3 Easy Steps to Making New Friends After Retirement

It’s always tough adjusting to big life changes and, as we get older, those changes seem to come faster and faster. Retiring, moving to a new city, or the death of a spouse can all be overwhelming and foster social withdrawal and isolation.

In fact, a recent survey of retirees showed that 11% of those questioned said they felt lonely and isolated, and almost half of those had recently moved to a new home. The AARP estimates that 42.6 million Americans over age 45 suffer from loneliness, which has been established as a risk factor for early illness and death, especially among seniors.

Fortunately, staying social is easier than ever in our modern age. Read on and learn some awesome methods for making and maintaining new friendships!

1. Follow Your Passions To Find Friends

It’s not easy knowing how to make friends when you are older. Stanford researchers have even suggested that baby boomers are withdrawing from social relationships more than any other group.

But finding new friends doesn’t have to be a guessing game. Just ask yourself a few simple questions: what do you like to do? What are you passionate about? What would you like to learn more about? Finding people with mutual interests and passions is the best place to start forging new friendships.

Social Networking for Seniors

More than ever, technology is helping us form and sustain new friendships. A quick Google search will bring you to senior friendship sites like Silversurfers or Buzz50, which feature forums and chat rooms tailored to older adults.

You can also find countless senior social media groups on platforms like Facebook, which have an increasingly large userbase over the age of 55. Here you can get connected with people online or even find a group that meets in real life. You can look for clubs, classes, or other hobby groups in your area and you’re sure to meet other like-minded social seniors.

2. Getting Out and About

In the social media age, congregating with people who have shared interests can be done from the comfort of your own home. But if you’re feeling cooped up, there are countless ways to meet new senior friends while staying active!

Senior Meetups

A senior meetup is a great place to meet seniors in your area that share your interests or passions. You may find these meetups at churches, gyms, retirement communities, or other places senior citizens hang out. There are even dedicated websites like Meetup.com, which connect you to in-person events based on your location and preferred activity. This helps provide a built-in ice breaker, as you can discuss your common interests.

If you are into photography or arts & crafts, find a workshop at a senior community center where you can advance your skills. If you enjoy cooking but are getting bored of the same old recipes, join a cooking class like the ones offered at Sur La Table. If you’re more of an outdoorsy type, there are groups that go for nature outings. Or you may prefer to find a group that gets together simply to eat, drink, and socialize.

Volunteer Opportunities for Seniors

Another great solution for the social isolation elderly people face is volunteering. This can be a great way to form social connections and do something good for others at the same time.

Organizations like Senior Corps offer programs that allow retirees to mentor young people, be a companion to other seniors who are less mobile, or share their expertise in community projects like building housing.

The AARP also has a program called the AARP Foundation Experience Corps, where those over the age of 50 can tutor young children to help improve their reading comprehension. This mentoring has an impressive impact on the students, improving their literacy skills by up to 60%.

Senior Fitness Classes

Working up a sweat is a tried-and-true strategy for staving off some of the side effects of isolation, such as depression and anxiety. But it can also be a terrific way to meet new people!

Active older adults can join a senior fitness program to help keep an exercise routine and chat with other seniors looking to stay in shape. Many of these programs, like Silversneakers®, may be covered by your insurance. If you have Medicare and are considering purchasing a Medicare Advantage plan to cover fitness programs, click here or give us a call at 844-431-1832 to speak with a licensed agent.

Medicare Advantage | Medicare Plan Finder

3. Get To Know Your New Friends

Once you have made some new acquaintances, it can be difficult to form a closer bond. Plus, as we get older, we usually have less interest in maintaining superficial or casual relationships. Getting organized and keeping to a routine can help tremendously in developing old and new friendships alike.

Keep A Schedule To Stay In Touch

The best way to uphold and develop a relationship is to keep in contact on a regular basis. As your social group grows, start a calendar.

A well-organized calendar can ensure you never miss a meetup or social event that you want to attend. You can also use your calendar to keep track of birthdays and anniversaries. A simple “happy birthday” can go a long way in strengthening a burgeoning friendship.

Just as modern technology can help us meet new people, it can also help us stay in touch with friends and family alike. On social media platforms like Facebook, you can stay engaged with your social groups, old and new, by liking or commenting on statuses and pictures, as well as posting a few of your own! Emails and phone calls can also keep you in the loop with new friends.

Whichever way you choose to find your new social group, remember that forming long-lasting bonds takes time. If a new acquaintance does not respond to your efforts, try not to take it personally. There are plenty more people out there looking for the same connections you are. Keep searching and don’t get discouraged!

The 9 Best Christmas Gifts for Seniors in 2020

Finding Christmas gifts for seniors may seem difficult. You may not know what to get, and you may run into the seniors in your life saying, “I don’t want anything.” That doesn’t make matters easier. We’ve put together a list of fun and useful gifts that the seniors in your life are sure to love.

1. Electric Tea Kettle

Electric tea kettles are easy-to-use and they can come with safety features such as automatic shut-off and cool handles. Automatic shut-off makes it so your favorite senior doesn’t need to remember to turn the kettle off after the water boils — the kettle does that for you. A cool handle means that you don’t have to worry about using hot pads when you’re pouring a cup.

Pro tip: Arthritic hands will do better with a small tea kettle. Large tea kettles are too heavy when they’re full of hot water.

2. Autobiographical Journals

Journals are a great way to preserve memories. With some journals, your loved one doesn’t have to worry about formatting. Some journals have questions that are organized into life sections such as past, present, and family history. The questions serve as a way to jog your loved one’s memory.

A journal is also a gift for you because you get to learn about your loved one’s experiences if they choose to share.

3. Book of the Month Subscriptions

This is the perfect gift for bookworms. With subscription services like bookofthemonth.com, your loved one gets to choose what books they want to read, and how often they want to receive new reading material.

When you log onto the website, you can browse the books of the month, which are separated by genre. The best part? You don’t have to ask a bookstore employee or browse online reviews for recommendations. The subscription service puts it all together and gives a synopsis of each title.

4. Smart Speakers

A smart speaker is a voice-activated device that can play music, answer questions, and give recipes. Many smart speakers such as the Amazon Echo, Apple HomePod, and Sonos One are easy-to-use and your loved one may enjoy the added sense of security that a smart speaker can bring. You can also use many smart speakers to make emergency calls.

5. Phone Case

According to PEW Research, 42 percent of seniors 65 and older have smartphones, and it makes sense. Smartphones are a great way to communicate with your friends and family, navigate to new locations, and take pictures & videos of grandchildren.

With all of the great features smartphones have, you’ll probably want to keep it in good shape. It can be extremely expensive to replace damaged parts if you drop your phone. For example, it can cost $279 to replace an iPhone 11 screen. A durable, protective case can help protect your loved one’s phone from damage. Look for a case with your loved one’s favorite pattern (camouflage, hound’s tooth, etc.) or their favorite sports team for a personalized touch.

6. Supplies for Your Loved One’s Favorite Hobby

Whether your loved one loves gardening, painting, or yoga, you can find supplies so they can keep up with their favorite activities. If your loved one enjoys spending time in the garden, look for gardening tool kits with trowels, spades, and clippers in a sturdy carrying case. See if you can locate brushes and paints for the artist in your life or a yoga mat for your favorite senior yogi.

An e-reader is a device that allows you to have an entire library of reading material in one spot. When you give your loved one an e-reader, you give them the opportunity to subscribe to their favorite periodicals and purchase new books from the comfort of their home.

Some seniors will want more features than e-readers provide such as browsing the internet, playing games, and watching videos. Those people will be better off with a tablet like an iPad. You can still purchase and store books and periodicals with a tablet, but you also get additional features.

8. Jigsaw Puzzles & Puzzle Books

Puzzles are a great hobby for seniors, especially for those who live alone. Not only are puzzle books and jigsaw puzzles a great way to pass the time, but mental games like sudoku and crossword puzzles can help delay the onset of dementia symptoms.

Your loved one may enjoy the challenge of completing a daily puzzle from a book or they might want to frame their favorite 1000-piece jigsaw puzzle. You can even buy a custom photo puzzle with pictures of their grandkids or pets!

9. Great Experiences

Your favorite senior may have every material thing they could ever want or need. If that’s the case, get them tickets to a show, a sporting event, or a gift certificate to their favorite restaurant.

Alternatively, you can book a spa day so your loved one can relax. Some spas even offer geriatric massages! If you live close, go to the event with your loved one. Quality time can be worth much more than the price of admission.

The Best Christmas Gifts for Seniors Come From the Heart

Sometimes it really is the thought behind a gift that means the most. Your loved one will appreciate the time and effort you spent making sure that their Christmas is special. Check out our blog for more holiday health tips including healthy recipes and meal tips.

What to Do After the AEP for Medicare Ends

The Medicare Annual Enrollment Period (AEP) is a time when many Medicare beneficiaries can change their plans so their coverage best fits their needs.

