More than 1.7 million Americans use hospice each year to maintain or improve their quality of life due to a terminal illness. Hospice care plans address physical, emotional, and spiritual pain and offer support to caregivers during the grieving process.

Hospice decisions can take an emotional and financial toll on you and your family, so you may be asking… “Does Medicare cover hospice?”

How does Medicare cover hospice care?

If you are enrolled in Medicare Part A (hospital insurance), you may qualify for hospice care. However, you must meet the following criteria:

Your doctor certifies that you are terminally ill (with a life expectancy of less than 6 months)

You accept palliative care (for comfort) rather than try to cure your condition

You sign an agreement choosing hospice care over other Medicare-covered benefits to treat your illness

You are not eligible if you had already made a hospice election or have not previously received pre-election hospice services (evaluation of your need for pain and symptom management).

If you meet the above criteria, the following services may be part of your hospice care plan and are covered in part by Medicare:

Other services focused on pain and symptom management

There may be a co-payment of $5 for your prescription drugs or other pain relief. You may also need to pay five percent of the Medicare-approved amount for respite care. However, the following services are not covered by Medicare:

Hospice is intended for people who have six months or less to live. To receive hospice care, you can not receive curative treatment.

If you decide to receive treatment, your hospice care is no longer covered. However, you can withdraw from your hospice care at any given point, and you can resume treatment as long as you are still eligible.

Prescription Drugs Intended to Cure

Just like you can’t pursue curative treatment, you can not take prescription drugs that are intended to cure your illness when receiving hospice care. Hospice only covers drugs that are intended for pain relief and control.

Care for Any Hospice Provider That Wasn’t Arranged by the Hospice Team

You are only eligible to receive care from the hospice team that you initially select.

You cannot get hospice coverage from a different provider unless you go through the switching process. However, you can still visit your regular doctor if they have been appointed to supervise your hospice care plan.

You can only switch to a different hospice provider once per benefit period. If you are interested in switching, be sure to do your research and pick a hospice team you feel comfortable with.

Does Medicare cover hospice room and board?

Medicare does not cover room and board regardless if you live at home, in a nursing home or inpatient assisted living facility, or inpatient hospice office. The only exception is during short-term inpatient or respite care stays in which Medicare will help cover the costs.

Emergency Care

Emergency transportation is not covered by Medicare’s hospice benefits. Medicare will not cover emergency inpatient hospital care unless they are arranged by your hospice team or unrelated to your terminal illness.

Does Medicare cover hospice in a nursing home or at home?

If you are eligible, Medicare will cover hospice care regardless if you receive the care in your home, nursing home, or inpatient facility. Some nursing homes work directly with a hospice team. In a nursing home setting, your hospice team can help with the following:

Regular visits to the nursing home

Consultations by specialized hospice physician as needed

Pain and medication management

Educating staff on symptoms, medications, and care

Emotional and spiritual support

Coordinating care across all patient’s medical providers including doctors, hospice team, and nursing home staff

How long will Medicare pay for hospice care?

Hospice care is intended for people who have less than an estimated six months to live. If you still require hospice care after six months, you can continue to receive benefits if a hospice doctor recertifies your terminal illness in a face-to-face meeting.

You can get hospice care for two 90-day benefit periods followed by an unlimited number of 60-day benefit periods.

Level One: This level includes basic care under Medicare’s hospice benefit. Services include nursing services, medical equipment & supplies, and medications.

Level Two: Medicare designates people who need continuous care such as home health care. The home health aide stays in the patient’s home for eight to 24 hours a day, but it’s short-term care. The patient’s needs are re-evaluated once every 24 hours.

Level Three: The third level of Medicare hospice coverage is general inpatient care. Some people have short-term symptoms that are so severe that they can’t get adequate treatment at home. With level three care, the patient has 24-hour care available.

Level Four: This level of care is more for the family than the patient. If the patient doesn’t meet the criteria for inpatient care and the family needs a break from daily care duties, respite care may be an option. Respite care provides caregivers temporary relief by admitting the patient to a hospital.

Medicare Palliative Care vs. Medicare Hospice Care Coverage

Medicare can cover palliative care for helping relieve symptoms in accordance with curative care. Some organizations define palliative care as “specialized medical care for people living with a serious illness” with the focus of care being symptom relief rather than to find a cure.

The difference between palliative care and hospice care is that palliative care can occur in conjunction with curative care.

Medicare may cover palliative care, but not under the Medicare hospice benefit.

Hospice and Medicare Supplements

Medicare Supplements can help cover the gaps in hospice care that Original Medicare may not, like prescription drugs for pain relief and respite care. After your Medicare coverage, you will likely be responsible for five percent of your total respite care costs and a $5 copay per prescription drug. Medicare Supplements can cover some, or all, of these gaps.

Medicare Supplement Plans A, B, D, G, M, N cover 100 percent of hospice coinsurance and copayments. Medigap Plan K covers 50 percent and Plan L covers 75 percent.

If you are interested in enrolling in a Medicare Supplement plan, or have questions on how these plans work with your correct coverage, click here to get in contact with a licensed agent.

2020 Medicare Supplement Comparison Chart

Hospice and Medicare Advantage

If you enroll in a Medicare Advantage plan, you will have the same hospice care coverage as with Original Medicare. However, Medicare Advantage plans can offer extra benefits like vision, hearing, and dental coverage. They may also offer fitness programs like SilverSneakers®.

If you are interested in enrolling in a Medicare Advantage plan, fill out this form, or give us a call at 844-431-1832. There is no cost to you to meet with one of our agents and there is never an obligation to enroll.

This post was originally published on April 16, 2019, and updated on November 18, 2019.

Retirement and Medicare Eligibility

What happens to your health insurance when you retire? Medicare and retirement can seem intimidating, but we’re here to ease some of your concerns and answer your questions.

There are currently an estimated 70 billion baby boomers who are nearing retirement. Planning for retirement is crucial to living a comfortable and healthy life. An annual estimate by Fidelity shows the average couple retiring at age 65 will need $280,000 to cover health-related costs. Fortunately, Medicare can help, but there is a set of guidelines and regulations regarding enrollment.

How Medicare and Retiree Coverage Work Together

Some employers may offer retiree health coverage, which can be a good option if you are not yet 65 and do not meet other Medicare eligibility requirements. If you are 65, it may be time to enroll in Medicare.

If you are already 65 when you retire and are interested in having both retiree coverage from your employer AND Medicare, the two can work together.

Your Medicare coverage will always come first. Your retiree coverage will work as extra coverage to backup your Medicare plan – kind of like a Medicare Supplement plan.

While retiree coverage is not a Medicare Supplement plan, it is very similar. It can cover things like copayments and deductibles, or even extra hospital stay days. All retiree plans are different, though, so look over your plan and call your insurance agent (or your former HR representative) to find out what it covers.

Do Retirees have to Pay for Medicare?

There are two parts to Original Medicare – Part A and B. If you have worked and paid Medicare taxes for at least 40 quarters (about 10 years), you can have premium-free Part A. If you did not work the 40 quarter minimum, then you will have to pay the Part A premium. For 2020, the Part A premium is $458 for 30+ quarters or $252 for 30-39 quarters.

The standard Part B premium for 2020 is $144.60, but you may pay more or less based on your own set of circumstances. An estimated 3.5% of beneficiaries will have a lower premium due to the Social Security “hold harmless” provision which prevents premiums from exceeding Social Security benefits. Plus, if you make more than $87,000 a year, your monthly Part B premium will be adjusted based on your income. The income-based 2019 Part B premiums are as follows:

2020 Medicare Part B Premiums

Do you Automatically get Medicare When you Turn 65?

If you currently receive Social Security benefits, you will be automatically enrolled in Medicare Parts A and B the month you turn 65. However, if you do not receive Social Security benefits, you will need to enroll yourself. Medicare enrollment begins three months before your 65th birthday and will end three months after. This is called your initial enrollment period.

It’s important to act right away because delaying your enrollment can result in a 10% Part B premium increase for every year you’re eligible but don’t enroll. If you don’t select prescription drug coverage and later enroll, you may have a penalty of 1% the national base Medicare Part D monthly premium for each month you were not enrolled.

Health Insurance After Retirement Before Medicare (Early Retirement)

Should you keep working or retire early? Your decision may be influenced by your age, health, budget, Medicare eligibility, social security benefits, and employer coverage.

Employer Retiree Coverage

Some employers offer retiree coverage after you leave the company. However, retiree coverage and Medicare are not the same. Retiree coverage is health coverage that is provided to former employees of a company. This typically pays second to Medicare, which means you still need to enroll in Medicare to be fully covered. However, retiree coverage can help with health-related expenses if you retire before 65.

