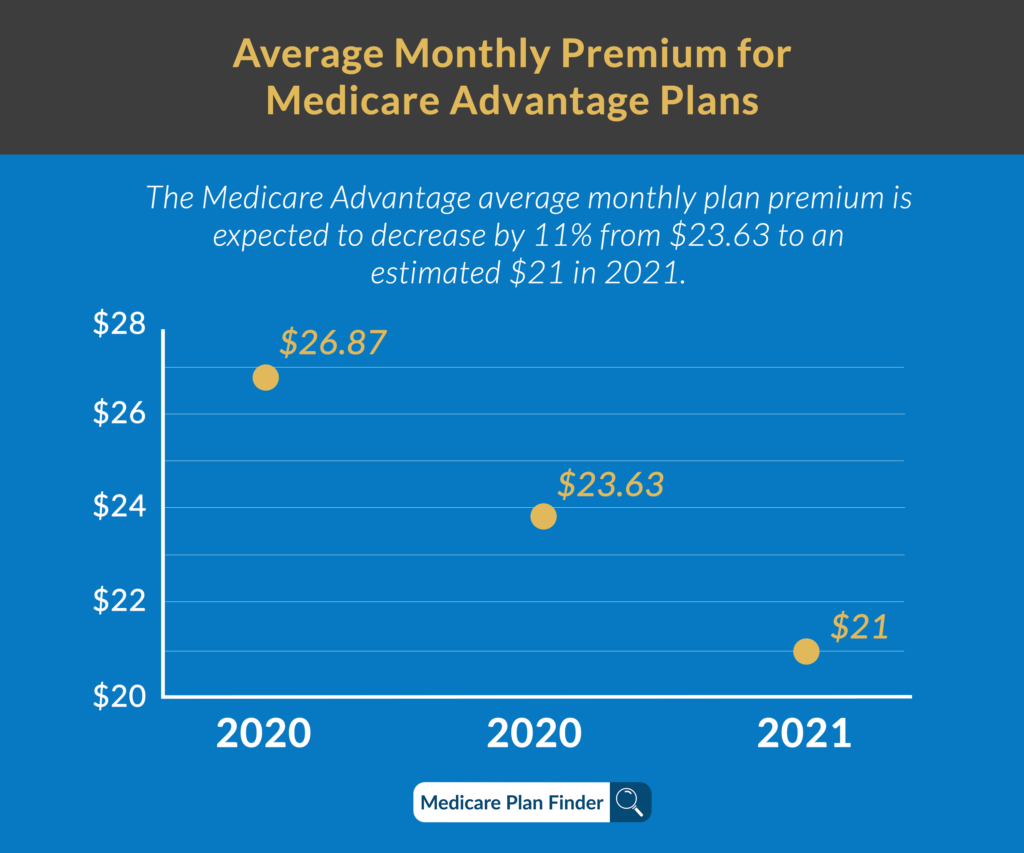

CMS (The Centers for Medicare & Medicaid Services) released a statement earlier this fall that said the average monthly premium for a Medicare Advantage plan in 2021 will be the lowest it’s been in 14 years (since 2007!)

In fact, the average Medicare Advantage (MA) premium will see a decrease of 34.2% from 2017, while plan choice and benefits continue to expand. In some states like Alabama, Nevada, and Kentucky, the average premium decrease since 2017 will be closer to 50%.

Medicare Part D prescription drug plans (PDPs) will also have low premiums in 2021, with standard plans averaging around $30.50 a month. This marks a 12% decrease in PDP premiums since 2017.

Average monthly Medicare Advantage premiums

Average star ratings increasing

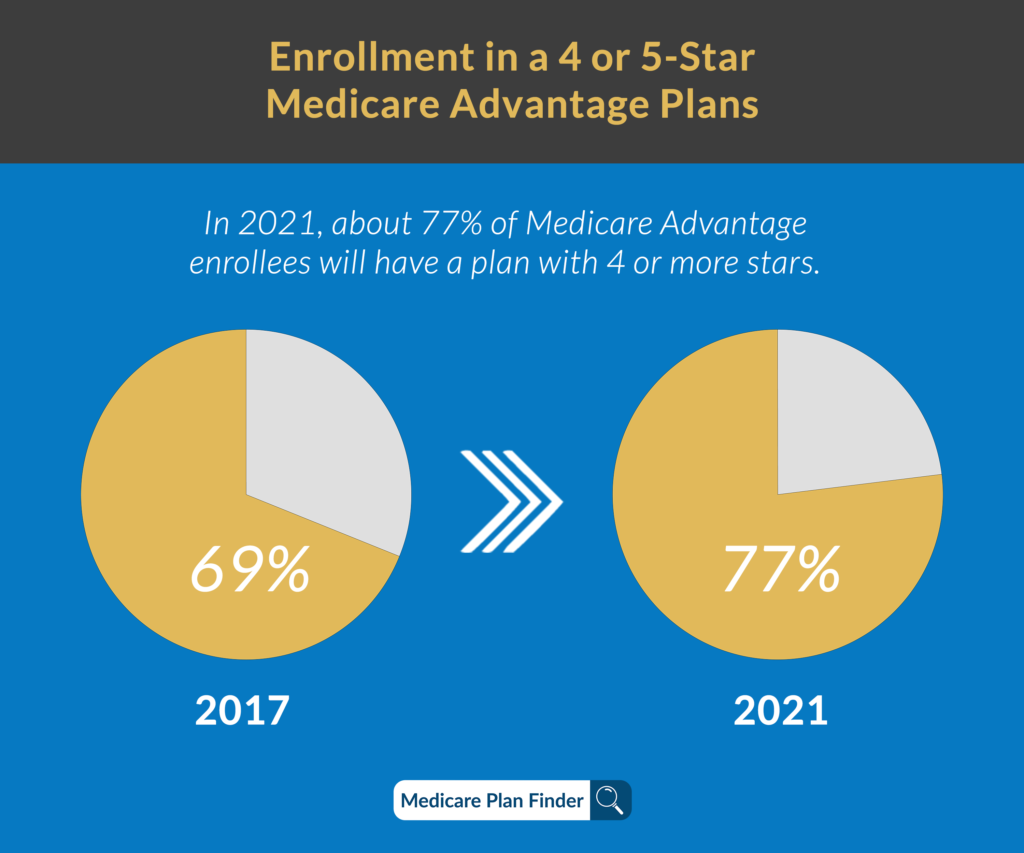

The average star ratings for Medicare Advantage and prescription drug plans in 2021 are set to increase significantly. About 77% of Medicare Advantage enrollees will have a plan with 4 or more stars, and 98% of those in a standalone PDP plan will have a rating of more than 3.5 stars.

