Medicare is different from other forms of insurance in a lot of ways. One of the biggest differences is that there are no family plans in Medicare. All Medicare coverage is individual-based.

However, even though Medicare and marriage are not directly related, your marital status can impact your Medicare costs in a few special ways.

Does Medicare Offer Spouse Coverage?

Medicare does not offer health coverage for spouses. You would have to be eligible on your own to qualify for Medicare – your spouse’s eligibility does not affect yours.

According to the rules set in place by the Centers for Medicare & Medicaid Services, marriage can affect your Medicare in the following ways:

Eligibility for Medicare cost savings can change due to your spouse’s income

Your Part D (prescription drug plan) premiums can be higher due to your spouse’s income

Premium-free Part A eligibility can be determined based on your spouse’s work history if they worked more than you.

So, can you get Medicare through your spouse? Not technically, no – but your marital status is not irrelevant.

Medicare if Spouse is Disabled

If one spouse is 65 and begins receiving Medicare and the other is not yet 65, there may be other ways to qualify. If you are diagnosed with ESRD or ALS or if you have been receiving SSDI (Social Security Disability Insurance) for at least two years, you can qualify for Medicare regardless of your age.

The good news is that if you do qualify for Medicare based on a disability, you may also qualify for a Medicare Special Needs Plan at a low cost.

Medicare Eligibility Requirements

The “main” Medicare program is called “Original Medicare.” You can qualify for Original Medicare by:

Unlike Medicaid, income does not impact Medicare eligibility. Additionally, unlike ACA plans, pre-existing conditions do not affect your Medicare costs or coverage. The only exception to this is in private Medigap (or Medicare Supplement) plans. If you do not enroll in a Medigap plan when you first become eligible for Medicare, you can be charged more based on your health history. Medigap plans are completely optional and are there for additional financial protection.

You can qualify for additional health and drug coverage through Medicare Advantage plans or Medicare prescription drug plans after you’ve enrolled in Original Medicare. Those plans cannot charge more based on your age or preexisting conditions.

Spouse Social Security Benefits

Even though the Social Security Administration manages Medicare enrollments, Social Security and Medicare are two vastly different things. There are a few differences in how your marital status affects your benefits.

For Social Security, your benefit is calculated based on your total household income according to your tax returns. That includes both your and your spouse’s income. Both you and your spouse can benefit from Social Security, even after one spouse has passed away.

Medicare does not work like that. Your marital status and income do not impact your eligibility, and there are no additional Medicare benefits given to a spouse after a Medicare beneficiary passes.

Health Insurance Options for Spouse of a Medicare Recipient

If one spouse is ineligible for Medicare and needs to find a different health plan, don’t panic – there are plenty of options for health insurance for the spouse of a Medicare recipient. You might want to start by checking to see if that spouse is eligible for Medicaid based on your total household income. If the answer is no, you’ll want to start looking at individual health plans in your area, which you can do through healthcare.gov/.

If the Medicare spouse has insurance through an employer when they become eligible for Medicare, the non-Medicare eligible spouse can also try getting COBRA until they are also eligible for Medicare. COBRA allows an individual, couple, or family to continue health coverage after leaving a job. However, keep in mind that even if you’re able to keep your health plan through COBRA, your costs may go up because your employer won’t be sponsoring the plan for you anymore.

Can my Wife get Medicare at 62?

To get Medicare, you have to either be 65 or have a qualifying disability.

If your husband or wife is just a few years short of Medicare eligibility, they can select an ACA plan or enroll in a short-term health plan. Short-term medical insurance can be renewed for up to 36 months, so it’s a good option if you’re within 36 months of becoming eligible for Medicare. Since these plans are designed for such short periods of time, they tend to be a bit cheaper than long-term plans, like the ones offered by your employer or the ACA.

Will non working spouse get Medicare?

People often wonder if Medicare is available for their non-working spouse. In short: yes, as long as they meet the age or disability requirements. However, your spouse’s costs may be different from yours. Your employment status does not determine your Medicare eligibility – but it can determine your Medicare costs as such:

If you or your spouse has worked and paid Medicare taxes for at least 40 quarters, you can qualify for premium-free Medicare Part A

If you and your spouse have worked and paid Medicare taxes for less than 30 quarters (or have not worked at all), your Medicare Part A premium will be $518/month in 2026.

Can my Wife get Medicare if she Never Worked?

Employment and marital status do not impact Medicare eligibility. Even someone who has never worked a day in their life can get Medicare, but their costs may be higher than someone who has been paying Medicare taxes.

Medicare vs. Medicaid

Unlike Medicare, your Medicaid coverage can be impacted by your marital status. While each state has somewhat different regulations, most of Medicaid eligibility is based on the Federal Poverty Line. Your income is calculated using your total household income, which is verified with your tax returns. Both your and your spouse’s income are included. That means that even if you qualify for Medicaid based on your income, you won’t be eligible if you and your spouse’s total income together is higher than your state’s limits.

How to Apply for Medicare Through a Spouse

You cannot apply for Medicare through your spouse. You’ll have to wait until you are eligible and then apply during your Initial Enrollment Period. If you qualify by turning 65, this period begins three months before your 65th birthday and ends three months after. If you miss that period, you can apply during the Open Enrollment Period from 1/1 through 3/31. To apply for Medicare online, visit the Social Security website, not medicare.gov.

How do I Apply for Spousal Medicare Benefits?

There are no spousal Medicare benefits – but you can apply for spousal Social Security benefits, here.

What is Not Covered Through Your Spouse’s Medicare?

Your spouse’s Medicare plan won’t provide health coverage for you. If you’re looking for Medicare for spouses, you’ll have to wait until the other spouse is eligible. Then, you can talk to an agent about finding separate plans that work for both of you and both fit into your household monthly budget.

Medicare Family Coverage

In general, Medicare is not available to non-qualifying spouses or dependants. However, if your child has a qualifying disability, they may be eligible for a Medicare plan of their own. Note that except for in the cases of ALS and ESRD, you will have to receive disability benefits for at least two years before you can enroll in Medicare.

How Does Getting Married Affect Medicare?

Getting married? Congrats! A new marriage often involves complicated discussions about finances, and you might be wondering, “will getting married affect my Medicare benefits?” The good news is that no, marriage does not affect your current Medicare benefits – but it CAN impact your eligibility for Medicare cost savings programs. For example, Medicare Savings Programs and Low-Income Subsidies for Medicare prescription coverage base eligibility on total household income. If your new spouse causes your household income to increase, you could become ineligible for these programs.

If you’re not yet 65, you might be wondering, “will I lose my disability Medicare if I get married?” No! Even if you are qualifying for Medicare based on disability and not age, your Medicare coverage won’t change based on your marital status.

Medicare Premium Payments: How Much Does Medicare cost for a Married Couple?

How much does a married couple pay for Medicare? Medicare is 100% individual, so each spouse will have to pay their own premium. There are no joint plans with joint costs.

Your Medicare Part A monthly premium will depend on your and your spouse’s work history and will range between $0 and $518 per month in 2026. Your Medicare Part B premium will be $185 in 2026 (unless you qualify for savings programs or have your premium covered by a Medigap plan). If you have Medicare Part D prescription drug coverage or either a Medicare Supplement or Medicare Advantage plan, you’ll pay a separate premium for those plans.

Do Husband and Wife pay Separate Medicare Premiums?

Yes – families and spouses cannot have joint Medicare plans. All premiums will be separate. Some people will have their premiums automatically deducted from their Social Security benefits.

How Your Spouse Might Affect how Much you Pay

Your spouse can reduce your Part A premium amount if they have worked more than you. Additionally, your spouse’s income can affect your eligibility for assistance programs such as Medicare Savings Programs, Medicaid, and Medicare Extra Help.

Medicare Plan Spousal Discounts

While Medicare does not provide spousal benefits, there are some plans that offer household discounts for plan premiums. You should always confirm with your agent whether or not a household discount exists as some companies may have specific requirements regarding spousal discounts.

Medicare Extra Help and Income Limits

The one thing that marriage will affect when it comes to Medicare is whether or not you qualify for the Extra Help Program, otherwise known as Low-Income Subsidy (LIS). LIS exists to help people with limited income pay for their prescription drugs. Those who qualify for the program pay less in drug premiums, copayments, and coinsurances.

Meet with a Licensed Agent

Even if you and your spouse have different Medicare plans, you can still share an agent!

Sharing an agent will make your enrollment process easier and help you build a relationship with someone who knows everything about Medicare plan options and can help you find savings.

Do you have a licensed agent? Have more questions about spouse Medicare? Give us a call today to set up a free meeting.

Our agents are licensed to sell many different insurance plans, so they can offer you an unbiased opinion and help you find the plan that truly works best for your needs.

However, the Medicare AEP only lasts from 10/15 through 12/7 of each year. Some people may qualify for a Special Enrollment Period and may be able to change plans outside of the AEP, but for many, this will be the only time to change plans!

What you Should do During Medicare AEP

Even if you think you have the best Medicare plan in the world, here are a few things you should definitely do during or leading up to Medicare AEP. If you need help with this, we advise giving us a call.

Check Eligibility for Savings.

Apply for LIS (Extra Help) prescription drug savings program) and other Medicare Savings Programs to see if you could be saving money. If you have low income, you may even want to try applying for Medicaid! The results could influence what coverage you are eligible for this AEP.

Review Current Medicare Coverage.

Did you receive your ANOC (Annual Notice of Change), and is anything in your plan changing? These letters are usually sent and received every year at the beginning of September.

What insurance do you have now?

Do you have Original Medicare only, or do you have a private plan as well?

Do you have enough coverage?

Does your plan fit into your budget, or could you be saving more money?

Are all of your doctors and prescriptions covered by your current plan?

Ask yourself these questions and take notes, because there may be something better out there.

Notate your Life Changes.

