Cost sharing is the reason we have any kind of insurance. In many cases, you don’t pay the full amount of medical expenses if you have health insurance. For example, Original Medicare covers 80 percent of approved costs, and you pay 20 percent. It may sound simple, but it can actually be pretty confusing when you take into account deductibles, copays, coinsurance, out-of-pocket maximums, and premiums.

Medicare Cost Sharing Definitions

Medicare cost sharing may seem more complex than other forms of insurance because Medicare has four different parts, and each one covers something different. Two of those parts are public (Parts A and B), and two are private (Parts C and D).

When you add Medicare Supplements to the mix, things may seem even more confusing. For example, you can’t have both a Medicare Part C plan and a Medicare Supplement plan at the same time. Also, if you have a Medicare Part C (Medicare Advantage) plan, you may not need a Part D (prescription drug) plan because some Medicare Advantage plans cover prescription drugs.

Before we go over what cost sharing looks like for each part of Medicare, we’re going to cover some basic Medicare cost-sharing terminology:

Coinsurance: A percentage of the total cost for medical services. The amount you pay may be different depending on the bill. For example, you may pay 20 percent of the total bill for a doctor visit. If your doctor bills Medicare $100, you’d pay $20.

Copayment: A set amount that you pay for medical services. For example, you may pay $10 upfront for a doctor’s appointment. If your doctor bills Medicare $100, you’d still pay $10 (though you may receive a larger bill for coinsurance later), depending on what your plan pays.

Deductible: The amount you pay out-of-pocket each year before insurance coverage “kicks in.”

Out-of-Pocket Maximum: An overall out-of-pocket spending limit you might have with certain Medicare Advantage plans. Once you reach the maximum, Medicare will cover 100 percent of all approved costs.

Premium: A set amount you pay every month to keep your coverage.

Medicare Part A Cost Sharing

Medicare Part A is hospital insurance and it covers inpatient procedures, hospice care, and skilled nursing facilities. Many Medicare eligibles don’t pay a monthly premium for Part A. If you don’t meet the “premium-free Part A” requirements, you may pay up to $458 per month in 2020.

The 2020 Part A deductible is $1,408. For inpatient hospital or skilled nursing facility stays, you may pay:

Days 1-60: $0 coinsurance

Days 61-90: $352 coinsurance per day in 2020

Days 91 and beyond: $704 coinsurance per day in 2020. You may be able to use “lifetime reserve days,” which are “extra” days Medicare may cover. You may have up to 60 lifetime reserve days. Once you’ve used your lifetime reserve days, you may be responsible for paying 100 percent of hospital services.

Medicare Part B Cost Sharing

Medicare Part B is medical insurance, and it helps pay for outpatient medical services such as doctor’s appointments, emergency medical transportation, outpatient therapy, and durable medical equipment (DME).