Not every employer offers retiree coverage. Since it isn’t required, your employer (or former employer) can cancel or change your retiree plan at any time. It’s safest for you to have Medicare as well. Plus, if you don’t enroll in Medicare when you first become eligible, you will face a penalty fee. Some retiree plans automatically stop when you turn 65 and become eligible for Medicare.

If your employer does not offer retiree coverage, retiring or losing your job gives you a SEP. A Special Enrollment Period means that you don’t have to wait for AEP, the Annual Enrollment Period, to buy coverage. You will have 60 days from your last day of work to enroll in a marketplace health plan. After those 60 days are over, you’ll have to wait until AEP (October 15 – December 7) to buy a marketplace plan, at which point you will be charged a penalty fee for having a lapse in coverage.

FERS/CSRS Retirement and Medicare

The CSRS, or Civil Service Retirement Act, became effective on August 1, 1920. It was replaced by the Federal Employees Retirement System (FERS) on January 1, 1987. Some people may still belong to CSRS. Both programs are for government employees only.

Both FERS and CSRS allow you to retire at age 62 if you have five or more years of service or at age 60 if you have 20 or more years of experience. Under FERS, you can retire between ages 55 and 57 (depending on your birth year) if you have 30 or more years of service.

Regardless of your FERS or CSRS status, if you’re 65, you’ll qualify for Medicare. You’ll also qualify for Medicare if you have a qualifying disability. If you are under 65 and do not qualify for Medicare, you can receive your FERS or CSRS benefits but will have to wait until you reach Medicare qualifying age.

Until then, you may qualify for the Federal Employees Health Benefits Program (FEHB). Once you do become eligible for Medicare, you may want to enroll in Part A anyway because there is no premium if you’ve worked for at least 40 quarters.

COBRA

When you leave your job, you’ll also have the option to enroll in COBRA. COBRA allows you to continue to belong to your employer’s group plan for a temporary period after you leave the company. The company can “kick you off” at any time, so this is not a permanent option. However, COBRA can help you out while you figure out what your other options are.

Ask your employer or your HR representative to find out what COBRA might look like for you.

Can you get Medicare at age 62?

It’s important to understand the differences between Social Security and Medicare. You can start to receive Social Security retirement benefits at the age of 62. This amount is typically reduced until you reach the age of 65. The average person does not qualify for Medicare until age 65, but there are exceptions.

You are automatically enrolled in Medicare once you have received Social Security benefits for two consecutive years. This means if you started receiving benefits at age 62, you will qualify for Medicare at age 64. Plus, you may qualify for Medicare before 65 if you have Lou Gehrig’s Disease (ALS) or End-Stage Renal Disease.

Importance of PlanningforRetirement

It’s never too early to start planning for retirement and Medicare. Our licensed agents can help explain your coverage options and answer all of your questions. Plus, they can provide bias-free assistance with a wide range of plan options because they are licensed with all major carriers in your state. Start planning now! Call us at 844-431-1832 or fill out this form to arrange a no-cost, no-obligation appointment.

This post was originally published on December 27, 2018, and was last updated on November 15, 2019.

How to Get Paid to be a Caregiver for Parents

There are close to 34 million Americans providing care for their parents, and many are not compensated for their time. The value that caregivers provide for “free” is estimated to reach $375 billion annually. That’s double the amount of what is actually spent on homecare services.

Being a caregiver is rewarding, but it comes at a cost. The average caregiver spends 20 hours a week caring for their loved ones and spends an average of $5,500 each year out-of-pocket.

At Medicare Plan Finder, we know how hard you work and how much you deserve financial support, and we want to help you understand how to get paid to be a caregiver for parents.

Can Caregivers Get Paid by Medicare?

Currently, Medicare does not pay caregivers. However, some state Medicaid programs do pay family members to provide care.

Medicaid Caregiver Compensation

Medicaid caregiver pay varies per state, but all states (and the District of Columbia) offer Medicaid waivers that allow qualified individuals to manage their own care. This means your parent can hire and fire their own caregivers. Certain states will permit a family member to be hired to provide the care.

The eligibility, benefits, coverage, and rules will vary depending on which state you live in. Some may pay for family caregivers but exclude spouses or in-laws. Others may only provide compensation if you do not live in the same house as the person in your care.

When you are researching programs in your state, be conscious of program names. Each state will have a different name (Self-Directed Care, In-Home Supportive Services, etc.).

To start the process, your parent(s) must qualify for Medicaid and meet state caregiver qualifications. Contact your state Medicaid office to start the application and learn about eligibility.

Your parent(s) will be assessed for risks, needs, strengths, and capacities that meet the requirements by the Centers for Medicare and Medicaid Services (CMS).

You and your parent(s) will write a service plan that details the type of daily assistance that will be provided. This can include bathing, dressing, meal preparation, feeding, laundry, driving, and other daily tasks. When this plan is set, you will be approved or denied for the state’s Medicaid compensation program.

Getting Paid to Be a Caregiver for Veterans

If your parent is a veteran, they may qualify for the Veteran Directed Home & Community Based Care program. This program is available in 37 states and the District of Columbia. It provides several medical benefits to people who need a high level of nursing facility care, but want to live at home with a caregiver.

The average monthly allowance is $2,500. The veteran will choose the caregiver. This can be a family member, including spouses, siblings, or children/grandchildren.

Another program that can help provide financial compensation is Aid and Attendance (A&A). This program provides benefits to veterans who qualify for a VA pension and have served at least 90 days in active duty and one day during a wartime period.

The program is intended to supplement the pension and help cover the cost of a caregiver. The caregiver can be any family member.

To qualify for A&A, at least one of the following must apply:

Confined to bed due to a disability

Be in a nursing home due to physical or mental limitations

Have limited eyesight (Corrected 5/200 visual acuity or less in both eyes)

Require the aid of another person to assist with daily living activities (bathing, dressing, feeding, etc.)

Long-Term Care Insurance and Caregivers

Long-term care insurance is a policy that helps cover the cost of long-term care. These costs can include assisted living, nursing homes, or in-home care (including caregivers). Plan benefits will vary, but if home care coverage is included in the plan, homecare caregivers may be covered as well.

However, it is important to note that all plans are different, and some plans may exclude these benefits. Additionally, some plans may have restrictions on who qualifies to be a paid caregiver. Some plans may exclude spouses or in-laws, and others may exclude family members altogether.

Other Paid Family Caregiver Options

If your parent does not qualify for any of the above programs, don’t worry! There are other ways to get some type of compensation. The following are round-about ways that explain how to get paid to be a caregiver for parents:

Tax Deductions: It may not be the same as a monthly paycheck, but tax deductions can help you save money each year for certain expenses you incur. You may be able to write off certain expenses like dental costs, medical costs, home modifications, and transportation costs.

Payment From a Family Member: Asking for payment from your parents or another family member may be awkward or uncomfortable. Put all of these feelings aside and discuss needs, wages, schedule, etc. Create a contract that includes the wage and services provided.

Area Agencies on Aging: Each state has a local Area Agency on Aging. You can find your closest office by searching your city in their directory tool. The staff at each location can help you find additional programs that you or your loved one qualify.

Paid Leave: If your parent’s needs are short-term, you may be eligible for a paid leave through your employer. This is not guaranteed, but there is no harm in talking to your HR representative to see what type of paid leave policies are offered by your company. Something as small as a few weeks of pay can still provide a financial cushion and allow you to go back to work in the future.

Remote Work: Paid leave can only help for a short time, and may not be the best solution for you and your family. Talk to your employer and see if telecommuting is an option. Again, each company will vary, but there is no harm in asking. Working full-time and acting as a caregiver can be difficult, so consider your workload when making these decisions and having these conversations.

Caregiver Support and Power of Attorney

There’s no doubting the weight that caring for a loved one can put on your shoulders. If you’re a caregiver, it’s crucial you feel supported so you can continue to help your loved one on a daily basis.

Medicare Plan Finder’s Caregiver Support page provides caregiver information specific to your loved one’s needs. Learn about how you can receive support for yourself while caring for your loved one, stress relief tips, support groups you can join, and Power of Attorney (POA) information.

Being a caregiver does not automatically grant you the ability to make certain medical, legal, or financial decisions on behalf of your parent. To do so, you will need to become their Power of Attorney.

If your parent is mentally competent, they can sign their rights over to you. If they are not, you will need to go before a judge and have their rights granted to you.

Medicare Coverage and Caregivers

As a caregiver, one of your biggest concerns, among understanding how to get paid to be a caregiver for parents, may be making sure your loved one has the best possible health plan for their unique needs and budget. At Medicare Plan Finder, we want to help make that happen!

