Additional Benefits with Medicare Advantage Plans: What You Need to Know

When exploring Medicare options, Medicare Advantage plans stand out due to their potential to offer benefits beyond what Original Medicare covers. These additional benefits can significantly enhance your healthcare coverage, but it’s important to remember that not all Medicare Advantage plans are the same. Each plan varies in the additional benefits offered, making it crucial for beneficiaries to compare plans carefully based on their health needs and preferences.

Understanding Medicare Advantage Plans

Medicare Advantage plans are offered by private insurance companies approved by Medicare. They provide all the benefits of Medicare Part A and Medicare Part B, often combined with other health services that Original Medicare does not cover. The inclusion of additional benefits is one of the primary reasons these plans have gained popularity among Medicare beneficiaries.

Types of Additional Benefits

Dental, Vision, and Hearing Care

Most notably, many MA plans include coverage for dental, vision, and hearing care—services not covered by Original Medicare. Dental benefits might cover routine check-ups, cleanings, x-rays, and even some types of dental surgery. Vision care often includes eye exams, glasses, or contact lenses, while hearing care might cover hearing aids and auditory exams.

Wellness Programs

Many plans incorporate wellness programs such as fitness memberships or discounts on health and wellness services. These benefits are designed to promote a healthy lifestyle among seniors, which can help prevent or manage common diseases associated with aging.

Over-the-Counter Allowances

Some MA plans offer allowances for over-the-counter (OTC) products such as vitamins, pain relievers, and first aid supplies. This benefit can be particularly helpful as it reduces out-of-pocket costs for everyday health items.

Telehealth Services

With the growing popularity of digital health services, many MA plans now include telehealth benefits, allowing beneficiaries to consult with healthcare providers from the comfort of their homes. This is especially beneficial for those with mobility challenges or those living in remote areas.

Transportation Benefits

Transportation to and from healthcare facilities can be a significant hurdle for many seniors. Some MA plans offer transportation benefits, which can be a deciding factor for those who do not have easy access to transportation or who are unable to drive.

Nutritional Support

Recognizing the importance of nutrition in health, some plans provide benefits aimed at nutritional support, including meal deliveries, especially after hospital stays, or nutritionist consultations to help manage dietary needs.

Choosing the Right Plan

When selecting a Medicare Advantage plan, consider the following steps:

Assess Your Health Needs: Understand your specific health requirements—do you need regular vision or dental services, or are you managing a chronic condition that might benefit from wellness programs?

Compare Plans in Your Area: Not all plans are available in every location, and benefits can vary widely between plans. Use the Medicare Plan Finder tool or consult with a licensed insurance advisor to compare the plans available in your area.

Read the Fine Print: Once you’ve narrowed down your choices, look closely at the plan’s summary of benefits to understand what is and isn’t covered, and at what cost. Pay attention to any specific limitations or rules regarding how you can use the benefits.

Check Provider Networks: Ensure that your preferred doctors and hospitals are included in the plan’s network. Medicare Advantage plans often have network restrictions, and going out of network can result in higher out-of-pocket costs.

Review Star Ratings: Medicare rates plans based on quality and performance. These ratings can help you understand the quality of care and customer service you can expect from different plans.

Conclusion

Medicare Advantage plans can offer a range of additional benefits that enhance your healthcare experience, but the key is to choose wisely based on your personal health needs and circumstances. By doing thorough research and understanding the specifics of each plan, you can find a Medicare Advantage plan that not only meets your health needs but also enhances your quality of life through additional benefits.

Does Medicare Cover the Cost of Hip Replacement Surgery?

An estimated 2.5 million Americans have undergone total hip replacements. Conditions such as osteoarthritis and rheumatoid arthritis can cause the hip joint to wear down so much that a hip replacement may be the only course of action to improve your mobility.

The total cost of hip replacement surgery can be staggering if you don’t have help from insurance. How much does a hip replacement cost with insurance?

A total hip replacement costs anywhere from $32,000 to $45,000, based on general coverage guidance from healthcare.gov. The total cost usually includes everything from the surgeon’s initial evaluation to post-operation hospital care.

Increases in year-to-year costs are small under stable economic conditions. There was only a small increase in hip replacement 2019 costs compared to medicare hip replacement 2018 costs.

If you’re one of the millions of Americans who needs a hip replacement, you may wonder, “Does Medicare cover hip replacements?” Yes, but you have to meet certain eligibility requirements, and you may still have some out-of-pocket costs even with Original Medicare.

You may also be asking, “How much does Medicare pay for hip replacement surgery?” The good news is that it will cover at least some of all types of costs.

Find Medicare Plans | Medicare Plan Finder

How Much Does Medicare Pay for Hip Replacement Surgery?

Cost of Hip Replacement Surgery with Medicare | Medicare Plan Finder

The likelihood of needing hip replacement surgery increases with age. Seniors 65 and older, people with ALS or ESRD, or people who have received SSDI for at least 25 months qualify for Medicare.

Original Medicare (Parts A and B) will help cover the cost of hip replacement surgery if your doctor determines it’s medically necessary because other treatments have failed. The answer to how much Medicare pays for hip replacement surgery will depend on whether it is medically necessary and what types of coverage you have.

Medicare Hip Replacement Costs With Medicare Part A

Medicare Part A is hospital insurance. This Medicare coverage helps pay for a semi-private room, meals and nursing care during your stay.

Part A will only cover a private room if your doctor says it’s medically necessary or it’s the only room available.

Medicare hip replacement reimbursement includes skilled nursing care after your surgery. Part A helps cover the first 100 days of in-patient care including physical therapy.

The Medicare Part A deductible can apply, and you may be responsible for copays or coinsurance.

Part B Coverage for Hip Replacement Surgery

Medicare Part B will help cover medical expenses such as doctor’s fees for the initial evaluation and post-op visits, surgery in an outpatient surgical facility, and outpatient physical therapy.

You may be responsible for paying the Part B deductible, which was $185 in 2019, and 20% of the Medicare-approved costs. Medicare Part B may also cover your post-operative durable medical equipment (DME) such as a cane or in-home grab bars.

Medicare Part D Coverage

Original Medicare does not cover post-op prescription drugs, but Medicare Part D includes prescription drug coverage. Your doctor may prescribe blood thinners to prevent clotting or painkillers to take during your recovery.

You can use Medicare Part D or private health insurance plans to cover prescription drugs.

Will Medicare Help Pay for a Knee Replacement?

Medicare Part A and Medicare Part B each cover a different aspect of joint replacement surgery. Medicare Part C will cover knee replacement, including both knees at once, only if your doctor considers it necessary.

Medicare Part D prescription drug program will cover the cost of painkillers, antibiotics, and anticoagulants required for the surgery.

What Medicare Advantage and Medicare Supplements Cover

Private insurance plans offer Medicare Advantage (MA) plans, and they are a great way to get all of the Part A and Part B benefits along with some unexpected offerings such as meal delivery, non-emergency transportation, vision and dental insurance.

Certain MA plans even cover prescription drugs! You will pay a monthly premium with MA plans, but some are as low as $0. Coverage varies depending on your location and the plans available, so look for a qualified professional to help you sort through the plans in your area and find the right one.

Medicare Supplement (Medigap) plans pick up where Original Medicare leaves off. Like MA plans, private insurance companies offer Medigap plans.

The difference is that Medigap Plans only cover your financial responsibilities such as coinsurance and deductibles. You cannot have both a Medicare Supplement and a Medicare Advantage plan at the same time, so it’s important to find out which one is best for you.

Medicare Supplement Insurance plans work with Medicare Part A and Medicare Part B to cover out-of-pocket costs for Medicare hip replacements.

Post-Hip Replacement Surgery Costs

Does medicare cover rehab after hip replacement? Yes. Sometimes, after hip replacement surgery, you may need some help.

For example, throughout your recovery, you might need orthotic devices or other equipment to help you get around. Medicare may cover those devices if your doctor says that they are medically necessary.

Some Medicare Advantage plans may provide extra coverage, and Medicare Supplement plans may cover your copayments for devices.

You also might be interested in Medicare Advantage plans that have an OTC or over-the-counter benefit. This can help offset some of your costs related to pain medication and other items you need to pick up from your pharmacy for your recovery.

Additionally, some people may need physical therapy to recover from surgery or other hip injuries. Medicare Part B may cover your physical therapy by as much as 80%, as long as it is deemed medically necessary.

Why You Might Need a Hip Replacement

Several conditions can cause the hip to deteriorate to the point of needing surgery including:

Hip replacement surgery can restore the hip joint and full range of motion. The type of replacement you receive depends on the doctor’s recommendation and your general health.

The surgery may use a cemented or uncemented prosthesis to connect the replacement parts to the healthy bone after the unhealthy cartilage is removed. The entire recovery process can take three to six months.

Understanding the Hip Replacement Procedure (Orthopedic Hip Arthroplasty)

Hip arthroplasty, also known as total hip replacement, is a common orthopedic procedure. During the surgery, your damaged bones and some soft tissue are removed.

The hip joint is replaced with an implant, which can be ceramic, plastic, or metal.

In a traditional replacement, a 10-12 inch incision is made on the side of the hip. In less-invasive procedures, the incision may only be three to six inches.

Some people may not be eligible for a minimally invasive procedure. Be sure to ask your doctor if you aren’t sure what your procedure will be like.

Man Discussing the Cost of Hip Replacement Surgery With Medicare With His Doctor | Medicare Plan Finder

Medicare Hip Replacement Scenario

To better understand how everything works together, let’s take the real-world example of a 75-year-old man who has osteoarthritis.

He’s been working with his doctor to manage his symptoms, and things have been going well. One day, the man takes a nasty fall and breaks his hip. This man’s Medicare hip replacement process involves several steps:

He doesn’t go to the hospital right away because the bruising around his hip looks like one of his routine injuries. The man makes another doctor’s appointment, and his doctor takes X-rays and determines the man will need a hip replacement.

His doctor will determine if the man is healthy enough for surgery, and then the doctor refers the man to an orthopedic surgeon. Until this point, everything falls under Medicare Part B.

The man decides to have his surgery in an outpatient facility. He’s responsible for his deductible if he hasn’t met it, or the out-of-pocket maximum for his plan.

The surgery is successful, so he has physical therapy appointments so he can recover as quickly as possible. The man has a Medicare Advantage Prescription Drug plan, so he collects his blood thinners and painkillers for only a small copayment at the pharmacy.

Along with prescription drugs, the man’s surgeon prescribes a cane and grab bars to help the man perform daily tasks. The man’s MA plan also covers those items, because his doctor determined they are medically necessary.

Contact Us Today

A comprehensive Medicare plan can help cover the cost of hip replacement surgery. If you need help finding coverage, we can help! Call us at (833)-567-3163 or contact us here today.

Contact Us | Medicare Plan Finder

This post was originally published on May 15, 2019, and updated on March 24, 2020.

Does Medicare Cover Dental Implants?

Sometimes plaque and tartar can build up to the point where the accumulation irritates the gums and cause damage to your teeth. The irritation and damage can even result in tooth loss. A dentist might recommend a dental implant to solve the problem.

If you’re one of the many people who need dental implants and you have Medicare insurance, you probably have a lot of questions such as, “What are dental implants,” and, “Does Medicare cover dental implants?”

What Are Dental Implants?

A dental implant is an artificial tooth with a titanium post that’s surgically attached to your jaw. About 450,000 people have dental implants every year.