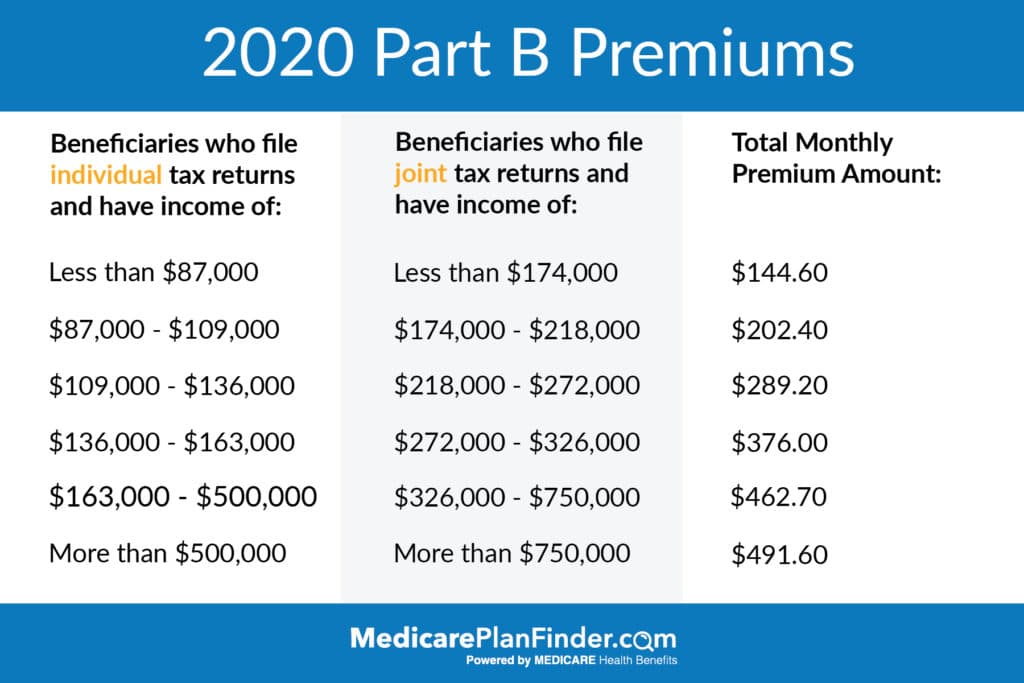

The standard Part B premium is $144.60 in 2020. You may have to pay more depending on your income.

The deductible for Medicare Part B is $198 in 2020. After you meet the deductible, you may pay 20 percent coinsurance of the Medicare-approved total amount.

2020 Medicare Part B Premiums

Medicare Part C Cost Sharing

Medicare Advantage (MA or Part C) are private plans that can cover additional benefits such as prescription drugs, dental, hearing, vision, and fitness classes. You must be enrolled in both Part A and Part B before you can enroll in a MA plan.

Premiums for MA depend on the plan*. They can be as low as $0, but as much as $200. The average premium in 2020 is $23.

Each Medicare Advantage plan may have a different deductible, copay, and/or coinsurance payment. In 2020, the Medicare MOOP (Maximum Out-Of Pocket) spending amount is $6,700**.

Your agent can help you decide if a Medicare Advantage plan is right for you.

*You will still have to pay your Part B premium even if you have a Medicare Advantage plan.

**Medicare MOOP only applies to Original Medicare-covered services. It does not apply to supplemental benefits.

Medicare Part D Cost Sharing

Medicare Part D is prescription drug coverage. You may have to pay a monthly premium, for which the average cost was $33.19 nationwide in 2019.

The 2020 Part D deductible is $435, meaning that Part D plans cannot charge a deductible any higher than that. Many plans may have lower deductibles. Your coverage won’t start until you’ve met your plan’s deductible.

After you meet the deductible, you’ll pay 25 percent of both generic and brand name drug costs. For example, if a prescription drug’s total cost is $40, you’ll pay $10, and your insurance plan will pay the remaining $30.

If your plan requires you to pay a copay or coinsurance, those costs will go toward your TrOOP (True Out-Of Pocket). For example, if your plan requires a $15 copay for a drug, that money will go toward your out-of-pocket limit.

After you pay $6,350, which is the TrOOP threshold, you enter Catastrophic Coverage, and you’ll pay only five percent of your prescription drug costs.

