What Can You Do During the Medicare Annual Enrollment Period?

Watch this brief video first!

Annual Enrollment Period… Explained

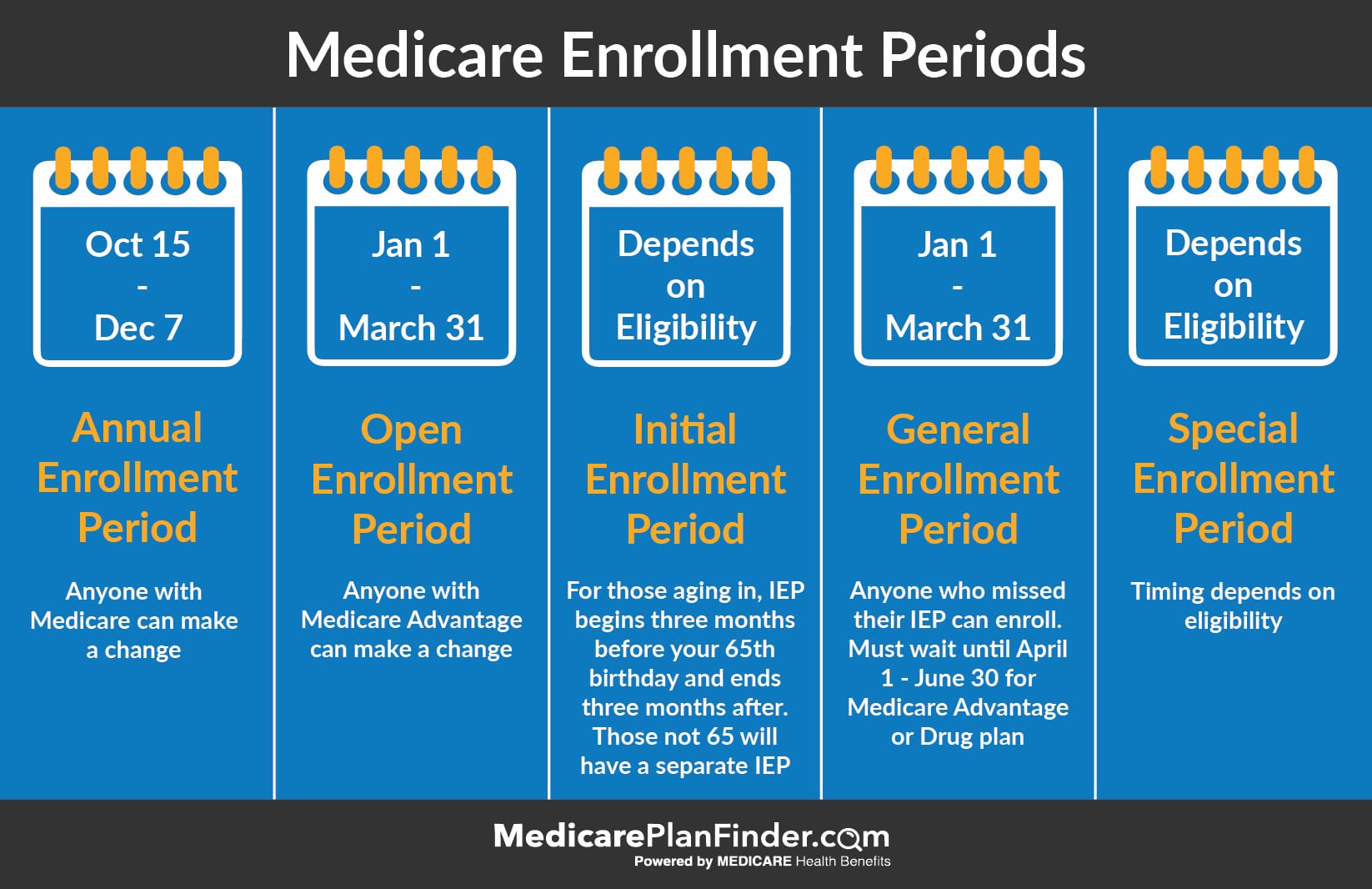

Did you know that there are five different Medicare enrollment periods throughout the year? Not everyone will be eligible for every period, but everyone who has Medicare is eligible for the Annual Enrollment Period.

Be sure to keep track of each enrollment period so that you know when it’s your turn to make changes. Don’t go months with a bad plan just because you missed your enrollment period!

What/When is the Annual Enrollment Period?

The Annual Enrollment Period runs from October 15 through December 7 of each year. This is the time when all Medicare beneficiaries are eligible to make changes, which will go into effect on January 1 of the following year. It does not apply to people who have not yet enrolled in any form of Medicare coverage. If you’re enrolling for the first time, you’ll have an “Initial Enrollment Period.” You can use the AEP later to make changes if you don’t like the choices you made during your IEP.

Changing Medicare Plans After the Annual Enrollment Period

There are a few other times throughout the year when you may be eligible to make changes.

The Initial Enrollment Period (IEP) is for those enrolling in Medicare for the first time. If you are aging into the program, this will begin three months before your 65th birthday and end three months after. If you become eligible due to disability, your IEP will depend on your disability status or diagnosis.

The General Enrollment Period (GEP) is for those who missed their IEP. It runs from January 1 through March 31. If you enroll during the GEP, your coverage will begin on July 1. You may face a late enrollment penalty fee for not enrolling during your IEP. If you want to enroll in Medicare Advantage during the OEP, you can do that between April 1 and June 30, or you can wait for the AEP.

The Special Enrollment Period (SEP) is not one specific time frame. You may qualify for a “temporary” SEP if you have a special circumstance that results in a loss of coverage, such as losing a job with coverage or moving to an area where different plans are available. You will likely have 30 days following the event to make a change. Some circumstances, like having a disability, can make you eligible for a different type of SEP. If you are disabled or have low-income and have a special needs plan, you can change plans once per quarter for the first three quarters of the year.

Medicare Enrollment Periods

How can I get a SEP for Medicare?

To qualify to change plans once every quarter for the first three quarters of the year, you must:

Be a member of a Medicare Savings Program or Medicaid

Be part of SPAP (State Pharmaceutical Assistance Program)

During AEP, you can make a number of different changes to your coverage, like:

Enroll in a Medicare Advantage plan

Switch to a different Medicare Advantage plan from what you had

Drop your Medicare Advantage plan and have only Part A and Part B

Add a Part D prescription drug plan

Change to a Medicare Advantage plan with a prescription drug benefit

Change from a MAPD (Medicare Advantage Prescription Drug Plan) to a Medicare Advantage plan without prescription coverage

Change from one Part D plan to another

Drop your prescription drug coverage and return to Original Medicare only

You can also add or remove Medicare Supplement (Medigap) coverage, but keep in mind that you can enroll in Medicare Supplements during any time of year. Enrollment periods to not apply to Medicare Supplement plans. However, if you enroll in Medigap any time past your Initial Enrollment Period, underwriting may apply, leaving you with higher costs than you could have had if you enrolled sooner.

The ability to make these changes every year is more important than you may realize.

Even if you think you’re happy with your plan, plans are allowed to change their benefits and costs every year. Your plan can add or remove benefits and make cost adjustments as they need to. At the same time, new plans are continually entering (and leaving) the market. It’s a good idea to take a look and see if there is a better plan for you each year.

Licensed agents are required to go through a training and certification process before they can sell to you. They are usually trained on what’s going on in the area that they sell in. They may be able to tell you about plans that you haven’t even heard about before, and they can help you sort through your options. It does not cost anything to meet with a Medicare Plan Finder licensed agent.

Can you Auto-Renew Medicare?

In most cases, you do not have to renew your plan each year. Your Medicare coverage will automatically continue as long as you want. The only reason your plan wouldn’t renew is if that specific plan itself leaves your service area or leaves Medicare.

However, that does not mean that you shouldn’t review your coverage each year. Have your finances or your healthcare needs changed? Has your plan changed its benefits or costs? Ask these questions every year to make sure you’re still getting the coverage you need.

New to Medicare

What’s new in 2020?

There are a few 2020 Medicare changes that may affect what you want to enroll in this year:

As of 2019, you may be able to change your Medicare Advantage plan during the OEP

How to Make Medicare Plan Changes

You can enroll in a new Medicare Advantage plan by getting help from a licensed agent. If you haven’t enrolled in Original Medicare yet, be sure to do that first by contacting Social Security either online or at 1-800-772-1213. You can also visit your local Social Security office.

To get in touch with a licensed agent in your area, click here or call 844-431-1832 (TTY 711). You can also go straight to our Medicare Plan Finder tool.

