Save Money on Prescription Drugs with Discount Cards

Do you have a high deductible or copayment for prescription drugs? Or maybe you’ve been prescribed a medication that isn’t covered by your insurance? Don’t worry, prescription discount cards could be the budget-friendly solution you need to cut down on costs.

What Are Prescription Discount Cards?

Prescription discount cards are offered through networks designed to help consumers save on medications. These cards are free, easy to use, and widely accepted at thousands of pharmacies nationwide. They can provide significant discounts on both brand-name and generic drugs, even for those without insurance.

Many of the top-rated prescription discount cards can be sent directly to your email or phone for immediate use.

By comparing available options and learning how these programs work, you can maximize your savings and make informed decisions about your prescription costs.

Why Consider Prescription Discount Cards?

Here are some key reasons why prescription discount cards are worth exploring:

Immediate Savings: You could save up to 80% or more on the retail price of prescription medications.

Ease of Use: Present your card at participating pharmacies and instantly access discounts.

Accessibility: These cards are free, require little to no personal information, and are available to everyone.

Versatility: Many programs also offer discounts on pet medications.

How Do They Work?

When you use a prescription discount card, the savings come from negotiated rates between pharmacies and pharmacy benefit managers (PBMs). PBMs act as middlemen, working to secure lower prices on drugs for consumers. This process often results in significant cost differences for the same medication at different pharmacies, so it’s essential to compare prices.

The Truth About Prescription Discount Cards

It’s normal to feel cautious about something that sounds too good to be true, especially when Medicare scams and other healthcare-related frauds are on the rise. Here’s how to identify legitimate prescription discount cards:

Clear Pricing Tools: Legitimate programs let you compare drug prices for both brand-name and generic medications online.

Pharmacy Acceptance: Ensure the card is accepted at your preferred pharmacies.

No Strings Attached: Reliable programs don’t require you to provide sensitive personal information.

Transparency: Discounts are consistent and comparable to other trusted programs.

Best Prescription Discount Cards in 2026

Not all prescription discount cards are created equal. Some may offer greater savings on specific medications or have more participating pharmacies in their network. Here are some of the top options to consider:

1. GoodRx

GoodRx is one of the most popular discount programs, allowing you to compare prices across 70,000+ pharmacies in real-time. The app provides coupons that can save you up to 80% on medications. Simply print, email, or text the coupon to yourself and present it at the pharmacy.

2. SingleCare

SingleCare offers a free prescription discount card that works at major pharmacies like CVS, Walmart, and Walgreens. Discounts can be as high as 80%. The program is user-friendly and doesn’t require personal information.

3. US Pharmacy Card

This free card is accepted at more than 59,000 pharmacies nationwide. It’s especially versatile, offering discounts on pet medications too. Cards can be printed, emailed, or texted directly to you.

4. Discount Drug Network

With potential savings of up to 85%, this card is another great option. It requires minimal information to sign up and offers a robust pricing tool for easy comparisons.

How to Use a Prescription Discount Card

Find a Participating Pharmacy: Popular options like Walmart, Walgreens, CVS, and Rite Aid often honor prescription discount cards.

Present Your Card: Show your card or coupon to the pharmacist when you pick up your prescription.

Compare Prices: Use online tools or mobile apps to compare prices before you head to the pharmacy.

Real-World Example: How Much Can You Save?

Let’s take the example of rosuvastatin (Crestor), one of the most commonly prescribed medications in the U.S.

Retail Price: $161.64 for a 30-day supply of 20 mg tablets (without insurance).

Discounted Price: With GoodRx, you could pay as little as $8.44 at Walmart.

That’s a massive saving of over $150 — just by using a free prescription discount card!

Prescription Discount Cards and Medicare

Navigating Medicare and prescription drug coverage can feel overwhelming. Fortunately, a licensed agent can help you understand your options, whether you’re looking at Part D plans, Medicare Advantage, or supplement plans.

If you’re interested in learning more, schedule a no-cost, no-obligation appointment with one of our licensed agents today. Call us at (833)-567-3163 or fill out our online form.

Final Thoughts

Prescription discount cards can be a game-changer for anyone looking to reduce their medication costs. Whether you’re uninsured, underinsured, or simply looking for a way to save, these programs provide an easy and effective solution.

Take the first step toward savings today. Explore your options, download a card, and start comparing prices at your local pharmacies.

Medicare Plan F Going Away (and Plan C) | ENROLL NOW!

What’s all this talk about “Medicare Plan F?” Is Plan F going away?

It’s true – Medicare Supplement Plan F is GOING AWAY in 2020! If you still want Plan F, you only have until December 31, 2019, to get locked in.

When you enroll in Original Medicare (Part A and Part B), you have the option of increasing coverage by purchasing a Medicare Supplement plan (also called Medigap). These plans work alongside Original Medicare and add financial benefits (like help paying for your copayments, coinsurance, and yearly deductibles).