We specialize in educating seniors on Medicare Advantage, Medicare Supplements, and Part D plans. Our licensed agents are contracted with all of the major carriers so you know your parent is being shown the best plans at the best price. Give us a call at 844-431-1832 or click here to get in contact with an agent.

This post was originally published on May 30, 2019, and updated on October 23, 2019.

Fall Prevention: Tips, Tricks, and Exercises

According to the Centers for Disease Control and Prevention, falls are the leading cause of injury and death in older adults. Falls can occur at any time and can range in severity.

Seniors and Medicare eligibles can suffer from significant injuries or pain. The average hospital cost for a fall injury can exceed $30,000. Fall prevention is important to help lower the risk of falling and potential injuries.

Preventing Falls at Home

According to the Department of Health and Human Services (HHS), the majority of falls (60 percent!) occur in the home. Something as minor as a slippery spot on the floor or an electrical cord out of place can have devastating consequences.

Thankfully, there are several steps you can take to help reduce the risk of falling. The following are quick and easy suggestions that can give you a greater sense of security in your home:

Eliminate Clutter

If you have clutter in narrow or close areas, like hallways or staircases, you can easily trip or lose your balance. One of the easiest steps you can take is keeping your home clean and tidy by eliminating clutter and keeping your pathways clear.

Remove Hazards

Every room in your home should be free of tripping hazards. These hazards can include loose carpet, slippery rugs, damaged wood floorboards, etc. You should examine your home for these hazards and if you find one, remove or repair it. It is better to opt for carpet over hardwoods if possible.

Install Handrails

Woman Using Grab Bar

Grab bars and handrails can help to lower your risk of falling, especially in the bathroom. Install handrails near the toilet and bathtub and in hallways and stairwells. If you are unable to install these yourself, contact a handyman or a family member.

Wear Properly Fitting Clothes

Everyone wants to be comfortable and able to relax in their home, but did you know that baggy clothes can make you more likely to fall? Wear clothes that are the proper length, and avoid wearing anything that drags on the floor.

Wear shoes or non-slip slippers when possible. Socks can be slippery and increase your risk of falling. Non-slip socks are great alternatives that help maintain comfort and lower your risk of falling.

Create Light

It’s important that your home is well lit so you can see where you are walking. Install brighter light bulbs in dark, high-risk falling areas like hallways or stairwells. Plus, night-lights in bathrooms or hallways can help you see during any time of the night.

Preventing Falls in Hospitals

If you are in a hospital for any given reason, there is a risk of falling, especially if you are staying long-term. If you need to get up or go to the bathroom, use the call light or ask the nurse for help.

Some medicines can make you feel sleepy or dizzy, so when you are getting up, move slowly. Be sure to wear your glasses or hearing aids when you are up and moving around.

Plus, use a walker or cane because bedside tables, IV poles, and other objects cannot provide the proper support. Lastly, if you have any concerns about your safety, be sure to alert the nursing staff.

How Can Seniors Prevent Falls?

Fall Prevention Exercise – Medicare Plan Finder

Exercising is a great way to increase your balance and help lower your risk of falling. These exercises can help strengthen your muscles, and when completed regularly, improve your muscles and joints. The following are great exercises that help prevent falls:

Chair Sit to Stand

Find a sturdy chair with arms. Practice getting in and out of the chair and focus on utilizing your leg muscles. Use the arms of the chair to help you get up, but as you improve, try using only one hand. Aim for 10 repetitions.

Marching in Place

Have a chair nearby in case you lose your balance. Practice marching in place, but bring your knees as high as you can. Use your muscles instead of your momentum. Aim for 10 knee raises on each leg.

Balance on One Leg

Find a sturdy surface like a chair or countertop. Use these surfaces for support. Raise one leg and try to find your balance while standing on the other. Aim for 10-15 seconds per leg.

Toe to Heel

Hold onto a chair or countertop. Raise up onto the balls of your feet and hold for a few seconds, then relax into a normal stance. Next, rock back on your heels and hold for a few seconds. Aim for ten repetitions.

Injuries and Complications

As we mentioned above, falls are the leading cause of injury and death in older adults. Did you know one out of five falls will result in a serious injury such as a broken bone or head injury?

These injuries can make living your day-to-day life difficult. Plus, if you have vitamin d deficiency or take certain medications like sedatives or antidepressants, your risk of falling increases. Common injuries from falling include:

Head injuries

Hip fractures

Back and spinal injuries

Shoulder injuries

Torn ligaments, tendons, and muscles

Neck injuries

What to Do If You Fall

In the unfortunate incident you do fall and you live alone, you may consider buying a medical alert system to contact emergency personnel. A medical alert system is a device that you wear that features a button you can push to call for help. The systems usually come with monthly fees, but Life Alert and other medical alert devices can help provide peace of mind.

You can also keep a cordless phone or smartphone with you at all times, so you can call for help if you fall.

Another option is wearing a smartwatch. According to NPR, the Apple Watch can detect when a user has fallen, and the device will generate a notification to emergency personnel. If you don’t respond for more than a minute after the alert, the watch can automatically call for help and send “a message with location to emergency contacts.”

Does Medicare Cover Fall Injuries?

Medicare generally covers most expenses if you have a fall. If you are admitted to a hospital from your injuries, Part A may cover this expense or any necessary treatments.

Your Part A deductible and coinsurance may apply after 60 days. If you go to an emergency room, doctor’s office, or clinic due to a fall, Part B generally covers these expenses. Similar to Part A, your deductible, coinsurance, or copay payment amounts may apply.

Fall prevention is one of many ways to remain proactive and practice a healthy lifestyle. Medicare Advantage plans can offer even more benefits and coverage that help you become the healthiest version of you. Many MA plans offer hearing, dental, and vision coverage, and some even offer group fitness classes like SilverSneakers®.

If you are interested in arranging a free, no-obligation appointment with a top agent, call us at 844-431-1832 or fill out this form.

*This post was originally published on November 13, 2018. Last Updated on October 18, 2019.

2019 Medicare Donut Hole: Part D Changes and Costs

According to the Henry J Kaiser Family Foundation (KFF), 43 million Medicare beneficiaries are enrolled in a Part D plan. This accounts for 72% of Medicare beneficiaries nationwide!

Medicare Part D started in 2006, and back then, you were required to pay 100% of the costs for brand name drugs. That percentage has lowered over the years, and better yet, 2020 brings super exciting news regarding the Medicare Part D donut hole.

How Does the Medicare Part D Donut Hole Work in 2019?

The Medicare donut hole is a gap in your Part D plan that starts after you’ve spent your deductible ($415 or less) and exceeded the initial coverage limit ($3,820) in total out-of-pocket costs.

You are in the gap until you reach the annual out-of-pocket threshold ($5,100). During this time, you are required to pay more for your prescriptions. This encourages you to choose generic options whenever possible.

Once you pass the donut hole and reach the catastrophic coverage period, you only have to pay 5% of all drug costs for the remainder of the year.

How Much Is the Donut Hole in 2019?

In 2019, you will pay 25% of brand-name drugs in the donut hole. This is the same as what you would pay before you enter the donut hole, meaning the Medicare donut hole is completely closed for brand-name drugs.

However, you will be responsible for up to 37% of generic drug costs in 2019. The plan is for this to decrease to a max of 25% in 2020, effectively closing the donut hole. Other Medicare donut hole 2019 costs include:

Initial Deductible: increasing by $10 ($405 to $415)

Initial Coverage Limit: increasing by $70 ($3,750 to $3,820)

Out-of-Pocket Threshold: increasing by $100 ($5,000 to $5,100)

In 2019, you’ll know if you’re in the donut hole based on your “EOB” notice. The EOB is an “Explanation of Benefits.” If you have a Part D plan, you should be receiving this every month.

The notice will tell you how much you’ve spent for the year on covered drugs and whether or not you’ve reached the coverage gap. Some people may never reach it – it depends on how much you’re spending on your prescriptions.

What Drugs are Covered in the Hole?

Your “formulary” does not change when you’re in the donut hole. The drugs that are listed on your formulary are the drugs that you can receive coverage for.

When Is the Donut Hole Going Away in 2020?

The Medicare Part D donut hole is scheduled to close completely in January 2020. Thanks to the Bipartisan Budget Act of 2018, the gap has closed a whole year ahead of schedule. However, the gap is only closing for brand-name drugs.

The gap for generic drugs will decrease, but will not be completely eliminated until 2020. This is great news for beneficiaries like you because generic drugs already have a lower price point – it’s the brand-name drugs that typically cause hardship in the donut hole.

What Will My Part D Costs Be in 2020?

The standard Part D deductible is $435 in 2020. After you meet the deductible, you’ll pay 25% of both brand name and generic drug prices.