Did you start seeing a new doctor this year, or do you have a problem with your current doctor? Not all plans accept the same doctors, so make sure you’re documenting your current physicians so you can easily confirm they are in network with any potential plans you’re considering for the new year.

Did you gain or lose a job, or suddenly develop financial stress? There are multiple ways to manage your Medicare based on a budget and a licensed agent can walk you through the options you may qualify for.

Were you diagnosed with a new health condition that requires expensive treatments? Some plans are specifically designed for certain chronic conditions.

Think about not only your past year but what you expect to happen over the next year. Think about what type of coverage you might need to get yourself through it all.

See What Medicare Plans are Available in 2026

Every year, new Medicare plans may come to the market, and old plans may change what they are offering. It’s important to look at the new information instead of just assuming that your old plan will stay the same. If your plan does change what they are offering, you will be notified – but it is important to look at other changes in your area as well.

Maybe there’s a great new doctor you’ve wanted to see, but she doesn’t accept your current plan! Or, maybe you suddenly have access to a plan with a five-star rating, when previously you only had access to four-star plans!

An important thing to note is that new benefits are not available to review and discuss each year until October 1st. You may need to speak with a licensed agent to ensure you’re reviewing the plans for the upcoming benefit year and not mistakenly comparing plan benefits that will ultimately be changing.

Meet with an Insurance Agent.

We know it’s nice to think that you can do it all yourself and that with the internet, you don’t need an insurance agent anymore! But, that’s not always true. The benefits of meeting with a licensed insurance agent are simple: it’s free, it’s easy, and it can’t hurt!

Our agents are licensed and represent a variety of different insurance companies, meaning they are not all biased towards one plan option.

Your plan won’t cost any more money whether you meet with an agent or not, so meeting an agent can only help you. A licensed agent can walk you through everything that is available in your local area and help you select the best option based on your needs. Plus, let us repeat – the meeting is free!

We’re here to help, so we don’t want to only talk about the positives. Here are some things that you should NOT do during the Medicare AEP:

Don’t Jump into a new Medicare Plan Too Fast.

Do you understand how to choose a Medicare plan? Sometimes good deals are tempting, and it’s easy to jump into a shiny new plan because the costs are lower or there’s an added benefit. Make sure you’ve considered everything before you switch because it might not be easy to switch back. Make sure that your doctors work with the new plan, it covers your prescriptions, and there aren’t any hidden costs. Also, make sure the new benefit is something that will actually be useful to you!

Misunderstand Medicare Supplements vs. Medicare Advantage Plans.

Medigap, or Medicare Supplements work differently from Medicare Advantage and other types of Medicare plans. Technically, Medigap enrollment is not limited to the AEP. However, that does not mean that you should just change back and forth between different Medigap plans any time.

If you enroll in Medigap outside of your Initial Enrollment Period (when you first become eligible for and enroll in Medicare), you may be put through an underwriting process and may have higher fees based on your age and any preexisting conditions. Medicare Advantage and Part D plans do NOT take age and preexisting conditions into account, but Medigap plans if you wait too long to enroll.

3. Don’t Avoid Researching Medicare Plan Options.

If you already know the name of a carrier, you might be tempted to go straight to their website and enroll in a plan that looks good online. However, there may be more than one carrier offering plans in your area. So, how do you look at all of them easily?

Start by using a plan comparison tool, like our free Medicare Plan Finder. Then, once you’ve compared a few options, consider taking that research to a licensed agent who can talk to you about what you’re looking at and why the differences matter.

Ready for AEP?

To schedule an appointment with one of our licensed agents, call (833)-567-3163 or click here. We can’t wait to help you get the coverage you deserve!

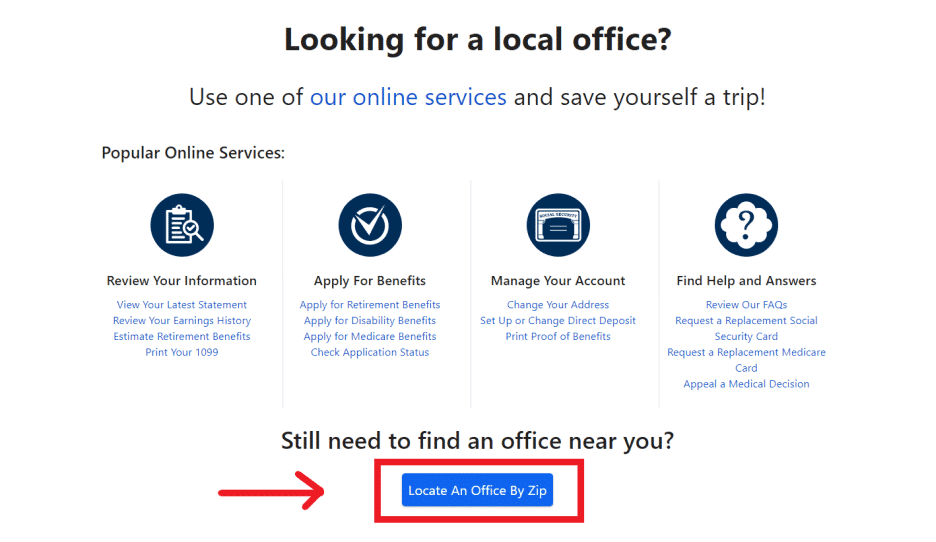

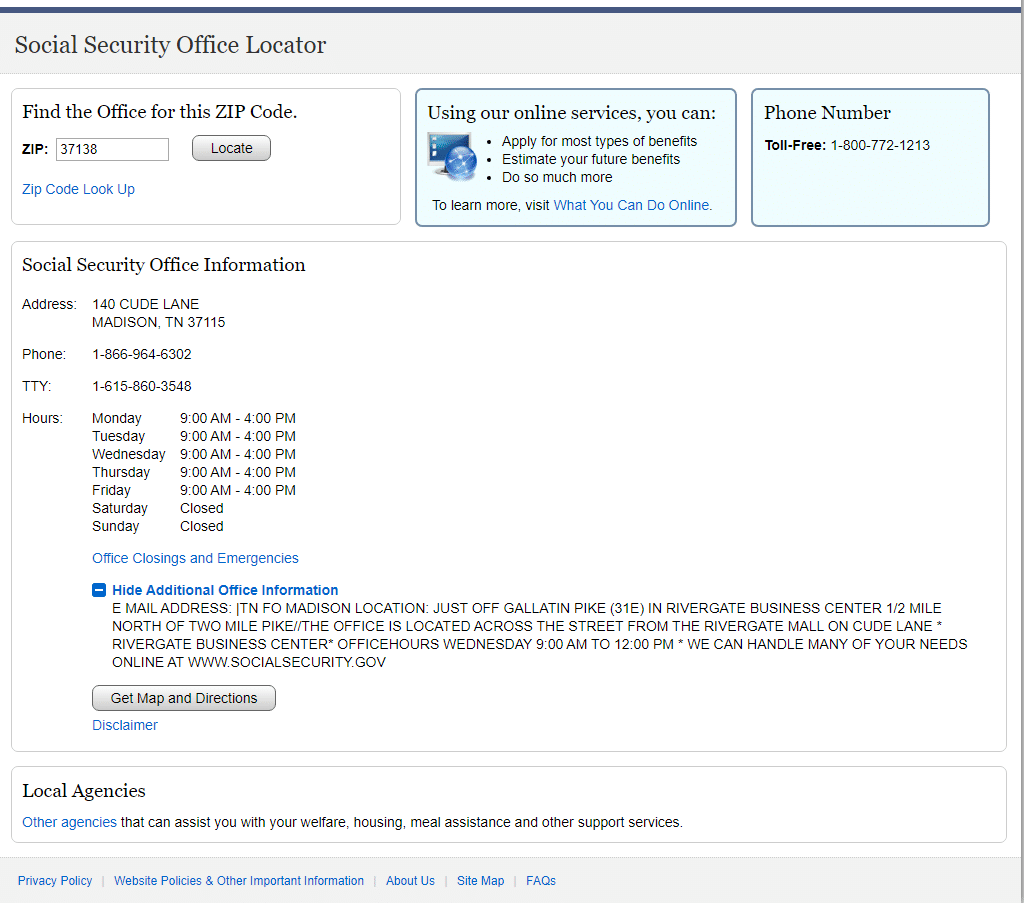

How to Find a Medicare Office Near You

While you can handle most of your healthcare online, some things are better handled in person at the Medicare office near you. Your local Medicare office may be able to help you enroll in Medicare, get a replacement Medicare card, and answer many other important questions.

Medicare offices are located within Social Security offices. Here are the simple steps to locate a Medicare office near you.

Visit the SSA website and use their field office locator tool.

Click on “Locate An Office By Zip.”

Enter your zip code and click “locate”

You’ll now see a list of the Medicare offices in your area. You’ll see each Medicare office’s address, phone number, office hours, and any other additional notes. Take a look at the screen shots below.

Why and How to Contact a Medicare Office

Calling MEDICARE allows you to:

Check your claim status

Find out if your medical service or product is covered

Ask your billing questions

Check your account balance for Part A or B

Report fraud

Report a lost or stolen Medicare card

Keep in mind that the Medicare office near you can’t help you with your private plan (like Medicare Advantage, Medicare Supplement, etc.). For questions with your private plan, you can contact your insurance agent or your insurance company directly.

Medicare Office Hours

Social Security hours will vary by location. When you use the office locator tool, you’ll be able to see their hours and their phone number.

Medicare Phone Number

The main Medicare helpline number that you can call with billing, claims, medical records, or expenses questions is 1-800 MEDICARE (1-800-633-4227)/TTY 1-877-486-2048.

Medicare Mailing Address

The main Medicare office (CMS office, Centers for Medicare and Medicaid Services) is located in Woodlawn, Maryland. There are additional regional Medicare offices in D.C., Boston, New York, Philadelphia, Atlanta, Chicago, Dallas, Kansas City, Denver, San Francisco, and Seattle.