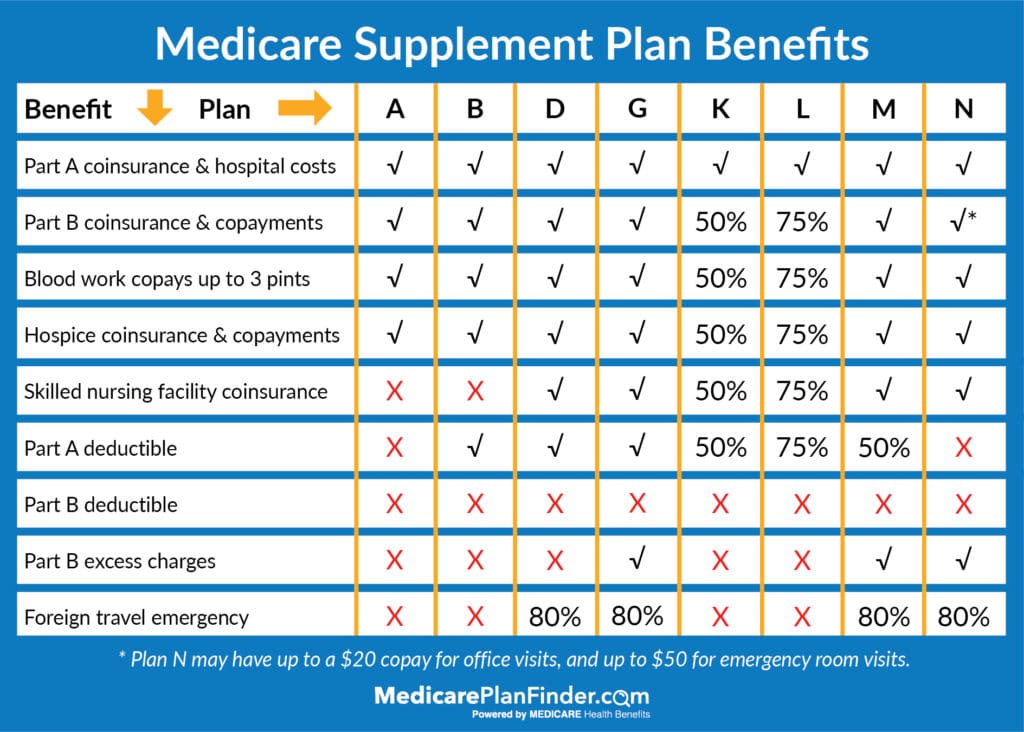

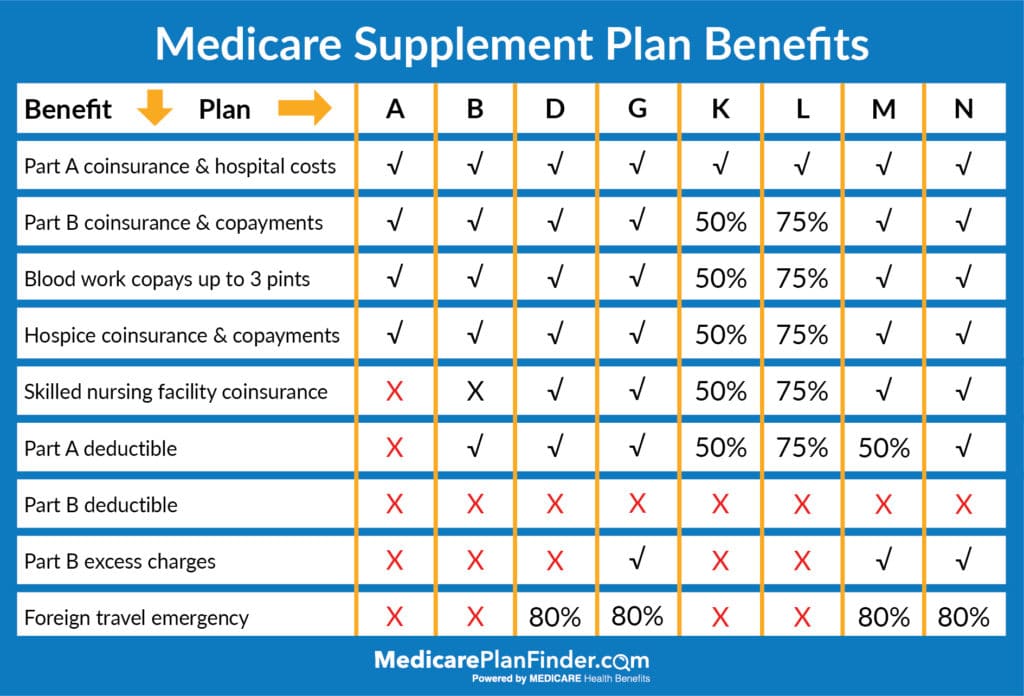

Every state (except Massachusetts, Minnesota, and Wisconsin) has ten different types of plans. Each plan is represented by a different letter (A, B, C, D, F, G, K, L, M, and N). Plan F and Plan C are the most inclusive, and in turn, are the most popular. But did you know both plans are going away in 2020?