Once you pay $4,020 out-of-pocket, you’ll still only pay 25% of your prescription drug costs, instead of entering the donut hole.

After you pay $6,350, you enter Catastrophic Coverage, and you’ll pay 5% of your prescription costs.

Medicare Pharmacist | Medicare Donut Hole 2020

What Are Your Medicare Part D Donut Hole Coverage Options?

Original Medicare (Part A and B) does not cover prescription drugs. If you are looking for prescription drug coverage, you have two options. You can enroll in either a Medicare Advantage or Part D plan.

If you are exclusively looking for prescription drug coverage, Part D may be right for you. If you are looking for prescription coverage along with other benefits like hearing, dental, or vision coverage, a Medicare Advantage plan is probably best for you.

Trying to decide between Medicare Advantage or a Part D plan can be difficult. Our licensed agents can help you enroll in the plan that best fits your unique needs and budget.

They can answer any questions or concerns you may have. Plus, our agents are contracted with most major carriers in your state, so there is no bias when we help you select a plan. If you’re interested in arranging a no-cost, no-obligation appointment, call us at 844-431-1832 or contact us here.

This post was originally published on January 10, 2019, and updated on October 16, 2019.

Does Medicare Cover Acupuncture in 2020?

East Asian countries have practiced acupuncture for centuries, but it has only been popular in the United States since the 1970s.

Today, more than 10 million acupuncture treatments are administered each year in the U.S – but is acupuncture covered by insurance? The practice is still often considered “alternative,” with some doctors wondering if acupuncture may be no more than a placebo effect. For that reason, there are lots of insurance policies that do not cover acupuncture.

Acupuncture is becoming increasingly popular among seniors because treatments can help reduce the effects of aging (such as stress, back pain, neck tension, and joint pain). However, your out-of-pocket costs can add up quickly, so you may be wondering…does Medicare cover acupuncture?

Does Medicare Cover Acupuncture for Pain? | Medicare Plan Finder

When does Medicare cover acupuncture?

You might be surprised to learn that starting in 2020, Medicare does cover acupuncture for qualified beneficiaries who experience chronic lower back pain. By definition, chronic lower back pain is pain that is not associated with surgery or disease and lasts for at least 12 weeks. If your doctor doesn’t recommend acupuncture or diagnose you with chronic pain, you might not qualify. Talk to your doctor to find out if acupuncture may be an option for you.

Does Medicare Part B pay for acupuncture?

Before 2020, acupuncture was not covered by Medicare because it was not considered medically necessary (and was considered a form of holistic or alternative medicine, which is traditionally not covered). It was added to Medicare Part B in 2020 as a part of the wider effort to reduce the opioid crisis in America. CMS (Centers for Medicare and Medicaid Services) decided that it was necessary to provide pain management alternatives, and acupuncture made the list.

Medicare Part B will cover up to 12 treatments within 90 days for chronic lower back pain. If the treatments are effective, you can receive an additional eight covered sessions. There is a limit of 20 treatments per year. Your treatments must come from a doctor with a degree in acupuncture or Oriental Medicine from an accredited school. The doctor must be licensed and unrestricted in your state.

Do Medicare Supplements Cover Acupuncture?

Medicare supplemental insurance for acupuncture may be a good idea, depending on your other health conditions. Medicare supplement plans do not provide additional health benefits (like acupuncture), but they provide additional financial support for all your healthcare needs.

For example, Medicare Supplement Plan G will cover your Part B coinsurance and copayments. Since Part B covers acupuncture, if you have Plan G, you won’t have to pay any coinsurance or copayments for your acupuncture services. That means that while Medicare Supplements usually don’t directly cover acupuncture, they can help you pay for your treatments.

Do Medicare Advantage Plans Cover Acupuncture?

Since Original Medicare did not cover acupuncture before 2020, private insurers sometimes included acupuncture and chiropractic treatments in their Medicare Advantage plans. Even though Part B now covers acupuncture treatments, you might still find a Medicare Advantage plan helpful.

There is currently a yearly maximum of 20 treatments for Medicare Part B acupuncture coverage. Some Medicare Advantage plans might offer coverage for additional treatments. Additionally, Medicare Advantage plans that include prescription drug coverage can help you out with pain medications and whatever other prescriptions you need to make up for the lack of acupuncture coverage.

Aside from acupuncture and pain relief benefits, Medicare Advantage plans often include additional benefits like dental, hearing, vision, and even physical fitness.

MSAs are different from other types of Medicare Advantage plans in that they typically do not cover prescription drugs. However, some Medicare MSA plans cover acupuncture.

This is an excellent option if you are healthy, not taking expensive prescriptions, and are more worried about cost savings than receiving additional health benefits.

When did Medicare start covering acupuncture?

Medicare began covering acupuncture in January of 2020. The Centers for Medicare & Medicaid Services (CMS) released a memo on January 21, 2020, announcing this change. Alex Azar, the Department of Health and Human Services Secretary, said, “Expanding options for pain treatment is a key piece of the Trump Administrations’ strategy for defeating our country’s opioid crisis.”

The whole point of providing acupuncture coverage is to offer a range of treatment options so that Americans (seniors in particular) who are experiencing severe pain don’t always have to resort to opioids.

Does Medicare Cover Other Naturopathic Treatments?

Naturopathy, or naturopathic medicine, is based on folk medicine and vitalism instead of traditional western medicine. It uses natural healing methods and promotes self-healing. Some might also call this “holistic” medicine.

Medicare typically does not cover any form of alternative medicine like naturopathy.One great example is chiropractic care. Medicare will only cover chiropractic services for medically necessary spinal manipulation when provided by a qualified chiropractor. Chiropractic services for massage therapy or pain treatment will not be covered.

How Much Does Acupuncture Cost?

According to Acufinder, an acupuncture referral service, you can expect to pay anywhere from $60 to $120 per service. Your rate can depend on where you are located. If you use a licensed acupuncturist and receive Medicare Part B coverage, you can expect to pay 20% of the fee, so you might only owe $12 to $24 per service. If you surpass the Medicare Part B limit of 20 treatments per year, or if you have not yet met your Part B deductible, you will have to pay full price. Once you meet the deductible ($144.60 in 2020), you can get your 80% coverage of acupuncture services.

Benefits of Acupuncture

Acupuncture is a unique and safe alternative to opioids for pain management. It works by inserting fine, sterile needles into the skin to stimulate very specific points (called acupoints).

The practice of acupuncture began in China thousands of years ago. The ancient Chinese believed that human bodies were filled with a force called “qi,” pronounced “chee,” and that when your “qi” was blocked, you would feel ill. Acupuncture was created to help humans achieve qi balance.

Studies have proven that even if there is no evidence of qi, we do know that acupuncture reduces chronic pain. Some doctors believe that acupuncture can also reduce the effects of allergies, anxiety and depression, insomnia, migraines, and more.

Acufinder.com is a great source for finding licensed acupuncturists.

Another way to find an acupuncturist is to simply run a Google search for “acupuncture near me.” However, make sure that you find a real, licensed acupuncturist. You can also try searching for “holistic doctors that accept Medicare near me.” Keep in mind that Medicare will cover not all holistic services, but a holistic doctor may be a qualified acupuncturist.

Even if you think an acupuncturist who doesn’t have the proper credentials is trustworthy, Medicare beneficiaries should always try to find certified doctors. Medicare.gov’s Physician Compare tool is a great source for finding doctors that accept Medicare. You can also try visiting your private health plan’s website or asking your insurance agent for help.

Get Acupuncture Coverage

If you want acupuncture coverage and general cost savings, a Medicare Advantage plan may be the way to go. More than 20.4 million beneficiaries are taking advantage of the benefits that MA plans offer.

Contact Us | Medicare Plan Finder

Ready to learn more? Our agents can offer most major plans in your state! This means that you can enroll in the MA plan that best fits your needs and budget. Call us at 844-431-1832 or fill out this form to arrange a no-cost, no-obligation appointment with an agent in your area.

The Ultimate Guide to Medigap Plan D

Medicare Supplements, also known as Medigap plans, add financial benefits that work alongside your Original Medicare. These benefits include help paying your copayments, coinsurance, and deductibles. Enrollment has increased every year since 2010, and there are more than 13 million beneficiaries taking advantage of Medigap plans in 2019.

There are more than ten types of plans (A, B, C, D, F, G, K, L, M, and N), that offer a wide range of coverage at different costs. Many plans are guaranteed renewable life which means you shouldn’t be dropped if a new health condition develops (as long as you pay your monthly premium on time). If you’re looking for financial benefits to supplement your Original Medicare coverage, Medigap Plan D may be the plan for you.