Does Medicare Cover Dental Implants? | Medicare Plan Finder

Original Medicare and Medicare Advantage Dental Coverage

Does original Medicare cover dental implants?

No. Original Medicare (Part A and Part B) does not cover dental implants or routine dental care.

Are dental implants covered by Medicare advantage plans?

Sometimes. This means some plans do and some plans don’t.

Private insurance policies called Medicare Advantage (MA) plans can offer coverage for additional services Original Medicare does not, including dental services. Sometimes the dental services offered include implants and sometimes they only include routine cleanings and x-rays.

If you need dental insurance, an agent with Medicare Plan Finder can work with you to find a Medicare Advantage plan in your area that offers dental implants. Some plans also offer coverage for vision, hearing and even fitness classes along with all of the services that Original Medicare covers.

Some people may find that their Medicare Advantage plan does not cover all of their dental needs. Those people may need additional dental coverage from private policies called commercial dental insurance plans to cover major procedures such as dental implants.

How to check if your Medicare Advantage plan covers dental implants.

In order to determine if your current plans covers dental implants, you’ll need to check the summary of benefits you received when you first enrolled in your plan.

There should be a section in your summary of benefits that will specifically address the dental benefits included as well as specifically covered benefits such as implants, dentures, cleanings, and x-rays.

As mentioned, every plan offers different benefits, so you should always verify with your plan summary benefits to be sure. If you do not know how to find your summary of benefits, you should call your insurance company or speak to a licensed agent.

Does Medicare Supplement Cover Dental Implants?

No. Medicare supplement plans do not cover dental implants.

Medicare Supplement (Medigap) plans can help pay for financial items such as copays and coinsurance that can come with Original Medicare.

Unlike Medicare Advantage plans, Medigap policies do not offer additional benefits. That means that a Medicare Supplement plan will not pay for routine dental care or dental implants. You cannot have both a Medicare Advantage policy and a Medigap plan at the same time, so it’s a great choice to learn the difference between the two.

A licensed agent with Medicare Plan Finder can help you determine what you need, and what’s available in your area. To learn more, call (833)-567-3163.

Does Medicaid Pay for Dental Implants?

Medicaid is both federally and state-funded. The program helps people who qualify to pay for their health insurance. Every state has different rules about dental coverage. While most states provide at least emergency dental services for adults, not all states provide comprehensive dental coverage.

If you qualify for Medicaid and have questions about what services your state covers, contact your local Medicaid office.

Elderly Dental Problems and Their Solutions

Tooth loss is not an inevitable part of aging, but many seniors can develop diseases which can make dental implants or other solutions a necessity. Conditions that affect older adults include dry mouth, gum disease, and oral cancer.

Dry Mouth

Many medications that treat common senior conditions have dry mouth as a side effect. Dry mouth can lead to cavities, which ultimately lead to gum disease. If you have dry mouth as a medication side effect, talk to your doctor about what drugs you take and the dosages.

Your doctor may change your prescriptions or recommend over-the-counter oral moisturizers or drinking more water. In order to further prevent cavities, your dentist may apply fluoride treatments.

Gum Disease

Periodontal, or gum disease results from bacteria in plaque irritating the gums. The gums become swollen and are more likely to bleed. Periodontal disease is widespread among older adults because it’s often painless until it becomes severe and many people don’t have regular dental exams.

If gum disease goes untreated, the gums can recede from the teeth and form spaces that can collect food particles and more plaque. Advanced periodontal disease can destroy the gums and the bones and ligaments that support the teeth. Your dentist can treat or help you prevent gum disease, so it’s important that you have regular check-ups.

Oral Cancer

Oral cancer is an uncontrollable growth of invasive cells that causes damage to the mouth, tongue, and throat. It can be life-threatening if it’s not treated early. Along with regular dental visits, you can prevent oral cancer by avoiding tobacco or heavy alcohol use.

Other risk factors include a family history of cancer, excessive sun exposure and having HPV. About 25 percent of oral cancer cases are people who don’t smoke or who only drink occasionally. Treatment for oral cancer involves surgery to remove the cancerous cells, or radiation and chemotherapy.

Does Medicare Cover Dentures or Other Alternatives to Traditional Dental Implants?

Dental Exams | Medicare Plan Finder

Some people may not be able to receive dental implants. For example, if your jaw cannot support a dental implant, a dental specialist will have to find an alternative.

Dental Implant Alternatives

Bridges: This alternative uses artificial teeth supported by crowns that attach to the natural teeth to solve the dental issue.

Full or Partial Dentures: Full dentures are a dental implant alternative for people who have lost most of their natural teeth. They are removable artificial teeth secured to a support piece in the mouth. Partial dentures are for people who have most of their natural teeth still, and they attach to natural teeth with metal clasps.

“Teeth in a Day”: Traditional dental implants require a lengthy recovery period that can last up to two years. “Teeth in a Day” is a procedure that uses computer-guided technology to find the best placement for implants and accurately insert new posts in an hour.

If you take care of your teeth, you can avoid many of the issues that contribute to tooth decay, gum disease, tooth loss, and ultimately avoid needing assistance with dental implants. A strong oral hygiene routine includes:

Brushing twice daily with fluoride toothpaste

Flossing between your teeth every day to remove plaque

Limiting alcoholic beverages

Refraining from smoking or chewing tobacco

Regular dental visits even if you have no natural teeth or you have dentures

Visiting your doctor or dentist if you experience abrupt changes in taste or smell

Working to control diabetes, which will decrease the risk of gum disease and other conditions

Many older adults will need assistance with everyday grooming and self-care. If you’re a caregiver, you can help the people you care for avoid gum disease by flossing and brushing their teeth every day and bringing them to their dentist visits.

Let Us Help You Find Dental Plans That Cover Dental Implants

Even though Medicare does not cover dental implants, the right Medicare Advantage plan or commercial dental insurance plan can help pay for the treatments your dentist recommends. Call (833)-567-3163 or contact us here to arrange an appointment with a licensed agent.

This post was originally published on June 12, 2019, and updated on January 15, 2025.

7 Important Things You Never Knew About Medicare

What is Medicare? Most people are familiar with short answer: Medicare is a federal health insurance program that covers people over the age of 65, people with certain disabilities, or those who suffer from either ESRD (end-stage renal disease) or ALS (Lou Gehrig’s Disease).

While this is probably the easiest way to explain Medicare, most people don’t know how complicated it can be once you dive below the surface. Here we’ve broken down the 7 most important facts about Medicare that you may have never heard before!

1. There are multiple parts of Medicare

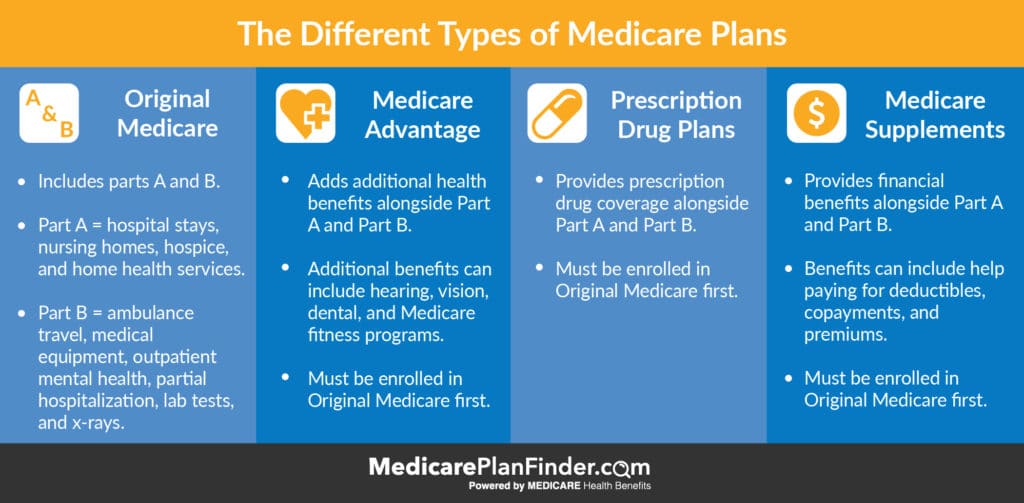

Perhaps the biggest misconception about Medicare is that it’s one gigantic program. In truth, what we refer to as Medicare actually has four distinct components, or “parts.” You might hear some different names used but usually these parts will be designated as A, B, C, or D.

The Original Medicare program consists of Part A and Part B. Part A primarily covers inpatient hospital care, while Part B handles outpatient services like doctor visits. These two components of Original Medicare represent the basic coverage that is available to you when you turn 65.

Part C, often called Medicare Advantage plans, are offered by private health insurance companies. These allow recipients of parts A and B to also receive benefits like dental, vision, and prescription drug coverage depending on the plan they choose.

Medicare Advantage | Medicare Plan Finder

Part D, sometimes called a prescription drug plan (PDP), offers prescription drug coverage to beneficiaries enrolled in Medicare. These are offered by private insurance companies as an addition to the Original Medicare benefits, as Original Medicare does not include any drug coverage.

2. You can’t enroll whenever you want

Unfortunately, Medicare is not a program you can just enroll in at any time. It’s true that you are eligible for Medicare when you turn 65, but unless you qualify for automatic enrollment, you will need to sign up during one of the five designated enrollment periods.

The Initial Enrollment Period (IEP) is usually your primary opportunity for Medicare enrollment. If you are aging into the program, this IEP begins three months before your 65th birthday and extends to three months after, giving you seven months in total to enroll.

There is actually a second IEP, sometimes called IEP2, available for those who are eligible for Medicare before they turn 65, such as those with disabilities. This period also lasts seven months and gives these beneficiaries an opportunity to make changes to their plan.

The General Enrollment Period (GEP) is offered for first-time Medicare enrollees who did not join during their IEP. This period occurs every year from January 1 to March 31. Coverage applied for during this period begins on July 1st.

The AEP, or Annual Enrollment Period, starts every 10/15 and runs until 12/7. This period provides an opportunity for those already enrolled in Medicare to make changes to their coverage, such as adding a Part D plan or converting your Original Medicare to a Medicare Advantage plan.

