Medicare Supplements are often referred to as Medigap plans. These plans provide financial benefits and help cover out-of-pocket expenses that Original Medicare does not, like copayments, coinsurance, and deductibles. More than 22% of Medicare beneficiaries are enrolled in a Medigap plan and enrollment has increased each year since 2010.

Medigap plans are broken down into ten standardized plans (A, B, C, D, F, G, K, L, M, and N). Each letter offers a different range of coverage at a different price point. You can evaluate which benefits are the most important to you and if you would rather pay a higher monthly premium for more benefits or pay less and receive less coverage.

Medicare Supplements are also popular because most are guaranteed renewable life, which means as long as you pay your premium on time, you will not be canceled from your plan due to new health conditions. Plus, Medicare Supplements are generally the same regardless of which carrier you enroll with. If you’re looking to supplement your Original Medicare, Medigap Plan K may be a good option.

What does Medigap Plan K Cover?

The fewer benefits a plan provides, the lower the monthly premium is. This means Plan K is cheaper than other plans on the market like Plan F or Plan G. Plan K covers:

Part A coinsurance and hospital costs

50% of Part B coinsurance and copayments

50% of bloodwork co-payments (up to 3 pints)

50% of hospice coinsurance and copayments

50% of skilled nursing facility coinsurance

50% of your Part A deductible

Other benefits of Medicare Supplements include:

You’re able to keep your current doctor (as long as they accept Medicare)

You can see a specialist without needing a referral

Coverage travels with you throughout the U.S.

Plan K Costs

Medigap plans are generally the same regardless of which carrier you enroll with. This means if you want to enroll in Medicare Supplement Plan K, you will have the same coverage whether you enroll with Blue Cross Blue Shield, Cigna, or another carrier. However, while the coverage may be the same, the costs are not. The cost of your plan will vary based on your zip code, age, gender, and tobacco use. Our licensed agents can show you available plans in your area and help you enroll in a plan that fits your needs and budget. Fill out this form or give us a call at 844-431-1832.

Medicare Supplement Eligibility

Medicare Supplement plans are designed to work alongside Original Medicare. To be eligible, you must be enrolled in Part A and B first. Medicare Supplements are sold through private insurance companies. However, most states are not required to sell Medigap plans to beneficiaries under 65. This means if you qualified for Medicare through ESRD (end-stage renal disease), ALS (Lou Gehrig’s disease), or SSDI (Social Security Disability Income), you could be denied Medigap coverage. Your best bet is to speak with one of our licensed agents. They can help you look for any plans that are available to you and discuss plan specifics. Fill out this form or give us a call at 844-431-1832.

Plan K Reviews

Some of the top Medigap carriers for 2019 include:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

AARP Medicare Supplement Plan K

AARP is a very popular choice when purchasing Medigap Plan K. AARP offers competitive rates that have only been increased an average of 2.9% over the last 5 years. They also provide fast service through the claims process. Most claims are processed within ten days or less. Lastly, AARP has a 98% customer satisfaction service rating. If you’re interested in enrolling in Medigap Plan K with AARP, fill out this form or give us a call at 844-431-1832.

Enroll in Medigap Plan K

You can enroll in a Medicare Supplement plan any time of the year, but if you wait too long, carriers can charge you more or deny you for your health conditions. The best time to enroll is during your initial enrollment period. During this time, you can enroll in any plan that is in your area and not be denied or charged more for pre-existing conditions. A licensed agent can show you available plans in your area and help you save money in the long-run. When you meet with one of our agents, there is never a cost to you and absolutely no obligation to enroll. Fill out this form or give us a call at 844-431-1832.

Does Medicare Cover Urgent Care?

More than 89 million patients visit an urgent care facility each year. In fact, the number of facilities nationwide has increased from 6,400 to 8,100 since 2014 with roughly 600 more expected to open in 2019. Urgent care is a cost-effective way to get the care you need. If you’re wondering if Medicare covers urgent care, look no further, Medicare Plan Finder makes understanding your coverage easy.