Plan F has been a top-seller in many states for years and is the most comprehensive Medigap plan. Medicare Plan F covers:

Blood work copays up to three pints (100%)

Foreign travel emergency (80%)

Hospice coinsurance and copayments (100%)

Part A coinsurance and hospital costs (100%)

Part A deductible (100%)

Part B coinsurance and copayments (100%)

Part B deductible (100%)

Part B excess charges (100%)

Skilled nursing facility coinsurance (100%)

Medicare Plan C Benefits

Medicare Plan C covers all of the gaps from Original Medicare except for Part B excess charges. More specifically, Plan C includes the following:

Blood work copays up to three pints (100%)

Foreign travel emergency (80%)

Hospice coinsurance and copayments (100%)

Part A coinsurance and hospital costs (100%)

Part A deductible (100%)

Part B coinsurance and copayments (100%)

Part B deductible (100%)

Skilled nursing facility coinsurance (100%)

Plan F vs Plan C

Plan F is very similar to Plan C. The only difference is that Plan C does not cover Medicare excess charges. If a doctor does not accept Medicare assignment rates, you will be responsible for excess charges, but it can not exceed 15% of what Medicare pays. Some states do not allow doctors to issue excess charges. If this is the case, Plan C will operate identically to Plan F.

Back in 2015, Congress passed the Medicare Access and CHIP Reauthorization Act. According to the act, starting on January 1, 2020, Medicare Supplement plans can no longer cover the Part B deductible, something that only Medigap Plans F and C currently cover.

When people don’t have to pay a deductible for services, they can end up overusing the doctor. For example, the might schedule an appointment with their doctor for a flu shot instead of using the free clinic inside their local grocery store. By visiting the doctor unnecessarily (and not paying for it), doctor’s offices are getting crowded and doctors aren’t being fully compensated for their time.

Eliminating Part B deductible coverage through Medigap works better financially for the Medicare program and for the doctors who accept it.

Thankfully, that Part B deductible is a small price to pay at $257 per year in 2026.

When will Medicare Plan F be discontinued? What about Plan C?

If you currently have Medicare Supplement Plan F or Plan C, don’t fret! This policy change only affects new beneficiaries. While your rates may increase (as they technically do every year), you will not lose your current coverage. However, if you leave your Medigap Plan F or Plan C for whatever reason, you will not be able to go back to it after 2020. If you do not have Plan F or Plan C, but you would like to, you can lock yourself in by enrolling NOW.

Due to this change, Plan F and Plan C beneficiaries will be given a chance to compare rates and switch to a new policy. If you decide you may want to switch, you can start by using our Medicare Plan Finder tool to decide what plan option (other than F) is best for you. If you still need help, click here to request a call from a local and licensed agent!

Will Plan F Costs Go Up in 2020?

It is certainly possible that Plan F costs will go up as it is phased out, though it hasn’t been confirmed yet.

Uniquely, the state of Idaho released a memo stating that the Idaho Department of Insurance “is NOT anticipating abnormally large premium increases on Plan F after 2020” in response to questions about Plan F leaving the market. Even people who already have Plan F in Idaho and want to switch to a different Plan F after this year should not face large rate increases.

Can I Get Plan F in 2025?

No, Medicare Plan F was discontinued back in 2020. If you already have Plan F, don’t worry – you can keep your coverage.

What is a good alternative to Plan F?

Many seniors and Medicare eligibles who already have Plan F are deciding to drop Plan F altogether and switch to Plan G. Plan G covers everything that Plan F does minus the Part B deductible, and it typically has a lower monthly premium.

Another popular plan is Plan N. The only benefit that is included in Plan G and not Plan N is the coverage for Part B excess charges. However, the thing to remember about excess charges is they are relatively rare. You will only be charged an excess charge if your provider does not accept Medicare.

Medicare Plan F vs Plan G

Great news! Plan G is almost identical to Plan F! The only difference is that Plan G does not cover the Part B deductible. Plan F may technically cover more, but many people consider Plan G to be a better value. Yes, you will need to pay your Part B deductible upon your first outpatient visit, but after you pay the deductible, you won’t need to pull your wallet out for the remainder of the year. Since you have to pay the Part B deductible yourself, Plan G has lower monthly premiums, and you could save more than $400 a year!

The standard Part B deductible for 2026 is $257, so the savings from choosing G over F significantly outweighs the cost of the deductible.

Is Medicare going away or just certain plans?

No, Medicare is not going away! Don’t panic!

Both Medicare Plan F and Medicare Plan C will be discontinued on January 1, 2020, but other options may be available in your area. We get it, Medicare coverage and plan options can be confusing and stressful. Policies are constantly changing, and healthcare will continue to evolve.

At Medicare Plan Finder, our agents are kept up to date on all the plans in your area and can help you find a plan that suits your needs and budget. If you’re interested in arranging a no-cost, no-obligation appointment, click here or give us a call at (833)-567-3163.

This blog was originally published on October 23, 2018, by Kelsey Davis. The latest update was updated on December 5, 2019, by Troy Frink.

What Does Medicare Cost in 2019-2020?

Surprise! Medicare is not free, as some may believe. Medicare beneficiaries can owe a variety of charges, including monthly premiums, yearly deductibles, and per-service copayments and coinsurance. What does that mean?

Coinsurance = the percentage of a medical service that you owe

Copayment = the fee you pay upon receiving a medical service or good

Deductible = the amount you will owe before your coverage begins

Premium = the amount you owe your insurance company or Medicare every month

Costs can change every year. We’ll keep this guide up-to-date so that you can know what to expect from your Medicare coverage this year.

How Much Does Medicare Cost at Age 65?

Medicare costs do not change as you age, but they can change if you wait too long to enroll. If you age into the Medicare program and sign up when you turn 65, it will cost $144.60 per month (2020) for Part B, unless you make too much money, in which case you’ll pay more. You’ll also play anywhere from $0-$458/month (2020) for Part A, depending on how much you’ve worked and contributed to Medicare taxes.