There will also be more plans with a 5-star rating than were available in 2020, including UnitedHealthcare, Cigna, and Anthem BCBS. Even the lowest-rated plans have improved to at least 2.5 stars.

CMS uses this Medicare star rating system for Medicare Advantage and Part D plans to determine whether or not a plan is doing its job, and whether or not it can stay on the market. Plans that consistently receive poor ratings (one or two stars) will eventually be removed from the market.

Plans are given a star rating between one and five, with one being “poor” and five being “excellent.”

Medicare Advantage plans are rated on the following factors:

Level of access to preventive services (including annual physical exams and screenings)

Care coordination

How often members receive treatment for long-term conditions

Current member satisfaction

Plan performance in comparison to the previous year

Customer service quality

Part D plans are rated on the following:

Number of member issues with the plan

How many people left over one year

Patient safety while using prescriptions in the plan

Accuracy of pricing

Quality of care

Customer service quality

More and more Medicare Advantage and Part D plan carriers are entering the market every year, meaning there is more competition. More competition means that more plans are trying to be the most valuable to be able to compete. That’s why even though costs may be going down, plan ratings are still increasing.

If you plan on meeting with a licensed agent during this year’s Annual Enrollment Period, be sure to ask about four and five-star plans in your area!

3300Medicare Advantage star ratings increasing

Remind me: What is Medicare Advantage?

You can enroll in Medicare Advantage as an addition to your Original Medicare coverage. Since Medicare Advantage plans are owned and operated by private insurance companies and are not the same as the government Medicare program, the coverage is a bit different.

Medicare Advantage plans are able to cover things that Original Medicare is not, such as fitness programs, dental, vision, and prescription drugs.

Medicare Advantage plans might come with copayments, coinsurance, and deductibles, but the average premium for 2021 is expected to be $21/month.

If you can afford to add a Medicare Advantage premium, the benefits may save you from thousands of dollars in healthcare costs later on.

Expanded benefits for 2021

Earlier this year, CMS released the 2021 benefit and cost sharing information on Medicare.gov. In large part due to the coronavirus pandemic, they are offering expanded benefits in several key areas, and many health care providers are taking advantage of this flexibility.

There will be over 4,800 Medicare Advantage plans in 2021 for enrollees to choose from, a 76.6% increase since 2017. The number of MA plans per country is also growing in the new calendar year.

In response to the COVID-19 pandemic, 94% of all MA plans will provide added telehealth benefits. The current health crisis also drove CMS to develop the Part D Savings Model, which sets a $35 monthly copay rate for insulin. Over 1,750 MA and PDP plans are participating in this new model in 2021.Many health plans are also expanding their benefits for enrollees with chronic conditions. About 500 Medicare Advantage plans will feature either supplemental benefits or lower copays to those with specific chronic diseases or other conditions.

$0 Premiums and Special Needs Plans

Some people may even be eligible for a $0 premium Medicare Advantage plan. Others still may be eligible for low-cost Medicare Advantage Special Needs Plans.

CSNPs are Chronic Special Needs Plans and are for people who have certain chronic conditions and need additional coverage. ISNPs are Institutional Special Needs Plans and are for people who have been living in an institution such as an inpatient medical facility for 90 days or more. DSNPs are Dual Eligible Special Needs Plans and are for people who are dual-eligible for both Medicare and Medicaid.

How to Get a Low-Cost, Five-Star Medicare Advantage Plan in 2020

Our licensed agents across the nation are contracted and certified to sell a number of Medicare Advantage plans. An agent can sit down with you and show you all of the top-rated plans available in your area and help you select which one is best for you.

To get in touch with a licensed agent, call 844-431-1832 or click here.