Medicare Supplement Plan D vs. Part D

Medicare Supplement Plan D can be easily confused with Medicare Part D. Medicare Supplement Plan D, is one of the ten types of Medigap plans, while Medicare Part D is prescription drug coverage.

Original Medicare (Part A and Part B) do not cover prescription drugs. Part D was created in 2006 and has since allowed beneficiaries to purchase prescription drug plans alongside Original Medicare to cut down on out-of-pocket drug costs. To learn more about Medicare Part D, click here.

Rx Discount Card | Medicare Plan Finder

Do You Need Medicare Part D If You Have Supplemental Insurance?

You are not required to enroll in a Part D plan whatsoever. However, once you are enrolled in Part A and B, you should consider enrolling in some type of prescription drug coverage to avoid a late-enrollment penalty down the road. Some Medicare Supplement plans cover prescription drug coverage, but this is rare.

You can get prescription drug coverage through some Medicare Advantage plans or a stand-alone Part D plan. You can be enrolled in a Medicare Supplement plan and Part D plan at the same time, however, you cannot be enrolled in a Medicare Supplement and Medicare Advantage plan at the same time.

If you prefer health benefits like dental, vision, or hearing coverage, or even group fitness classes like SilverSneakers®, you may be better suited for a Medicare Advantage plan. Your best bet is to talk with a licensed agent who can explain plan and benefit details that are available in your area. Fill out this form or give us a call at 844-431-1832.

Doctor’s Appointment | Medicare Plan Finder

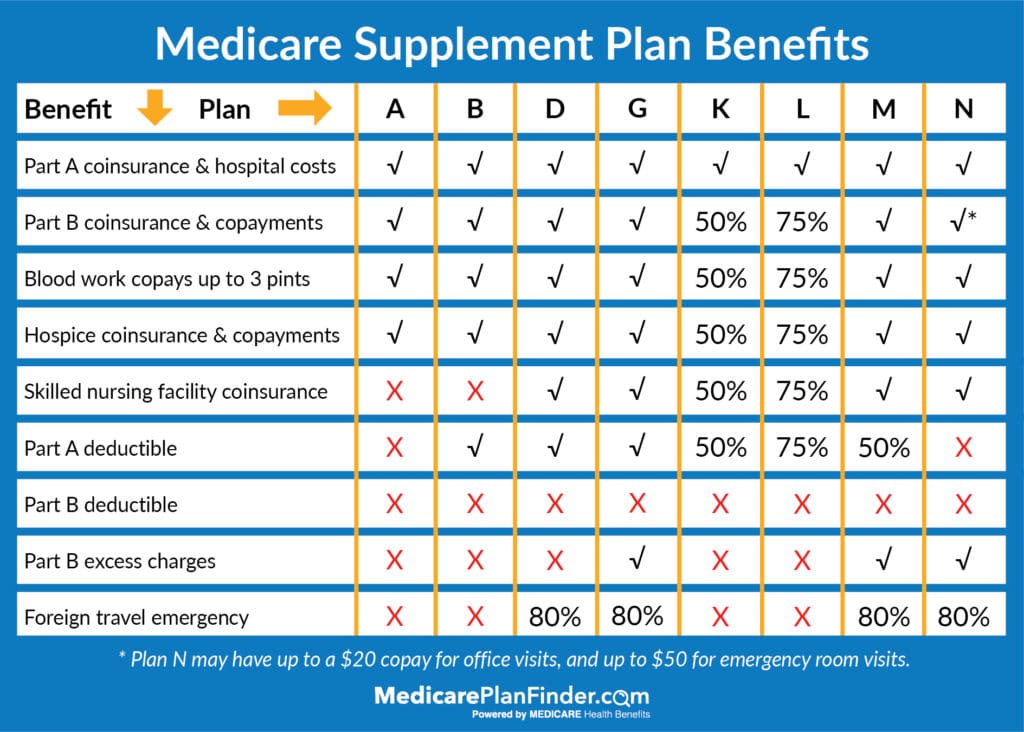

What Does Medigap Plan D Cover?

Medigap Plan D covers all of the gaps from Original Medicare except for the Part B deductible and Part B excess charges. More specifically, Plan D includes the following:

Part A coinsurance and hospital costs

Part B coinsurance and copayments

Blood work copays up to three pints

Hospice coinsurance and copayments

Skilled nursing facility coinsurance

Part A deductible

Foreign travel emergency

Medigap Plan D Costs

If you enroll in Medigap Plan D, you will be responsible for a monthly premium, your Part B deductible, and any Part B excess charges. The Part B deductible in 2019 is $185. Part B excess charges are up to 15% of what Medicare paid for a product or service. You are only responsible for the excess charges if your doctor does not accept Medicare assignment rates.

Medigap plans generally provide the same coverage no matter who you enroll with, but they have different prices. There is no reason to overpay for a plan when there may be a cheaper plan with identical coverage.

The costs can also vary based on carrier, zip code, age, gender, and tobacco. A licensed agent can show you all of the available plans in your area and make sure you do not overpay. Fill out this form or give us a call at 844-431-1832.

Medicare Supplements | Medicare Plan Finder

Use Our Medigap Plan Finder Tool to Compare Rates

Medicare Plan Finder has a tool to help you find Medicare Supplement Plan D options in your area. To get started, click here. Step one is to enter your zip code so you can find local plans. We used 37209, which is the zip code for our corporate headquarters in Nashville, TN.

Medigap Plan Finder Tool Step 1 | Medicare Plan Finder

Then answer the questions in the red box. Then click “Next,” in green.

Medigap Plan Finder Tool Step 2 | Medicare Plan Finder

You will then select a plan preference shown in green. We chose “I don’t have a preference,” for demonstration purposes. Then click “Next,” shown in red.

Medigap Plan Finder Tool Step 3 | Medicare Plan Finder

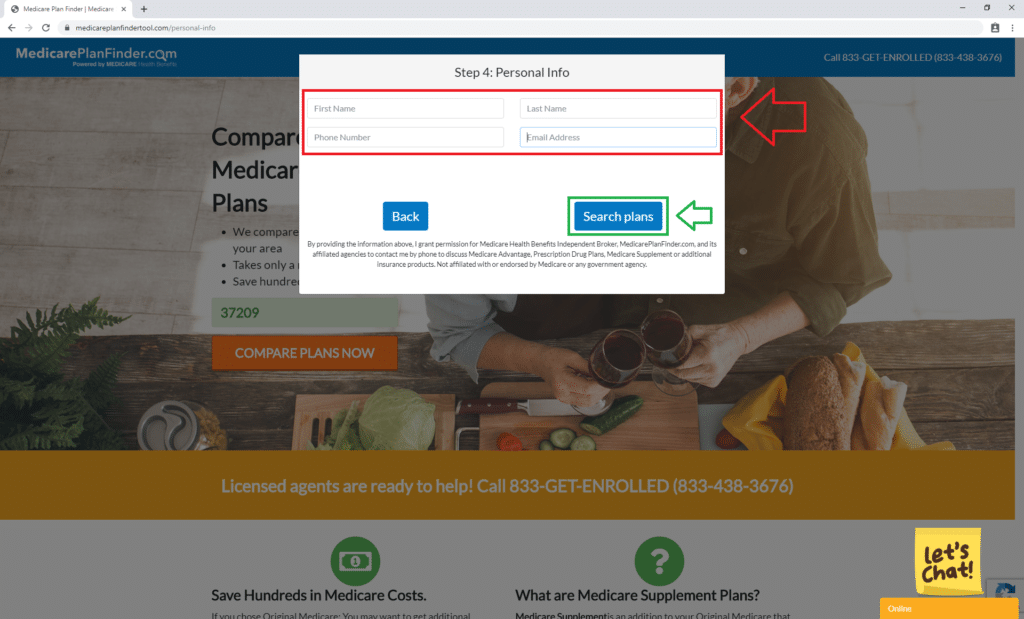

Enter your contact info on the next page in the red box, then click “Search plans,” in green.