Urgent Care Services Covered by Medicare

Urgent care is typically covered by Medicare Part B. It’s important to note that urgent care centers are not required to accept Medicare. While it’s rare for a facility to deny Medicare, it’s ultimately up to the centers and doctors. Part B covers lab tests, x-rays, emergency transportation, durable medical equipment, mental health, and partial outpatient hospitalization. Urgent care centers provide several services that fall under Part B including illness treatment, minor injury care, x-rays, lab tests, annual exams, and immunizations.

Does Medicare Part B pay for Urgent Care?

Yes, Medicare Part B would cover your urgent care costs if certain conditions apply:

You are already enrolled in Medicare Part B

Your Part B deductible ($185 in 2019) is met

You visit an urgent care facility that participates in Medicare

What is the Medicare Copay for Urgent Care?

Typically, after your deductible is met, Medicare Part B will cover 80% of your costs. You will be responsible for a 20% copay. This may be different if you are enrolled in some sort of savings program or plan that covers Part B copayments (like certain Medicare Supplement plans).

Without insurance, urgent care visits can cost over $100. Imagine having to pay only $20 instead of $100!

What Does Medicare pay for Emergency Room Visits?

Medicare will typically pay up 80% of most services, including emergency room visits. That means that you will likely owe 20% of your emergency room bill. This again can differ if you have a certain Medicare Supplement plan or are part of a savings program that covers your copayments and coinsurance.

It’s important to know where the closest urgent care facility that accepts Medicare is. Don’t abuse your local emergency room. Go to an urgent care facility if you are feeling sick and can’t get a doctor’s appointment.

Click on your city below to see urgent care facilities in your area that accept Medicare (we’re adding more cities weekly). If your city is not yet listed, visit medicare.gov to search for facilities near you that accept Medicare.

How Much Does Medicare Pay for Urgent Care Visits?

Urgent care visits cost less than the emergency room, but can still cost $100 on average before insurance. Since urgent care centers cover a wide array of illnesses and injuries, it’s hard to estimate how much your visit will be. However, Medicare will cover 80% of your costs in urgent care. You will be responsible for the remaining 20% and up to $20 copay unless you are enrolled in a Medicare Supplement plan.

Medicare Supplements and Urgent Care

Medicare Supplement (Medigap) plans are financial benefits that can work alongside Original Medicare. They help to cover costs that Original Medicare does not including deductibles, copays, and coinsurance. There are ten plans available (A, B, C, D, F, G, K, L, M, and N), and each letter represents different coverage at a different price point. Medigap plans can help pay for the remaining 20% of your urgent care costs. For example, if you visit an urgent care facility, and had not met your deductible yet, and were billed with a $20 copayment and 20% coinsurance, Medicare Supplements could help with those costs. Depending on which plan you enroll with, you could pay as low as nothing out of pocket.

Medicare Advantage and Urgent Care

Medicare Advantage plans (MA) are required to provide, at a minimum, the same coverage as Original Medicare. This means that urgent care is still covered. However, MA plans offer several benefits that Original Medicare does not including dental, vision, or hearing coverage, and even group fitness classes like SilverSneakers®. It’s important to keep in mind that Medicare Advantage plans have networks so you will need to make sure the urgent care facilities you visit are covered. At Medicare Plan Finder, our licensed agents can help you enroll in a plan that offers the additional benefits you want with the network you need. Why wait? FIll out this form or give us a call at 844-431-1832. Appointments are no cost to you and there’s never an obligation to enroll.

Urgent Care vs. Emergency Room

Urgent care centers and emergency rooms both address your issues quickly and provide same-day relief. They are both covered under Medicare, but trips to the emergency room can leave you with higher out-of-pocket costs and can take longer to get the medical attention you need. It’s important to understand the difference between these facilities so you better understand where to go in the future.

