Surprise! Medicare is not free, as some may believe. Medicare beneficiaries can owe a variety of charges, including monthly premiums, yearly deductibles, and per-service copayments and coinsurance. What does that mean?

Coinsurance = the percentage of a medical service that you owe

Copayment = the fee you pay upon receiving a medical service or good

Deductible = the amount you will owe before your coverage begins

Premium = the amount you owe your insurance company or Medicare every month

Costs can change every year. We’ll keep this guide up-to-date so that you can know what to expect from your Medicare coverage this year.

How Much Does Medicare Cost at Age 65?

Medicare costs do not change as you age, but they can change if you wait too long to enroll. If you age into the Medicare program and sign up when you turn 65, it will cost $144.60 per month (2020) for Part B, unless you make too much money, in which case you’ll pay more. You’ll also play anywhere from $0-$458/month (2020) for Part A, depending on how much you’ve worked and contributed to Medicare taxes.

However, if you miss your Initial Enrollment Period (which begins three months before you turn 65 and ends three months after), you may be charged a late enrollment penalty fee. The penalty means that your premiums can be up to 10% higher than the base cost. Don’t wait to enroll!

Turning 65 Checklist

What Does Medicare Cost Per Month in 2019-2020?

Your monthly Medicare costs will depend largely on what you qualify for and what you’ve signed up for.

Part A costs depend on how much you’ve worked. If you:

Worked and paid Medicare taxes for over 39 quarters of your life? You won’t pay a Medicare Part A premium in 2019

Worked and paid Medicare taxes for 30-39 quarters of your life? You’ll pay $252/month in 2020

Worked and paid Medicare taxes for less than 30 quarters of your life? You’ll pay $458/month in 2020

Additionally, if you are eligible for retirement benefits from either Social Security or the Railroad Retirement Board, you will not owe a Part A premium.

The Part A inpatient hospital deductible has increased from $1,340 in 2019 to $1,408 in 2020.

Despite these premium costs, you may incur other costs, like deductibles, coinsurance, and copayments.

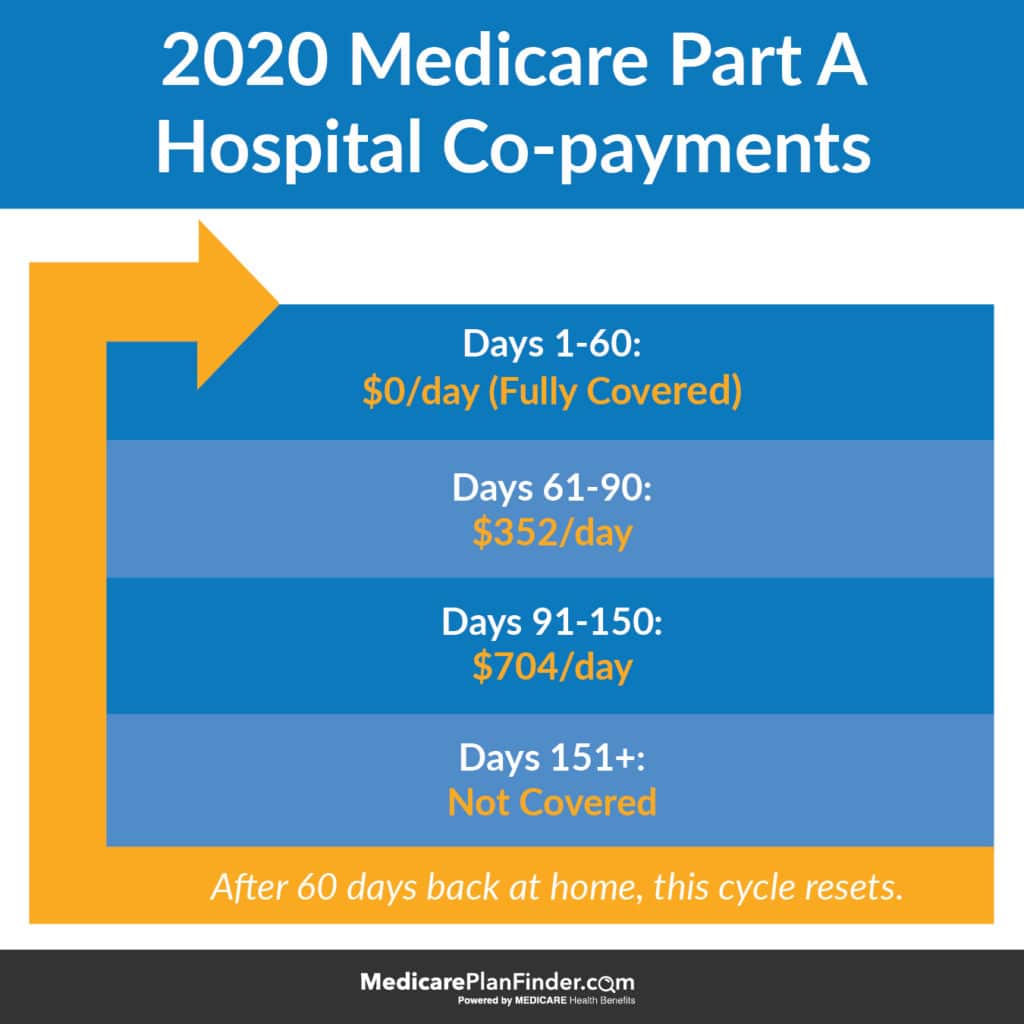

Hospital copayments depend on how many days you’ve been in the hospital. Your first 60 days are completely covered, then you’ll face copayments. Remember that you will also have to pay your deductible first ($1,408 in 2020).

2020 Medicare Part A Copayments

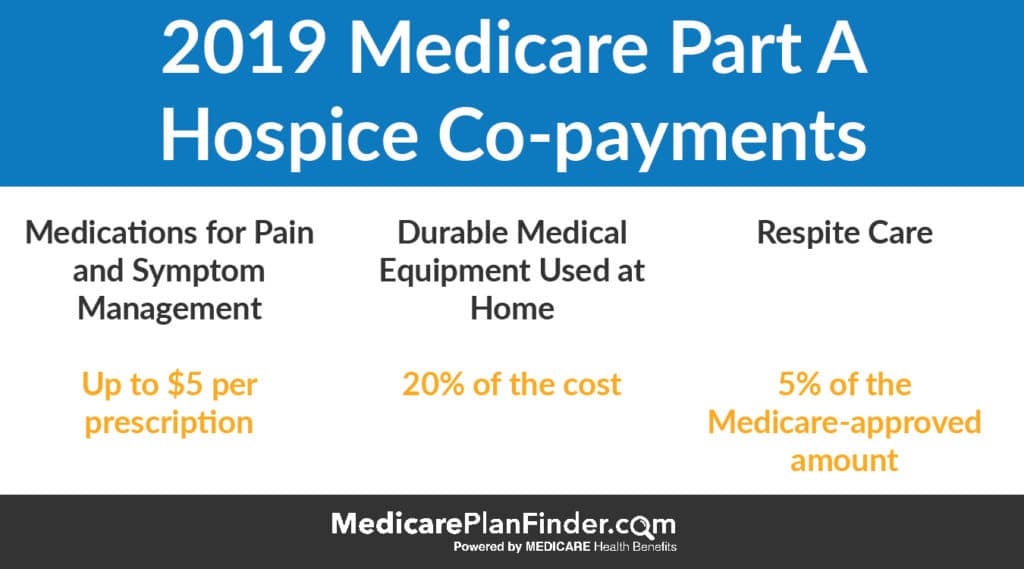

Hospice and nursing facilities are a bit different. The charts below explain some of the hospice and nursing facility costs that you may incur with Part A.

2020 Medicare Part A Skilled Nursing CopaymentsMedicare Part A Hospice Copayments | Medicare Plan Finder

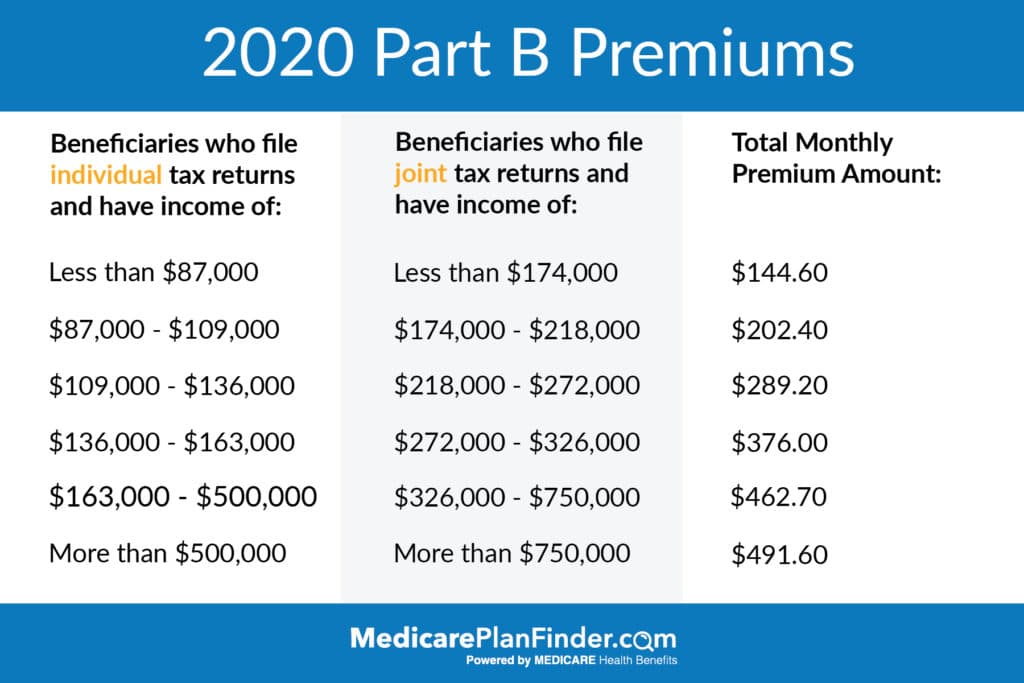

The standard monthly premium for Part B in 2020 is $144.60, but that can change based on your income.

An estimated 3.5% of beneficiaries (2 million) will pay less than this amount due to the Social Security “hold harmless” provision which prevents the increased premium to exceed the increase in Social Security benefits.

Additionally, if you make more than $87,000 a year, your monthly Part B premium will be adjusted based on your income. The income-based 2020 premiums for Part B are as follows:

2020 Medicare Part B Premiums

Will Medicare Part B Premiums Increase in 2019?

Generally, Medicare premiums change once per year. The change has historically been incremental and has even been a decrease in certain years.

The standard Part B premium decreased in 1989 and 1996. Since 2000, it has been steadily increasing to the $144.60 that we have today.