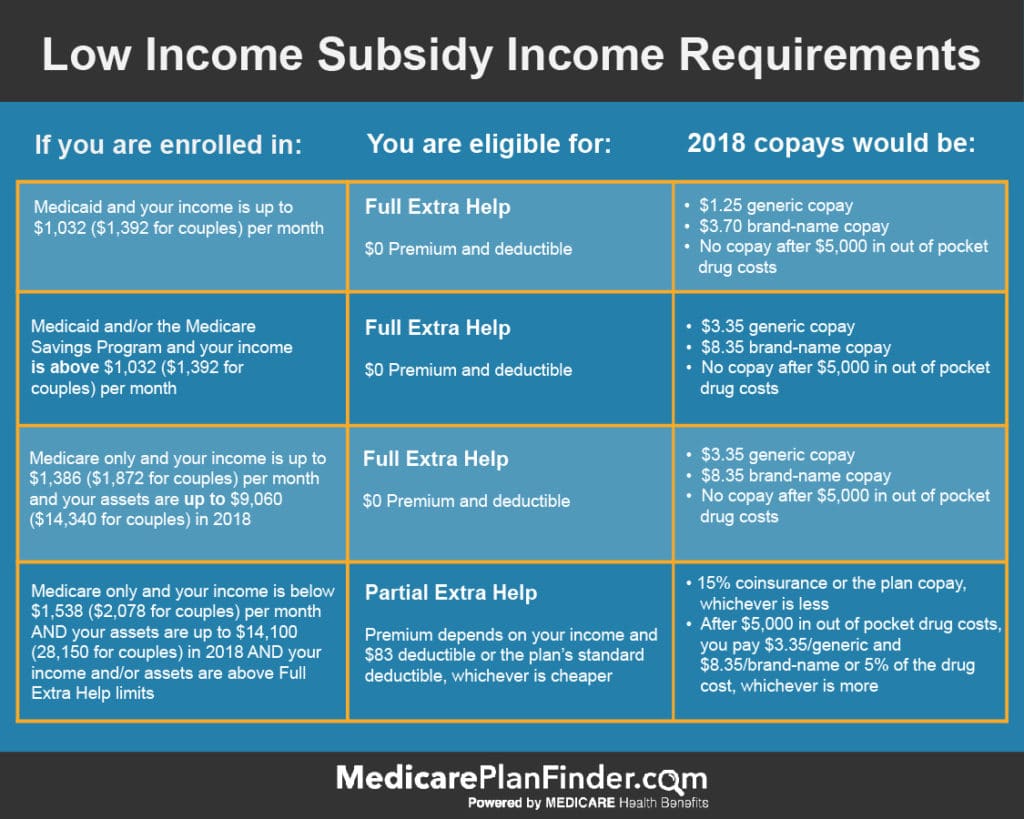

Medicare SEP Changes 2020: When You Can Enroll If You’re Eligible for a DSNP or LIS

DSNPs (Dual Special Needs Plans) are Medicare Advantage plans for people who are eligible for both Medicare and Medicaid. LIS (Low Income Subsidy), or Medicare Extra Help is a federal program that helps Medicare beneficiaries save money on prescription drugs.

If you are eligible for either DSNPs or LIS, your enrollment periods might be a bit different from others.

Am I Eligible for LIS?

If you’re eligible for Medicare and you make less than 150 percent of the Federal Poverty Level, you may qualify for LIS. You can also automatically qualify for Extra Help if you’re already on SSI or you qualify for a DSNP.

What Does LIS Cover?

LIS helps qualifying people pay for prescription drugs and it covers items such as Part D premiums, deductibles, and the “Donut Hole”.

LIS coverage is offered on a sliding scale. That means the subsidy provides more or less help depending on your qualifications.

For example, if you’re single and you qualify for full LIS and Medicare only, you’ll pay no more than $3.40 for covered generic drugs and $8.50 for covered brand-name drugs. You will have no copay once you spend $5,000 out-of-pocket for covered prescription drugs.

What are Medicare DSNPs (Dual-Eligible Special Needs Plans)?

DSNPs cover your Original Medicare premiums and services, and, since they’re Medicare Advantage plans, they can offer additional benefits* such as:

Many DSNPs have $0 monthly premiums, and if you see healthcare providers in your plan’s network, you shouldn’t have to pay Medicare deductibles and copays.

*Plan benefits and availability depend on many different factors such as location and carrier. Talk to your licensed agent to learn about available plans and covered services.

What Are the Changes to My SEP?

In the past, if you qualified for a lifelong SEP, you could enroll in a new DSNP, Medicare Advantage, or Part D plan up to once a month for the entire year.

In 2019 and 2020, if you’re eligible for a DSNP, LIS, or you only qualify for Medicare Savings Programs (MSPs) such as the Qualified Medicare Beneficiary (QMB) program or the Specified Low-Income Medicare Beneficiary (SLMB) program, the 2019-2020 CMS guidelines state that you can enroll in a new plan or drop coverage once per quarter for the first three quarters of the year (January – September).

Any changes you make during this time will become effective on the first of the month following the date you made the change. For example, if you enroll in a new DSNP plan on February 10, that change will become effective on March 1. You would not be able to make another change until the next quarter.

Q1: January – March

Q2: April – June

Q3: July – September

Q4: October – December

So, what does that mean for the rest of the year? Well, it means that you’ll fall into the AEP like everyone else.

The Annual Enrollment Period (AEP), which is October 15 to December 7, is a time when anyone can make changes to their existing Medicare coverage. Any AEP changes will take effect on January 1 of the following year. For example, if you make a change during AEP on November 15, that change will become effective on January 1.

Get the Medicare Health Insurance You Need Today

A licensed agent with Medicare Plan Finder may be able to help you find the coverage you need to stay in optimal health. Our agents are highly trained and they can find out what’s available in your area and help you make the right decision.

Our agents focus on the individual and offer an unbiased approach to helping you enroll in Medicare plans. To schedule a no-cost, no-obligation appointment, call 833-431-1832 or contact us here now.

2020 Medicare Changes & Trump’s Executive Order

Every year, CMS (Centers for Medicare and Medicaid Services) reserves the right to make changes to the Medicare program. Rules and regulations around enrollment periods, penalty fees, marketing, and plan benefits are released in late summer and early fall for the following year. Costs can rise, and brand new plans can enter or leave the market.

Medicare is confusing as it is. When you add these yearly changes into the mix, choosing the right plan can be stressful. Our goal is to make all of this less stressful for you. Our website is a great educational tool, and our licensed agents can provide free assistance!

Here are the changes you need to know about for Medicare in 2020.

On October 3, 2019, President Donald Trump signed an executive order “protecting” the Medicare program. What does this mean?

Alex Azar, Health and Human Services (HHS) Secretary, said that Trump told HHS to take “specific, significant steps” towards improving Medicare funding and improving healthcare for American seniors. These steps include lowering Medicare Advantage costs, allowing savings accounts, and improving access to new medical technology. It also leaves room for more plan options, more telehealth, more wellness benefits, and a stronger financial model.

In his post-executive order speech given in Florida yesterday morning, Trump stated, “In my campaign for president, I made you a sacred pledge that I would strengthen, protect and defend Medicare for all of our senior citizens.” That was the intent of the executive order.

Is Medicare Going Up in 2020?

New 2020 Medicare premiums and costs for 2020 have not been released yet. The new numbers are usually released in early fall of the year prior, so we are expecting to see them over the coming months. The Wall Street Journal reported in April that 2020 Medicare Part B premiums are likely to increase by $8.80/month to a total of $144.30, but this is not final.

We will continue to update this post with new 2020 costs as they are released. Thank you for your patience!

2020 Medigap Changes

Just like the Original Medicare program, private plans like Medicare Advantage, Medicare Supplements, and standalone benefit plans can change every year.