Medigap Plan Finder Tool Step 4 | Medicare Plan Finder

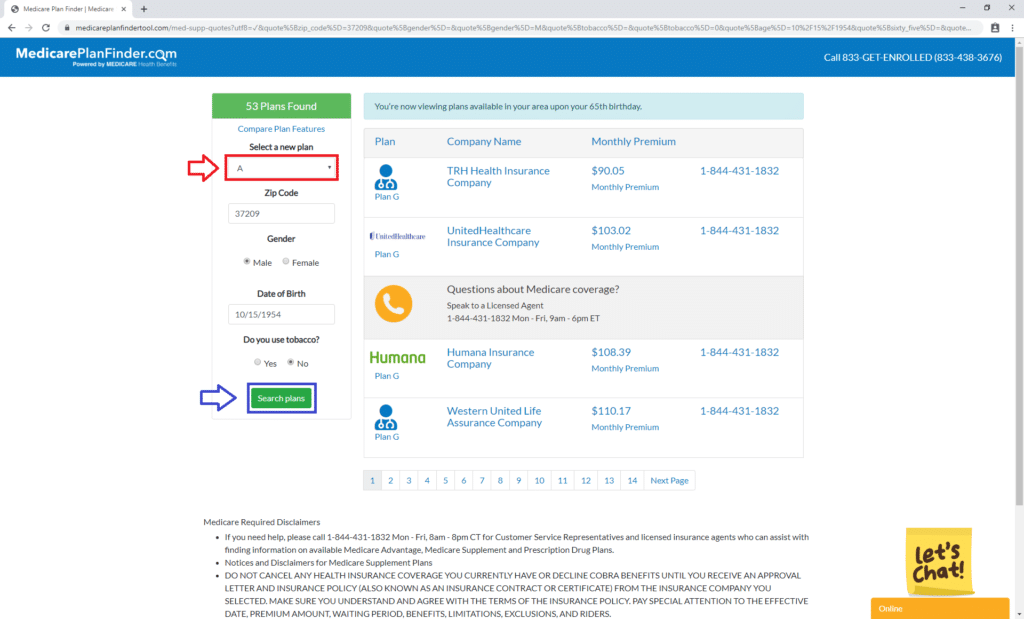

You can use the tool to look for any Medicare Supplement plan in your area, but for this blog we’re only going to look for Plan D. To find Medigap Plan D options in your area, use the drop-down menu in red to select “D”.

Medigap Plan Finder Tool Step 5 | Medicare Plan Finder

Plan D Reviews

The top carriers for Medicare Supplement Plan D in 2019 include:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

Enroll in Medigap Plan D

Did you know you can enroll in Medicare Supplement plans year around? However, carriers can charge you more, or even deny you, if you enroll outside of your initial enrollment period.

Our licensed agents can show you which Medicare Supplement plans are available in your area and help you enroll in a plan that fits your needs and budget.

Why wait? Start saving on your out-of-pocket Medicare costs now! Fill out this form or give us a call at 844-431-1832to schedule an appointment with a licensed agent. As always, appointments are cost-free to you, and there is never an obligation to enroll.

Medicare Supplement Plan Finder | Medicare Plan Finder

This post was originally published on May 10, 2019, by Kelsey Davis and updated on August 20, 2019, by Troy Frink.

Medicare Power of Attorney 101

If you are a caregiver for your parent or loved one, you may not realize that you’re unable to make medical and financial decisions on their behalf until it’s too late.

You don’t want to get caught in a tough situation and feel powerless. Fortunately, a power of attorney can help, but it’s crucial you understand the different types of POAs and common misconceptions.

Types of Power of Attorney

Learning About the Types of Power of Attorney | Medicare Plan Finder

A lot of people don’t understand that a power of attorney is one of the most powerful legal documents you can obtain.

It allows the “principal” (the person granting the power) to select an “agent” (the person receiving the power) to be in charge of a wide range of certain medical and financial matters. Depending on the type of POA granted, you may be given the ability to:

Collect Social Security benefits on the principal’s behalf

Use the principal’s money to pay various bills

File the principal’s taxes

Make financial decisions on their behalf

Buy, sell, or manage the principal’s property

Give gifts or donations on behalf of the principal

Make decisions regarding the principal’s health

Your loved one can appoint several people to be a POA. However, multiple agents can make the decision-making process sloppy. The best bet is to designate people in the areas they have experience in or where they feel comfortable holding responsibility.

Help your parent or loved one make the best decision by educating them on the different types of POA:

Non-Durable: This type of POA is set for a specific amount of time and is generally used for one particular transaction. Once the transaction is over, the POA ceases.

Durable: A durable POA can be used to manage all of the principal’s affairs. Durable POAs are effective immediately and only expire when the principal passes away.

Special or Limited: This type of POA is typically used on a limited basis for one-time financial decisions, like a sale of a particular property. This is most commonly used when the principal cannot complete the transaction due to other commitments or illnesses. The POA has no other power apart from the one-time financial transaction.

Medical: A medical POA has authority on all healthcare decisions if the principal becomes incapacitated. This generally takes effect upon approval of a presiding physician. It’s important to note that you would not be able to make any health decisions if they have the mental and physical capacity to make decisions on their own.

Springing: This type of POA will become effective in the future, only if a specific event occurs. This event can include incapacitation or a triggering event, like leaving the country. This POA can be durable or non-durable and can encompass any affair. This allows the principal to create a POA that is specific to their needs.

What is a Medicare Power of Attorney?

Technically, a Medicare Power of Attorney should be appropriately referred to as a Durable Power of Attorney as it is the only POA that allows you to make health decisions alongside your parent before they become incapacitated.

Medical POA only grants you power after your parent becomes incapacitated. However, a Durable POA gives the power to help your parents make decisions regarding Medicare Advantage, Medicare Supplements, Part D plans, and more. If you are looking to become a “Medicare Power of Attorney,” you will need to explore the Durable Power of Attorney instead.

It’s crucial that you understand that a power of attorney document doesn’t make you the sole decision maker. You and your parent would have the same legal weight in the decision-making process. Plus, your parent can revoke the POA at any time.

Does Medicare Recognize Power of Attorney?

Yes! When it comes to Medicare, you need legal authorization anytime you are acting on behalf of your parent. This means, unless you have the appropriate POA, Medicare will not allow you to make any decisions or even discuss their healthcare plans. However, a Durable Power of Attorney gives you equal power when making your parent’s healthcare decisions.

This means unless you have Durable Power of Attorney, Medicare will not allow your parent to make an appointment with a licensed agent to enroll, change, or switch their plan with your presence or consent.

How to Get Power of Attorney for Elderly Parents

Elder Law Attorney | Medicare Plan Finder

When creating a power of attorney, your parent must be mentally competent at the time of signing. As a general rule, you should start these conversations as soon as possible. Once your parent selects an agent and type of POA, they will need to fill out the proper forms and have it authorized by a notary.

There are several POA documents available online, however, it is recommended that you avoid downloading any forms and that you work directly with an elder law attorney or courthouse.

Once the documents are finalized, you and your parent should make several copies and store them in a safe and secure location.

Power of Attorney Medicare Enrollment

Once you have durable POA, fill out this CMS medical release form provided by CMS and attach your Power of Attorney document. The form will allow you to view your parent’s medical information.

Your durable POA document will allow you to meet with an agent and make decisions on your parent’s behalf including enrolling in a Medicare plan.