2020 Medicare Part B Deductible Increase

The Medicare Part B deductible increased from $185 in 2019 to $198 in 2020, an increase of $12.

Medicare as a whole has been trying to discourage beneficiaries from taking advantage of small deductibles, as evidenced by the removal of Medigap Plan F from the market.

Who Has to Pay for Medicare Part B?

Everyone enrolled has to pay the Medicare Part B premium, but some people may qualify for savings. For example, if you are eligible for a Medicare Savings Program, you may be able to have your Medicare Part A and B premiums, deductibles, coinsurance, and copayments covered (depending on which program you qualify for).

How to Save on Medicare Premiums in 2020

You may be able to save on Medicare premiums by qualifying for Low-Income Subsidies (LIS), also known as Medicare Extra Help, or a Medicare Savings Program (MSP). LIS provides help with Medicare prescription costs, and MSPs provide help with a variety of other costs, such as premiums and deductibles.

There are four major MSPs:

Qualified Medicare Beneficiary Program (QMB). Can help pay premiums for Part A and Part B, as well as copays, deductibles, and coinsurance. An individual may qualify in 2019 with an income up to $1,061 per month or $1,430 per month for a couple. If you qualify for QMB, you may also be eligible for Extra Help (LIS) paying for Part D prescription coverage.

Specified Low Income Medicare Beneficiary Program (SLMB). Can help pay premiums for Part B. A single person may qualify in 2019 with an income up to $1,269 per month or $1,711 per month for a couple. If you qualify as a SLMB, you’re may be eligible for LIS paying for Part D prescription coverage.

Qualified Disabled and Working Individuals Program (QDWI). Can help to pay Part A premiums. This MSP is for disabled people who lost their premium-free Medicare Part A when they went back to work. The income limits for QDWI are $4,249 per month for an individual, and $5,722 for a couple in 2019. The asset limit is $4,000 for an individual and $6,000 for a couple.

In 2019, people with LIS did not pay more than $3.40 for generic drugs and $8.50 for brand-name drugs!

To qualify for LIS, you must have a monthly income of less than $1,405 for an individual or less than $1902 for a couple in 2019. You must also

Have Original Medicare (Part A and Part B) coverage

Have prescription drug coverage (either a Medicare Part D plan or a Medicare Advantage plan with prescription drug benefits)

Have American citizenship

Not have savings, investments, and real estate valuing more than $28,150 if you are married or $14,100 if you are single

Medicare Advantage and Medicare Supplement 2019–2020

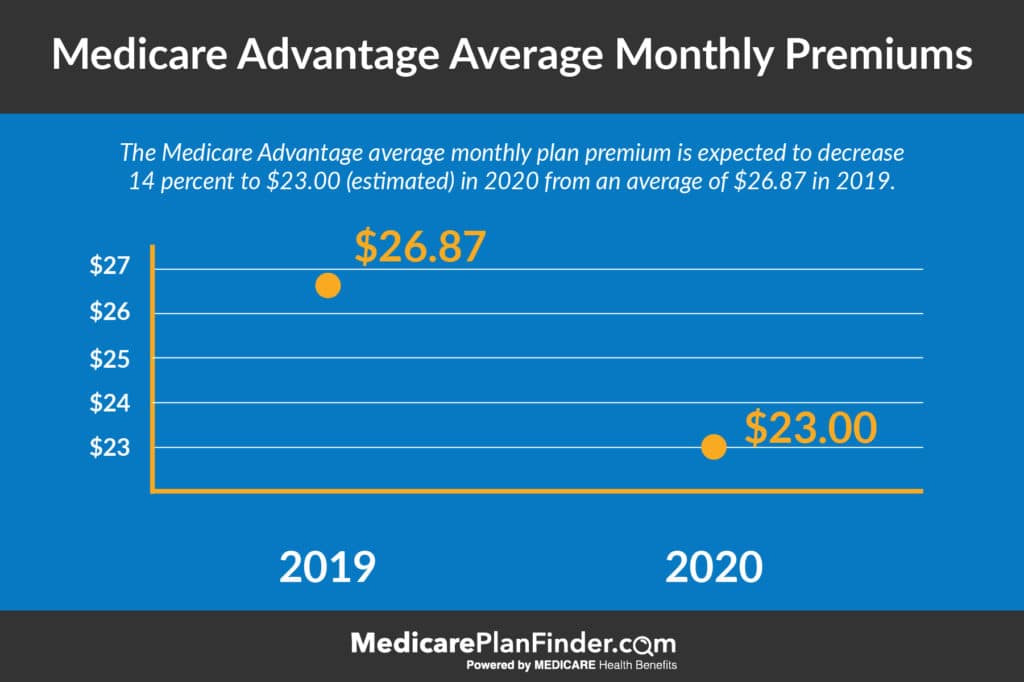

In 2020, Medicare Advantage premiums have decreased on average.

Medicare Advantage Premiums 2020

What does this mean for you? If your premium went up and you need a better option, the time is now! The annual enrollment period is October 15 through December 7. During this time you can switch or enroll in the best plan that fits your needs and budget. Our licensed agents can answer any questions you may have. If you’re interested in scheduling a no-cost, no-obligation appointment, fill out this form or call us at 844-431-1832.

This post was originally published on November 1, 2018, and was last updated on November 5, 2019.

Medicare and SSI (Supplemental Security Income)

There’s SSI, SSDI, Social Security retirement, Medicare and Medicaid…so many government programs. It can be hard to keep track! Sometimes, qualifying for one government program can indicate eligibility for another. Do you know what you’re eligible for?

Today we’re going to dive into SSI, the Social Security Administration’s Supplemental Security Income program, and how it relates to other benefits.

What is Supplemental Security Income (SSI)?

SSI is a government program that is funded by “general tax revenues” as opposed to Social Security taxes. The program provides cash assistance for the purpose of paying for basic needs like food, clothing, and shelter. SSI is only for those who have little or no income/resources and are aged (over 65), blind, or disabled.

SSI Benefits

If you qualify for SSI, you’ll receive a monthly cash benefit. This benefit is determined by the FBR, or Federal Benefit Rate. The 2019 FBR is $771 for single people and $1,157 for married couples. This amount is subject to change each year.

Some states also add money to this based on where you live. Arizona, Arkansas, Georgia, Mississippi, Oregon, Tennessee, Texas, and West Virginia do NOT add money to the SSI benefit.

Can I Get Medicare if I Have SSI?

Not necessarily. It may be possible to qualify for both programs. You can qualify for Medicare if you:

If any of those things apply to you and you are ALSO eligible for SSI, then you may be able to have both programs.

Those who do have Medicare and SSI will be automatically eligible for “Extra Help,” also called LIS or Low-income Subsidies. The Extra Help program provides savings on Medicare prescription drug coverage.

Click here to read more about Medicare Extra Help.

Maybe. There are 32 U.S. states (and D.C.) that will automatically qualify you for Medicaid if you have SSI. However, if you live in Alaska, Connecticut, Hawaii, Idaho, Illinois, Indiana, Kansas, Minnesota, Missouri, Nebraska, New Hampshire, Nevada, North Dakota, Ohio, Oklahoma, Oregon, Utah, Virginia, or the Northern Mariana Islands, you will have to apply for SSI and Medicaid separately, and one does not automatically qualify you for the other.

What is the Difference Between SSI and SSDI?

SSI and SSDI are very similar programs, and their names are similar, too, so it’s easy to get confused! The main difference between the two is that SSI is need-based and does not take work history into account, while SSDI candidates have earned “work credits” by working for a certain number of years and contributing to Social Security taxes.

Additionally, people with SSI are usually able to receive Medicaid and food stamps, as well. On the other hand, people with SSDI automatically qualify for Medicare after two years in the program.

“Blind” is defined as “central visual acuity for distance of 20/200 or less in your better eye with use of a correcting lens” or “visual field limitation in your better eye…”

Disabled means that you have a physical or mental impairment which offers “severe functional limitations,” may result in death, and has lasted for at least one year.

Living with limited income and resources

2019 resources cannot exceed $2,000 for a child or individual adult and $3,000 for an adult couple.

Income refers to money earned from work, benefit programs, and free food or shelter.

Resources refer to cash, bank accounts, stocks, bonds, land, cars, personal property, life insurance, and other valuable goods.

*If you give away or sell your resources in order to qualify for SSI, you may become ineligible for SSI for up to 36 months.

A U.S. citizen, national, or qualified alien

A legal resident of a state, D.C., or the Northern Mariana Islands

Not absent from the U.S. for 30 or more consecutive days

Exceptions may be made for students studying abroad and for children of military parents who are stationed overseas.

Not confined to a hospital, prison, or other institution at the government’s expense

Also applying for other cash benefits and programs

Social Security work incentives give disabled and blind SSI recipients an opportunity to go back to work without losing their benefits.

First, there is an “earned income exclusion.” The SSA does not count the first $65 plus half of the amount over $65 when determining SSI eligibility. What this basically means is that your SSI benefit will only be reduced by $1 for every $2 you earn after the first $65.

For example, let’s say you work and earn $85. The first $65 doesn’t count, so the SSA is looking at your extra $20. Of that $20, they’re only going to count half. That means you’re only being “penalized” for $10 of the $85 you made. That penalty means that your benefit will be reduced by $10. You still get to keep the rest of your benefit, and you’ve basically made an extra $75.

Additional incentives:

Students under 22 may receive exclusions for up to $1,870/month (but not exceeding $7,550 in a calendar year)

Disabled and blind workers may receive exclusions for out-of-pocket expenses related to being able to work with your disability, such as car modifications or special software applications.

PASS (Plan to achieve self-support):

Blind or disabled persons can set aside income or resources towards reaching an employment goal

Kids living with parents may exclude some of their parents’ income/resources

The “Ticket to Work” and Work Incentive Improvement Act of 1999 was passed to help people between the ages of 18 and 64 with Social Security benefits return to work or find higher-paying jobs. The “ticket” program provides free employment services to eligible beneficiaries. The service can help you design a career plan, achieve milestones, and find jobs.

How to Apply for SSI

Even if you are not sure whether or not you are eligible, it may be a good idea to apply for SSI as soon as possible so that you don’t miss out on valuable benefits. There is no charge to complete the SSI application.

Call Social Security at 1-800-772-1213 (TTY 1-800-325-0778) and make an appointment

Visit your local Social Security office (expect a wait if you don’t have an appointment)

If you are applying in person, be sure to bring financial and medical documentation with you. You may need proof of age, citizenship status, medical history/disability, income, and resources.

If you or someone you know needs help with their application, you must have an “Appointment of Representative” form (Form SSA-1696).

If you or someone you know does not speak English well, you may not need a representative. Social Security can provide a free interpreter (or you can use a bilingual friend or family member).