If you are enrolled in Medicare, you will receive an annual notice of change (ANOC) which explains the changes coming to your current plan for the following year. After reviewing your ANOC, you may decide you need to switch to a new plan.

The AEP for Medicare lasts from October 15th to December 7th, but once it’s over and you’ve enrolled in a new plan, you may wonder what to do next.

You may wonder if you forgot something important or how you can take advantage of your plan’s new benefits. Here’s what to do after the Medicare AEP ends:

Review Your Medicare Advantage Plan

If you enrolled in a Medicare Advantage (MA) plan and you decide that it doesn’t fit your needs, you can switch to a different Medicare Advantage plan from January 1st to March 31st the following year. This time period is called the Medicare Advantage Open Enrollment Period (OEP).

For example, if you enroll in a Medicare Advantage plan and it turns out that your doctor doesn’t take your new insurance, you may be able to enroll in a new policy that your doctor accepts.* Talk to your agent about what plan options your doctor accepts and see if one of them can work for you.

Be sure to review a new plan’s deductibles, copays, and/or coinsurance. Your agent can help you determine your out-of-pocket costs and what your out-of-pocket maximum will be.

If you decide that Medicare Advantage (or Part C) isn’t for you, you can drop MA and return to Original Medicare (Medicare Part A and Part B) during the OEP. You can also enroll in a Medicare Part D (Prescription Drug) plan and/or a Medicare Supplement (Medigap) plan.

*Medicare Advantage plans are different in every location. We cannot guarantee that your doctor will accept any plans in your area.

Take a Look at Your Medicare Part D Prescription Drug Costs

Original Medicare does not cover most prescription drugs. If you needed Medicare prescription drug coverage during the annual election period for Medicare, you may have either signed up for a Medicare Part D prescription drug plan or a Medicare Advantage plan with prescription coverage.

Some Medicare Advantage plans even cover over-the-counter drugs! Neither Original Medicare nor Medicare Part D cover over-the-counter items. Your agent can help you determine what type of Medicare prescription coverage will work best for you.

Watch your drug costs and make sure that your plan is covering your medications properly. If your insurance company no longer covers one of your prescription drugs, talk to your agent. They can help you file an appeal.

Talk to your doctor before you file an appeal. Find out if there are alternatives that are on your plan’s formulary or if there are any less expensive drugs you can take.

You should also get a written explanation (coverage determination) from your prescription drug plan (PDP). The coverage determination document will go over whether a certain drug is covered, the qualifications to get a certain drug, your costs, and if the plan will make an exception to the coverage rules.

You should ask for an exception from your PDP if:

Your doctor prescribes a drug that’s not on your plan’s formulary

Your healthcare provider prescribes a drug that’s on your plan’s formulary, but you think you should pay less because no lower-tier drugs work for you

Your PDP will send you a letter with the coverage decision. You can file an appeal with Medicare if you disagree with the decision.

The appeals process has five different levels:

1. Redetermination from your plan: In this level, your plan re-evaluates your request for an exception.

2. Independent Review Entity (IRE) review: This is when a third party reviews your request for an exception, which you can request if your plan denies coverage after the redetermination.

3. Office of Medicare Hearings and Appeals (OMHA) decision: You can file an appeal with OMHA if you disagree with the IRE’s decision.

4. Medicare Appeals Council review: If OMHA doesn’t make a timely decision or you disagree with it, you can file an appeal with the Medicare Appeals Council.

5. Federal district court judicial review: This level is reserved for cases that meet a minimum dollar amount. You should get instructions on how to file an appeal in federal court with your Medicare Appeals Council letter.

Evaluate Your Medicare Supplement Plan

The AEP for Medicare is one of the only times of year most people can enroll in a Medicare Advantage plan.* During AEP, schedule a meeting with your agent to talk about your needs. You may determine that a Medigap plan provides all the coverage you need at a price you can afford, or you may determine that a Medicare Advantage plan is a better fit (Reminder: Medigap plans cover Original Medicare costs such as Part B copayments).

Medicare Advantage plans cover additional benefits that can include fitness classes, hearing, dental, and vision coverage. Your monthly premium may be lower with a MA plan, but your provider network may be smaller.

You must choose a Medigap plan or a Medicare Advantage plan. You cannot have both at the same time.

Use the Open Enrollment Period that starts on January 1 if you need to cancel your Medicare Advantage coverage and you want to return to your Medicare Supplement plan. For example, let’s say your doctor accepts Original Medicare, but they don’t accept any Medicare Advantage plans in your area.

You may want to enroll in a Medicare Supplement plan if you want coverage for copays and coinsurance. You may be responsible for paying Original Medicare coinsurance if you don’t have a Medigap plan that covers it.

Medigap plans cover different items than Medicare Advantage plans. While MA plans cover additional health benefits, Medicare Supplements cover financial items such as coinsurance and copays.

You can enroll in a Medicare Supplement plan at any time of year, so the time after AEP is a great time to learn about Medigap. Remember — most people can drop Medicare Advantage coverage only during AEP and OEP. You can only get a Medicare Supplement plan if you don’t already have a Medicare Advantage plan.

*Not all plans will be available in your service area or make sense for you.

Meet With Your Agent to Discuss Ancillary Products

Many health insurance agents also sell ancillary products such as life and final expense insurance. The beginning of the year is a great time to contact your agent because they might have more time for you than during the busy AEP for Medicare.

Schedule an appointment to talk about your retirement plan and how you can help your loved ones after you pass away. Write down a list of your long-term goals, financial risks, and plans for your 401(k) or other retirement accounts. The beginning of the year is a great time to create a solid plan for your financial future.

Let Us Help During OEP and Every Other Time of Year

If you have questions about your Medicare coverage, one of our highly-trained, licensed agents can help. An agent may be able to help you find a plan in your area that suits your budget and lifestyle needs. Whether it’s AEP or you’re enrolling in Medicare for the first time, let us help. Call 1-844-431-1832 or contact us here to arrange a no-cost, no-obligation appointment today.

Medicare Plan F Going Away (and Plan C) | ENROLL NOW!

What’s all this talk about “Medicare Plan F?” Is Plan F going away?

It’s true – Medicare Supplement Plan F is GOING AWAY in 2020! If you still want Plan F, you only have until December 31, 2019, to get locked in.

When you enroll in Original Medicare (Part A and Part B), you have the option of increasing coverage by purchasing a Medicare Supplement plan (also called Medigap). These plans work alongside Original Medicare and add financial benefits (like help paying for your copayments, coinsurance, and yearly deductibles).

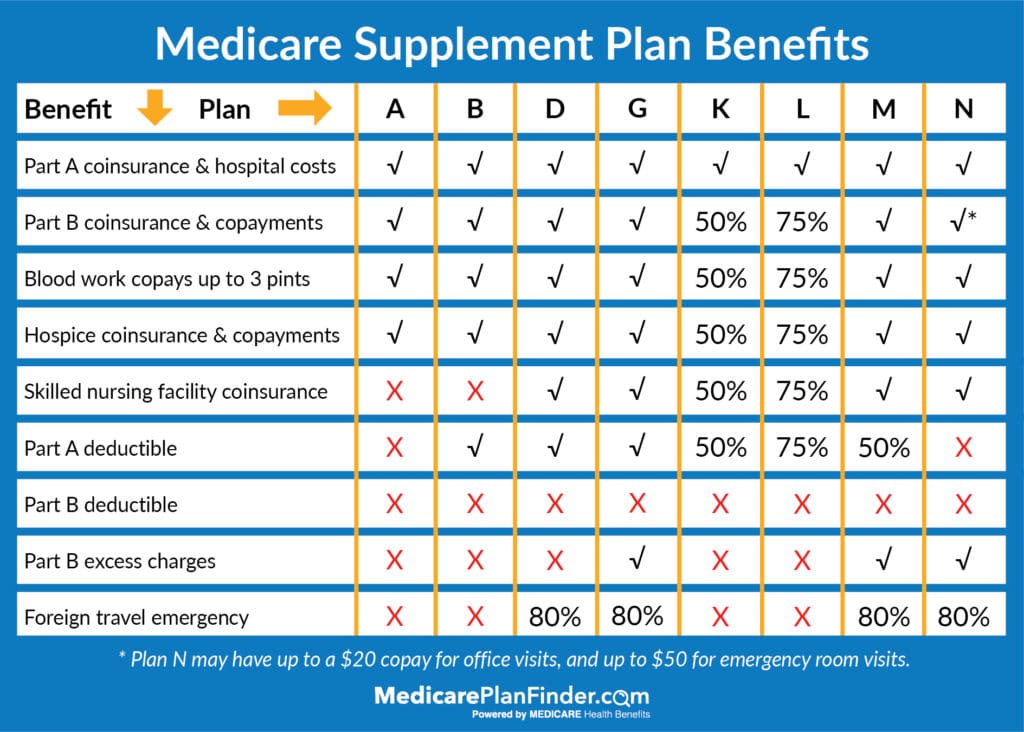

Every state (except Massachusetts, Minnesota, and Wisconsin) has ten different types of plans. Each plan is represented by a different letter (A, B, C, D, F, G, K, L, M, and N). Plan F and Plan C are the most inclusive, and in turn, are the most popular. But did you know both plans are going away in 2020?