The Ultimate Guide to Medigap Plan D

Medicare Supplements, also known as Medigap plans, add financial benefits that work alongside your Original Medicare. These benefits include help paying your copayments, coinsurance, and deductibles. Enrollment has increased every year since 2010, and there are more than 13 million beneficiaries taking advantage of Medigap plans in 2019.

There are more than ten types of plans (A, B, C, D, F, G, K, L, M, and N), that offer a wide range of coverage at different costs. Many plans are guaranteed renewable life which means you shouldn’t be dropped if a new health condition develops (as long as you pay your monthly premium on time). If you’re looking for financial benefits to supplement your Original Medicare coverage, Medigap Plan D may be the plan for you.

Medicare Supplement Plan D vs. Part D

Medicare Supplement Plan D can be easily confused with Medicare Part D. Medicare Supplement Plan D, is one of the ten types of Medigap plans, while Medicare Part D is prescription drug coverage.

Original Medicare (Part A and Part B) do not cover prescription drugs. Part D was created in 2006 and has since allowed beneficiaries to purchase prescription drug plans alongside Original Medicare to cut down on out-of-pocket drug costs. To learn more about Medicare Part D, click here.

Rx Discount Card | Medicare Plan Finder

Do You Need Medicare Part D If You Have Supplemental Insurance?

You are not required to enroll in a Part D plan whatsoever. However, once you are enrolled in Part A and B, you should consider enrolling in some type of prescription drug coverage to avoid a late-enrollment penalty down the road. Some Medicare Supplement plans cover prescription drug coverage, but this is rare.

You can get prescription drug coverage through some Medicare Advantage plans or a stand-alone Part D plan. You can be enrolled in a Medicare Supplement plan and Part D plan at the same time, however, you cannot be enrolled in a Medicare Supplement and Medicare Advantage plan at the same time.

If you prefer health benefits like dental, vision, or hearing coverage, or even group fitness classes like SilverSneakers®, you may be better suited for a Medicare Advantage plan. Your best bet is to talk with a licensed agent who can explain plan and benefit details that are available in your area. Fill out this form or give us a call at 844-431-1832.

Doctor’s Appointment | Medicare Plan Finder

What Does Medigap Plan D Cover?

Medigap Plan D covers all of the gaps from Original Medicare except for the Part B deductible and Part B excess charges. More specifically, Plan D includes the following:

Part A coinsurance and hospital costs

Part B coinsurance and copayments

Blood work copays up to three pints

Hospice coinsurance and copayments

Skilled nursing facility coinsurance

Part A deductible

Foreign travel emergency

Medigap Plan D Costs

If you enroll in Medigap Plan D, you will be responsible for a monthly premium, your Part B deductible, and any Part B excess charges. The Part B deductible in 2019 is $185. Part B excess charges are up to 15% of what Medicare paid for a product or service. You are only responsible for the excess charges if your doctor does not accept Medicare assignment rates.

Medigap plans generally provide the same coverage no matter who you enroll with, but they have different prices. There is no reason to overpay for a plan when there may be a cheaper plan with identical coverage.

The costs can also vary based on carrier, zip code, age, gender, and tobacco. A licensed agent can show you all of the available plans in your area and make sure you do not overpay. Fill out this form or give us a call at 844-431-1832.

Medicare Supplements | Medicare Plan Finder

Use Our Medigap Plan Finder Tool to Compare Rates

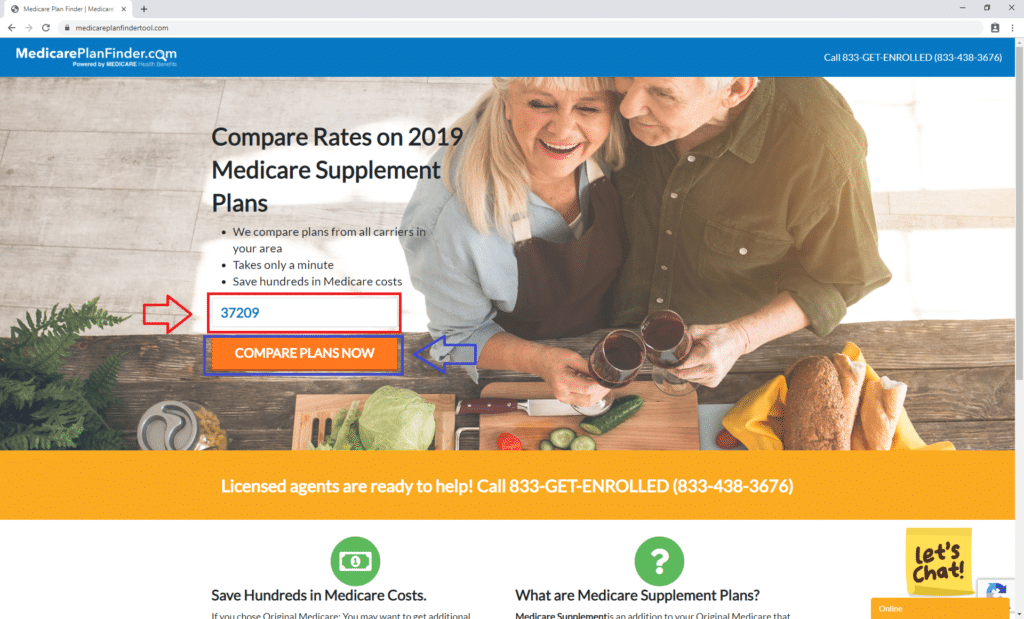

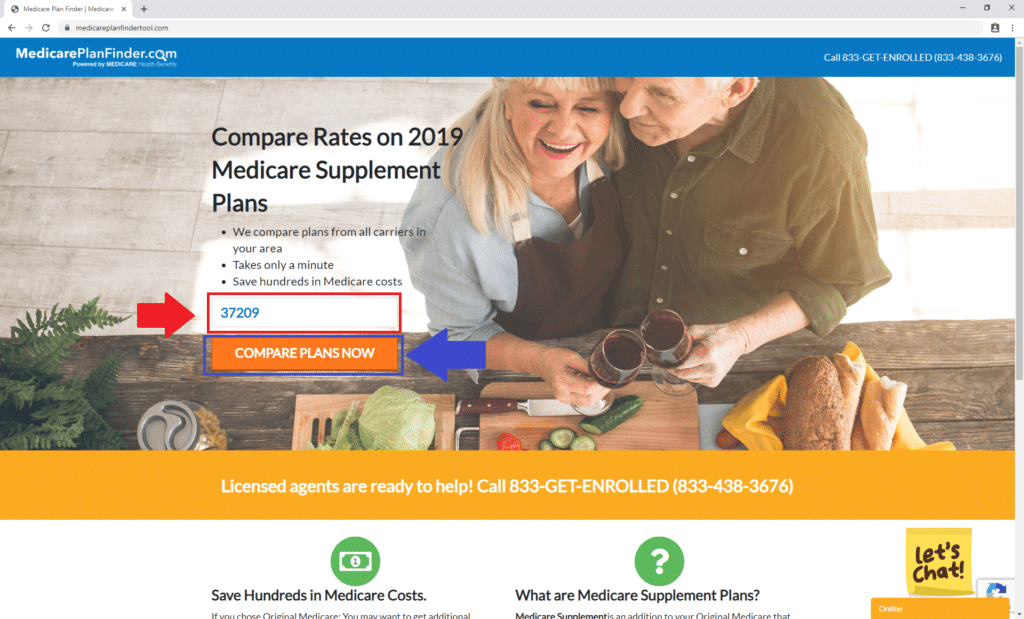

Medicare Plan Finder has a tool to help you find Medicare Supplement Plan D options in your area. To get started, click here. Step one is to enter your zip code so you can find local plans. We used 37209, which is the zip code for our corporate headquarters in Nashville, TN.