If you or someone you know is deaf or hard of hearing, you can bring an ASL interpreter or use a Social Security Administration interpreter at no cost.

How to Use Medicare Easy Pay

In this digital age, it’s now easier than ever to pay your Medicare bills. There’s no reason to forget to send your checks out or to have to go to the post office to buy stamps anymore. Paying your bills can be as easy as clicking a button!

We’re available to answer all your burning questions about who has to pay what for Medicare, how to pay your Medicare bills, and more.

Medicare Easy Pay

Do I Have to Pay for Medicare?

We get this question a lot, and we understand why you may be confused or upset. If you were employed for any extended period of time in your life, you’re probably thinking, “I already paid for Medicare through taxes!” It’s true that most people paid Medicare taxes during their working careers, but there are still some costs involved in Medicare for most people.

Those Medicare taxes that you paid all those years certainly helped fund the Medicare program, but it’s not enough. Healthcare is expensive!

Medicare parts A and B are different. If you worked for at least 39 quarters, you may not have to pay a premium for Part A at all. However, anyone who does not qualify for financial assistance will owe a premium for Part B. The Part B premium can change based on income, but the standard in 2020 is $144.60/month.

If you worked over 39 quarters (about ten years), your Part A premium will be $0

If you worked 30-39 quarters, your Part A premium will be $252 in 2020

IF you worked for less than 30 quarters, your Part A premium will be $458 in 2020.

2020 Medicare Part B Premiums

Medicare Premiums Deducted From Social Security Payments

If you have low income and receive Social Security assistance, you may receive premium-free Medicare.

Depending on your income, some people with Social Security benefits may still have to pay for Medicare. However, you can have your Medicare payments automatically deducted from your Social Security benefits.

You will receive a bill in the mail for your Medicare payments, unless one of the following applies to you:

If you receive Social Security benefits, your payments may be automatically deducted from your benefits.

If you receive Railroad Retirement benefits, your payments may be automatically deducted from your benefits.

If you retire from civil services, your payments may be automatically deducted from your annuities

Once you receive your bill, there are a few ways you can pay it. You can pay directly through your bank (set this up through your bank), you can send in a check or money order, you can pay by debit or credit card by filling in the card information on your bill slip and mailing it back in, or you can sign up for Medicare Easy Pay, a free service which will automatically deduct the premium from your bank account.

Keep in mind that aside from your premiums, you may still have to pay copayments when you visit a doctor or other provider.

If your payments are automatically deducted from your benefits or if you’re signed up for Easy Pay, you will receive a statement in the mail. The statement and will say “This is not a bill,” somewhere on it. That is just a statement telling you what was taken from your account, and you will not have to send in money. Don’t let this confuse you, you don’t want to pay twice!

How to Get More Money From Social Security Disability

Some Medicare Advantage carriers actually offer a program that can put more money back in your social security check. Some plans will give you a discount on your Medicare Part B (the part that pays for your doctor visits). You’ll see this discount reflected in your Social Security benefits since less money will be taken out for Medicare.

What Is Medicare Easy Pay?

Medicare Easy Pay

Medicare Easy Pay automatically deducts your Medicare premium from a designated checking or savings account. You’ll still get a “Medicare Premium Bill” in the mail, but it will say, “This is not a bill.” It will serve as a statement letting you know that your premium has automatically been deducted from your bank account.

If you prefer to not have your Medicare premiums automatically deducted, there are a few other ways you can pay:

You can sign onto MyMedicare.gov and pay your premiums online with your credit card or debit card.

If you receive Social Security benefits, you can have your Medicare premiums deducted from your benefits.

If you prefer to pay by check or credit card, you can return your Medicare bill with a check or credit card number by mail.

Using Medicare Easy Pay will save you time and prevent you from accidentally forgetting to pay your premiums.

How to Set up Medicare Easy Pay

Enrolling in Medicare Easy Pay and paying Medicare online is easy! All you need to do is fill out this Medicare Easy Pay form and submit it to the following address.

It can take up to 6-8 weeks to process, so make sure you continue to pay your bill until your Medicare Easy Pay becomes active.

Once it’s active, you’ll notice that your premium is deducted from your bank account on the 20th of the month. You’ll see it on your bank statement as “Automated Clearing House (ACH).”

Mail your Medicare Easy Pay form to:

Medicare Premium Collection Center PO Box 979098 St. Louis, MO 63197-9000

How to Cancel Medicare Easy Pay

If you need to change your Medicare Easy Pay bank account, address, or any other information, resubmit your Medicare Easy Pay form but select the “change” option.

If you no longer want to use Medicare Easy Pay for any reason, resubmit your Medicare Easy Pay form but select the “stop” option. Complete all the boxes in the form so that Medicare can locate your information to make changes.

Medicare Advantage Payment

If you have a Medicare Advantage plan, your plan is hosted by a private carrier. That means that instead of paying Medicare directly, you’ll be paying your carrier.

Each carrier hosts their billing differently. You’ll likely need to either send in a check or pay online. Check with your plan details or your carrier website to learn how to make a Medicare Advantage payment. A Medicare Plan Finder licensed agent may be able to help you figure it out.

Find Medicare Advantage Plans | Medicare Plan Finder

Part D Payment

Your Part D (prescription drug plan payment) will differ based on the type of prescription drug plan coverage you have.

If you have an MAPD (Medicare Advantage Prescription Drug Plan), your Part D/prescription drug coverage is included in your Medicare Advantage plan and you will most likely only have premium to pay each month. I

f your prescription drug plan is not included in your Medicare Advantage plan, you will have to look into your individual Part D plan to find a billing address to mail checks to or a website to enroll in digital payments.

Medicare Advantage is a way to wrap up your hospital coverage, doctor coverage, prescription drug coverage, and extra coverage (dental, vision, hearing) into one plan with one premium.

Medicare Supplement plans are a way to get coverage for your deductibles, coinsurance, and copayments.

If you didn’t do this in your Initial Enrollment Period (IEP), you have the chance to every year during AEP (the annual enrollment period), from October 15 through December 7.

What Happens If I Don’t Pay My Premiums on Time?

If you don’t pay your Part B premiums on time, you could lose coverage. It won’t happen immediately, however.

You have a 90-day grace period after the due date. Once the grace period passes, Medicare will send you a letter letting you know that you have 30 days to pay the bill or you will lose coverage. That makes a total of four months to pay your bill before Medicare will stop paying for covered services.

Private insurance plans (Medigap, Part D, or Medicare Advantage) may treat late payments differently. Check with your plan carrier if you have questions about the policies.

Still Need Help?

If you need help to pay Medicare online, one of our agents may be able to help you set it up! Give us a call and we’ll send a licensed agent your way to help you figure it out and make sure you’re in the best plan for your health and financial needs. Call us at844-431-1832 or contact us here today.

Contact Us | Medicare Plan Finder

This post was originally published on October 19, 2017, by Anastasia Iliou. The latest update was completed on October 8, 2019, by Troy Frink.

2020 Medicare Changes & Trump’s Executive Order

Every year, CMS (Centers for Medicare and Medicaid Services) reserves the right to make changes to the Medicare program. Rules and regulations around enrollment periods, penalty fees, marketing, and plan benefits are released in late summer and early fall for the following year. Costs can rise, and brand new plans can enter or leave the market.

Medicare is confusing as it is. When you add these yearly changes into the mix, choosing the right plan can be stressful. Our goal is to make all of this less stressful for you. Our website is a great educational tool, and our licensed agents can provide free assistance!

Here are the changes you need to know about for Medicare in 2020.

On October 3, 2019, President Donald Trump signed an executive order “protecting” the Medicare program. What does this mean?

Alex Azar, Health and Human Services (HHS) Secretary, said that Trump told HHS to take “specific, significant steps” towards improving Medicare funding and improving healthcare for American seniors. These steps include lowering Medicare Advantage costs, allowing savings accounts, and improving access to new medical technology. It also leaves room for more plan options, more telehealth, more wellness benefits, and a stronger financial model.

In his post-executive order speech given in Florida yesterday morning, Trump stated, “In my campaign for president, I made you a sacred pledge that I would strengthen, protect and defend Medicare for all of our senior citizens.” That was the intent of the executive order.

Is Medicare Going Up in 2020?

New 2020 Medicare premiums and costs for 2020 have not been released yet. The new numbers are usually released in early fall of the year prior, so we are expecting to see them over the coming months. The Wall Street Journal reported in April that 2020 Medicare Part B premiums are likely to increase by $8.80/month to a total of $144.30, but this is not final.

We will continue to update this post with new 2020 costs as they are released. Thank you for your patience!

2020 Medigap Changes

Just like the Original Medicare program, private plans like Medicare Advantage, Medicare Supplements, and standalone benefit plans can change every year.

Plan availability may not be the same for everyone. Medigap eligibility, in particular, can depend on your age when you enroll, preexisting conditions, and where you live. Plans can be different not only in every state but also in every county and zip code.

Use our plan finder tool to find out what Medigap plans are available in your area for 2020.

Is Medicare Supplement Plan F Going Away in 2020?

Starting in 2020, you will no longer be able to purchase Medigap Plan F or Medigap Plan C. Plan F was one of the most popular plans, and Plan C was fairly similar. The plans are going away because they include coverage for the Part B deductible (only $185 in 2019).

You might here plans C and F referred to as “first-dollar” plans because they virtually eliminate out-of-pocket costs. CMS decided that taking away the Part B deductible coverage was a smart move to discourage people from overusing their primary physician offices and costing the Medicare program a lot of money for unnecessary doctor’s visits.

If you already have Medigap Plan F or Medigap Plan C, you can be grandfathered in. That means that you will not lose your coverage in 2020. However, if you leave your Plan F or Plan C in favor of a different Medigap plan, you won’t be able to re-enroll in F or C.

Will Plan F Premiums Rise After 2020?

As Plan F sees less and less enrollees, Plan F premiums will likely begin to rise. We can’t say this for sure and we will certainly have to wait and see what happens, but generally less enrollees means higher costs for the companies, resulting in higher premiums.

Will There be a High Deductible Plan G in 2020?

Since people will not be able to purchase Plan F or Plan C in 2020, CMS did want there to be another option with similar benefits. Plan G was already that option, given that the only difference is that Plan G does not cover the Part B deductible.

The other difference is that previously, Plan G was not offered with a high-deductible. If you typically have low medical costs, you may prefer a high-deductible option. Having a high deductible often means that your premiums will be lower. This way, you don’t have to pay as much until you start experiencing health concerns. The high deductible Plan G option can replace the high deductible F option.