However, if you miss your Initial Enrollment Period (which begins three months before you turn 65 and ends three months after), you may be charged a late enrollment penalty fee. The penalty means that your premiums can be up to 10% higher than the base cost. Don’t wait to enroll!

Turning 65 Checklist

What Does Medicare Cost Per Month in 2019-2020?

Your monthly Medicare costs will depend largely on what you qualify for and what you’ve signed up for.

Part A costs depend on how much you’ve worked. If you:

Worked and paid Medicare taxes for over 39 quarters of your life? You won’t pay a Medicare Part A premium in 2019

Worked and paid Medicare taxes for 30-39 quarters of your life? You’ll pay $252/month in 2020

Worked and paid Medicare taxes for less than 30 quarters of your life? You’ll pay $458/month in 2020

Additionally, if you are eligible for retirement benefits from either Social Security or the Railroad Retirement Board, you will not owe a Part A premium.

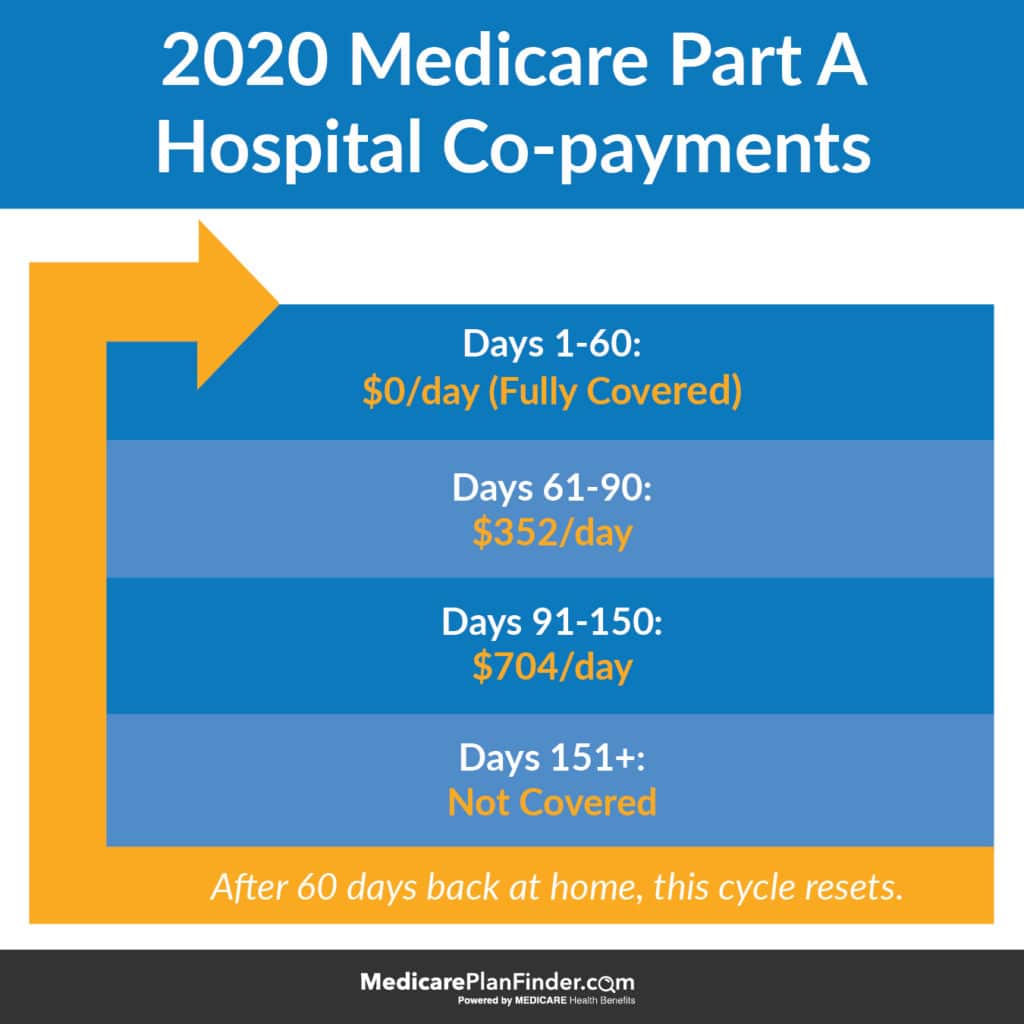

The Part A inpatient hospital deductible has increased from $1,340 in 2019 to $1,408 in 2020.

Despite these premium costs, you may incur other costs, like deductibles, coinsurance, and copayments.

Hospital copayments depend on how many days you’ve been in the hospital. Your first 60 days are completely covered, then you’ll face copayments. Remember that you will also have to pay your deductible first ($1,408 in 2020).