If you need to mail something to Medicare, use the following address:

Medicare Contact Center Operations

PO Box 1270

Lawrence, KS 66044

____________________________

Regional offices are as follows:

Washington, D.C. The Hubert H. Humphrey Building 200 Independence Ave., S.W. Washington, DC 20001

Boston, MA John F. Kennedy Federal Building 15 New Sudbury St., Room 2325 Boston, MA 02203-0003

New York, NY 26 Federal Plaza, Room 3811 New York, NY 10278-0063

Philadelphia, PA 801 Market Street Suite 9400 Philadelphia, PA 19107-3134

Atlanta, GA Atlanta Federal Center, 4th Floor 61 Forsyth Street, SW, Suite 4T20 Atlanta, GA 30303-8909

Chicago, IL 233 North Michigan Ave, Suite 600 Chicago, IL 60601

Dallas, TX 1301 Young Street, Room 714 Dallas, TX 75202

Kansas City, MO Richard Bolling Federal Building 601 East 12th Street, Room 355 Kansas City, MO 64106-2808

Denver, CO 1961 Stout Street, Room 08-148 Denver, CO 80202

San Francisco, CA 90 7th Street, #5-300 (W) San Francisco, CA 94103-6706

Seattle, WA 701 Fifth Avenue, Suite 1600 Seattle, WA 98104

Can you get Medicare Online?

Yes, you may not have to visit your local Medicare office or call Medicare at all.

As long as you feel comfortable using your computer instead, you can apply for Medicare, manage your benefits, get answers to your questions, and even request a new Medicare card all online.

If you do want to visit your local Medicare office in person instead, it may be a good idea to call ahead and make sure that they can help you with your question or concern.

Senior stylish woman taking notes in notebook while using laptop at home. Old freelancer writing details on book while working on laptop in living room. Focused cool lady writing notary in notepad.

Why would you need to go to a Social Security Office?

Most things can be done online nowadays, but there are still a few non-Medicare related tasks that you may need to visit your local Social Security office for. For example, there are ten states that don’t allow you to get a replacement Social Security card online, though this may change in the future. The ten states are Alabama, Connecticut, Minnesota, Nevada, New Hampshire, Ohio, Oklahoma, Oregon, Utah, and West Virginia.

Other services you may need to handle in-person are completing benefits applications with a translator, applying for survivor benefits, and getting a Social Security number for the first time if you didn’t get one as a baby.

Contact Us

For additional questions, please contact us directly at (833)-567-3163.

Does Medicare Cover Physical Therapy?

Does Medicare cover physical therapy? It depends. Medicare can help pay for physical therapy, which may be a crucial part of injury or surgery recovery. However, Medicare’s coverage has limits.

Every Medicare beneficiary begins with Original Medicare, which includes Part A, hospital coverage, and Part B, medical coverage. Most physical therapy services will fall under Medicare Part B – however, there are specific Medicare guidelines for physical therapy in-home health services and doctor services.

It can be confusing to navigate the different coverage caps and figure out what Medicare therapy coverage you have. Let’s break it down.

Does Medicare Cover Physical Therapy for Back Pain?

Back pain is one of the most common symptoms that leads to physical therapy. As you age, back pain is almost inevitable. It’s easy to fall into bad habits and poor posture. If you have back pain that lasts for a few weeks or longer, most doctors will recommend physical therapy.

A licensed and professional physical therapist will not only help you decrease pain but also educate you on how to prevent back pain in the future. He or she may even teach you some physical therapy exercises to perform at home.

Alternatively, seniors and Medicare eligibles who have a hard time getting to a doctor’s office may opt for a home nurse who is licensed to assist with physical therapy. In most cases, if your home nurse happens to double as a physical therapist, you will be covered under Part B.

Unfortunately, these services are not free.

Medicare Physical Therapy Cap | Medicare Plan Finder

How Much Does Medicare Pay for Physical Therapy?

Medicare Part B will cover your medically necessary outpatient therapy (physical, speech-language pathology, occupational) at 80 percent, you will likely be responsible for 20 percent of all Medicare-approved costs.

Previously, Medicare only covered up to 80 percent of $2,040 ($1,608) for physical and speech-language therapy services and another 80 percent of $2,040 ($1,608) for occupational therapy services. That meant that, for example, if your physical therapy appointments cost you $100, Medicare would have only covered about 20 visits per year.

Beneficiaries were receiving notices titled, “Advance Beneficiary Notice of Noncoverage.” The notice will tell you what Medicare will can or cannot continue to cover so that you can make informed choices about whether or not you want to continue your physical therapy.

Thankfully, physical, occupational, and speech therapy patients with Medicare won’t have that problem in (833)-567-3163.

Medicare Physical Therapy Billing

Medicare Physical Therapy Caps | Medicare Plan Finder

When it comes to paying the bills for your physical therapy, you may want to consider adding either a Medicare Advantage plan or a Medicare Supplement plan. Even though Original Medicare Part B covers physical therapy, the cap will hold you back. Adding Medicare Advantage or Medicare Supplements may give you the coverage you need to pay the bills.

The good news is that everyone who is eligible for Original Medicare is also eligible for Medicare Advantage and Medicare Supplement plans. You can’t have both, so you’ll have to choose one.

Medicare Advantage plans are offered by private insurance companies and are designed to add additional covered services like dental, vision, hearing, fitness.

Alternatively, Medicare Supplement plans do not provide coverage for additional services but instead provide additional financial coverage. These plans are designed to help you pay for your coinsurance, copayments, and deductibles. You’ll have to decide what makes the most sense for you and your needs: more financial coverage, or more covered services?

Your physical therapist can discuss the physical therapy benefits specific to your condition and personal medical history.

Does Medicare Cover Transportation to Physical Therapy Appointments?

Original Medicare does not cover non-emergency medical transportation. Some Medicare Advantage plans can cover Medicare transportation benefits including travel to and from doctor’s appointments.

How to Find a Physical Therapist Who Accepts Medicare

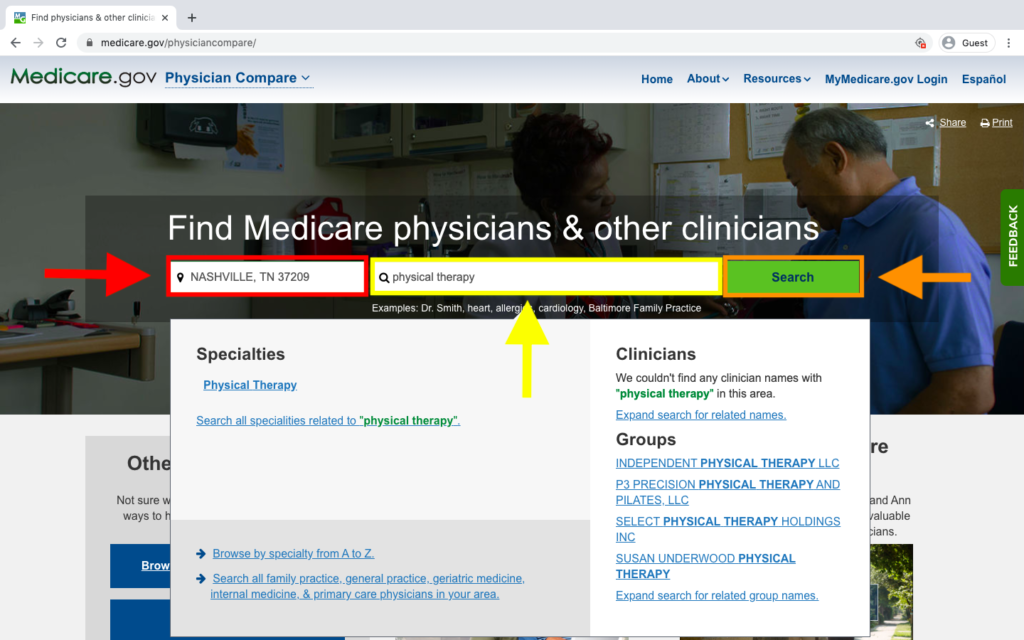

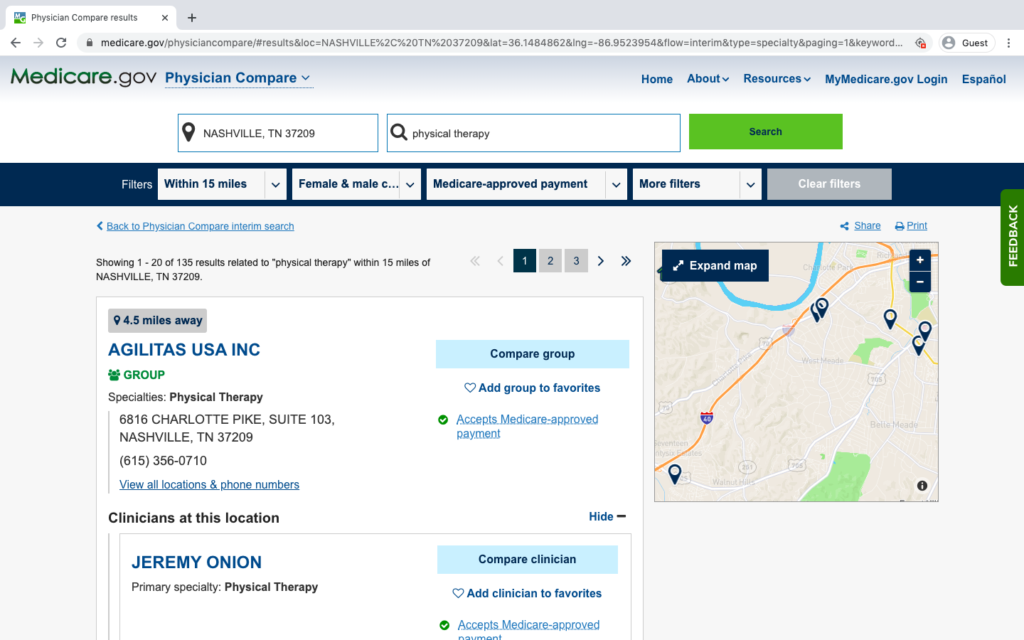

Finding a local physical therapy practice that takes Medicare may be easier than you think. If you’re looking for physical therapy near you, click here to get started. Medicare.gov’s Physician Compare website allows you to find providers who specialize in the services you need including physical therapy.