Donut Hole Closing in 2020

In addition to all of these plan changes, the infamous “Donut Hole” will be effectively closing in 2020. The Bipartisan Budget Act of 2019 closed the coverage gap for brand-name drugs in 2019, and the generic drug coverage gap will be eliminated in 2020. This basically means that, if you have a Medicare Part D plan, you will only be responsible for 25% of your covered prescription drug costs instead of 44%.

2020 Medicare Advantage Changes

There may be more Medicare Advantage plan changes to come in 2020, but we wanted to make sure you had heard about the changes from last year.

On October 12, 2018, the Centers for Medicare and Medicaid (CMS) announced the 2019 Original Medicare premium and deductible increase, but what about Medicare Advantage (MA) plans? Unlike Medicare Part A and B, beneficiaries enrolled in MA plans may see a decrease in their premiums in 2019 and 2020 compared to 2018.

2020Medicare Advantage Cost Changes and 2020 Premiums

In September of 2018, CMS announced that on average, Medicare Advantage premiums will decrease by 6%. This is great for beneficiaries interested in affordable vision, dental, and hearing coverage or even fitness classes like SilverSneakers®!

CMS estimated that 83% of beneficiaries would have equal or lower premiums for 2019 and 46% will have a $0 premium! Premiums for MA plans have steadily declined, and this is the lowest premium we’ve seen in three years. This is a perfect example of a private and public collaboration that allows beneficiaries to drive and define the value. The 2019 Medicare Advantage changes are a quick glance of what you can expect to continue in the future.

2020 cost changes for Part A and B premiums and deductibles have not officially been released yet but are not expected to increase by very much. We will continue to monitor this information and will update as soon as the cost changes are officially announced.

Early in 2018, CMS (Centers for Medicare and Medicaid Services) released new rules that allow Medicare Advantage plans to offer a few benefits, like “daily maintenance,” transportation, telehealth, and durable medical equipment.

Some plans in 2020* are really going above and beyond, offering benefits like new air conditioners and pest control!

*These benefits are not included in all MA plans. Your agent may be able to help you find a plan that includes more.

Daily Maintenance

The addition of the “daily maintenance” benefit means that Medicare Advantage plans are now able to offer at-home care items, such as wheelchair ramps and other home modifications. Tied in with that benefit are other forms of durable medical equipment, like hospital beds, oxygen equipment, blood sugar monitors, etc, as well as “non-skilled” services. Non-skilled refers to items that do not require a licensed doctor or nurse, such as aides who can assist with bathing and dressing or homemakers who can help with cleaning and cooking.

Non-Emergency Medical Transportation Coverage

CMS has also added the ability for MA plans to provide non-emergency transportation coverage, a service that several Medicaid plans provide. This benefit (if your plan covers it) will allow you to receive free or low-cost rides to medical appointments and pharmacies. In most cases, you can only qualify for this benefit if you do not have another adequate means of transportation. The appointment that you are requesting a ride to must be for a Medicare-covered service.

Telemedicine and Telehealth

MA plans can now provide coverage for telehealth. That means you can have live video interaction with your doctor through digital clinics like HealthTap, Teladoc, and MDLive. Telehealth can also include health alerts delivered to your phone, health education apps, electronic medical data transfers, mail-order prescriptions, digital appointment scheduling and exam reminders, and more.

New Enrollment Period (OEP)

Before 2019, most people were only able to switch into new Medicare Advantage plans during the Annual Enrollment Period in the fall. Now, if you already have a Medicare Advantage plan, you may be eligible to make a change during OEP. OEP, or the Open Enrollment Period, takes place from January 1 through March 31. During this time, you can switch from one Medicare Advantage plan to another or drop your Medicare Advantage plan in favor of Original Medicare (Part A and Part B only).

Future of Medicare Advantage Plans

According to the Henry J Kaiser Family Foundation, enrollment has tripled to 19 million beneficiaries since 2003 and continues to grow each year. CMS estimates that MA enrollment will hit an all-time high of 22.6 million beneficiaries in 2019 (an 11.5% increase)!

As enrollment continues to increase, plan selection and variety increase too, with approximately 600 new plans offered in 2019! 99% of seniors and Medicare-eligibles have access to a MA plan – and 91% can choose from 10 or more plan options. Beneficiaries will not only see more plans to choose from, but also new supplemental Medicare benefits!

Enroll in a Medicare Advantage Plan in 2020

Are you interested in getting coverage beyond Original Medicare? Along with the new benefits, many Medicare Advantage plans offer dental, hearing, and vision coverage.

Our agents at Medicare Plan Finder can contract with nearly every carrier in your state! This means that you can enroll in the MA plan that best fits your needs and budget.

The Annual Enrollment Period runs from October 15 through December 7. Start looking over your plan benefits now so that you’re ready to enroll before December 7!

Ready to learn more? Call us at 844-431-1832 or fill out this form to arrange a no-cost, no-obligation appointment with an agent in your area.

*This post was originally posted on November 8, 2018, and was last updated on October 4, 2019.

Does Medicare Cover Mammograms and Other Women’s Health Services?

Medicare is not just for sick days! Did you know you could use your Medicare coverage for annual wellness exams, like check-ins with your gynecologist or OB/GYN? This post will tell you about all the ways women can use Medicare preventative benefits to stay healthy.

Does Medicare Cover Gynecology?

As long as you have an OB/GYN that accepts Medicare, your Medicare Part B gives you access to preventative women’s health care.

There are no exceptions – every woman enrolled in Medicare Part B has gynecology coverage. You should be taking advantage of these benefits! Remember that your Medicare is designed not just to help you in a time of illness or injury, but also to prevent those illnesses or injuries from occurring.

If you are enrolled in Medicare, your annual mammogram screening is covered 100% so long as your provider accepts Medicare. Diagnostic mammograms are covered at 80%, which leaves you responsible for the remaining 20% ($60 on average). Diagnostic mammograms are used if you have suspicious or concerning results from your annual mammogram.

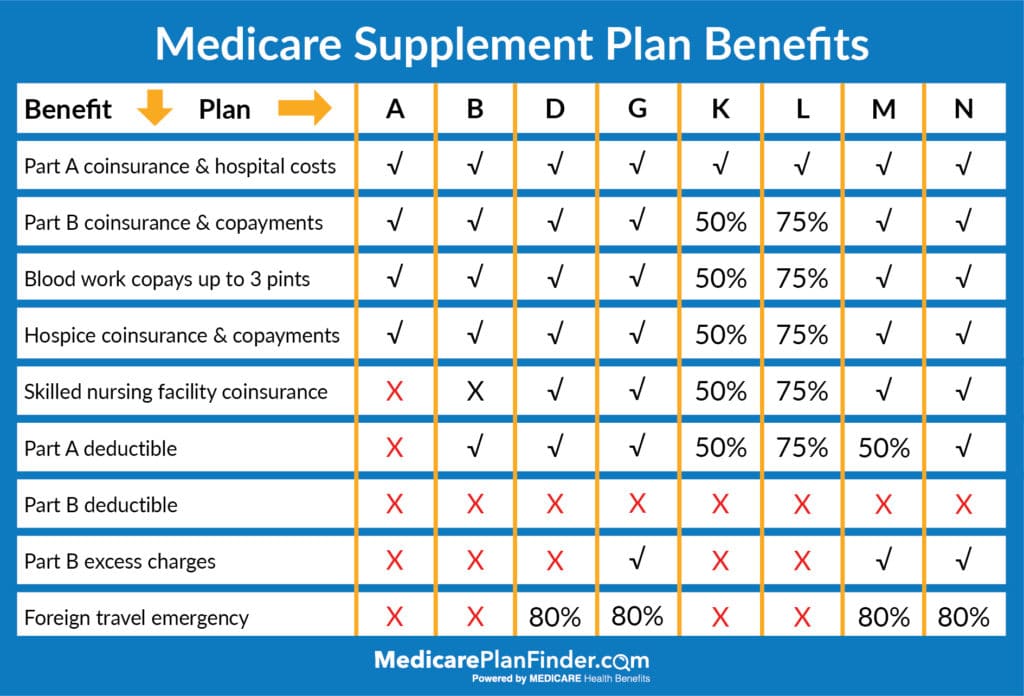

A Medicare Supplement plan can help cover the additional costs of diagnostic mammograms and other services. Depending on which type of Medicare Supplement plan you purchase, benefits can include:

Part A coinsurance and hospital costs

Part B coinsurance and copayments

Blood work copays (up to three pints)

Hospice coinsurance and copayments

Skilled nursing facility coinsurance

Part A deductible

Part B deductible

Part B excess charges

Foreign emergency travel

These financial benefits can help with any of your health-related costs, not just mammograms. If you would rather pay a small monthly premium to help protect yourself from unforeseen health expenses, a Medicare Supplement plan may be right for you.

Medicare Advantage plans are required to cover, at a minimum, the same as Original Medicare. This means that your annual mammogram is still cost-free to you and diagnostic mammograms are covered at 80%.

However, Medicare Advantage plans can offer several additional benefits beyond Original Medicare that can help you maintain a healthy and proactive lifestyle. These benefits include vision, hearing, and dental coverage, monthly OTC pharmacy allowance, non-emergency transportation, group fitness classes like SilverSneakers®, and so much more! These plans have continued to grow in popularity each year, and more than 20.4 million beneficiaries are taking advantage of these benefits.

Medicare Mammogram Eligibility

To be eligible for preventive mammogram screening coverage, you need to be a woman enrolled in Original Medicare (Part A and B) or a Medicare Advantage plan. Men are not eligible for annual Medicare-covered mammograms. While it is possible for men to get breast cancer, it is very rare. That’s why most men are not eligible for preventive mammograms. However, men who are at high-risk can have diagnostic mammograms covered at 80%, just like women.

How Often Does Medicare Pay for Mammograms?

We know Medicare covers Mammograms, but how many? Medicare will cover one preventive mammogram per year. If your results are concerning or show you have a high risk of developing cancer, Medicare will continue to pay 80% for each diagnostic mammogram needed. There is no limit on how many diagnostic mammograms Medicare will cover.

Does Medicare Cover Gynecological Exams?

Gynecological exams and services covered by Medicare include:

Gynecological exams

Breast exams

Pap smears

Gynecological cancer screenings

Testing for HPV, HIV, and other sexually transmitted diseases

Treatment for pelvic and vaginal infections

Treatment for abnormal vaginal bleeding

Contraception counseling

Menstrual pain and irregularities

Menopausal management

Does Medicare Cover Pelvic Exams, Pap Smears, and Breast Exams?

Your Medicare gives you access to pelvic exams, pap smears, and breast exams. These tests check for cervical, vaginal, and breast cancer. Coverage is available for pelvic exams and pap smears once every two years. If you’ve had abnormal results in the past three years, you’ll be covered for yearly tests instead.

You’ll also be covered for clinical breast exams. Breast cancer is the most common cancer for women. Risk increases with age, and you can be cured much more easily if it is caught early on. Take advantage of free preventative care!