Plan availability may not be the same for everyone. Medigap eligibility, in particular, can depend on your age when you enroll, preexisting conditions, and where you live. Plans can be different not only in every state but also in every county and zip code.

Use our plan finder tool to find out what Medigap plans are available in your area for 2020.

Is Medicare Supplement Plan F Going Away in 2020?

Starting in 2020, you will no longer be able to purchase Medigap Plan F or Medigap Plan C. Plan F was one of the most popular plans, and Plan C was fairly similar. The plans are going away because they include coverage for the Part B deductible (only $185 in 2019).

You might here plans C and F referred to as “first-dollar” plans because they virtually eliminate out-of-pocket costs. CMS decided that taking away the Part B deductible coverage was a smart move to discourage people from overusing their primary physician offices and costing the Medicare program a lot of money for unnecessary doctor’s visits.

If you already have Medigap Plan F or Medigap Plan C, you can be grandfathered in. That means that you will not lose your coverage in 2020. However, if you leave your Plan F or Plan C in favor of a different Medigap plan, you won’t be able to re-enroll in F or C.

Will Plan F Premiums Rise After 2020?

As Plan F sees less and less enrollees, Plan F premiums will likely begin to rise. We can’t say this for sure and we will certainly have to wait and see what happens, but generally less enrollees means higher costs for the companies, resulting in higher premiums.

Will There be a High Deductible Plan G in 2020?

Since people will not be able to purchase Plan F or Plan C in 2020, CMS did want there to be another option with similar benefits. Plan G was already that option, given that the only difference is that Plan G does not cover the Part B deductible.

The other difference is that previously, Plan G was not offered with a high-deductible. If you typically have low medical costs, you may prefer a high-deductible option. Having a high deductible often means that your premiums will be lower. This way, you don’t have to pay as much until you start experiencing health concerns. The high deductible Plan G option can replace the high deductible F option.

Donut Hole Closing in 2020

In addition to all of these plan changes, the infamous “Donut Hole” will be effectively closing in 2020. The Bipartisan Budget Act of 2019 closed the coverage gap for brand-name drugs in 2019, and the generic drug coverage gap will be eliminated in 2020. This basically means that, if you have a Medicare Part D plan, you will only be responsible for 25% of your covered prescription drug costs instead of 44%.

2020 Medicare Advantage Changes

There may be more Medicare Advantage plan changes to come in 2020, but we wanted to make sure you had heard about the changes from last year.

On October 12, 2018, the Centers for Medicare and Medicaid (CMS) announced the 2019 Original Medicare premium and deductible increase, but what about Medicare Advantage (MA) plans? Unlike Medicare Part A and B, beneficiaries enrolled in MA plans may see a decrease in their premiums in 2019 and 2020 compared to 2018.

2020Medicare Advantage Cost Changes and 2020 Premiums

In September of 2018, CMS announced that on average, Medicare Advantage premiums will decrease by 6%. This is great for beneficiaries interested in affordable vision, dental, and hearing coverage or even fitness classes like SilverSneakers®!

CMS estimated that 83% of beneficiaries would have equal or lower premiums for 2019 and 46% will have a $0 premium! Premiums for MA plans have steadily declined, and this is the lowest premium we’ve seen in three years. This is a perfect example of a private and public collaboration that allows beneficiaries to drive and define the value. The 2019 Medicare Advantage changes are a quick glance of what you can expect to continue in the future.

2020 cost changes for Part A and B premiums and deductibles have not officially been released yet but are not expected to increase by very much. We will continue to monitor this information and will update as soon as the cost changes are officially announced.

Early in 2018, CMS (Centers for Medicare and Medicaid Services) released new rules that allow Medicare Advantage plans to offer a few benefits, like “daily maintenance,” transportation, telehealth, and durable medical equipment.

Some plans in 2020* are really going above and beyond, offering benefits like new air conditioners and pest control!

*These benefits are not included in all MA plans. Your agent may be able to help you find a plan that includes more.

Daily Maintenance

The addition of the “daily maintenance” benefit means that Medicare Advantage plans are now able to offer at-home care items, such as wheelchair ramps and other home modifications. Tied in with that benefit are other forms of durable medical equipment, like hospital beds, oxygen equipment, blood sugar monitors, etc, as well as “non-skilled” services. Non-skilled refers to items that do not require a licensed doctor or nurse, such as aides who can assist with bathing and dressing or homemakers who can help with cleaning and cooking.

Non-Emergency Medical Transportation Coverage

CMS has also added the ability for MA plans to provide non-emergency transportation coverage, a service that several Medicaid plans provide. This benefit (if your plan covers it) will allow you to receive free or low-cost rides to medical appointments and pharmacies. In most cases, you can only qualify for this benefit if you do not have another adequate means of transportation. The appointment that you are requesting a ride to must be for a Medicare-covered service.

Telemedicine and Telehealth

MA plans can now provide coverage for telehealth. That means you can have live video interaction with your doctor through digital clinics like HealthTap, Teladoc, and MDLive. Telehealth can also include health alerts delivered to your phone, health education apps, electronic medical data transfers, mail-order prescriptions, digital appointment scheduling and exam reminders, and more.

New Enrollment Period (OEP)

Before 2019, most people were only able to switch into new Medicare Advantage plans during the Annual Enrollment Period in the fall. Now, if you already have a Medicare Advantage plan, you may be eligible to make a change during OEP. OEP, or the Open Enrollment Period, takes place from January 1 through March 31. During this time, you can switch from one Medicare Advantage plan to another or drop your Medicare Advantage plan in favor of Original Medicare (Part A and Part B only).

Future of Medicare Advantage Plans

According to the Henry J Kaiser Family Foundation, enrollment has tripled to 19 million beneficiaries since 2003 and continues to grow each year. CMS estimates that MA enrollment will hit an all-time high of 22.6 million beneficiaries in 2019 (an 11.5% increase)!

As enrollment continues to increase, plan selection and variety increase too, with approximately 600 new plans offered in 2019! 99% of seniors and Medicare-eligibles have access to a MA plan – and 91% can choose from 10 or more plan options. Beneficiaries will not only see more plans to choose from, but also new supplemental Medicare benefits!

