What Can You Do During the Medicare Annual Enrollment Period?

Medicare Enrollment Periods

Did you know that there are five different Medicare enrollment periods throughout the year? Not everyone will be eligible for every period, but everyone who has Medicare is eligible for the Annual Enrollment Period.

Be sure to keep track of each enrollment period so that you know when it’s your turn to make changes. Don’t go months with a bad plan just because you missed your enrollment period!

What/When is the Annual Enrollment Period?

The Annual Enrollment Period runs from 10/15 through 12/7 of each year. This is the time when all Medicare beneficiaries are eligible to make changes, which will go into effect on January 1 of the following year. It does not apply to people who have not yet enrolled in any form of Medicare coverage. If you’re enrolling for the first time, you’ll have an “Initial Enrollment Period.” You can use the AEP later to make changes if you don’t like the choices you made during your IEP.

Changing Medicare Plans After the Annual Enrollment Period

There are a few other times throughout the year when you may be eligible to make changes.

The Initial Enrollment Period (IEP) is for those enrolling in Medicare for the first time. If you are aging into the program, this will begin three months before your 65th birthday and end three months after. If you become eligible due to disability, your IEP will depend on your disability status or diagnosis.

The General Enrollment Period (GEP) is for those who missed their IEP. It runs from January 1 through March 31. If you enroll during the GEP, your coverage will begin on July 1. You may face a late enrollment penalty fee for not enrolling during your IEP. If you want to enroll in Medicare Advantage during the OEP, you can do that between April 1 and June 30, or you can wait for the AEP.

The Special Enrollment Period (SEP) is not one specific time frame. You may qualify for a “temporary” SEP if you have a special circumstance that results in a loss of coverage, such as losing a job with coverage or moving to an area where different plans are available. You will likely have 30 days following the event to make a change. Some circumstances, like having a disability, can make you eligible for a different type of SEP. If you are disabled or have low-income and have a special needs plan, you can change plans once per quarter for the first three quarters of the year.

How can I get a SEP for Medicare?

To qualify to change plans once every quarter for the first three quarters of the year, you must:

Be a member of a Medicare Savings Program or Medicaid

Be part of SPAP (State Pharmaceutical Assistance Program)

Be in a Medicare Savings Program or LIS (Extra Help)

To qualify for to change plans once following an event, you must:

Move to a new service area that has different plan options available

Involuntarily lose your coverage

Find a contract violation with your plan

Lose or gain a job where you are enrolled in employer benefits

Move into or out of a medical facility

Leave imprisonment

Suddenly gain or lose Medicaid eligibility

Suddenly gain or lose Medicare Savings Program or LIS eligibility

Have been automatically enrolled in Part D

OEP vs. AEP

OEP is not the same as AEP. During AEP, you can make a lot of different changes to your coverage. During OEP, you can only do one of the following:

Switch from one Medicare Advantage plan to another

Change from a Medicare Advantage plan with prescription drug coverage to Original Medicare + Part D

Switch from Medicare Advantage to Original Medicare (can also add Part D)

What can I do During the AEP?

During AEP, you can make a number of different changes to your coverage, like:

Enroll in a Medicare Advantage plan

Switch to a different Medicare Advantage plan from what you had

Drop your Medicare Advantage plan and have only Part A and Part B

Add a Part D prescription drug plan

Change to a Medicare Advantage plan with a prescription drug benefit

Change from a MAPD (Medicare Advantage Prescription Drug Plan) to a Medicare Advantage plan without prescription coverage

Change from one Part D plan to another

Drop your prescription drug coverage and return to Original Medicare only

You can also add or remove Medicare Supplement (Medigap) coverage, but keep in mind that you can enroll in Medicare Supplements during any time of year. Enrollment periods to not apply to Medicare Supplement plans. However, if you enroll in Medigap any time past your Initial Enrollment Period, underwriting may apply, leaving you with higher costs than you could have had if you enrolled sooner.

Why the AEP is so Important for Medicare

The ability to make these changes every year is more important than you may realize.

Even if you think you’re happy with your plan, plans are allowed to change their benefits and costs every year. Your plan can add or remove benefits and make cost adjustments as they need to. At the same time, new plans are continually entering (and leaving) the market. It’s a good idea to take a look and see if there is a better plan for you each year.

Licensed agents are required to go through a training and certification process before they can sell to you. They are usually trained on what’s going on in the area that they sell in. They may be able to tell you about plans that you haven’t even heard about before, and they can help you sort through your options. It does not cost anything to meet with a Medicare Plan Finder licensed agent.

Can you Auto-Renew Medicare?

In most cases, you do not have to renew your plan each year. Your Medicare coverage will automatically continue as long as that plan is still available for the current year. The only reason your plan wouldn’t renew is if that specific plan itself leaves your service area or leaves Medicare.

However, that does not mean that you shouldn’t review your coverage each year. Have your finances or your healthcare needs changed? Has your plan changed its benefits or costs? Ask these questions every year to make sure you’re still getting the coverage you need.

New to Medicare

How to Make Medicare Plan Changes

You can enroll in a new Medicare Advantage plan by getting help from a licensed agent. If you haven’t enrolled in Original Medicare yet, be sure to do that first by contacting Social Security either online or at 1-800-772-1213. You can also visit your local Social Security office.

To get in touch with a licensed agent in your area, click here or call us at (833)-567-3163.

Medicare Hearing Aids Coverage

Hearing aids can turn your entire life around, but you may need a private Medicare plan to be able to afford it. Original Medicare (Part A and Part B) will only cover hearing tests under limited circumstances. That means no ear treatments, no hearing aids, or anything else.

Not every Medicare-eligible person needs ear treatments, which is why Medicare does not consider it an “essential benefit”.

Does Medicare Cover Hearing Aids Costs?

Doctor’s Appointment | Medicare Plan Finder

Hearing aids can cost anywhere from $400 per ear to $4,000 or more per ear. Even if the initial device is not too expensive, you’ll have to remember that you’ll need to pay the costs of a hearing aid fitting, hearing aid exams, cleanings, and replacement hearing aids every five years or so.

Some providers may offer free cleanings and fittings with your hearing aid. When you add everything together, you could be paying thousands upon thousands over your lifetime for your ear care. Luckily, there is a solution that can help you out financially.

You may be able to get cheaper hearing aids by ordering online. However, by ordering a hearing aid online, you miss out on the doctor consultation and fitting.

Even if you think you don’t need the doctor consultation, remember that an experienced doctor can give you the medical advice you need to determine what kind of hearing aid you need and help you get the right fit.

Does Medicare Cover Hearing Tests?

Medicare does not cover hearing aid tests, fittings, or routine hearing exams. Medicare Part B will only cover hearing and balance tests if your doctor orders them to diagnose medical conditions.

Medicare Advantage Plans that Cover Hearing Aids

The easiest way to get Medicare coverage for audiology appointments, treatments, hearing aids is to enroll in a Medicare Advantage plan. While some separate hearing benefit plans are available, it’s often not as cost-effective.

Medicare Advantage is a plan offered by private insurers that covers hospital visits, doctor visits, and other benefits like prescription drugs, vision, dental, and hearing.

