Before reading further, please note the very important fact listed below about Medicare supplement insurance benefits and cost that can easily be found and verified directly on Medicare’s website by going here.

Key Fact About Medicare Supplement Plan G and other Plans.

“The benefits in each lettered plan are the same, no matter which insurance company sells it. The premium amount is the only difference between policies with the same plan letter sold by different companies.” – Centers for Medicare and Medicaid’s Medicare and You Handbook 2025 – page 77, paragraph 1.

So, then what?

This means that if you know a Medicare supplement is the right type of insurance for you, you are simply shopping the price, and the prices can vary greatly due to many variables. It’s important to understand the rate history and claims paying ability of the insurance company you choose as that is a great indicator if you will be subject to excessive future rate increases vs. future rate stability and moderate increases.

Do not let a low price tag fool you and lock you into the wrong insurance company.

Now, lets dive into more detail about the Plan G Medicare supplement.

What is Medicare Supplement Plan G?

Medicare Plan G is one of several Medigap Plans you can buy from a private company to pay healthcare costs not covered by Medicare Part A and Medicare Part B. Medigap plans are often referred to as Supplemental plans as well.

These plans help cover co-payments, deductibles, and coverage during international travel.

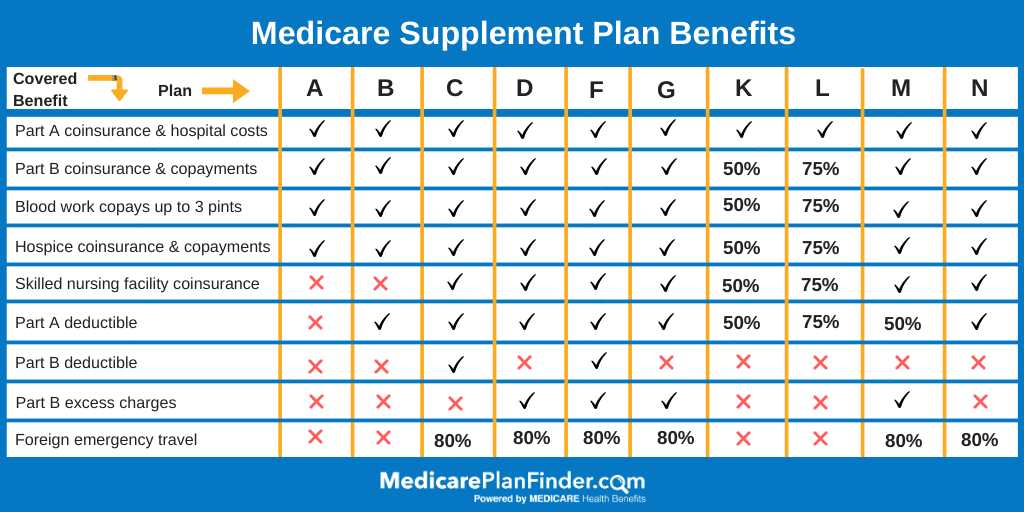

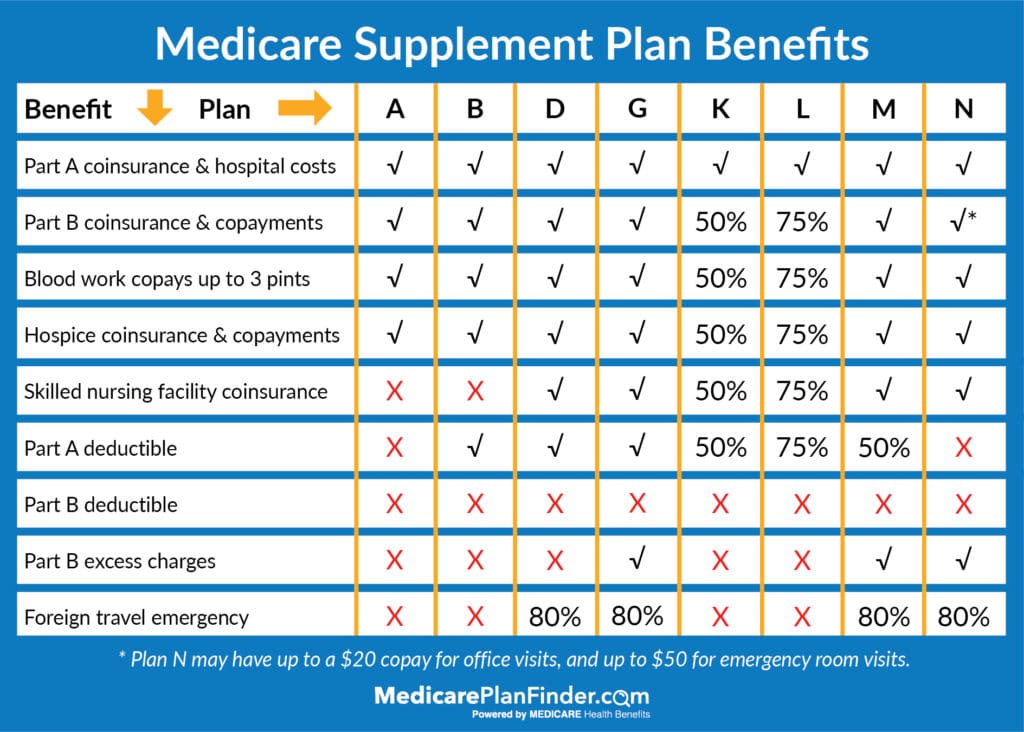

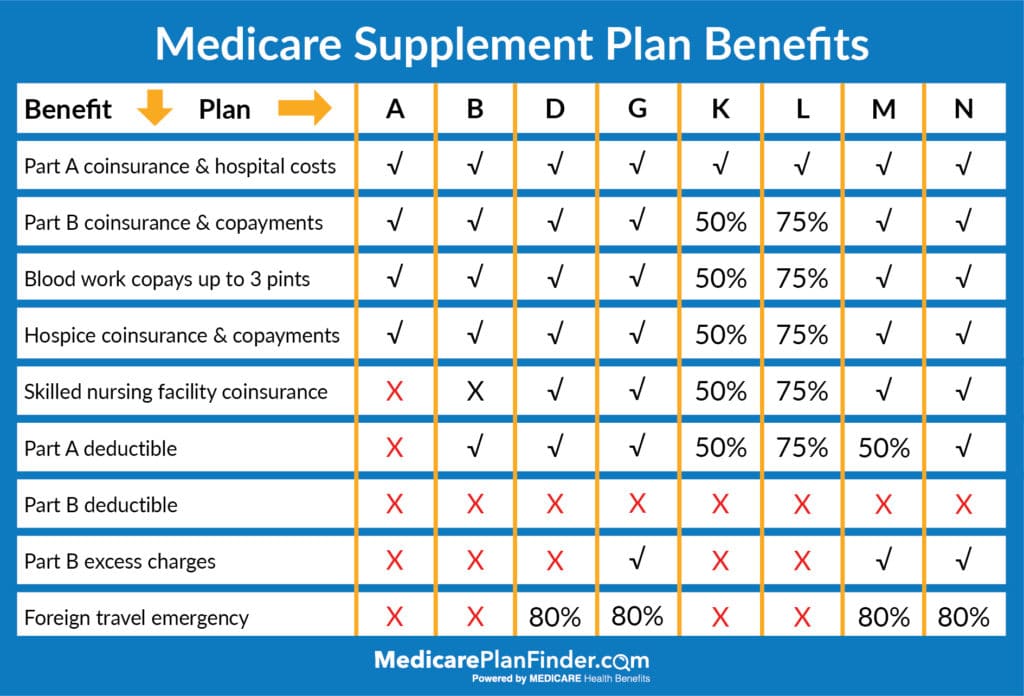

Medigap plans are identified by letter, A through N. Current offerings include Plans A, B, C, D, F, G, K, L, M and plan N. Plans E, H, I, and J are no longer available to new subscribers.

It’s important to note that Medigap Plans A, B, C, and D are not the same as Medicare Parts with the same corresponding letters. Medicare has four parts, but Medigap policies are referred to as plans.

Overall, about 1 in 5 Medicare enrollees also purchase a Medigap plan.

Each plan is different in terms of exact coverage and costs. There are a variety of plans so that you can buy a plan that best fits your individual needs.

Plan G is characterized by providing excellent benefits to beneficiaries who want to pay a small annual deductible. That protects them from spending more on out-of-pocket expenses for unexpected health issues.

It is similar to Medicare Plan F, which prior to it being cancelled, was the most popular Medigap plan.

Medicare Plan G: Who is it for?

Many people choose Plan G because it’s the most comprehensive plan available as of 2026. For individuals who prefer to have more control over their expenses, plan G is a strong choice for Medicare supplement as it’s very clear what the monthly costs are.

However, to decide if Plan G is right for you, it’s best to take a closer look at the specific benefits. You may also want to look at other plans to see if one is better suited for you as well. A common plan many choose over a plan G is a plan N due to the premium being lower in exchange for copays at the doctor, ambulance rides and ER visits.

What Medicare Plan G covers

Plan G covers all the gaps in Part A and Part B coverage, except for the Part B deductible. Specifically, those benefits include:

Part A deductible

Part A coinsurance and hospital costs

Part B coinsurance and co-payments

Blood work, and the first three pints of blood for medical needs

Hospice care co-payments and coinsurance

Foreign travel medical emergencies (up to $50,000)

Skilled nursing facility coinsurance

Outpatient medical services such as lab work, diabetes supplies, durable medical equipment, doctor visits, ambulance services, and more.

All Medigap plans do not include prescription drug coverage. You will need to buy a Part D plan to be covered unless medications are prescribed as part of Plan B coverage and include drugs such as for chemotherapy or autoimmune diseases that must be administered in a clinical setting.

Also, Medigap plans do not cover routine dental care.

How Medigap Plan G works with Original Medicare

To sign up for a Plan G policy, you must first be enrolled in Medicare Part A and Part B.

Original Medicare will pay its share of the Medicare-approved amount for covered services. Plan G will then pay its share.

It’s important to note that you cannot have a Medicare Part C plan and a Medigap plan in force at the same time.

Unlike Medicare Advantage plans, Medigap plans are all the same no matter from which company you buy a policy.

In fact, CMS publishes this every year in the Medicare and You Manual and states the following:

The benefits in each lettered plan are the same, no matter which insurance company sells it. The premium amount is the only difference between policies with the same plan letter sold by different companies.

This means you’ll get the same coverage if you buy a Plan G policy from Cigna or buy a Plan G policy from Aetna, or any other provider.