2020 Medicare Part A Copayments

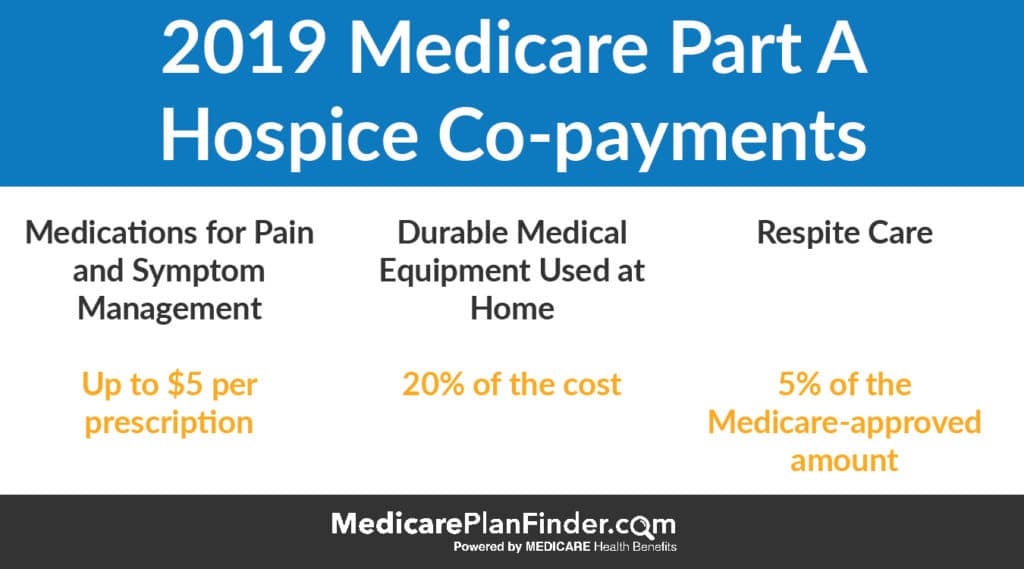

Hospice and nursing facilities are a bit different. The charts below explain some of the hospice and nursing facility costs that you may incur with Part A.

2020 Medicare Part A Skilled Nursing CopaymentsMedicare Part A Hospice Copayments | Medicare Plan Finder

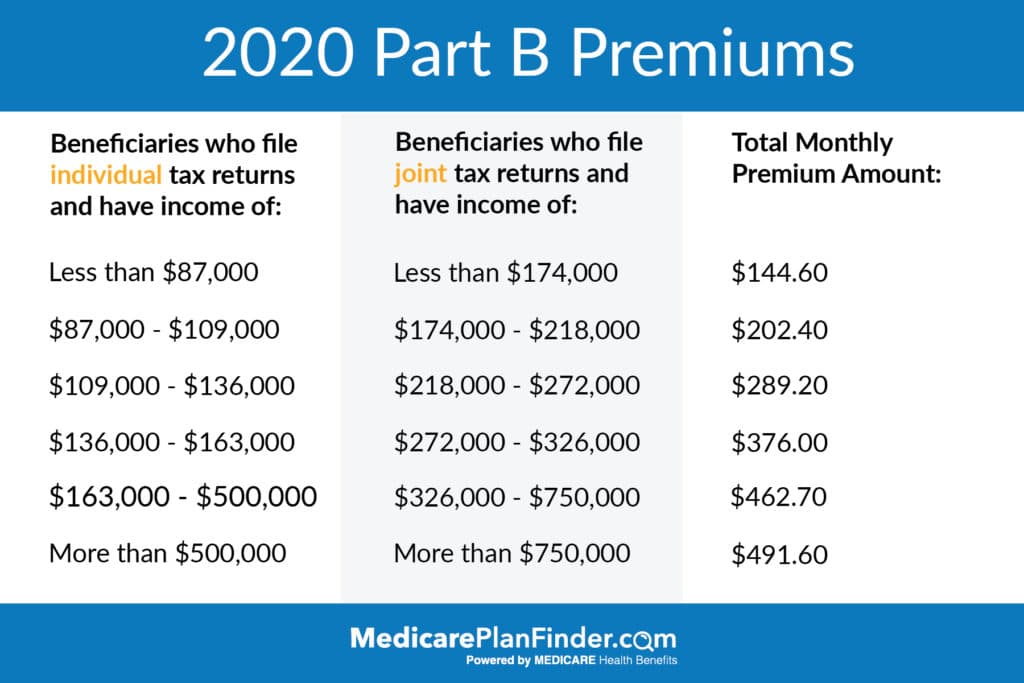

The standard monthly premium for Part B in 2020 is $144.60, but that can change based on your income.

An estimated 3.5% of beneficiaries (2 million) will pay less than this amount due to the Social Security “hold harmless” provision which prevents the increased premium to exceed the increase in Social Security benefits.

Additionally, if you make more than $87,000 a year, your monthly Part B premium will be adjusted based on your income. The income-based 2020 premiums for Part B are as follows:

2020 Medicare Part B Premiums

Will Medicare Part B Premiums Increase in 2019?

Generally, Medicare premiums change once per year. The change has historically been incremental and has even been a decrease in certain years.

The standard Part B premium decreased in 1989 and 1996. Since 2000, it has been steadily increasing to the $144.60 that we have today.

2020 Medicare Part B Deductible Increase

The Medicare Part B deductible increased from $185 in 2019 to $198 in 2020, an increase of $12.

Medicare as a whole has been trying to discourage beneficiaries from taking advantage of small deductibles, as evidenced by the removal of Medigap Plan F from the market.

Who Has to Pay for Medicare Part B?

Everyone enrolled has to pay the Medicare Part B premium, but some people may qualify for savings. For example, if you are eligible for a Medicare Savings Program, you may be able to have your Medicare Part A and B premiums, deductibles, coinsurance, and copayments covered (depending on which program you qualify for).