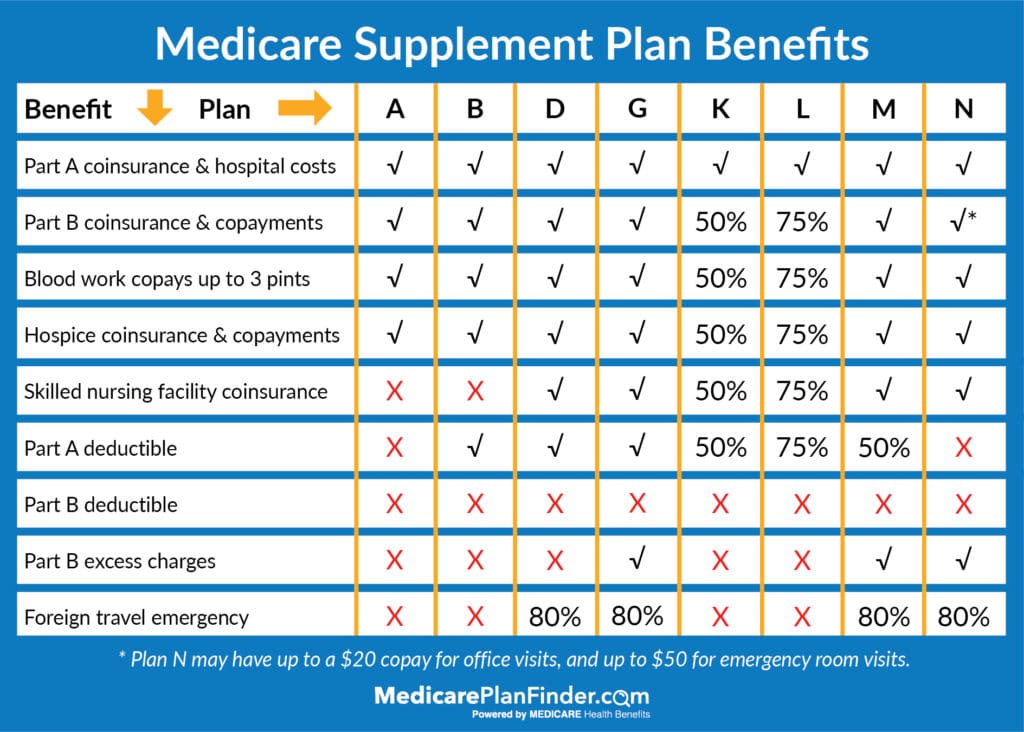

Medicare Supplement (Medigap) plans have a different cost sharing structure than MA plans. Medigap plans have eight standardized coverage levels*. In 2020 there are eight different coverage levels:

2020 Medicare Supplement Comparison Chart

Medicare Supplement plans work like this: You pay a monthly premium** and the plan covers the financial items in the chart above. Medigap plans only cover Medicare-approved costs, not additional benefits like MA plans.

Talk to your agent to discuss your needs and whether a Medigap plan is right for you.

**You will still be responsible for paying Part B premiums with a Medicare Supplement plan.

We Can Help You Navigate Medicare Cost Sharing

Cost sharing with Medicare may seem complicated, and a licensed agent with Medicare Plan Finder can help you determine what you need. Our agents are highly trained, and they can find the Medicare Advantage, Medicare Supplement, and/or Medicare Part D plans in your area. To arrange a no-cost, no-obligation appointment with an agent, call 1-844-431-1832 or contact us here.

FreeStyle Libre Medicare Coverage

FreeStyle Libre is a continuous glucose monitor (CGM) that consists of a small, water-proof, fully disposable sensor that you wear on your arm for 14 days, plus a reader device.

The reader shows your blood glucose levels in real time, and it doesn’t require a finger stick like most CGMs do. FreeStyle Libre is approved for monitoring blood glucose levels in both Type 1 and Type 2 diabetics.

FreeStyle Libre Medicare coverage is much like other Medicare coverage for durable medical equipment (DME). You may have to pay coinsurance or copays, and you have to purchase your DME from a Medicare-approved supplier.

How does FreeStyle Libre Medicare Part B coverage work?

Medicare Part B is medical insurance, and it helps pay for outpatient doctor’s appointments, preventive care such as diabetes screenings, and durable medical equipment (DME). In order for Medicare to approve your DME, your doctor must prescribe it, and it must be a device that will last for three years or more.

You may be responsible for 20 percent of approved Medicare costs for FreeStyle Libre including the equipment itself and your doctor’s supervision.

Medicare Supplement Coverage for FreeStyle Libre

Medicare Supplements (Medigap) plans are private insurance plans that can help pay for expenses that you may incur with Original Medicare (Part A and Part B) such as coinsurance and copays. They work like this: you pay a monthly premium, and your copays and coinsurance, including what you’d pay for durable medical equipment, are covered.

Medicare Advantage FreeStyle Libre Coverage

Medicare Advantage (MA or Part C) plans are also private plans. They work differently than Medigap plans because MA plans offer additional benefits rather than help paying for financial items.

You cannot have both a Medigap plan and a Part C plan, so it’s best to contact your agent to discuss your individual needs, including coverage for diabetes and durable medical equipment.

How much does FreeStyle Libre cost without insurance?

According to GoodRx, FreeStyle Libre can cost about $135 every two weeks. That adds up to $3,510 per year.

Medicare Coverage for Insulin

Original Medicare does not help cover insulin unless it’s in conjunction with an insulin pump. Medicare Part D or certain Medicare Advantage plans may help cover insulin products such as Lantus and Novolin.

According to GoodRx, Lantus is the most popular insulin drug. The average copay is $37.50-$67.50.

Where can I get FreeStyle Libre?