Medigap Plan Finder Tool Step 1 | Medicare Plan Finder

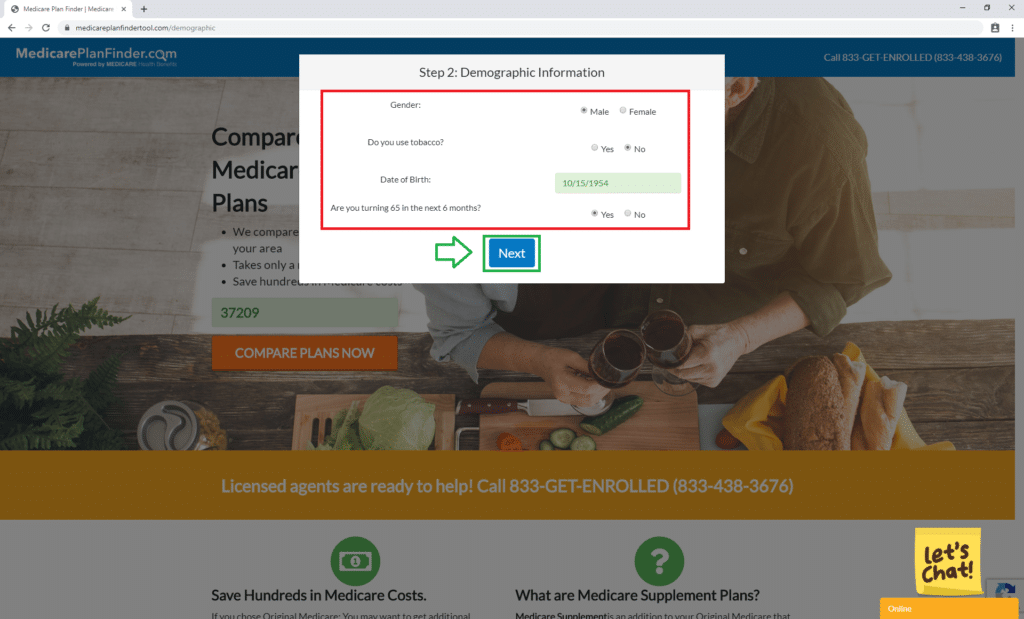

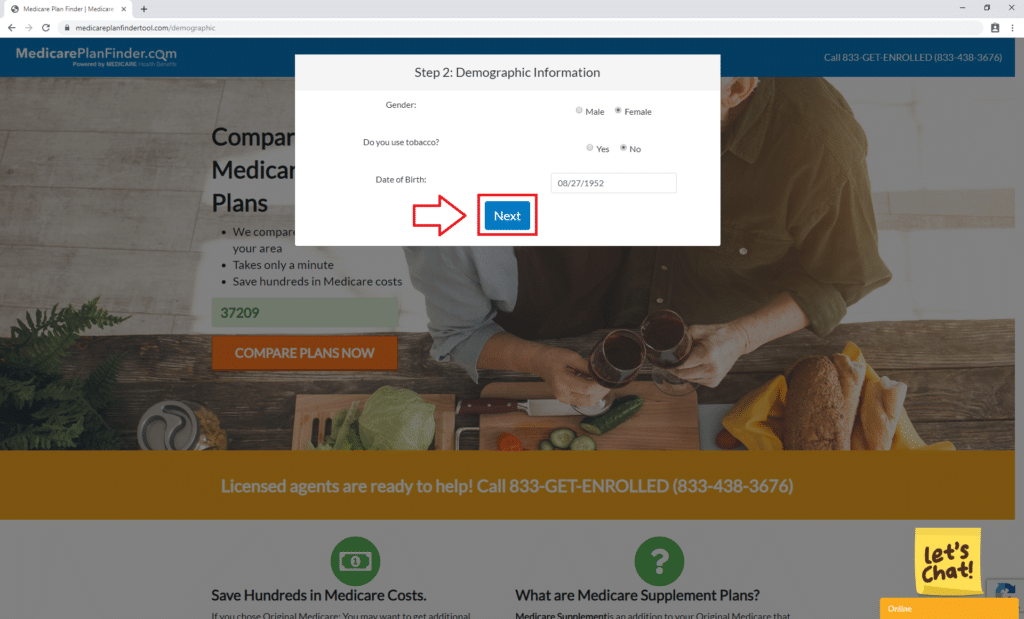

Then answer the questions in the red box. Then click “Next,” in green.

Medigap Plan Finder Tool Step 2 | Medicare Plan Finder

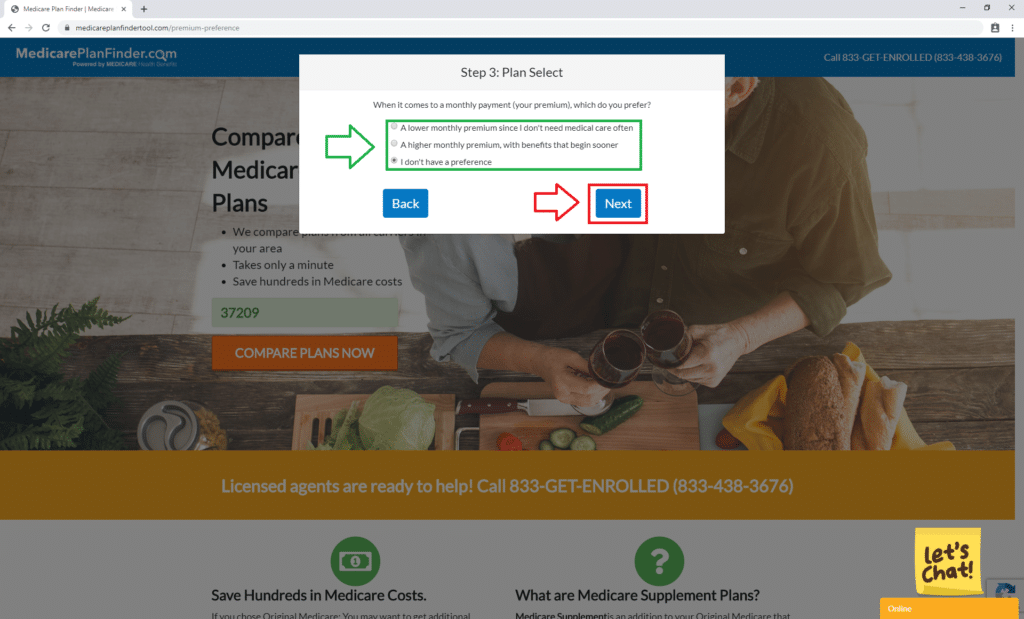

You will then select a plan preference shown in green. We chose “I don’t have a preference,” for demonstration purposes. Then click “Next,” shown in red.

Medigap Plan Finder Tool Step 3 | Medicare Plan Finder

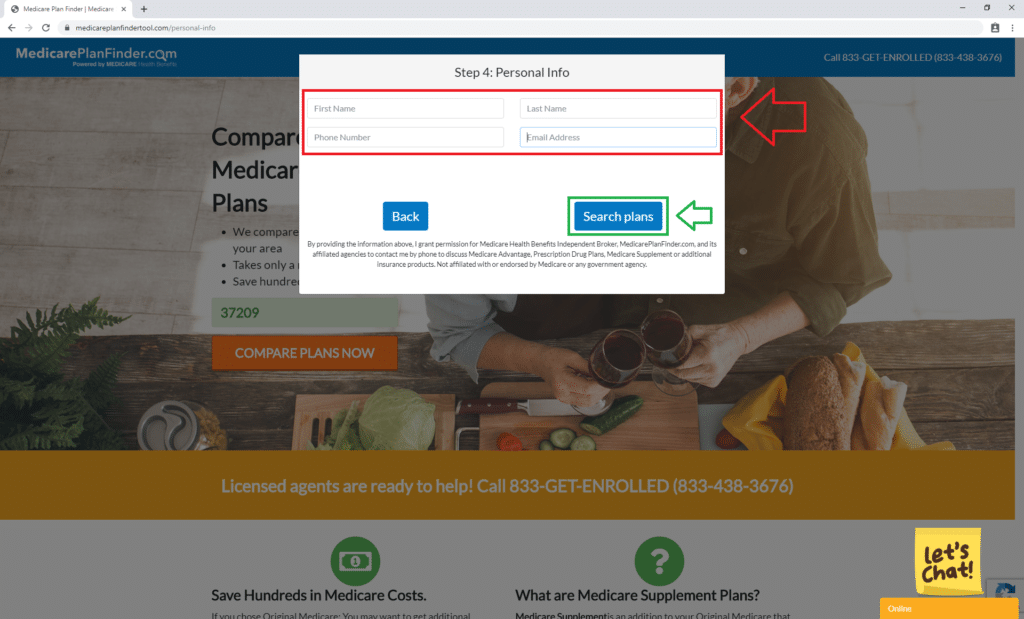

Enter your contact info on the next page in the red box, then click “Search plans,” in green.