Plan F has been a top-seller in many states for years and is the most comprehensive Medigap plan. Medicare Plan F covers:

Blood work copays up to three pints (100%)

Foreign travel emergency (80%)

Hospice coinsurance and copayments (100%)

Part A coinsurance and hospital costs (100%)

Part A deductible (100%)

Part B coinsurance and copayments (100%)

Part B deductible (100%)

Part B excess charges (100%)

Skilled nursing facility coinsurance (100%)

Medicare Plan C Benefits

Medicare Plan C covers all of the gaps from Original Medicare except for Part B excess charges. More specifically, Plan C includes the following:

Blood work copays up to three pints (100%)

Foreign travel emergency (80%)

Hospice coinsurance and copayments (100%)

Part A coinsurance and hospital costs (100%)

Part A deductible (100%)

Part B coinsurance and copayments (100%)

Part B deductible (100%)

Skilled nursing facility coinsurance (100%)

Plan F vs Plan C

Plan F is very similar to Plan C. The only difference is that Plan C does not cover Medicare excess charges. If a doctor does not accept Medicare assignment rates, you will be responsible for excess charges, but it can not exceed 15% of what Medicare pays. Some states do not allow doctors to issue excess charges. If this is the case, Plan C will operate identically to Plan F.

Back in 2015, Congress passed the Medicare Access and CHIP Reauthorization Act. According to the act, starting on January 1, 2020, Medicare Supplement plans can no longer cover the Part B deductible, something that only Medigap Plans F and C currently cover.

When people don’t have to pay a deductible for services, they can end up overusing the doctor. For example, the might schedule an appointment with their doctor for a flu shot instead of using the free clinic inside their local grocery store. By visiting the doctor unnecessarily (and not paying for it), doctor’s offices are getting crowded and doctors aren’t being fully compensated for their time.

Eliminating Part B deductible coverage through Medigap works better financially for the Medicare program and for the doctors who accept it.

Thankfully, that Part B deductible is a small price to pay at less than $200 per year.

When will Medicare Plan F be discontinued? What about Plan C?

If you currently have Medicare Supplement Plan F or Plan C, don’t fret! This policy change only affects new beneficiaries. While your rates may increase (as they technically do every year), you will not lose your current coverage. However, if you leave your Medigap Plan F or Plan C for whatever reason, you will not be able to go back to it after 2020. If you do not have Plan F or Plan C, but you would like to, you can lock yourself in by enrolling NOW. You must enroll before January 1, 2020, to receive Plan F or Plan C coverage.

Due to this change, Plan F and Plan C beneficiaries will be given a chance to compare rates and switch to a new policy. If you decide you may want to switch, you can start by using our Medicare Plan Finder tool to decide what plan option (other than F) is best for you. If you still need help, click here to request a call from a local and licensed agent!

Will Plan F Costs Go Up in 2020?

It is certainly possible that Plan F costs will go up as it is phased out, though it hasn’t been confirmed yet.

Uniquely, the state of Idaho released a memo stating that the Idaho Department of Insurance “is NOT anticipating abnormally large premium increases on Plan F after 2020” in response to questions about Plan F leaving the market. Even people who already have Plan F in Idaho and want to switch to a different Plan F after this year should not face large rate increases.

Can I Get Plan F in 2020?

Medicare Plan F is discontinued in 2020. If you missed the deadline of December 31, 2019, you won’t be able to enroll in Plan F for the first time. If you already have Plan F, don’t worry – you can keep your coverage.

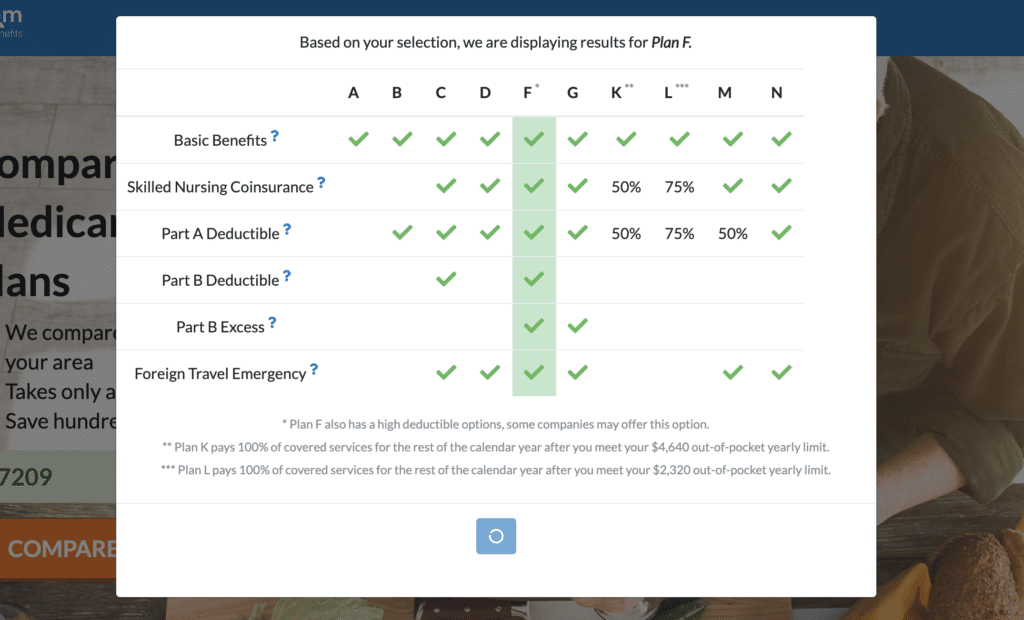

You’ll be asked to enter your zip code to get started. Then, you’ll have to answer a few questions: your gender, your date of birth, whether or not you smoke, and what kind of premium you want. After submitting some basic information, you’ll see a list of the plans that the tool recommends for you.

The system may or may not recommend Plan F based on the way you answered the questions.

Medicare Plan Finder Tool Results

When to Enroll in Plan F

If you still want Medigap Plan F, you have just a little bit of time left to enroll. The deadline is December 31, 2019. After then, Plan F will be discontinued for new members.

What is a good alternative to Plan F?

Many seniors and Medicare eligibles who already have Plan F are deciding to drop Plan F altogether and switch to Plan G. Plan G covers everything that Plan F does minus the Part B deductible, and it typically has a lower monthly premium.

Another popular plan is Plan N. The only benefit that is included in Plan G and not Plan N is the coverage for Part B excess charges. However, the thing to remember about excess charges is they are relatively rare. You will only be charged an excess charge if your provider does not accept Medicare.

Medicare Plan F vs Plan G

Great news! Plan G is almost identical to Plan F! The only difference is that Plan G does not cover the Part B deductible. Plan F may technically cover more, but many people consider Plan G to be a better value. Yes, you will need to pay your Part B deductible upon your first outpatient visit, but after you pay the deductible, you won’t need to pull your wallet out for the remainder of the year. Since you have to pay the Part B deductible yourself, Plan G has lower monthly premiums, and you could save more than $400 a year!

The standard Part B deductible for 2020 is $198, so the savings from choosing G over F significantly outweighs the cost of the deductible.

Is Medicare going away or just certain plans?

No, Medicare is not going away! Don’t panic!

Both Medicare Plan F and Medicare Plan C will be discontinued on January 1, 2020, but other options may be available in your area. We get it, Medicare coverage and plan options can be confusing and stressful. Policies are constantly changing, and healthcare will continue to evolve.

At Medicare Plan Finder, our agents are kept up to date on all the plans in your area and can help you find a plan that suits your needs and budget. If you’re interested in arranging a no-cost, no-obligation appointment, click here or give us a call at 833-431-1832.

This blog was originally published on October 23, 2018, by Kelsey Davis. The latest update was updated on December 5, 2019, by Troy Frink.

Medicare Transportation Solutions

As ridesharing services like Uber and Lyft grow in popularity, more and more Medicare Advantage plans are including transportation services as a benefit. In 2018, CMS (Centers for Medicare and Medicaid Services) announced that in 2019, Medicare Advantage plans will have more freedom to provide coverage for services such as food delivery and transportation.

Does Medicare cover transportation for medical services?

Medicare Part B may cover emergency ambulance transportation to a hospital or skilled nursing facility if transporting in a different vehicle would put your health at risk. Medicare may cover non-emergency transportation in an ambulance if you have a written doctor’s note explaining why an ambulance is medically necessary.

Medicare generally covers up to 80% of the transportation associated costs, but you are responsible for the remaining 20%. If you don’t want to pay for these out-of-pocket costs, a Medicare Supplement plan can help you get full coverage.