Urgent care centers are intended for injuries or illnesses that are not life-threatening and cannot wait to be treated by your primary care physician. This includes injuries or illnesses like:

Allergic reactions

Muscle sprains

Rashes, cuts, or scrapes

Swelling or irritation

Mild fever

Cold or allergies

Nausea, vomiting or diarrhea

Sore throat

Flu

Emergency rooms are for serious or life-threatening injuries and illnesses that need immediate attention. This includes injuries or illnesses like:

Heart attack

Stroke

Chest pain

Coughing up blood

High fever

Loss of consciousness

Severe wound

Major fracture

Serious burn

Enroll Today

If you’re interested in enrolling in a Medicare Advantage or Medicare Supplement plan, fill out this form or give us a call at 844-431-1832. Our agents are happy to answer any questions regarding plans in your area, eligibility requirements, coverage, costs, and so much more.

What is Medicare Supplement Plan C?

Medicare Supplements, also known as Medigap plans, help cover out-of-pocket expenses that Original Medicare does not. This includes copayments, coinsurance, and deductibles. More than 22% of Medicare enrollees are taking advantage of these financial benefits, and enrollment has increased every year since 2010.

There are more than 10 types of plans (A, B, C, D, F, G, K, L, M, and N) and each plan offers different coverage at different prices. Most plans are guaranteed renewable life, which means as long as you pay your premium on time, you should not be canceled from your plan if a new health condition develops.

Plus, unlike Medicare Advantage plans, Supplements generally include the same coverage regardless of which carrier you enroll with (though some will add additional benefits). If you’re looking for additional financial benefits to supplement your Original Medicare, Medicare Supplement Plan C may be the way to go.

Medicare Part C vs. Plan C

Medicare Part C and Plan C are two very different things. There are four main parts of Medicare (A, B, C, and D). Original Medicare includes Part A, hospital insurance, and Part B, medical insurance. Prescription drug coverage can be purchased through Part D.

Part C is better known as Medicare Advantage (MA). MA plans are offered through private health insurance companies and provide the same coverage as Original Medicare, but with several additional benefits like hearing, vision, and dental coverage, and even fitness programs like SilverSneakers®.

However, Plan C is one of the ten Medicare Supplement plans that are available. You may hear Plan C referred to as Part C, but Plan C is the correct term.

Is Medicare Plan C Going Away?

Medicare Plan C, along with Plan F, will be discontinued in 2020. Plans C and F both include coverage for the Part B deductible, which is a benefit that the Medicare program wants to discontinue. They have found that some consumers are taking advantage of that benefit by visiting their doctor much more often than needed, costing Medicare millions of dollars. That money can be much better spent on providing coverage for people who truly need it.

If you currently have Plan C or Plan F, you will not be kicked off your coverage. If you are interested in enrolling in Plan C or Plan F, you need to do so by January 1, 2020, to be grandfathered in. Click here to get in contact with a licensed agent.

Medicare Supplement Plan C vs. Plan F

Plan F is the most popular Medicare Supplement plan but is very similar to Medicare Plan C. The only difference is that Medicare Plan C does not include Medicare excess charge coverage. If a doctor does not accept Medicare assignment rates, you will be responsible for excess charges, but it can not exceed 15% of what Medicare pays. Some states do not allow doctors to issue excess charges. If this is the case, Plan C will operate identically to Plan F.

What Does Medicare Supplement Plan C Cover?

Medicare Plan C covers all of the gaps from Original Medicare except for Part B excess charges. More specifically, Plan C includes the following:

Part A coinsurance and hospital costs

Part B coinsurance and copayments

Blood work copays up to three pints

Hospice coinsurance and copayments

Skilled nursing facility coinsurance

Part A deductible

Part B deductible

Foreign travel emergency

Plan C Costs

Medicare Supplement plans are generally the same regardless of which carrier you enroll with. This means if you want to enroll in Plan C, you will have the same coverage whether you enroll with Aetna, Cigna, Blue Cross Blue Shield, etc. However, costs will vary based on carrier, zip code, age, gender, and tobacco use. There’s no need to overpay for a plan if there’s a cheaper alternative on the market with identical coverage.

Plan C is an extremely comprehensive Medicare Supplement plan. If you would prefer a less comprehensive plan at a cheaper price point, you should consider Plan A or Plan B. Your best bet is to speak with a licensed agent who can show you all of the Medicare Supplement plans that are available in your area and help you enroll in the plan best suited for your needs and budget.