Medigap Plan Finder Tool Step 4 | Medicare Plan Finder

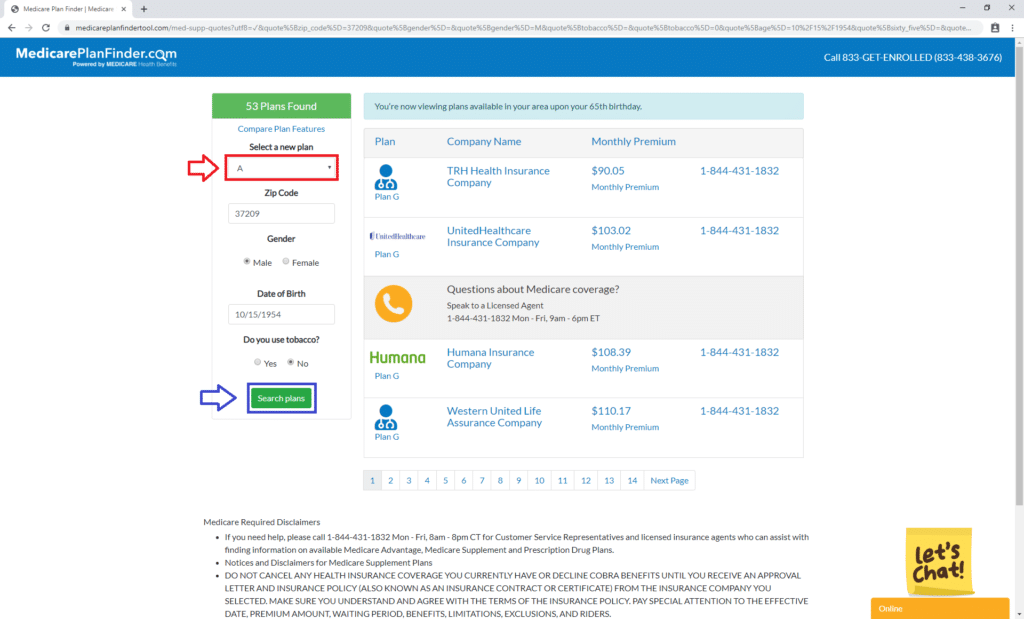

You can use the tool to look for any Medicare Supplement plan in your area, but for this blog we’re only going to look for Plan D. To find Medigap Plan D options in your area, use the drop-down menu in red to select “D”.

Medigap Plan Finder Tool Step 5 | Medicare Plan Finder

Plan D Reviews

The top carriers for Medicare Supplement Plan D in 2019 include:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

Enroll in Medigap Plan D

Did you know you can enroll in Medicare Supplement plans year around? However, carriers can charge you more, or even deny you, if you enroll outside of your initial enrollment period.

Our licensed agents can show you which Medicare Supplement plans are available in your area and help you enroll in a plan that fits your needs and budget.

Why wait? Start saving on your out-of-pocket Medicare costs now! Fill out this form or give us a call at 844-431-1832to schedule an appointment with a licensed agent. As always, appointments are cost-free to you, and there is never an obligation to enroll.

Medicare Supplement Plan Finder | Medicare Plan Finder

This post was originally published on May 10, 2019, by Kelsey Davis and updated on August 20, 2019, by Troy Frink.

As you age, it can become difficult to perform everyday tasks such as bathing or getting dressed, and you may need assistance to do those things.

Long term care may consist of skilled nursing services or physical therapy immediately following an illness or injury, or it may consist of someone coming to your house to help you with day-to-day tasks.

Does Medicare Cover Long Term Care?

Medicare Long Term Care Coverage | Medicare Plan Finder

Original Medicare does not cover long term care unless it follows a hospital stay or is for necessary medical treatment.

However, you can use certain Medicare Advantage (Part C) or Medigap (Medicare Supplement) insurance plans to help pay for non-medically necessary long term care. Here’s what Original Medicare will cover:

Medicare Skilled Nursing Coverage

Medicare Part A will cover short stays (100 days or less) in skilled nursing facilities if you meet these qualifications:

You’ve been admitted to the hospital for at least three days

A Medicare-certified skilled nursing facility admits you within 30 days of the initial hospital stay

Your treatment plan involves skilled care such as physical therapy or skilled nursing services.

Medicare will cover 100 percent of the costs for the first 20 days. In 2019, your copay for days 21-100 is $170.50.

For Medical Treatment

In order for Medicare to cover long term care for medical treatment, your doctor must first deem it medically necessary. Medicare Part B will cover the following services:

Intermittent and part-time skilled nursing care

Physical therapy

Occupational Therapy

Speech pathology

Your durable medical equipment (DME) can be covered if your doctor prescribes it and it will be used for at least three years. Medicare Part B also covers mental health services to help manage the psychological and cultural issues that come with having an illness.

There is no limit on how long you can receive the above services if your doctor reorders them every 60 days.

Chronic Special Needs Plans (C-SNP) will cover long term care services for people with chronic illnesses. The covered services for conditions such as Parkinson’s and ALS are to help prevent and slow the progression of the symptoms.

Original Medicare will NOT cover prescription drugs for chronic illnesses, however. Prescription coverage falls under Medicare Part D and certain Part C plans.

Part D Checklist | Medicare Plan Finder

Medicare Hospice Coverage

If you have a terminal illness with no chance of improvement, are expected to live less than six months, and are looking for peace instead of a cure, Medicare will cover hospice care.

In order for Medicare to cover drugs to control the symptoms and to relieve pain, you must be receiving care from a Medicare-approved hospice provider.

You can receive hospice care at your home, in a nursing home, or in a hospice care facility. When you enter hospice care, you will have an entire team of people focused on your overall comfort and well-being including your spiritual and emotional needs, not just your physical needs.

Long Term Care Coverage With Medicare Supplement Vs. Medicare Advantage

Private insurance companies offer plans that can go beyond what Medicare Parts A and B will cover. For non-medically necessary long term care, you won’t be able to use Original Medicare, and, for the most part, you won’t be able to use Medicare Supplements, either. If you want long term care coverage, a Medicare Advantage plan may be your best option.

Long Term Care Medicare Supplement

Medicare Supplements (Medigap) plans are designed to fill in the financial gaps Original Medicare creates. For example, you are financially responsible for that $170.50 copay. You can use a Medicare Supplement to help make those payments easier.

Medicare Advantage

Medicare Advantage (MA) plans are insurance plans that can cover medical services Original Medicare does not. While Medigap plans are strictly for help paying for out-of-pocket costs, MA plans are for additional medical coverage. Certain Part C plans can include coverage for DME and non-medical long term care, so it’s critical you know what your options are.

Note: You cannot have both a Medicare Supplement and a Medicare Advantage plan, so having someone help you sift through the thousands of plans out there and find the right one for you is extremely important to your overall health and well-being.

Medicare Advantage | Medicare Plan Finder

Why It’s Important to Have a Plan

Long term care can easily cost hundreds or thousands of dollars a month, and those costs will only increase. By 2050 the baby boomer population in the US will be 80 million, and that means more competition for home health care and therefore steeper prices. Having a health insurance plan to help with those costs might not only help you stay in good health, but also give you peace of mind.

Get Medicare Long Term Care Coverage Today

Are you looking for Medicare long term care coverage? One of our licensed agents can answer your questions and help you find the right plan for you. Fill out this form or call us at 844-431-1832 for a no-obligation appointment today.

Find Medicare Plans | Medicare Plan Finder

.

Everything You Need to Know About Medigap Plan M

More than one in four beneficiaries are enrolled in a Medicare Supplement (Medigap) plan. These plans work alongside Original Medicare and provide financial protection like help paying for your deductibles, coinsurance, and copays. There are ten different types of plans (A, B, C, D, F, G, K, L, M, and N) and each letter represents a different level of protection for a different price. You can have fewer benefits for a smaller monthly premium, or get more benefits for a slightly higher monthly premium. Is Medigap Plan M right for you?

What is Medigap Plan M?

Medigap Plan M is one of the cheaper options on the market because it doesn’t offer as many benefits. However, it still has more benefits than other plans (like plans K, L, and A). Specifically, Plan M covers:

100% of blood work copays (up to three pints)

100% of hospice coinsurance & copayments

100% of skilled nursing facility insurance

100% of your Part A coinsurance & hospital costs

100% of your Part B coinsurance & copayments

100% of your Part B excess charges

50% of your Part A deductible

80% of a foreign travel emergency

The only benefit that is not covered is the Part B deductible. The only plans that cover the Part B deductible are Plan F and Plan C, but they are both going away in 2020. This is because Congress found that paying the Part B deductible encouraged people to go to the doctor more often than needed. You will need to enroll before 2020 to be grandfathered-in. However, if you choose to enroll in another plan (like Plan M), you will be responsible for the Part B deductible, but it’s only $185 in 2019.

Medicare Plan M vs. Medicare Part M (Are They Different?)

Medicare can be overwhelming, and it’s easy to confuse all the different parts and plans. Medicare “parts” refer to parts A and B (Original Medicare), Part C (Medicare Advantage), and Part D (prescription drug coverage). “Medicare plans” are generally referring to Medigap plans, and as we mentioned there are ten different types. There is no “Medicare Part M.” The proper name for Medicare Plan M is “Medicare Supplement Plan M” or “Medigap Plan M.”