Every year, you have the chance to enroll in a Medicare Advantage plan between October 15 and December 7. You should start thinking about your needs now so you can be ready to switch in the fall!

Not all Medicare Advantage plans cover hearing benefits, so make sure you read everything carefully before you buy. Some plans will require that you buy a hearing aid from a specific provider.

Hearing loss affects more than just your hearing. Your hearing is directly connected to your sense of balance, so hearing loss can lead to more trips and falls, leading to higher medical bills.

Additionally, people who experience hearing loss or more likely to also experience high blood pressure, depression, and even dementia. Hearing aids can reduce all of these symptoms and side effects.

Signs of Hearing Loss

Some signs of hearing loss might include:

Trouble focusing on a person’s speech, especially when there is background noise

Tinnitus (ringing in the ears)

Finding yourself constantly raising the volume on your television or radio

Having a harder time hearing extremely high or extremely low pitches

Missing certain consonant sounds like “sh,” “th,” and “p.”

Leaving your car’s turn signal on because you don’t hear it

Not hearing your alarm clock in the morning

Hearing Loss Prevention

Some hearing loss prevention is purely the result of old age, but there are certain ways you can prevent the development of this ailment. The best way is to avoid circumstances where you will be surrounded by loud noises. Wear earplugs when attending concerts or events with big crowds, pay attention to the volume on your radio and TV, don’t sit too close to the speakers, etc.

You should also be sure to attend your yearly wellness exams. Your doctor may or may not check your hearing during these appointments (you may face an extra co-payment for audiology). Medicare Advantage plans often including a hearing benefit so that you can get coverage for regular hearing exams.

About Medicare Hearing Aids

While hearing aids can’t give a deaf person the ability to hear, they can help people with minimal to moderate hearing loss regain some hearing ability. Hearing aids effectively make sounds louder. There are a handful of ways to lose hearing ability, but hearing aids help those who have sensory cell damage in the inner ear.

Types of Hearing Aids

Medicare Hearing aids can work in two different ways: analog and digital. Analog hearing aids convert sound waves into amplified electrical signals. Digital hearing aids convert sound waves into numerical codes, then amplify them.

There are six different types of analog and digital hearing aids: IIC, CIC, ITC, ITE, RIC, and BTE. Your doctor may recommend one type over another based on your specific hearing needs and your budget.

IIC (Invisible n Canal) – Fitted for your ear canal and invisible when worn. For mild to moderate hearing loss.

CIC (Completely in Canal) – Fitted for your ear canal, small handle may be visible; for mild to moderate hearing loss

ITC (In the Canal) – Fitted to your ear canal, small portion will show; for mild to mildly severe hearing loss

ITE (In the Ear) – Fitted to your outer ear; for mild to severe hearing loss

RIC (Reciever in Canal) – Barely visible, open and comfortable fit; uses electrical wires (as opposed to a plastic tube). For mild to moderate hearing loss

BTE (Behind the Ear) – Fitted behind the ear, directs sound into a mold inside the ear; for moderate to severe hearing loss

Best Hearing Aids on the Market

Your doctor may recommend one hearing aid brand over another, and we recommend listening to your doctor’s opinion. However, we can tell you that some of the most highly-rated hearing aid brands are Resound, Phonak, Starkey, Widex, and Oticon.

If you’re getting coverage for your hearing aid from a Medicare Advantage plan, be careful. Your plan may require that you select from specific Medicare hearing aids. You should also consider that some hearing aid companies will offer trial periods.

Get Your Medicare Hearing Aids

Before you select and purchase a hearing aid, be sure to speak to a Medicare agent about finding coverage for your ear care. We recommend Medicare Advantage for most seniors and other Medicare-eligible people with hearing deficiencies.

Most people who are eligible for Medicare are eligible for several different Medicare Advantage plans. Our agents are licensed to sell most of those plans and can help you select the best one for your needs. To set up your free appointment, send us a note or call us at 844-431-1832.

Contact Us | Medicare Plan Finder

*This post was originally published on February 22, 2018, and updated on August 19, 2019.

What Is a Medicare Advantage HMO?

A HMO, or Health Maintenance Organization, is a type of Medicare Advantage (MA or Part C) plan. HMO plans always offer the same benefits as any other Medicare plan, but they are also able to provide additional benefits, many plans include vision, dental, and hearing coverage.

HMO plans are different from other Medicare Advantage plans because they require a strict network and you will usually need to select and stick with one primary care doctor.

Pros and Cons of Medicare HMO Plan Networks

PCP Discussing HMO Referral With Patient | Medicare Plan Finder

The HMO option is certainly not for everyone. Having a strict network means that you will turn to the same doctor for most of your healthcare needs.

Some plans are called “HMO POS,” or HMO Point-of-Service plans. These allow you to see providers outside of your network for certain services. If you need to use that benefit, you will usually have to get approval from your plan first, and your provider needs to recommend the other provider.

For example, if your primary care physician (PCP) suggests that you need to see a nutritionist or other specialist, your PCP can refer you to a nutritionist that he or she trusts and send a request for coverage to your HMO. The “con” to the HMO option is that your plan can deny your out-of-network coverage.

The “pro” to selecting one primary physician and having a Health Maintenance Organization is that all of your care is grouped together and managed in one place. Your providers usually work together to manage your care, preventing unnecessary costs.

A licensed agent with Medicare Plan Finder can help you determine if a HMO is right for you. Our agents can help you find the right plan based on your budget and lifestyle needs. To learn more, call 844-431-1832 or contact us here.

Contact Us | Medicare Plan Finder

Medicare HMO vs. PPO

Where an HMO requires a very specific network, a PPO, or Preferred Provider Organization, can cover services outside of your network. With a PPO plan, you’ll be able to see any provider without needing a referral from your primary physician.

Granted, the added flexibility of a PPO plan comes with a higher premium than an HMO plan. If costs are your primary concern, HMOs are the way to go – but if you can afford the flexibility, a PPO may be for you.

If you have questions about HMOs vs. PPOs, your agent can answer all of them and help you make the right choice for you.

What is Medicare Advantage?

Medicare HMO plans and other types of Medicare Advantage plans are great options for people who want more coverage than what Original Medicare provides.

Original Medicare is what everyone who has Medicare will have, but its coverage is limited. Medicare Advantage plans can add anything from extra medical coverage to additional benefits like home healthcare, telemedicine, and full dental coverage.

Many MA plans can offer coverage for whole health benefits. Along with additional medical and dental benefits, MA plans can offer coverage for meal delivery, non-emergency medical transportation and even fitness classes!

Your agent can discuss the differences between other types of Medicare plans like Medicare Supplements and Medicare Advantage plans.

Medicare Advantage | Medicare Plan Finder

HMO Eligibility and Costs

HMO Costs | Medicare Plan Finder

Most people who are eligible for Medicare are eligible for HMO plans. The only exceptions are that not every county has HMO plans available, and most HMO plans do not accept Medicare beneficiaries with ESRD (End-Stage Renal Disease).