Enroll in a Medicare Advantage Plan in 2020

Are you interested in getting coverage beyond Original Medicare? Along with the new benefits, many Medicare Advantage plans offer dental, hearing, and vision coverage.

Our agents at Medicare Plan Finder can contract with nearly every carrier in your state! This means that you can enroll in the MA plan that best fits your needs and budget.

The Annual Enrollment Period runs from October 15 through December 7. Start looking over your plan benefits now so that you’re ready to enroll before December 7!

Ready to learn more? Call us at 844-431-1832 or fill out this form to arrange a no-cost, no-obligation appointment with an agent in your area.

*This post was originally posted on November 8, 2018, and was last updated on October 4, 2019.

How to Choose the Best Type of Medicare Plan for You

When it’s time to choose a Medicare plan, it’s easy to get overwhelmed. There are quite a few different types of Medicare plans to choose from. Once you choose what type you want – you still have to choose a plan! Making the right choice is important because it may not be easy to change plans if you change your mind.

The Annual Enrollment Period (October 15 through December 7) is when anyone can make changes, and for some people, it’s the only time. If you make the wrong choice, you might have to wait a whole year before you can change again (unless you qualify for the OEP or have a SEP).

Which Types of Medicare Plans are Best for Me?

To figure out which Medicare plan is best for you, ask yourself the following questions:

What specific medical services do I need coverage for (ex: lab tests, blood work, surgery, chemotherapy, dental, etc.)?

How much room do I have in my budget? Am I able to pay a little more to have more benefits?

Would I rather pay more on a monthly basis and pay very little when I visit the doctor, or is it better to pay a small amount every month but risk having higher copayments?

Who are the doctors and other providers who I want to be covered in my plan?