You can get FreeStyle Libre at most major pharmacies, however, Medicare may only cover the device if you get it at a “participating DME supplier.” According to Abbot, the FreeStyle Libre manufacturer, Medicare will help pay for the device if you purchase it from one of the following suppliers:

Advanced Diabetes Supply

Better Living Now

Byram Healthcare

CCS Medical

Diabetes Management & Supplies

Edgepark Medical Supplies

Edwards Health Care Services

HealthLink Solara Medical Supplies

J&B Medical Supply

Mini Pharmacy

United States Medical Supply

In order for Medicare to cover your durable medical equipment, your doctor must say it’s medically necessary. You may need to have periodic follow-up appointments in order for Medicare to continue covering FreeStyle Libre.

How do I use a FreeSyle Libre system?

With the FreeStyle Libre 14-day system, you’ll wear a small sensor on the back of your upper arm that automatically* monitors your glucose 24 hours a day.

Instead of finger pricks**, you simply swipe the reader over the sensor on your arm for a painless, one-second scan. Each scan provides an up-to-the-minute glucose reading, a graph to spot trends, and an eight-hour history of your glucose levels.

*The FreeStyle Libre system requires a one-hour warmup period when you first wear the device before you can check your blood glucose levels.

**You may still have to prick your fingers in certain situations including when your symptoms don’t match your CGM readings and when you suspect that the readings may not be accurate.

Difference Between FreeStyle Libre and Other Constant Glucose Monitors

According to the Diatribe Foundation, a company that distributes information about diabetes, another CGM called the Dexcom G6 received Medicare DME approval in early 2019.

Like Abbot’s FreesStyle Libre, Dexcom’s G6 is covered for people on “intensive insulin therapy like multiple daily injections or use of an insulin pump.”

Both devices feature a smartphone app that you can use to closely monitor your blood glucose and manage your insulin treatment. According to Diatribe, Medicare covers CGM smartphone apps “including sharing features.”

The main differences between FreeStyle Libre and G6 are the “warmup periods” and how long you can wear the devices. FreeStyle Libre features a one-hour warmup period, and you can wear the device for two weeks. The Dexcom G6’s warmup period is two hours, and you can wear the device for 10 days.

Who needs constant glucose monitoring?

Diabetic people need constant glucose monitoring because their bodies can’t produce insulin or efficiently use the insulin it makes. Insulin is a hormone that regulates blood sugar levels.

FreeStyle Libre is best for diabetics who use insulin pumps or need multiple insulin injections per day. According to the Mayo Clinic, if you don’t manage diabetes, it may lead to the following complications:

Along with managing blood glucose levels, a balanced diet such as the Mediterranean diet, exercising regularly, and maintaining a healthy weight may help prevent type 2 diabetes or manage type 1 diabetes symptoms and complications. Work with your doctor to develop a comprehensive treatment plan.

If you have diabetes and you want to learn more about Medicare coverage for FreeStyle Libre, a licensed agent with Medicare Plan Finder can help.

Our agents are highly trained, and they may be able to find plans in your area that cover fitness programs, meal delivery, hearing, and/or routine vision care. To set up a no-cost, no-obligation appointment to discuss your needs, call 1-844-431-1832 or contact us here now.

The Ultimate Guide to Medicare Coverage for Arthritis

Arthritis is an inflammation of the joints. The condition can affect one or more joints, and it can cause pain and stiffness. According to the Centers for Disease Control and Prevention (CDC), approximately 54.4 million adults 18 and older have diagnosed arthritis, and the “prevalence of arthritis increases with age.”

Some types of arthritis may be preventable and the symptoms may be manageable. Medicare may cover different treatments and services for arthritis.

Common Types of Arthritis

There are more than 100 types of arthritis, but the most common types are:

Rheumatoid arthritis is an autoimmune condition in which the immune system attacks your joints and organs. Rheumatoid arthritis has no known cause. According to the Mayo Clinic, your primary care provider may refer you to a rheumatologist if you have the following symptoms:

Tender, warm, and/or swollen joints

Stiff joints that are worse in the morning or periods of inactivity

Inflammation tests such as erythrocyte sedimentation rate (ESR)

Rheumatoid Factor (RF) tests to look for antibodies that indicate rheumatoid arthritis

Imaging tests such as X-Ray, MRI, and Ultrasound to examine joints

Medicare Coverage for Rheumatoid Arthritis

Original Medicare helps cover doctor-recommended diagnostic testing for RA, doctor’s appointments, and some doctor-administered drugs such as disease-modifying antirheumatic drugs (DMARDs). Other covered treatments can include physical therapy, over-the-counter (OTC) drugs such as ibuprofen, and corticosteroids (inflammation relief drugs) such as prednisone. In rare circumstances, your doctor may recommend surgery.