Medigap Plan M Eligibility

To be eligible for any Medigap plan, you must be enrolled in parts A and B first. Medigap plans are sold through private insurance companies. However, most states are not required to sell Medigap plans to beneficiaries under 65. This means if you qualified for Medicare through ESRD (end-stage renal disease), ALS (Lou Gehrig’s disease), or SSDI (Social Security Disability Income) and are not 65, you can be denied Medigap coverage. To find out if you’re eligible, click here or give us a call at 844-431-1832.

What is the Cost of Medigap Plan M?

Medigap plans (A, B, C, D, F, G, K, L, M, and N) are generally very similar no matter which carrier you buy from. For example, Plan M from Carrier one would offer mostly the same benefits as Plan M from Carrier two. However, pricing can differ based on carrier, zip code, age, gender, and tobacco use. Our licensed agents can show you all of the available plans in your area and help you enroll in the plan with the best price. Click here or call 844-431-1832 to contact a licensed agent.

Medicare Plan M Reviews

Top Medigap carriers for 2019 include:

AARP

Aetna

Blue Cross Blue Shield

Cigna

Conseco

Gerber

Mutual of Omaha

Liberty National

Oxford

Physicians Mutual

State Farm

TransAmerica

Medicare Plan M vs Plan N (and other popular plans)

Some people confuse Medigap Plan M with Plan N. Plan N is one of the most popular plans (along with Plan G). Plan G covers everything except the Part B deductible. More specifically, it covers:

Blood work copays up to three pints (100%)

Foreign emergency travel (80%)

Hospice coinsurance and copayments (100%)

Part A coinsurance and hospital costs (100%)

Part B coinsurance and copayments (100%)

Part A deductible (100%)

Part B excess charges (100%)

Skilled nursing facility coinsurance (100%)

The only benefit that is included in Plan G that Plan N does not cover is the Part B excess charges. However, excess charges are relatively rare. You will only be charged an excess charge if your provider does not accept Medicare. If you would prefer to pay a bit more towards your monthly premium in exchange for coverage on excess charges, Plan G may be perfect for you.

Other popular plans include Plan F and Plan C, but as we mentioned, they are going away in 2020. These plans are popular because they cover the Part B deductible. The only difference between Plan F and Plan C is that Plan F covers Part B excess charges. Click here to find out which Medigap plan is best for you.

How to Enroll in Medigap Plan M

Did you know you can enroll in Medigap Plan M (or any Medigap plan) any time of the year? But if you wait too long, carriers can charge you more or even deny you coverage based on any health conditions you may have. Your best bet is to enroll during your Initial Enrollment Period (IEP). During this time, you shouldn’t be denied or charged more based on any conditions. If you IEP has already passed, that’s okay! One of our licensed can still show you plans that are available in your area. Click here or call 844-431-1832h.

Prescription Drug Price Trends

About one in four people say they have a tough time affording their prescription drugs. Prescription drug prices have been on the rise since 2017. According to Rueters, drug companies announced price increases for more than 250 medications in 2019.

According to the Centers for Medicare and Medicaid (CMS), prescription drugs already account for 20 percent of Medicare’s spending, and with the prescription drug price trend increasing, that number will only increase in the near future. That may mean that your vital medications will cost you more.

How to Get Prescription Drug Discounts

Rising prices shouldn’t mean that you have to stop taking your needed drugs. Wouldn’t it be great if you could get a discount for your necessary medications? You can with this free discount drug card!

Prescription Drug Discount Card | Medicare Plan Finder

This discount card is not an insurance plan. However, you can use your discount card to receive up to 75 percent off your prescriptions at more than 68,000 pharmacies. Simply download, print and show your card to the pharmacist when you check out to save money on your important medications.

Why Are Prescription Drug Costs Rising Rapidly?

Senior Man With Pill in Hand | Medicare Plan Finder

The prescription drug price trend may be going up due to a lack of competition for pharmaceutical companies, and mergers and acquisitions in the pharmaceutical industry.

Lack of Competition for Pharmaceutical Companies

Many major pharmaceutical companies own patents for their drugs. That means other manufacturers cannot legally create generic equivalents, and the patent holders can charge whatever they want for their products.

Usually, manufacturers will produce generic drugs once a brand name patent expires. Some drugs are expensive to develop even with an expired patent, so that often means the original manufacturer is the only company producing their drug.

Mergers and Acquisitions in the Pharmaceutical Industry

Drug manufacturers make deals to expand their product bases. Unfortunately, when pharmaceutical companies merge, they get a lot of bargaining power. The pharmaceutical companies can demand that pharmacy benefit managers (PBM) – people responsible for contracting with pharmacies and getting drug discounts – set prices higher. Those costs get passed on to the government and ultimately to you.

Sometimes, pharmacy benefit managers merge with health plans, like in the cases of Cigna and Express Scripts and CVS and Aetna. Those mergers may actually be able to HELP you, by lowering costs due to reduced overhead and improved communication.

Medicare Prescription Drug Price Negotiation Act

One reason the prescription drug price trend is rapidly increasing is that CMS cannot legally negotiate drug prices. The Medicare Prescription Drug Price Negotiation Act is a bill that would require Medicare to negotiate prescription prices with pharmaceutical companies. It was first introduced in the House of Representatives in 2017, and re-introduced in 2019.

Other federal and state entities are making efforts to help reduce drug prices. The Food and Drug Administration is working toward approving more generic versions of brand name medicines. Many states have passed laws requiring drug companies to justify price increases.

Medicare Prescription Drug Plans

Prescription Drugs | Medicare Plan Finder

As prices rise, you may want to consider a new form of prescription drug coverage. Original Medicare does not help pay for prescriptions, but you can get prescription drug coverage through Medicare Part D, or through certain Medicare Advantage (Part C or MA) plans.

You can still use your discount drug card along with your insurance plan. When you go to the pharmacy to pick up your prescriptions, the pharmacist can determine your cost with each option.

Medicare Part D

Medicare Part D plans are also called prescription drug plans (PDPs). You can use PDPs to cover your medication costs. Many people who have PDPs also purchase Medicare Supplement (Medigap) plans to help pay for items such as coinsurance and copays.

Even though Medicare Supplements and Medicare Advantage plans sound similar, they are actually very different. Medigap plans “fill in” the gap between what you owe and what Original Medicare covers. MA plans help pay for medical expenses. If you have questions, one of our highly trained, licensed agents will be happy to help. Your agent can help you find the right plan for your budget and lifestyle.

PDPs typically use formularies that divide medications into tiers according to their copays. For example, one plan may feature four tiers with varying expenses. The first tier may only include generic drugs and cost $5 per prescription. Tier two may include preferred brand name medications and cost $15 per prescription.

Medicare Part D Checklist | Medicare Plan Finder

Medicare Advantage Prescription Drug Plans

Medicare Advantage plans are privately owned insurance policies that cover everything Original Medicare covers, but they can offer additional services including vision, hearing, and dental. Certain MA policies called Medicare Advantage Prescription Drug (MAPD) plans offer medication coverage.

Like PDPs, MAPDs use a formulary that lists every covered drug and separates them into tiers. The difference is that MAPD plans come with only one monthly premium for your covered services, and it includes prescription drugs.

Medicare Over-the-Counter Drug Coverage

Many people use over-the-counter (OTC) drugs along with their prescription medications. Like with prescription medications, Original Medicare does not cover OTC drugs. However, certain MA plans help pay for OTC medications. Some plans feature a pre-paid card that allows you to purchase covered items such as bandages and cold medicine.

How We Can Help You With Rising Prescription Drug Prices

Your agent can help you find a plan that not only includes all of your prescriptions, but covers the additional services you need. Call us at 844-431-1832or contact us here to learn more today.

Contact Us | Medicare Plan Finder

What is Medigap Plan L?

Medicare Supplement plans (also known as Medigap plans) work alongside Original Medicare to provide financial benefits and protection. More than nine million beneficiaries are enrolled in a Medigap plan, and enrollment increases each year.

There are ten standardized plans broken down by letters (A, B, C, D, F, G, K, L, M, and N). Each letter represents a different range of coverage for a different price. You can have fewer benefits for a smaller monthly premium, or get more benefits for a slightly higher monthly premium.

Most plans are guaranteed renewable for life, meaning as long as you pay your premium on time, you should not be canceled from your plan due to a new health condition. Plans are also generally the same regardless of which carrier you enroll with. If you’re looking for financial benefits to supplement your Part A and B, Medigap Plan L may be perfect for you.

What Does Medigap Plan L Cover?