Additionally, you can ask your doctor for STI (sexually transmitted infection) screenings and counseling. Counseling is recommended for those who are at a higher risk. Part B covers yearly tests for the most common STIs – chlamydia, gonorrhea, syphilis, and hepatitis B, as well as HIV. STI tests are completely free with a doctor who accepts Medicare assignment.

Gynecologists Covered by Medicare

Are you ready to see a gynecologist? The best way to confirm that your gynecologist accepts Medicare as insurance is to ask when you set your first appointment, but there are tools you can use to find out who accepts Medicare before you start calling around.

Remember that if you have a Medicare Advantage or Medicare Supplement plan, you may want to check to make sure that the doctor accepts your plan. If you only have Original Medicare (parts A and B), you can use the Medicare.gov physician finder tool to look for gynecologists in your area who accept Medicare.

To start, enter your location and the phrase “gynecologist” or “ob/gyn” in the search bar. The tool will not let you enter the type of doctor you’re looking for until you’ve entered your location.

Medicare.Gov Physician Finder Tool

After clicking the green “search” button, you’ll see a list of doctors in your area who accept Medicare for gynecology. The tool will tell you where they are located, how far they are from the location you entered, etc.

Medicare.Gov Physician Finder Tool

Get Women’s Health Coverage

Fortunately, Original Medicare covers most women’s health needs. However, Medicare Advantage and Medicare Supplements can supplement your Original Medicare coverage. If you are looking for additional health benefits through Medicare Advantage or financial benefits through Medicare Supplements, our licensed agents can help. They are contracted with all the major carriers so they can enroll you in a plan without bias. With Medicare Plan Finder, there’s never an obligation to enroll and appointments are always cost-free to you. Fill out this form or give us a call at 844-431-1832.

This blog was originally published on July 20, 2017 and last updated on October 3, 2019 by Anastasia Iliou.

Does Medicare Cover Music Therapy?

Have you considered trying out music therapy? Music therapy is a form of psychological healing. Even ancient civilizations used music as a form of healing!

It’s possible because different aspects of music, like the pitch and rhythm, affect different parts of your brain. It can help those with anything from depression to Alzheimer’s and everything in between.

If you have Medicare, you may wonder, “Does Medicare cover music therapy?”

Medicare Coverage for Music Therapy

Does Medicare Cover Music Therapy? | Medicare Plan Finder

Medicare covers music therapy under certain conditions. For example, Medicare Part B (medical insurance) may cover music therapy as part of a mental health treatment plan.

Music therapy by a licensed music therapist is considered a reimbursable service with Medicare under Partial Hospitalization Programs (PHP). This means that as long as your music therapy services are prescribed by a doctor, are documented on a treatment plan, and are reasonably necessary, Medicare may cover the service. You may be responsible for coinsurance or deductibles.

Medicare Advantage Alternative Therapy Coverage

Because music therapy is an alternative form of medicine, the most basic plans may not cover it.

Some private insurance policies called Medicare Advantage plans can cover music therapy along with other alternative therapies such as acupuncture and chiropractic care.

We can help you find out if you can get coverage for music therapy. Give us a call at (833)-567-3163 or contact us here.

Find Medicare Plans | Medicare Plan Finder

How Does Music Therapy Work?

Licensed music therapists are trained in both music and psychology. They know which parts of the brain need stimulation for healing and know how to encourage it. It works differently for everyone.

When it comes to memory loss, a music therapist may encourage a patient to listen to songs from their past. Music releases certain hormones that can induce memory and remind us of other times that we’ve heard the same music. It can help patients recover memories they may have thought were lost.

When it comes to pain relief, a music therapist might encourage a patient to listen to calm, soothing sounds. When it comes to depression and mental illness, a music therapist might encourage a patient to learn to play an instrument or to express themselves by writing music.

What Does Music Therapy Help?

You may be surprised by the number of conditions that music therapy can help with! These are just a few examples:

Heart Health: Music therapy can improve blood pressure levels by reducing stress hormones. Your body responds to the rate of the music.

Memory Loss: Music therapists often visit nursing homes and hospitals to care for Alzheimer’s patients or others who are suffering from memory loss. Music can improve cognitive functions.

Fetal Development: Research has proven that babies who listen to music while in the womb are born more responsive. Those babies typically develop faster, sleep better, and bond better with their parents.

Depression: Music can induce feelings of happiness by releasing happy hormones like dopamine. It also allows depressed patients to focus their energy.

Mental Disabilities: Individuals with autism are commonly music therapy patients. It’s a great way for them to practice communication and creativity.

Pain Management: Music can increase oxytocin levels (love hormone), which is very similar to what pain medications do but without the addictive qualities. Music therapy provides a great alternative to over-medication.

How to Find a Music Therapist

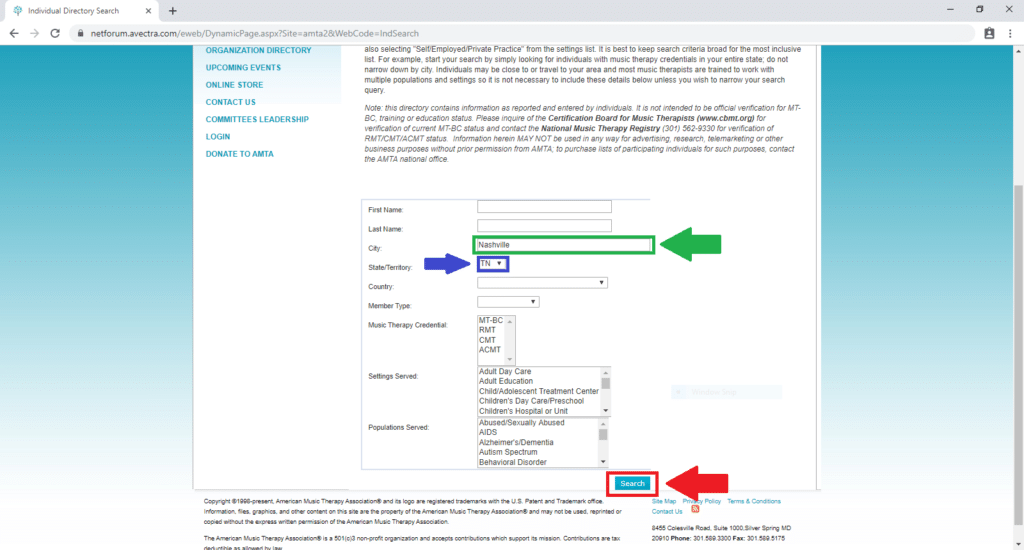

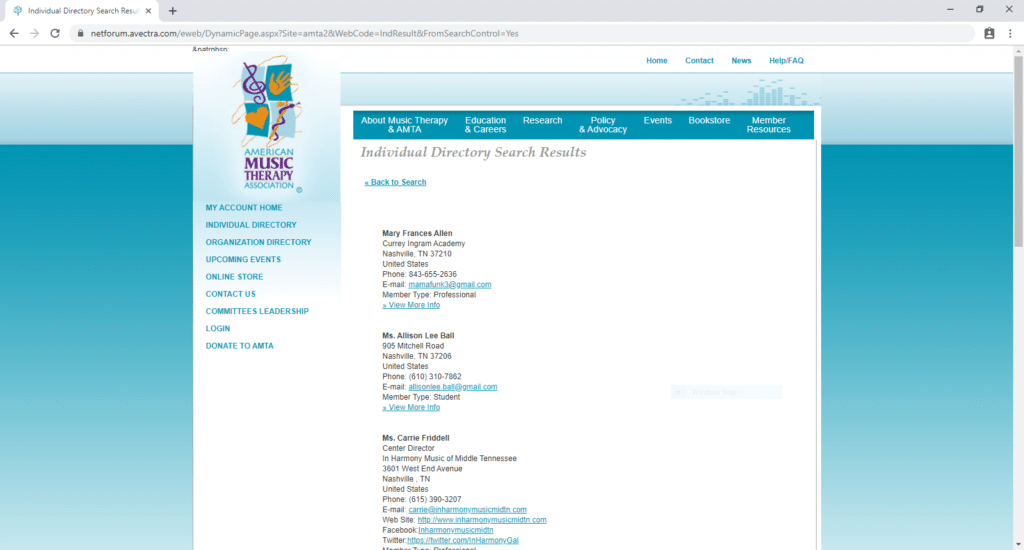

If you’re looking for a music therapist in your area, click here. You’ll reach the search tool for the American Music Therapy Association. From there, enter your city in the bar beside the green arrow. Then select your state from the drop-down menu beside the blue arrow. We chose Nashville, Tennessee because that’s the location of our home office. Once you’ve completed that, click “Search” beside the red arrow.

How to Find a Music Therapist Step 1 | Medicare Plan Finder

Then you’ll reach a list of music therapists in your area with contact info. You may need to call more than one to find the right fit.

How to Find a Music Therapist Step 2 | Medicare Plan Finder

Find Coverage for Music Therapy Today

A licensed agent with Medicare Plan Finder may be able to help you find an insurance plan that fits your needs.

Depending on what plans are available in your area, you may be able to find one that covers music therapy along with supplemental benefits such as vision, hearing, dental, and fitness classes! To set up a no-cost, no-obligation appointment, call us at (833)-567-3163 or contact us here today.

Contact Us | Medicare Plan Finder

This post was originally published on February 15, 2018, and updated on October 2, 2019.

BREAKING NEWS: Tennessee SilverSneakers® Program Splits from YMCA

SilverSneakers® announced on Tuesday, September 17, that the Tennessee State Alliance of YMCAs decided to leave the SilverSneakers® network effective January 1, 2020, citing financial disagreement.

The alliance apologized, stating, “Seniors are a vital part of our membership, and we apologize for any inconvenience this decision may cause. Tennessee Ys are committed to continuing to serve seniors in our community.”

SilverSneakers® is a Medicare fitness program that allows eligible Medicare beneficiaries access to gyms, fitness centers, and classes. Many of these often take place within YMCAs, offering not only physical fitness benefits but also a social atmosphere.

Eligibility for the program is simple – anyone who is age 65 or older and has a private Medicare plan that includes the SilverSneakers® benefit can join.

Watch this brief video to learn more about Medicare fitness programs:

The news that SilverSneakers® may not cooperate with Tennessee YMCAs anymore may be detrimental to seniors who made use of that benefit. If you’re one of those people, what should you do next?