Original Medicare does not cover prescription drugs that you take at home, but Medicare Part D or certain Medicare Advantage plans might.

Medicare Advantage plans are private insurance plans that can cover benefits Original Medicare does not such as meal delivery, OTC drugs, and non-emergency medical transportation.

Osteoarthritis

According to the National Institute of Arthritis and Musculoskeletal and Skin Diseases (NIAMS), osteoarthritis is the most common type of arthritis. The disease causes damage to a joint’s protective cartilage, which wears down over time. Osteoarthritis can affect any joint, but it most commonly occurs in the hands, knees, hips, and spine.

Joint stress caused by repetitive physical activity (sports, active jobs, etc.)

Osteoarthritis can have the following symptoms:

Joint stiffness, especially after sitting for long periods of time

Swelling or tenderness in one or more joints

The feeling of bone on bone, or a “crunching” feeling

Osteoarthritis Treatment and Medicare Coverage

Treatment for osteoarthritis includes over-the-counter drugs such as Tylenol and ibuprofen. Prescription-drug treatment can include antidepressants such as Cymbalta, which can ease arthritis-related pain if OTC drugs don’t work. Medicare Part D and certain Medicare Advantage (MA) plans can cover prescription drugs, and some MA plans may cover OTC drugs.

Non-medication treatments can include physical therapy, occupational therapy, and if the condition becomes severe, surgery such as osteotomy and joint replacement.

Psoriatic Arthritis

Psoriatic arthritis is an autoimmune condition like rheumatoid arthritis. Like rheumatoid arthritis, psoriatic arthritis can cause joint stiffness and pain. According to the Arthritis Foundation, about 30 percent of people who have the skin condition psoriasis also get psoriatic arthritis.

Symptoms of psoriatic arthritis include:

Joint pain and stiffness

Tendon or ligament pain

Rashes or changes to fingernails and toenails

Fatigue

Limited range of motion

Vision problems

Psoriatic arthritis is also linked with irritable bowel syndrome (IBS), Crohn’s disease, and other digestive issues such as diarrhea.

Medicare Coverage for Psoriatic Arthritis

Psoriatic arthritis treatment includes prescription drugs such as DMARDs and corticosteroid injections, and topical treatments such as calcipotriene. Over-the-counter treatments include topical treatments such as salicylic acid gel and NSAIDs.

Fibromyalgia is a condition that causes chronic pain, fatigue, memory problems, and changes in mood. It is not one disease, but a collection of manageable symptoms. The cause is unknown. Symptoms include:

Pain: The most common fibromyalgia symptom is widespread pain in the joints, bones, and muscles.

Fatigue: Many people with fibromyalgia experience exhaustion, flu-like fatigue, and/or disturbances to sleep.

Problems with concentration and mood: Depression is a common symptom of fibromyalgia, along with difficulty concentrating or performing simple mental tasks. Stressful times often exacerbate these symptoms.

Headaches: People with fibromyalgia often experience tension headaches and/or migraines.

Fibromyalgia Treatment

Treatment for fibromyalgia does not cure the condition, but it helps manage symptoms.

According to the Arthritis Foundation, “There are currently three FDA-approved medications for fibromyalgia –– pregabalin, duloxetine and milnacipran.” Some Medicare Part D and Medicare Advantage plans may cover those drugs.

Other treatments can include exercise, acupuncture, and biofeedback, which teaches people how to change physiological functions such as slowing a rapid heart rate.

Gout

According to the Arthritis Foundation, “Gout is a form of inflammatory arthritis that develops in some people who have high levels of uric acid in the blood.” Gout usually starts in the big toe or a joint in the lower body. Gout usually starts after an illness, injury, or infection, and it affects one joint at a time.

Gout Treatment

According to the Arthritis Foundation, gout treatment includes medication and “lifestyle changes.”

Prescription drugs to treat pain and inflammation include colchicine and corticosteroid injections. Drugs to reduce uric acid include Zyloprim and Uloric. OTC medications include NSAIDs.