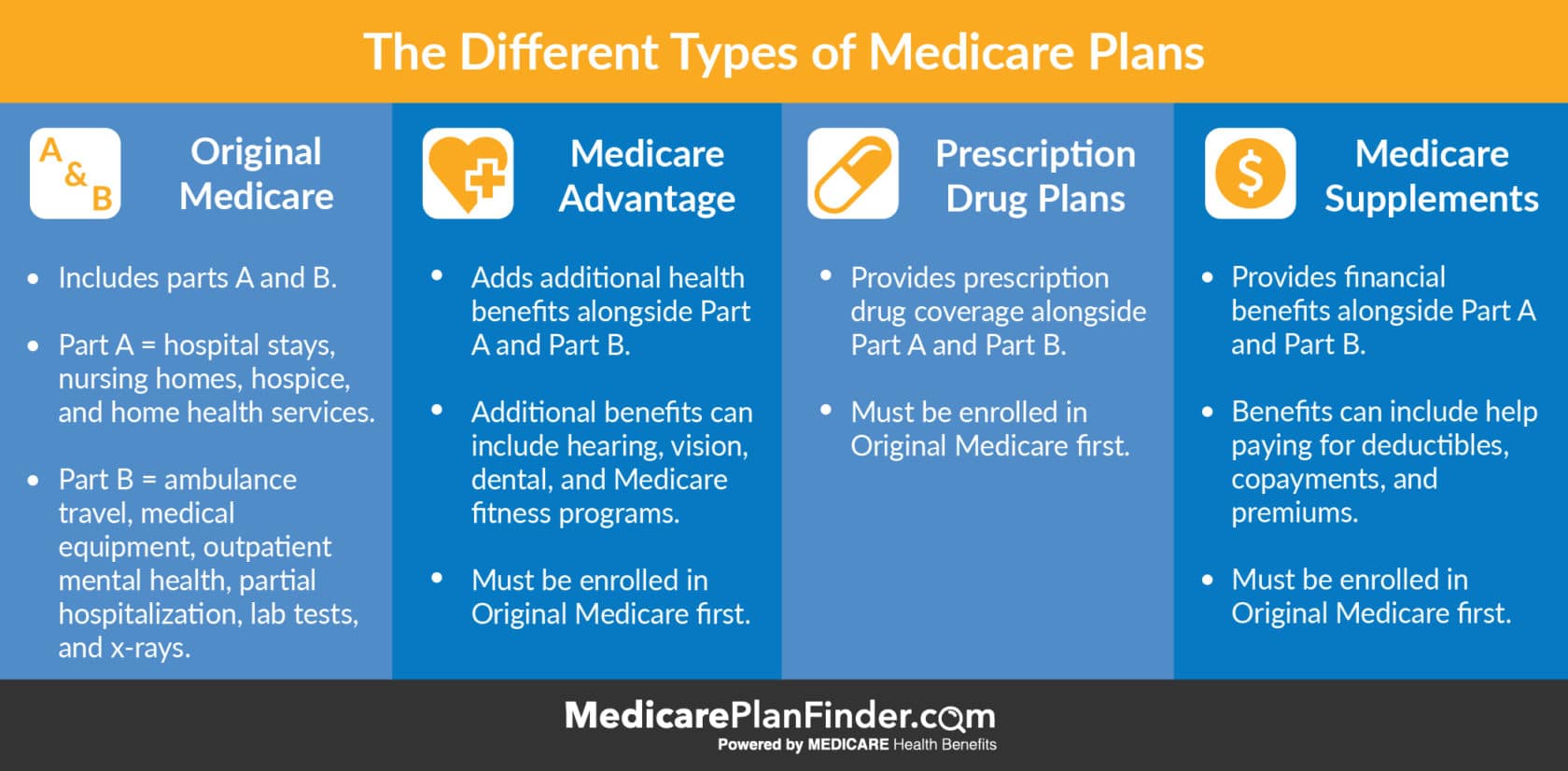

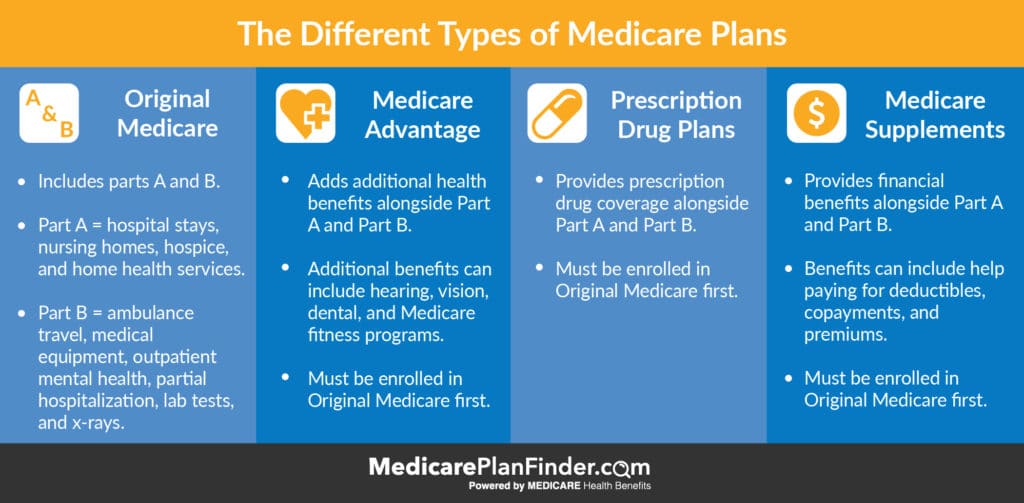

There are four main types of Medicare plans to consider when you begin your Medicare plan search. Start by comparing Original Medicare, Medicare Advantage, Prescription Drug Plans, and Medicare Supplements.

Keep in mind that you cannot have Medicare Advantage and a Prescription Drug Plan at the same time. You also cannot have Medicare Advantage and a Medicare Supplement plan at the same time.

Which plan or combination of plans works best for you?

Medicare Advantage: A private plan that you can purchase once you have Original Medicare. Can add additional benefits such as hearing, vision, dental, fitness, etc. Can include a prescription benefit.

Prescription Drug Plans: Another type of private plan that you can purchase once you have Original Medicare. Usually only includes a prescription benefit.

Medicare Supplements (Medigap): Another type of private plan that you can have in addition to Original Medicare. Adds more financial coverage, like for copayments and deductibles. This type of plan would also require you to have a stand alone part D drug plan.

Different Types of Medicare Plans

Choosing a Medicare Advantage Plan

So, did you decide to go with Medicare Advantage? Great! Now, there are a few types of Medicare Advantage plans that may be available for you. First, ask yourself whether or not you need a large network and whether the freedom to see any doctor is important to you. Then, read through these important differences:

HMO Plans (Health Maintenance Organization) – You’ll select one primary physician. In some cases, you may only receive coverage for that one doctor (unless he or she refers you to a specialist). Requirements may vary based on your plan.

HMO-POS Plans (Point-Of-Service) – You’ll select one primary physician, but you’ll have the freedom to visit any specialist in your network for your other needs. You will be charged a fee for visiting specialists.

PPO Plans (Preferred Provider Organization) – You can see any doctor, but your costs will usually be lower if you choose one that is in your network.

PFFS Plans (Private Fee-For-Service) – You will not need referrals or a primary physician, but you’ll have to pick a doctor that accepts your PFFS plan.

SNP (Special Needs Plans) – Designed for those who are eligible for both Medicare and Medicaid, live in a nursing home, or have a chronic illness or disability.

MSA (Medical Savings Account) – Works like a tax-free savings account for your medical bills. Medicare will deposit money into your HSA. You can use that account to pay for medical expenses.