Enter your zip code beside the red arrow. We used our home office’s zip code in Nashville, Tennessee, which is 37209. Then type “physical therapy” in above the yellow arrow. After that, click “Search” beside the orange arrow.

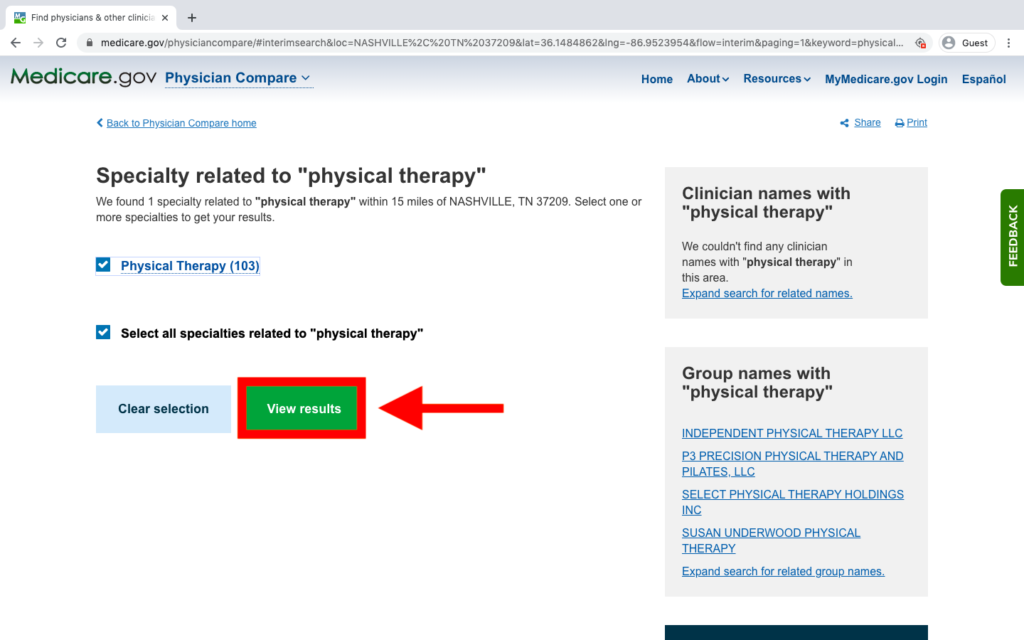

You confirm the service you need on the next page. If the boxes beside “Physical Therapy” and “Select all specialties related to ‘physical therapy'” are white, click in them to make both boxes have check marks. Then click “View results.”

The last step is scrolling through the list of providers and making some calls. You may have to call more than one physical therapy practice to find one that fits your medical and budget needs.

Need a New Medicare Plan?

Our agents can help you decide if Medicare Advantage or Medicare Supplements are right for you. We have agents in 50 states and we’re constantly growing!

Plus, our agents are licensed to sell plans from many of the major insurance carriers in your area, which means we are NOT biased. We can help you set up an appointment with an agent who can show you how to choose the right Medicare plan for your needs.

Most seniors and Medicare beneficiaries will have to wait until AEP (10/15 to 12/7) to change plans. Check outour post about Special Election Periods to see if you qualify for a SEP. Not sure if you qualify? That’s OK. Your licensed agent can help you find out if you qualify. Give us a call at (833)-567-3163 or click here to have Medicare Plan Finder call you.

This post was originally published on January 4, 2018, by Anastasia Iliou, and was most recently updated on January 6, 2020, by Troy Frink.

How to Find a Home Chair Lift You Can Afford

A chair lift (also called a stair lift or lift chair) is an assistive device that helps users go up and down stairs without having to climb. The user rides in a seat attached to a track, and the device glides up the staircase. Chair lifts can help people be more independent.

Purchasing a lift chair for your home doesn’t have to be extremely expensive. Here are some ways to get financial assistance for home stair lifts.

How to Find Home Chair Lift Assistance

You may be eligible for federal and/or state financial assistance for purchasing and installing a lift chair. The best way to find out if you qualify for assistance is to apply for the various programs and ask what’s available. If you think you’re eligible, you can apply for Medicare, Medicaid, Social Security, and veterans benefits.

Does Medicare cover stair lifts?

Original Medicare does not cover stair lifts*. However, certain private plans called Medicare Advantage (Part C) plans might. There are hundreds of Medicare Advantage plans available throughout the country, but they can all offer slightly different coverage. Additionally, not all plans will be available in your area.

*Original Medicare may help pay for an elevating seat to help the rider sit and stand safely. The coverage may only cover the seat, which is considered to be durable medical equipment. According to Medicare, home chair lifts fall under home modifications, not durable medical equipment.

Will Medicaid pay for a lift chair?

Medicaid is a state and federal program that helps eligible people receive healthcare coverage. Your state’s Medicaid program may help pay for a lift chair if you qualify.

A DSNP qualifies you for a Special Enrollment Period (SEP) that allows you to make one change per quarter for the first three quarters of the year (January – September). You can make a change in your coverage during the fourth quarter (October – December), but only during the Annual Enrollment Period (AEP), which is from October 15 – December 7. The change you make during AEP will take effect on January 1 of the following year.

Stair Lifts for Disabled Veterans

The Department of Veterans Affairs (VA) may help disabled veterans who cannot safely navigate stairs pay for a stair lift. The benefit applies to veterans whose disabilities are the result of their military service. You may need a home visit and skills evaluation before the VA approves your stair lift.

You may also qualify for VA benefits if you or your spouse is disabled and the disability is not the result of military service. Some veterans qualify for the VA Aid and Attendance benefit, which may help pay for “care-related services.”

If you aren’t eligible for a lift chair due to service-related injuries, and you don’t qualify for the VA Aid and Attendance benefit, local assistance programs called Veterans Directed Home and Community Based Services may help. These are specific to local VA medical centers, and they help veterans live at home, rather than at nursing homes.

Some long-term care insurance policies may cover stair lifts if it means that you can live at home, rather than transitioning to a long-term care facility.

In addition, you may be able to save by looking for used stair lifts. Some manufacturers may offer financing so you don’t have to pay all at once.

Chair Lifts for Stairs With Landings

Chair lifts for stairs with landings come in a variety of configurations to accommodate different types of stairs. Most chair lifts fall into two categories: straight or curved.

Straight Chair Lifts

Straight chair lifts only work on straight staircases without curves or corners. However, you can use multiple straight chair lifts on straight portions of your staircase with landings or turns.

For example, one chair lift can go from the floor to the first landing. Then another can go from the first landing to the top of the stairs.

The advantage to installing multiple chair lifts is that it can be less expensive than one curved lift chair. The disadvantage is that once you reach the first landing, you must get up and transfer to the second chair. The transfer may be unsafe for some people.

Curved Chair Lifts

Every staircase can be different, and to work, most curved chair lifts must be custom-fit to accommodate your home’s twists and turns. However, there are some common configurations that include:

Top or Bottom Overrun: An overrun can be at the top, bottom, both ends of a staircase. The “overrun” is where the stair lift track extends past the staircase and onto the landing and/or the floor at the bottom of the stairs. This feature may make it easier for the user to sit into or stand up from the chair.

Intermediate Landing: An “intermediate landing” is a landing before the top of the stairs. Curved stair lifts can rise with the staircase, become level at the intermediate landing, then continue rising to the top of the stairs.

90° Flat Landing: This is a type of staircase with a landing that has right-angle change of direction in the staircase. Like with the intermediate landing, the lift chair’s track travels up the staircase, levels out at the landing, then travels up again.

180° Flat Landing: The same as the 90° flat landing but the turn is 180° at the landing.

Spiral Stair Lift: These chair lifts feature tracks that curve around the entire length of a spiral or curved staircase.

Original Medicare does not offer coverage for home chair lifts. If you want help finding assistance for a home stair lift, one of our licensed agents may be able to help you find a Medicare Advantage plan, a long-term care policy, or other financial assistance. Our agents are highly trained and they can help you determine the right fit for your budget and medical needs. To schedule a no-cost, no-obligation appointment, call 1-844-431-1832 or contact us here today.

What is Medicare Part B Buy Back/Give Back?

Are Medicare Buy Back plans too good to be true?

No!

Can they really put money back into your social security check?

Yes, it’s offered through SOME Medicare Advantage plans but not all.

Here is how it works.

Some Medicare Advantage plans out there that can “buy back” your monthly Part B premiums, ultimately putting money back into your pocket. You’ve likely seen this on TV, but unfortunately it’s misleading as this specific benefit is narrowly used by a few plans across the country.

These plans are effectively paying you instead of the other way around! Let me explain.