Elder Law Attorney Finder

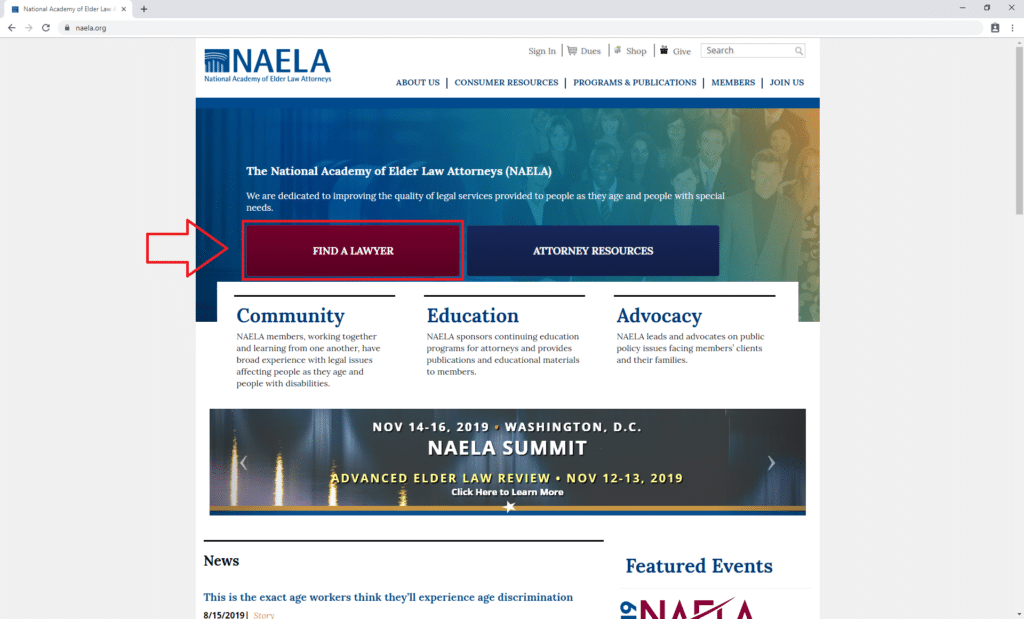

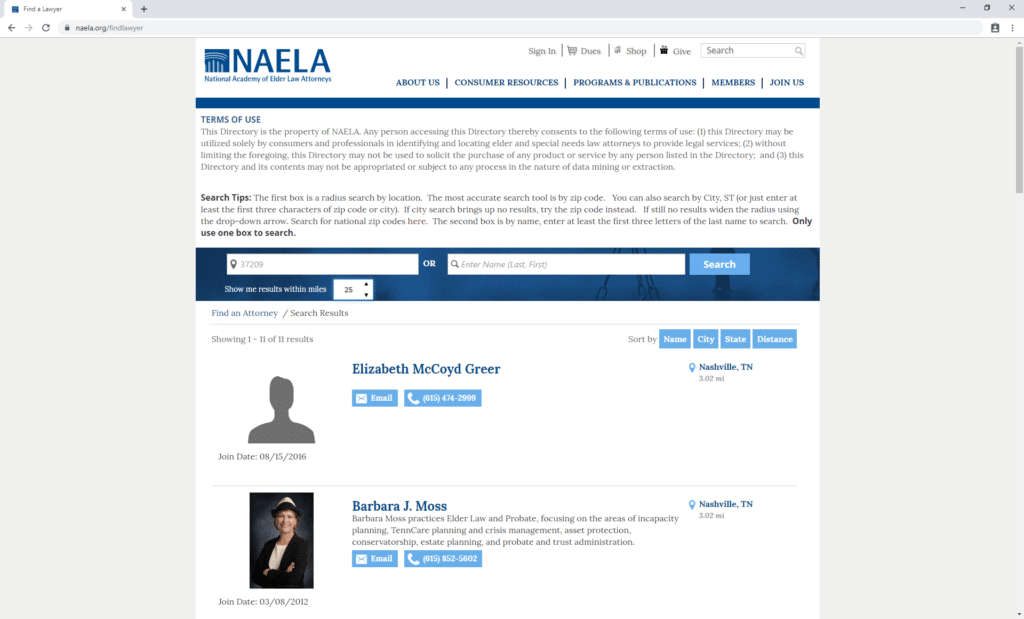

An elder law attorney is a lawyer who focuses on the needs of seniors. Elder law is a broad field that includes Medicare law and power of attorney. If you need a lawyer to help with POA, the National Academy of Elder Law Attorneys (NAELA) is a great place to start. To use NAELA’s attorney finder tool, click here.

That will lead you to NAELA’s homepage. Click “Find a Lawyer.”

Elder Law Attorney Finder Step 1 | Medicare Plan Finder

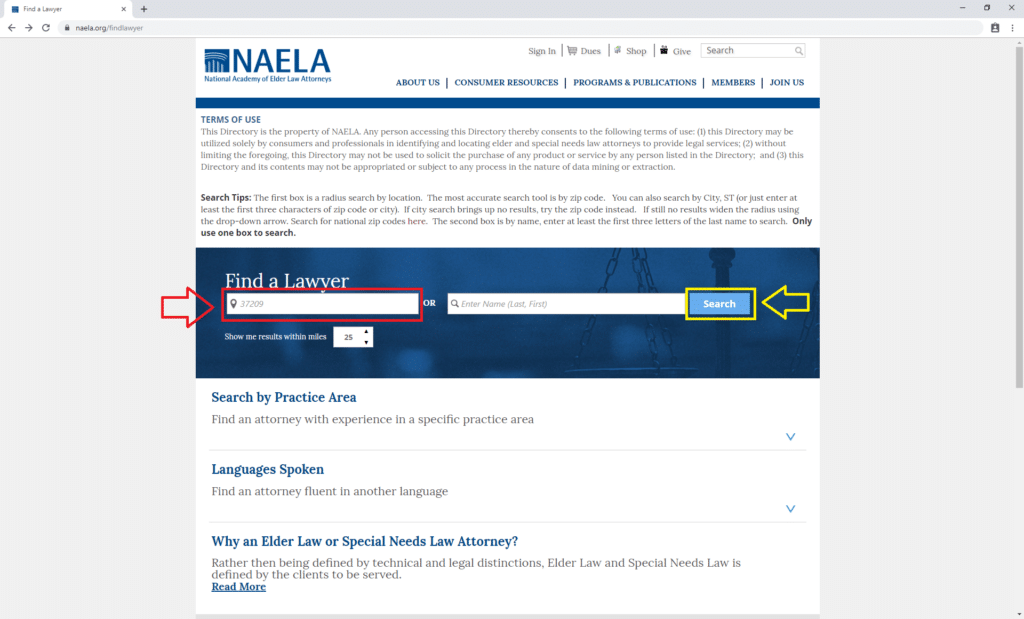

Enter your zip code in the search bar as shown below in red. For our purposes, we’re using 37209, which is the zip code for our corporate headquarters in Nashville, TN. Then click “Search,” shown in yellow.

Elder Law Attorney Finder Step 2 | Medicare Plan Finder

That will lead you to a list of elder law attorneys in your area with contact info. You may have to call more than one to find a good fit.

Elder Law Attorney Finder Step 3 | Medicare Plan Finder

Power of Attorney for Elderly Parent With Dementia

If your loved one is starting to develop Alzheimer’s or dementia, you should try to have the conversation about a POA immediately. In order for your parent to sign a POA, they need to be mentally competent and understand what they are signing.

If the Alzheimer’s or dementia worsens, your parent may be unable to sign and you cannot be granted a POA. If this happens, you can explore becoming a conservator. Conservators act similarly to a POA. You will still be able to make certain medical and financial decisions, but there will be a costly court procedure.

How to Get Power of Attorney for Parent in Hospital

If your parent is sick in the hospital, they can still sign a power of attorney form. You will just need to bring the document to the hospital. A notary will also need to meet you at the hospital if your parent is unable to leave.

Some facilities have on-staff notaries. Once the document is signed, the process is the same as if they weren’t in the hospital. There should be several copies made and stored in a safe place.

Common POA Misconceptions

Misconception: POAs extend after the principal’s death. Truth: All POAs expire when the principal passes away.

Misconception: If a principal signs a POA, they forfeit their independence and rights to make their own decisions. Truth: The scope of POAs can be as broad or as narrow as the principal wants. Many times, principals can require a physician statement to attest if they are incapable of making their own decisions.

Misconception: POAs are the same in every state. Truth: POAs can vary across different states. Be sure to research the type of POA and state guidelines before signing.

Misconception: POAs can be found online. Truth: You can find POA documents online, but your best bet is to work directly with a lawyer or courthouse to guarantee authenticity.

Misconception: POAs take away your parent’s decision making power. Truth: A POA document does not remove your parent’s ability to make decisions on their own, it just authorizes someone else to act under the limitations that they have set.

Medicare POA and How to Get Coverage for Your Loved One

If you are a Medicare power of attorney for your parent, you hold some responsibility in ensuring they have the best health coverage for their unique needs and budget.

At Medicare Plan Finder, we make sure both you and your parent are educated in plan options including Medicare Advantage, Medicare Supplements, and Part D plans. If you are interested in arranging a no-cost, no-obligation appointment for you and your parent, click here or give us a call at 844-431-1832.

This post was originally published on May 31, 2019, and updated on August 16, 2019.

Does Medicare Cover Rehab for Stroke Recovery?

Strokes are fatal in 17% of cases and are the fifth leading cause of death in the United States. For the remaining 73%, stroke recovery is needed to reduce brain injury, but it can cost an average of $17,000 in the first year! It’s important to understand the role of Medicare and how a Medicare Supplement plan can help you save on costs.

Medicare Coverage for Stroke Victims

Stroke Recovery Appointment | Medicare Plan Finder

An inpatient rehabilitation facility requires you to participate in three hours of therapy every day. If you are unable to participate in three hours of care per day, you can move into a skilled nursing facility with a rehab program.

Choosing the right stroke rehabilitation facility is crucial for recovery. Once you are released from the hospital, your options include an inpatient rehabilitation facility, a skilled nursing facility, or a long-term care hospital. Depending on the severity of your stoke, you may be able to return home and utilize home healthcare or outpatient therapy.

Here are some questions to keep in mind when choosing a facility:

Are they accredited through the Commission on the Accreditation of Rehabilitation Facilities?

What medical services are available?

How intense is the recovery program?

How much does Medicare pay for stroke rehab?

Inpatient Rehabilitation:

Medicare will pay for an inpatient rehabilitation facility the same way it covers hospital stays. This means you are fully covered for 60 days. After 60 days, you will pay $341/day until you reach 90 days, and then $682/day until you reach 150 days. If your care extends past 150 days, you will have to pay the full amount, but your cycle resets after you spend 60 days at home.