How to Save on Medicare Premiums in 2020

You may be able to save on Medicare premiums by qualifying for Low-Income Subsidies (LIS), also known as Medicare Extra Help, or a Medicare Savings Program (MSP). LIS provides help with Medicare prescription costs, and MSPs provide help with a variety of other costs, such as premiums and deductibles.

There are four major MSPs:

Qualified Medicare Beneficiary Program (QMB). Can help pay premiums for Part A and Part B, as well as copays, deductibles, and coinsurance. An individual may qualify in 2019 with an income up to $1,061 per month or $1,430 per month for a couple. If you qualify for QMB, you may also be eligible for Extra Help (LIS) paying for Part D prescription coverage.

Specified Low Income Medicare Beneficiary Program (SLMB). Can help pay premiums for Part B. A single person may qualify in 2019 with an income up to $1,269 per month or $1,711 per month for a couple. If you qualify as a SLMB, you’re may be eligible for LIS paying for Part D prescription coverage.

Qualified Disabled and Working Individuals Program (QDWI). Can help to pay Part A premiums. This MSP is for disabled people who lost their premium-free Medicare Part A when they went back to work. The income limits for QDWI are $4,249 per month for an individual, and $5,722 for a couple in 2019. The asset limit is $4,000 for an individual and $6,000 for a couple.

In 2019, people with LIS did not pay more than $3.40 for generic drugs and $8.50 for brand-name drugs!

To qualify for LIS, you must have a monthly income of less than $1,405 for an individual or less than $1902 for a couple in 2019. You must also

Have Original Medicare (Part A and Part B) coverage

Have prescription drug coverage (either a Medicare Part D plan or a Medicare Advantage plan with prescription drug benefits)

Have American citizenship

Not have savings, investments, and real estate valuing more than $28,150 if you are married or $14,100 if you are single

Medicare Advantage and Medicare Supplement 2019–2020

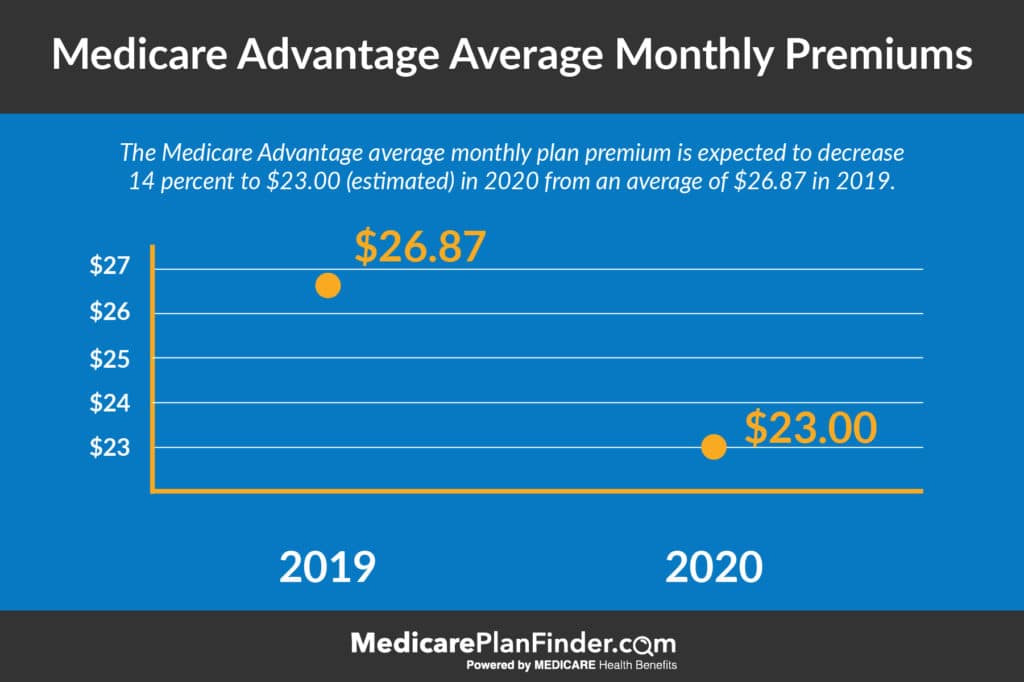

In 2020, Medicare Advantage premiums have decreased on average.

Medicare Advantage Premiums 2020

What does this mean for you? If your premium went up and you need a better option, the time is now! The annual enrollment period is October 15 through December 7. During this time you can switch or enroll in the best plan that fits your needs and budget. Our licensed agents can answer any questions you may have. If you’re interested in scheduling a no-cost, no-obligation appointment, fill out this form or call us at 844-431-1832.

This post was originally published on November 1, 2018, and was last updated on November 5, 2019.

2020 Medicare Changes & Trump’s Executive Order

Every year, CMS (Centers for Medicare and Medicaid Services) reserves the right to make changes to the Medicare program. Rules and regulations around enrollment periods, penalty fees, marketing, and plan benefits are released in late summer and early fall for the following year. Costs can rise, and brand new plans can enter or leave the market.

Medicare is confusing as it is. When you add these yearly changes into the mix, choosing the right plan can be stressful. Our goal is to make all of this less stressful for you. Our website is a great educational tool, and our licensed agents can provide free assistance!

Here are the changes you need to know about for Medicare in 2020.