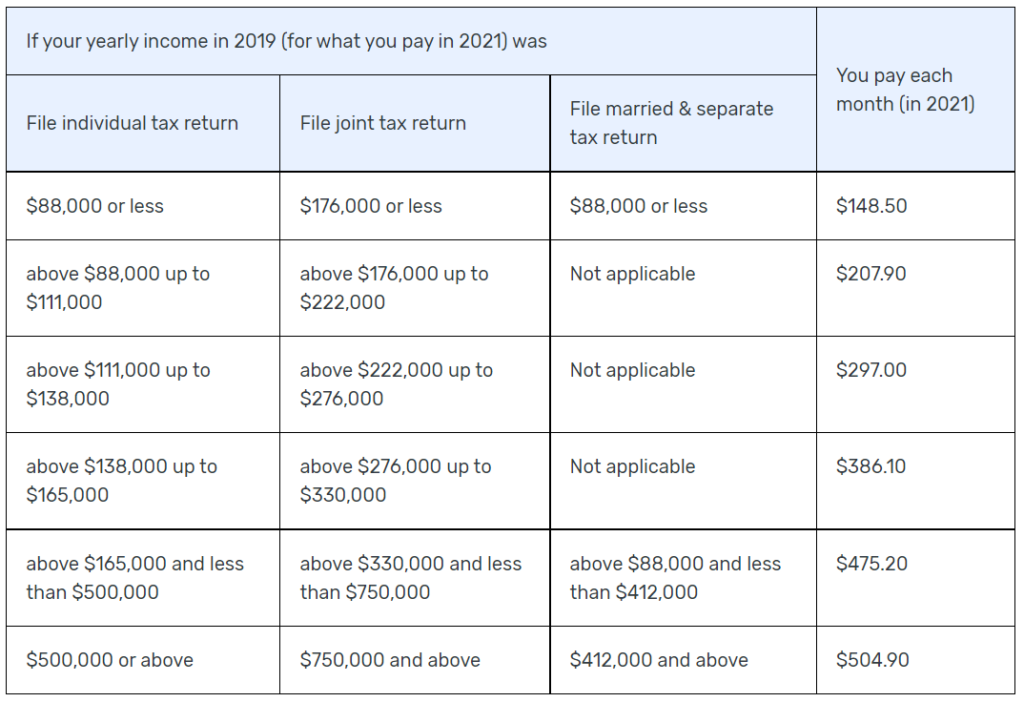

Medicare Part B Premiums in 2022

In 2022, the standard Medicare Part B premium will be $148.50. Your premium may be a bit higher if you have a higher income. Below is a snap shot directly from Centers for Medicare and Medicaid about the current Part B premium scale.

The reason you have to keep paying this premium is because Medicare Part B is a paid program, unlike Medicare Part A which you earned during your working years by paying social security taxes. By default, everyone has to pay for Medicare Part B unless they get some kind of financial assistance.

While Medicare Part B is a part of original Medicare, Medicare Advantage plans are privately owned and offer additional benefits beyond original Medicare. In particular, Part B buy back is an additional benefit offered by some plans. This is sometimes confusing to many people, so bear with me.

To have Medicare Advantage, you must be enrolled in original Medicare Parts A and Parts B. In order to be enrolled in original Medicare, you must have worked 40 quarters (or 10 years) paying into social security to earn Part A, and then pay a monthly premium for Part B. To stay enrolled, you have to continue paying your premiums!

You can’t get a Medicare Advantage plan without having original Medicare.

What are Medicare Advantage Part B Buy Back Plans?

Medicare Advantage plans are additions to your existing Medicare coverage. They can vary greatly in coverage amounts and premium prices. Some Medicare Advantage plans can come with a $0 premium or a low premium in addition to a Part B buy back (or give back, as some plans call it).

If you pay your Part B premium automatically out of your Social Security check, this could feel like a bonus added to your monthly checks! You’ll start seeing a bit more coming in, which is nice, assuming the plan you choose has the buy back option.

Premium Give Back Plan? What’s the Catch?

You’re probably skeptical about the idea of an insurance company wanting to give YOU money.

However, there’s not really a catch. According to Quality Health Plans of New York, Medicare Advantage plans “may choose to use some of the funding it receives” to “reduce its members Medicare Part B premium.”

So, what these plans are doing is providing you an incentive to sign up for their plans.

Even if they give you some of that money back for your Part B premiums, they still get paid from your copayments, deductibles, etc.

As you’re looking into available Medicare Advantage plans that offer Part B buy back benefits in your area, be sure to consider what you might be giving up.

Remember, all plans are different, but it is possible that a plan with a Part B buy back option will have higher copayments and deductibles – which may not matter to you if you don’t spend a lot of time in the doctor’s office! The devil is in the details.

I guess you could say the only true “catch” to these plans is that you have to stay enrolled in Medicare parts A and B – but that’s true of any Medicare Advantage plan. You’ll have to continue paying your A and B premiums, even if you do get some of that money back.

Additionally, it may be a few months after you sign up for your premium give back plan before you receive your first Part B reimbursement.

How do I Get a Part B Buy Back (Give Back) Plan?

Great question! As you can imagine, these plans might be harder to find than more standard Medicare Advantage plans, and there may or may not be one available in your area.

Unfortunately, CMS (Centers for Medicare and Medicaid Services) does have certain rules in place that forbid us from sharing the plan details with you publically. However, we have licensed agents across the nation who can meet with you either in person or by phone to help you choose a plan.

If you’re interested, call us at 800-691-1832. Let us know that you’re interested in Part B buy back plans, and we’ll do all we can to help! You can also leave us a message here, and we’ll get back to you.

2020 Medicare Changes & Trump’s Executive Order

Every year, CMS (Centers for Medicare and Medicaid Services) reserves the right to make changes to the Medicare program. Rules and regulations around enrollment periods, penalty fees, marketing, and plan benefits are released in late summer and early fall for the following year. Costs can rise, and brand new plans can enter or leave the market.

Medicare is confusing as it is. When you add these yearly changes into the mix, choosing the right plan can be stressful. Our goal is to make all of this less stressful for you. Our website is a great educational tool, and our licensed agents can provide free assistance!

Here are the changes you need to know about for Medicare in 2020.

On October 3, 2019, President Donald Trump signed an executive order “protecting” the Medicare program. What does this mean?

Alex Azar, Health and Human Services (HHS) Secretary, said that Trump told HHS to take “specific, significant steps” towards improving Medicare funding and improving healthcare for American seniors. These steps include lowering Medicare Advantage costs, allowing savings accounts, and improving access to new medical technology. It also leaves room for more plan options, more telehealth, more wellness benefits, and a stronger financial model.

In his post-executive order speech given in Florida yesterday morning, Trump stated, “In my campaign for president, I made you a sacred pledge that I would strengthen, protect and defend Medicare for all of our senior citizens.” That was the intent of the executive order.

Is Medicare Going Up in 2020?

New 2020 Medicare premiums and costs for 2020 have not been released yet. The new numbers are usually released in early fall of the year prior, so we are expecting to see them over the coming months. The Wall Street Journal reported in April that 2020 Medicare Part B premiums are likely to increase by $8.80/month to a total of $144.30, but this is not final.

We will continue to update this post with new 2020 costs as they are released. Thank you for your patience!

2020 Medigap Changes

Just like the Original Medicare program, private plans like Medicare Advantage, Medicare Supplements, and standalone benefit plans can change every year.

Plan availability may not be the same for everyone. Medigap eligibility, in particular, can depend on your age when you enroll, preexisting conditions, and where you live. Plans can be different not only in every state but also in every county and zip code.

Use our plan finder tool to find out what Medigap plans are available in your area for 2020.

Is Medicare Supplement Plan F Going Away in 2020?

Starting in 2020, you will no longer be able to purchase Medigap Plan F or Medigap Plan C. Plan F was one of the most popular plans, and Plan C was fairly similar. The plans are going away because they include coverage for the Part B deductible (only $185 in 2019).

You might here plans C and F referred to as “first-dollar” plans because they virtually eliminate out-of-pocket costs. CMS decided that taking away the Part B deductible coverage was a smart move to discourage people from overusing their primary physician offices and costing the Medicare program a lot of money for unnecessary doctor’s visits.

If you already have Medigap Plan F or Medigap Plan C, you can be grandfathered in. That means that you will not lose your coverage in 2020. However, if you leave your Plan F or Plan C in favor of a different Medigap plan, you won’t be able to re-enroll in F or C.

Will Plan F Premiums Rise After 2020?

As Plan F sees less and less enrollees, Plan F premiums will likely begin to rise. We can’t say this for sure and we will certainly have to wait and see what happens, but generally less enrollees means higher costs for the companies, resulting in higher premiums.

Will There be a High Deductible Plan G in 2020?

Since people will not be able to purchase Plan F or Plan C in 2020, CMS did want there to be another option with similar benefits. Plan G was already that option, given that the only difference is that Plan G does not cover the Part B deductible.

The other difference is that previously, Plan G was not offered with a high-deductible. If you typically have low medical costs, you may prefer a high-deductible option. Having a high deductible often means that your premiums will be lower. This way, you don’t have to pay as much until you start experiencing health concerns. The high deductible Plan G option can replace the high deductible F option.

Donut Hole Closing in 2020

In addition to all of these plan changes, the infamous “Donut Hole” will be effectively closing in 2020. The Bipartisan Budget Act of 2019 closed the coverage gap for brand-name drugs in 2019, and the generic drug coverage gap will be eliminated in 2020. This basically means that, if you have a Medicare Part D plan, you will only be responsible for 25% of your covered prescription drug costs instead of 44%.

2020 Medicare Advantage Changes

There may be more Medicare Advantage plan changes to come in 2020, but we wanted to make sure you had heard about the changes from last year.

On October 12, 2018, the Centers for Medicare and Medicaid (CMS) announced the 2019 Original Medicare premium and deductible increase, but what about Medicare Advantage (MA) plans? Unlike Medicare Part A and B, beneficiaries enrolled in MA plans may see a decrease in their premiums in 2019 and 2020 compared to 2018.

2020Medicare Advantage Cost Changes and 2020 Premiums

In September of 2018, CMS announced that on average, Medicare Advantage premiums will decrease by 6%. This is great for beneficiaries interested in affordable vision, dental, and hearing coverage or even fitness classes like SilverSneakers®!