Plan C Reviews

Here is a list of some of the top Medigap carriers for 2019:

AARP

Aetna

Cigna

Humana

Mutual of Omaha

WellCare

When to Enroll in Medicare Supplement Plan C

You can enroll in a Medicare Supplement plan any time of the year, but carriers can charge you more, (or even deny you), for existing health conditions. The best time to enroll is during your initial enrollment period. This way, you can enroll in any plan that is in your area and not be denied or charged more for pre-existing conditions.

Medigap Plan Finder Tool

A licensed agent can show you available plans in your area and help you save money in the long-run. When you meet with one of our agents, there is never a cost to you and absolutely no obligation to enroll. Fill out this form or give us a call at 844-431-1832.

You can also start comparing different Medigap plans by using our Medigap plan finder tool at medicareplanfindertool.com.

Medicare Supplement Plan B: Costs and Benefits

Medicare Supplement (Medigap) plans help cover out-of-pocket Medicare expenses including co-payments, coinsurance, and deductibles. Enrollment in these plans has increased every year, and more than 22% of Medicare enrollees take advantage of this type of supplemental coverage in 2019.

There are ten types of Medicare Supplement plans (A, B, C, D, F, G, K, L, M, N) and unlike Medicare Advantage plans, they provide the same basic benefits regardless of which carrier you enroll with.

Plus, most plans are “guaranteed life,” which means that as long as you pay your premium on time, you won’t be canceled from your plan if a new health condition develops.

Medicare Supplement plans are great for beneficiaries who would rather pay a small annual deductible for financial protection in the event of an unforeseen health expense.

What does Medicare Supplement Plan B Coverage Include?

Medicare Supplement Plan B is very similar to Medicare Supplement Plan A. The only difference is Plan B covers your Medicare Part A deductible. Plan B covers:

Part A coinsurance and hospital costs

Part B coinsurance and co-payments

Bloodwork co-payments (up to 3 pints)

Hospice coinsurance and co-payments

Part A deductible

Medicare Plan B Cost

Even though the benefits are mostly the same per carrier, the costs of the plan will vary based on carrier, zip code, age, gender, and tobacco use. Some plans are as low as $80/ while some are as high as $140/month.

The fewer benefits a plan provides, the lower the monthly premium is. Since Plan B offers less coverage, it is typically one of the cheapest plans on the market.

Medicare Plan B Deductible

If you choose to enroll in a Plan B Medicare Supplement plan, you will be responsible for your Part B deductible, but your Part A deductible will be included in your plan. The 2019 Medicare Part B deductible is $185.

You will also be responsible for any skilled nursing facility care coinsurance, Part B excess charges, and emergency health costs while traveling. This is great if you rarely see unexpected health costs and would rather have lower monthly costs than high premiums for benefits you don’t use.

If you generally have high costs in the areas that Plan B does not cover, it may not be the best plan for you. Instead, you should consider the more comprehensive Plan G. Alternatively, if Plan B sounds great, but you would prefer a cheaper monthly payment, you should explore Plan A, which has fewer benefits but typically has the lowest costs.

Medicare Supplement Plan Finder | Medicare Plan Finder

Medicare Supplement Plan B vs. Medicare Part B

Medicare Plan B and Medicare Part B are two entirely different things but can be easily confused. Medicare Supplement Plan B is a Medigap plan and Medicare Part B works alongside Part A to form Original Medicare. It covers medically necessary doctor services and treatments as well as preventative services like yearly wellness visits. This includes lab tests, x-rays, emergency transportation, durable medical equipment, mental health, and partial hospitalization. If you want to enroll in Plan B (or any Medicare Supplement), you need to be enrolled in Part A and B first.