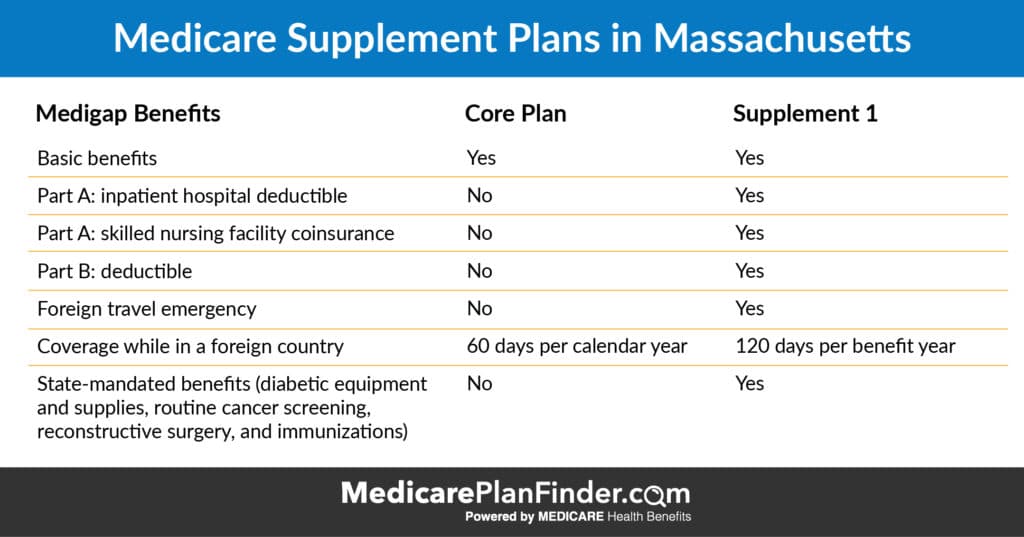

If you live in Wisconsin, Minnesota, or Massachusetts, you may not have access to Plan G. Medigap policies are standardized differently in these states:

Even though by law, all Plan G policies must cover the same thing, premium costs can vary. These costs will depend on the carrier, zip code, age, gender, and whether or not you smoke.

Plans are typically priced between $80 and $170 per month and are in addition to your Part B premium. If you go with a high deductible Plan G, your premiums will be less.

Like other Medigap policies, a Plan G policy only covers one person. If you and your spouse both want Plan G coverage, you will both need to buy policies.

You’ll need to work with a licensed agent to plug in all the variables and come up with the best and most affordable plan for your particular needs.

Also, keep in mind that if you don’t enroll during your Initial Enrollment Period, there’s no guarantee you’ll get coverage, and if you do, it could cost you more. If you can get coverage and you have a pre-existing condition, you may have to wait for up to an additional six months for coverage to kick in.

One other important thing to know is that if you buy a Plan G policy and drop it, there’s no guarantee you be able to re-enroll.

Medigap Plan G vs. other Medicare Supplement plans

Here’s how Plan G stacks up against other Medigap plans.

Is Medicare Plan G better than Plan F?

Plan G and Plan F are almost identical to each other.

The only difference is that Plan F covers the Medicare Part B deductible. However, Plan C and Plan F are being phased out, and only people enrolled in those two plans before December 31, 2019, get to keep those plans.

The good news is that Plan G is cheaper than Plan F with almost identical benefits, so many beneficiaries prefer Plan G anyway because it is viewed as a better overall value.

For example, you will need to pay the Part B deductible, but with lower monthly premiums for Plan G, you could save $400 or more each year.

The standard Part B deductible in 2020 is $198, but Medicare also introduced a high deductible Plan G with an annual deductible of $2,340 in January 2020.

When Can I Get Medicare Supplement Plan G?

The best time to get a Plan G policy is during your Initial Enrollment Period. You are guaranteed coverage for any plan that’s available in your neighborhood, regardless of any existing health conditions.

You can enroll at any other time during the year, but an insurance company can charge you more for existing conditions or deny you coverage outright.

Your best bet is to speak with an agent who will give you complete details.

What you need to know before enrolling in Medigap Plan G

One of the most important aspects of all Medigap plans is that they are guaranteed renewable, even if you develop health problems. You can’t be canceled by an insurance company as long as you pay your premium.

Also, guaranteed issue rights are in play in certain situations. This means an insurance provider must offer you certain Medigap policies when you are not in your Medigap Open Enrollment Period.

If you qualify, a provider must sell you a policy, cover your pre-existing conditions, and can’t charge you more even if you have past or present health problems.

Typically, guaranteed issue rights are available when you lose other health coverage or your existing coverage changes. You also have a trial right if you decide to buy a Medicare Advantage plan and want to change your mind and return to a Medigap policy.

Guaranteed issue rights are federal law. Many states also provide additional Medigap rights.

Plan G policies are not going away per se, but first dollar coverage is, due to deductible coverage no longer being offered for Part B. High Deductible Plan G is also a new change for 2020 as well.

If you have questions about Medigap coverage in your state or to make sure you qualify for all benefits, contact your State Health Insurance Assistance Program (SHIP).

Medicare also published a comprehensive guide to choosing a Medigap policy that may answer several questions as well.

To buy an affordable Medigap plan, you need to compare policies to see which one best meets your needs. Your best bet is to work with a licensed insurance agent in your area.

You can also use the Medicare.gov website to find a Medigap policy or call your SHIP for information.

An agent will help you compare costs once you decide which plan to buy. Keep in mind all coverage by letter is the same, but premium costs can be different.

When you buy a policy, the insurance company must give you a plain-language summary of your benefits. Read it and make sure you understand everything. If you don’t, be sure to ask questions.

Companies that offer Plan G

You have several choices when deciding which Plan G to buy. Price is a significant factor. And there are also several A, and B rated companies that offer policies.

Overall, consider that companies with higher ratings have plans with higher ratings. Outstanding customer service is an essential factor.

Top Medicare Supplement Companies in 2026:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

The top of this Medicare supplement list doesn’t necessarily mean the best rates or the best claims ratio. The list is written in alphabetical order from top to bottom.

Surgeons perform more than 3.8 million cataract procedures every year in the United States. As you age, your risk of developing cataracts increases. Approximately half of all Americans will develop cataracts by age 75.

Before factoring in health care coverage, cataract surgery can cost $3,700 to $7,000 per eye. If you have one of the millions of cases of cataracts, you may wonder, “Does Medicare cover cataract surgery and implants?” Yes. Medicare covers these costs for qualified Medicare beneficiaries.

How Much Does Medicare Pay for Cataract Surgery?

Original Medicare (Part A or Part B) generally* does not include vision coverage. However, cataract surgery is an exception. Medicare Part B covers basic lens implants and cataract removal.

If your provider recommends an advanced lens implant, you may need to pay some or all of the additional costs. It’s essential to talk with your doctor to get a clear understanding of the necessary procedure.

*Medicare Part A may cover emergency services in a hospital.

Medicare Part D, which is the prescription drug plan, may cover any prescription medications you need after you have had your cataract surgery.

Incidentally, any medications you need before surgery, such as prescription eye drops, will be covered by Medicare Part B. Part B will also cover eyeglasses or a set of contact lenses for cataract surgery that implants monofocal intraocular lenses (IOL).

Since Part D has no deductibles, you may be responsible for a specified copayment amount that you must pay when you get your prescription drugs.

What Type of Cataract Surgery Does Medicare Cover?

Medicare covers two types of surgery: manual blade surgery and laser surgery.

Medicare will also pay for an intraocular lens (IOL), which corrects presbyopia or astigmatism, but only if these lenses should be replaced because of cataracts.

Does Medicare Pay for Laser Cataract Surgery?

Medicare coverage for cataract surgery doesn’t depend on the surgical method. Medicare will cover 80% of the cataract removal and basic lens whether the procedure is conventional or bladeless with a computer-controlled laser. Similar to conventional surgery, laser surgery requires you to pay the additional costs if you require an advanced lens.

Does Medicare Pay for Cataract Surgery With Astigmatism?

Since you can correct astigmatism with glasses, Medicare will only cover a cataract surgery with astigmatism if the cataract surgery itself is considered necessary. If this is the case, Medicare will pay for the cataract surgery.

Does Medicare Cover Glasses or Contacts?

For the most part, Medicare does not cover routine vision care, glasses, or contact lenses. However, Medicare can make an exception

You may be wondering, “How much does Medicare pay for glasses after cataract surgery?” After your surgery, Medicare will cover 80% of the costs for prescription glasses or contacts, but you must purchase them through a provider who accepts Medicare assignment.

You will be responsible for the remaining 20%. Some beneficiaries have trouble getting Medicare to cover the pair of glasses or contacts.

If you are denied coverage, you can appeal the decision and request that they are covered. If you already paid for them out of your own pocket, you can request reimbursement.

You and your health provider can write a letter to add to your appeal, just be sure to state that you had met the requirements for cataract surgery, so your glasses or contacts must be covered.

What Is the Average Cost of Cataract Surgery?

Cataract surgery can range from $3,800 to $7,000 per eye without a health insurance plan. For standard cataract surgery, the average cost is $3,700.

However, the average cost of astigmatism-correcting surgery is $5,000, and presbyopia-correcting is about $7,000.

What does Medicare pay toward cataract surgery? It depends on the Medicare plan you are enrolled in. If you are only enrolled in Original Medicare, you will need to pay a 20% coinsurance and your Medicare Part B deductible, which is $185 in 2019.

You may be able to get even more coverage through a Medicare Supplement plan (Medigap) or Medicare Advantage plan. Additionally, because cataracts cloud the eye lens, eye surgery is classified as a medical condition.

This means that Medicaid could also pay some of your cataract surgery costs.

How to Find a Cataract Surgeon Who Accepts Medicare

Ophthalmologists are eye doctors who specialize in vision correction and care. Many times your ophthalmologist will perform your cataract surgery.

Since not every ophthalmologist will accept Medicare Advantage and you may not want to go through the trouble of finding another healthcare provider, then ask your health insurance provider to give you a Medicare eye doctor list.

However, it may be a little more difficult to find a cataract surgeon who accepts Medicare in 2020 because the physician fee schedule has changed since last year. Eye surgeons have had to take a 15% cut in reimbursement compared to Medicare coverage for cataract surgery in 2019.

So another option is to use the Medicare.gov’s physician compare tool to help you find an eye surgeon who accepts Medicare.

Click here to get started. First you’ll come to the physician finder tool. Enter your zip code in the search bar beside the red arrow. We used 37209, which is our corporate offices’ zip code in Nashville, TN.

Then type “ophthalmology” in the search bar above the green arrow. Then click “Search” beside the yellow arrow.

Then you’ll come to a list of ophthalmologists who currently accept Medicare. Use the contact info to call different doctors to find the right fit.

Medicare Requirements for Cataract Surgery

Your vision must be 20/40 or worse to qualify for surgery. Your doctor will need to document that your vision is at this level or lower.

You also need to have difficulty completing daily living activities like reading, sewing, watching television, or driving.

It’s important to remember that the cloudiness in your eye is not directly correlated to the severeness of your cataracts. If you are unsure of your vision level or whether or not you qualify, visit your eye doctor.

Cataract Surgery and Medicare Supplements

Medicare Supplements work alongside Original Medicare and are a great way to add financial benefits to your current coverage. They can help cover your 20% coinsurance and your Medicare Part B deductible.

Plan F is currently the only plan that covers your Part B deductible.

However, Plan F was discontinued in 2020. If you enrolled in it before the start of 2020 you are locked into this plan and will maintain coverage. If you are interested in enrolling in Medicare Supplement Plans, fill out this form or give us a call at (833)-567-3163.

Cataract Surgery and Medicare Advantage

Medicare Advantage plans are required to cover, at a minimum, the same as Original Medicare. However, MA plans offer several additional benefits like prescription drug coverage, hearing and dental coverage, group fitness classes like SilverSneakers, and additional vision coverage.