Just like your Original Medicare coverage, you will receive a card in the mail when you enroll in a HMO plan. When you visit a doctor or hospital, use your HMO card instead of your Medicare card to get the most coverage.

Every Medicare Advantage plan is different, but you will generally be responsible for paying certain costs.

All HMO plans come with a premium you will owe every month, but some are as low as $0.

You’ll also be responsible for paying copays such as $10 or $20 when you see a doctor and you may have to pay a deductible before your coverage starts.

Medicare Advantage plans are rated based on the following criteria:

How easy it is to access preventive services (such as annual physical exams and health screenings)

Care coordination between providers

How often plan members receive treatment for chronic conditions

Member satisfaction

Plan performance from year to year

Customer service quality

Five-star HMO plans may be available in your area. Talk to your agent to learn more.

Medicare Advantage HMOs Near You

Medicare Advantage HMO plans are not available in every zip code. However, we have highly-trained, licensed agents in 38 states who can help you discover the options available in your neighborhood. To get started, send us a message or give us a call at 844-431-1832.

Contact Us | Medicare Plan Finder

This post was originally published on February 26, 2019, by Anastasia Iliou and was updated on August 12, 2019, by Troy Frink.

Why Medicare Advantage Plans Are Bad

Someone may have told you a million reasons why Medicare Advantage plans are bad. The truth is they’re just misunderstood. More than 34 percent of Medicare beneficiaries are enrolled in Medicare Advantage (MA) plans, so they can’t be all bad.

What Is Wrong With Medicare Advantage Plans?

Medicare Advantage plans have pros and cons like any other type of health insurance plan. They may not make sense for some people, but they can be extremely beneficial for others, and here’s why.

They Can Be Expensive

Why Medicare Advantage Plans Are Bad | Medicare Plan Finder

Medicare Advantage plans all come with monthly premiums. Some of them have $0-premiums, but the average monthly premium in 2019 is $28. Some people may think, “free,” when they hear “$0 premium,” but that’s not necessarily the case. Even if you enroll in a MA plan, you may still be responsible for paying your Medicare Part B premium and other costs, like copayments.

Along with monthly premiums, MA plans can come with high out-of-pocket maximums. An out-of-pocket limit is designed to protect you. Once you reach your limit, the insurance company pays for your covered services. However, some plans’ out-of-pocket limits can be as high as $6700.

The out-of-pocket limit resets at the beginning of the year, but you could end up paying $13,400 if you have two major procedures within a few months.

For example, if you have hip replacement surgery in November, you might reach the $6700 limit just from that. Then,after your out-of-pocket maximum resets in January, you need knee replacement surgery. You would owe another $6700, just a few months later. You would then be covered for the rest of the year, but that total of $13,400 within a few months can certainly hurt.

Medicare Advantage Plans Have Smaller Networks

Most MA plans have provider networks you have to stay within. You can go out-of-network to find a doctor, but you may have to pay significantly more than if you stayed in your network.

You may even go to your favorite doctor and get turned away because your doctor isn’t in your plan’s coverage network.

Many people don’t realize that MA plans have networks when they enroll, and that may be why Medicare Advantage plans are bad according to some people.

Specific Coverage Areas

Most MA plans have coverage specific to one location. That’s great if you’re close to home and you need medical treatment, but that means your plan may not cover a doctor’s appointment if you get sick when you’re out of town. Original Medicare is a federal program, so it is likely that you’ll be able to find a doctor when you’re on vacation in another part of the country.

Your Plan Could Change Every Year

Many Medicare Advantage plans change their benefits every year. Sometimes they add or remove providers, covered services, and/or prescription drugs on the plan’s formulary.

Plans can also change how much you pay in monthly premiums, copays, and/or deductibles.

That means you’ll have to change plans if your current plan drops vision coverage, and you signed up for your plan specifically because you wanted the annual eye exam benefit. The problem is that you can only change plans during certain parts of the year.

Most people have to wait until the Annual Enrollment Period (AEP), which is from October 15 – December 7 to enroll in new plans or make changes to existing ones. Exceptions to that rule include people who are about to turn 65, or who just had their 65th birthday.

The Initial Enrollment Period (IEP) for people aging into the program is the three months before you turn 65, and the three months after. During that seven-month period you can choose a new Medicare health insurance plan. If you are eligible due to ALS or ESRD, your IEP is the week after your diagnosis. If you are eligible due to receiving SSDI for at least 25 months, your IEP is your 25th month of benefits.

You may qualify for a Special Enrollment Period (SEP) if you meet certain conditions. Your SEP may be lifelong or temporary, but it will allow you to make changes to your plan outside of the other enrollment periods.

Some Plans Require Doctor Referrals

Many Medicare Advantage plans are HMOs, which require you to select a primary care provider (PCP). In most cases, your PCP will need to give you a referral before you can see a specialist.

To illustrate what this looks like, let’s take the example of a man* who has a MA HMO. The man notices a mole that’s changed in size and shape. He knows he needs to see a dermatologist because he’s had skin cancer before, and the new mole likes like his previous carcinoma.

The man can’t just go to a dermatologist, however. He needs to first make an appointment with his PCP, and the PCP can then refer him to a dermatologist. The man will owe a copay to see his PCP, and then he’ll need to pay the dermatologist a copay, too. Specialist copays are usually higher than PCP copays. You may pay $10 for a PCP visit, but $40 for a specialist.

On the flip side, because the man went to his primary physician first, he got a really good recommendation and was able to see one of the best dermatologists in his town on short notice. That doctor referral requirement may have brought more help than harm.**

*This example is not real and only represents a possible circumstance.

**Not all doctors will be able to see you on short notice, regardless of your plan.

Benefits of Medicare Advantage Plans

The reasons why MA plans are good may outnumber why Medicare Advantage plans are bad. The truth is everyone has different healthcare and financial needs. MA plans make sense for people who want coverage for a variety of health services.

Medicare Advantage Plans May Actually Cost Less

Even though you may still owe the Part B monthly premium, you could end up paying less overall if you have Medicare Advantage.

Your cost-sharing may also be less with a MA plan. If you only have Original Medicare, you will owe 20 percent of covered services, and Original Medicare will pay 80 percent of approved costs.

To illustrate what this looks like, let’s say you see your doctor because you have the flu. Your doctor charges Medicare $100. Medicare approves the charge and you owe $20.

Many MA plans have copays of $10 or less for doctor’s appointments. That $10 savings for one doctor’s visit may not seem like much, but it adds up over time.

Plans Can Be a “One-Stop-Shop” for Covered Services

Many Medicare Advantage plans are designed to provide the beneficiary with comprehensive healthcare coverage. MA plans can offer coverage for services Original Medicare does not, including vision, hearing, dental, and fitness classes.

Many MA plans even include prescription drug coverage, which Original Medicare does not.

That also means that you may have access to doctors with a variety of specialties, provided they’re in-network. All of your providers can coordinate with each other to provide a complete health plan to keep you in optimal health.