Medicare Supplement Plan B Options

There are several Medicare Supplement plans on the market, but availability will vary based on your location. As we’ve mentioned, plans generally offer the same coverage regardless of carrier, so why do some plans have better reviews? Companies with higher ratings generally offer plans with higher ratings. Customer service is another factor. Here is a list of the top Medigap carriers in 2019:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

Use Our Medicare Supplement Plan Finder Tool to Find Plan B Options in Your Area

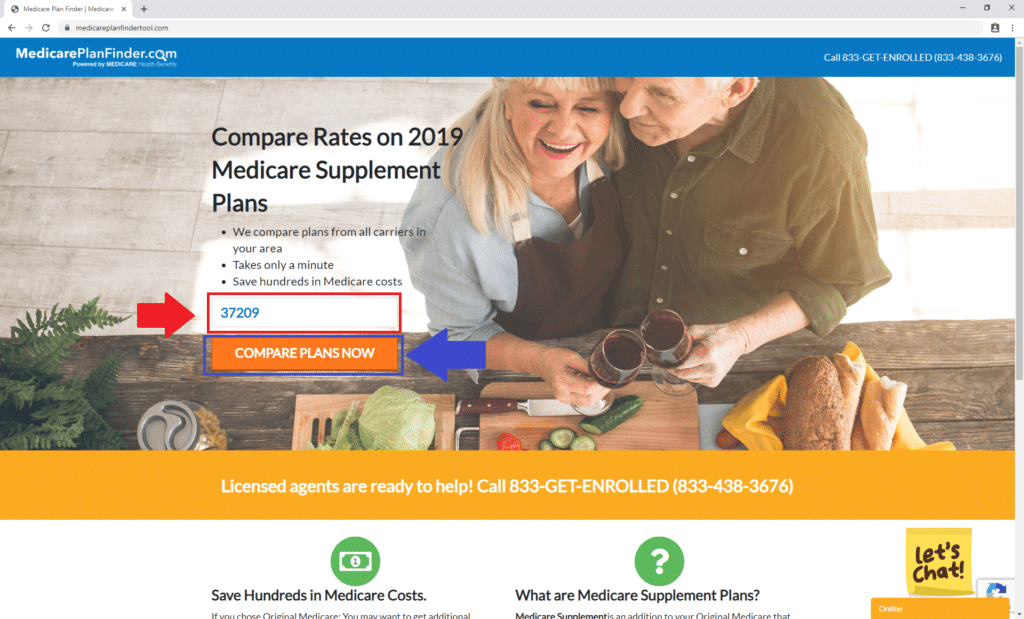

Our Medicare Supplement Plan Finder tool can help you find Plan B options in your area. Click here to get started. Enter your zip code in the box beside the red arrow. We chose 37209 because that’s the zip code for our corporate offices in Nashville, Tennessee.

Medicare Supplement Finder Tool Step 1 | Medicare Plan Finder

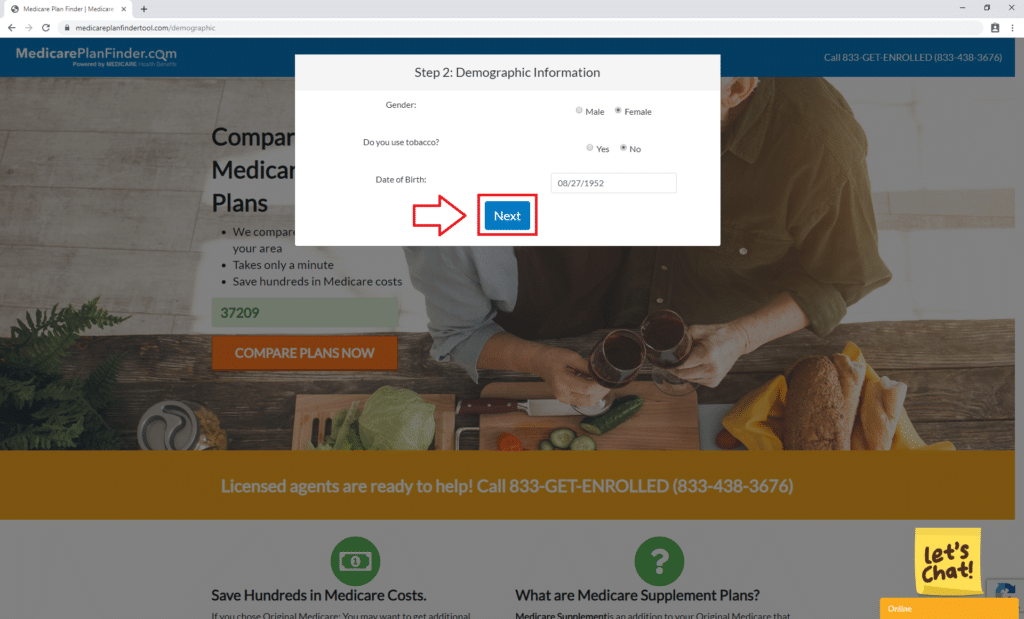

Next, choose the appropriate circles for your gender and tobacco use and enter your date of birth. Then click “Next.”