Benefits will vary by plan but can include routine eye exams, eyeglasses, contacts, frames, and fittings. These benefits allow you to check your vision each year and update your prescription, lenses, and frames as needed.

If you are only enrolled in Original Medicare, you will need to pay for these expenses out of your own pocket.

What Are Cataracts?

Our eyes have a lens that works much like a camera. The lens bends light so you can see your surroundings.

A cataract makes that clear lens cloudy, and it can be more difficult to read or drive a car.

What Causes Cataracts?

Most of the time, cataracts develop with age, or when an injury changes your eye’s lens. As you age, the lens can become stiffer, thicker, and less transparent.

Sometimes genetic disorders, other eye conditions, medical conditions such as diabetes, or past eye surgery can contribute to cataract development. Other causes can be long-term steroid medication use.

Cataract Symptoms

According to the Mayo Clinic, signs and symptoms of cataracts can include:

Cloudy, blurry or dim vision

Increasing difficulty seeing at night

Sensitivity to light and glare

Need for brighter light for reading and other activities

Seeing “halos” around lights

Frequent changes in glasses or contact lens prescription

Fading or yellowing of colors

Double vision in one eye

How Do You Know If You Need Cataract Surgery?

Talk to your doctor if you experience any changes to your vision such as cloudiness or halos around lights. According to Harvard University, you should have an eye exam every year if you’re 65 or older.

Dr. Laura Fine, an ophthalmologist with Massachusetts General Hospital, says you don’t need cataract surgery until you think you need to see better.

Learn More About Medicare and Cataract Surgery

A licensed agent with Medicare Plan Finder may be able to find plans in your area that fit your budget and lifestyle needs.

Are you interested in learning about available plans in your area? Fill out this form or give us a call at (833)-567-3163 to schedule a no-cost, no obligation appointment with a licensed agent.

Does Medicare Cover Hospice Care?

More than 1.7 million Americans use hospice each year to maintain or improve their quality of life due to a terminal illness. Hospice care plans address physical, emotional, and spiritual pain and offer support to caregivers during the grieving process.

Hospice decisions can take an emotional and financial toll on you and your family, so you may be asking… “Does Medicare cover hospice?”

How does Medicare cover hospice care?

If you are enrolled in Medicare Part A (hospital insurance), you may qualify for hospice care. However, you must meet the following criteria:

Your doctor certifies that you are terminally ill (with a life expectancy of less than 6 months)

You accept palliative care (for comfort) rather than try to cure your condition

You sign an agreement choosing hospice care over other Medicare-covered benefits to treat your illness

You are not eligible if you had already made a hospice election or have not previously received pre-election hospice services (evaluation of your need for pain and symptom management).

If you meet the above criteria, the following services may be part of your hospice care plan and are covered in part by Medicare:

Other services focused on pain and symptom management

There may be a co-payment of $5 for your prescription drugs or other pain relief. You may also need to pay five percent of the Medicare-approved amount for respite care. However, the following services are not covered by Medicare:

Hospice is intended for people who have six months or less to live. To receive hospice care, you can not receive curative treatment.

If you decide to receive treatment, your hospice care is no longer covered. However, you can withdraw from your hospice care at any given point, and you can resume treatment as long as you are still eligible.

Prescription Drugs Intended to Cure

Just like you can’t pursue curative treatment, you can not take prescription drugs that are intended to cure your illness when receiving hospice care. Hospice only covers drugs that are intended for pain relief and control.

Care for Any Hospice Provider That Wasn’t Arranged by the Hospice Team

You are only eligible to receive care from the hospice team that you initially select.

You cannot get hospice coverage from a different provider unless you go through the switching process. However, you can still visit your regular doctor if they have been appointed to supervise your hospice care plan.

You can only switch to a different hospice provider once per benefit period. If you are interested in switching, be sure to do your research and pick a hospice team you feel comfortable with.

Does Medicare cover hospice room and board?

Medicare does not cover room and board regardless if you live at home, in a nursing home or inpatient assisted living facility, or inpatient hospice office. The only exception is during short-term inpatient or respite care stays in which Medicare will help cover the costs.

Emergency Care

Emergency transportation is not covered by Medicare’s hospice benefits. Medicare will not cover emergency inpatient hospital care unless they are arranged by your hospice team or unrelated to your terminal illness.

Does Medicare cover hospice in a nursing home or at home?

If you are eligible, Medicare will cover hospice care regardless if you receive the care in your home, nursing home, or inpatient facility. Some nursing homes work directly with a hospice team. In a nursing home setting, your hospice team can help with the following:

Regular visits to the nursing home

Consultations by specialized hospice physician as needed

Pain and medication management

Educating staff on symptoms, medications, and care

Emotional and spiritual support

Coordinating care across all patient’s medical providers including doctors, hospice team, and nursing home staff

How long will Medicare pay for hospice care?

Hospice care is intended for people who have less than an estimated six months to live. If you still require hospice care after six months, you can continue to receive benefits if a hospice doctor recertifies your terminal illness in a face-to-face meeting.

You can get hospice care for two 90-day benefit periods followed by an unlimited number of 60-day benefit periods.

Level One: This level includes basic care under Medicare’s hospice benefit. Services include nursing services, medical equipment & supplies, and medications.

Level Two: Medicare designates people who need continuous care such as home health care. The home health aide stays in the patient’s home for eight to 24 hours a day, but it’s short-term care. The patient’s needs are re-evaluated once every 24 hours.

Level Three: The third level of Medicare hospice coverage is general inpatient care. Some people have short-term symptoms that are so severe that they can’t get adequate treatment at home. With level three care, the patient has 24-hour care available.

Level Four: This level of care is more for the family than the patient. If the patient doesn’t meet the criteria for inpatient care and the family needs a break from daily care duties, respite care may be an option. Respite care provides caregivers temporary relief by admitting the patient to a hospital.

Medicare Palliative Care vs. Medicare Hospice Care Coverage

Medicare can cover palliative care for helping relieve symptoms in accordance with curative care. Some organizations define palliative care as “specialized medical care for people living with a serious illness” with the focus of care being symptom relief rather than to find a cure.

The difference between palliative care and hospice care is that palliative care can occur in conjunction with curative care.

Medicare may cover palliative care, but not under the Medicare hospice benefit.

Hospice and Medicare Supplements

Medicare Supplements can help cover the gaps in hospice care that Original Medicare may not, like prescription drugs for pain relief and respite care. After your Medicare coverage, you will likely be responsible for five percent of your total respite care costs and a $5 copay per prescription drug. Medicare Supplements can cover some, or all, of these gaps.

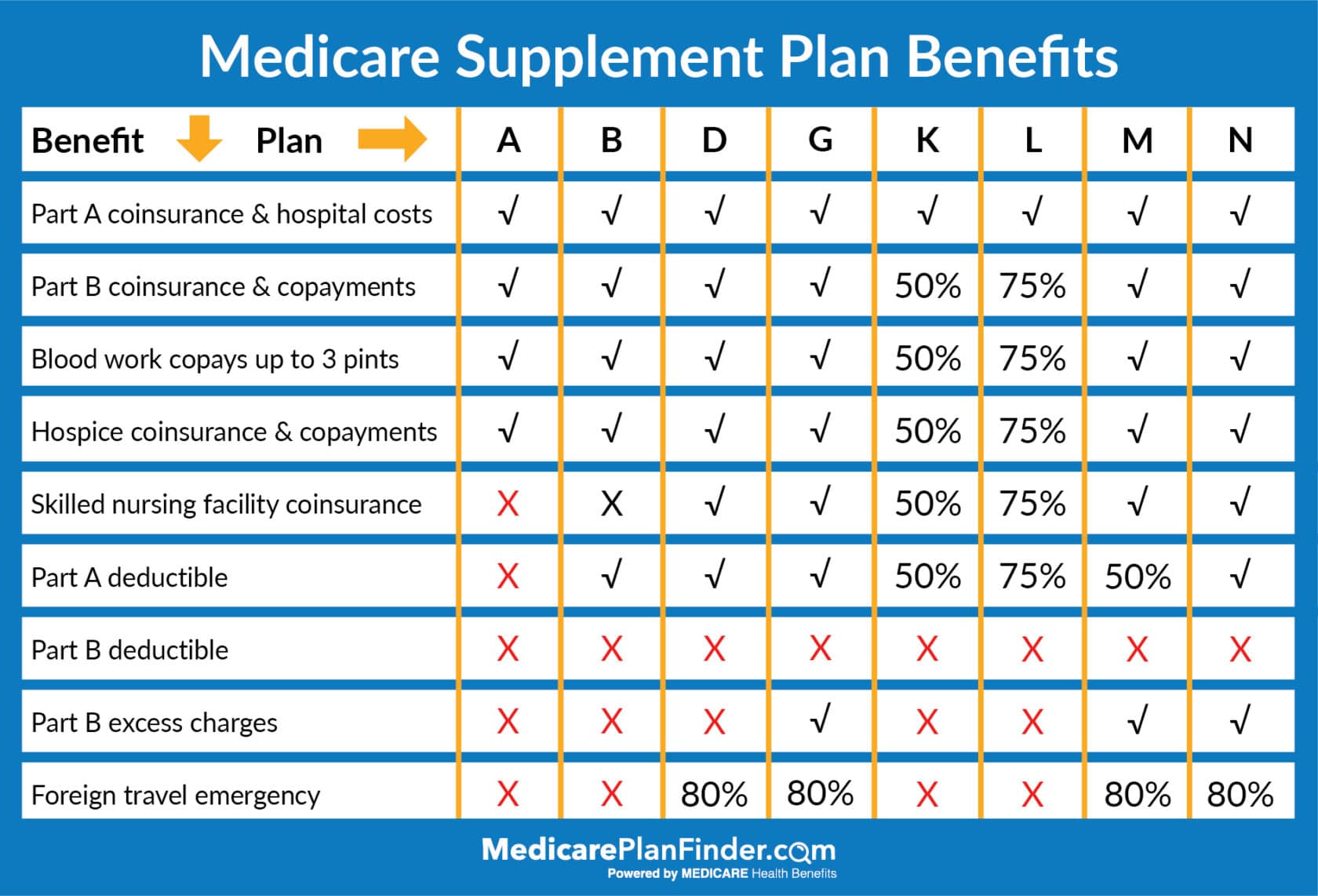

Medicare Supplement Plans A, B, D, G, M, N cover 100 percent of hospice coinsurance and copayments. Medigap Plan K covers 50 percent and Plan L covers 75 percent.

If you are interested in enrolling in a Medicare Supplement plan, or have questions on how these plans work with your correct coverage, click here to get in contact with a licensed agent.

2020 Medicare Supplement Comparison Chart

Hospice and Medicare Advantage

If you enroll in a Medicare Advantage plan, you will have the same hospice care coverage as with Original Medicare. However, Medicare Advantage plans can offer extra benefits like vision, hearing, and dental coverage. They may also offer fitness programs like SilverSneakers®.

If you are interested in enrolling in a Medicare Advantage plan, fill out this form, or give us a call at 844-431-1832. There is no cost to you to meet with one of our agents and there is never an obligation to enroll.

This post was originally published on April 16, 2019, and updated on November 18, 2019.