Fitness Class | Medicare Plan Finder

Find out Why Medicare Advantage Plans Are Bad (or Good) for You

A Medicare Advantage plan may be a good fit if you need coverage for a variety of services and you want to have a whole care team creating your treatment plan. A licensed agent with Medicare Plan Finder can help you determine if a MA plan is right for your budget and lifestyle needs. To get started, call us at 844-431-1832 or contact us here today.

As you age, it can become difficult to perform everyday tasks such as bathing or getting dressed, and you may need assistance to do those things.

Long term care may consist of skilled nursing services or physical therapy immediately following an illness or injury, or it may consist of someone coming to your house to help you with day-to-day tasks.

Does Medicare Cover Long Term Care?

Medicare Long Term Care Coverage | Medicare Plan Finder

Original Medicare does not cover long term care unless it follows a hospital stay or is for necessary medical treatment.

However, you can use certain Medicare Advantage (Part C) or Medigap (Medicare Supplement) insurance plans to help pay for non-medically necessary long term care. Here’s what Original Medicare will cover:

Medicare Skilled Nursing Coverage

Medicare Part A will cover short stays (100 days or less) in skilled nursing facilities if you meet these qualifications:

You’ve been admitted to the hospital for at least three days

A Medicare-certified skilled nursing facility admits you within 30 days of the initial hospital stay

Your treatment plan involves skilled care such as physical therapy or skilled nursing services.

Medicare will cover 100 percent of the costs for the first 20 days. In 2019, your copay for days 21-100 is $170.50.

For Medical Treatment

In order for Medicare to cover long term care for medical treatment, your doctor must first deem it medically necessary. Medicare Part B will cover the following services:

Intermittent and part-time skilled nursing care

Physical therapy

Occupational Therapy

Speech pathology

Your durable medical equipment (DME) can be covered if your doctor prescribes it and it will be used for at least three years. Medicare Part B also covers mental health services to help manage the psychological and cultural issues that come with having an illness.

There is no limit on how long you can receive the above services if your doctor reorders them every 60 days.

Chronic Special Needs Plans (C-SNP) will cover long term care services for people with chronic illnesses. The covered services for conditions such as Parkinson’s and ALS are to help prevent and slow the progression of the symptoms.

Original Medicare will NOT cover prescription drugs for chronic illnesses, however. Prescription coverage falls under Medicare Part D and certain Part C plans.

Part D Checklist | Medicare Plan Finder

Medicare Hospice Coverage

If you have a terminal illness with no chance of improvement, are expected to live less than six months, and are looking for peace instead of a cure, Medicare will cover hospice care.

In order for Medicare to cover drugs to control the symptoms and to relieve pain, you must be receiving care from a Medicare-approved hospice provider.

You can receive hospice care at your home, in a nursing home, or in a hospice care facility. When you enter hospice care, you will have an entire team of people focused on your overall comfort and well-being including your spiritual and emotional needs, not just your physical needs.

Long Term Care Coverage With Medicare Supplement Vs. Medicare Advantage

Private insurance companies offer plans that can go beyond what Medicare Parts A and B will cover. For non-medically necessary long term care, you won’t be able to use Original Medicare, and, for the most part, you won’t be able to use Medicare Supplements, either. If you want long term care coverage, a Medicare Advantage plan may be your best option.

Long Term Care Medicare Supplement

Medicare Supplements (Medigap) plans are designed to fill in the financial gaps Original Medicare creates. For example, you are financially responsible for that $170.50 copay. You can use a Medicare Supplement to help make those payments easier.

Medicare Advantage

Medicare Advantage (MA) plans are insurance plans that can cover medical services Original Medicare does not. While Medigap plans are strictly for help paying for out-of-pocket costs, MA plans are for additional medical coverage. Certain Part C plans can include coverage for DME and non-medical long term care, so it’s critical you know what your options are.

Note: You cannot have both a Medicare Supplement and a Medicare Advantage plan, so having someone help you sift through the thousands of plans out there and find the right one for you is extremely important to your overall health and well-being.

Medicare Advantage | Medicare Plan Finder

Why It’s Important to Have a Plan

Long term care can easily cost hundreds or thousands of dollars a month, and those costs will only increase. By 2050 the baby boomer population in the US will be 80 million, and that means more competition for home health care and therefore steeper prices. Having a health insurance plan to help with those costs might not only help you stay in good health, but also give you peace of mind.

Get Medicare Long Term Care Coverage Today

Are you looking for Medicare long term care coverage? One of our licensed agents can answer your questions and help you find the right plan for you. Fill out this form or call us at 844-431-1832 for a no-obligation appointment today.

Find Medicare Plans | Medicare Plan Finder

.

Original Medicare vs. Medicare Advantage

The Annual Enrollment Period is quickly approaching and starting October 15, you will be able to switch Medicare Plans. Which do you favor in the battle of Medicare vs Medicare Advantage? If you’re not quite sure, we’re here to help! By understanding the basic principles of each, you will be better prepared to make that decision.

What is Medicare?

Medicare is operated under the federal government and covers a variety of health care expenses and provides benefits for seniors over 65 as well as those with Social Security benefits or certain health conditions. There are many parts, policies, and new standards associated with Medicare. We get it – it’s confusing! It’s important to understand the history of Medicare Part A B C D, because AEP is right around the corner!

Created in 1965, Original Medicare is a federally-regulated healthcare program designed largely for senior citizens. Original Medicare includes Part A (hospital coverage) and Part B (medical coverage).

Part A covers inpatient and outpatient care at hospitals, nursing homes, hospice care, and home health services. Part B covers doctor visits and ambulance rides. Most beneficiaries receive Part A for free. Most people pay the same rate for Part B coverage, but a small number of beneficiaries may have income-adjusted premiums.

Original Medicare allows beneficiaries to go to any provider that accepts Medicare, which is over 900,000 physicians nationwide! This means that no matter which Medicare provider you visit, the costs will stay the same. This is ideal for beneficiaries who travel often or want doctors in different locations.

If you are enrolled in Original Medicare, you are able to enroll in a Medigap plan. Medigap plans provide financial benefits for an extra monthly premium. This can include help paying your copayments, coinsurance, and deductibles. Additionally, some of these Medigap plans cover prescription drugs. However, if your plan does cover prescription drugs, you cannot purchase a separate drug plan.

Time to get the coverage you need with Medicare!

History of Medicare

National health coverage wasn’t even discussed until President Roosevelt in 1912. He ran on a platform that included providing health coverage to anyone who needed it. Flash forward to 1945 when President Truman took office. Within seven months, he called for a national health fund that would be available to all Americans.

Truman fought hard, but it took another 25 years before anything went into effect. In 1965, Lyndon B Johnson signed legislation that provided benefits for seniors over 65. As of 2018, the Centers for Medicare and Medicaid Services (CMS) estimate that over 58.5 million people benefit from Medicare. As more policies and new standards go into effect and technology creates healthcare innovations in this industry, Medicare will continue to evolve.

Medicare Part A B C D

Medicare is broken into specific parts and each part is unique. Original Medicare consists of Parts A and B. Part A covers inpatient hospital fees, hospice care, and home health services. Part B covers doctor services, outpatient care, and physical therapy.