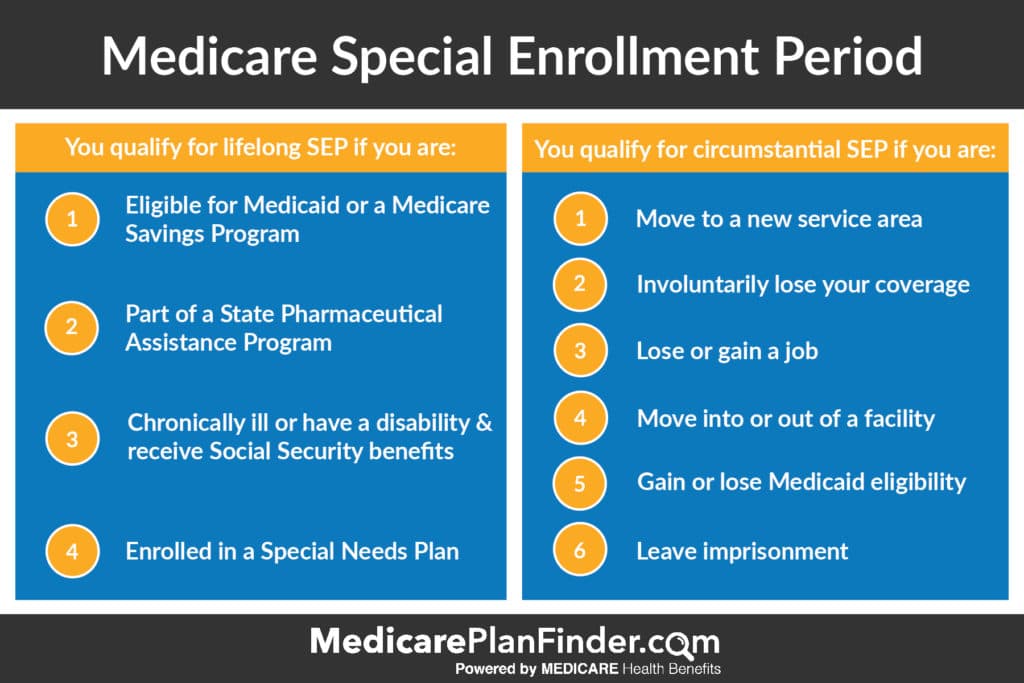

Special Enrollment Periods (SEPs) allow Medicare beneficiaries to make changes to their coverage outside of AEP. During these periods, people who are enrolled in a Special Needs Plan or who have recently lost a job can add to or switch their coverage. Check out the handy graphic below to see if you qualify for one of these SEPs.

Special Enrollment Period | Medicare Plan Finder

In 2019, a new enrollment period was introduced, called the Open Enrollment Period, or OEP. This period lasts from 1/1 to 3/31, and lets those who enrolled in Medicare Advantage during AEP make changes in their coverage without having to wait for the next AEP.

3. You may have to pay if you delay

If you do miss your IEP, you may have to pay penalties when you finally do enroll. The amount you will pay and the duration you will have to pay depends on which part of Medicare you enroll in and how long you waited.

The Part A penalty is incurred if you do not qualify for free, automatic enrollment and you fail to sign up for it when you are eligible. This penalty will be added to your premium to the tune of 10%, which you will have to pay for twice the number of years that you neglected to sign up.

If you enroll late in Part B, your premium will go up by about 10% for every year you were eligible but didn’t sign up. You will then have to pay this increased premium for the entire time you have Medicare Part B. You may also have to pay a penalty if you do not enroll in a Part D plan within the first three months that your Parts A & B are active. However, some of these penalties may be avoided if you qualify for a Special Enrollment Period.

4. Original Medicare only covers 80%

Once you are finally enrolled, you might wonder: “How much does Medicare cover?” The unfortunate truth is that it will not fully cover your medical expenses. Parts A & B will only cover up to 80% of the cost of Medicare-covered services, leaving you to pay the remaining 20% coinsurance.

This might not be too much trouble for routine doctor visits, but in the case of a medical emergency or hospital stay, the amount you pay out-of-pocket can skyrocket quickly. To cover that last 20%, consider purchasing a Medicare Supplement plan to add on to your Original Medicare coverage.

5. Original Medicare doesn’t cover dental, hearing, or vision

Many people might not realize that Medicare covers very little in the way of dental and hearing expenses, and virtually nothing when it comes to vision. Part A will sometimes pay for specific dental services if you have to get them while you are staying in a hospital, but will not pay for cleanings, fillings, dentures etc.

Medicare will sometimes cover diagnostic hearing exams if your physician orders it as part of their treatment, but will not cover hearing aids under any circumstances. For vision coverage, your options with Original Medicare are even more limited, as it will not pay for eye exams, glasses, or contact lenses.

There are some options that can provide vision, hearing, and dental coverage for seniors. A DVH (or Dental, Vision, Hearing) plan can be purchased to add to your Original Medicare benefits, or you might look to a Medicare Advantage policy to consolidate all of that coverage into one plan.

If you think Part C might be the best coverage option for you, click here or give us a call at (833)-567-3163 to have a licensed agent help you compare Medicare Advantage plans!

6. Original Medicare will not cover you abroad

Aside from a few very specific circumstances, Medicare Parts A and B will not cover your health care while you are traveling outside the United States. Medicare Part D plans are also invalid once you are more than 6 hours away from a U.S. port.

But there are some Medicare coverage options available for foreign travel, primarily in the form of Medicare Supplement (Medigap) plans.

7. Supplement plans have the same coverage, different cost

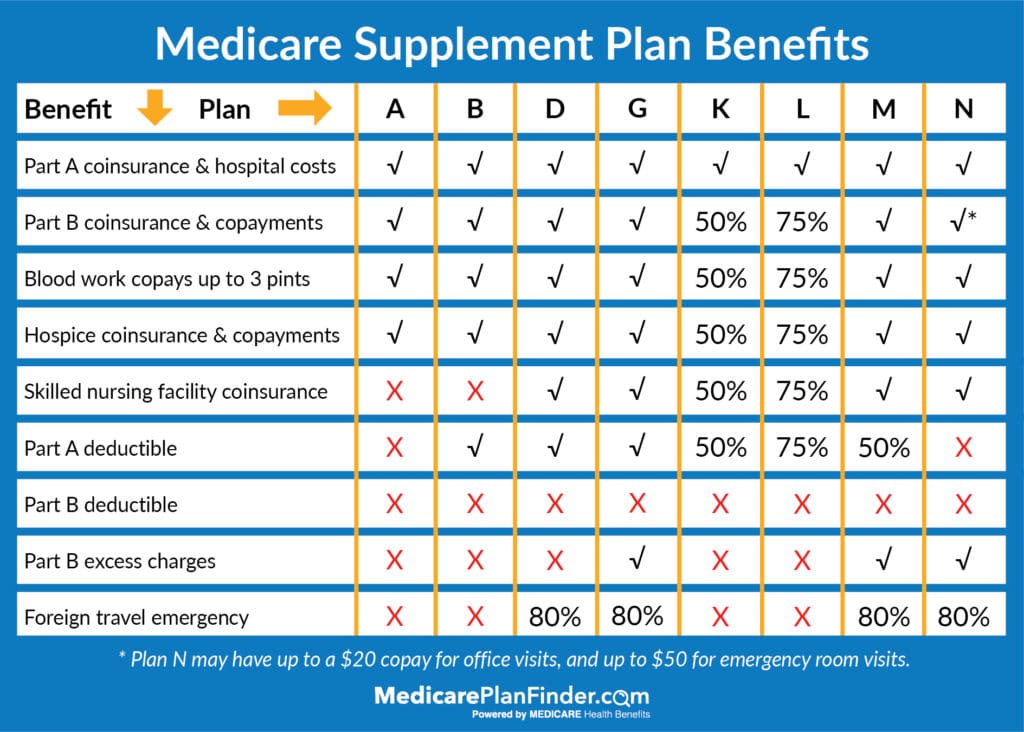

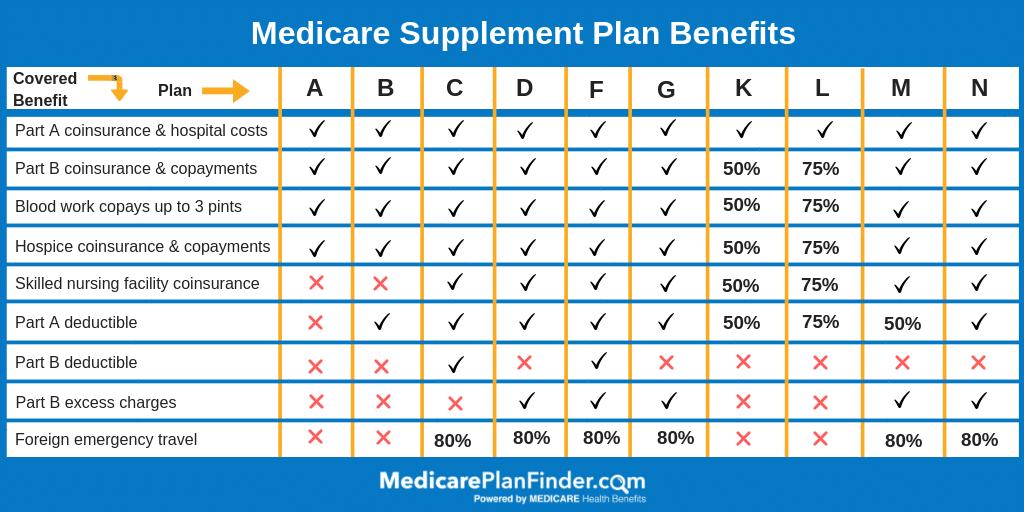

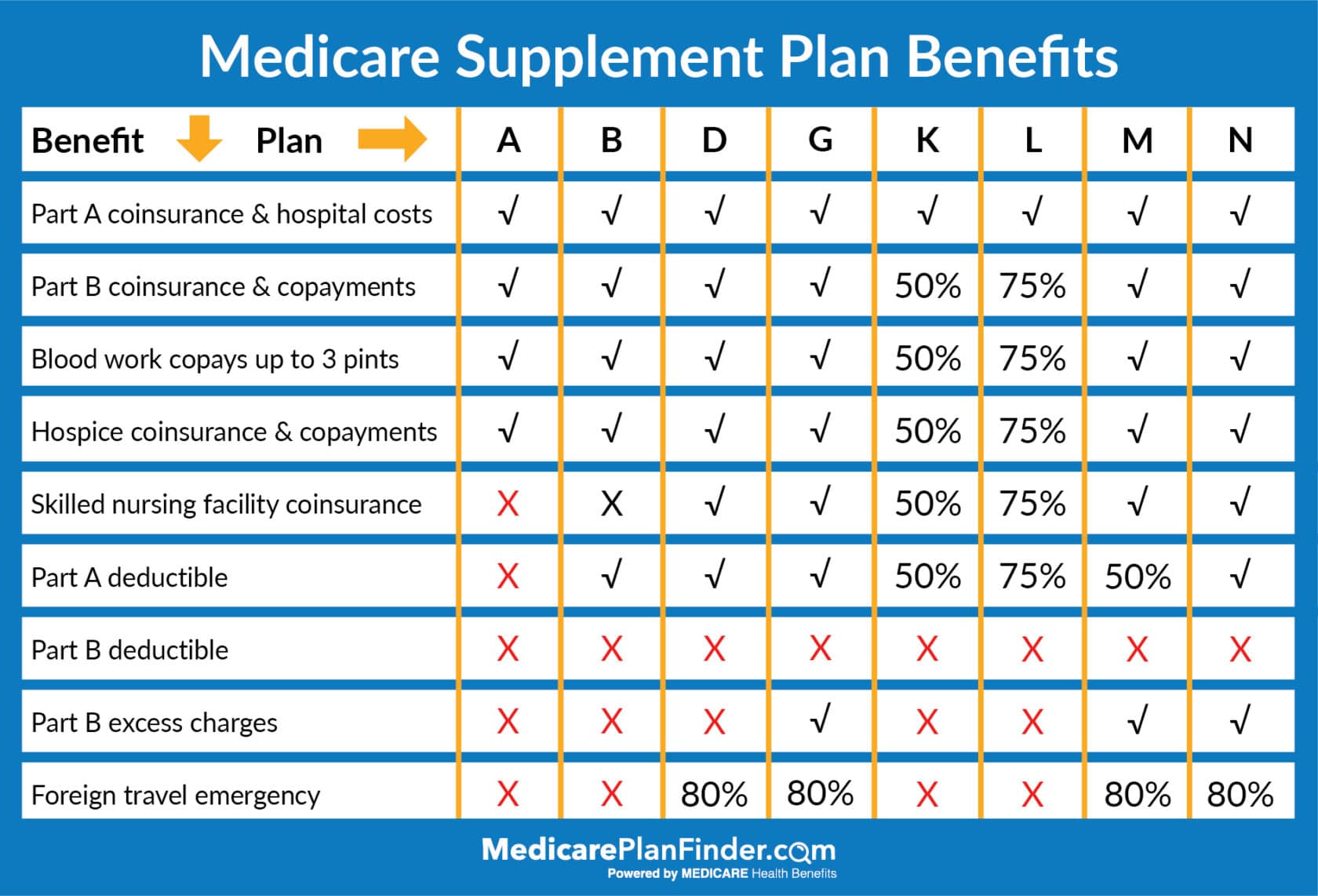

Medicare Supplement, or Medigap, insurance can be used to cover the out-of-pocket costs you may have to pay with Parts A and B. Insurance carriers offer many different types of Medigap plans, often sorted alphabetically, but they all must follow the same government regulations.