If you have a gout flare-up, you should take anti-inflammatory medication, ice and elevate the joint, stay hydrated (but not with sugary soda), relax, and ask for help to perform daily tasks.

Get Medicare Coverage for Arthritis Today

If you need help getting Medicare coverage for arthritis, an agent with Medicare Plan Finder can help. Our agents can help determine your budget, lifestyle, and medical needs, and search for a plan in your area that suits you. To set up a no-cost, no-obligation appointment with a licensed agent, call 1-844-431-1832 or contact us here today.

Does Medicare Cover Hospice Care?

More than 1.7 million Americans use hospice each year to maintain or improve their quality of life due to a terminal illness. Hospice care plans address physical, emotional, and spiritual pain and offer support to caregivers during the grieving process.

Hospice decisions can take an emotional and financial toll on you and your family, so you may be asking… “Does Medicare cover hospice?”

How does Medicare cover hospice care?

If you are enrolled in Medicare Part A (hospital insurance), you may qualify for hospice care. However, you must meet the following criteria:

Your doctor certifies that you are terminally ill (with a life expectancy of less than 6 months)

You accept palliative care (for comfort) rather than try to cure your condition

You sign an agreement choosing hospice care over other Medicare-covered benefits to treat your illness

You are not eligible if you had already made a hospice election or have not previously received pre-election hospice services (evaluation of your need for pain and symptom management).

If you meet the above criteria, the following services may be part of your hospice care plan and are covered in part by Medicare:

Other services focused on pain and symptom management

There may be a co-payment of $5 for your prescription drugs or other pain relief. You may also need to pay five percent of the Medicare-approved amount for respite care. However, the following services are not covered by Medicare:

Hospice is intended for people who have six months or less to live. To receive hospice care, you can not receive curative treatment.

If you decide to receive treatment, your hospice care is no longer covered. However, you can withdraw from your hospice care at any given point, and you can resume treatment as long as you are still eligible.

Prescription Drugs Intended to Cure

Just like you can’t pursue curative treatment, you can not take prescription drugs that are intended to cure your illness when receiving hospice care. Hospice only covers drugs that are intended for pain relief and control.

Care for Any Hospice Provider That Wasn’t Arranged by the Hospice Team

You are only eligible to receive care from the hospice team that you initially select.

You cannot get hospice coverage from a different provider unless you go through the switching process. However, you can still visit your regular doctor if they have been appointed to supervise your hospice care plan.

You can only switch to a different hospice provider once per benefit period. If you are interested in switching, be sure to do your research and pick a hospice team you feel comfortable with.

Does Medicare cover hospice room and board?

Medicare does not cover room and board regardless if you live at home, in a nursing home or inpatient assisted living facility, or inpatient hospice office. The only exception is during short-term inpatient or respite care stays in which Medicare will help cover the costs.

Emergency Care

Emergency transportation is not covered by Medicare’s hospice benefits. Medicare will not cover emergency inpatient hospital care unless they are arranged by your hospice team or unrelated to your terminal illness.

Does Medicare cover hospice in a nursing home or at home?

If you are eligible, Medicare will cover hospice care regardless if you receive the care in your home, nursing home, or inpatient facility. Some nursing homes work directly with a hospice team. In a nursing home setting, your hospice team can help with the following:

Regular visits to the nursing home

Consultations by specialized hospice physician as needed

Pain and medication management

Educating staff on symptoms, medications, and care

Emotional and spiritual support

Coordinating care across all patient’s medical providers including doctors, hospice team, and nursing home staff

How long will Medicare pay for hospice care?

Hospice care is intended for people who have less than an estimated six months to live. If you still require hospice care after six months, you can continue to receive benefits if a hospice doctor recertifies your terminal illness in a face-to-face meeting.

You can get hospice care for two 90-day benefit periods followed by an unlimited number of 60-day benefit periods.

Level One: This level includes basic care under Medicare’s hospice benefit. Services include nursing services, medical equipment & supplies, and medications.

Level Two: Medicare designates people who need continuous care such as home health care. The home health aide stays in the patient’s home for eight to 24 hours a day, but it’s short-term care. The patient’s needs are re-evaluated once every 24 hours.

Level Three: The third level of Medicare hospice coverage is general inpatient care. Some people have short-term symptoms that are so severe that they can’t get adequate treatment at home. With level three care, the patient has 24-hour care available.