Medigap Plan L is one of the cheaper options on the market because it doesn’t cover as much as some of the other plan types. Specifically, Plan L covers:

100% of your Part A coinsurance & hospital costs

75% of blood work copays (up to three pints)

75% of hospice coinsurance & copayments

75% of skilled nursing facility insurance

75% of your Part A deductible

75% of your Part B coinsurance & copayments

Other benefits of Medigap plans include coverage for:

Part B deductible

Part B excess charges

Foreign travel emergency

Plan L Costs

Medigap plans (A, B, C, D, F, G, K, L, M, and N) are generally very similar no matter which carrier you buy from. This means that, for example, Plan L from Carrier 1 would offer mostly the same benefits as Plan L from Carrier 2. However, pricing can differ based on carrier, zip code, age, gender, and tobacco use. Our licensed agents can show you all of the available plans in your area and help you enroll in the plan with the best price. Click here or call 844-431-1832 to contact a licensed agent.

Medicare Supplement Eligibility

To be eligible for a Medicare Supplement plan, you need to be enrolled in Original Medicare (Part A and B). Medigap plans are sold through private insurance companies and are not required to sell a plan to beneficiaries under 65. This means if you qualified for Medicare by turning 65, having ESRD (end-stage renal disease) or ALS (Lou Gehrig’s Disease), or through Social Security Disability Income (SSDI), you may not be eligible for a Medigap plan. However, a licensed agent can help you find any available plans in your area that you may qualify for. Click here or call 844-431-1832 to contact a licensed agent.

Plan L Reviews

Some of the top Medigap carriers for 2019 include:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

Popular Medicare Supplements

Some of the most popular Medigap plans are Plan G and Plan F because they offer the most coverage. Plan F is almost identical to G, the only difference is Plan F covers the Part B deductible. However, Plan F is going away, and you must be enrolled in Plan F no later than January 1, 2020, to maintain coverage. Plan G is cheaper than Plan F with almost identical benefits, so many beneficiaries prefer Plan G.

If you would prefer to pay a higher monthly premium, but have more financial protection, Plan G or F may be right for you. Contact a licensed agent to talk about plan specifics. Click here or call 844-431-1832.

Enroll in a Medigap Plan

You can enroll in Medigap Plan L (or any Medicare Supplement plan) any time of the year, but if you wait too long, carriers can charge you more or even deny you coverage based on your health conditions. You should consider enrolling in a Medigap plan during your Initial Enrollment Period (IEP). During your IEP, you should not be denied or charged more for any pre-existing conditions. If your IEP has already passed, that’s okay! A licensed agent can still show you plans in your area and help you enroll in a qualified plan. Click here or call 844-431-1832 to contact a licensed agent.

Guide to Medicare Supplement Plan N

Medicare Supplement plans, also known as Medigap plans, add financial benefits that work alongside Original Medicare. More than nine million beneficiaries are taking advantage of this additional financial protection, and enrollment continues to increase each year.

There are ten different types of Medigap plans, (A, B, C, D, F, G, K, L, M, and N), and each letter represents a different level of coverage. Plans are the same regardless of which carrier you enroll with. This means if you want to enroll in Plan N, the benefits are the same whether you enroll with Aetna, Cigna, etc.

Plus, most plans are guaranteed renewable life, which means you shouldn’t be dropped if a new health condition develops (as long as you pay your monthly premium on time). If you’re looking for financial benefits to supplement your Original Medicare, but don’t want a huge monthly premium, Medicare Supplement Plan N may be right for you.

What is Medicare Plan N?

Medicare Supplement Plan N was introduced in 2010 and has been a popular choice for beneficiaries ever since. Plan N covers:

Part A coinsurance and hospital costs

Part B coinsurance and copayments

Blood work copays up to three pints

Hospice coinsurance and copayments

Skilled nursing facility coinsurance

Part A deductible

Foreign travel emergency

Medicare Supplement Plan N Eligibility

To be eligible for any Medicare Supplement plan, you must be enrolled in Part A and B first. Medicare Supplements are sold through private insurance companies. However, most states are not required to sell Medigap plans to beneficiaries under 65. This means if you qualified for Medicare through ESRD (end-stage renal disease), ALS (Lou Gehrig’s disease), or SSDI (Social Security Disability Income) and are not 65, you can be denied a Medigap plan. To find out if you’re eligible, click here or give us a call at 844-431-1832.

What is the Cost of Medicare Supplement Plan N?

As we mentioned, plan benefits are usually the same from carrier to carrier. However, that doesn’t mean the pricing is the same. Plan N requires some cost sharing in certain situations. There is typically a copayment of up to $20 for doctor appointments and $50 for hospital admittance. Medicare Plan N does not cover the Part B deductible ($185 in 2019) or Part B excess charges. Part B excess charges are up to 15% of what Medicare paid for a product or service. You are only responsible for the excess charges if your doctor does not accept Medicare assignment rates.

The cost of your monthly plan premium will vary based on your zip code, age, gender, and tobacco use. There’s no need to overpay for a plan if there is a cheaper plan available in your area that offers identical benefits. Our licensed agents can show you plans specific to your zip code and can help prevent overpaying. Click here or give us a call at 844-431-1832.

Medicare Supplement Plan N Reviews

If plan benefits are the same across carriers, why are some plans reviewed higher than others? Well, price is a huge factor. Companies with higher customer ratings have plans with higher ratings. Lastly, customer service is an important factor. Here is a list of some of the top Medigap carriers for 2019:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

Medicare Plan N vs Plan G

Medicare Supplement Plan G is another popular Medigap plan. The only benefit that is included in Plan G that Plan N does not cover is the Part B excess charges. However, the thing to remember about excess charges is they are relatively rare. You will only be charged an excess charge if your provider does not accept Medicare. If you would prefer to pay a bit more towards your monthly premium in exchange for coverage on excess charges, Plan G may be perfect for you. One of our licensed agents can help you enroll. Click here or give us a call at 844-431-1832.

Medicare Plan N vs Plan F

Plan F has been a top-selling Medicare Supplement for years. The only difference between Plan F and Plan N is that Plan F covers the Part B deductible and Part B excess charges. Plan F is going away in 2020 (along with Plan C). The Centers for Medicare and Medicaid Services believe that coverage for the Part B deductible results in beneficiaries visiting the doctor too often, costing Medicare millions of dollars. If this benefit is something that is appealing to you, you need to enroll before 2020 to be grandfathered in. Fortunately, one of our licensed agents can help. Click here or give us a call at 844-431-1832.

How do I get Medicare Plan N?

You can enroll in a Medicare Supplement plan any time of the year, but carriers can charge you more or deny coverage if you wait too long. The best time to enroll is during your Initial Enrollment Period. During this time, you can enroll in any plan that is in your area without being denied or charged more for pre-existing conditions. Click here or give us a call at 844-431-1832 to get in contact with a licensed agent.

What is Medigap Plan K?

Medicare Supplements are often referred to as Medigap plans. These plans provide financial benefits and help cover out-of-pocket expenses that Original Medicare does not, like copayments, coinsurance, and deductibles. More than 22% of Medicare beneficiaries are enrolled in a Medigap plan and enrollment has increased each year since 2010.

Medigap plans are broken down into ten standardized plans (A, B, C, D, F, G, K, L, M, and N). Each letter offers a different range of coverage at a different price point. You can evaluate which benefits are the most important to you and if you would rather pay a higher monthly premium for more benefits or pay less and receive less coverage.

Medicare Supplements are also popular because most are guaranteed renewable life, which means as long as you pay your premium on time, you will not be canceled from your plan due to new health conditions. Plus, Medicare Supplements are generally the same regardless of which carrier you enroll with. If you’re looking to supplement your Original Medicare, Medigap Plan K may be a good option.

What does Medigap Plan K Cover?

The fewer benefits a plan provides, the lower the monthly premium is. This means Plan K is cheaper than other plans on the market like Plan F or Plan G. Plan K covers:

Part A coinsurance and hospital costs

50% of Part B coinsurance and copayments

50% of bloodwork co-payments (up to 3 pints)

50% of hospice coinsurance and copayments

50% of skilled nursing facility coinsurance

50% of your Part A deductible

Other benefits of Medicare Supplements include:

You’re able to keep your current doctor (as long as they accept Medicare)

You can see a specialist without needing a referral

Coverage travels with you throughout the U.S.

Plan K Costs

Medigap plans are generally the same regardless of which carrier you enroll with. This means if you want to enroll in Medicare Supplement Plan K, you will have the same coverage whether you enroll with Blue Cross Blue Shield, Cigna, or another carrier. However, while the coverage may be the same, the costs are not. The cost of your plan will vary based on your zip code, age, gender, and tobacco use. Our licensed agents can show you available plans in your area and help you enroll in a plan that fits your needs and budget. Fill out this form or give us a call at 844-431-1832.