Sometimes, Medicare Advantage plans cover non-emergency transportation through third-party vendors. As long as the vendor works with your health plan, you may be able to receive rides to and from doctor’s appointments, pharmacies, and hospitals.

Medicare Transportation | Medicare Plan Finder

Medicare Transportation Services

Ground medical Transportation services can cost hundreds or even thousands of dollars (depending on distance), and air medical transportation can cost well over $10,000.

In an emergency, you should always call 911. If you’re not in an emergency, you can shop around and compare prices with different ambulance and medical transportation services in your area.

Medicare Transportation | Medicare Plan Finder

Medicare Transportation By State:

While there are a handful of national players, there are several local medical transportation companies in each state.

Medicare Transportation Arizona

The most popular private transportation services in Arizona include:

ABC Ambulance

Arizona Ambulance Transport

ABC Ambulance covers the greater Phoenix region. They provide rapid response times alongside basic patient transportation services.

Arizona Ambulance Transport transports patients from the Southeastern Arizona Medical Center to Bisbee, Sierra Vista, and Tucson.

Medicare Transportation Kentucky, Indiana, and Ohio

The most popular private transportation services in Kentucky, Indiana, and Ohio include:

Yellow Ambulance (KY, IN)

MTS Ambulance Services (KY, IN, and OH)

Rural/Metro Corporation (20 states)

Heartland Ambulance Service (IN)

TransCare (IN)

Yellow Ambulance is the preferred transportation provider for Louisville and Bullitt County in Kentucky and Floyd and Marion County in Indiana. They provide basic and advanced life support, specialty care transport (dialysis, ventilator, chemotherapy), long-distance transportation, and bariatric transport.

MTS has 24-hour paramedic crews and offers emergency and non-emergency transportation. This includes rides to hospitals, dialysis treatments, and cancer treatments. They also offer wheelchair van service in KY, IN, and OH.

Rural/Metro is a semi-national company that provides emergency and non-emergency transportation. They also have a community fire protection program and offer personal emergency response systems.

Heartland Ambulance Service offers emergency transportation, basic and advanced life support, and a fixed wing air ambulance. They are available in several central Indiana locations.

TransCare serves Terre Haute, Indianapolis, Vincennes, and Columbus. They offer transportation to and from hospitals, dialysis treatments, doctor appointments, and radiation therapy.

Medicare Transportation | Medicare Plan Finder

Medicare Transportation Louisiana

The most popular private transportation services in Louisiana include:

Acadian Ambulance Service (LA, MS, TX, and TN)

A-Med Ambulance Service

Acadian serves 70 counties/parishes in Louisiana, Texas, Mississippi, and Tennessee. Their largest state is Louisiana. They offer emergency transportation, air services, non-emergency transportation, and bariatric transport.

A-Med serves the greater New Orleans region including Metairie, New Orleans, Kenner, Jefferson Parish, Orleans Parish, Saint Bernard Parish, and Plaquemines Parish. They offer medical transportation to hospitals, nursing homes, and critical care facilities. They also offer wheelchair van transportation.

Medicare Transportation Northeast

The most popular private transportation services in the Northeast include:

Citywide Ambulance (NY)

Lifeline Ambulance (NY)

Northeast Community Ambulance (PA)

Citywide Ambulance provides basic and advanced life support, bariatric transports, airport transfers, long-distance transport, and luxury transportation options. They serve the greater New York area.

Lifeline provides basic and advanced life support and transportation to and from nursing homes, rehab hospitals, dialysis, radiation, assisted living centers, and retirement centers.

Northeast Community Alliance provides 24/7 emergency transportation. Plus, they offer non-emergency transportation to and from doctor’s appointments, dialysis treatments, and hospital discharges.

Medicare Transportation Northwest

The most popular private transportation services in the Northwest include:

Olympic Ambulance (WA)

Northwest Ambulance Transport (WA)

Tri-Med Ambulance (WA)

Olympic Ambulance offers 911 response, basic and advanced life support, and bariatric transports. They also provide wheelchair van transportation to those who need it.

Northwest Ambulance Transport provides advanced and basic life support in a mobile hospital setting. They also provide standby coverage for several cities in the area.

Tri-Med Ambulance offers ambulance services and critical care transport. They also provide wheelchair accessible transportation for medical treatments or doctor visits.

Contact Us | Medicare Plan Finder

Medicare Transportation Tennessee

The most popular private transportation services in Tennessee include:

Lifeguard Ambulance Service (IL, TN, OK, TX, AL, GA, SC, and FL)

BlueShield EMS

American Medical Response

Lifeguard serves several states and provides EMS solutions to rural and urban locations. They offer emergency and non-emergency transportation, health system partnerships, and mobile integrated healthcare.

BlueShield EMS provides ambulatory cars, wheelchair vans, stretcher vans, and ambulances for basic and advanced life support.

American Medical Response provides basic and advanced life support, ventilators, and bariatric transportation services to the greater Nashville and Davidson County area.

The most popular private transportation services in Texas include:

City Ambulance Service

First Medical Response of Texas

BestCare

City Ambulance Service serves the entire states of Texas. They provide basic and advanced life support, and wheelchair, dialysis, and chemotherapy transportation.

First Medical Response of Texas provides a mobile intensive care unit providing advanced life support. They also provide EMT basics, bike medical teams, and medical gators.

BestCare offers non-emergency, emergency, and critical care medical transportation. They also offer air ambulance, wheelchair service, dialysis transports, and long-distance transfers.

How to Use Medicare TransportationServices

Medicare transportation can be used for emergencies and non-emergencies. This can help ensure transportation to and from providers, doctor offices, pharmacies, therapy, critical care units, nursing homes, assisted living facilities, etc.

Medicare Transportation | Medicare Plan Finder

Medicare Transportation to Doctor’s Appointments

Medicare Advantage plans can help cover the costs of utilizing private transportation companies like the ones above. You can request a ride just before you need to leave your home, or you can schedule a pick-up in advance.

Medicare Transportation to Dialysis

If you have End-Stage Renal Disease (ESRD) and require dialysis, Medicare may cover non-emergency transportation to and from a dialysis facility. However, they will only cover the closest facility.

If you choose to be transported to a facility further away, Medicare will not cover it. If there are no facilities within your local area, Medicare will pay for the nearest facility outside of your area.

Ambulance Transportation

Medicare Part B covers ambulance services, but only when necessary. For example, if you are bleeding heavily, unconscious, or need immediate treatment and can’t wait until you get to the hospital, Part B can cover your ambulance transportation. This is only covered if the ambulance is taking you to the nearest facility – you can’t make a special request.

Air ambulance transportation may be covered if your location can’t be reached easily by ground or if obstacles like heavy traffic can stop you from getting the care you need in a timely fashion.

Non-Emergency Medical Transportation

If you need a ride to a doctor’s appointment or a hospital that does not warrant an ambulance, you may have options.

You may want to start by calling your local Office on Aging. They may have a program in place to help you out regardless of your healthcare plan. Some Medicare allow transportation benefits through Uber, Lyft, and other ridesharing services.

These plans will require that you have a specific need for transportation, and you would only be able to use your coverage for healthcare-related transportation. This can include rides to doctor’s appointments, pharmacies, and other healthcare providers.

TheFuture of Medicare Transportation

Ride-sharing companies have grown significantly in recent years. Uber and Lyft have dominated the industry. There are 75 million Uber users and 23 million Lyft users. Medicare Advantage plans are capitalizing on this market and providing new benefits to MA enrollees.

Medicare and Lyft

Medicare Transportation | Medicare Plan Finder

Some carriers are quickly forming partnerships with Lyft to provide enrollees transportation to and from Walgreens and CVS pharmacies. They have plans to create a “no-cost” service that provides insured transportation to and from health appointments.

This is not intended to be a replacement for emergency transportation, but an extra alternative for non-emergency situations. Lyft Concierge is a website that allows you to schedule or book a ride from a computer alongside your plan’s coverage.

Medicare and Uber

Medicare Transportation | Medicare Plan Finder

Uber has plans to partner with several organizations nationwide. They will provide transportation to patients traveling to and from their medical appointments.

Uber will allow parents, caregivers, and medical staff to schedule transportation on your behalf. Plus, Uber has created “Uber Health” which is a HIPAA-compliant and cost-effective way for you to book rides with your plan’s coverage.

Medicare and Roundtrip

Roundtrip, a digital NEMT marketplace for the betterment of health, is offering transportation as a benefit for 2020 Medicare plans. Roundtrip works with hospitals, health systems, paratransit, and health plans nationally to remove transportation as a barrier to health and wellness.

With Roundtrip, members can efficiently book all levels of transport: rideshare, Medical Sedans, Wheelchair Van, and Non-Emergency Ambulances (BLS, ALS, SCT, Bariatric Ambulance with our easy-to-use platform. The Roundtrip software is HIPAA compliant and verifies member eligibility. Roundtrip uses real-time GPS tracking and automatically sends text and call notifications to the members about their rides.