This means that Plan G from one carrier must provide the same benefits as Plan G from another carrier. Below is a quick breakdown of all the benefits covered by the different Medigap plan types.

Medicare Supplement Comparison Chart

Once you have found a Medigap plan type that meets your needs, you must consider the price. Insurance carriers must cover what is mandated by the government guidelines, but may charge very different rates for that coverage.

To find the best price, reach out to one of our licensed agents here or call us at (833)-567-3163 to have them run a personalized quote.

5 Common Types of Mental Illness In The Elderly

Most of today’s senior citizens grew up in a time when mental illness was almost never discussed in public. Over the years though, the stigma around mental health has largely eroded and conversations about mental health often dominate the national discourse.

As mental illness becomes less taboo, its far-reaching impact on society is coming more into focus. For example, the effects of mental illness in seniors are studied much more closely than ever before.

Common Types of Mental Illness In Seniors

With this more extensive research, it’s easier to see what mental health issues are common in the elderly population. The most prominent issues in senior mental health are:

1. Depression

Depression is often cited as the most endemic mental illness in the elderly population today. Many older adults may shrug depression symptoms off as simply “feeling down,” meaning it often goes undiagnosed and may be even more pervasive than the research suggests.

There are many risk factors that specifically contribute to depression in the elderly. Retiring from work can cause strong feelings of boredom or listlessness, and the death or illness of a spouse can leave many stressed and sorrowful.

Not only can depression exacerbate the symptoms of other chronic health issues, it is also noted as a symptom of more severe mental disorders like dementia. This means seniors and their loved ones must be vigilant in watching for these depression symptoms:

Feelings of sadness, hopelessness, or emptiness

Lack of motivation or interest in previously enjoyed activities

Trouble concentrating and decision making

Thoughts of suicide or self-harm

2. Anxiety

Anxiety disorders can take many different forms, such as obsessive-compulsive disorder (OCD), panic disorder, or generalized anxiety disorder. These are usually characterized by intense fear or nervousness over issues most would consider normal, routine aspects of everyday life – locking doors or finding a parking spot, for example.

Like depression, anxiety in older adults is extraordinarily common and is often underdiagnosed. Older adults are especially prone to ignoring this illness, perhaps because the conventional medical wisdom of previous decades downplayed psychiatric symptoms if no physical issues existed.

It is important to note however, that some physical symptoms such as restlessness or fatigue may accompany anxiety, further confusing a potential diagnosis. Be on the lookout for these symptoms of anxiety in the elderly:

Irrational, obsessive, or catastrophic thoughts

Isolating behavior and withdrawal from others

Irritability or agitated moods

Fatigue and muscle soreness

3. Bipolar Disorder

Bipolar disorder is usually diagnosed in younger people, whose moods can swing quickly from elation to depression. If this diagnosis is made when the person is an older adult, it is referred to as late onset bipolar disorder and it is more likely to manifest as agitation.

Diagnosing bipolar disorder in seniors is made even more difficult by the misinterpretation of symptoms. Many of the warning signs of late onset bipolar disorder might be dismissed as simply the natural effects of aging. Furthermore, some symptoms may resemble the side effects of certain medications, like antidepressants and corticosteroids.

As the population steadily increases, the number of cases of late onset bipolar disorder is expected to rise along with it. Professional help should thus be sought if you or those close to you observe any of these bipolar symptoms in adults:

Agitation and irritability

Hyperactivity or distractibility

Loss of memory, judgment, or perception

4. Schizophrenia

Similar to bipolar disorder, schizophrenia is a condition usually diagnosed in younger individuals. Late onset schizophrenia is the terminology used when this disorder is observed in patients over the age of 45.

Schizophrenia is characterized by a broad range of symptoms, from the so-called “negative” symptoms, like loss of interest or enthusiasm in activities, all the way to delusions and hallucinations. While late onset schizophrenia is less common than the early onset variety, older sufferers are more likely to experience these severe symptoms.

Currently, doctors are unsure what causes late onset schizophrenia and why it is different from its other forms. Some have theorized that it is a subtype of the disorder which is triggered by life events. Regardless, it is vitally important that seniors and their loved ones keep an eye out for these late onset schizophrenia symptoms:

Delusions or hallucinations

Disorganized speech or behavior

“Negative” symptoms (absence or lack of interest in normal behaviors)

5. Dementia

Though it is classified separately from mental illnesses by the medical community, dementia is still a disorder that severely affects mental health. There are many different stages and forms of dementia but the most common incarnation is Alzheimer’s disease, which affects around 3 million people over age 65.

Alzheimer’s and other forms of dementia can develop from the natural cognitive decline that happens as we age, drawing a startling link between aging and mental health. All demographics should make mental health a priority but seniors especially should watch for these dementia symptoms:

Disorientation or confusion (forgetting dates, years etc.)

Decrease in memory

Decline in ability to communicate

Mood swings and emotional issues

Treatment & Medication

Mental illness treatment can involve inpatient or outpatient care.

Mental illness treatment can be a tricky process and it begins with a proper diagnosis of the condition’s type and cause. To do this, your doctor may administer several different types of tests, from cognitive and psychiatric evaluations to brain scans and lab tests.

Several different mental conditions have symptoms that overlap and make them difficult to diagnose without extensive medical experience. Once the condition is properly diagnosed, a doctor may suggest one of these common forms of mental illness treatment.

Outpatient Care

The most common forms of outpatient mental illness treatment are based around medication or psychotherapy, often used in conjunction. The efficacy of these treatments varies from person to person and sometimes multiple treatment options must be attempted before an effective one is found.

For depression and anxiety disorders, pharmacological methods of treatment usually utilize antidepressants. These can be prescribed in addition or as an alternative to psychotherapeutic approaches like “talk therapy.” The Anxiety and Depression Association of America (ADAA) also suggestsregular exercise and a balanced diet as ways of staving off these common mental illnesses, stressing the link between brain and gut health.

The primary medications used in treating bipolar disorder and schizophrenia in seniors are classified as antipsychotics, usually prescribed at a lower dosage than people diagnosed at a younger age. For non-drug treatments of more severe cases, inpatient care is often required for proper rehabilitation.

For the treatment of dementia in the elderly, no cure is currently known. But the symptoms can be managed and the Alzheimer’s Association recommends a non-drug approach before attempting medication. These can begin with something as simple as changing the environment of those with dementia to remove obstacles and promote a general ease of mind.

If these non-drug approaches are not effective, certain types of medications like cholinesterase inhibitors and memantine may be prescribed to temporarily relieve some symptoms. Other approaches may include the use of antidepressants or anxiolytics, depending on the specific behaviors and symptoms that manifest.

Inpatient Care

With the more serious mental illnesses widely seen among seniors, outpatient care may not be an option. Those suffering from bipolar disorder or dementia may not be able to maintain their daily functions on their own and must turn to medical services that can attend to their needs 24 hours a day.

For example, the most common form of therapy for conditions like schizophrenia is a psychosocial approach, where a team of doctors, nurses, social workers and other professionals work in close contact with the patient to monitor their symptoms, both mental and physical, and help them maintain social skills and daily activities.

In these severe cases of mental illness, the accessibility of quality inpatient care has been shown to be a determining factor in recovery. The psychosocial interactions common in inpatient care are now considered to play a necessary role in a comprehensive intervention plan, as isolation can intensify many of the symptoms of these conditions.

What mental health services does Medicare cover?

Medicare can help pay for your mental health care.

When faced with one of these potentially life-changing illnesses, it is important to know what exactly is covered by your health insurance. Depending on the condition and its severity, some patients may need an extended stay in a hospital, which can quickly skyrocket the cost of care. Fortunately, Medicare covers many mental health services.

Medicare Part A Coverage

The types of mental health coverage offered differ depending on which elements of Medicare you are covered by. Medicare Part A covers inpatient care, or the medical services you receive while staying in a hospital. The out-of-pocket costs not covered are the same regardless of the type of hospital, general or psychiatric.

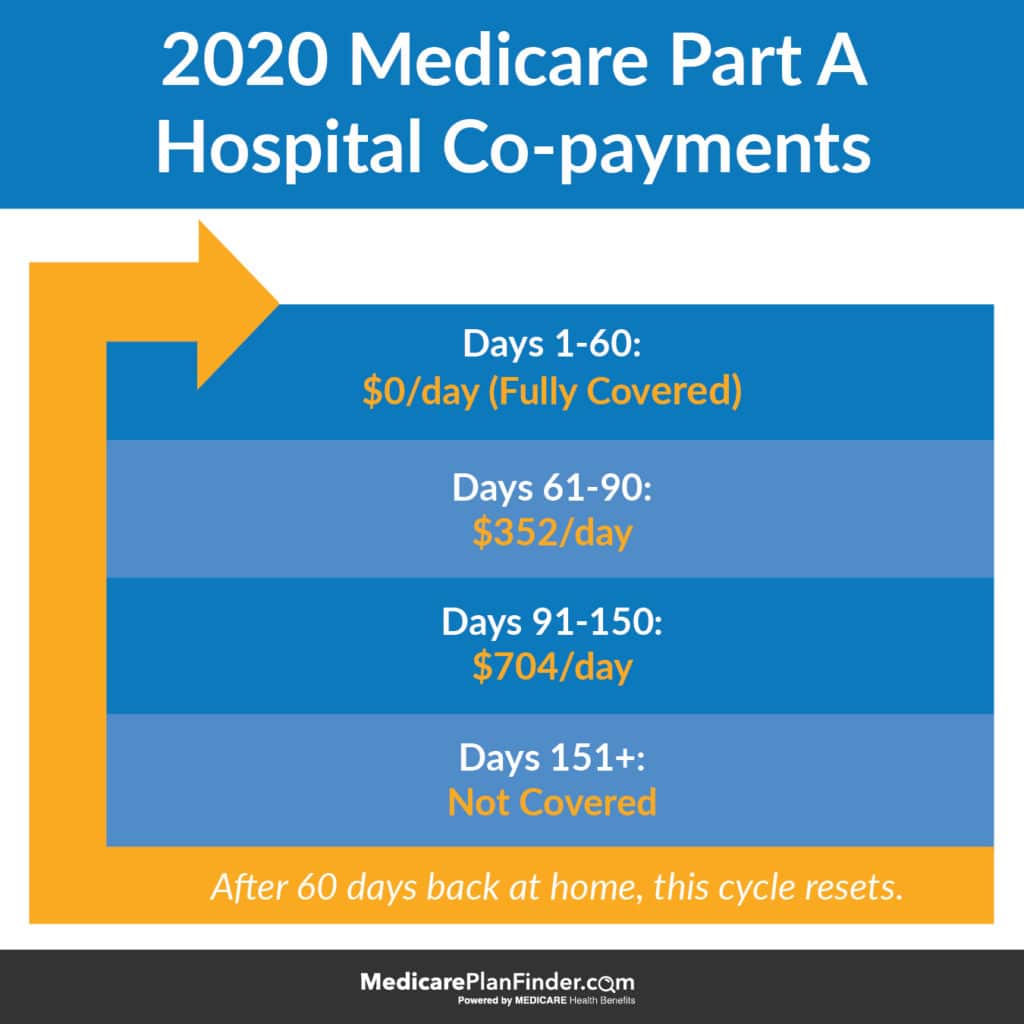

Medicare measures your use of hospital facilities using benefit periods. These benefit periods are tallied in increments of 60 days, beginning on the day you’re admitted to a hospital and ending when you haven’t used any hospital services for 60 consecutive days.