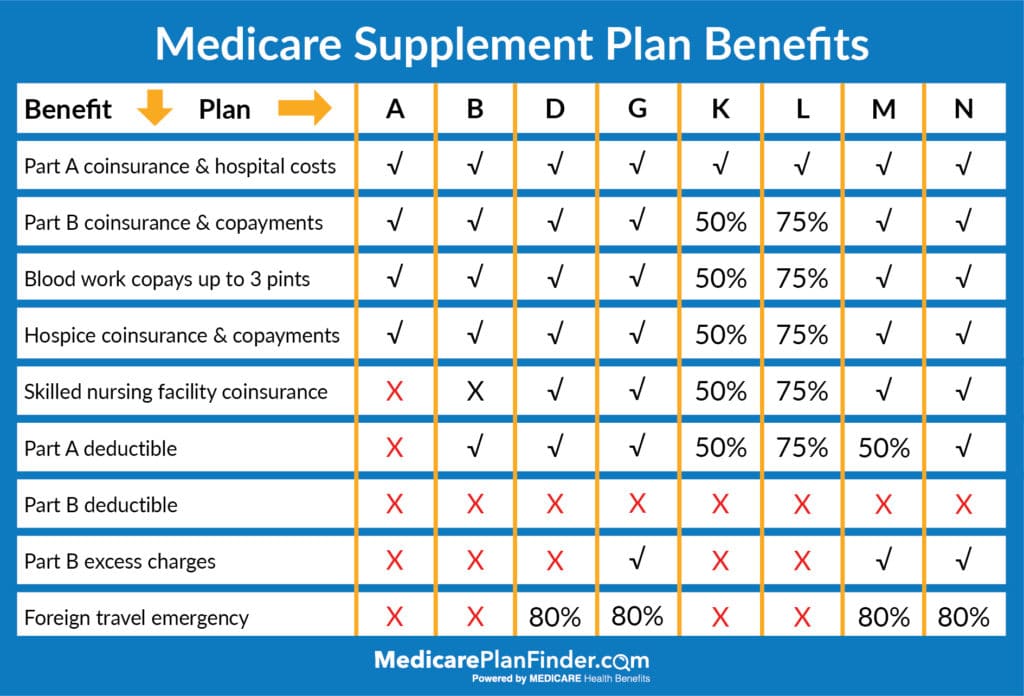

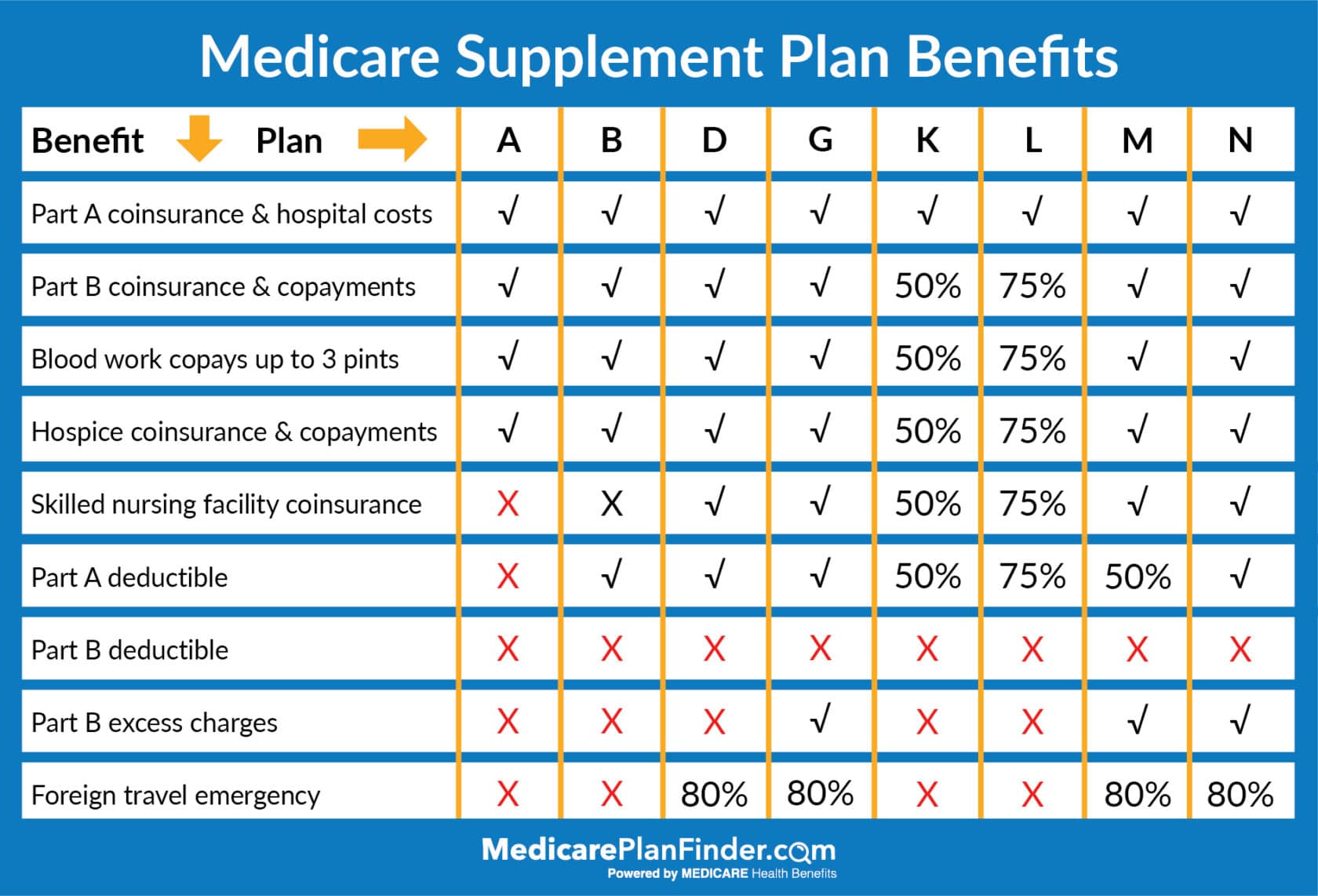

How do I Pick a Medicare Supplement Plan?

If you’ve decided that you want a Medicare Supplement plan, you’ll want to start by selecting the plan letter that corresponds with the coverage you need. Use the chart below for reference.

Once you’ve made that decision, you may have a few different carriers available in your area to choose from (some smaller cities may not have several options available).

Finding Medicare Plans in your area just got easier. Our Medicare Plan Finder tool can help you not only see what is available, but see which options may be best for your unique needs.

You can enroll by yourself, or you can meet with a licensed agent (for free) who can walk you through the process to make sure you don’t make any mistakes. The licensed agent can also talk to you about a variety of different types of plans in your area and answer all your questions.

This unbiased approach is a great way to get the help you need when selecting a Medicare plan.

To set up your free meeting with a Medicare Plan Finder licensed agent, call 833-567-3163 or click here.