Talk to your insurance agent to find out if Roundtrip is included in your plan.

Pick a Plan With Medical Transportation Coverage

If your plan does not offer transportation and you would like to have that benefit, we may be able to find a better plan for you. It all depends on your location and eligibility. We can send one of our agents to your home for a free appointment to figure out what your plan options are.

Just complete this form to request a call or call us at 844-431-1832.

Contact Us | Medicare Plan Finder

This post was originally published on May 31, 2018, by Anastasia Iliou, and updated on December 4, 2019, by Troy Frink.

5 Common Types of Mental Illness In The Elderly

Most of today’s senior citizens grew up in a time when mental illness was almost never discussed in public. Over the years though, the stigma around mental health has largely eroded and conversations about mental health often dominate the national discourse.

As mental illness becomes less taboo, its far-reaching impact on society is coming more into focus. For example, the effects of mental illness in seniors are studied much more closely than ever before.

Common Types of Mental Illness In Seniors

With this more extensive research, it’s easier to see what mental health issues are common in the elderly population. The most prominent issues in senior mental health are:

1. Depression

Depression is often cited as the most endemic mental illness in the elderly population today. Many older adults may shrug depression symptoms off as simply “feeling down,” meaning it often goes undiagnosed and may be even more pervasive than the research suggests.

There are many risk factors that specifically contribute to depression in the elderly. Retiring from work can cause strong feelings of boredom or listlessness, and the death or illness of a spouse can leave many stressed and sorrowful.

Not only can depression exacerbate the symptoms of other chronic health issues, it is also noted as a symptom of more severe mental disorders like dementia. This means seniors and their loved ones must be vigilant in watching for these depression symptoms:

Feelings of sadness, hopelessness, or emptiness

Lack of motivation or interest in previously enjoyed activities

Trouble concentrating and decision making

Thoughts of suicide or self-harm

2. Anxiety

Anxiety disorders can take many different forms, such as obsessive-compulsive disorder (OCD), panic disorder, or generalized anxiety disorder. These are usually characterized by intense fear or nervousness over issues most would consider normal, routine aspects of everyday life – locking doors or finding a parking spot, for example.

Like depression, anxiety in older adults is extraordinarily common and is often underdiagnosed. Older adults are especially prone to ignoring this illness, perhaps because the conventional medical wisdom of previous decades downplayed psychiatric symptoms if no physical issues existed.

It is important to note however, that some physical symptoms such as restlessness or fatigue may accompany anxiety, further confusing a potential diagnosis. Be on the lookout for these symptoms of anxiety in the elderly:

Irrational, obsessive, or catastrophic thoughts

Isolating behavior and withdrawal from others

Irritability or agitated moods

Fatigue and muscle soreness

3. Bipolar Disorder

Bipolar disorder is usually diagnosed in younger people, whose moods can swing quickly from elation to depression. If this diagnosis is made when the person is an older adult, it is referred to as late onset bipolar disorder and it is more likely to manifest as agitation.

Diagnosing bipolar disorder in seniors is made even more difficult by the misinterpretation of symptoms. Many of the warning signs of late onset bipolar disorder might be dismissed as simply the natural effects of aging. Furthermore, some symptoms may resemble the side effects of certain medications, like antidepressants and corticosteroids.

As the population steadily increases, the number of cases of late onset bipolar disorder is expected to rise along with it. Professional help should thus be sought if you or those close to you observe any of these bipolar symptoms in adults:

Agitation and irritability

Hyperactivity or distractibility

Loss of memory, judgment, or perception

4. Schizophrenia

Similar to bipolar disorder, schizophrenia is a condition usually diagnosed in younger individuals. Late onset schizophrenia is the terminology used when this disorder is observed in patients over the age of 45.

Schizophrenia is characterized by a broad range of symptoms, from the so-called “negative” symptoms, like loss of interest or enthusiasm in activities, all the way to delusions and hallucinations. While late onset schizophrenia is less common than the early onset variety, older sufferers are more likely to experience these severe symptoms.

Currently, doctors are unsure what causes late onset schizophrenia and why it is different from its other forms. Some have theorized that it is a subtype of the disorder which is triggered by life events. Regardless, it is vitally important that seniors and their loved ones keep an eye out for these late onset schizophrenia symptoms:

Delusions or hallucinations

Disorganized speech or behavior

“Negative” symptoms (absence or lack of interest in normal behaviors)

5. Dementia

Though it is classified separately from mental illnesses by the medical community, dementia is still a disorder that severely affects mental health. There are many different stages and forms of dementia but the most common incarnation is Alzheimer’s disease, which affects around 3 million people over age 65.

Alzheimer’s and other forms of dementia can develop from the natural cognitive decline that happens as we age, drawing a startling link between aging and mental health. All demographics should make mental health a priority but seniors especially should watch for these dementia symptoms:

Disorientation or confusion (forgetting dates, years etc.)

Decrease in memory

Decline in ability to communicate

Mood swings and emotional issues

Treatment & Medication

Mental illness treatment can involve inpatient or outpatient care.

Mental illness treatment can be a tricky process and it begins with a proper diagnosis of the condition’s type and cause. To do this, your doctor may administer several different types of tests, from cognitive and psychiatric evaluations to brain scans and lab tests.

Several different mental conditions have symptoms that overlap and make them difficult to diagnose without extensive medical experience. Once the condition is properly diagnosed, a doctor may suggest one of these common forms of mental illness treatment.

Outpatient Care

The most common forms of outpatient mental illness treatment are based around medication or psychotherapy, often used in conjunction. The efficacy of these treatments varies from person to person and sometimes multiple treatment options must be attempted before an effective one is found.

For depression and anxiety disorders, pharmacological methods of treatment usually utilize antidepressants. These can be prescribed in addition or as an alternative to psychotherapeutic approaches like “talk therapy.” The Anxiety and Depression Association of America (ADAA) also suggestsregular exercise and a balanced diet as ways of staving off these common mental illnesses, stressing the link between brain and gut health.

The primary medications used in treating bipolar disorder and schizophrenia in seniors are classified as antipsychotics, usually prescribed at a lower dosage than people diagnosed at a younger age. For non-drug treatments of more severe cases, inpatient care is often required for proper rehabilitation.

For the treatment of dementia in the elderly, no cure is currently known. But the symptoms can be managed and the Alzheimer’s Association recommends a non-drug approach before attempting medication. These can begin with something as simple as changing the environment of those with dementia to remove obstacles and promote a general ease of mind.

If these non-drug approaches are not effective, certain types of medications like cholinesterase inhibitors and memantine may be prescribed to temporarily relieve some symptoms. Other approaches may include the use of antidepressants or anxiolytics, depending on the specific behaviors and symptoms that manifest.

Inpatient Care

With the more serious mental illnesses widely seen among seniors, outpatient care may not be an option. Those suffering from bipolar disorder or dementia may not be able to maintain their daily functions on their own and must turn to medical services that can attend to their needs 24 hours a day.

For example, the most common form of therapy for conditions like schizophrenia is a psychosocial approach, where a team of doctors, nurses, social workers and other professionals work in close contact with the patient to monitor their symptoms, both mental and physical, and help them maintain social skills and daily activities.

In these severe cases of mental illness, the accessibility of quality inpatient care has been shown to be a determining factor in recovery. The psychosocial interactions common in inpatient care are now considered to play a necessary role in a comprehensive intervention plan, as isolation can intensify many of the symptoms of these conditions.

What mental health services does Medicare cover?

Medicare can help pay for your mental health care.

When faced with one of these potentially life-changing illnesses, it is important to know what exactly is covered by your health insurance. Depending on the condition and its severity, some patients may need an extended stay in a hospital, which can quickly skyrocket the cost of care. Fortunately, Medicare covers many mental health services.