Medicare Supplement Finder Tool Step 2 | Medicare Plan Finder

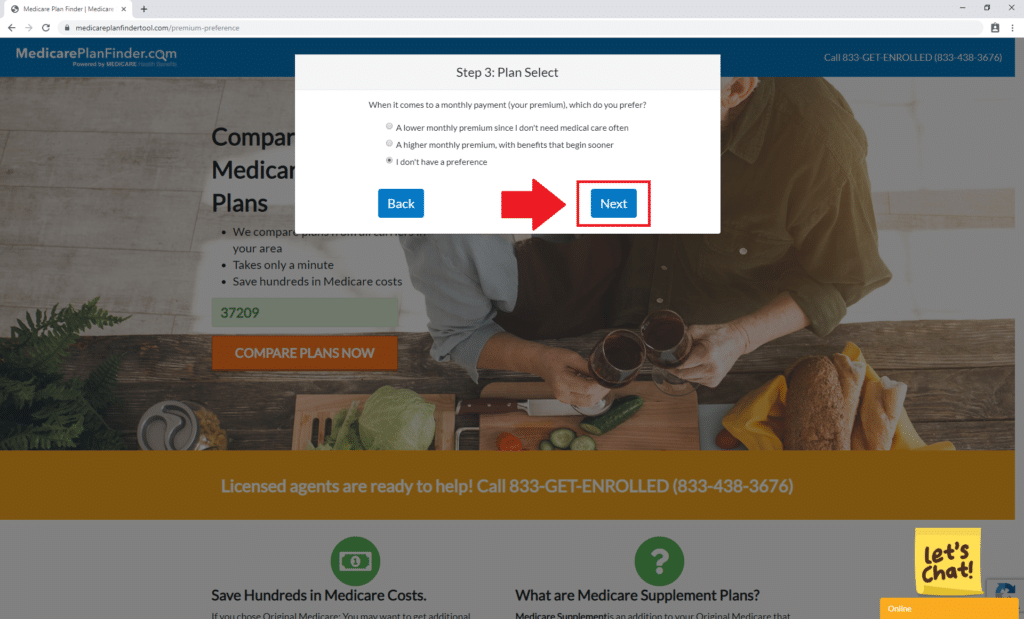

Then select your plan preference and click “Next.”