If your stay is in a general hospital, there is no limit to the amount of benefit periods Medicare will cover. In a specialized psychiatric facility though, Part A will only pay for up to 190 days of inpatient care during your lifetime.

For further information on how the co-payments break down, check out this handy graphic or see our more in-depth article here.

2020 Medicare Part A Copayments

Medicare Part B Coverage

Medicare Part B will cover most of the cost associated with outpatient mental healthcare. This primarily includes any doctor visits that may relate to your mental health, including appointments with psychiatrists, psychologists, nurses, and social workers.

Therapy and counseling may or may not be covered depending on if the doctor accepts Medicare assignment. Finding a therapist who takes Medicare is now easier than ever, using tailored search tools like the one developed by Psychology Today, available here.

After you meet your Part B deductible, Medicare will cover 80% of their approved amount to the doctor or therapist. This leaves a 20% copay that will have to be paid out-of-pocket. For some, this may still be too expensive and that’s where Medicare Advantage, Supplement, and Part D plans can help!

Medicare Advantage, Supplement & Part D Coverage

There are several types of supplemental coverage that can help pay for Medicare mental health benefits.

Part D plans, for example, offer coverage for prescription drugs which are not covered by original Medicare. For the year of 2020, these plans will have an annual deductible of $435 but, since they are provided by private insurance, there is some variation in the deductible, which may be waived, reduced, or charged upfront.

Medicare Advantage plans, also referred to as Part C, can offer far more benefits than parts A and B alone, including prescription drugs, dental and vision coverage, and group fitness classes tailored to seniors.

Medicare Advantage | Medicare Plan Finder

Alternately, you may choose to apply for a Medicare Supplement plan, which provides additional financial benefits to help with mental health-related costs like copayments and deductibles. There are up to ten distinct types of Medicare Supplement plans (designated alphabetically from A – N). Each plan may differ in coverage and price.

Medicare Supplements | Medicare Plan Finder

Whatever supplemental coverage you are looking for, it is best to seek the help of a licensed agent who can fully explain the details of each plan and find one that works best for you or your loved one. To contact one of these professionals directly for free, no-strings-attached information, fill out this form or give us a call at 844-431-1832 and get covered today!

What Is a Medicare SELECT Plan?

Medicare is a giant healthcare system that helps eligible people receive medical services. However, it doesn’t cover everything health-related. One tool that people use to afford healthcare is called a Medicare SELECT plan.

What Is Medicare SELECT?

A Medicare SELECT plan is a type of Medicare Supplement (Medigap) plan. Medigap plans are private insurance policies that can help close the gap between your coverage and what you pay. Medicare SELECT plans require you to use a specific network of medical facilities and healthcare providers.

How Does a Medicare SELECT Plan Work?

A regular Medicare Supplement plan provides coverage anywhere that accepts Medicare. In 2019, there are 10 standardized Medigap plans you can enroll in. Covered services depend on which “letter” you buy, but each letter offers the same coverage in every state.

Medicare Supplement Plans Comparison Chart

Plans that cover the Medicare Part B deductible (Plan C and Plan F) will not be available to anyone newly eligible for Medicare after January 1, 2020. If you qualify for Medicare and want coverage for those items now, talk to an agent today!

Medicare SELECT policies are different from other Medigap plans because they aren’t accepted everywhere that takes Medicare. Also, Medicare SELECT is different because not all 50 states have plans available.

Medicare SELECT premiums depend on a variety of factors, but because they feature smaller networks than normal Medigap plans, Medicare SELECT premiums may be less.

Is Medicare SELECT Different Than Medicare Advantage?

Medicare SELECT is different than Medicare Advantage because of what the plans cover. Because Medicare SELECT is a type of Medicare Supplement policy, it only covers financial items such as deductibles, coinsurance, and copays.

Like Medigap policies, Medicare Advantage plans are private insurance policies. However, Medicare Advantage plans cover medical services, and they can offer supplemental benefits such as vision, hearing, dental, and fitness classes. You must choose either a Medigap plan or a Medicare Advantage plan. You cannot have both.

Certain Medicare Advantage plans called HMOs are a lot like Medicare SELECT, because they can feature smaller networks of providers than Medicare Advantage PPOs or regular Medigap plans.

When Can I Buy Medicare SELECT?

According to the Medicare Rights Center, the best time to enroll in a Medigap plan is during your Open Enrollment Period (OEP), which is the six months after you’ve enrolled in Medicare Part B.

If you miss your Open Enrollment Period, you can buy a Medigap plan when you have a guaranteed issue right. For example, you have guaranteed issue within “63 days of losing or ending certain kinds of health coverage.”

You may also have a guaranteed issue right if you enrolled in a Medicare Advantage plan when you were first eligible for Medicare and disenrolled within one year. Other circumstances that may allow you to have guaranteed issue are if your private Medicare plan ends coverage or you move out of the plan’s service area.

If you decide a Medicare SELECT or any Medicare Supplement policy isn’t for you, you can cancel within 30 days of starting coverage. However, you should cancel with caution, because you may not be able to buy another policy depending on where you live, and you might get charged more because of your health.

If you buy a Medicare SELECT policy and you don’t like it, you can switch to a standard Medicare Supplement plan within 12 months of your Medicare SELECT policy taking effect.

Learn More About Medicare SELECT

Medicare SELECT plans aren’t available in every state. A licensed agent with Medicare Plan Finder can show you what’s available in your area and help you make a decision. Our agents are highly trained and may be able to find a plan that fits your budget and lifestyle. Call 844-431-1832 or contact us here to set up a no-cost, no-obligation appointment today.

Find Medicare Plans | Medicare Plan Finder

A Guide to Medicare Coverage for Dementia

A Guide to Medicare Coverage for Dementia

Dementia is a decline in mental capacity that becomes severe enough to hinder a person’s ability to function. According to the Alzheimer’s Association, one-third of Americans die with some form of dementia.

Medicare Parts A and B (Original Medicare) will cover everything that’s medically necessary for dementia patients, but many other services won’t be covered.

Original Medicare dementia care may be limited, but certain Medicare Advantage plans offer coverage for more services that can include unexpected offerings like meal delivery.

Medicare Coverage for Dementia Patients Clarified

Doctor Explaining Medical Treatment for Dementia | Medicare Plan Finder

An Original Medicare plan will cover services that your doctor deems medically necessary. Medicare Part A covers inpatient hospital care, and Medicare Part B covers outpatient care and medical expenses such as doctors’ appointment costs.

Original Medicare will pay for the first 100 days of care in a skilled nursing facility (there may be some associated fees), and some Medicare Advantage (Part C) plans may include long-term care coverage as well as skilled nursing care.

Private insurance companies offer Medicare Advantage plans, so they have the freedom to cover benefits Original Medicare doesn’t. Medicare Part D or certain Medicare Part C plans cover prescription drugs such as cholinesterase inhibitors that can temporarily improve symptoms of dementia.

Medicare Advantage | Medicare Plan Finder

Medicare Supplements

Medicare Supplements (Medigap) plans can help cover the expenses that Original Medicare does not. Unlike Medicare Advantage plans, Medigap plans do not cover medical expenses, but they cover financial items such as Part A and B coinsurance and copayments. Even though Medigap and Medicare Advantage are two different types of plans, you cannot enroll in both at the same time.

Find Medicare Supplements | Medicare Plan Finder

Does Medicare Pay for Dementia Testing?

Medicare Part B covers cognitive testing for dementia during annual wellness visits. A doctor may decide to perform the test for patients who are experiencing memory loss.

The test consists of about 30 questions like, “What year is this?” to assess the patient’s memory and awareness. The test can be used as a baseline evaluation for future wellness visits and can be a valuable tool for catching dementia early.

Medicare Testing for Alzheimer’s

Dementia is a symptom that can result from many different diseases. Alzheimer’s disease is just one cause of dementia. The risk of developing Alzheimer’s increases with age and with a family history of Alzheimer’s.

There is a correlation between genes called apolipoprotein E (APOE) and Alzheimer’s, but those genes do not necessarily cause the disease. Medicare will not cover genetic testing for APOE genes.

Dementia as a SEP-Qualifying Condition

Medicare eligibles with dementia also qualify for specific Medicare Advantage plans called Chronic Special Needs Plans (CSNPs). These health insurance plans involve coordination and communication between the patient’s entire medical team to help ensure the patient gets the best possible care.

The best way to sort through the thousands of plans available and find the right CSNP for you is enlisting the help of a qualified professional by contacting us here.

If you’re diagnosed with dementia and already enrolled in Medicare Parts A and B, you will qualify for the Special Enrollment Period (SEP). The SEP allows you to enroll in new Medicare coverage or make changes to your existing CSNP whenever you need to instead of having to wait for certain times of the year.

Special Needs Plans | Medicare Plan Finder

Eligibility for Medicare Coverage for Dementia

If you meet the eligibility requirements for Medicare Parts A & B, you will also be eligible for the dementia coverage provided by Medicare. You can obtain Medicare coverage for dementia services if you are:

Age 65 or older

Any age and have a disability, or end-stage renal disease (ESRD)

Dementia patients are also eligible for other specific Medicare plans once they are officially diagnosed with the condition, like special needs plans (SNPs) and chronic care management services (CCMR.)

Medicare can also cover home health care that dementia patients often need. In order to receive this coverage, it must be certified as necessary by a doctor. The patient must also be classified as homebound, meaning they have trouble leaving the house without help.

Does Medicare Cover Memory Care?

Memory care is a specific type of long-term care for Alzheimer’s patients or people with dementia. Original Medicare will cover occupational therapy but does not cover assisted living facilities. However, certain Medicare Part C plans may include coverage for Medicare dementia care services such as adult day care or help to get dressed or to bathe.

Medicare dementia coverage is split between its component parts. Part A helps cover the cost of inpatient hospital stays, including the meals, nursing care, and medication that you need while you’re there. Meanwhile, Part B will cover the doctor’s services that you might receive during your stay in the hospital, such as testing or medical equipment.

Even more services can be covered by Part C, also called Medicare Advantage. In addition to everything covered by Parts A & B, these plans can also offer options for long-term and home care for dementia patients.

How Much Does Medicare pay for dementia care?