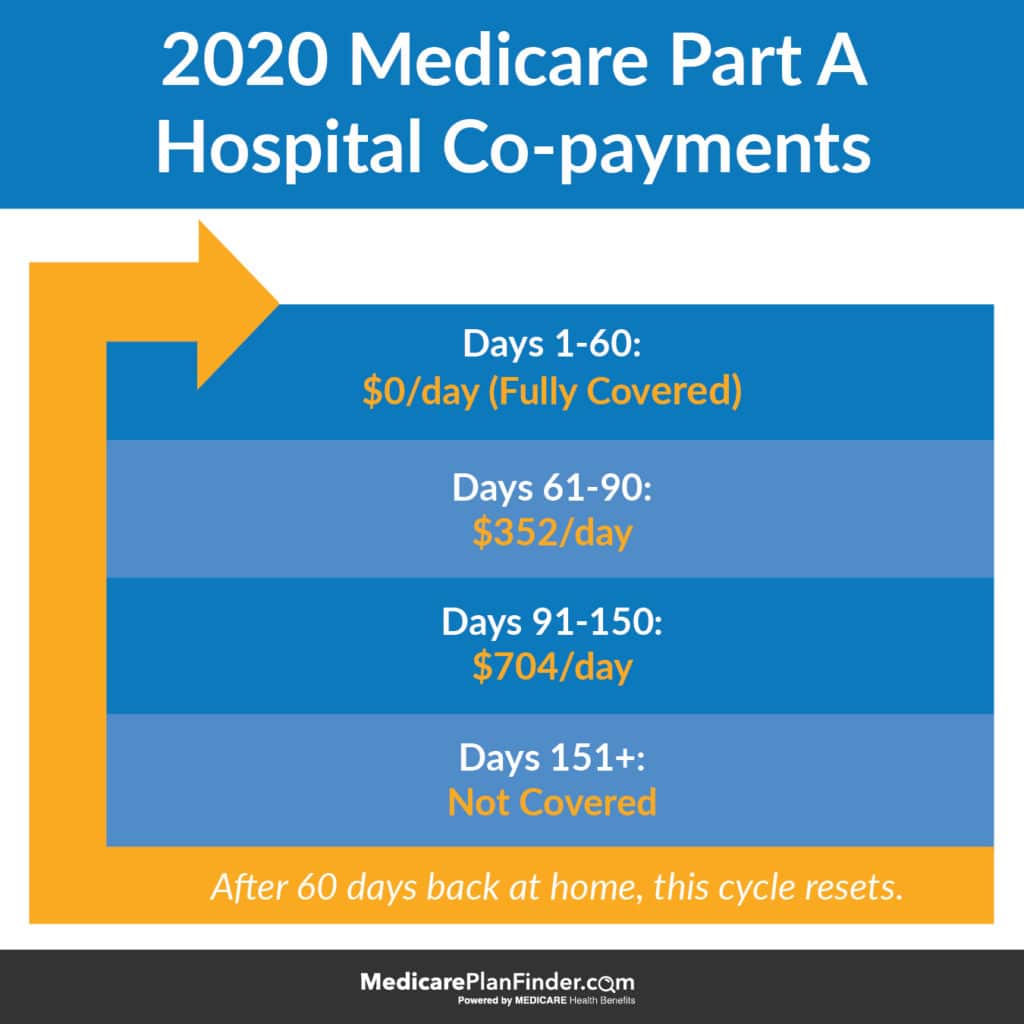

Medicare Part A Coverage

The types of mental health coverage offered differ depending on which elements of Medicare you are covered by. Medicare Part A covers inpatient care, or the medical services you receive while staying in a hospital. The out-of-pocket costs not covered are the same regardless of the type of hospital, general or psychiatric.

Medicare measures your use of hospital facilities using benefit periods. These benefit periods are tallied in increments of 60 days, beginning on the day you’re admitted to a hospital and ending when you haven’t used any hospital services for 60 consecutive days.

If your stay is in a general hospital, there is no limit to the amount of benefit periods Medicare will cover. In a specialized psychiatric facility though, Part A will only pay for up to 190 days of inpatient care during your lifetime.

For further information on how the co-payments break down, check out this handy graphic or see our more in-depth article here.

2020 Medicare Part A Copayments

Medicare Part B Coverage

Medicare Part B will cover most of the cost associated with outpatient mental healthcare. This primarily includes any doctor visits that may relate to your mental health, including appointments with psychiatrists, psychologists, nurses, and social workers.

Therapy and counseling may or may not be covered depending on if the doctor accepts Medicare assignment. Finding a therapist who takes Medicare is now easier than ever, using tailored search tools like the one developed by Psychology Today, available here.

After you meet your Part B deductible, Medicare will cover 80% of their approved amount to the doctor or therapist. This leaves a 20% copay that will have to be paid out-of-pocket. For some, this may still be too expensive and that’s where Medicare Advantage, Supplement, and Part D plans can help!

Medicare Advantage, Supplement & Part D Coverage

There are several types of supplemental coverage that can help pay for Medicare mental health benefits.

Part D plans, for example, offer coverage for prescription drugs which are not covered by original Medicare. For the year of 2020, these plans will have an annual deductible of $435 but, since they are provided by private insurance, there is some variation in the deductible, which may be waived, reduced, or charged upfront.

Medicare Advantage plans, also referred to as Part C, can offer far more benefits than parts A and B alone, including prescription drugs, dental and vision coverage, and group fitness classes tailored to seniors.

Medicare Advantage | Medicare Plan Finder

Alternately, you may choose to apply for a Medicare Supplement plan, which provides additional financial benefits to help with mental health-related costs like copayments and deductibles. There are up to ten distinct types of Medicare Supplement plans (designated alphabetically from A – N). Each plan may differ in coverage and price.

Medicare Supplements | Medicare Plan Finder

Whatever supplemental coverage you are looking for, it is best to seek the help of a licensed agent who can fully explain the details of each plan and find one that works best for you or your loved one. To contact one of these professionals directly for free, no-strings-attached information, fill out this form or give us a call at 844-431-1832 and get covered today!

9 Questions a Caregiver Should Ask Their Parent’s Doctor

Being a caregiver can be fulfilling and joyful, but it can also be a lot of work. You may not know where to find information about your parent’s health condition or treatment plan. Luckily, your parent’s doctor can be a valuable resource who you can –– and should –– rely on for answers. Here are nine questions a caregiver should ask their parent or loved one’s doctor:

1. What can you tell me about my caregiving situation?

Every caregiver’s situation is different. Your loved one may have different medical, nutritional, or assistive needs, and your doctor can tell you the best place to start with meeting your loved one’s healthcare needs.

For example, your parent may need non-emergency medical transportation to their various appointments, and they might need special care. Your parent’s doctor may be able to provide contact information for medical transportation services, or even schedule rides to the office. You might not have considered that your loved one may need an EMT-certified driver, especially with rideshare apps like Uber and Lyft offering rides to doctor’s appointments.

When you ask your parent’s healthcare provider about your unique situation, the physician can discuss the individual needs your parent has. Your loved one’s doctor should feel like a partner in providing the best quality care. Your doctor may even tell you ways to take care of yourself, because it can be easy to forget your own needs when you’re so focused on someone else’s.

2. Can you help me connect with other caregivers in similar situations to me?

It can be easy to feel like you’re on your own as a caregiver. An important question a caregiver should ask is what type of non-medical support they might need. Your parents’ provider may recommend resources such as caregiver support groups and online forums. It’s valuable to connect with other people in similar situations.

When you feel like you have emotional support, you’re able to take better care of your parent. It can be easy to feel frustrated or overwhelmed as a caregiver. A support group can give you ideas to cope, tips for providing better care, and/or just lend an empathetic ear. Your parent’s doctor can give you ideas about how to build a support system.

3. What can I do to build confidence in my caregiving activities and skills?

Your parent’s doctor should talk about your parent’s treatment plan and care needs with you. You should feel confident in your abilities to properly administer medications or help with physical therapy. If you’re unsure of how to do something the doctor recommends, ask them to explain the task further.

Ask if there are any shortcuts, tips, or tricks you need to know about. Find out if you can practice complex tasks so you can help effectively. Some tasks may be dangerous to perform on your own, and you may need to find outside assistance. Find out if you need to look into home health care services or if you can perform the tasks on your own.

4. Can you help me arrange respite care when I need a break?

Providing 24-hour care can be rewarding, but also exhausting. Sometimes you need to take a break. “Respite care” is when your loved one stays at a hospital or other care facility so you can get some much-needed rest. It may give you peace of mind to know that your parent is staying at a facility with qualified professionals.

Your loved one’s healthcare provider can point you in the right direction for finding respite care services.

5. What do I need to know about my parent’s diagnosis?

Every health condition or disease may have different need-to-know information. For example, your doctor may tell you to avoid fatty cuts of beef if your loved one has high cholesterol.

Your parent’s provider should tell you how and when to administer medications, how often you need to make follow-up appointments, and what symptoms to watch out for. The healthcare provider should help you provide the best possible care for your loved one, and that includes knowing the ins and outs of your parent’s health.

6. How will you coordinate with my loved one’s other healthcare providers?

Some diagnoses mean that your parent requires a care team. For example, your loved one might have a gerontologist, a physical therapist, and a neurologist. Ask how the team will coordinate your loved one’s care and keep you in the loop.

For example, some healthcare facilities feature apps to contact care team members if you have questions or need to refill prescriptions. Health facility apps can also include post-appointment notes so you can access any information you need.

7. I found this information on the internet. Is it accurate?

Google has a wealth of information about any disease you can think of. Sources such as WebMD and the Mayo Clinic offer information about symptoms, causes, risk factors, and treatments for a seemingly infinite number of health conditions.

Even though the internet has more information that you could ever need, the information can pose a problem for doctors and patients.

For example, your loved one could fall and bruise their knee. You Google “knee pain,” and read the first web page you see from WebMD. The article you read could have you thinking that your loved one needs a full knee replacement, but all they really need is an ice pack and some over-the-counter pain medications.