Medicare Supplement Finder Tool Step 3 | Medicare Plan Finder

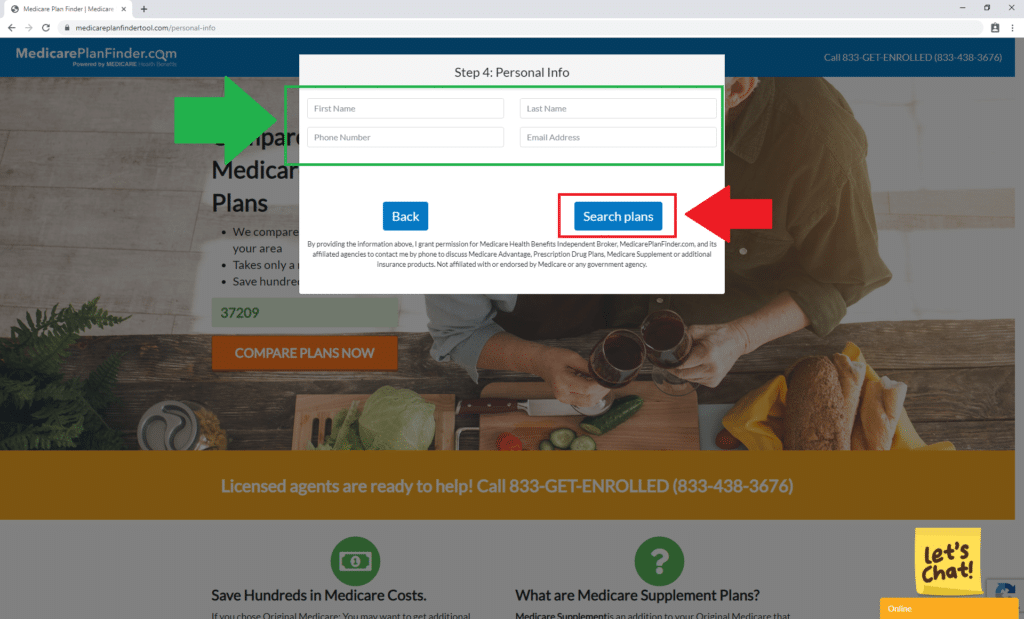

Next enter your personal information in the boxes beside the green arrow. Then click “Search plans” beside the red arrow.

Medicare Supplement Finder Tool Step 4 | Medicare Plan Finder

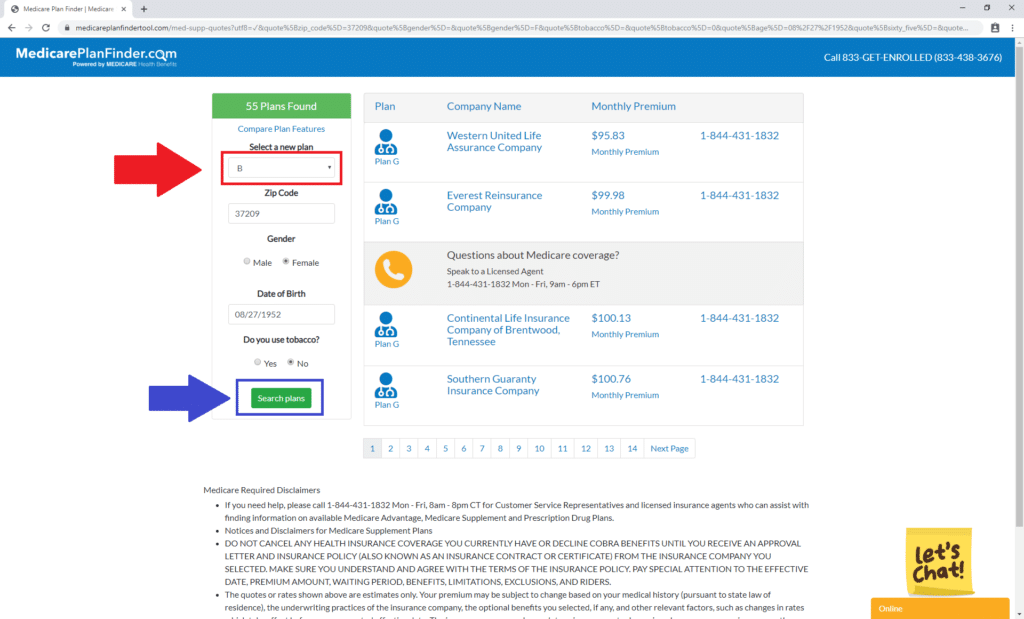

The final step is viewing the Plan B options in your area. Select “B” from the drop-down menu beside the red arrow. Then click “Search plans” beside the blue arrow.

Medicare Supplement Finder Tool Step 5 | Medicare Plan Finder

Medicare Plan B Enrollment

You can enroll in a Medicare Supplement plan during any time of the year, but carriers can deny you or charge you more for existing conditions. The best time to enroll is during your Initial Enrollment Period (IEP), which is the seven months around your 65th birthday. During this time, you can enroll in any plan that is available in your area regardless of any health issues you may have.

If saving money is important to you, a licensed agent can help you enroll in the cheapest plan available in your area. When you meet with one of our agents, there is never an obligation to enroll, and the appointment is entirely cost-free to you. Fill out this form or give us a call at 844-431-1832.