Most beneficiaries receive Part A for free and Part B is covered by a monthly Medicare premium. Beyond Original Medicare, there are Parts C and D. Part C is Medicare Advantage (MA).

MA plans combine Part A (hospital fees insurance) and Part B (medical insurance) and usually prescription drug coverage. Part D is a standalone plan that is purchased separately on top of Original Medicare. It can help cover the cost of prescription drugs.

What is Medigap?

If you are enrolled in Original Medicare, you are eligible to purchase a Medigap plan. What is Medigap? Medigap plans help pay some of the cost that Original Medicare does not cover. This can include copayments, coinsurance, and deductibles. Medigap plans generally don’t cover vision or dental care but may include prescription drug coverage. They are sold by private insurance companies. You cannot be enrolled in a Medicare Advantage plan and Medigap, so it’s important to compare and evaluate your budget and needs.

Pros and Cons of Medicare

Some people love Medicare, and others don’t care for it.

Why Medicare is Awesome

Premiums: If you worked for most of your life, you won’t have to pay any premium for Medicare Part A!

Healthcare Innovation: Medicare has increased healthcare innovations in the medical market tremendously. Thanks to Medicare, millions of Americans suddenly have access to health coverage they otherwise would be unable to afford. Millions of dollars have been invested in healthcare innovation and development!

Medicare “Rules:” CMS has steady Medicare rules that help prevent fraud, waste, and abuse. Without breaking the Medicare Rules, Medicare agents and plans can’t take advantage of you!

Why Some People Dislike Medicare

Hospital Fees: Even with the help of Medicare, hospital fees can still cost a pretty penny. Medicare beneficiaries typically pay 20% of the total fee. Additionally, Medicare typically does not have a cap. This means that if you have a series of health issues within a year, you may be spending more than you originally budgeted.

Prescription Drug Coverage: Medicare does not cover prescription drugs. If you are looking to purchase drug coverage, you will need to purchase separate prescription drug coverage through Medicare Advantage or Part D.

Limitations: Original Medicare provides the same health coverage for everyone. There is no personalization or choosing the exact benefits you want, unless you enroll in Medicare Advantage. If you are seeking more than basic health coverage, an MA plan could be perfect for you.

Enrolling in Medicare Advantage

What is Medicare Advantage?

The history of MA plans is relatively short compared to Original Medicare. Just like Medicare, MA plans have benefits for seniors over 65 and certain disabled persons. These plans are rising in popularity and may be the best option for you!

Medicare Advantage plans can allow you to have a monthly premium for all your additional benefits, like dental, vision, and prescription drugs. There is no hassle with sending payments for multiple plans. Some MA plans may offer a lower deductible in exchange for a higher monthly premium. This is a great option for healthy seniors and other Medicare eligibles. With MA plans, you only pay for the services you use rather than paying a higher upfront cost.

The History of the Medicare Advantage Program

Medicare Advantage plans were not offered until 2003. Since then, enrollment has tripled to 19 million beneficiaries according to the Henry J Kaiser Family Foundation. Medicare Advantage plans are available through private insurance companies and must cover the same benefits as Original Medicare. However, many MA plans offer extra benefits like vision and dental coverage and even SilverSneakers®. These plans have a set network of providers you must choose from, but don’t worry! There are many different networks and plans available.

Medicare Advantage (Part C) Popularity

According to the Henry J Kaiser Family Foundation, enrollment has tripled to 19 million beneficiaries since 2003. Medicare Advantage plans are available through private insurance companies and must cover the same benefits as Original Medicare. However, many MA plans offer extra benefits like vision and dental coverage and even fitness programs like SilverSneakers®. These plans have a set network of Medicare providers you must choose from, but don’t worry! There are many different networks and plans available.

Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs) are the most popular plans among Medicare Advantage.

HMOs:

An HMO, or Health Maintenance Organization, has a closed provider network. You’ll have to select one primary provider for most of your healthcare needs. HMOs may require you to get a referral for more severe injuries or illnesses.

PPOs:

PPOs, or Preferred Provider Organizations, allow you to see any doctor, but staying in your network you will save you money. Additionally, they don’t require referrals and like HMOs, they often cover Part D supplements.

Medicare Advantage plans have one monthly premium. There is no hassle with sending payments for multiple plans. Some MA plans may offer a lower deductible in exchange for a higher monthly premium. This is a great option for healthy seniors. With MA plans, you only pay for the services you use rather than paying a higher upfront cost.

Pros and Cons of Medicare Advantage

Why Medicare Advantage Plans are Awesome

Premiums:KFF reported that half of Medicare Advantage beneficiaries in 2019 pay no premium at all, and most others pay between $20 and $100.

Out-of-pocket Max: Although you pay a premium with both Original Medicare and Medicare Advantage, MA plans may offer a lower deductible in exchange for a higher monthly premium. Also, MA plans have a limit for your out-of-pocket costs, saving you even more in the long run!

Prescription Drugs: Prescription drug coverage is often included in Medicare Advantage plans. This allows you to bundle your health coverage – saving you money and creating more convenience for you!

Unexpected Benefits: Some Medicare Advantage plans even include cool benefits like gym memberships!

Flexibility: There is a broad range of Medicare Advantage plans out there, so you may be able to choose between a few options to get the one that’s right for you.

Why Some People Don’t Like Medicare Advantage Plans

Limited Networks: There is usually no nationwide coverage with Medicare Advantage plans. This can be an issue if you frequently travel within the US. Additionally, your network may require that you only see specialists that your doctor refers you to.

Price Fluctuation: The specifics of your Medicare Advantage plan varies per provider. You may still be required to pay copays and coinsurance fees. Additionally, your Medicare premiums and copayments may change each year.

Medicare Doctor

Medicare Advantage vs. Medigap

When comparing Medicare Advantage vs Medigap, it’s easy to get confused. Medigap can only be purchased alongside Original Medicare. You cannot have a Medicare Advantage and Medigap plan at the same time. Medigap plans cost an additional monthly Medicare premium, but they help fill the cost gaps in coverage – this means less out of pocket costs for you.

Medicare Advantage vs Medigap prices can vary. If this is something you’re interested in, it’s important to compare policies.

medicareplanfindertool.com

Difference Between Medicare and Medicare Advantage

What is the difference between Medicare and Medicare Advantage? It is easy to confuse the two. The main difference is that while Original Medicare is the federal program, Medicare Advantage plans are privately owned. Medicare Advantage plans still have to follow all the rules determined by CMS (Centers for Medicare and Medicaid Services), but they are able to offer benefits that the federal program cannot. med

How to get Medicare Advantage

Does a Medicare Advantage plan look attractive to you? Did we grab your attention? AEP is coming soon!

From October 15 to December 7, anyone with Medicare can make changes to their plans. If you’re interested in purchasing a Medicare Advantage plan or hearing more about how to get covered, complete this form or call us at 844-431-1832 to arrange a free, no-obligation appointment with an agent and get covered today.

*This blog was originally published on September 20, 2018, and updated on July 28, 2019.