Your parent’s doctor will be able to help determine what’s really going on and sort out the facts from the fiction.

8. Should I be concerned about these new symptoms I’m observing?

If your parent has a degenerative health condition or they have new symptoms, ask the doctor if you should be concerned. Your loved one’s healthcare provider will let you know if they need to see your loved one or if you notice something normal. Your parent’s doctor should be available to answer your questions in a timely manner.

9. How will I know when it’s time to look into hospice care?

At some point, your loved one may need to switch from curative (to find a cure) care to palliative (to provide comfort) care. Your parent may be eligible for hospice care if curative care will not work and palliative care is the only option.

Ask your doctor to let you know when it’s time to start palliative care only, and if they know of any resources to find hospice care.

Find Medicare Caregiver Resources

As a caregiver, you’ve got a lot on your plate. Use this list of questions a caregiver should ask their loved one’s doctor can be a valuable source of information if you ask the right questions.

Another valuable resource is your parent’s health insurance plan. If you have durable power of attorney, you can make Medicare decisions for your loved one. A licensed agent with Medicare Plan Finder may be able to help you find a Medicare Supplement or Medicare Advantage plan that suits your healthcare needs and fits your budget. Call 1-844-431-1832 or contact us here to schedule a no-cost, no-obligation appointment today.

Does Medicare Cover Weight Loss Programs [2020]?

Did you know that you can use your Medicare coverage to fight obesity? Medicare coverage for weight loss can include obesity screenings, obesity counseling sessions, nutritionists, and qualified dietitians. It may even include gym membership discounts. If you think eating well and exercising is too expensive, think again: your Medicare plan can cover it!

Medicare Part B Weight Management Services

Medicare Weight Loss Programs | Medicare Plan Finder

Since obesity is classified as a disease, Medicare Part B covers it like any other ailment. It all starts with your “Welcome to Medicare” annual wellness visit when you first enroll, and it continues with your yearly wellness visits. At your appointments, your doctor should check your height, weight, blood pressure, and BMI – all things that can help your doctor diagnose you with obesity and provide proper treatment. These appointments do not require cost-sharing.

If your doctor considers you at risk for obesity, you may be eligible for preventative counseling and even appointments with a nutritionist. Medicare Part B can cover medically necessary obesity counseling and nutrition therapy.

Obesity commonly leads to heart disease. Medicare Part B covers cardiac rehabilitation (exercise, education, and counseling) for those who have had a heart attack, heart failure, or a related surgery.

Nutritionists & Dietitians

Your doctor may recommend that you see a nutritionist or dietician.

Be careful when choosing a nutritionist or dietitian, because Medicare does not cover all of them. For Part B to cover this service, you must medically require it, and the nutritionist or dietitian must accept Medicare assignment. Medicare only covers trained nutritionists under Part B as MNT (medical nutrition therapy). Any patient who has diabetes, kidney disease, or has had a kidney transplant is eligible based on medical need.

As long as you have Medicare Part B and have a BMI (body mass index) of 30 or higher, you are eligible for obesity screenings and counseling. The National Heart, Lung, and Blood Institute has a free BMI calculator on its website, but a doctor’s screening will be much more accurate. Your BMI is the percentage of your bodyweight that is made up of fat. Remember that some fat is healthy – you are not aiming for a BMI of zero. A healthy BMI is between 18 and 25. Lower than 18 is too little, 25-30 is a bit high, and above 30 is obese.

When you do get your free obesity screening, you might consider behavioral counseling for body fat loss. Your primary physician should offer their own obesity counseling. If not, they might recommend another Medicare-covered service.

The only true “Medicare weight loss programs” are fitness programs.

Original Medicare (Part A and Part B) does not cover gym memberships or fitness programs, but private plans may include a gym membership or fitness center discounts. These are usually offered through major Medicare fitness programs such as SilverSneakers® and Silver & Fit®.

Plans with these benefits are not available in every county. Look over your plan or speak with your agent if you aren’t sure about fitness coverage in your Medicare plan.

Obesity Is a Disease

In 2013, the American Medical Association officially started recognizing obesity as a disease. As such, with a BMI of 30 or higher, you can qualify for “obesity behavioral therapy.

The disease affects approximately ⅓ of Americans, and this recognition allows it to be taken more seriously in the medical community and increase research funding. The classification also helps decrease the stigma involved with obesity. It is a commonplace lie that obesity is merely the result of overeating and a lack of exercise. Some people lack the mental strength to control their eating habits and others are incapable of exercising for one reason or another. Saying that obesity is a disease opens the door for obesity counseling and physical therapy as a form of treatment.

Obesity is a common disease in the senior citizen community due to a reduction in physical activity and a lack of access to good nutrition. Additionally, other common senior conditions like heart disease, diabetes, and physical impairments can make it harder to focus on nutrition and exercise. That’s why it’s so important to use your Medicare coverage for healthy eating, exercise, and weight loss.

Does Medicare Cover Weight Loss Surgery/Bariatric Surgery?

Medicare Part B covers bariatric surgeries such as gastric bypass surgery and laparoscopic banding surgery (LAP-BAND). However, you must meet certain criteria. For example, your doctor must determine that Medicare weight-loss surgery is necessary.

Bariatric surgery is a procedure that reduces the amount of food the stomach can hold, effectively forcing you to eat less. However, it is invasive and not recommended for everyone.

Medicare does NOT cover cosmetic surgeries, such as excess skin removal for weight loss surgery.

Types of Bariatric/Weight-Loss Surgeries

The most common bariatric surgeries are a gastric bypass, a sleeve gastrectomy, an adjustable gastric band, and a biliopancreatic diversion with duodenal switch.

Generally, bariatric surgery is recommended for people with:

A gastric bypass is a weight-loss surgery that has been performed for over 50 years, making it the most experienced bariatric operation. In this procedure, a large section of the stomach is stapled off, creating a pouch that connects to the small intestine. The pouch can only hold a few ounces of food, so patients are unable to eat as much as they used to (and won’t feel as hungry).

This procedure requires that patients make major dietary changes. Protein, vitamin B12, iron, and calcium become increasingly important. Sweet and fatty foods must be avoided.

Sleeve Gastrectomy

A sleeve gastrectomy is performed laparoscopically. About 75% of the stomach is removed, causing it to form a “sleeve” shape. This procedure is used for people with a BMI over 40. It often results in 60% weight loss.

A sleeve gastrectomy cannot be reversed. It typically does not have an effect on diet (except for during recovery time).

Adjustable Gastric Band

A laparoscopic gastric banding procedure is the least invasive. A soft, silicone ring with an expandable balloon is implanted at the top of the stomach. It basically creates two compartments for the stomach. The patient will only eat enough food to fill the top part. Over time, the food will pass through into the second (original) compartment of the stomach and will be digested.

This surgery is newer and was not approved until 2001. There may be some long-term complications with this surgery, such as frequent vomiting, implant malposition, erosion, or weight loss failure.

Biliopancreatic Diversion with Duodenal Switch

The duodenal switch procedure starts with a sleeve gastrectomy. Then, the lower intestine is divided, leaving only a few feet of intestine connected to the digestive tract.

This procedure usually results in the greatest weight loss, but patients will likely have frequent and loose bowel movements and gas. Patients will also need to be closely monitored for healthy vitamin, mineral, and protein levels.

In some cases, a doctor or surgeon may recommend that you undergo the sleeve gastrectomy first, then revisit the duodenal switch in 9-12 months.

The duodenal switch often results in 60-80 percent excess weight loss within two years.

Finding a Doctor for Obesity Treatment

Your primary physician can at least help you get started on your obesity treatment but might refer you to a nutritionist or other specialist if necessary.

Be sure to check with your plan network to make sure your doctors and specialists are covered. You can use Medicare.gov’s Physician Finder to find out if a doctor accepts Medicare, and visit your private plan’s website to find out if your doctor or specialist is in your plan’s network.

Are There any Medicare-approved Weight Loss Programs?

Medicare has not formally approved any weight loss programs or fad diets. Speak to your doctor before joining a new program. Here is some information about popular weight loss programs.

Recently, private Medicare Advantage plans have been given the ability to cover more benefits, and dietary programs like this could be one of them. However, it is more common to find Medicare Advantage plans that cover Medicare fitness programs and nutritionists.

Optifast

Optifast is advertised as a “medically-supervised” and “science-based program that delivers weight loss for health gains.” On average, Optifast users ave lost 30 pounds over 26 weeks (which is a healthy ratio). They’ve also seen decreases in blood glucose levels, blood pressure, and cholesterol.

The program provides meal replacements that include 100% of the recommended daily value of 24 different vitamins and minerals. There are five daily servings. Optifast comes in shake mix, bars, soups, and chewable vitamins.

The Jenny Craig plan includes a variety of foods and a personal consultant that you can connect with weekly. The meal plans ask you to eat every two to three hours and allow you to mix in your own fresh fruits, vegetables, and dairy. Three entrees and two snacks cost less than $25 per day.