2020 Medicare Changes & Trump’s Executive Order

Every year, CMS (Centers for Medicare and Medicaid Services) reserves the right to make changes to the Medicare program. Rules and regulations around enrollment periods, penalty fees, marketing, and plan benefits are released in late summer and early fall for the following year. Costs can rise, and brand new plans can enter or leave the market.

Medicare is confusing as it is. When you add these yearly changes into the mix, choosing the right plan can be stressful. Our goal is to make all of this less stressful for you. Our website is a great educational tool, and our licensed agents can provide free assistance!

Here are the changes you need to know about for Medicare in 2020.

On October 3, 2019, President Donald Trump signed an executive order “protecting” the Medicare program. What does this mean?

Alex Azar, Health and Human Services (HHS) Secretary, said that Trump told HHS to take “specific, significant steps” towards improving Medicare funding and improving healthcare for American seniors. These steps include lowering Medicare Advantage costs, allowing savings accounts, and improving access to new medical technology. It also leaves room for more plan options, more telehealth, more wellness benefits, and a stronger financial model.

In his post-executive order speech given in Florida yesterday morning, Trump stated, “In my campaign for president, I made you a sacred pledge that I would strengthen, protect and defend Medicare for all of our senior citizens.” That was the intent of the executive order.

Is Medicare Going Up in 2020?

New 2020 Medicare premiums and costs for 2020 have not been released yet. The new numbers are usually released in early fall of the year prior, so we are expecting to see them over the coming months. The Wall Street Journal reported in April that 2020 Medicare Part B premiums are likely to increase by $8.80/month to a total of $144.30, but this is not final.

We will continue to update this post with new 2020 costs as they are released. Thank you for your patience!

2020 Medigap Changes

Just like the Original Medicare program, private plans like Medicare Advantage, Medicare Supplements, and standalone benefit plans can change every year.

Plan availability may not be the same for everyone. Medigap eligibility, in particular, can depend on your age when you enroll, preexisting conditions, and where you live. Plans can be different not only in every state but also in every county and zip code.

Use our plan finder tool to find out what Medigap plans are available in your area for 2020.

Is Medicare Supplement Plan F Going Away in 2020?

Starting in 2020, you will no longer be able to purchase Medigap Plan F or Medigap Plan C. Plan F was one of the most popular plans, and Plan C was fairly similar. The plans are going away because they include coverage for the Part B deductible (only $185 in 2019).

You might here plans C and F referred to as “first-dollar” plans because they virtually eliminate out-of-pocket costs. CMS decided that taking away the Part B deductible coverage was a smart move to discourage people from overusing their primary physician offices and costing the Medicare program a lot of money for unnecessary doctor’s visits.

If you already have Medigap Plan F or Medigap Plan C, you can be grandfathered in. That means that you will not lose your coverage in 2020. However, if you leave your Plan F or Plan C in favor of a different Medigap plan, you won’t be able to re-enroll in F or C.

Will Plan F Premiums Rise After 2020?

As Plan F sees less and less enrollees, Plan F premiums will likely begin to rise. We can’t say this for sure and we will certainly have to wait and see what happens, but generally less enrollees means higher costs for the companies, resulting in higher premiums.

Will There be a High Deductible Plan G in 2020?

Since people will not be able to purchase Plan F or Plan C in 2020, CMS did want there to be another option with similar benefits. Plan G was already that option, given that the only difference is that Plan G does not cover the Part B deductible.

The other difference is that previously, Plan G was not offered with a high-deductible. If you typically have low medical costs, you may prefer a high-deductible option. Having a high deductible often means that your premiums will be lower. This way, you don’t have to pay as much until you start experiencing health concerns. The high deductible Plan G option can replace the high deductible F option.

Donut Hole Closing in 2020

In addition to all of these plan changes, the infamous “Donut Hole” will be effectively closing in 2020. The Bipartisan Budget Act of 2019 closed the coverage gap for brand-name drugs in 2019, and the generic drug coverage gap will be eliminated in 2020. This basically means that, if you have a Medicare Part D plan, you will only be responsible for 25% of your covered prescription drug costs instead of 44%.

2020 Medicare Advantage Changes

There may be more Medicare Advantage plan changes to come in 2020, but we wanted to make sure you had heard about the changes from last year.

On October 12, 2018, the Centers for Medicare and Medicaid (CMS) announced the 2019 Original Medicare premium and deductible increase, but what about Medicare Advantage (MA) plans? Unlike Medicare Part A and B, beneficiaries enrolled in MA plans may see a decrease in their premiums in 2019 and 2020 compared to 2018.

2020Medicare Advantage Cost Changes and 2020 Premiums

In September of 2018, CMS announced that on average, Medicare Advantage premiums will decrease by 6%. This is great for beneficiaries interested in affordable vision, dental, and hearing coverage or even fitness classes like SilverSneakers®!

CMS estimated that 83% of beneficiaries would have equal or lower premiums for 2019 and 46% will have a $0 premium! Premiums for MA plans have steadily declined, and this is the lowest premium we’ve seen in three years. This is a perfect example of a private and public collaboration that allows beneficiaries to drive and define the value. The 2019 Medicare Advantage changes are a quick glance of what you can expect to continue in the future.

2020 cost changes for Part A and B premiums and deductibles have not officially been released yet but are not expected to increase by very much. We will continue to monitor this information and will update as soon as the cost changes are officially announced.

Early in 2018, CMS (Centers for Medicare and Medicaid Services) released new rules that allow Medicare Advantage plans to offer a few benefits, like “daily maintenance,” transportation, telehealth, and durable medical equipment.

Some plans in 2020* are really going above and beyond, offering benefits like new air conditioners and pest control!

*These benefits are not included in all MA plans. Your agent may be able to help you find a plan that includes more.

Daily Maintenance

The addition of the “daily maintenance” benefit means that Medicare Advantage plans are now able to offer at-home care items, such as wheelchair ramps and other home modifications. Tied in with that benefit are other forms of durable medical equipment, like hospital beds, oxygen equipment, blood sugar monitors, etc, as well as “non-skilled” services. Non-skilled refers to items that do not require a licensed doctor or nurse, such as aides who can assist with bathing and dressing or homemakers who can help with cleaning and cooking.

Non-Emergency Medical Transportation Coverage

CMS has also added the ability for MA plans to provide non-emergency transportation coverage, a service that several Medicaid plans provide. This benefit (if your plan covers it) will allow you to receive free or low-cost rides to medical appointments and pharmacies. In most cases, you can only qualify for this benefit if you do not have another adequate means of transportation. The appointment that you are requesting a ride to must be for a Medicare-covered service.

Telemedicine and Telehealth

MA plans can now provide coverage for telehealth. That means you can have live video interaction with your doctor through digital clinics like HealthTap, Teladoc, and MDLive. Telehealth can also include health alerts delivered to your phone, health education apps, electronic medical data transfers, mail-order prescriptions, digital appointment scheduling and exam reminders, and more.

New Enrollment Period (OEP)

Before 2019, most people were only able to switch into new Medicare Advantage plans during the Annual Enrollment Period in the fall. Now, if you already have a Medicare Advantage plan, you may be eligible to make a change during OEP. OEP, or the Open Enrollment Period, takes place from January 1 through March 31. During this time, you can switch from one Medicare Advantage plan to another or drop your Medicare Advantage plan in favor of Original Medicare (Part A and Part B only).

Future of Medicare Advantage Plans

According to the Henry J Kaiser Family Foundation, enrollment has tripled to 19 million beneficiaries since 2003 and continues to grow each year. CMS estimates that MA enrollment will hit an all-time high of 22.6 million beneficiaries in 2019 (an 11.5% increase)!

As enrollment continues to increase, plan selection and variety increase too, with approximately 600 new plans offered in 2019! 99% of seniors and Medicare-eligibles have access to a MA plan – and 91% can choose from 10 or more plan options. Beneficiaries will not only see more plans to choose from, but also new supplemental Medicare benefits!

Enroll in a Medicare Advantage Plan in 2020

Are you interested in getting coverage beyond Original Medicare? Along with the new benefits, many Medicare Advantage plans offer dental, hearing, and vision coverage.

Our agents at Medicare Plan Finder can contract with nearly every carrier in your state! This means that you can enroll in the MA plan that best fits your needs and budget.

The Annual Enrollment Period runs from October 15 through December 7. Start looking over your plan benefits now so that you’re ready to enroll before December 7!

Ready to learn more? Call us at 844-431-1832 or fill out this form to arrange a no-cost, no-obligation appointment with an agent in your area.

*This post was originally posted on November 8, 2018, and was last updated on October 4, 2019.

How Medigap is Unique in Minnesota, Wisconsin, and Massachusetts

In most of the United States, Medigap (also called Medicare Supplements) can be characterized by eight different types of plans (A, B, D, G, K, L, M, N). However, there are three states that work completely differently: Massachusetts, Minnesota, and Wisconsin.

A lot of the information you’ll see on the internet about Medicare Supplement plans talks about those eight plans, but we haven’t forgotten about you, Massachusetts, Minnesota, and Wisconsin! If you live in one of those three states, this guide is for you.

Psst…click below to read more about Medicare programs in each state:

If you already have a basic understanding of Medigap, you can skip ahead to the section about your state below.

Medigap is a type of private Medicare insurance that is not technically part of the government-sponsored Medicare program. Medigap plans are also called Medicare Supplements. The two terms can be used interchangeably. To enroll in Medigap, you have to enroll in Original Medicare first.

Additionally, you cannot have a Medicare Supplement plan and a Medicare Advantage plan at the same time. Click here to find out if Medicare Advantage is better for you than Medicare supplements.

What Does Medigap Cover?

Uniquely, Medicare Supplement plans do not typically provide additional health benefits. Instead, Medigap plans provide additional financial protection. For example, let’s say you get sick and have to go to the doctor at least once per month for treatment. Original Medicare may not cover the entire cost for you. You might have to pay your deductible first ($185 for Part B in 2019) and then 20% coinsurance on every visit.

If you have a Medicare Supplement plan that includes deductible and coinsurance coverage, you may not have to pay that $185 and 20%. Instead, you’ll only have to pay your Part B* premium and your Medigap premium.

You may have heard that you cannot be denied Medicare coverage based on your age or preexisting conditions. While that’s true, Medigap is a little different. If you enroll in a Medicare Supplement plan during your Initial Enrollment Period (the time when you first become eligible for Medicare), that holds true. However, if you wait too long to enroll, there is a chance that your plan will be put through underwriting and your prices may increase, or you may be denied coverage based on your age and preexisting conditions.

*Some people may have a Part A premium as well.