On October 3, 2019, President Donald Trump signed an executive order “protecting” the Medicare program. What does this mean?

Alex Azar, Health and Human Services (HHS) Secretary, said that Trump told HHS to take “specific, significant steps” towards improving Medicare funding and improving healthcare for American seniors. These steps include lowering Medicare Advantage costs, allowing savings accounts, and improving access to new medical technology. It also leaves room for more plan options, more telehealth, more wellness benefits, and a stronger financial model.

In his post-executive order speech given in Florida yesterday morning, Trump stated, “In my campaign for president, I made you a sacred pledge that I would strengthen, protect and defend Medicare for all of our senior citizens.” That was the intent of the executive order.

Is Medicare Going Up in 2020?

New 2020 Medicare premiums and costs for 2020 have not been released yet. The new numbers are usually released in early fall of the year prior, so we are expecting to see them over the coming months. The Wall Street Journal reported in April that 2020 Medicare Part B premiums are likely to increase by $8.80/month to a total of $144.30, but this is not final.

We will continue to update this post with new 2020 costs as they are released. Thank you for your patience!

2020 Medigap Changes

Just like the Original Medicare program, private plans like Medicare Advantage, Medicare Supplements, and standalone benefit plans can change every year.

Plan availability may not be the same for everyone. Medigap eligibility, in particular, can depend on your age when you enroll, preexisting conditions, and where you live. Plans can be different not only in every state but also in every county and zip code.

Use our plan finder tool to find out what Medigap plans are available in your area for 2020.

Is Medicare Supplement Plan F Going Away in 2020?

Starting in 2020, you will no longer be able to purchase Medigap Plan F or Medigap Plan C. Plan F was one of the most popular plans, and Plan C was fairly similar. The plans are going away because they include coverage for the Part B deductible (only $185 in 2019).

You might here plans C and F referred to as “first-dollar” plans because they virtually eliminate out-of-pocket costs. CMS decided that taking away the Part B deductible coverage was a smart move to discourage people from overusing their primary physician offices and costing the Medicare program a lot of money for unnecessary doctor’s visits.

If you already have Medigap Plan F or Medigap Plan C, you can be grandfathered in. That means that you will not lose your coverage in 2020. However, if you leave your Plan F or Plan C in favor of a different Medigap plan, you won’t be able to re-enroll in F or C.

Will Plan F Premiums Rise After 2020?

As Plan F sees less and less enrollees, Plan F premiums will likely begin to rise. We can’t say this for sure and we will certainly have to wait and see what happens, but generally less enrollees means higher costs for the companies, resulting in higher premiums.

Will There be a High Deductible Plan G in 2020?

Since people will not be able to purchase Plan F or Plan C in 2020, CMS did want there to be another option with similar benefits. Plan G was already that option, given that the only difference is that Plan G does not cover the Part B deductible.

The other difference is that previously, Plan G was not offered with a high-deductible. If you typically have low medical costs, you may prefer a high-deductible option. Having a high deductible often means that your premiums will be lower. This way, you don’t have to pay as much until you start experiencing health concerns. The high deductible Plan G option can replace the high deductible F option.

Donut Hole Closing in 2020

In addition to all of these plan changes, the infamous “Donut Hole” will be effectively closing in 2020. The Bipartisan Budget Act of 2019 closed the coverage gap for brand-name drugs in 2019, and the generic drug coverage gap will be eliminated in 2020. This basically means that, if you have a Medicare Part D plan, you will only be responsible for 25% of your covered prescription drug costs instead of 44%.

2020 Medicare Advantage Changes

There may be more Medicare Advantage plan changes to come in 2020, but we wanted to make sure you had heard about the changes from last year.

On October 12, 2018, the Centers for Medicare and Medicaid (CMS) announced the 2019 Original Medicare premium and deductible increase, but what about Medicare Advantage (MA) plans? Unlike Medicare Part A and B, beneficiaries enrolled in MA plans may see a decrease in their premiums in 2019 and 2020 compared to 2018.

2020Medicare Advantage Cost Changes and 2020 Premiums

In September of 2018, CMS announced that on average, Medicare Advantage premiums will decrease by 6%. This is great for beneficiaries interested in affordable vision, dental, and hearing coverage or even fitness classes like SilverSneakers®!

CMS estimated that 83% of beneficiaries would have equal or lower premiums for 2019 and 46% will have a $0 premium! Premiums for MA plans have steadily declined, and this is the lowest premium we’ve seen in three years. This is a perfect example of a private and public collaboration that allows beneficiaries to drive and define the value. The 2019 Medicare Advantage changes are a quick glance of what you can expect to continue in the future.

2020 cost changes for Part A and B premiums and deductibles have not officially been released yet but are not expected to increase by very much. We will continue to monitor this information and will update as soon as the cost changes are officially announced.

Early in 2018, CMS (Centers for Medicare and Medicaid Services) released new rules that allow Medicare Advantage plans to offer a few benefits, like “daily maintenance,” transportation, telehealth, and durable medical equipment.

Some plans in 2020* are really going above and beyond, offering benefits like new air conditioners and pest control!

*These benefits are not included in all MA plans. Your agent may be able to help you find a plan that includes more.