Each different part of Medicare will pay for its benefits in different ways. For example, Part A will cover the entire cost of your hospital or skilled nursing facility stay for the first 60 days. After this period, you will need to pay 20% coinsurance until day 90, when Part A will stop paying entirely.

Part B, on the other hand, will usually pay for 80% of all services that it covers. Medicare Supplement plans are often purchased to cover the remaining costs, and can also provide additional benefits to the patient.

Does Medicare cover long term care for dementia?

The long-term care insurance offered by Medicare depends on the nature of the service being provided to the patient. In many cases, the long-term care needed by dementia patients is classified as custodial care and won’t be covered by Medicare.

However, if your doctor prescribes a long-term care service as “medically necessary,” Medicare may help cover the costs. These exceptions can include services like hospice care, and part-time nursing care or occupational therapy provided in the home.

Does Medicare Pay for Home Health Care for Dementia Patients?

It is usually difficult to obtain coverage from Medicare for elderly care at home. However, it can completely cover some home health services that are deemed medically necessary by your doctor, including:

Physical and occupational therapies

Part-time skilled nursing care

Medicare social services

Most nursing home care is also classified as custodial care by Medicare, meaning it will not be covered. Medicare will cover custodial home health care for dementia patients only if it’s a part of hospice care.

Medicare Advantage plans, however, can offer many different home health benefits for those who suffer with dementia. Examples include personal care assistance, homemaker services, and meal delivery.

Does Medicare Cover Assisted Living for Dementia?

Original Medicare will not cover any services that are deemed custodial or personal care, including any that aid in typical activities of daily living, such as:

Eating

Getting Dressed

Bathing

Using the restroom

This rule also applies to assisted living and memory care facilities which provide these services. But depending on your state and the facility of choice, Medicaid may be able to help cover the cost of long-term custodial care provided in assisted living facilities.

Medicare Dementia Hospice Criteria

In order for Medicare to cover hospice care, your doctor must first document that you have less than six months to live. You or your durable power of attorney must sign documents indicating that you agree to accept care for comfort and that you waive other Medicare benefits.

What dementia services does Medicare not cover?

In almost all cases, Medicare will not cover any non-medical care services, such as:

Assisted-living or long-term care

Custodial services provided in a facility or in the home

Homemaker services

Meal delivery

There are exceptions to these rules, but the service in question must be recommended as medically necessary by your doctor. Medicare Advantage plans may offer coverage for these and other personal care services not covered by Medicare.

How to Cover the Gaps with Medicare and Dementia

Paying for dementia care can be daunting, even for Medicare beneficiaries. Both Parts A & B have deductibles you have to meet, and Part B only pays for 80% of its covered services. At the end of the day, a patient and their family may be left wondering how to pay for Alzheimer’s care.

The answer may come in the form of Medicare Part C, also called Advantage plans, which can pay for many of the custodial care costs not covered by Original Medicare. Another option may be a Medicare SNP, or special needs plan, which are geared toward patients with certain chronic conditions such as dementia.

Early Signs and Symptoms of Dementia

Dementia can have a variety of symptoms depending on the cause, as well as if the patient is in the early stages or late stages of the disease. However, some common signs symptoms include:

Cognitive changes

Loss of memory

Difficulty finding the right words during conversation

Getting lost while driving to and from familiar places

Difficulty with logical reasoning or solving problems

Difficulty with completing complex tasks

Difficulty with planning and organizing day-to-day activities

Difficulty with muscular coordination and motor functions

Being confused or disoriented

Psychological changes

Changes in personality

Depression

Anxiety

Inappropriate or irrational behavior

Paranoia

Agitation

Hallucinations

How to Find Memory Care

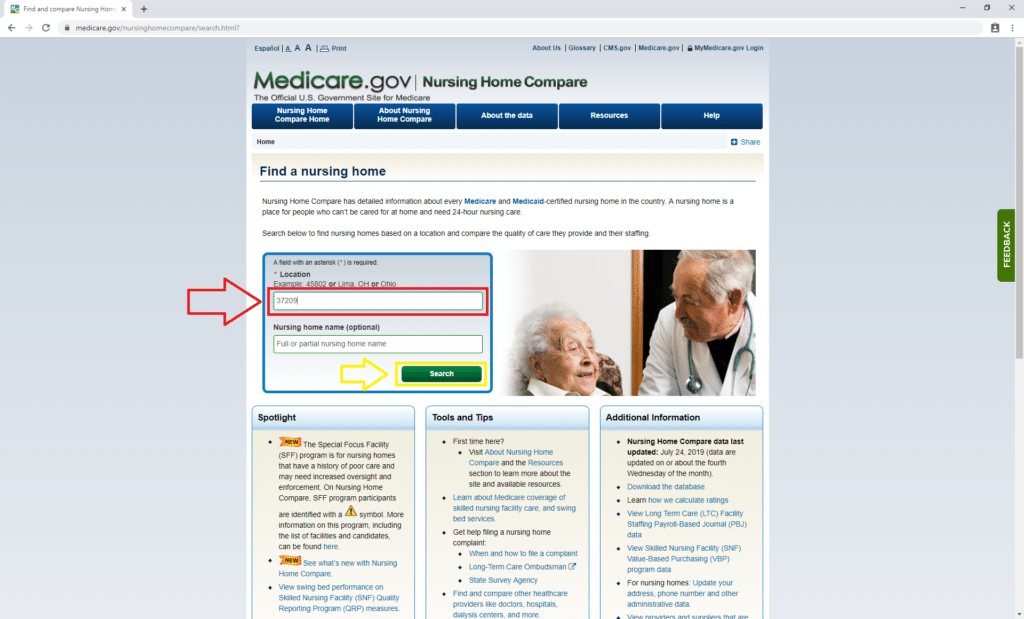

Medicare.gov has a tool to find nursing homes that accept Medicare for medical services. To get started, click here. Not all of these facilities have dedicated memory care teams, so you’ll need to contact them to verify their services.

Once you’re on the nursing home finder tool page, enter your zip code as shown below in red. We used 37209, which is our corporate headquarters’ zip code in Nashville, Tennessee. Then click “Search,” shown in yellow.

How to Find Memory Care Step 1 | Medicare Plan Finder

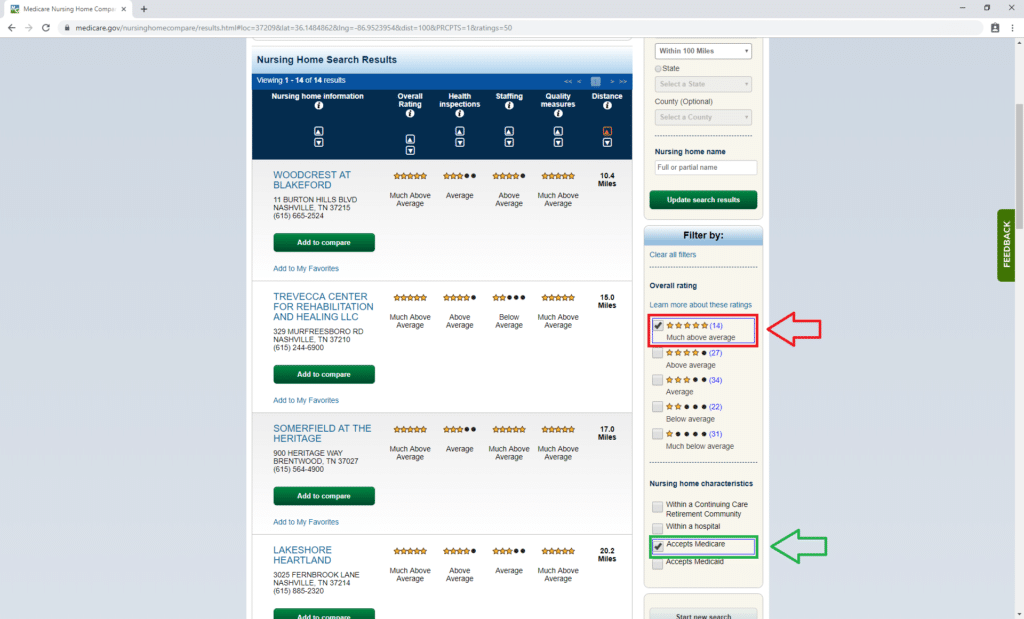

Then you’ll reach a list of nursing homes in your area. The nursing home finder tool lets you sort facilities by star rating, which is based on a scale of one to five.

Basically, the higher the rating, the better the care the facility provides. For demonstration purposes, we only chose to see homes that have a five-star rating (shown below in red) and that take Medicare insurance (in green.)

How to Find Memory Care Step 2 | Medicare Plan Finder

You may have to contact more than one facility to find the right one for you. Ask about costs and how they help patients with dementia. If one seems like it may be a good fit, ask to tour the home to really get a feel for it.

Resources for Families

Family members of dementia patients have access to a wide variety of resources to help them cope. The first step for helping your loved ones is to educate yourself about the disease and to learn how you can be the most supportive.

You should also look into support groups for your family so they can find like-minded people who are having similar experiences. Dementia should not be dealt with alone.

If you are a caregiver for a parent with dementia, you should consider important things such as who will have the power of attorney and make financial decisions for the patient at the end of his or her life. If you haven’t enrolled in a life or a final expense insurance policy, you should consider doing so now.

We Can Help You Find Medicare Coverage for Dementia

Dementia is difficult for everyone involved. If you or a loved one has dementia, we can help you navigate Medicare dementia care and find a Chronic Special Needs Plan that’s right for you. Set up a no-obligation appointment with a licensed agent by calling 844-431-1832 or contacting us here today.

Contact Us | Medicare Plan Finder

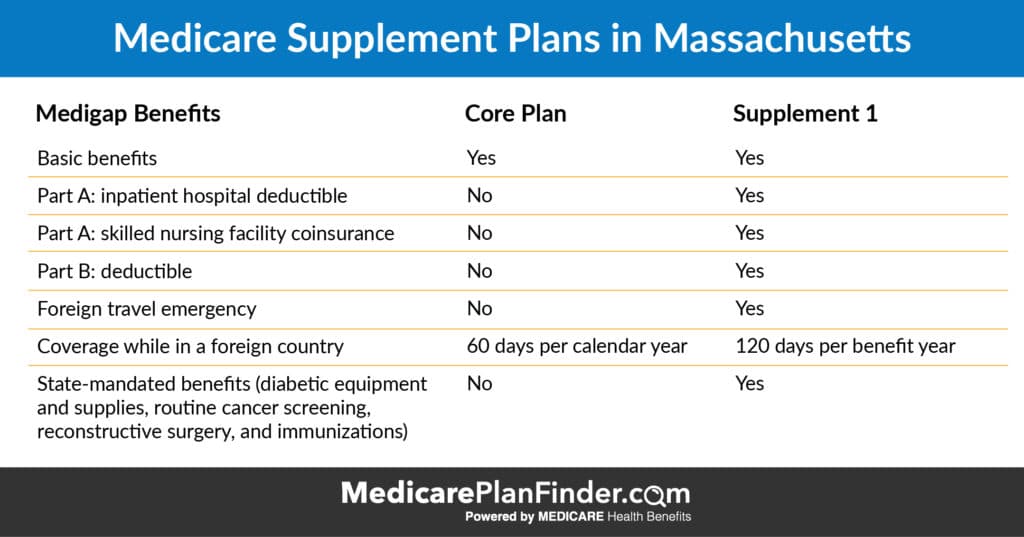

How Medigap is Unique in Minnesota, Wisconsin, and Massachusetts

In most of the United States, Medigap (also called Medicare Supplements) can be characterized by eight different types of plans (A, B, D, G, K, L, M, N). However, there are three states that work completely differently: Massachusetts, Minnesota, and Wisconsin.