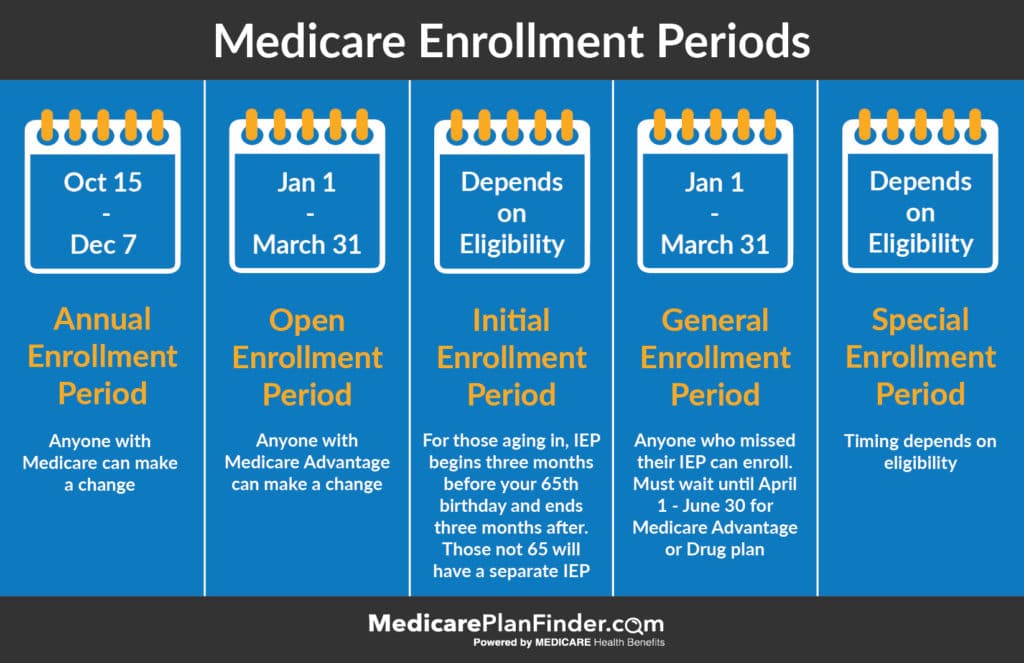

5 Medicare Enrollment Periods & What You Can Do During Each One

Did you know there are five different Medicare enrollment periods? You may qualify to enroll or make changes to your current coverage and have no idea! AEP is just a few months away, so we’d like to share with you what you can do during the various enrollment periods so you are properly prepared.

Initial Enrollment Period

Your Initial Enrollment Period (IEP) is typically your first opportunity to enroll in Medicare. Your IEP is three months before your 65th birthday and three months after. This gives you a seven-month window to enroll in your preferred coverage.

In most cases, if you do not enroll in Part A and Part B (Original Medicare) during your IEP, you will be charged a late enrollment penalty fee that will be added to your monthly Part B premium. If you do not have prescription drug coverage, you should also consider enrolling in a Part D plan to avoid other penalties down the road. You are not required to enroll in a Medicare Advantage or Medicare Supplement plan, but you should consider enrolling to optimize your coverage.

The General Enrollment Period (GEP) is for those who are enrolling in Medicare for the first time but missed their IEP. The GEP runs from January 1 to March 31 each year, and coverage will begin in July.

During the GEP, you can:

Enroll in Original Medicare if you missed your IEP

*If you enroll for the first time during the GEP, you can follow up by enrolling in a Medicare Advantage plan during a period from April 1 through June 30.

Annual Enrollment Period

The Annual Enrollment Period (AEP) runs from October 15 to December 7 each year. During this time, all Medicare beneficiaries can make changes to their plans. You may not need to do anything during AEP. However, major insurance carriers can change the benefits that they offer every year. It’s possible that a change in your plan benefits or your provider network will change how you feel about your plan. Ultimately, it’s always a good idea to speak with an agent. Any changes you make during AEP become effective on January 1 of the following year.

Most people can only make changes to their plans once a year (during AEP), but if you qualify for a Special Enrollment Period you can make those changes during different times of the year or even all year long. Lifelong SEPs allow you to change plans once every quarter for the first three quarters of the year. Circumstantial SEPS allow you to change plans once following a particular event.

Starting in 2019, there will be a new “Medicare Open Enrollment Period” that will run from January 1 through March 30. OEP was created for anyone who signs up for a Medicare Advantage plan during AEP to enroll in a different plan, without having to wait until the following fall. You do not have to do anything during OEP unless you are unhappy with the coverage you enrolled in during AEP.

Change from Medicare Advantage to Original Medicare only, with the option to add a prescription drug plan

Contact Medicare Plan Finder

Are you looking to enroll in Medicare Advantage, Medicare Supplements, or Part D? Are you still confused on which Medicare enrollment periods you qualify for?

Our agents at Medicare Plan Finder can answer any of your questions and simplify the enrollment process. They are contracted with most of the major carriers in your state so the agent should not show bias when enrolling. To speak with a licensed agent and to learn about plans in your area, click here or call 844-431-1832.

This blog was originally published on 10/23/18 and was updated on 7/15/19.

OTC Medicare Drug Coverage

According to the Consumer Healthcare Products Association, the average American makes 26 trips per year to buy over-the-counter (OTC) products. As you age, this number may increase. This means you may be spending more on these products each year.

Every penny counts and understanding the products, drugs, and the role of a Medicare Advantage OTC pre-paid card can help you save in the long run.

Contact Us | Medicare Plan Finder

What Are Over-the-Counter Medications?

These medications don’t require a doctor’s prescription to be purchased. They can help ease pains such as backaches, help prevent or treat illnesses such as athlete’s foot and allergic reactions, and help manage recurring issues such as migraines.

The most common over the counter medications are fever reducers, anti-inflammatories, allergy pills, and cold medicine.

OTC Medicare | Medicare Plan Finder

Does Medicare Cover Over-the-Counter Drugs?

Original Medicare (Part A and Part B) does not cover over-the-counter products and medications. Some stand-alone Part D plans may cover the costs, but generally, a Medicare Advantage plan is your best option if this type of drug coverage is important to you.

Your Medicare Advantage plan provider should give clear instructions on how to utilize your allowance towards medications and products.

Oftentimes, your insurance carrier will provide a website or downloadable document that lists the eligible products/medications, instructions to purchase, and the details of the benefit. If you have any issues, feel free to contact a licensed agent here.

Medicare Advantage | Medicare Plan Finder

What Is Medicare Advantage OTC Card Coverage?

Certain Medicare Advantage plans offer beneficiaries a unique way to buy over the counter products: a pre-paid card! These cards can be used to purchase most OTC products and medications.

Once you exceed your allowance (average of $50-$100/month for most providers), the card is no longer valid until it is reloaded by your insurance provider. Most plans reload the cards to the set amount on a monthly basis and any previous balance will be lost.

What Can I Buy With My OTC Card?