In some areas, you’ll be able to visit and pick up your food from a local weight loss center. Otherwise, you can join Jenny Craig online.

Weight Watchers

Weight Watchers revolutionized fad dieting with their point system.

Each Weight Watchers user will have a unique amount of “points” they are able to use each day. Every piece of food is awarded a point value (though some may be worth 0 points). Your daily point budget is based on your age, height, weight, and sex. Technically, you can eat whatever you want as long as you don’t go above your daily points budget.

Weight Watchers is not very expensive, starting at $3.07 per week for the digital-only plan. You can download the Weight Watchers app and do it all yourself!

What’s nice about the Weight Watchers diet is that you don’t have to eat frozen foods shipped to you, you can keep buying your own groceries and cooking healthy meals. You may even be able to keep enjoying some of your favorite foods, as long as you enjoy them in moderation.

Medicare for Diabetes and Weight Loss

Obesity can put you at a higher risk of developing diabetes. You can use your Medicare coverage to help prevent both obesity AND diabetes.

Medicare Part B covers diabetes self-management training (DSMT), blood sugar monitors, blood test strips, lancets devices, lancets, therapeutic shoes or inserts, and external insulin pumps.*

Additionally, Medicare can cover your participation in the 16-session Diabetes Prevention Program if you:

Have a BMI over 25 (23 if you are Asian)

Have never been diagnosed with either diabetes or ESRD

Have not participated in this program before

Have a hemoglobin A1c test result of 5.7-6.4%, a fasting plasma glucose result of 110-125 mg/dL, or a two-hour plasma glucose result of 140-199 mg/dL (test results must be from the past 12 months)

Medicare Part A covers hospital stays, and Medicare Part B covers physician services. If you are over the age of 65, you automatically qualify for Medicare coverage. You can also qualify by receiving SSDI (Social Security Disability Income) for 25 months or more or by being diagnosed with either ALS (Lou Gehrig’s Disease) or ESRD. Most people will get premium-free Part A but will have to pay a monthly premium for Part B.

To add more to your Medicare plan, the best option is to enroll in a MAPD, or Medicare Advantage Prescription Drug plan. These plans include everything that Part A and Part B covers plus prescription drug coverage and other benefits like dental, vision, and fitness programs like SilverSneakers® and Silver & Fit®.

We have benefits advisors in 38 states that can help you select the best Medicare Advantage Prescription Drug plan for your needs. Some people may even be able to get a MAPD plan with a $0 premium! To find out more, chat with us, send us a message, or give us a call at 844-431-1832.

This post was originally posted on June 22, 2017, and was last updated on December 3, 2019.

Is UnitedHealthcare Dropping SilverSneakers in 2020?

As of January 1, 2019, UHC no longer offers SilverSneakers® with Medicare Advantage plans in 11 states:

California

Connecticut

Illinois

Indiana

Iowa

Kansas

Missouri

Nebraska

Nevada

North Carolina

Utah

Along with Medicare Supplement (Medigap) plans in nine states:

Arizona

California

Connecticut

Illinois

Indiana

North Carolina

Ohio

Utah

Wisconsin

Why Did UHC and SilverSneakers® Part Ways?

According to Sam Warner, who leads UHC’s Medicare Advantage product team, the company’s move away from SilverSneakers® is to “reach a broader portion of our membership” with a “wider variety of fitness resources.” Warner noted that “over 90 percent of policyholders who are eligible for SilverSneakers® “never step foot in a gym.”

Will UnitedHealthcare offer any fitness benefit in 2020?

Fitness Benefit | Medicare Plan Finder

Yes. Starting in 2020, UHC will offer new fitness benefits* with some plans. As plans can vary in every zip code, ask your licensed agent whether or not this benefit can apply to you!

Medicare beneficiaries with certain UHC Medigap plans may feature a fitness benefit that includes gym membership discounts and phone access to wellness coaches along with other health resources.

Medicare Advantage policyholders may be able to join a program called Renew Active™, which will replace SilverSneakers® in January 2020. The Renew Active™ benefit may include access to fitness centers, classes, and group activities along with tools to exercise your brain health.

*Always check with your doctor before starting any fitness program to make sure the program suits your individual needs.

How Does Renew Active™ Work?

The new Renew Active™ program includes a gym membership, an online “brain health program,” and access to local events. You can use the Renew Active™ website to find a facility close to you that participates in the program. Renew Active™ works with popular gym chains and local gyms. It may include some Planet Fitness locations, YMCAs, and more.

At no additional cost, Renew Active™ also comes with a personalized fitness plan. You’ll get an introductory one-on-one personal training session to set your initial goals and then you’ll be able to meet with your trainer at least yearly.

You’ll be able to work on strength, aquatic exercises, cardio, mind & body, and other specialty activities (like self-defense or Zumba®).

Renew Active™ can also coordinate with your Fitbit as well as your AARP® Staying Sharp program.

You can get Renew Active ™ if your UHC/AARP ™ Medicare plan supports it.

When Can I Enroll in a Medicare Advantage or Medicare Supplement Plan?

The Annual Enrollment Period (AEP) is from October 15 – December 7, which is the time of year many Medicare beneficiaries can enroll in new plans or make changes to existing ones.

Some members qualify for a Special Enrollment Period (SEP). Depending on your eligibility, you may have a lifelong SEP, which allows you to make one change per quarter for the first three quarters of the year — instead of only during AEP. Some people may only be eligible for a temporary SEP due to a life change, like moving to a new service area.

If you have just become eligible for Medicare for the first time, you can enroll in Medicare Advantage during your Initial Enrollment Period (IEP).

When You Can Enroll in Medicare Supplement Plans

You can enroll in a Medicare Supplement plan at any time during the year as long as you meet the requirements for Original Medicare (Part A and Part B).

Note: Don’t wait too long to enroll in Original Medicare because once you’re out of your IEP you may require underwriting, because insurance carriers aren’t required to honor your “Guaranteed Issue Rights”.

Tennessee YMCA Locations Breaks Partnership With SilverSneakers ®

In related news, the Tennessee State Alliance of YMCAs decided to leave the SilverSneakers® network. The change is effective January 1, 2020.

The two organizations parting ways means that you must find different coverage if you want to continue exercising at Tennessee YMCA locations.

Tennessee YMCA locations still accept Silver & Fit®, and you may be able to use Renew Fit.

Other Supplemental Benefits With Medicare Advantage Plans

Along with fitness benefits, some Medicare Advantage plans can offer coverage for vision, dental, and hearing services. Other supplemental benefits include meal delivery, non-emergency medical transportation, and drug coverage (prescription and over-the-counter).

Find Medicare Plans With a Fitness Benefit

If you want a Medicare plan with a fitness benefit or any other supplemental benefit, one of our licensed agents may be able to help. Our agents are highly trained and they can help you sort through the plans available in your location. To set up a no-cost, no-obligation appointment, call 844-431-1832 or contact us here today!

This blog was originally published on October 1, 2019. The latest update was on November 26, 2019.

Dental Vision Hearing Insurance for Seniors and Medicare Beneficiaries

It’s important to always be mindful of your overall health. That includes everything – from the aches and pains you feel to your teeth and your eyesight!

Unfortunately, Original Medicare does not include extensive dental, vision, and hearing insurance for seniors and Medicare beneficiaries. If you are looking for dental, vision, and hearing insurance, you should consider a Medicare Advantage plan.

Original Medicare only includes Part A (hospital coverage) and Part B (doctor coverage), but Medicare Advantage plans, also called Part C, generally include dental benefits, vision benefits, hearing benefits, prescription drug coverage, and more!

Original Medicare covers limited dental, vision, and hearing procedures:

Oral examinations as part of another hospital stay

A jaw disease, oral cancer, face tumor, or face fracture-related procedure

Infections caused by dental procedures

Severe and medically necessary eye procedures and tests such as cataract surgery and corrective lenses following surgery

Macular Degeneration, Glaucoma, and Diabetic Retinopathy tests

Hearing tests that are a part of your primary physician’s routine well-visit

Cochlear implants

Does Medicare pay for hearing aids?

Original Medicare does not cover everything. Medicare Advantage plans can add the following hearing insurance for seniors benefits:

Treatments for hearing problems

Hearing aids

Hearing aid fittings

Hearing aid exams

Hearing tests

Hearing Aid Costs

Medicare Advantage health insurance plans can help cover hearing aid costs associated with fittings, exams, and tests.

Hearing aid costs can range anywhere from $400 to $4,000 per ear. Even if the initial device isn’t too expensive, you may have to pay the costs of a hearing aid fitting, hearing aid exams, and replacement hearing aids every five years or so.

When you add everything together, you could be paying thousands of dollars over your lifetime for your ear care. Luckily, a Medicare Advantage plan is a solution that may help you out financially.

Hearing Aid Brands