What to do if You’re Losing Your YMCA SilverSneakers® Benefit

If you have SilverSneakers® but are no longer going to be able to visit a YMCA with your membership, all hope is not lost! There are a few steps you can take:

Pay for your own senior YMCA membership ($59/month in Middle TN. Prices range based on location)

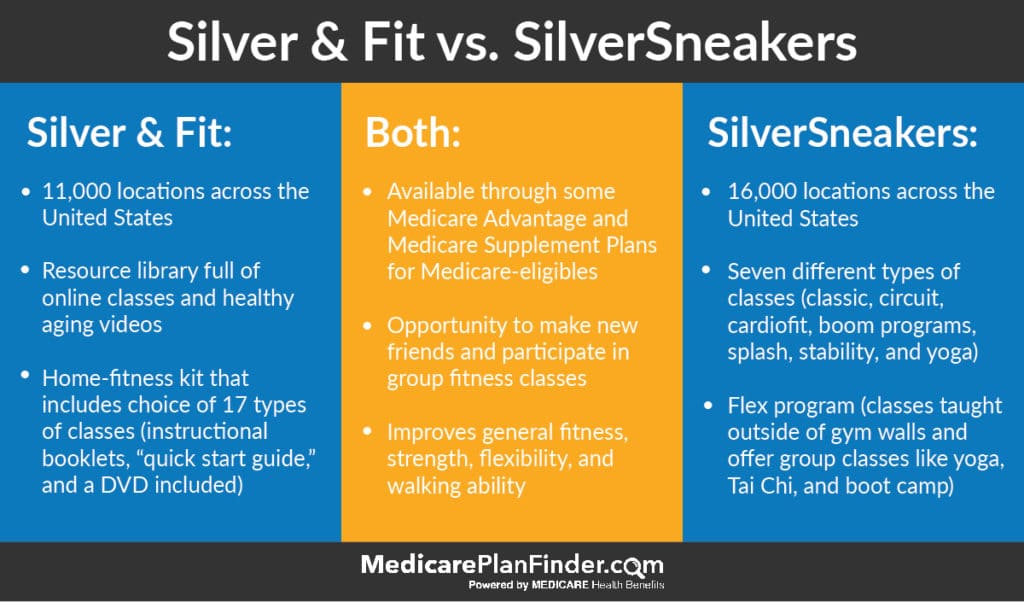

Find a plan that has Silver & Fit® instead (another Medicare fitness program that is very similar to SilverSneakers® but still works with YMCAs as of September 2019)

Silver & Fit vs. SilverSneakers

Other Gyms You can Visit with SilverSneakers ®

Tivity Healthcare, the company that operates the SilverSneakers® program, wants to make it clear that there are still over 350 facilities in the state of Tennessee that SilverSneakers® members can use. Planet Fitness, Gold’s Gym, Anytime Fitness, and Workout Anytime as well as a variety of community centers are still part of the SilverSneakers® network in Tennessee and may be a great option for you.

Planet Fitness

Planet Fitness locations across the state of Tennessee offer benefits like massages, tanning, and even discounts on travel and Reebok products. Most locations have long hours, and some are open 24-7. Many of them also have free WiFi!

Gold’s Gym

Gold’s gym locations offer group exercise classes, personal training, and more. Group exercise classes include Yoga, Zumba, Mixed Martial Arts, Group Cycle, and High-Intensity Interval Training.

Anytime Fitness

Different Anytime Fitness locations offer different equipment such as treadmills, ellipticals, cycles, stair climbers, rowing machines, weights, kettlebells, etc. They also offer different classes like Zumba, cardio, yoga, and additional services like tanning, private showers, wellness programs, and personal training.

Workout Anytime

Workout Anytime locations have high-quality equipment from Matrix Fitness, which has received rewards for innovation. They also have high-quality polypropylene, antimicrobial flooring that is beautiful, comfortable, and clean.

If you decide that you would rather stick to a YMCA membership and do not want to try out some of the other SilverSneakers® locations options, a licensed agent can help you find a plan that includes Silver & Fit® instead.

Silver & Fit® is similar to SilverSneakers® and includes a digital resource library, home fitness kits, community activities, and several different fitness classes at various fitness centers in Tennessee.

Silver & Fit® locations across major cities in Tennessee are listed below:

To find a plan that includes Silver & Fit®, call 844-431-1832 or send us a message. We’ll connect you with a licensed agent in your area who may be able to help you make the switch.

How Mail Order Prescriptions Can Save You Time and Money

Did you know that you can order your prescriptions online and save money? That’s right – no more rushing to get to the pharmacy on time or having to ask someone to pick up your prescriptions for you. You may even be able to schedule your prescriptions to deliver exactly when you need them with automatic refills!

Pros and Cons of Mail Order Pharmacy

Using a Mail-Order Pharmacy | Medicare Plan Finder

Ordering prescriptions from a mail order pharmacy comes with pros and cons.

Pros

Time Saving: You can save hours by not having to make monthly, weekly, or daily trips to the pharmacy. All you’ll have to do is click a button and wait to receive your medications – no standing in line, no rushing to get to the pharmacy.

Cost Saving: You can save money on gas and help minimize wear and tear on your car. Using a mail order pharmacy eliminates the need to travel.

Automatic Refills: Most mail-order offer an automatic refill option. This is great for people who forget to have their prescriptions refilled or pick them up. Some pharmacies will even call your doctor to renew your prescriptions!

Cons

Waiting for Prescriptions: Even though you can order your prescriptions with the click of a button, you still have to wait for your prescriptions. That can be a drawback if you need your prescription immediately.

Prescriptions Can Be Lost: It’s rare, but sometimes prescriptions can be lost in the mail. However, most mail-order pharmacies will re-ship your medication at no additional cost. If you’re concerned about package theft, it may be in your best interest to pick up prescriptions in person.

Automatic Refills: Having your prescriptions refilled automatically can be both a pro and a con. If you’re someone who usually sets and forgets, you could end up with a lot more pills than you need!

The Delivery Fee

Contrary to popular belief, most mail order prescriptions can be delivered without a shipping fee! If delivery fees are what was holding you back from using an online pharmacy, you can check that off your list. Pharmacies don’t have to charge a shipping fee because mailing your prescriptions can actually save them money.

They don’t have to pay for the time and labor it takes to stock prescriptions in-store and they can ship to you directly from a warehouse. There may be shipping fees associated with medical equipment and supplies, but most prescriptions can ship free.

When Should I Stick to my Local Retail Pharmacy?

There are only a few downsides to mail order prescriptions. Mainly, you will lose out on the face-to-face interaction with your pharmacist. However, you can always call your pharmacist to ask questions or speak to your doctor instead.

Your local retail pharmacy, like a CVS or Walgreens, can delivery your prescriptions to your door as well. If you are comfortable using your local retail pharmacy instead of searching for a new mail order pharmacy, stick to it instead of trying to fix what is not broken.

When Should I Expect to Receive my Prescription?

Some prescriptions may take up to 14 days to arrive at your door, so you may still need to visit your pharmacy in person to get your cold medicine and other immediate needs.

Long-term prescriptions, though, can be automatically mailed when you need them. If you work with your pharmacy to set up auto-refills, you should receive your prescription in the mail well before you need it so that you never run out of your medication.

Top Mail Order Pharmacies

It’s always a good idea to start by checking if your health plan has its own mail order pharmacy. Many carriers do, and they can save you a lot of money that way! For example, Cigna just merged with digital pharmacy Express Scripts. You can also check with your favorite drugstore chain. CVS, Walgreens, and Publix are just three examples of chains that offer prescription delivery services. You can also consider the following:

Blink Health – What’s unique about Blink Health is that you can have your prescriptions delivered to your home, or you can pick them up from a local participating pharmacy. Either way, you can see the prices before you buy and choose the cheapest and easiest option for you.

EnvisionPharmacies – Envision is divided into three parts. Envision Mail is a typical mail order prescription service, EnvisionSpecialty provides patient, caregiver, and provider support, and Envision Compounding is quite different. The compounding sector creates alternative forms of medications and sends them to patients who cannot swallow pills or have unique allergies.

HealthWarehouse.com – Selling both brand name and generic prescriptions for both you and your pets! Over the counter drugs, diabetic supplies, and home medical equipment is also available. Just create an account and ask your doctor to send your prescriptions to HealthWarehouse.

PillPack – Not only does PillPack allow you to order your medications online, but they can also sort your pills by dose for you. For example, if you both Drug A and Drug B at 8 AM every day, and you take Drug C at both 8 AM and 8 PM every day, you’ll receive two packs for each day: one that contains Drug A, Drug B, and Drug C and is labeled “8 AM,” and one that contains Drug C and is labeled “8 PM.” They are dated so that you won’t lose track. PillPack is now owned by Amazon.

How to Find a Safe Online Pharmacy

Any pharmacy your Medicare plan recommends will likely be legitimate. However, there are many fake online pharmacies that will try to scam you. They appear to be legitimate pharmacies but they actually send fake drugs.

To help raise awareness about these fake online pharmacies, the Food and Drug Administration (FDA) launched BeSafeRx. According to the FDA, a legitimate pharmacy will:

Require a valid prescription from your provider

Be licensed by your state board of pharmacy, or equivalent state agency. (To verify a pharmacy’s licensing status, check your state board of pharmacy.)

Have a U.S. state-licensed pharmacist on staff and on call to answer your questions

Be located in the United States, and provide a physical street address, not just a post office box

How to Report Illegal Medicine Sales

If you become aware of unlawful medicine sales, you can report the rogue pharmacy with the FDA. Fill out the form here with as much detail as possible.

How is my Insurance Plan’s Mail Order Pharmacy Different From Other Online Pharmacies?

Excellent question! Not every insurance plan has its own Medicare mail order pharmacy, so it is important to check your coverage and be sure that you have access to mailed prescriptions.

Additionally, some insurance plan mail order pharmacies are limited in what they can offer, while private online pharmacies operate independently and can function just like a brick and mortar drug store.

Compare Prescription Costs

Even if you don’t want to use the internet for ordering prescriptions and having them delivered, you can at least use it to view drug prices. GoodRx is a leader in drug price tracking. All you have to do is type in the name of the prescription drug you need, and GoodRx can tell you what pharmacy has the best price! You can also use GoodRx to print free coupons and save as much as 80% on some drugs!