Before you ask yourself, “What can I buy with my OTC card,” you should first look at your plan’s OTC catalog. Eligible products and medications may vary through your plan provider, but common eligible items include:

Acne aids

Cough, cold, and flu medications

Antibiotic creams

Bandages

Denture products

Digestive aids

Ear care

First-aid kits

Orthopedic support

Pain relievers

Sleep aids

Wart removal

Generally, these items are not covered:

Chapstick

Deodorant

Dietary supplements

Mouthwash

Perfume

Soaps

Teeth whitening products

OTC Medicare | Medicare Plan Finder

Where Can I Use My Medicare Advantage OTC Card?

Stores and locations that accept your card will vary by provider. However, the following stores are included in most plans:

Along with an extensive inventory of over-the-counter products in the stores, many of the major pharmacies listed above also have a mail-order feature so you can have many of your favorite OTC and even prescription items shipped straight to your door! You may be able to use your OTC card at the following online pharmacies*:

*This is not an exhaustive list of online pharmacies.

Medicare OTC Card Activation

Your card should come with information about how to activate it. If you’re unsure how to activate your card, contact your plan’s customer service center and ask about OTC card activation.

How to Check Your OTC Card Balance

For information about how to check your OTC card balance, go to the website your plan gave you. If you’re not sure how to access it, call your plan’s customer service center for help.

How Do I Save on My Prescriptions?

While a Medicare Advantage OTC benefit can certainly be a great perk to have, you’re probably still wondering how you can cut down on your prescription costs.

You may want to start by finding out if you’re eligible for “Extra Help,” a Medicare savings program for prescription drugs. Then, look at your current coverage and make sure you have the right plans for your needs. A licensed agent can help you.

Then, download our free prescription drug savings card. It works in many major pharmacies and is sort of like a coupon. Just show the card when you pick up your prescriptions, and your pharmacist can tell you whether or not your prescriptions can be cheaper with the card. It’s worth a try!

How Do I Get Medicare Advantage OTC Coverage and Prescription Drug Coverage?

Are you interested in getting OTC Medicare coverage? Our licensed agents are contracted with most major carriers in your state. There are countless plans that can fit your personal needs and budget all while having the additional benefit of over-the-counter drug coverage.

Already enrolled in a Medicare Advantage plan? You may unknowingly have this benefit already, and we want to help you use it. Call us today at 844-431-1832 or fill out this form to get started.

Find Medicare Plans | Medicare Plan Finder

This post was originally published on January 17, 2019, by Kelsey Davis and updated on July 15, 2019, by Troy Frink, and November 12, 2020, by Anastasia Iliou.

Medicare Dental Plans: What You Need to Know

According to the National Institute of Dental and Craniofacial Research, most people over the age of 65 are missing an average of 13 teeth. In fact, it is estimated that 27% have no remaining teeth at all. Dental problems are among the most common health issues for older adults. A Medicare dental plan can make a huge difference in you having a bright, healthy smile.

Original Medicare (Part A and B) covers very few dental-related costs. Jaw diseases, oral cancer, face tumors, or face fracture-related procedures and infections caused by dental procedures are covered by Medicare Part B. Oral examinations may be covered by Part A if they are related to another hospital stay. However, Original Medicare does not cover important services to prevent or detect severe dental problems such as routine exams or cleanings. Furthermore, Original Medicare doesn’t cover dentures, denture care, fillings or pullings. Medicare Advantage plans can fill in those gaps.

Medicare Supplemental Dental Insurance or Stand-Alone Plans

Medicare Supplemental Dental Insurance | Medicare Plan Finder

Even though Original Medicare does not cover the majority of dental services, there are a couple of options for Medicare supplemental dental insurance plans or stand-alone plans to help you save money.

Medicare Advantage

Medicare Advantage (MA) plans are private insurance plans that contract with Original Medicare. MA plans offer the same coverage as Original Medicare, but they can include additional benefits such as dental, vision, and hearing coverage. Some plans even offer coverage for fitness classes!

Medicare Advantage plans may include dental coverage for services including:

Cleanings (prophylaxis)

Dental X-rays

Diagnostic services

Endodontics (root canal treatment)

Extractions

Oral exams

Restorative services such as fillings

Periodontics (gum disease and oral inflammation treatment)

Extractions

Prosthodontics (crowns, bridges, dental implants, and dentures)

Medicare Advantage dental services typically come with a copay or coinsurance. Your coinsurance will usually be a percentage. For example, you will owe 20 percent of the covered service costs. A copay is a set dollar amount that you will owe for services, such as $20 for X-rays, an exam, and cleaning.

You will usually have a monthly premium with your Medicare Advantage supplemental dental insurance plan, but some areas have plans with $0-premiums.

There may be many MA plans in your area to choose from, and it may seem daunting. A licensed agent with Medicare Plan Finder can help you find a plan that fits your budget and lifestyle. Our agents are highly trained and they are experts in Medicare Advantage. They are dedicated to finding the best plan for you.

Find Medicare Advantage Plans | Medicare Plan Finder

Stand-Alone Dental Insurance Plans

Some people may find that Medicare Advantage plans don’t offer coverage for the dental care they need, or that the MA plans in their area don’t offer dental coverage. Those people may find coverage through private dental insurance plans that aren’t contracted with Medicare.

Many stand-alone dental insurance plans cover 100 percent of routine and preventive care, such as cleanings and exams. You will likely owe a monthly premium, but you may save money overall because you won’t have as many out-of-pocket costs.

Dental insurance plans can also cover 70-80 percent of treatments such as fillings or extractions. You may pay 50 percent of major procedures such as crowns or bridges.

Dental Savings Plans

A dental savings plan is much like a shopping club: you pay an annual or monthly fee and you get discounts from a certain group of dentists. This type of savings plan is not insurance, but it is a way to save money on dental care.

Dental Issues Facing the Elderly

Researchers have found links between poor oral health and other health problems such as cardiovascular disease, dementia, respiratory infections, diabetes, cancer, and more. It’s important to be aware of elderly dental problems so you can rectify the issue as soon as possible. Some common problems include:

Darkened Teeth

As you age, your teeth become discolored naturally. When enamel wears away, dark dentin underneath is exposed. These bone-like tissues lie underneath your tooth enamel. Dentin is affected by your diet and medications. Smoking and drinking coffee, tea, and soda can contribute to the darkening of your teeth.

Dry Mouth

Dry mouth is caused by a lack of saliva. As you age, you may start taking more medications which could result in a dry mouth. When our mouths are producing the proper amount of saliva, our teeth are protected from decay and bacteria. Although it may seem like a minor issue, dry mouth can lead to viruses and fungi forming in your mouth. Dehydration from excessive sweating, vomiting, and diarrhea can also lead to dry mouth. Be sure to drink a minimum of 8 glasses of water a day. Water is crucial for dental hygiene. Plus, vital organs in your body perform best when you’re hydrated!

Root Decay

If you do not exercise proper oral hygiene habits, your gums can recede. When this happens, your roots are exposed. Tooth roots are covered by cementum, not enamel. Cementum is responsible for anchoring the tooth to the jawbone. However, cementum is not designed to protect your teeth the same way as enamel. When this part of the tooth is exposed, your risk of tooth decay increases. The naked eye can not see tooth decay, so it’s important to practice good dental hygiene and visit your dentist regularly.