Senior couple speaking with a doctor

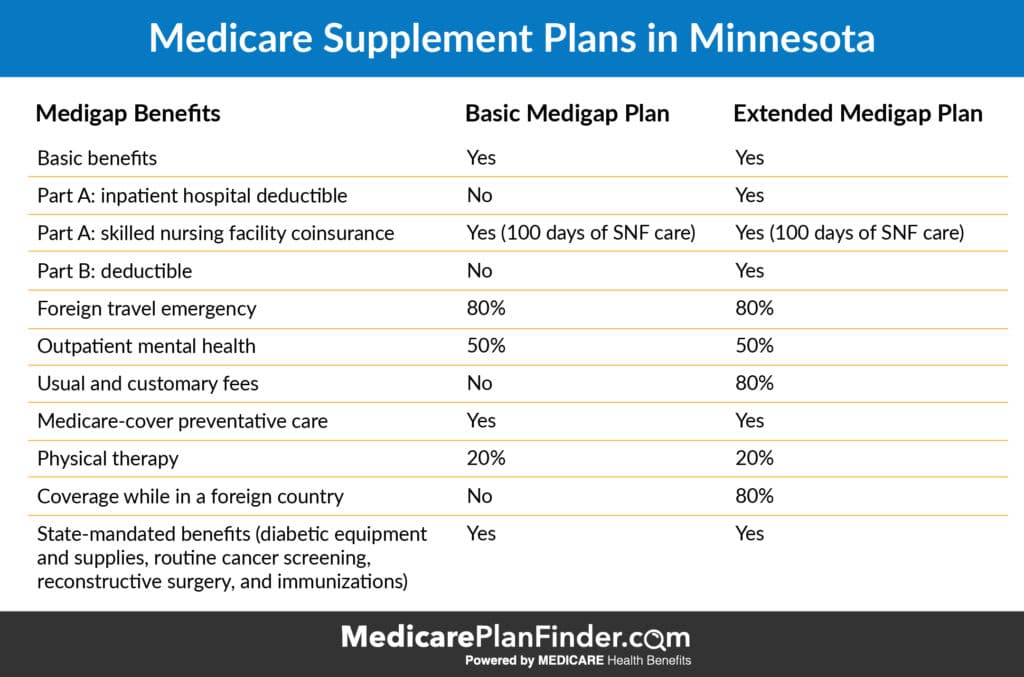

Minnesota Medicare Supplement Plans

While you can’t get the same eight plans (A, B, D, G, K, L, M, N) in Minnesota that are offered in other states, there are technically modified versions of plans K, L, M, and N available.

Additionally, Minnesota offers two unique plans: The “Basic Plan,” and the “Extended Basic Plan.”

The preexisting conditions underwriting may apply. However, you’ll get a 6-month Medigap enrollment period (where age and preexisting conditions do not apply) if you return to work or if you drop Part B in favor of your employer’s health plan.

80% of foreign travel emergency, then 100% after you spend $1,000 per year out-of-pocket

80% of “usual and customary fees,” then 100% after you spend $1,000 per year out-of-pocket

Minnesota Medicare Supplement Plans

So you’re probably wondering, if the Minnesota Medigap Basic Plan and the Extended Basic Plan both always offer the same benefits, why would you choose one Basic Plan over another?

The answer is that costs can vary and plans are allowed to add some extra benefits. There are four additional benefits that plans are permitted to add to the Basic and Extended Basic plans: Part A inpatient deductible, Part B deductible (no longer available in 2020), usual and customary fees, and non-Medicare preventive care.

At least $30,000 for kidney disease treatment (dialysis, transplants, etc.)

Insulin pumps, self-management training, and other diabetes care

50% and 25% cost-sharing plans are also available, which are similar to Medigap Plan K and Medigap Plan L (which would be available in other states).

So, you might be wondering why you have multiple options to choose from for Wisconsin Medigap plans if they are all supposed to be the same “basic” plan. The answer to that is that plans ARE allowed to add additional benefits other than what is in the basic plan, and the costs can vary. Companies are allowed to add the following benefits:

Why Can’t I get Part B Deductible Coverage in 2020?

When MACRA (The Medicare Access and CHIP Reauthorization Act) passed in 2015, a couple of changes were made that didn’t take effect right away; Losing Part B deductible coverage was one of them.

Congress made the decision to not allow plans to cover the Part B deductible starting in 2020. This decision saves money for the Medicare program and doesn’t have an astronomical effect on you. The Part B deductible was only $185 in 2019. All this means is that you will have to pay $185 out-of-pocket before the rest of your coverage kicks in.

It also means that if you are already enrolled in one of the plans listed above that includes the Part B deductible, you won’t lose that coverage. However, if you decide to switch plans or drop that coverage at any time, you won’t be able to get back into it starting in 2020.

How do I Decide Which Medigap Plan is Right For Me?

Regardless of which state you live in, we have a plan finder tool that can help you compare your options.

We also have licensed agents available to answer your questions and help you make your final decision. To find out if there is an agent near you that you can meet with, call 844-431-1832 or send us a message by clicking the “let’s chat” button in the bottom right corner.

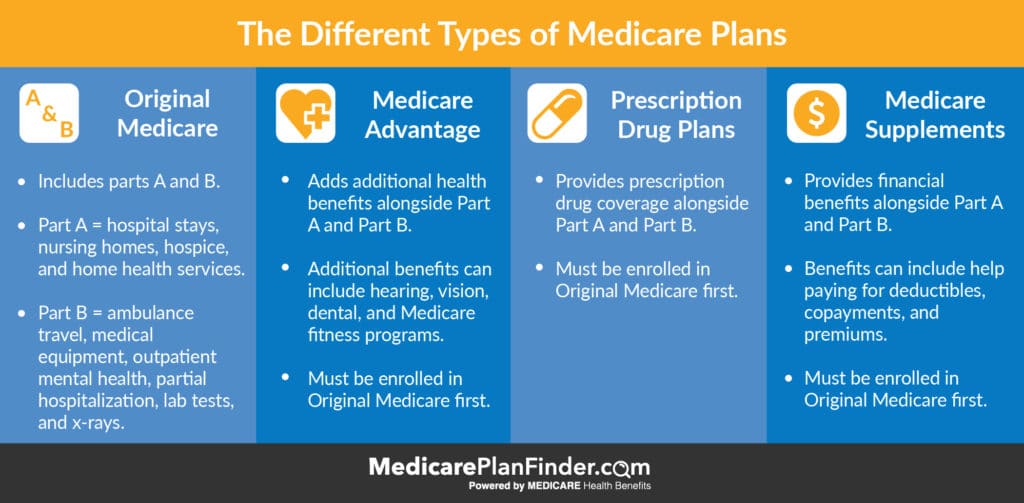

How to Choose the Best Type of Medicare Plan for You

When it’s time to choose a Medicare plan, it’s easy to get overwhelmed. There are quite a few different types of Medicare plans to choose from. Once you choose what type you want – you still have to choose a plan! Making the right choice is important because it may not be easy to change plans if you change your mind.

The Annual Enrollment Period (October 15 through December 7) is when anyone can make changes, and for some people, it’s the only time. If you make the wrong choice, you might have to wait a whole year before you can change again (unless you qualify for the OEP or have a SEP).

Which Types of Medicare Plans are Best for Me?

To figure out which Medicare plan is best for you, ask yourself the following questions:

What specific medical services do I need coverage for (ex: lab tests, blood work, surgery, chemotherapy, dental, etc.)?

How much room do I have in my budget? Am I able to pay a little more to have more benefits?

Would I rather pay more on a monthly basis and pay very little when I visit the doctor, or is it better to pay a small amount every month but risk having higher copayments?

Who are the doctors and other providers who I want to be covered in my plan?

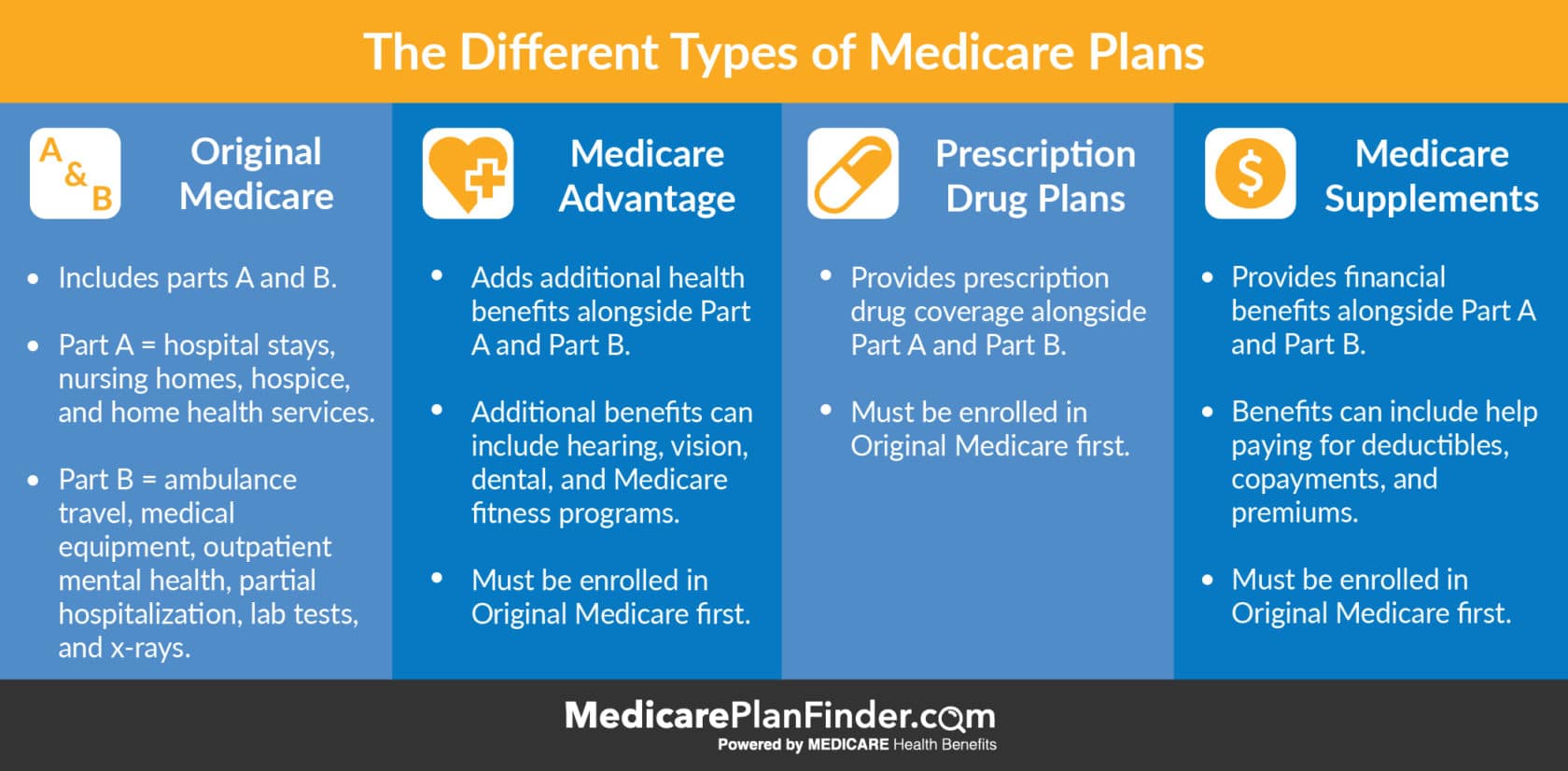

There are four main types of Medicare plans to consider when you begin your Medicare plan search. Start by comparing Original Medicare, Medicare Advantage, Prescription Drug Plans, and Medicare Supplements.

Keep in mind that you cannot have Medicare Advantage and a Prescription Drug Plan at the same time. You also cannot have Medicare Advantage and a Medicare Supplement plan at the same time.