CMS estimated that 83% of beneficiaries would have equal or lower premiums for 2019 and 46% will have a $0 premium! Premiums for MA plans have steadily declined, and this is the lowest premium we’ve seen in three years. This is a perfect example of a private and public collaboration that allows beneficiaries to drive and define the value. The 2019 Medicare Advantage changes are a quick glance of what you can expect to continue in the future.

2020 cost changes for Part A and B premiums and deductibles have not officially been released yet but are not expected to increase by very much. We will continue to monitor this information and will update as soon as the cost changes are officially announced.

Early in 2018, CMS (Centers for Medicare and Medicaid Services) released new rules that allow Medicare Advantage plans to offer a few benefits, like “daily maintenance,” transportation, telehealth, and durable medical equipment.

Some plans in 2020* are really going above and beyond, offering benefits like new air conditioners and pest control!

*These benefits are not included in all MA plans. Your agent may be able to help you find a plan that includes more.

Daily Maintenance

The addition of the “daily maintenance” benefit means that Medicare Advantage plans are now able to offer at-home care items, such as wheelchair ramps and other home modifications. Tied in with that benefit are other forms of durable medical equipment, like hospital beds, oxygen equipment, blood sugar monitors, etc, as well as “non-skilled” services. Non-skilled refers to items that do not require a licensed doctor or nurse, such as aides who can assist with bathing and dressing or homemakers who can help with cleaning and cooking.

Non-Emergency Medical Transportation Coverage

CMS has also added the ability for MA plans to provide non-emergency transportation coverage, a service that several Medicaid plans provide. This benefit (if your plan covers it) will allow you to receive free or low-cost rides to medical appointments and pharmacies. In most cases, you can only qualify for this benefit if you do not have another adequate means of transportation. The appointment that you are requesting a ride to must be for a Medicare-covered service.

Telemedicine and Telehealth

MA plans can now provide coverage for telehealth. That means you can have live video interaction with your doctor through digital clinics like HealthTap, Teladoc, and MDLive. Telehealth can also include health alerts delivered to your phone, health education apps, electronic medical data transfers, mail-order prescriptions, digital appointment scheduling and exam reminders, and more.

New Enrollment Period (OEP)

Before 2019, most people were only able to switch into new Medicare Advantage plans during the Annual Enrollment Period in the fall. Now, if you already have a Medicare Advantage plan, you may be eligible to make a change during OEP. OEP, or the Open Enrollment Period, takes place from January 1 through March 31. During this time, you can switch from one Medicare Advantage plan to another or drop your Medicare Advantage plan in favor of Original Medicare (Part A and Part B only).

Future of Medicare Advantage Plans

According to the Henry J Kaiser Family Foundation, enrollment has tripled to 19 million beneficiaries since 2003 and continues to grow each year. CMS estimates that MA enrollment will hit an all-time high of 22.6 million beneficiaries in 2019 (an 11.5% increase)!

As enrollment continues to increase, plan selection and variety increase too, with approximately 600 new plans offered in 2019! 99% of seniors and Medicare-eligibles have access to a MA plan – and 91% can choose from 10 or more plan options. Beneficiaries will not only see more plans to choose from, but also new supplemental Medicare benefits!

Enroll in a Medicare Advantage Plan in 2020

Are you interested in getting coverage beyond Original Medicare? Along with the new benefits, many Medicare Advantage plans offer dental, hearing, and vision coverage.

Our agents at Medicare Plan Finder can contract with nearly every carrier in your state! This means that you can enroll in the MA plan that best fits your needs and budget.

The Annual Enrollment Period runs from October 15 through December 7. Start looking over your plan benefits now so that you’re ready to enroll before December 7!

Ready to learn more? Call us at 844-431-1832 or fill out this form to arrange a no-cost, no-obligation appointment with an agent in your area.

*This post was originally posted on November 8, 2018, and was last updated on October 4, 2019.

BREAKING NEWS: Tennessee SilverSneakers® Program Splits from YMCA

SilverSneakers® announced on Tuesday, September 17, that the Tennessee State Alliance of YMCAs decided to leave the SilverSneakers® network effective January 1, 2020, citing financial disagreement.

The alliance apologized, stating, “Seniors are a vital part of our membership, and we apologize for any inconvenience this decision may cause. Tennessee Ys are committed to continuing to serve seniors in our community.”

SilverSneakers® is a Medicare fitness program that allows eligible Medicare beneficiaries access to gyms, fitness centers, and classes. Many of these often take place within YMCAs, offering not only physical fitness benefits but also a social atmosphere.

Eligibility for the program is simple – anyone who is age 65 or older and has a private Medicare plan that includes the SilverSneakers® benefit can join.

Watch this brief video to learn more about Medicare fitness programs:

The news that SilverSneakers® may not cooperate with Tennessee YMCAs anymore may be detrimental to seniors who made use of that benefit. If you’re one of those people, what should you do next?

What to do if You’re Losing Your YMCA SilverSneakers® Benefit

If you have SilverSneakers® but are no longer going to be able to visit a YMCA with your membership, all hope is not lost! There are a few steps you can take:

Pay for your own senior YMCA membership ($59/month in Middle TN. Prices range based on location)

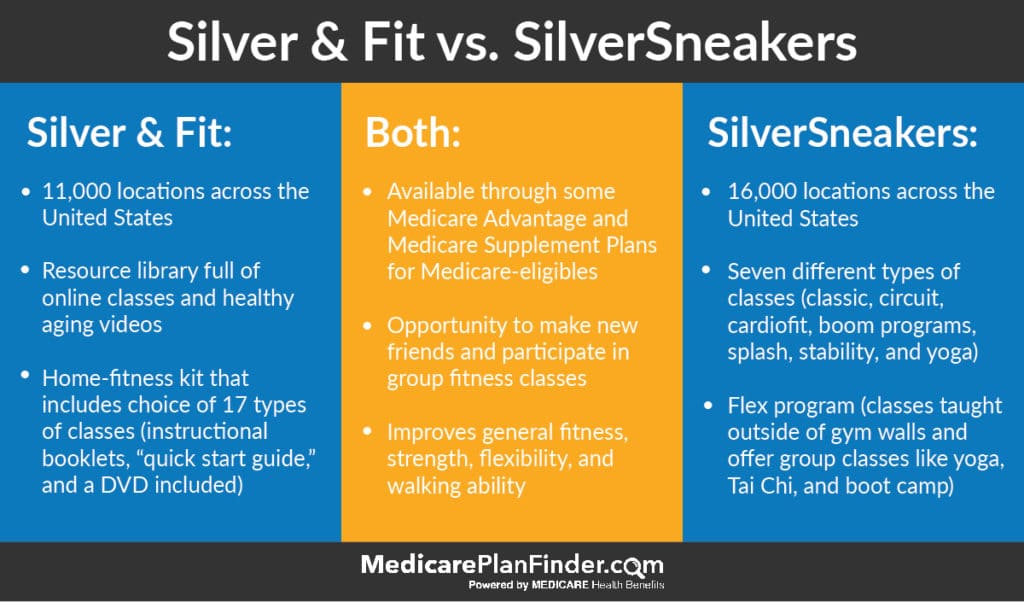

Find a plan that has Silver & Fit® instead (another Medicare fitness program that is very similar to SilverSneakers® but still works with YMCAs as of September 2019)

Silver & Fit vs. SilverSneakers

Other Gyms You can Visit with SilverSneakers ®

Tivity Healthcare, the company that operates the SilverSneakers® program, wants to make it clear that there are still over 350 facilities in the state of Tennessee that SilverSneakers® members can use. Planet Fitness, Gold’s Gym, Anytime Fitness, and Workout Anytime as well as a variety of community centers are still part of the SilverSneakers® network in Tennessee and may be a great option for you.

Planet Fitness

Planet Fitness locations across the state of Tennessee offer benefits like massages, tanning, and even discounts on travel and Reebok products. Most locations have long hours, and some are open 24-7. Many of them also have free WiFi!

Gold’s Gym

Gold’s gym locations offer group exercise classes, personal training, and more. Group exercise classes include Yoga, Zumba, Mixed Martial Arts, Group Cycle, and High-Intensity Interval Training.

Anytime Fitness

Different Anytime Fitness locations offer different equipment such as treadmills, ellipticals, cycles, stair climbers, rowing machines, weights, kettlebells, etc. They also offer different classes like Zumba, cardio, yoga, and additional services like tanning, private showers, wellness programs, and personal training.

Workout Anytime

Workout Anytime locations have high-quality equipment from Matrix Fitness, which has received rewards for innovation. They also have high-quality polypropylene, antimicrobial flooring that is beautiful, comfortable, and clean.

If you decide that you would rather stick to a YMCA membership and do not want to try out some of the other SilverSneakers® locations options, a licensed agent can help you find a plan that includes Silver & Fit® instead.

Silver & Fit® is similar to SilverSneakers® and includes a digital resource library, home fitness kits, community activities, and several different fitness classes at various fitness centers in Tennessee.

Silver & Fit® locations across major cities in Tennessee are listed below:

To find a plan that includes Silver & Fit®, call 844-431-1832 or send us a message. We’ll connect you with a licensed agent in your area who may be able to help you make the switch.

It’s perfectly natural to lose some mental “processing speed” as we age. This process is called cognitive aging and usually starts as soon as we reach adulthood. While certain brain functions like vocabulary might even improve as we get older, others will gradually decline. A common list of cognitive changes in elderly people typically includes slower problem solving, diminished spatial awareness, and a decline in perceptual speed and memory.

Most of these aging brain symptoms are entirely normal but the rate of this decline may increase, leading to MCI (mild cognitive impairment) or even dementia. However, scientific research has uncovered several methods proven to help maintain elderly brain health and most of them are simple things you can do in your day-to-day life!

Staying Active At Any Age

The connection between exercise and brain health for seniors has long been established. But new studies are suggesting that staying active may be the best way to prevent memory loss in old age! While it might be most effective before severe memory loss begins, it also appears to benefit those with advanced conditions like Alzheimer’s or vascular dementia.