Gum Disease

Have you ever experienced gum bleeding while brushing your teeth? This is a sign that you may be developing gum disease. Gum disease develops when there is an excess of plague caused by small pieces of food being left in your teeth. This is often caused by a lack of brushing or flossing. The risk of gum disease is higher in those who smoke tobacco, have unhealthy diets, or wear poor-fitting dentures. Gum disease can lead to tooth loss and many other health issues in your body.

Oral Cancer

When cells on your lips or mouth have changes in their DNA, a cancerous tumor can form. Oral cancer can appear on your lips, cheek lining, gums, tongue, and top of your mouth. Symptoms include a sore that won’t go away, red or white patches, numbness, and difficulty chewing, swallowing, or speaking. Having a healthy diet and avoiding excess sun exposure to your mouth and lips can help prevent oral cancer or at least limit your symptoms. However, regular visits to your dentist are the best way to find and fix any underlying issues.

Best Oral Hygiene Practices

Proper dental care for seniors and Medicare eligibles doesn’t have to be a daunting task. Spending a few extra minutes a day on your teeth can help prevent some of the common elderly dental problems discussed above. If you’re looking for easy ways to improve your dental hygiene, follow these simple tips:

Brush your teeth twice per day with fluoride toothpaste

Floss once per day

Use an electric toothbrush

Use mouthwash after brushing your teeth

If you wear dentures, clean them daily

Visit your dentist regularly

Drink plenty of water

Get Medicare Dental Insurance Today

Many seniors and Medicare eligibles may be watching their income, and that’s where Medicare Plan Finder can help. Your agent can help find a Medicare Advantage plan that covers your necessary medical expenses including dental coverage.

When you enlist Medicare Plan Finder’s help, you get an expert in Medicare on your side who can help you weigh the pros and cons of the plans in your area, and help you decide if a Medicare Advantage plan with dental coverage, a stand-alone dental plan, or a dental savings plan is right for you. Call 844-431-1832 or contact us here to learn more today.

This post was originally published on December 13, 2018, by Kelsey Davis, but was updated on July 03, 2019, by Troy Frink.

Prescription Drug Price Trends

About one in four people say they have a tough time affording their prescription drugs. Prescription drug prices have been on the rise since 2017. According to Rueters, drug companies announced price increases for more than 250 medications in 2019.

According to the Centers for Medicare and Medicaid (CMS), prescription drugs already account for 20 percent of Medicare’s spending, and with the prescription drug price trend increasing, that number will only increase in the near future. That may mean that your vital medications will cost you more.

How to Get Prescription Drug Discounts

Rising prices shouldn’t mean that you have to stop taking your needed drugs. Wouldn’t it be great if you could get a discount for your necessary medications? You can with this free discount drug card!

Prescription Drug Discount Card | Medicare Plan Finder

This discount card is not an insurance plan. However, you can use your discount card to receive up to 75 percent off your prescriptions at more than 68,000 pharmacies. Simply download, print and show your card to the pharmacist when you check out to save money on your important medications.

Why Are Prescription Drug Costs Rising Rapidly?

Senior Man With Pill in Hand | Medicare Plan Finder

The prescription drug price trend may be going up due to a lack of competition for pharmaceutical companies, and mergers and acquisitions in the pharmaceutical industry.

Lack of Competition for Pharmaceutical Companies

Many major pharmaceutical companies own patents for their drugs. That means other manufacturers cannot legally create generic equivalents, and the patent holders can charge whatever they want for their products.

Usually, manufacturers will produce generic drugs once a brand name patent expires. Some drugs are expensive to develop even with an expired patent, so that often means the original manufacturer is the only company producing their drug.

Mergers and Acquisitions in the Pharmaceutical Industry

Drug manufacturers make deals to expand their product bases. Unfortunately, when pharmaceutical companies merge, they get a lot of bargaining power. The pharmaceutical companies can demand that pharmacy benefit managers (PBM) – people responsible for contracting with pharmacies and getting drug discounts – set prices higher. Those costs get passed on to the government and ultimately to you.

Sometimes, pharmacy benefit managers merge with health plans, like in the cases of Cigna and Express Scripts and CVS and Aetna. Those mergers may actually be able to HELP you, by lowering costs due to reduced overhead and improved communication.

Medicare Prescription Drug Price Negotiation Act

One reason the prescription drug price trend is rapidly increasing is that CMS cannot legally negotiate drug prices. The Medicare Prescription Drug Price Negotiation Act is a bill that would require Medicare to negotiate prescription prices with pharmaceutical companies. It was first introduced in the House of Representatives in 2017, and re-introduced in 2019.

Other federal and state entities are making efforts to help reduce drug prices. The Food and Drug Administration is working toward approving more generic versions of brand name medicines. Many states have passed laws requiring drug companies to justify price increases.

Medicare Prescription Drug Plans

Prescription Drugs | Medicare Plan Finder

As prices rise, you may want to consider a new form of prescription drug coverage. Original Medicare does not help pay for prescriptions, but you can get prescription drug coverage through Medicare Part D, or through certain Medicare Advantage (Part C or MA) plans.

You can still use your discount drug card along with your insurance plan. When you go to the pharmacy to pick up your prescriptions, the pharmacist can determine your cost with each option.

Medicare Part D

Medicare Part D plans are also called prescription drug plans (PDPs). You can use PDPs to cover your medication costs. Many people who have PDPs also purchase Medicare Supplement (Medigap) plans to help pay for items such as coinsurance and copays.

Even though Medicare Supplements and Medicare Advantage plans sound similar, they are actually very different. Medigap plans “fill in” the gap between what you owe and what Original Medicare covers. MA plans help pay for medical expenses. If you have questions, one of our highly trained, licensed agents will be happy to help. Your agent can help you find the right plan for your budget and lifestyle.

PDPs typically use formularies that divide medications into tiers according to their copays. For example, one plan may feature four tiers with varying expenses. The first tier may only include generic drugs and cost $5 per prescription. Tier two may include preferred brand name medications and cost $15 per prescription.

Medicare Part D Checklist | Medicare Plan Finder

Medicare Advantage Prescription Drug Plans

Medicare Advantage plans are privately owned insurance policies that cover everything Original Medicare covers, but they can offer additional services including vision, hearing, and dental. Certain MA policies called Medicare Advantage Prescription Drug (MAPD) plans offer medication coverage.

Like PDPs, MAPDs use a formulary that lists every covered drug and separates them into tiers. The difference is that MAPD plans come with only one monthly premium for your covered services, and it includes prescription drugs.

Medicare Over-the-Counter Drug Coverage

Many people use over-the-counter (OTC) drugs along with their prescription medications. Like with prescription medications, Original Medicare does not cover OTC drugs. However, certain MA plans help pay for OTC medications. Some plans feature a pre-paid card that allows you to purchase covered items such as bandages and cold medicine.

How We Can Help You With Rising Prescription Drug Prices

Your agent can help you find a plan that not only includes all of your prescriptions, but covers the additional services you need. Call us at 844-431-1832or contact us here to learn more today.