Which plan or combination of plans works best for you?

Medicare Advantage: A private plan that you can purchase once you have Original Medicare. Can add additional benefits such as hearing, vision, dental, fitness, etc. Can include a prescription benefit.

Prescription Drug Plans: Another type of private plan that you can purchase once you have Original Medicare. Usually only includes a prescription benefit.

Medicare Supplements (Medigap): Another type of private plan that you can have in addition to Original Medicare. Adds more financial coverage, like for copayments and deductibles. This type of plan would also require you to have a stand alone part D drug plan.

Different Types of Medicare Plans

Choosing a Medicare Advantage Plan

So, did you decide to go with Medicare Advantage? Great! Now, there are a few types of Medicare Advantage plans that may be available for you. First, ask yourself whether or not you need a large network and whether the freedom to see any doctor is important to you. Then, read through these important differences:

HMO Plans (Health Maintenance Organization) – You’ll select one primary physician. In some cases, you may only receive coverage for that one doctor (unless he or she refers you to a specialist). Requirements may vary based on your plan.

HMO-POS Plans (Point-Of-Service) – You’ll select one primary physician, but you’ll have the freedom to visit any specialist in your network for your other needs. You will be charged a fee for visiting specialists.

PPO Plans (Preferred Provider Organization) – You can see any doctor, but your costs will usually be lower if you choose one that is in your network.

PFFS Plans (Private Fee-For-Service) – You will not need referrals or a primary physician, but you’ll have to pick a doctor that accepts your PFFS plan.

SNP (Special Needs Plans) – Designed for those who are eligible for both Medicare and Medicaid, live in a nursing home, or have a chronic illness or disability.

MSA (Medical Savings Account) – Works like a tax-free savings account for your medical bills. Medicare will deposit money into your HSA. You can use that account to pay for medical expenses.

How do I Pick a Medicare Supplement Plan?

If you’ve decided that you want a Medicare Supplement plan, you’ll want to start by selecting the plan letter that corresponds with the coverage you need. Use the chart below for reference.

Once you’ve made that decision, you may have a few different carriers available in your area to choose from (some smaller cities may not have several options available).

Finding Medicare Plans in your area just got easier. Our Medicare Plan Finder tool can help you not only see what is available, but see which options may be best for your unique needs.

You can enroll by yourself, or you can meet with a licensed agent (for free) who can walk you through the process to make sure you don’t make any mistakes. The licensed agent can also talk to you about a variety of different types of plans in your area and answer all your questions.

This unbiased approach is a great way to get the help you need when selecting a Medicare plan.

To set up your free meeting with a Medicare Plan Finder licensed agent, call 833-567-3163 or click here.

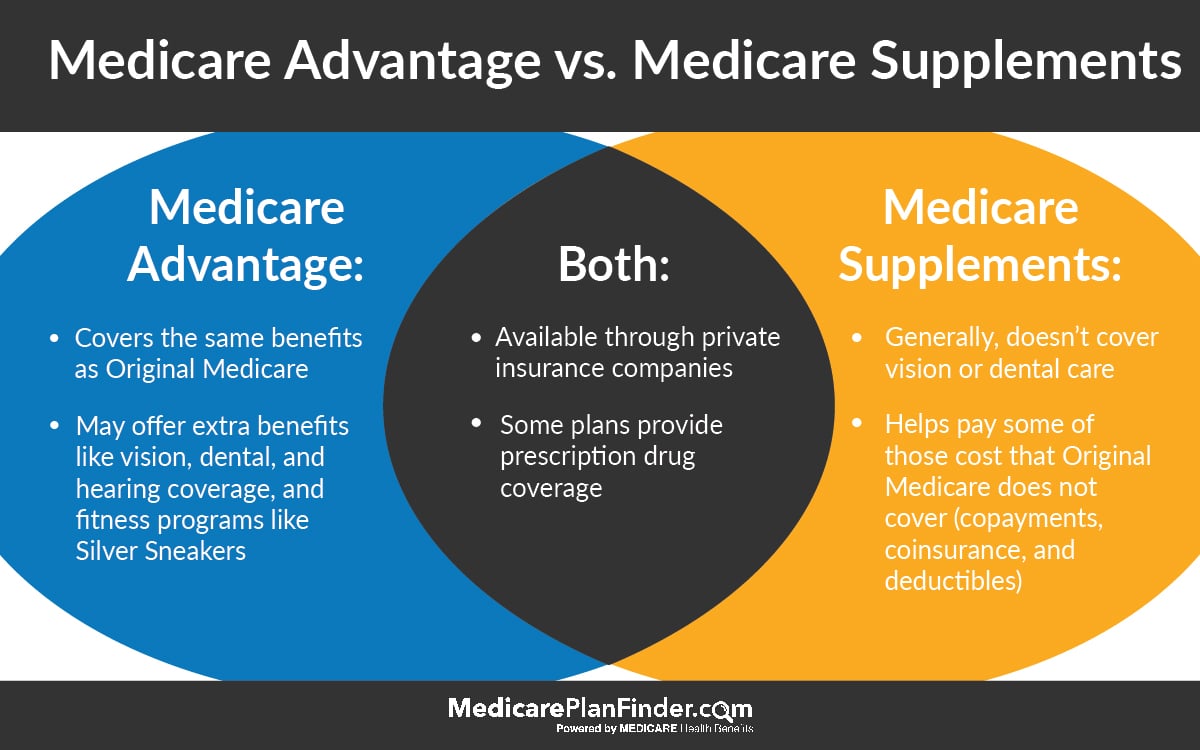

Medicare Advantage vs. Medicare Supplement

Medicare Advantage and Medicare Supplements (also called Medigap) are very different insurance plans with distinct benefits. The answer to the question “is Medicare Advantage better than Medigap?” depends on your circumstances and needs.

What is Medicare Advantage?

Medicare Advantage plans are private plans (not owned by the federal government) that can offer additional health benefits. To have Medicare Advantage, you have to enroll in Original Medicare first. You may have to continue to pay your Medicare Part B premium even if you have Medicare Advantage (MA), but MA premiums can be as little as $0.

Medicare Advantage plans are not all the same, but they can provide benefits like (click on the links to learn more about each one):

There are many different types of Medicare Advantage plans, although not every plan type may be available in your area.

A health maintenance organization (HMO) is a network of health-care providers and facilities where you choose a primary care physician to coordinate your care.

A preferred provider organization (PPO) is also a network of health-care providers and facilities but typically you do not need to select a primary care physician, and you have more flexible options regarding out-of-network care.

A private fee-for-service (PFFS) plan is a mode of benefit delivery where you are not limited to a network. However, there are no guarantees that your doctor or hospital will accept the plan. If you choose to receive your Medicare health coverage through a private Medicare Advantage plan, you must continue paying your Part B premium regardless, because you remain enrolled in Original Medicare (Part A and Part B), even after joining a Part C plan.

What is Medigap?

Medigap is more different from Medicare Advantage than you might think. While Medicare Advantage plans are able to offer health benefits, Medicare Supplement plans (also called Medigap) offer financial benefits. For example, some Medigap plans can cover your Part B premium.

The chart below explains the differences between available Medigap plans in 2020. You can also use our Medicare Plan Finder search tool to compare plans in your area.

2020 Medicare Supplement Comparison Chart

Comparing Medicare Advantage vs. Medicare Supplement plans

Let’s look at Medicare Advantage vs. Medigap. In short, the difference between Medicare Advantage and Medicare Supplement plans is that one can supply health benefits while the other can supply financial coverage.

Medicare Supplement Insurance is a policy that’s added to Original Medicare, Part A and Part B, to provide additional financial coverage. Medicare Advantage is a private plan option that may provide you with other health benefits that Original Medicare does not cover (like dental, vision, fitness programs, etc.).

You cannot have both Medicare Advantage and Medigap at the same time.

Medicare Advantage vs Medicare Supplements | Medicare Plan Finder

A given plan type (e.g., Plan F) has the same benefits regardless of the insurance company that provides the policy, or the state in which you reside. This is not true of Medicare Advantage plans, however, because coverage details may vary by plan.

Excluding prescription drug coverage, any standard Medigap plan with Part A and B will have more benefits than a standard Medicare Advantage plan. However, as mentioned above, some Medicare Advantage plans offer benefits beyond those found in Part A and Part B.

Some Medicare Advantage plans offer prescription drug coverage (often for an additional monthly cost). With a Medigap plan, in contrast, you would need to enroll in a separate prescription drug plan. When comparing plan options, consider your costs for drug coverage. In some cases, Medigap with a stand-alone prescription drug plan has lower total costs than a Medicare Advantage plan with drug coverage. In other cases, the reverse might be true.

[Tweet “Do your research! Comparing #Medicare Advantage vs Medicare Supplement”]

Real-Life Examples: Medicare Advantage vs. Medicare Supplements

Let’s take a look at some real-life examples to help you decide whether Medicare Advantage or Medicare Supplements are right for you.

If you have Medicare Parts A (hospital coverage), B (medical coverage), and D (prescription coverage) and you are hospitalized for cancer treatments for 90 days, you may have out of pocket costs. The Part A deductible means you would pay well over $1,000 first. Once you meet your deductible, your costs will go down. However, after day 60, you’ll be responsible for a portion of every day that you stay there.

If you have Medigap Plan B, your deductible and many of your other hospital costs will be covered. This plan would be in addition to your Part B coverage, so it would all work together to provide extra coverage.

If you have Medicare Advantage, you may have additional health benefits. You’d still likely be responsible for some of those out-of-pocket hospital costs, but your plan might provide a home healthcare benefit, meaning you can get a private in-home nurse when you are released from the hospital. You might also have coverage for medical equipment, such as bathroom safety equipment or a walker.

Comparison is key: Medicare Advantage vs. Medicare Supplements

When choosing between a Medigap plan and a Medicare Advantage plan, take the time to do your research. Read the benefit descriptions of every Medigap and Medicare Advantage plan you are considering. Be certain to look at:

Monthly premium

Deductibles

Doctor and healthcare facility restrictions

Benefits

Anticipated plan costs given your typical use of health-care and hospitalization services

Prescription drug coverage cost sharing as it relates to your medication usage

In the end, your decision is going to be the one that you feel the most comfortable with. The challenge is often wading through all the material to get to the bottom line. Want to make that a little easier? Give us a call at 844-431-1832.

This post was originally published on October 23, 2018, and was last updated on August 29, 2019.

The Ultimate Guide to Medigap Plan D

Medicare Supplements, also known as Medigap plans, add financial benefits that work alongside your Original Medicare. These benefits include help paying your copayments, coinsurance, and deductibles. Enrollment has increased every year since 2010, and there are more than 13 million beneficiaries taking advantage of Medigap plans in 2019.

There are more than ten types of plans (A, B, C, D, F, G, K, L, M, and N), that offer a wide range of coverage at different costs. Many plans are guaranteed renewable life which means you shouldn’t be dropped if a new health condition develops (as long as you pay your monthly premium on time). If you’re looking for financial benefits to supplement your Original Medicare coverage, Medigap Plan D may be the plan for you.

Medicare Supplement Plan D vs. Part D

Medicare Supplement Plan D can be easily confused with Medicare Part D. Medicare Supplement Plan D, is one of the ten types of Medigap plans, while Medicare Part D is prescription drug coverage.