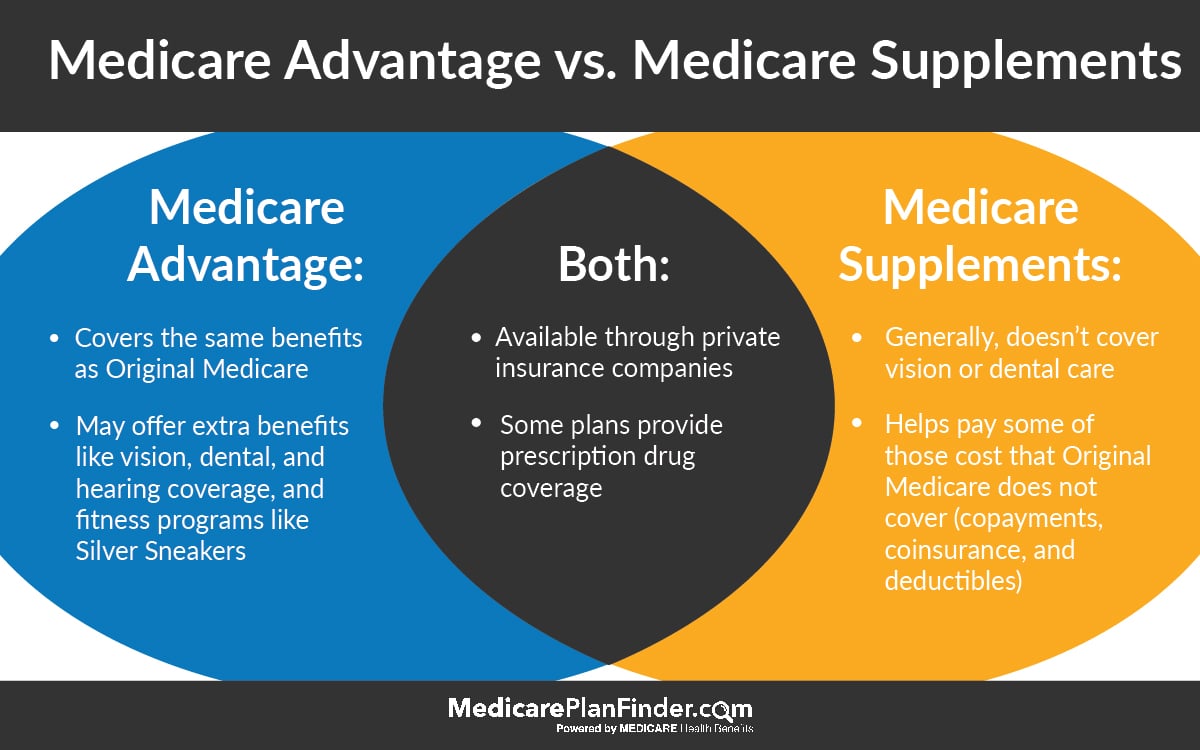

Medicare Advantage vs. Medicare Supplement

Medicare Advantage and Medicare Supplements (also called Medigap) are very different insurance plans with distinct benefits. The answer to the question “is Medicare Advantage better than Medigap?” depends on your circumstances and needs.

What is Medicare Advantage?

Medicare Advantage plans are private plans (not owned by the federal government) that can offer additional health benefits. To have Medicare Advantage, you have to enroll in Original Medicare first. You may have to continue to pay your Medicare Part B premium even if you have Medicare Advantage (MA), but MA premiums can be as little as $0.

Medicare Advantage plans are not all the same, but they can provide benefits like (click on the links to learn more about each one):

There are many different types of Medicare Advantage plans, although not every plan type may be available in your area.

A health maintenance organization (HMO) is a network of health-care providers and facilities where you choose a primary care physician to coordinate your care.

A preferred provider organization (PPO) is also a network of health-care providers and facilities but typically you do not need to select a primary care physician, and you have more flexible options regarding out-of-network care.

A private fee-for-service (PFFS) plan is a mode of benefit delivery where you are not limited to a network. However, there are no guarantees that your doctor or hospital will accept the plan. If you choose to receive your Medicare health coverage through a private Medicare Advantage plan, you must continue paying your Part B premium regardless, because you remain enrolled in Original Medicare (Part A and Part B), even after joining a Part C plan.

What is Medigap?

Medigap is more different from Medicare Advantage than you might think. While Medicare Advantage plans are able to offer health benefits, Medicare Supplement plans (also called Medigap) offer financial benefits. For example, some Medigap plans can cover your Part B premium.

The chart below explains the differences between available Medigap plans in 2020. You can also use our Medicare Plan Finder search tool to compare plans in your area.

2020 Medicare Supplement Comparison Chart

Comparing Medicare Advantage vs. Medicare Supplement plans

Let’s look at Medicare Advantage vs. Medigap. In short, the difference between Medicare Advantage and Medicare Supplement plans is that one can supply health benefits while the other can supply financial coverage.

Medicare Supplement Insurance is a policy that’s added to Original Medicare, Part A and Part B, to provide additional financial coverage. Medicare Advantage is a private plan option that may provide you with other health benefits that Original Medicare does not cover (like dental, vision, fitness programs, etc.).

You cannot have both Medicare Advantage and Medigap at the same time.

Medicare Advantage vs Medicare Supplements | Medicare Plan Finder

A given plan type (e.g., Plan F) has the same benefits regardless of the insurance company that provides the policy, or the state in which you reside. This is not true of Medicare Advantage plans, however, because coverage details may vary by plan.

Excluding prescription drug coverage, any standard Medigap plan with Part A and B will have more benefits than a standard Medicare Advantage plan. However, as mentioned above, some Medicare Advantage plans offer benefits beyond those found in Part A and Part B.

Some Medicare Advantage plans offer prescription drug coverage (often for an additional monthly cost). With a Medigap plan, in contrast, you would need to enroll in a separate prescription drug plan. When comparing plan options, consider your costs for drug coverage. In some cases, Medigap with a stand-alone prescription drug plan has lower total costs than a Medicare Advantage plan with drug coverage. In other cases, the reverse might be true.

[Tweet “Do your research! Comparing #Medicare Advantage vs Medicare Supplement”]

Real-Life Examples: Medicare Advantage vs. Medicare Supplements

Let’s take a look at some real-life examples to help you decide whether Medicare Advantage or Medicare Supplements are right for you.

If you have Medicare Parts A (hospital coverage), B (medical coverage), and D (prescription coverage) and you are hospitalized for cancer treatments for 90 days, you may have out of pocket costs. The Part A deductible means you would pay well over $1,000 first. Once you meet your deductible, your costs will go down. However, after day 60, you’ll be responsible for a portion of every day that you stay there.

If you have Medigap Plan B, your deductible and many of your other hospital costs will be covered. This plan would be in addition to your Part B coverage, so it would all work together to provide extra coverage.

If you have Medicare Advantage, you may have additional health benefits. You’d still likely be responsible for some of those out-of-pocket hospital costs, but your plan might provide a home healthcare benefit, meaning you can get a private in-home nurse when you are released from the hospital. You might also have coverage for medical equipment, such as bathroom safety equipment or a walker.

Comparison is key: Medicare Advantage vs. Medicare Supplements

When choosing between a Medigap plan and a Medicare Advantage plan, take the time to do your research. Read the benefit descriptions of every Medigap and Medicare Advantage plan you are considering. Be certain to look at:

Monthly premium

Deductibles

Doctor and healthcare facility restrictions

Benefits

Anticipated plan costs given your typical use of health-care and hospitalization services

Prescription drug coverage cost sharing as it relates to your medication usage

In the end, your decision is going to be the one that you feel the most comfortable with. The challenge is often wading through all the material to get to the bottom line. Want to make that a little easier? Give us a call at 844-431-1832.

This post was originally published on October 23, 2018, and was last updated on August 29, 2019.