Medicare Supplements | Medicare Plan Finder

What is Medicare Supplement Plan A?

Medicare Supplement Plan A is often referred to as Medigap Plan A or Medicare Plan A. Like other Medicare Supplements, Plan A helps cover the gaps that Original Medicare does not, including coinsurance, copayments, and deductibles. There are ten types of Medicare Supplement plans (A, B, C, D, F, G, K, L, M, N).

About Medicare Supplements

Most plans are guaranteed renewable life, meaning as long as you pay your premium on time, you won’t be canceled from your plan due to a new health condition. Plus, unlike Medicare Advantage plans, Medigap plans are generally the same no matter which carrier you enroll with. If you’re looking for coverage assistance, a Medigap plan may be the way to go – but which one? Here’s everything you need to know about Plan A.

What does Medicare Supplement Plan A cover?

Plan A offers the least amount of benefits among all Medicare Supplements, but that doesn’t mean you shouldn’t consider it! The less benefits a plan provides, the lower the monthly premium is. Since Plan A offers the least coverage, it is typically one of the cheapest plans on the market. Plan A covers:

Part A coinsurance and hospital costs

Part B coinsurance and co-payments

Bloodwork co-payments (up to 3 pints)

Hospice coinsurance and co-payments

Plan A Costs

All Medigap plans provide the same basic benefits regardless of which carrier you choose. This means if you want to purchase Plan A, you will have the same coverage whether you enroll with Aetna, Blue Cross Blue Shield, or Cigna, etc. However, here’s the catch… the costs will vary based on carrier, zip code, age, gender, and tobacco use. Some plans are as low as $70/month while some are as high as $140/month. Certain plans can add extra benefits, like SilverSneakers®, but this is rare.

If you choose to enroll in a Plan A Medicare Supplement plan, you will be responsible for your Medicare Part A and B deductibles. You will also be responsible for any skilled nursing facility care coinsurance, Part B excess charges, and emergency health costs while traveling. This is great if you rarely see unexpected health costs and would rather have lower monthly costs than high premiums for benefits you don’t use.

You know your health better than anyone, and if you generally have high costs in the areas that Plan A does not cover, it may not be the best plan for you. Instead, you should consider the popular, more comprehensive, Plan G.

Plan A Reviews

If the benefits are going to be mostly the same no matter which carrier you choose to go with, why do the prices differ? There is no reason to overpay when the benefits are the same. There are so many top rated companies that sell Medigap. Companies with higher ratings have plans with higher ratings. Customer service is also an important factor. Here is a list of the top Medigap carriers for 2019:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

Plan A for Disabled People

If you are under 65 and qualify for Medicare through a disability, you may be able to enroll in a Medicare Supplement plan. The availability of these plans will vary depending on where you live. Federal law doesn’t require companies to sell you a plan if you are under 65 unless you live in California, Massachusetts, or Vermont. These states are required to offer at least one Medigap policy. Other states may offer Medigap plans, but they are not required to by law. Policies for those under 65 often cost more, so you may want to consider a Medicare Advantage plan instead.

Medicare Part A vs. Plan A

Medicare can be confusing, and it’s easy to confuse all the different parts and plans. We don’t want you to confuse Medicare Supplement (Medigap) Plan A with Medicare Part A. Part A is part of Original Medicare and covers hospital care, skilled nursing facility care, hospice, and home health services. Plan A is one of the ten Medicare Supplement Plans. You may hear Plan A referred to as Part A, but Plan A is the correct term. Here’s an easy way to remember it: Medicare only has four parts (A, B, C, and D), while all Medicare Supplements are referred to as plans.

Enroll in Medicare Supplement Plan A

The best time to enroll in a Medicare Supplement plan is during your initial enrollment period (three months before and after your 65th birthday). During this time, you can enroll in any plan that’s available in your area regardless of any health issues you may have. Outside of your IEP, you can enroll year around, but carriers can deny you or charge you more for existing conditions. Your best bet is to speak with a licensed agent. There is never a cost for meeting with one of our agents, and you are never obligated to enroll. Fill out this form or give us at a call at 844-431-1832.