A lot of the information you’ll see on the internet about Medicare Supplement plans talks about those eight plans, but we haven’t forgotten about you, Massachusetts, Minnesota, and Wisconsin! If you live in one of those three states, this guide is for you.

Psst…click below to read more about Medicare programs in each state:

If you already have a basic understanding of Medigap, you can skip ahead to the section about your state below.

Medigap is a type of private Medicare insurance that is not technically part of the government-sponsored Medicare program. Medigap plans are also called Medicare Supplements. The two terms can be used interchangeably. To enroll in Medigap, you have to enroll in Original Medicare first.

Additionally, you cannot have a Medicare Supplement plan and a Medicare Advantage plan at the same time. Click here to find out if Medicare Advantage is better for you than Medicare supplements.

What Does Medigap Cover?

Uniquely, Medicare Supplement plans do not typically provide additional health benefits. Instead, Medigap plans provide additional financial protection. For example, let’s say you get sick and have to go to the doctor at least once per month for treatment. Original Medicare may not cover the entire cost for you. You might have to pay your deductible first ($185 for Part B in 2019) and then 20% coinsurance on every visit.

If you have a Medicare Supplement plan that includes deductible and coinsurance coverage, you may not have to pay that $185 and 20%. Instead, you’ll only have to pay your Part B* premium and your Medigap premium.

You may have heard that you cannot be denied Medicare coverage based on your age or preexisting conditions. While that’s true, Medigap is a little different. If you enroll in a Medicare Supplement plan during your Initial Enrollment Period (the time when you first become eligible for Medicare), that holds true. However, if you wait too long to enroll, there is a chance that your plan will be put through underwriting and your prices may increase, or you may be denied coverage based on your age and preexisting conditions.

*Some people may have a Part A premium as well.

Senior couple speaking with a doctor

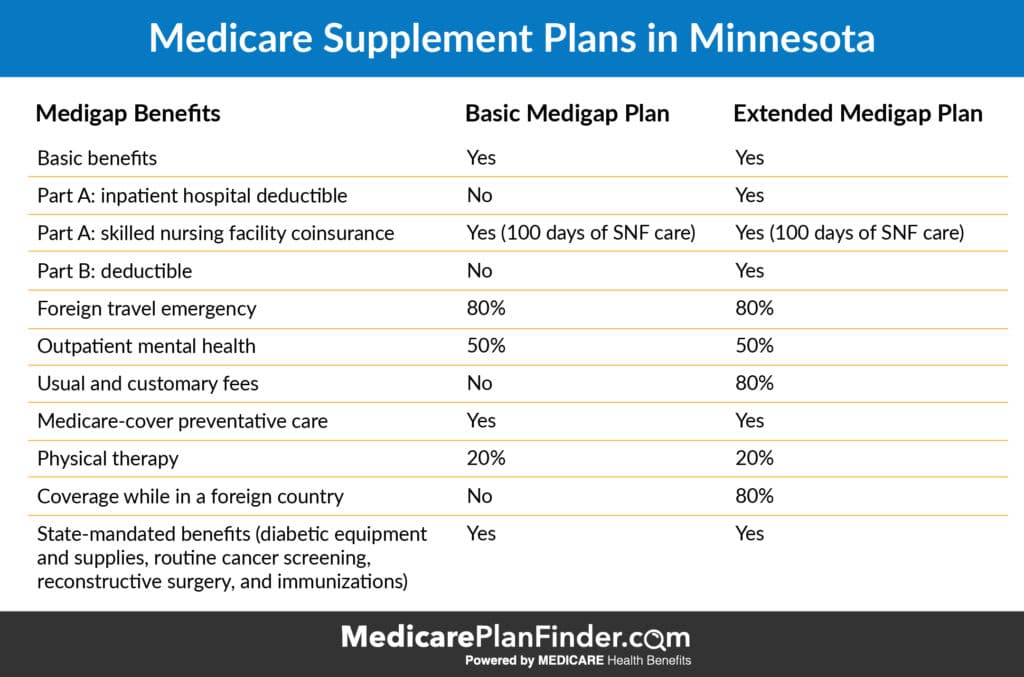

Minnesota Medicare Supplement Plans

While you can’t get the same eight plans (A, B, D, G, K, L, M, N) in Minnesota that are offered in other states, there are technically modified versions of plans K, L, M, and N available.

Additionally, Minnesota offers two unique plans: The “Basic Plan,” and the “Extended Basic Plan.”

The preexisting conditions underwriting may apply. However, you’ll get a 6-month Medigap enrollment period (where age and preexisting conditions do not apply) if you return to work or if you drop Part B in favor of your employer’s health plan.

80% of foreign travel emergency, then 100% after you spend $1,000 per year out-of-pocket

80% of “usual and customary fees,” then 100% after you spend $1,000 per year out-of-pocket

Minnesota Medicare Supplement Plans

So you’re probably wondering, if the Minnesota Medigap Basic Plan and the Extended Basic Plan both always offer the same benefits, why would you choose one Basic Plan over another?

The answer is that costs can vary and plans are allowed to add some extra benefits. There are four additional benefits that plans are permitted to add to the Basic and Extended Basic plans: Part A inpatient deductible, Part B deductible (no longer available in 2020), usual and customary fees, and non-Medicare preventive care.

At least $30,000 for kidney disease treatment (dialysis, transplants, etc.)

Insulin pumps, self-management training, and other diabetes care

50% and 25% cost-sharing plans are also available, which are similar to Medigap Plan K and Medigap Plan L (which would be available in other states).

So, you might be wondering why you have multiple options to choose from for Wisconsin Medigap plans if they are all supposed to be the same “basic” plan. The answer to that is that plans ARE allowed to add additional benefits other than what is in the basic plan, and the costs can vary. Companies are allowed to add the following benefits:

Why Can’t I get Part B Deductible Coverage in 2020?

When MACRA (The Medicare Access and CHIP Reauthorization Act) passed in 2015, a couple of changes were made that didn’t take effect right away; Losing Part B deductible coverage was one of them.

Congress made the decision to not allow plans to cover the Part B deductible starting in 2020. This decision saves money for the Medicare program and doesn’t have an astronomical effect on you. The Part B deductible was only $185 in 2019. All this means is that you will have to pay $185 out-of-pocket before the rest of your coverage kicks in.

It also means that if you are already enrolled in one of the plans listed above that includes the Part B deductible, you won’t lose that coverage. However, if you decide to switch plans or drop that coverage at any time, you won’t be able to get back into it starting in 2020.

How do I Decide Which Medigap Plan is Right For Me?

Regardless of which state you live in, we have a plan finder tool that can help you compare your options.

We also have licensed agents available to answer your questions and help you make your final decision. To find out if there is an agent near you that you can meet with, call 844-431-1832 or send us a message by clicking the “let’s chat” button in the bottom right corner.

How to Choose the Best Type of Medicare Plan for You

When it’s time to choose a Medicare plan, it’s easy to get overwhelmed. There are quite a few different types of Medicare plans to choose from. Once you choose what type you want – you still have to choose a plan! Making the right choice is important because it may not be easy to change plans if you change your mind.

The Annual Enrollment Period (October 15 through December 7) is when anyone can make changes, and for some people, it’s the only time. If you make the wrong choice, you might have to wait a whole year before you can change again (unless you qualify for the OEP or have a SEP).

Which Types of Medicare Plans are Best for Me?

To figure out which Medicare plan is best for you, ask yourself the following questions:

What specific medical services do I need coverage for (ex: lab tests, blood work, surgery, chemotherapy, dental, etc.)?

How much room do I have in my budget? Am I able to pay a little more to have more benefits?

Would I rather pay more on a monthly basis and pay very little when I visit the doctor, or is it better to pay a small amount every month but risk having higher copayments?

Who are the doctors and other providers who I want to be covered in my plan?

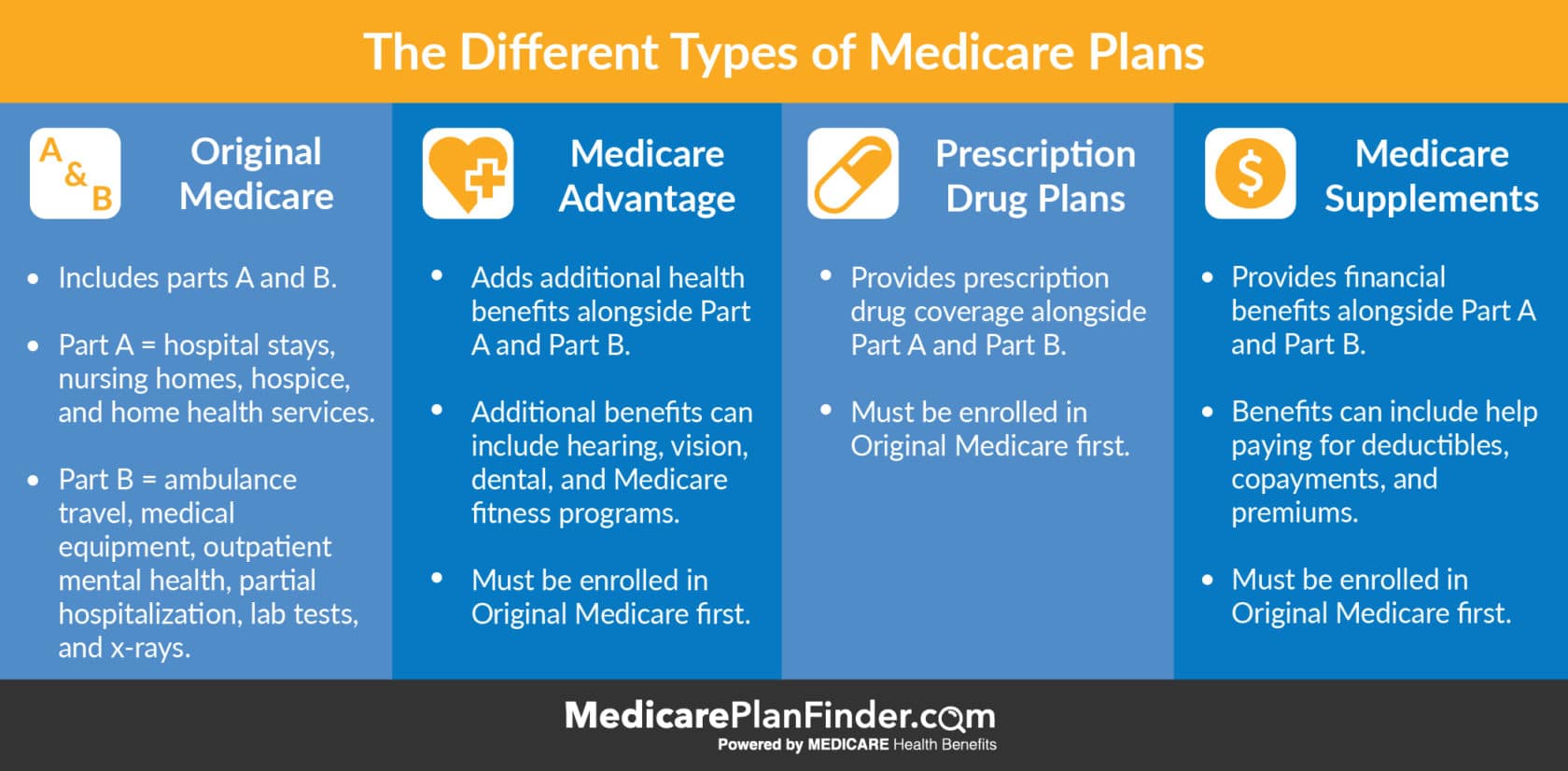

There are four main types of Medicare plans to consider when you begin your Medicare plan search. Start by comparing Original Medicare, Medicare Advantage, Prescription Drug Plans, and Medicare Supplements.