Original Medicare (Part A and Part B) do not cover prescription drugs. Part D was created in 2006 and has since allowed beneficiaries to purchase prescription drug plans alongside Original Medicare to cut down on out-of-pocket drug costs. To learn more about Medicare Part D, click here.

Rx Discount Card | Medicare Plan Finder

Do You Need Medicare Part D If You Have Supplemental Insurance?

You are not required to enroll in a Part D plan whatsoever. However, once you are enrolled in Part A and B, you should consider enrolling in some type of prescription drug coverage to avoid a late-enrollment penalty down the road. Some Medicare Supplement plans cover prescription drug coverage, but this is rare.

You can get prescription drug coverage through some Medicare Advantage plans or a stand-alone Part D plan. You can be enrolled in a Medicare Supplement plan and Part D plan at the same time, however, you cannot be enrolled in a Medicare Supplement and Medicare Advantage plan at the same time.

If you prefer health benefits like dental, vision, or hearing coverage, or even group fitness classes like SilverSneakers®, you may be better suited for a Medicare Advantage plan. Your best bet is to talk with a licensed agent who can explain plan and benefit details that are available in your area. Fill out this form or give us a call at 844-431-1832.

Doctor’s Appointment | Medicare Plan Finder

What Does Medigap Plan D Cover?

Medigap Plan D covers all of the gaps from Original Medicare except for the Part B deductible and Part B excess charges. More specifically, Plan D includes the following:

Part A coinsurance and hospital costs

Part B coinsurance and copayments

Blood work copays up to three pints

Hospice coinsurance and copayments

Skilled nursing facility coinsurance

Part A deductible

Foreign travel emergency

Medigap Plan D Costs

If you enroll in Medigap Plan D, you will be responsible for a monthly premium, your Part B deductible, and any Part B excess charges. The Part B deductible in 2019 is $185. Part B excess charges are up to 15% of what Medicare paid for a product or service. You are only responsible for the excess charges if your doctor does not accept Medicare assignment rates.

Medigap plans generally provide the same coverage no matter who you enroll with, but they have different prices. There is no reason to overpay for a plan when there may be a cheaper plan with identical coverage.

The costs can also vary based on carrier, zip code, age, gender, and tobacco. A licensed agent can show you all of the available plans in your area and make sure you do not overpay. Fill out this form or give us a call at 844-431-1832.

Medicare Supplements | Medicare Plan Finder

Use Our Medigap Plan Finder Tool to Compare Rates

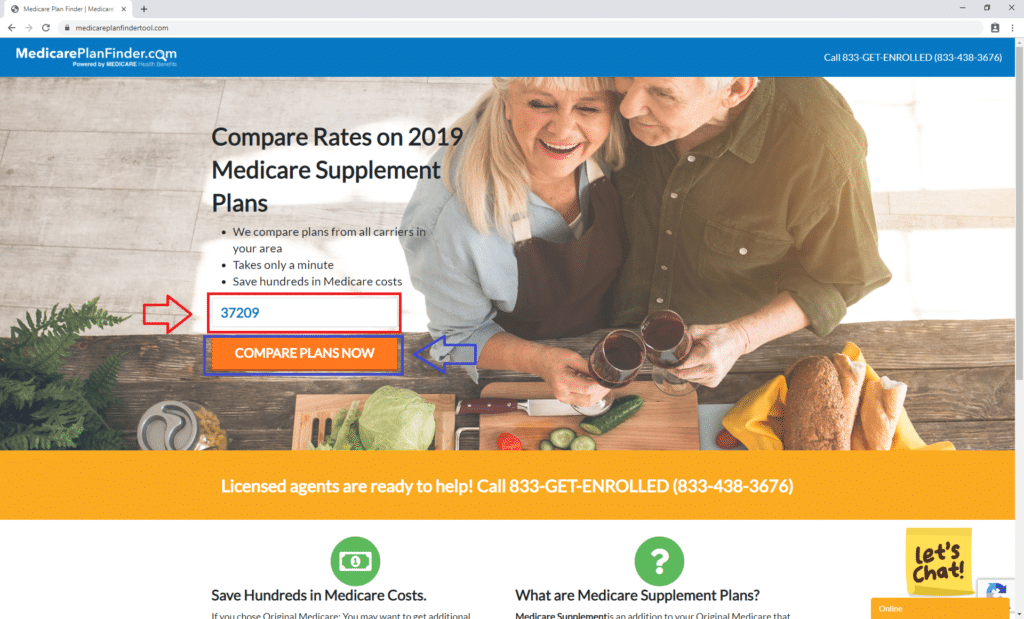

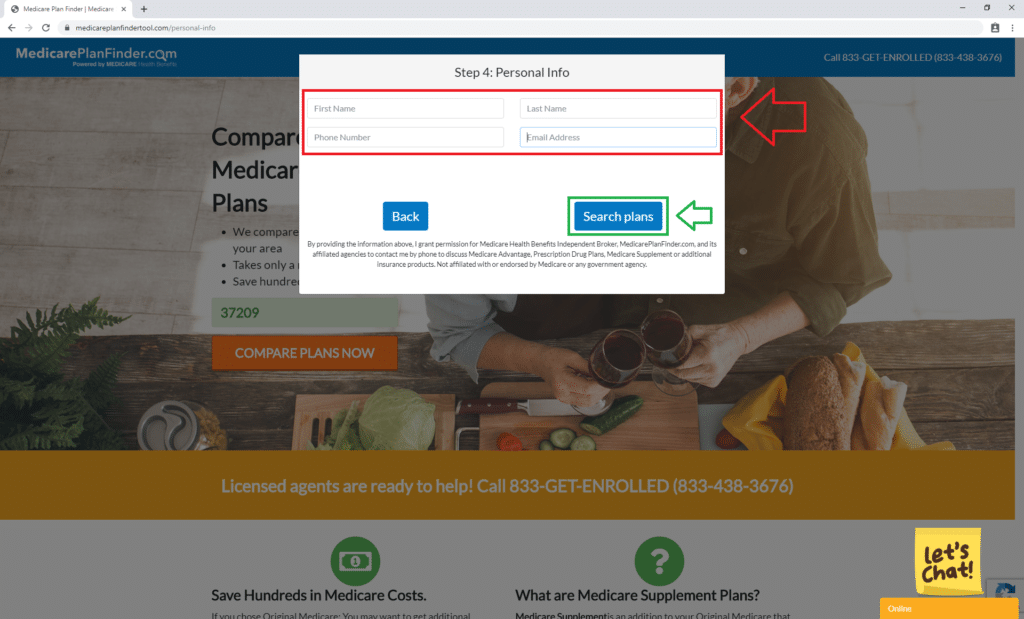

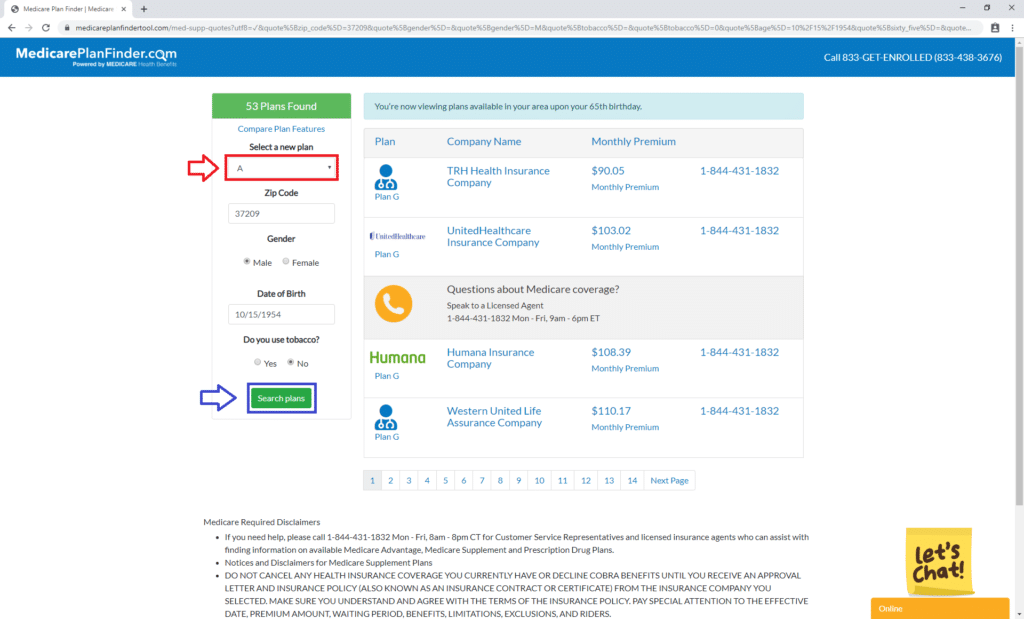

Medicare Plan Finder has a tool to help you find Medicare Supplement Plan D options in your area. To get started, click here. Step one is to enter your zip code so you can find local plans. We used 37209, which is the zip code for our corporate headquarters in Nashville, TN.

Medigap Plan Finder Tool Step 1 | Medicare Plan Finder

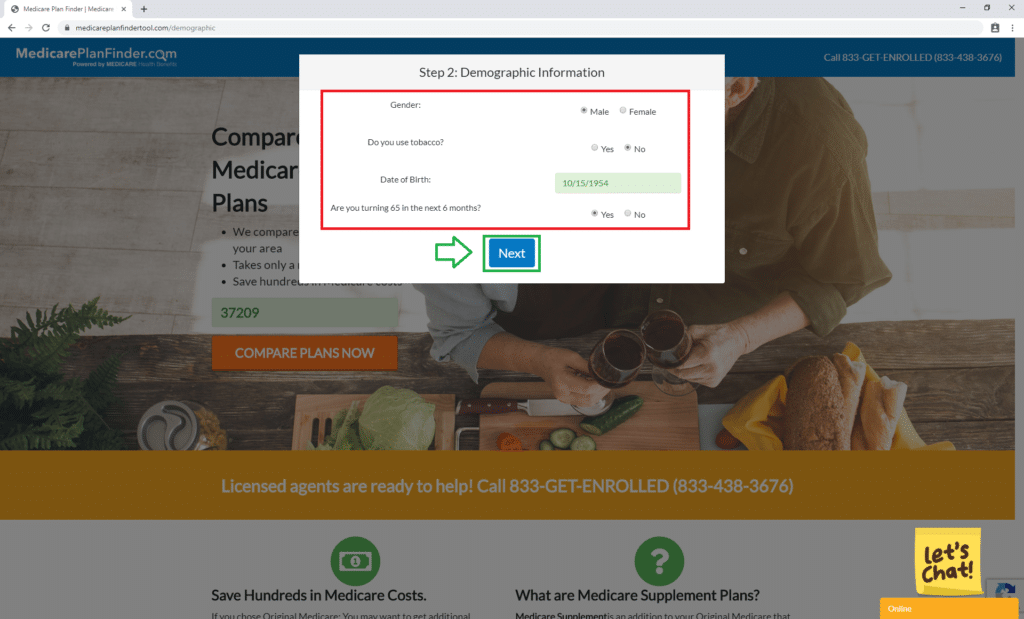

Then answer the questions in the red box. Then click “Next,” in green.