Medicare Supplement Eligibility

Medicare Supplement plans are designed to work alongside Original Medicare. To be eligible, you must be enrolled in Part A and B first. Medicare Supplements are sold through private insurance companies. However, most states are not required to sell Medigap plans to beneficiaries under 65. This means if you qualified for Medicare through ESRD (end-stage renal disease), ALS (Lou Gehrig’s disease), or SSDI (Social Security Disability Income), you could be denied Medigap coverage. Your best bet is to speak with one of our licensed agents. They can help you look for any plans that are available to you and discuss plan specifics. Fill out this form or give us a call at 844-431-1832.

Plan K Reviews

Some of the top Medigap carriers for 2019 include:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

AARP Medicare Supplement Plan K

AARP is a very popular choice when purchasing Medigap Plan K. AARP offers competitive rates that have only been increased an average of 2.9% over the last 5 years. They also provide fast service through the claims process. Most claims are processed within ten days or less. Lastly, AARP has a 98% customer satisfaction service rating. If you’re interested in enrolling in Medigap Plan K with AARP, fill out this form or give us a call at 844-431-1832.

Enroll in Medigap Plan K

You can enroll in a Medicare Supplement plan any time of the year, but if you wait too long, carriers can charge you more or deny you for your health conditions. The best time to enroll is during your initial enrollment period. During this time, you can enroll in any plan that is in your area and not be denied or charged more for pre-existing conditions. A licensed agent can show you available plans in your area and help you save money in the long-run. When you meet with one of our agents, there is never a cost to you and absolutely no obligation to enroll. Fill out this form or give us a call at 844-431-1832.

What is Medicare Supplement Plan C?

Medicare Supplements, also known as Medigap plans, help cover out-of-pocket expenses that Original Medicare does not. This includes copayments, coinsurance, and deductibles. More than 22% of Medicare enrollees are taking advantage of these financial benefits, and enrollment has increased every year since 2010.

There are more than 10 types of plans (A, B, C, D, F, G, K, L, M, and N) and each plan offers different coverage at different prices. Most plans are guaranteed renewable life, which means as long as you pay your premium on time, you should not be canceled from your plan if a new health condition develops.

Plus, unlike Medicare Advantage plans, Supplements generally include the same coverage regardless of which carrier you enroll with (though some will add additional benefits). If you’re looking for additional financial benefits to supplement your Original Medicare, Medicare Supplement Plan C may be the way to go.

Medicare Part C vs. Plan C

Medicare Part C and Plan C are two very different things. There are four main parts of Medicare (A, B, C, and D). Original Medicare includes Part A, hospital insurance, and Part B, medical insurance. Prescription drug coverage can be purchased through Part D.

Part C is better known as Medicare Advantage (MA). MA plans are offered through private health insurance companies and provide the same coverage as Original Medicare, but with several additional benefits like hearing, vision, and dental coverage, and even fitness programs like SilverSneakers®.

However, Plan C is one of the ten Medicare Supplement plans that are available. You may hear Plan C referred to as Part C, but Plan C is the correct term.

Is Medicare Plan C Going Away?

Medicare Plan C, along with Plan F, will be discontinued in 2020. Plans C and F both include coverage for the Part B deductible, which is a benefit that the Medicare program wants to discontinue. They have found that some consumers are taking advantage of that benefit by visiting their doctor much more often than needed, costing Medicare millions of dollars. That money can be much better spent on providing coverage for people who truly need it.

If you currently have Plan C or Plan F, you will not be kicked off your coverage. If you are interested in enrolling in Plan C or Plan F, you need to do so by January 1, 2020, to be grandfathered in. Click here to get in contact with a licensed agent.

Medicare Supplement Plan C vs. Plan F

Plan F is the most popular Medicare Supplement plan but is very similar to Medicare Plan C. The only difference is that Medicare Plan C does not include Medicare excess charge coverage. If a doctor does not accept Medicare assignment rates, you will be responsible for excess charges, but it can not exceed 15% of what Medicare pays. Some states do not allow doctors to issue excess charges. If this is the case, Plan C will operate identically to Plan F.

What Does Medicare Supplement Plan C Cover?

Medicare Plan C covers all of the gaps from Original Medicare except for Part B excess charges. More specifically, Plan C includes the following:

Part A coinsurance and hospital costs

Part B coinsurance and copayments

Blood work copays up to three pints

Hospice coinsurance and copayments

Skilled nursing facility coinsurance

Part A deductible

Part B deductible

Foreign travel emergency

Plan C Costs

Medicare Supplement plans are generally the same regardless of which carrier you enroll with. This means if you want to enroll in Plan C, you will have the same coverage whether you enroll with Aetna, Cigna, Blue Cross Blue Shield, etc. However, costs will vary based on carrier, zip code, age, gender, and tobacco use. There’s no need to overpay for a plan if there’s a cheaper alternative on the market with identical coverage.

Plan C is an extremely comprehensive Medicare Supplement plan. If you would prefer a less comprehensive plan at a cheaper price point, you should consider Plan A or Plan B. Your best bet is to speak with a licensed agent who can show you all of the Medicare Supplement plans that are available in your area and help you enroll in the plan best suited for your needs and budget.

Plan C Reviews

Here is a list of some of the top Medigap carriers for 2019:

AARP

Aetna

Cigna

Humana

Mutual of Omaha

WellCare

When to Enroll in Medicare Supplement Plan C

You can enroll in a Medicare Supplement plan any time of the year, but carriers can charge you more, (or even deny you), for existing health conditions. The best time to enroll is during your initial enrollment period. This way, you can enroll in any plan that is in your area and not be denied or charged more for pre-existing conditions.

Medigap Plan Finder Tool

A licensed agent can show you available plans in your area and help you save money in the long-run. When you meet with one of our agents, there is never a cost to you and absolutely no obligation to enroll. Fill out this form or give us a call at 844-431-1832.

You can also start comparing different Medigap plans by using our Medigap plan finder tool at medicareplanfindertool.com.

Medicare Supplement Plan B: Costs and Benefits

Medicare Supplement (Medigap) plans help cover out-of-pocket Medicare expenses including co-payments, coinsurance, and deductibles. Enrollment in these plans has increased every year, and more than 22% of Medicare enrollees take advantage of this type of supplemental coverage in 2019.

There are ten types of Medicare Supplement plans (A, B, C, D, F, G, K, L, M, N) and unlike Medicare Advantage plans, they provide the same basic benefits regardless of which carrier you enroll with.

Plus, most plans are “guaranteed life,” which means that as long as you pay your premium on time, you won’t be canceled from your plan if a new health condition develops.

Medicare Supplement plans are great for beneficiaries who would rather pay a small annual deductible for financial protection in the event of an unforeseen health expense.

What does Medicare Supplement Plan B Coverage Include?

Medicare Supplement Plan B is very similar to Medicare Supplement Plan A. The only difference is Plan B covers your Medicare Part A deductible. Plan B covers:

Part A coinsurance and hospital costs

Part B coinsurance and co-payments

Bloodwork co-payments (up to 3 pints)

Hospice coinsurance and co-payments

Part A deductible

Medicare Plan B Cost

Even though the benefits are mostly the same per carrier, the costs of the plan will vary based on carrier, zip code, age, gender, and tobacco use. Some plans are as low as $80/ while some are as high as $140/month.

The fewer benefits a plan provides, the lower the monthly premium is. Since Plan B offers less coverage, it is typically one of the cheapest plans on the market.

Medicare Plan B Deductible

If you choose to enroll in a Plan B Medicare Supplement plan, you will be responsible for your Part B deductible, but your Part A deductible will be included in your plan. The 2019 Medicare Part B deductible is $185.

You will also be responsible for any skilled nursing facility care coinsurance, Part B excess charges, and emergency health costs while traveling. This is great if you rarely see unexpected health costs and would rather have lower monthly costs than high premiums for benefits you don’t use.

If you generally have high costs in the areas that Plan B does not cover, it may not be the best plan for you. Instead, you should consider the more comprehensive Plan G. Alternatively, if Plan B sounds great, but you would prefer a cheaper monthly payment, you should explore Plan A, which has fewer benefits but typically has the lowest costs.