Keep in mind that you cannot have Medicare Advantage and a Prescription Drug Plan at the same time. You also cannot have Medicare Advantage and a Medicare Supplement plan at the same time.

Which plan or combination of plans works best for you?

Medicare Advantage: A private plan that you can purchase once you have Original Medicare. Can add additional benefits such as hearing, vision, dental, fitness, etc. Can include a prescription benefit.

Prescription Drug Plans: Another type of private plan that you can purchase once you have Original Medicare. Usually only includes a prescription benefit.

Medicare Supplements (Medigap): Another type of private plan that you can have in addition to Original Medicare. Adds more financial coverage, like for copayments and deductibles. This type of plan would also require you to have a stand alone part D drug plan.

Different Types of Medicare Plans

Choosing a Medicare Advantage Plan

So, did you decide to go with Medicare Advantage? Great! Now, there are a few types of Medicare Advantage plans that may be available for you. First, ask yourself whether or not you need a large network and whether the freedom to see any doctor is important to you. Then, read through these important differences:

HMO Plans (Health Maintenance Organization) – You’ll select one primary physician. In some cases, you may only receive coverage for that one doctor (unless he or she refers you to a specialist). Requirements may vary based on your plan.

HMO-POS Plans (Point-Of-Service) – You’ll select one primary physician, but you’ll have the freedom to visit any specialist in your network for your other needs. You will be charged a fee for visiting specialists.

PPO Plans (Preferred Provider Organization) – You can see any doctor, but your costs will usually be lower if you choose one that is in your network.

PFFS Plans (Private Fee-For-Service) – You will not need referrals or a primary physician, but you’ll have to pick a doctor that accepts your PFFS plan.

SNP (Special Needs Plans) – Designed for those who are eligible for both Medicare and Medicaid, live in a nursing home, or have a chronic illness or disability.

MSA (Medical Savings Account) – Works like a tax-free savings account for your medical bills. Medicare will deposit money into your HSA. You can use that account to pay for medical expenses.

How do I Pick a Medicare Supplement Plan?

If you’ve decided that you want a Medicare Supplement plan, you’ll want to start by selecting the plan letter that corresponds with the coverage you need. Use the chart below for reference.

Once you’ve made that decision, you may have a few different carriers available in your area to choose from (some smaller cities may not have several options available).

Finding Medicare Plans in your area just got easier. Our Medicare Plan Finder tool can help you not only see what is available, but see which options may be best for your unique needs.

You can enroll by yourself, or you can meet with a licensed agent (for free) who can walk you through the process to make sure you don’t make any mistakes. The licensed agent can also talk to you about a variety of different types of plans in your area and answer all your questions.

This unbiased approach is a great way to get the help you need when selecting a Medicare plan.

To set up your free meeting with a Medicare Plan Finder licensed agent, call 833-567-3163 or click here.

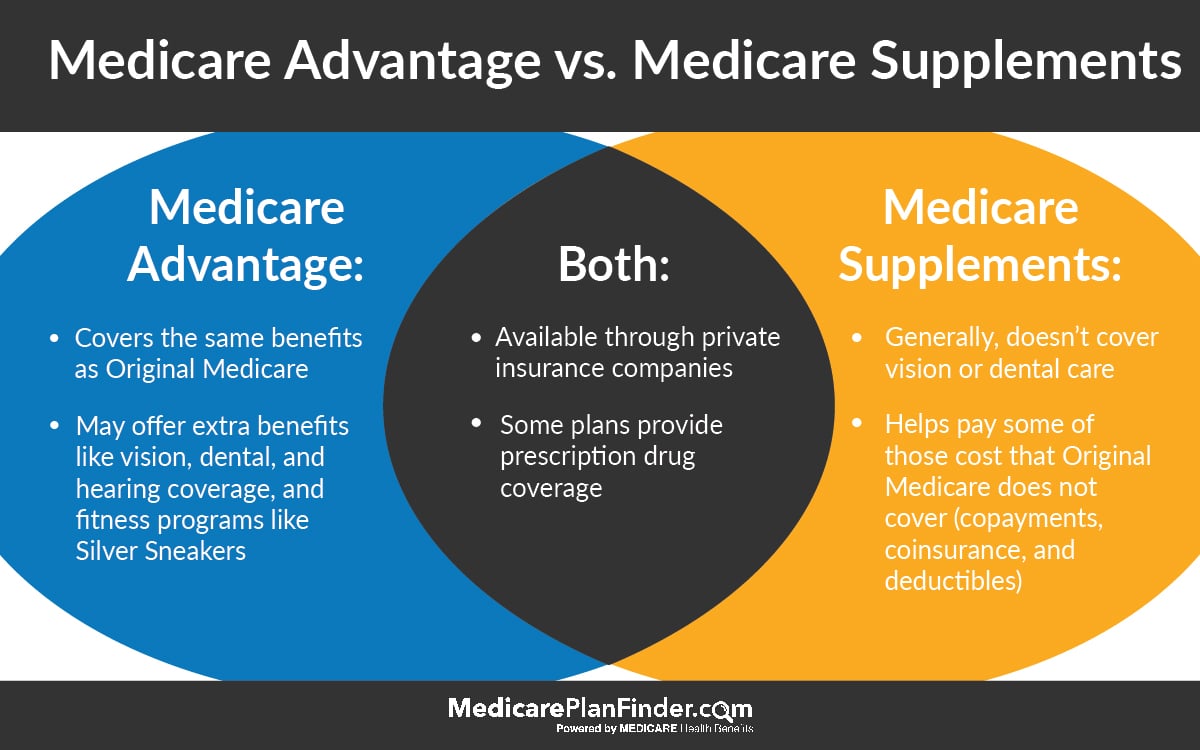

Medicare Advantage vs. Medicare Supplement

Medicare Advantage and Medicare Supplements (also called Medigap) are very different insurance plans with distinct benefits. The answer to the question “is Medicare Advantage better than Medigap?” depends on your circumstances and needs.

What is Medicare Advantage?

Medicare Advantage plans are private plans (not owned by the federal government) that can offer additional health benefits. To have Medicare Advantage, you have to enroll in Original Medicare first. You may have to continue to pay your Medicare Part B premium even if you have Medicare Advantage (MA), but MA premiums can be as little as $0.

Medicare Advantage plans are not all the same, but they can provide benefits like (click on the links to learn more about each one):

There are many different types of Medicare Advantage plans, although not every plan type may be available in your area.

A health maintenance organization (HMO) is a network of health-care providers and facilities where you choose a primary care physician to coordinate your care.

A preferred provider organization (PPO) is also a network of health-care providers and facilities but typically you do not need to select a primary care physician, and you have more flexible options regarding out-of-network care.

A private fee-for-service (PFFS) plan is a mode of benefit delivery where you are not limited to a network. However, there are no guarantees that your doctor or hospital will accept the plan. If you choose to receive your Medicare health coverage through a private Medicare Advantage plan, you must continue paying your Part B premium regardless, because you remain enrolled in Original Medicare (Part A and Part B), even after joining a Part C plan.

What is Medigap?

Medigap is more different from Medicare Advantage than you might think. While Medicare Advantage plans are able to offer health benefits, Medicare Supplement plans (also called Medigap) offer financial benefits. For example, some Medigap plans can cover your Part B premium.

The chart below explains the differences between available Medigap plans in 2020. You can also use our Medicare Plan Finder search tool to compare plans in your area.

2020 Medicare Supplement Comparison Chart

Comparing Medicare Advantage vs. Medicare Supplement plans

Let’s look at Medicare Advantage vs. Medigap. In short, the difference between Medicare Advantage and Medicare Supplement plans is that one can supply health benefits while the other can supply financial coverage.

Medicare Supplement Insurance is a policy that’s added to Original Medicare, Part A and Part B, to provide additional financial coverage. Medicare Advantage is a private plan option that may provide you with other health benefits that Original Medicare does not cover (like dental, vision, fitness programs, etc.).

You cannot have both Medicare Advantage and Medigap at the same time.

Medicare Advantage vs Medicare Supplements | Medicare Plan Finder

A given plan type (e.g., Plan F) has the same benefits regardless of the insurance company that provides the policy, or the state in which you reside. This is not true of Medicare Advantage plans, however, because coverage details may vary by plan.

Excluding prescription drug coverage, any standard Medigap plan with Part A and B will have more benefits than a standard Medicare Advantage plan. However, as mentioned above, some Medicare Advantage plans offer benefits beyond those found in Part A and Part B.

Some Medicare Advantage plans offer prescription drug coverage (often for an additional monthly cost). With a Medigap plan, in contrast, you would need to enroll in a separate prescription drug plan. When comparing plan options, consider your costs for drug coverage. In some cases, Medigap with a stand-alone prescription drug plan has lower total costs than a Medicare Advantage plan with drug coverage. In other cases, the reverse might be true.

[Tweet “Do your research! Comparing #Medicare Advantage vs Medicare Supplement”]

Real-Life Examples: Medicare Advantage vs. Medicare Supplements

Let’s take a look at some real-life examples to help you decide whether Medicare Advantage or Medicare Supplements are right for you.

If you have Medicare Parts A (hospital coverage), B (medical coverage), and D (prescription coverage) and you are hospitalized for cancer treatments for 90 days, you may have out of pocket costs. The Part A deductible means you would pay well over $1,000 first. Once you meet your deductible, your costs will go down. However, after day 60, you’ll be responsible for a portion of every day that you stay there.

If you have Medigap Plan B, your deductible and many of your other hospital costs will be covered. This plan would be in addition to your Part B coverage, so it would all work together to provide extra coverage.

If you have Medicare Advantage, you may have additional health benefits. You’d still likely be responsible for some of those out-of-pocket hospital costs, but your plan might provide a home healthcare benefit, meaning you can get a private in-home nurse when you are released from the hospital. You might also have coverage for medical equipment, such as bathroom safety equipment or a walker.

Comparison is key: Medicare Advantage vs. Medicare Supplements

When choosing between a Medigap plan and a Medicare Advantage plan, take the time to do your research. Read the benefit descriptions of every Medigap and Medicare Advantage plan you are considering. Be certain to look at:

Monthly premium

Deductibles

Doctor and healthcare facility restrictions

Benefits

Anticipated plan costs given your typical use of health-care and hospitalization services

Prescription drug coverage cost sharing as it relates to your medication usage

In the end, your decision is going to be the one that you feel the most comfortable with. The challenge is often wading through all the material to get to the bottom line. Want to make that a little easier? Give us a call at 844-431-1832.

This post was originally published on October 23, 2018, and was last updated on August 29, 2019.