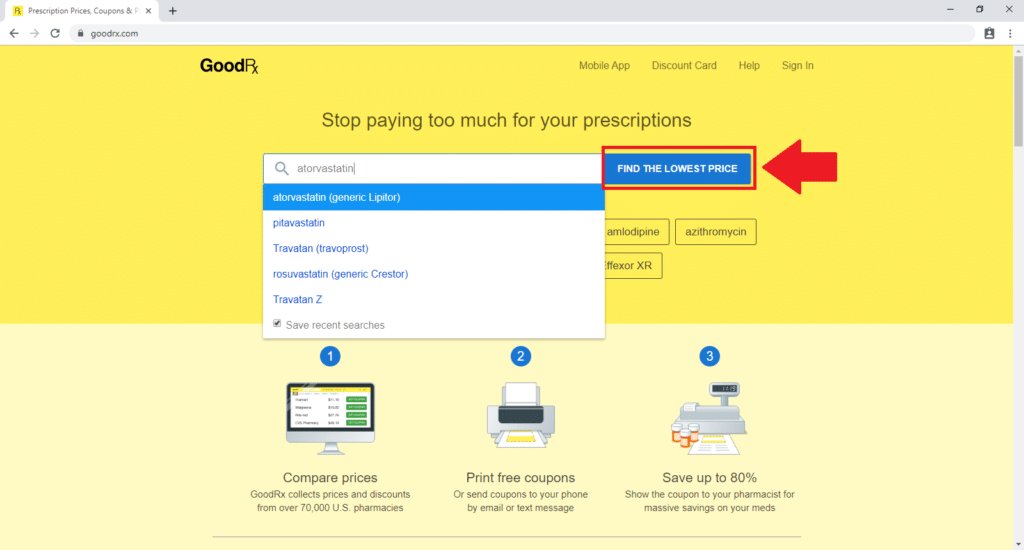

GoodRx Prescription Finder Tool

To use GoodRx’s prescription finder tool, click here. Then type your prescription in the search bar. We’re using atorvastatin (Lipitor) for demonstration purposes, but you can use any medication you want prices for. Then click “Find the Lowest Price” beside the red arrow.

Prescription Finder Step 1 | Medicare Plan Finder

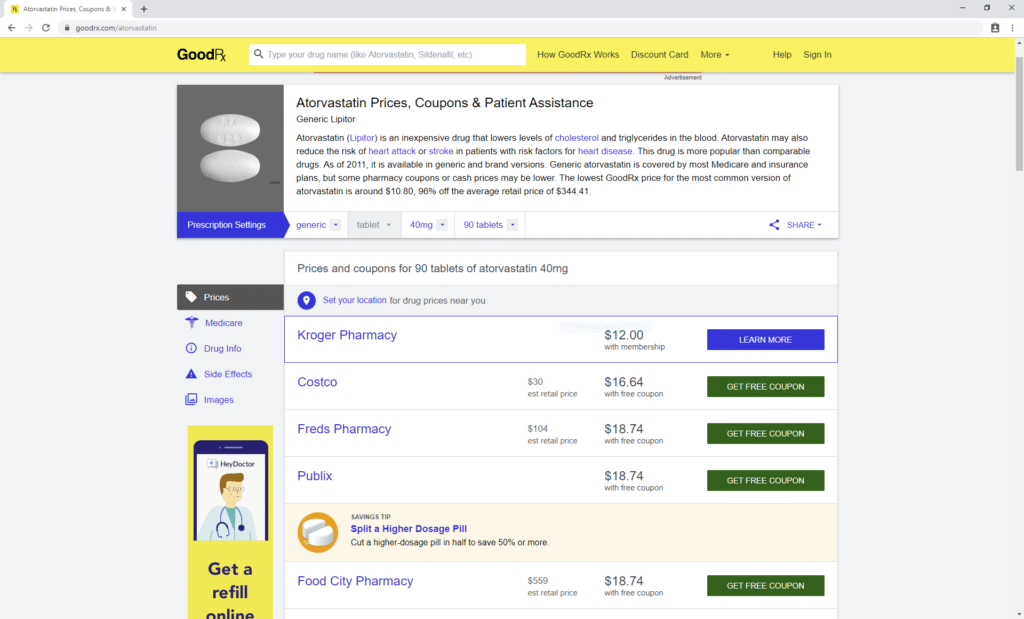

Then you’ll come to the price list with several pharmacy options.

Prescription Finder Step 2 | Medicare Plan Finder

Prescription Savings Coupons

When GoodRx, mail-order prescriptions, and your Medicare coverage aren’t enough, there are prescription drug discount cards! Since these cards are not part of Medicare, you can sign up for a card at any time. Having a prescription drug savings card is sort of like having a coupon book.

There may be times when you don’t need your Rx card because your Medicare coverage gets you even bigger savings, but there are other times when your card can save you a lot of money!

Free Prescription Discount Card

Get Medicare Mail Order Pharmacy Coverage Today

Do you have a Medicare Advantage or a Part D prescription drug plan? Do you know if you qualify for LIS, a prescription drug savings program for Medicare beneficiaries? We can help answer your questions and make sure you are getting the best benefits at the best price, and make sure you are eligible for mail order prescriptions.Set up an appointment at no cost to you by calling us at 844-431-1832 or contact us here.

Contact Us | Medicare Plan Finder

*This post was originally published on February 8, 2018 and last updated on September 23, 2019.

Simply Explained: Ancillary Insurance

Private Medicare plans like Medicare Advantage and Medicare Supplements can cover a lot of benefits, but they generally don’t cover everything. Ancillary insurance products like separate dental plans, heart attack insurance, and life insurance are all important too.

Depending on what Medicare plan(s) you have, ancillary insurance products might be necessary to provide you with the comprehensive coverage and peace of mind you need.

What Are Ancillary Insurance Products?

What Are Ancillary Products? | Medicare Plan Finder

Our ancillary insurance definition is any insurance product that is beyond the scope of traditional health insurance or is not included in your healthcare plan. One of the most common ancillary products is life insurance – but ancillary goes far beyond that. Ancillary private health insurance can help you cover the healthcare needs that your Medicare insurance does not cover.

Here are some of the ancillary products that our agents sell:

You might think, “wow, do I really need all of those?” You might not – but if you do, you might be able to bundle your benefits. For example, you might be able to find a combination dental and vision plan, or a combination heart attack and stroke plan. Whether or not you need any of these products can depend on your finances, your genetic probability of contracting certain conditions, and what types of plans are available in your area.

Ancillary insurance products are never meant to replace your current health insurance. They are additional products that supplement your existing coverage.

What are examples of ancillary services?

The term “ancillary services” refers to medical services that are not typically provided by your primary care physician. It could mean a service provided by a specialist for your critical illness, a therapist for your long-term disability, etc. Some of these services might already be covered by your disability insurance, Medicaid, or another health plan – but many are likely not covered.

Here’s a list of ancillary services to consider when deciding whether or not you need ancillary insurance:

Ambulance care

At-home preventative care

Audiology

Behavioral health

Chronic care

Heart monitoring

Home healthcare and private nurses

Home medical equipment

Hospice

Infusion therapy

Lab tests

Medical daycare

Mobile services and testing

Orthotics/prosthetics

Radiology

Rehabilitation of any kind

Specialized imaging

Transitional care

Ventilator services

Dental, Vision, and Hearing

Three of the most common types of ancillary insurance plans are those for hearing, vision, and dental coverage. Original Medicare will only pay for some of your very specific dental, vision, and hearing costs.

Medicare Part A and Medicare Part B ancillary services are limited to what your primary physician or hospital staff can do. For example, if you schedule an annual wellness visit with your primary physician and they perform a quick hearing and eye exam, that visit is still covered under your Medicare Part B. Additionally, if you have a medically necessary jaw surgery or receive face tumor treatment in a hospital, most of the related dental work falls under your Medicare Part A. However, if you end up needing more dental, hearing, or vision care, it won’t be covered by Original Medicare.

Private vision, hearing, and dental insurance can help you cover your costs and help you stay on top of your healthcare. Some Medicare Advantage plans include all of these benefits, so before you select an ancillary product, check to see if there is a Medicare Advantage plan in your zip code that makes sense for you.

Short-Term Care

A short-term plan will cover you for up to a year for a temporary injury or illness. For the most part, long-term care is included in your Original Medicare. Short-term care, however, is always an add-on option through a qualified ancillary insurance plan. If you’re concerned about short-term care, let your insurance agent know. They will help you decide whether Medicare Advantage, Medicare Supplements, or another ancillary product will be best for your short-term care needs.

Cancer, Heart Attack, Stroke

Medicare parts A and B, respectively, will cover your hospital stays and doctor visits relating to cancer, heart attacks, and strokes. Some policies are as simple as large payments upon diagnosis.

Others may include annual payouts based on costs, even including loss of income, childcare, travel to facilities, home health care, rehabilitation/therapy, and any other out-of-pocket costs that Original Medicare does not cover.

If you feel comfortable, it helps to disclose your and your family’s medical history when speaking with an agent. That way, the agent can determine whether an ancillary plan for cancer, heart attacks, or strokes is right for you.

Hospital Indemnity

Ancillary hospital indemnity policies are the best, cheapest way to save your piggy bank in the event of an extended hospital stay.

The average cost for one night in the hospital is between $1500-$3000. Your Medicare plan will help cover most of that, but not all, and does not include additional procedures and prescription drugs.

You’ll send in a claim stating what your copayment was, and your carrier will send you a check for a percentage of that amount. This will be especially beneficial if you foresee any medical procedures that will require an extended hospital stay.

Life & Final Expense

Final expenses are any costs associated with funerals, burials, and sometimes medical bills for your final hours. You can buy a final expense whole life plan, meaning the policy lasts for your entire life, or a final expense term life plan, which lasts for a set number of years.

Final expense policies help to reimburse your family members for expenses surrounding your death. You must appoint a beneficiary to receive the reimbursement when you purchase your policy. You will have the ability to change your beneficiary after your policy has been active for a year.

Life insurance is different from final expense because it insures additional finances. For example, it can help your family pay off your mortgage or other debts after you pass. If you don’t already have life insurance, it’s best to invest as soon as possible, because costs will increase as you age.

How Ancillary Benefits Work

Your ancillary insurance carriers could be the same as your carriers for other insurance plans, or they could be different. For example, carriers who sell auto and home insurance are likely also to sell life insurance. Additionally, carriers who sell Medicare Advantage plans are likely to sell other individual health benefit plans.

Even if you have Medicare, ancillary plans provide voluntary benefits and do not fall under Medicare laws. You can enroll in ancillary products during any time of the year (unless you are enrolling through your employee benefits package, in which case your employer might have an enrollment period).

Ancillary billing will be completely separate from your Medicare coverage. If you are still employed, some ancillary benefits can be employer-contributory, meaning your employer agrees to pay part of your premium.

Many ancillary products, like cancer insurance plans, pay by lump sum. With our cancer example, you would receive a lump sum cash benefit upon diagnosis. Keep in mind that a product like that may not be available after you’ve already been diagnosed. Unlike Medicare Advantage plans, ancillary products can and will put you through medical underwriting and can deny you for preexisting conditions.

The Advantages of Ancillary Benefits

When you start looking through all of the available Medicare health plans, you may discover that while many of the available plans could work for you, they aren’t perfect. Additional benefits for Medicare beneficiaries can be hard to come by, especially if you live in an area that does not have many plan options to choose from. Some Medicare plans do offer additional rider insurance (extra health benefits), but they might not be exactly what you need.