Seniors who exercise regularly can experience reduced inflammation, improved blood flow, and even increased growth of new blood vessels in the brain. An active lifestyle can also improve the quality of sleep, which we will see later is another crucial factor in maintaining brain health. In fact, sustaining a moderate regimen of low impact exercises from six months to a year has even been associated with increased volume in the prefrontal and medial temporal cortices, the parts of the brain responsible for memory and critical thinking!

Medicare Fitness Programs

Unfortunately, the research also indicates that exercise must be a regular commitment in order to see some of these amazing benefits. But dedicating at least three hours a week can be difficult for seniors who don’t have access to a gym. This is where Medicare plans that include fitness programs can help. Plans can include Medicare fitness programs Programs like SilverSneakers® and Silver&Fit® that are designed specifically for seniors and can provide access to fitness and exercise centers. Some may supply their less mobile members with home fitness kits.

Many of us probably remember our mothers extolling the virtues of “brain food.” Turns out she was right! A diet consisting of mostly fruits, vegetables, nuts, beans, and fish has been closely linked to brain health and a lower risk of dementia. This “Mediterranean diet” is also often touted for its positive effects on heart health and cardiovascular risk factors, which can indirectly influence the health of the brain.

In addition to a more healthy diet, many seniors take supplements to get a higher dose of these crucial ingredients than can be found in the foods themselves. Some of the most popular include fish oils like omega-3 fatty acids, antioxidants such as resveratrol, as well as creatine and even caffeine.

Companies have begun producing memory supplements targeted at seniors. Some of these include:

Brainol (includes 19 ingredients for improved cognition, like B-Vitamins, Huperzine A, L-Theanine, and DMAE.

Neurofuse (includes B-Vitamins, L-Theanine, DMAE Bitartrate, and Huperzine A.)

Irwin Naturals Brain Awake (includes Vitamin B6 and L-Theanine)

BriteSmart (includes Huperzine A)

While memory supplements are not typically covered by Medicare, some Medicare Advantage plans might have an OTC (over the counter) allowance benefit which would allow you to purchase supplements. Click here to read more about OTC benefits in Medicare.

One of the easiest methods for seniors to maintain mental acuity is daily brain training. This interactive practice can take on many forms, from crossword puzzles to arts and crafts. And now more than ever, there are services and applications specifically designed to give you your daily dose of critical thinking.

Activities for Alzheimer’s Patients at Home

There are countless ways for seniors to get their brains engaged on a daily basis. Many are things you might already enjoy, including puzzles or card games. In the technological age, of course, many of these activities can be done on a computer or smartphone.

In addition to these traditional games, there are many apps that are designed specifically as activities for seniors with dementia and Alzheimer’s. Apps like Lumosity are great for challenging your brain on a daily basis and some, such as Mindmate, even include exercise and nutrition tips. A cursory Google search may also help you find other free brain games for seniors.

Some doctors suggest that one of the best ways to retain memory and cognitive functioning is to remain engaged with a social group. Many seniors use social media to stay in touch with family and friends and there are even apps like Timeless that are designed to help people with dementia or Alzheimer’s stay social.

Clear Your Mind (And The Rest Will Follow)

The importance of everyday factors like stress and sleep on brain health for seniors shouldn’t be overlooked, especially for the elderly. A good night’s sleep will clear the brain of toxins that accumulate throughout the day like beta-amyloid, a protein which is also commonly found in Alzheimer’s patients. Stress can also play a huge role in how the brain functions by introducing high levels of cortisol and even possibly reducing the size of the prefrontal cortex, the part of your brain that governs memory and learning.

Meditation and Aging

Meditation has been shown to increase the thickness of the hippocampus and decrease the volume of the amygdala, which is responsible for stress and anxiety. Research into mindfulness meditation has even indicated an effect on the process of aging itself. A 2017 UCLA study showed that the brains of people who meditate regularly actually declined at a slower rate than those who did not.

Natural Sleep Remedies For The Elderly

We know that sleep is essential for overall brain health for seniors, but many older adults experience trouble sleeping. Some practices for getting better sleep include turning off screens and lights, regular exercise, reducing sugar intake, and keeping a consistent sleep schedule with naps no longer than 20 minutes. If something more serious is causing you to lose sleep, you might need to consult a physician to test for sleep apnea or to evaluate any medications you might be taking.

Medicare Annual Wellness Visit

If the decline in cognitive functions persists or accelerates, you may need to seek professional help as a preventive measure. As part of your Medicare benefits, you may be entitled to a paid Annual Wellness Visit with your primary care provider to develop a personalized prevention plan that takes into account your lifestyle and risk factors.

In addition to checking physical factors like height, weight, and blood pressure, they can perform a cognitive assessment and screen for various forms of dementia or cognitive impairment. Additionally, a Special Needs Plan might be used to supplement your Medicare benefits. These plans are Medicare Advantage products specifically focused on providing care and coverage for patients with dementia.

Prescription Drug Plans for Alzheimer’s

If your condition or that of a loved one develops into Alzheimer’s or another form of dementia, Medicare Part D may cover the cost of prescription drugs to treat the symptoms. These medications include brands like Aricept and Exelon. Though they are not cures for the disease itself, they are effective at temporarily improving common symptoms of dementia, such as confusion or aggression.

Memory Care Through Medicare

Some severe cases of dementia and Alzheimer’s can make it nearly impossible to handle all the daily duties that come with living alone. In these cases, Medicare may help pay for nursing home care for a period of up to 100 days but will not cover such a solution in the long-term. However, some Medicare Part C plans may help cover the high costs of a nursing home or memory care facility.

For help enrolling in a Medicare plan that covers memory care and other brain health services, call us at 844-431-1832 or click here.

How to Choose the Best Type of Medicare Plan for You

When it’s time to choose a Medicare plan, it’s easy to get overwhelmed. There are quite a few different types of Medicare plans to choose from. Once you choose what type you want – you still have to choose a plan! Making the right choice is important because it may not be easy to change plans if you change your mind.

The Annual Enrollment Period (October 15 through December 7) is when anyone can make changes, and for some people, it’s the only time. If you make the wrong choice, you might have to wait a whole year before you can change again (unless you qualify for the OEP or have a SEP).

Which Types of Medicare Plans are Best for Me?

To figure out which Medicare plan is best for you, ask yourself the following questions:

What specific medical services do I need coverage for (ex: lab tests, blood work, surgery, chemotherapy, dental, etc.)?

How much room do I have in my budget? Am I able to pay a little more to have more benefits?

Would I rather pay more on a monthly basis and pay very little when I visit the doctor, or is it better to pay a small amount every month but risk having higher copayments?

Who are the doctors and other providers who I want to be covered in my plan?

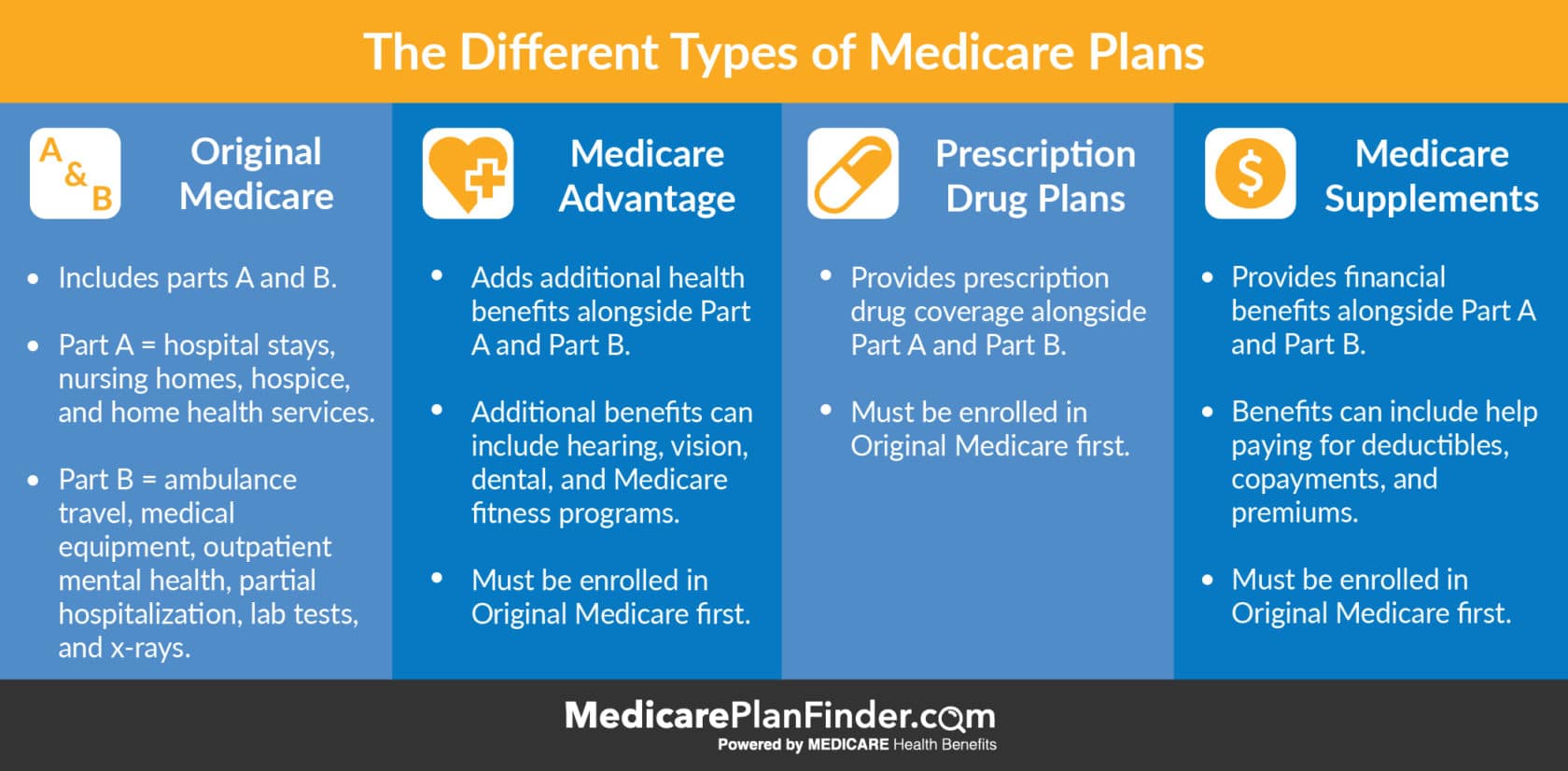

There are four main types of Medicare plans to consider when you begin your Medicare plan search. Start by comparing Original Medicare, Medicare Advantage, Prescription Drug Plans, and Medicare Supplements.