Daily Maintenance

The addition of the “daily maintenance” benefit means that Medicare Advantage plans are now able to offer at-home care items, such as wheelchair ramps and other home modifications. Tied in with that benefit are other forms of durable medical equipment, like hospital beds, oxygen equipment, blood sugar monitors, etc, as well as “non-skilled” services. Non-skilled refers to items that do not require a licensed doctor or nurse, such as aides who can assist with bathing and dressing or homemakers who can help with cleaning and cooking.

Non-Emergency Medical Transportation Coverage

CMS has also added the ability for MA plans to provide non-emergency transportation coverage, a service that several Medicaid plans provide. This benefit (if your plan covers it) will allow you to receive free or low-cost rides to medical appointments and pharmacies. In most cases, you can only qualify for this benefit if you do not have another adequate means of transportation. The appointment that you are requesting a ride to must be for a Medicare-covered service.

Telemedicine and Telehealth

MA plans can now provide coverage for telehealth. That means you can have live video interaction with your doctor through digital clinics like HealthTap, Teladoc, and MDLive. Telehealth can also include health alerts delivered to your phone, health education apps, electronic medical data transfers, mail-order prescriptions, digital appointment scheduling and exam reminders, and more.

New Enrollment Period (OEP)

Before 2019, most people were only able to switch into new Medicare Advantage plans during the Annual Enrollment Period in the fall. Now, if you already have a Medicare Advantage plan, you may be eligible to make a change during OEP. OEP, or the Open Enrollment Period, takes place from January 1 through March 31. During this time, you can switch from one Medicare Advantage plan to another or drop your Medicare Advantage plan in favor of Original Medicare (Part A and Part B only).

Future of Medicare Advantage Plans

According to the Henry J Kaiser Family Foundation, enrollment has tripled to 19 million beneficiaries since 2003 and continues to grow each year. CMS estimates that MA enrollment will hit an all-time high of 22.6 million beneficiaries in 2019 (an 11.5% increase)!

As enrollment continues to increase, plan selection and variety increase too, with approximately 600 new plans offered in 2019! 99% of seniors and Medicare-eligibles have access to a MA plan – and 91% can choose from 10 or more plan options. Beneficiaries will not only see more plans to choose from, but also new supplemental Medicare benefits!

Enroll in a Medicare Advantage Plan in 2020

Are you interested in getting coverage beyond Original Medicare? Along with the new benefits, many Medicare Advantage plans offer dental, hearing, and vision coverage.

Our agents at Medicare Plan Finder can contract with nearly every carrier in your state! This means that you can enroll in the MA plan that best fits your needs and budget.

The Annual Enrollment Period runs from October 15 through December 7. Start looking over your plan benefits now so that you’re ready to enroll before December 7!

Ready to learn more? Call us at 844-431-1832 or fill out this form to arrange a no-cost, no-obligation appointment with an agent in your area.

*This post was originally posted on November 8, 2018, and was last updated on October 4, 2019.

The Medicaid Look Back Period: What You Need to Know

What is the Medicaid look back period?

Medicaid is designed to provide health care to those with low income or limited assets and is administered through each state. When applying for Medicaid, the state social security office is responsible for confirming you have limited income and assets. The Medicaid look back period is a period of time the office will review to see if you sold, donated, transferred, or gifted any of your assets. The period is 5 years for every state except California where it is 2.5 years. This period starts on the date you apply for Medicaid.

Is there a penalty?

Yes, there is! If the social security agency finds that you sold, donated, transferred, or gifted any of your assets beyond the granted exemptions, you will have a penalty. The penalty is a length of time that you will be ineligible for Medicaid. This is called the penalty period, and there is no limit on the amount of time you can be penalized for.

The penalty is based on the dollar amount of sold, donated, transferred, or gifted assets divided by the monthly private patient rate of care in a nursing home. For example, if you gifted $60,000 during the look back period and the average monthly cost of nursing home care is $4,000, your penalty would be 15 months of Medicaid ineligibility ($60,000 gift/$4,000 average month cost = 15 months).

Can you avoid the penalty?

Planning is key in an attempt to avoid the penalty. Did you know you can gift up to $15,000 a year without paying a gift tax? This is a great option if you’re wanting to leave a certain amount of your savings to a child or loved one. If you want to gift $60,000 it will take 4 years to avoid taxation. This means that you would need to start gifting 9 years before applying for Medicaid to avoid the look back penalty.

Are there exemptions?

Fortunately, there are exceptions that allow applicants to transfer assets without a penalty. The exceptions include:

Spouses

Medicaid applicants can transfer a certain amount of their assets to their spouse. The spouse cannot be in the Medicaid application process and must plan to live independently in the community. The total amount of assets able to be transferred will change annually, but in 2018 the limit is $123,600.

Disabled Children

Applicants can transfer their assets or establish trust funds for disabled children who are under the age of 21, including children who are legally blind.

Siblings

A home can be transferred to a sibling who has equity in the home and resided in the home for a minimum of one year prior to a nursing home placement.

Caregivers

Applicants can transfer their home to their adult children if they lived in the home for a minimum of two years before the Medicaid application was started. The child must be the primary caregiver.

Debt

Applicants can pay off their debt without a penalty.

If you’re interested in learning more Medicaid information that is specific to your state, visit our Medicaid by State page. Plus, you may be eligible for both Medicare and Medicaid! Our licensed agents can help answer any questions you may have and help you sort through your health care options. To get started, fill out this form or call us at 844-431-1832.