That’s why ancillary services insurance may be a good idea. If you can’t find a good Medicare Advantage plan that covers all of your additional medical concerns, like dental, vision, hearing, cancer, heart attack, etc. – ancillary might be the route to go. You will still need coverage for healthcare, so make sure you stay enrolled in Medicare. Then, you can add whichever ancillary products make sense for you.

Frequently Asked Questions About Ancillary Insurance Products

Discussing Ancillary Insurance Products With an Agent | Medicare Plan Finder

You may have many questions about ancillary products, insurance coverage, and costs, including:

Q: Why aren’t these ancillary benefits included in my Medicare plan?

A: Each individual who has enrolled in Medicare has different healthcare needs. You can select a Medicare Advantage or Medicare Supplemental insurance plan that fits your needs, then select any additional ancillary products separately.

Q: Why didn’t my agent discuss these with me sooner?

A: If an agent visited with you to discuss Original Medicare, Medicare Advantage, or Medicare Supplements, they likely were not legally allowed to discuss ancillary plans with you. The Centers for Medicare and Medicaid Services (CMS) has specific rules in place to protect you. If you’d like to discuss ancillary insurance products, your agent will need to come back another day.

Q: How much do these products cost?

A: Costs for ancillary plans vary depending on your needs and what the policy covers. Your agent can discuss any details and help you find the right fit.

Q: So how do I get ancillary insurance?

A: If you are employed, your employer may or may not provide ancillary plans. The best way to get information about ancillary benefits is to speak to your agent.

Get the Ancillary Plans You Need Today

We have insurance agents available who can help you select from the available Medicare Advantage plans for 2020 as well as other ancillary products. Speak with a licensed & local agent today by calling 844-431-1832 or contact us here.

Call Medicare Plan Finder | Medicare Plan Finder

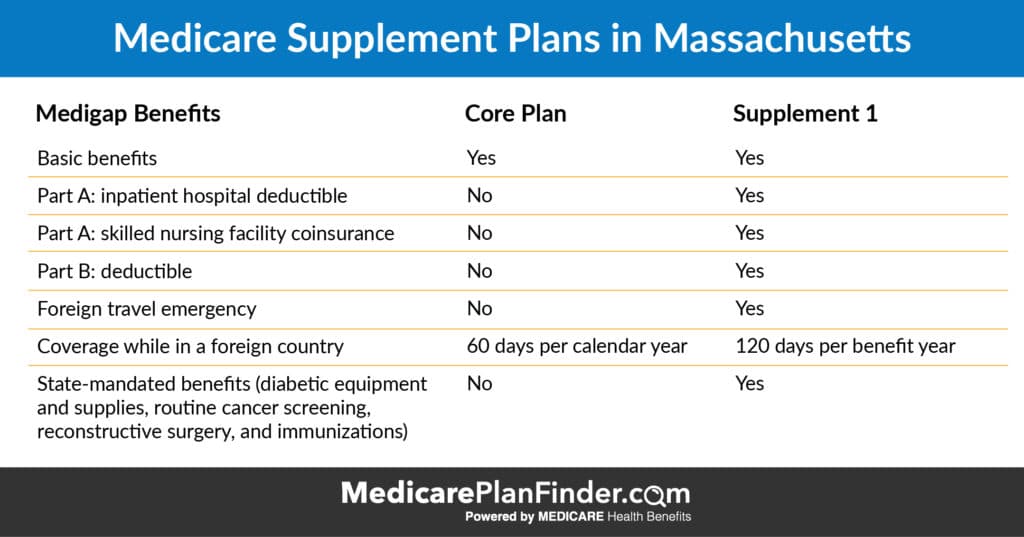

How Medigap is Unique in Minnesota, Wisconsin, and Massachusetts

In most of the United States, Medigap (also called Medicare Supplements) can be characterized by eight different types of plans (A, B, D, G, K, L, M, N). However, there are three states that work completely differently: Massachusetts, Minnesota, and Wisconsin.

A lot of the information you’ll see on the internet about Medicare Supplement plans talks about those eight plans, but we haven’t forgotten about you, Massachusetts, Minnesota, and Wisconsin! If you live in one of those three states, this guide is for you.

Psst…click below to read more about Medicare programs in each state:

If you already have a basic understanding of Medigap, you can skip ahead to the section about your state below.

Medigap is a type of private Medicare insurance that is not technically part of the government-sponsored Medicare program. Medigap plans are also called Medicare Supplements. The two terms can be used interchangeably. To enroll in Medigap, you have to enroll in Original Medicare first.

Additionally, you cannot have a Medicare Supplement plan and a Medicare Advantage plan at the same time. Click here to find out if Medicare Advantage is better for you than Medicare supplements.

What Does Medigap Cover?

Uniquely, Medicare Supplement plans do not typically provide additional health benefits. Instead, Medigap plans provide additional financial protection. For example, let’s say you get sick and have to go to the doctor at least once per month for treatment. Original Medicare may not cover the entire cost for you. You might have to pay your deductible first ($185 for Part B in 2019) and then 20% coinsurance on every visit.

If you have a Medicare Supplement plan that includes deductible and coinsurance coverage, you may not have to pay that $185 and 20%. Instead, you’ll only have to pay your Part B* premium and your Medigap premium.

You may have heard that you cannot be denied Medicare coverage based on your age or preexisting conditions. While that’s true, Medigap is a little different. If you enroll in a Medicare Supplement plan during your Initial Enrollment Period (the time when you first become eligible for Medicare), that holds true. However, if you wait too long to enroll, there is a chance that your plan will be put through underwriting and your prices may increase, or you may be denied coverage based on your age and preexisting conditions.

*Some people may have a Part A premium as well.

Senior couple speaking with a doctor

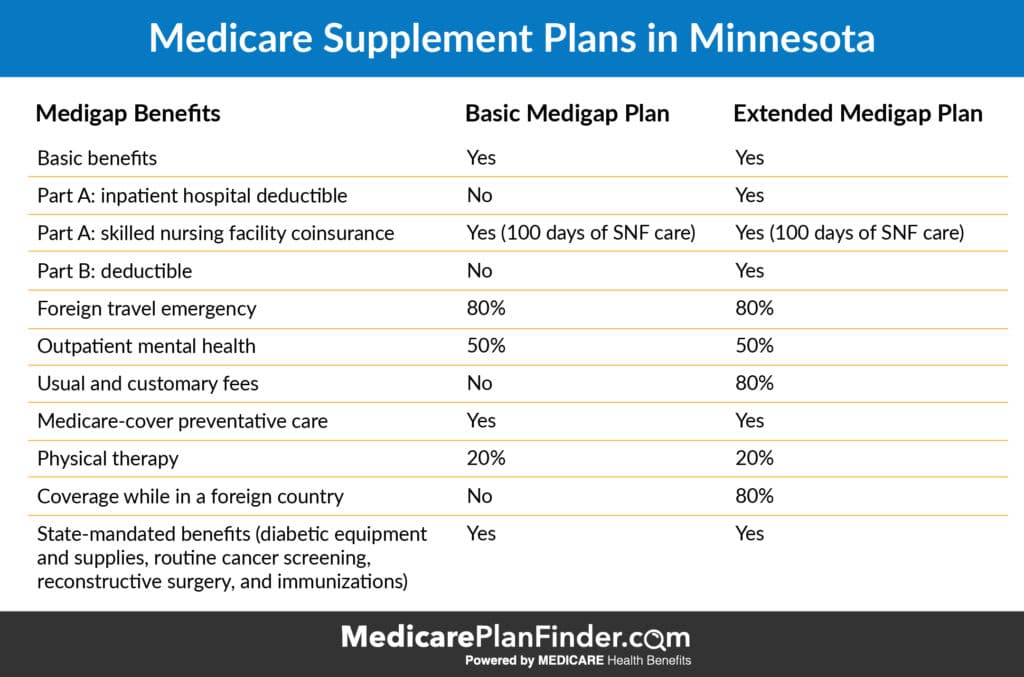

Minnesota Medicare Supplement Plans

While you can’t get the same eight plans (A, B, D, G, K, L, M, N) in Minnesota that are offered in other states, there are technically modified versions of plans K, L, M, and N available.

Additionally, Minnesota offers two unique plans: The “Basic Plan,” and the “Extended Basic Plan.”

The preexisting conditions underwriting may apply. However, you’ll get a 6-month Medigap enrollment period (where age and preexisting conditions do not apply) if you return to work or if you drop Part B in favor of your employer’s health plan.

80% of foreign travel emergency, then 100% after you spend $1,000 per year out-of-pocket

80% of “usual and customary fees,” then 100% after you spend $1,000 per year out-of-pocket

Minnesota Medicare Supplement Plans

So you’re probably wondering, if the Minnesota Medigap Basic Plan and the Extended Basic Plan both always offer the same benefits, why would you choose one Basic Plan over another?

The answer is that costs can vary and plans are allowed to add some extra benefits. There are four additional benefits that plans are permitted to add to the Basic and Extended Basic plans: Part A inpatient deductible, Part B deductible (no longer available in 2020), usual and customary fees, and non-Medicare preventive care.

At least $30,000 for kidney disease treatment (dialysis, transplants, etc.)

Insulin pumps, self-management training, and other diabetes care

50% and 25% cost-sharing plans are also available, which are similar to Medigap Plan K and Medigap Plan L (which would be available in other states).

So, you might be wondering why you have multiple options to choose from for Wisconsin Medigap plans if they are all supposed to be the same “basic” plan. The answer to that is that plans ARE allowed to add additional benefits other than what is in the basic plan, and the costs can vary. Companies are allowed to add the following benefits:

Why Can’t I get Part B Deductible Coverage in 2020?

When MACRA (The Medicare Access and CHIP Reauthorization Act) passed in 2015, a couple of changes were made that didn’t take effect right away; Losing Part B deductible coverage was one of them.

Congress made the decision to not allow plans to cover the Part B deductible starting in 2020. This decision saves money for the Medicare program and doesn’t have an astronomical effect on you. The Part B deductible was only $185 in 2019. All this means is that you will have to pay $185 out-of-pocket before the rest of your coverage kicks in.

It also means that if you are already enrolled in one of the plans listed above that includes the Part B deductible, you won’t lose that coverage. However, if you decide to switch plans or drop that coverage at any time, you won’t be able to get back into it starting in 2020.

How do I Decide Which Medigap Plan is Right For Me?

Regardless of which state you live in, we have a plan finder tool that can help you compare your options.

We also have licensed agents available to answer your questions and help you make your final decision. To find out if there is an agent near you that you can meet with, call 844-431-1832 or send us a message by clicking the “let’s chat” button in the bottom right corner.