Medigap Plan Finder Tool Step 2 | Medicare Plan Finder

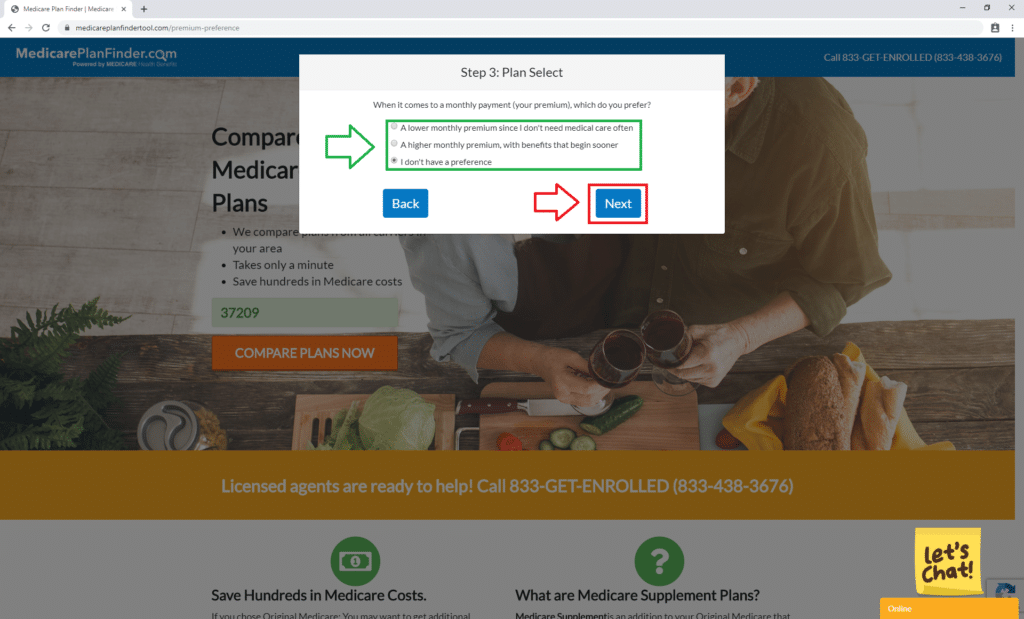

You will then select a plan preference shown in green. We chose “I don’t have a preference,” for demonstration purposes. Then click “Next,” shown in red.

Medigap Plan Finder Tool Step 3 | Medicare Plan Finder

Enter your contact info on the next page in the red box, then click “Search plans,” in green.

Medigap Plan Finder Tool Step 4 | Medicare Plan Finder

You can use the tool to look for any Medicare Supplement plan in your area, but for this blog we’re only going to look for Plan D. To find Medigap Plan D options in your area, use the drop-down menu in red to select “D”.

Medigap Plan Finder Tool Step 5 | Medicare Plan Finder

Plan D Reviews

The top carriers for Medicare Supplement Plan D in 2019 include:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

Enroll in Medigap Plan D

Did you know you can enroll in Medicare Supplement plans year around? However, carriers can charge you more, or even deny you, if you enroll outside of your initial enrollment period.

Our licensed agents can show you which Medicare Supplement plans are available in your area and help you enroll in a plan that fits your needs and budget.

Why wait? Start saving on your out-of-pocket Medicare costs now! Fill out this form or give us a call at 844-431-1832to schedule an appointment with a licensed agent. As always, appointments are cost-free to you, and there is never an obligation to enroll.

Medicare Supplement Plan Finder | Medicare Plan Finder

This post was originally published on May 10, 2019, by Kelsey Davis and updated on August 20, 2019, by Troy Frink.

What is Medigap Plan L?

Medicare Supplement plans (also known as Medigap plans) work alongside Original Medicare to provide financial benefits and protection. More than nine million beneficiaries are enrolled in a Medigap plan, and enrollment increases each year.

There are ten standardized plans broken down by letters (A, B, C, D, F, G, K, L, M, and N). Each letter represents a different range of coverage for a different price. You can have fewer benefits for a smaller monthly premium, or get more benefits for a slightly higher monthly premium.

Most plans are guaranteed renewable for life, meaning as long as you pay your premium on time, you should not be canceled from your plan due to a new health condition. Plans are also generally the same regardless of which carrier you enroll with. If you’re looking for financial benefits to supplement your Part A and B, Medigap Plan L may be perfect for you.

What Does Medigap Plan L Cover?

Medigap Plan L is one of the cheaper options on the market because it doesn’t cover as much as some of the other plan types. Specifically, Plan L covers:

100% of your Part A coinsurance & hospital costs

75% of blood work copays (up to three pints)

75% of hospice coinsurance & copayments

75% of skilled nursing facility insurance

75% of your Part A deductible

75% of your Part B coinsurance & copayments

Other benefits of Medigap plans include coverage for:

Part B deductible

Part B excess charges

Foreign travel emergency

Plan L Costs

Medigap plans (A, B, C, D, F, G, K, L, M, and N) are generally very similar no matter which carrier you buy from. This means that, for example, Plan L from Carrier 1 would offer mostly the same benefits as Plan L from Carrier 2. However, pricing can differ based on carrier, zip code, age, gender, and tobacco use. Our licensed agents can show you all of the available plans in your area and help you enroll in the plan with the best price. Click here or call 844-431-1832 to contact a licensed agent.

Medicare Supplement Eligibility

To be eligible for a Medicare Supplement plan, you need to be enrolled in Original Medicare (Part A and B). Medigap plans are sold through private insurance companies and are not required to sell a plan to beneficiaries under 65. This means if you qualified for Medicare by turning 65, having ESRD (end-stage renal disease) or ALS (Lou Gehrig’s Disease), or through Social Security Disability Income (SSDI), you may not be eligible for a Medigap plan. However, a licensed agent can help you find any available plans in your area that you may qualify for. Click here or call 844-431-1832 to contact a licensed agent.

Plan L Reviews

Some of the top Medigap carriers for 2019 include:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

Popular Medicare Supplements

Some of the most popular Medigap plans are Plan G and Plan F because they offer the most coverage. Plan F is almost identical to G, the only difference is Plan F covers the Part B deductible. However, Plan F is going away, and you must be enrolled in Plan F no later than January 1, 2020, to maintain coverage. Plan G is cheaper than Plan F with almost identical benefits, so many beneficiaries prefer Plan G.

If you would prefer to pay a higher monthly premium, but have more financial protection, Plan G or F may be right for you. Contact a licensed agent to talk about plan specifics. Click here or call 844-431-1832.

Enroll in a Medigap Plan

You can enroll in Medigap Plan L (or any Medicare Supplement plan) any time of the year, but if you wait too long, carriers can charge you more or even deny you coverage based on your health conditions. You should consider enrolling in a Medigap plan during your Initial Enrollment Period (IEP). During your IEP, you should not be denied or charged more for any pre-existing conditions. If your IEP has already passed, that’s okay! A licensed agent can still show you plans in your area and help you enroll in a qualified plan. Click here or call 844-431-1832 to contact a licensed agent.

Guide to Medicare Supplement Plan N

Medicare Supplement plans, also known as Medigap plans, add financial benefits that work alongside Original Medicare. More than nine million beneficiaries are taking advantage of this additional financial protection, and enrollment continues to increase each year.

There are ten different types of Medigap plans, (A, B, C, D, F, G, K, L, M, and N), and each letter represents a different level of coverage. Plans are the same regardless of which carrier you enroll with. This means if you want to enroll in Plan N, the benefits are the same whether you enroll with Aetna, Cigna, etc.

Plus, most plans are guaranteed renewable life, which means you shouldn’t be dropped if a new health condition develops (as long as you pay your monthly premium on time). If you’re looking for financial benefits to supplement your Original Medicare, but don’t want a huge monthly premium, Medicare Supplement Plan N may be right for you.

What is Medicare Plan N?

Medicare Supplement Plan N was introduced in 2010 and has been a popular choice for beneficiaries ever since. Plan N covers:

Part A coinsurance and hospital costs

Part B coinsurance and copayments

Blood work copays up to three pints

Hospice coinsurance and copayments

Skilled nursing facility coinsurance

Part A deductible

Foreign travel emergency

Medicare Supplement Plan N Eligibility

To be eligible for any Medicare Supplement plan, you must be enrolled in Part A and B first. Medicare Supplements are sold through private insurance companies. However, most states are not required to sell Medigap plans to beneficiaries under 65. This means if you qualified for Medicare through ESRD (end-stage renal disease), ALS (Lou Gehrig’s disease), or SSDI (Social Security Disability Income) and are not 65, you can be denied a Medigap plan. To find out if you’re eligible, click here or give us a call at 844-431-1832.

What is the Cost of Medicare Supplement Plan N?

As we mentioned, plan benefits are usually the same from carrier to carrier. However, that doesn’t mean the pricing is the same. Plan N requires some cost sharing in certain situations. There is typically a copayment of up to $20 for doctor appointments and $50 for hospital admittance. Medicare Plan N does not cover the Part B deductible ($185 in 2019) or Part B excess charges. Part B excess charges are up to 15% of what Medicare paid for a product or service. You are only responsible for the excess charges if your doctor does not accept Medicare assignment rates.

The cost of your monthly plan premium will vary based on your zip code, age, gender, and tobacco use. There’s no need to overpay for a plan if there is a cheaper plan available in your area that offers identical benefits. Our licensed agents can show you plans specific to your zip code and can help prevent overpaying. Click here or give us a call at 844-431-1832.

Medicare Supplement Plan N Reviews

If plan benefits are the same across carriers, why are some plans reviewed higher than others? Well, price is a huge factor. Companies with higher customer ratings have plans with higher ratings. Lastly, customer service is an important factor. Here is a list of some of the top Medigap carriers for 2019:

AARP

Aetna

Amerigroup

Cigna

Humana

Mutual of Omaha

WellCare

Medicare Plan N vs Plan G

Medicare Supplement Plan G is another popular Medigap plan. The only benefit that is included in Plan G that Plan N does not cover is the Part B excess charges. However, the thing to remember about excess charges is they are relatively rare. You will only be charged an excess charge if your provider does not accept Medicare. If you would prefer to pay a bit more towards your monthly premium in exchange for coverage on excess charges, Plan G may be perfect for you. One of our licensed agents can help you enroll. Click here or give us a call at 844-431-1832.

Medicare Plan N vs Plan F

Plan F has been a top-selling Medicare Supplement for years. The only difference between Plan F and Plan N is that Plan F covers the Part B deductible and Part B excess charges. Plan F is going away in 2020 (along with Plan C). The Centers for Medicare and Medicaid Services believe that coverage for the Part B deductible results in beneficiaries visiting the doctor too often, costing Medicare millions of dollars. If this benefit is something that is appealing to you, you need to enroll before 2020 to be grandfathered in. Fortunately, one of our licensed agents can help. Click here or give us a call at 844-431-1832.

How do I get Medicare Plan N?

You can enroll in a Medicare Supplement plan any time of the year, but carriers can charge you more or deny coverage if you wait too long. The best time to enroll is during your Initial Enrollment Period. During this time, you can enroll in any plan that is in your area without being denied or charged more for pre-existing conditions. Click here or give us a call at 844-431-1832 to get in contact with a licensed agent.