Your hospital coverage includes a semi-private room, hospital meals, nursing services, intensive care, drugs and medical supplies used during your stay, lab tests and x-rays, operation and recovery services, some blood transfusions, rehabilitation, and symptom management.

It does NOT include non-medically necessary amenities like completely private hospital rooms, private nurses, and personal care items that hospitals may provide (shower supplies, TV, etc.). To learn more about Medicare Part A coverage, click here.

Home Health Care:

If you are discharged to your home, Medicare will cover up to 60 days for home health services. Medicare Part B will cover your outpatient therapy (physical, speech-language pathology, occupational) at 80%; you will be responsible for 20%.

How many days will Medicare pay for a rehab facility?

Medicare has a 100-day rule for skilled nursing coverage, meaning that Part A will cover 100 days in a skilled nursing facility. The first 20 days are covered completely, but the remaining days (21-100) require coinsurance of $170.50/day.

When you are hospitalized for a stroke, you have 30 days to enter the skilled nursing facility. Like hospital stays, benefit periods last for 60 days. If you leave the facility and are back home for at least 60 days, the next time you enter a facility your “day count” will reset to 0.

Stroke Rehabilitation

The goal of stroke rehabilitation is to recover your body’s functions as much as possible. The process includes exercises to improve actions like talking, walking, and using the restroom.

In some cases, full recovery may be difficult. In this case, your therapist will teach you compensatory strategies. For example, if you lose the ability to use your arm, your therapist will teach you other ways to use the restroom, get into bed, and cook your own meals.

How long does it take for a person to recover from a stroke?

The average stroke patient will see the most improvement in the first three months. However, recovery time will vary on a case-by-case basis depending on the stroke severity. If your brain stem was damaged during the stroke, your recovery time could be a year or longer.

What percentage of stroke patients make a full recovery?

The National Stroke Association estimates that roughly 10% of stroke patients make a complete recovery. This may sound like a small percentage, but don’t let that discourage you! 25% recover almost completely excluding minor impairments (like minimal vision or memory loss). Another 40% will recover but require special short-term care.

Can paralysis from a stroke be reversed?

When you have a stroke, the lack of oxygen and blood cells to your brain can cause damage to millions of brain cells, which can lead to paralysis. This damage is irreversible if the cells are killed, but damaged cells can resume function over time.

Plus, scientists at the Pacific Neuroscience Institute are researching ways to reverse the effects of a stroke by transplanting stem cells and using them as a source for brain cell regeneration. This research will continue, but for now, stroke rehabilitation is the best method to regain independence and recover several of your body’s functions.

How soon after a stroke can you start rehab?

Stroke recovery starts as soon as you are stable. This is typically 24 to 48 hours after a stroke. The first stage of recovery typically takes place in the hospital, but this is dependent on your unique circumstances. After you are discharged from the hospital, your doctors, nurses, and family can help you choose a suitable living arrangement based on your needs.

Benefits of Medicare Supplements

The costs for stroke recovery can add up quickly, and these costs should not disrupt your rehabilitation plan. A Medicare Supplement plan can help cover your copayments, coinsurance, and deductibles. There are 10 plan options (Plan A, B, C, D, F, G, K, L, M, and N). The costs will vary per plan and on which state and county you live in.

Plan F is the most popular Medicare Supplement plan. If you do not have Plan F but you would like to, you can lock yourself in by enrolling NOW. You must enroll before January 1, 2020, to receive Plan F coverage. If you miss this deadline, there’s good news!

Plan G is almost identical to Plan F! The only difference is that Plan G does not cover the Part B deductible (which is less than $200 for most people). In reality, by switching to Plan G you will not be losing much at all. However, keep in mind that you can still keep your Plan F after January 1, 2020, if you enroll in 2019.

If you are interested in exploring Medicare Supplements or have any questions regarding your current coverage, contact us! We have licensed agents across 38 states who are dedicated to making sure you are enrolled in the plan that best fits your needs and budget.

If you are looking for coverage beyond Original Medicare, our agents can help you select a Medicare Advantage (MA) plan instead. Many MA plans offer hearing, dental, and vision coverage, and some even offer group fitness classes like SilverSneakers®. Call us at 844-431-1832 or fill out this form to get in contact with an agent.

Contact Us | Medicare Plan Finder

This post was originally published on March 7, 2019, by Kelsey Davis and was updated on August 7, 2019, by Troy Frink.

OTC Medicare Drug Coverage

According to the Consumer Healthcare Products Association, the average American makes 26 trips per year to buy over-the-counter (OTC) products. As you age, this number may increase. This means you may be spending more on these products each year.

Every penny counts and understanding the products, drugs, and the role of a Medicare Advantage OTC pre-paid card can help you save in the long run.

Contact Us | Medicare Plan Finder

What Are Over-the-Counter Medications?

These medications don’t require a doctor’s prescription to be purchased. They can help ease pains such as backaches, help prevent or treat illnesses such as athlete’s foot and allergic reactions, and help manage recurring issues such as migraines.

The most common over the counter medications are fever reducers, anti-inflammatories, allergy pills, and cold medicine.

OTC Medicare | Medicare Plan Finder

Does Medicare Cover Over-the-Counter Drugs?

Original Medicare (Part A and Part B) does not cover over-the-counter products and medications. Some stand-alone Part D plans may cover the costs, but generally, a Medicare Advantage plan is your best option if this type of drug coverage is important to you.

Your Medicare Advantage plan provider should give clear instructions on how to utilize your allowance towards medications and products.

Oftentimes, your insurance carrier will provide a website or downloadable document that lists the eligible products/medications, instructions to purchase, and the details of the benefit. If you have any issues, feel free to contact a licensed agent here.

Medicare Advantage | Medicare Plan Finder

What Is Medicare Advantage OTC Card Coverage?

Certain Medicare Advantage plans offer beneficiaries a unique way to buy over the counter products: a pre-paid card! These cards can be used to purchase most OTC products and medications.

Once you exceed your allowance (average of $50-$100/month for most providers), the card is no longer valid until it is reloaded by your insurance provider. Most plans reload the cards to the set amount on a monthly basis and any previous balance will be lost.

What Can I Buy With My OTC Card?

Before you ask yourself, “What can I buy with my OTC card,” you should first look at your plan’s OTC catalog. Eligible products and medications may vary through your plan provider, but common eligible items include:

Acne aids

Cough, cold, and flu medications

Antibiotic creams

Bandages

Denture products

Digestive aids

Ear care

First-aid kits

Orthopedic support

Pain relievers

Sleep aids

Wart removal

Generally, these items are not covered:

Chapstick

Deodorant

Dietary supplements

Mouthwash

Perfume

Soaps

Teeth whitening products

OTC Medicare | Medicare Plan Finder

Where Can I Use My Medicare Advantage OTC Card?

Stores and locations that accept your card will vary by provider. However, the following stores are included in most plans:

Along with an extensive inventory of over-the-counter products in the stores, many of the major pharmacies listed above also have a mail-order feature so you can have many of your favorite OTC and even prescription items shipped straight to your door! You may be able to use your OTC card at the following online pharmacies*:

*This is not an exhaustive list of online pharmacies.

Medicare OTC Card Activation

Your card should come with information about how to activate it. If you’re unsure how to activate your card, contact your plan’s customer service center and ask about OTC card activation.

How to Check Your OTC Card Balance

For information about how to check your OTC card balance, go to the website your plan gave you. If you’re not sure how to access it, call your plan’s customer service center for help.

How Do I Save on My Prescriptions?

While a Medicare Advantage OTC benefit can certainly be a great perk to have, you’re probably still wondering how you can cut down on your prescription costs.

You may want to start by finding out if you’re eligible for “Extra Help,” a Medicare savings program for prescription drugs. Then, look at your current coverage and make sure you have the right plans for your needs. A licensed agent can help you.

Then, download our free prescription drug savings card. It works in many major pharmacies and is sort of like a coupon. Just show the card when you pick up your prescriptions, and your pharmacist can tell you whether or not your prescriptions can be cheaper with the card. It’s worth a try!

How Do I Get Medicare Advantage OTC Coverage and Prescription Drug Coverage?

Are you interested in getting OTC Medicare coverage? Our licensed agents are contracted with most major carriers in your state. There are countless plans that can fit your personal needs and budget all while having the additional benefit of over-the-counter drug coverage.

Already enrolled in a Medicare Advantage plan? You may unknowingly have this benefit already, and we want to help you use it. Call us today at 844-431-1832 or fill out this form to get started.

Find Medicare Plans | Medicare Plan Finder

This post was originally published on January 17, 2019, by Kelsey Davis and updated on July 15, 2019, by Troy Frink, and November 12, 2020, by Anastasia Iliou.