Keep in mind that you cannot have Medicare Advantage and a Prescription Drug Plan at the same time. You also cannot have Medicare Advantage and a Medicare Supplement plan at the same time.

Which plan or combination of plans works best for you?

Medicare Advantage: A private plan that you can purchase once you have Original Medicare. Can add additional benefits such as hearing, vision, dental, fitness, etc. Can include a prescription benefit.

Prescription Drug Plans: Another type of private plan that you can purchase once you have Original Medicare. Usually only includes a prescription benefit.

Medicare Supplements (Medigap): Another type of private plan that you can have in addition to Original Medicare. Adds more financial coverage, like for copayments and deductibles. This type of plan would also require you to have a stand alone part D drug plan.

Different Types of Medicare Plans

Choosing a Medicare Advantage Plan

So, did you decide to go with Medicare Advantage? Great! Now, there are a few types of Medicare Advantage plans that may be available for you. First, ask yourself whether or not you need a large network and whether the freedom to see any doctor is important to you. Then, read through these important differences:

HMO Plans (Health Maintenance Organization) – You’ll select one primary physician. In some cases, you may only receive coverage for that one doctor (unless he or she refers you to a specialist). Requirements may vary based on your plan.

HMO-POS Plans (Point-Of-Service) – You’ll select one primary physician, but you’ll have the freedom to visit any specialist in your network for your other needs. You will be charged a fee for visiting specialists.

PPO Plans (Preferred Provider Organization) – You can see any doctor, but your costs will usually be lower if you choose one that is in your network.

PFFS Plans (Private Fee-For-Service) – You will not need referrals or a primary physician, but you’ll have to pick a doctor that accepts your PFFS plan.

SNP (Special Needs Plans) – Designed for those who are eligible for both Medicare and Medicaid, live in a nursing home, or have a chronic illness or disability.

MSA (Medical Savings Account) – Works like a tax-free savings account for your medical bills. Medicare will deposit money into your HSA. You can use that account to pay for medical expenses.

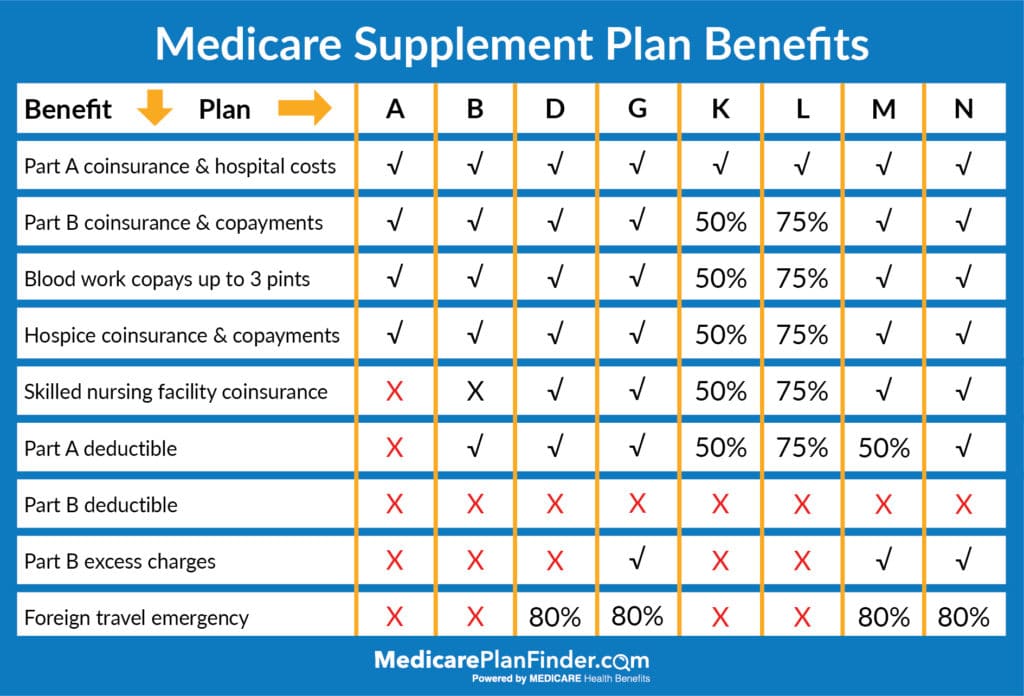

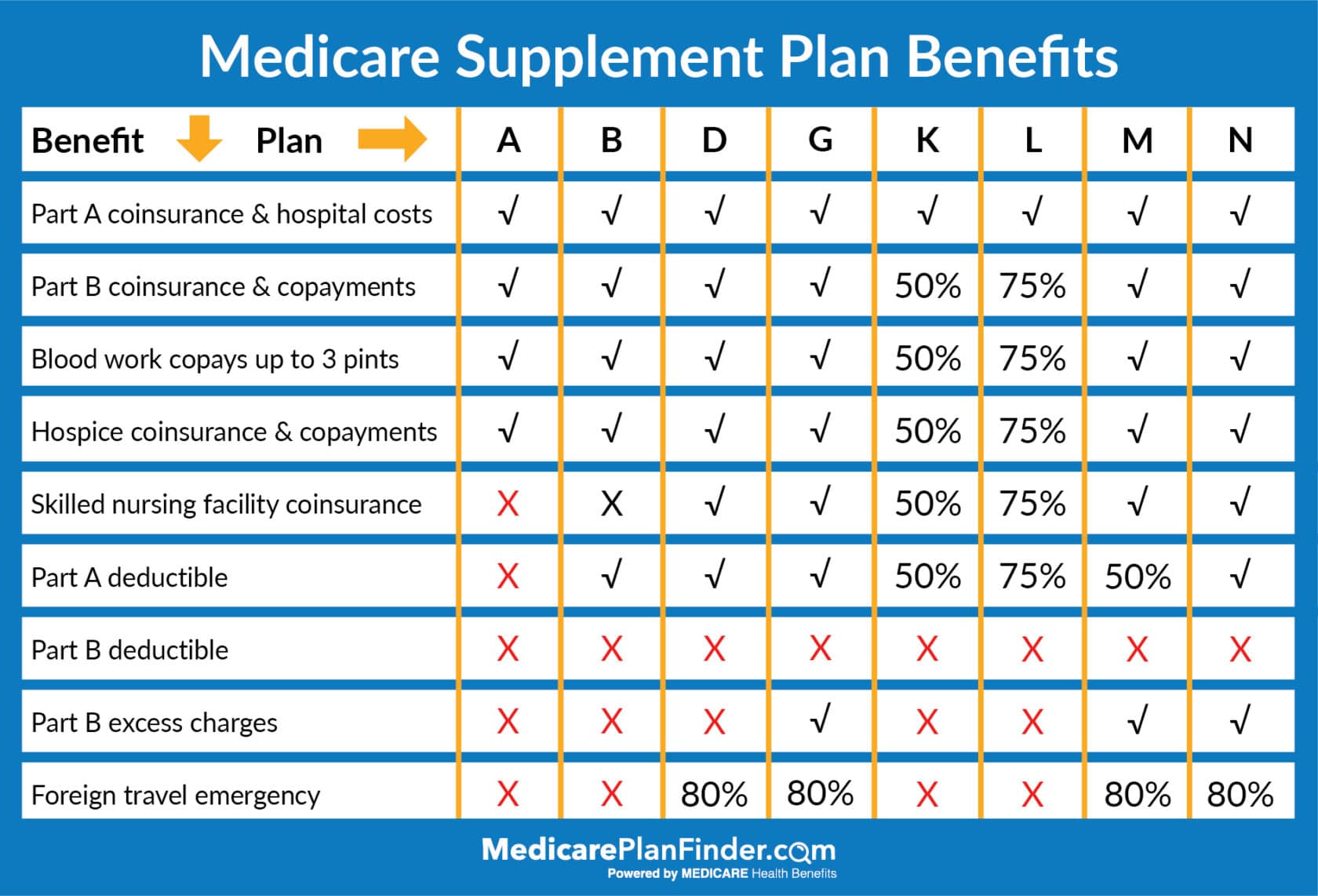

How do I Pick a Medicare Supplement Plan?

If you’ve decided that you want a Medicare Supplement plan, you’ll want to start by selecting the plan letter that corresponds with the coverage you need. Use the chart below for reference.

Once you’ve made that decision, you may have a few different carriers available in your area to choose from (some smaller cities may not have several options available).

Finding Medicare Plans in your area just got easier. Our Medicare Plan Finder tool can help you not only see what is available, but see which options may be best for your unique needs.

You can enroll by yourself, or you can meet with a licensed agent (for free) who can walk you through the process to make sure you don’t make any mistakes. The licensed agent can also talk to you about a variety of different types of plans in your area and answer all your questions.

This unbiased approach is a great way to get the help you need when selecting a Medicare plan.

To set up your free meeting with a Medicare Plan Finder licensed agent, call 833-567-3163 or click here.