Medicare Supplement Plan Finder | Medicare Plan Finder

Medicare Supplement Plan B vs. Medicare Part B

Medicare Plan B and Medicare Part B are two entirely different things but can be easily confused. Medicare Supplement Plan B is a Medigap plan and Medicare Part B works alongside Part A to form Original Medicare. It covers medically necessary doctor services and treatments as well as preventative services like yearly wellness visits. This includes lab tests, x-rays, emergency transportation, durable medical equipment, mental health, and partial hospitalization. If you want to enroll in Plan B (or any Medicare Supplement), you need to be enrolled in Part A and B first.

Medicare Supplement Plan B Options

There are several Medicare Supplement plans on the market, but availability will vary based on your location. As we’ve mentioned, plans generally offer the same coverage regardless of carrier, so why do some plans have better reviews? Companies with higher ratings generally offer plans with higher ratings. Customer service is another factor. Here is a list of the top Medigap carriers in 2019:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

Use Our Medicare Supplement Plan Finder Tool to Find Plan B Options in Your Area

Our Medicare Supplement Plan Finder tool can help you find Plan B options in your area. Click here to get started. Enter your zip code in the box beside the red arrow. We chose 37209 because that’s the zip code for our corporate offices in Nashville, Tennessee.

Medicare Supplement Finder Tool Step 1 | Medicare Plan Finder

Next, choose the appropriate circles for your gender and tobacco use and enter your date of birth. Then click “Next.”

Medicare Supplement Finder Tool Step 2 | Medicare Plan Finder

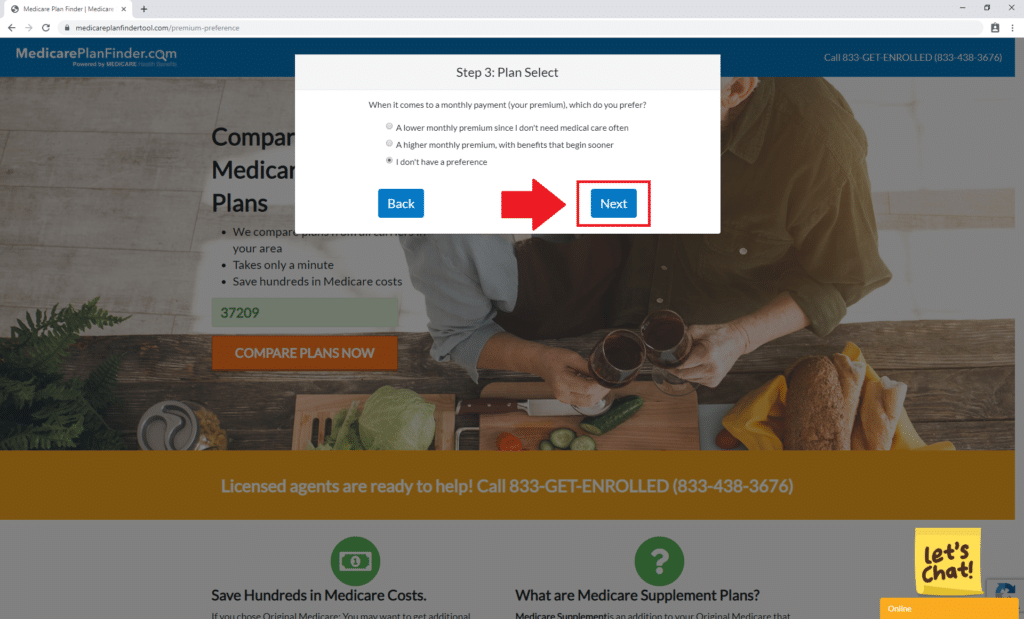

Then select your plan preference and click “Next.”

Medicare Supplement Finder Tool Step 3 | Medicare Plan Finder

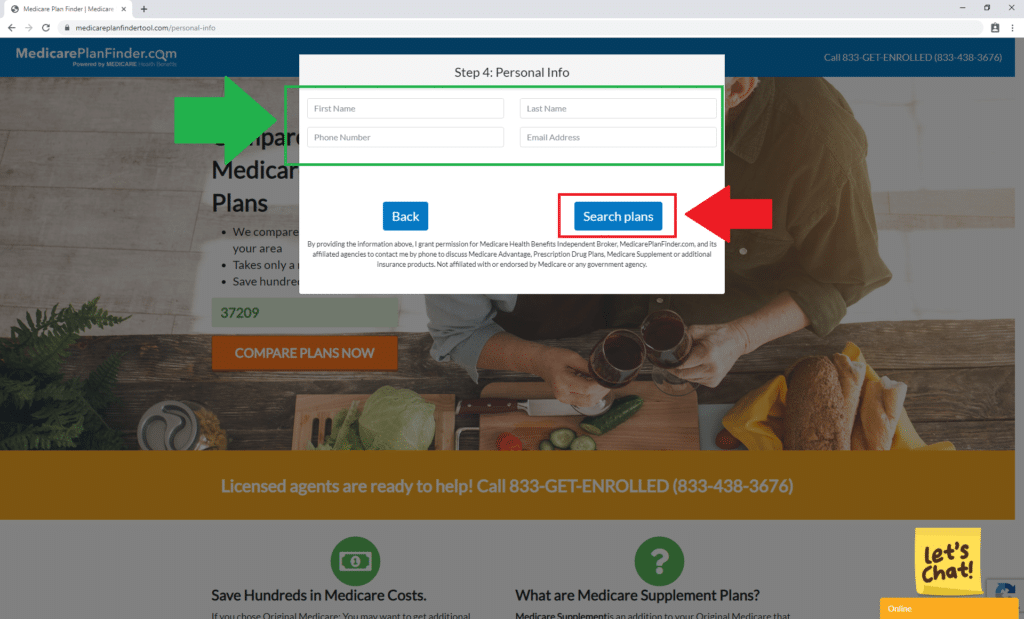

Next enter your personal information in the boxes beside the green arrow. Then click “Search plans” beside the red arrow.

Medicare Supplement Finder Tool Step 4 | Medicare Plan Finder

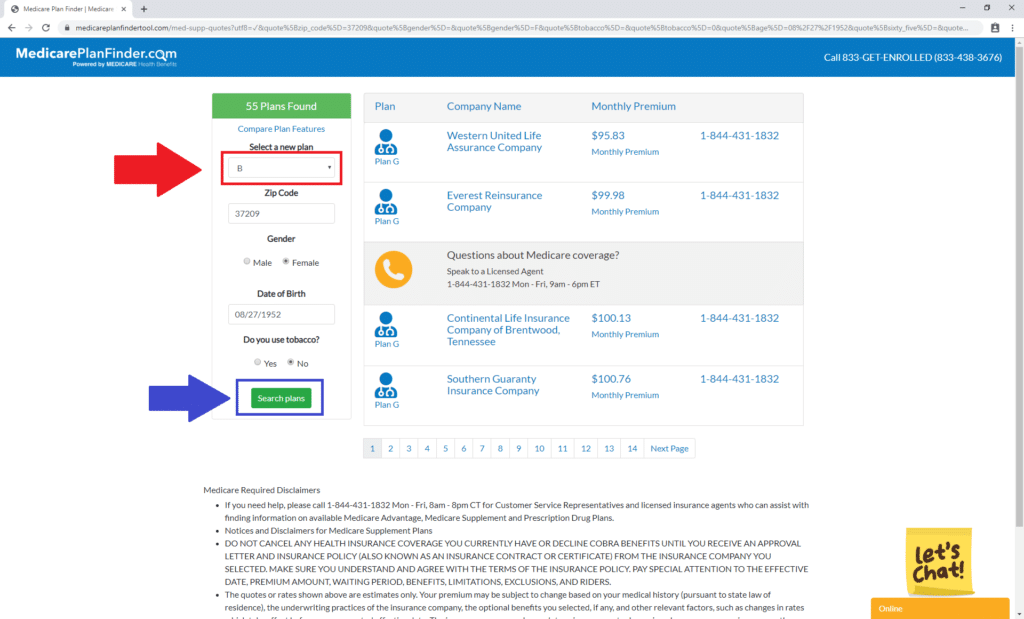

The final step is viewing the Plan B options in your area. Select “B” from the drop-down menu beside the red arrow. Then click “Search plans” beside the blue arrow.

Medicare Supplement Finder Tool Step 5 | Medicare Plan Finder

Medicare Plan B Enrollment

You can enroll in a Medicare Supplement plan during any time of the year, but carriers can deny you or charge you more for existing conditions. The best time to enroll is during your Initial Enrollment Period (IEP), which is the seven months around your 65th birthday. During this time, you can enroll in any plan that is available in your area regardless of any health issues you may have.

If saving money is important to you, a licensed agent can help you enroll in the cheapest plan available in your area. When you meet with one of our agents, there is never an obligation to enroll, and the appointment is entirely cost-free to you. Fill out this form or give us a call at 844-431-1832.