Level Four: This level of care is more for the family than the patient. If the patient doesn’t meet the criteria for inpatient care and the family needs a break from daily care duties, respite care may be an option. Respite care provides caregivers temporary relief by admitting the patient to a hospital.

Medicare Palliative Care vs. Medicare Hospice Care Coverage

Medicare can cover palliative care for helping relieve symptoms in accordance with curative care. Some organizations define palliative care as “specialized medical care for people living with a serious illness” with the focus of care being symptom relief rather than to find a cure.

The difference between palliative care and hospice care is that palliative care can occur in conjunction with curative care.

Medicare may cover palliative care, but not under the Medicare hospice benefit.

Hospice and Medicare Supplements

Medicare Supplements can help cover the gaps in hospice care that Original Medicare may not, like prescription drugs for pain relief and respite care. After your Medicare coverage, you will likely be responsible for five percent of your total respite care costs and a $5 copay per prescription drug. Medicare Supplements can cover some, or all, of these gaps.

Medicare Supplement Plans A, B, D, G, M, N cover 100 percent of hospice coinsurance and copayments. Medigap Plan K covers 50 percent and Plan L covers 75 percent.

If you are interested in enrolling in a Medicare Supplement plan, or have questions on how these plans work with your correct coverage, click here to get in contact with a licensed agent.

2020 Medicare Supplement Comparison Chart

Hospice and Medicare Advantage

If you enroll in a Medicare Advantage plan, you will have the same hospice care coverage as with Original Medicare. However, Medicare Advantage plans can offer extra benefits like vision, hearing, and dental coverage. They may also offer fitness programs like SilverSneakers®.

If you are interested in enrolling in a Medicare Advantage plan, fill out this form, or give us a call at 844-431-1832. There is no cost to you to meet with one of our agents and there is never an obligation to enroll.

This post was originally published on April 16, 2019, and updated on November 18, 2019.

Those golden years have arrived. If you’re lucky, retirement is just around the corner. Before you retire, you need to make the following important considerations:

Setting a retirement date

Making withdrawals from retirement accounts

Receiving Social Security benefits

Enrolling in Medicare

Writing a will

Paying for your final expenses

Retired couple dancing on the beach

Setting a Retirement Date

While you may have been eager for your retirement to start as soon as you began working, you need to consider your financial situation before you retire.

Take a look at your savings account and your retirement accounts. Think about how much your Social Security benefits will be. If you have a health savings account, also consider those numbers.

Determine your living expenses, health expenses, and the costs of your other retirement dreams.

Go over your available funds and expenses with a financial adviser to estimate how much you need to take care of yourself during retirement and compare those numbers with what you have in your retirement accounts and what you can receive from Social Security.

Making Withdrawals From Retirement Accounts

When you start planning withdrawals from your retirement accounts, you need to understand how taxes work on them and what the age requirements are.

Some retirement accounts, like 401(k)s, are tax-deferred accounts, which means that you’ll owe taxes on what you withdraw.

Other retirement accounts, like Roth IRAs, are made of taxed income. Since these funds were already taxed before growing in the account, they are not taxed when you make withdrawals.

Understanding how taxes work for your retirement accounts will help you plan your withdrawals and anticipate your taxes each year.

You can start making withdrawals without penalties from your retirement accounts at age 59 and a half.

Meet with a financial planner or advisor to review the specifics of your situation and discuss the best option for planning your withdrawals. In some cases, making some withdrawals before the first required minimum distribution may help with tax-planning.

Financial advisor shaking hands with senior woman in living room

Receiving Social Security Benefits

You should also discuss Social Security retirement benefits with a financial advisor. You can start receiving benefits as early as age 62, but the benefit amount may be lower than it could be because you’re receiving the benefit early.

Deciding when to start receiving Social Security retirement benefits depends on your situation, including how long you want to work, your financials, and your health. Whenever you decide to start receiving Social Security benefits, be sure to apply four months in advance of that date.

While there are some exceptions that allow you to become eligible for Medicare earlier, you become eligible for Medicare when you turn 65 years old. Your initial enrollment period (IEP) starts three months before your 65th birthday and ends three months after your 65th birthday. If you retire from the railroad, you may automatically be enrolled.

During this first enrollment period, you do not have to worry about passing an underwriting process or being charged more or denied for pre-existing conditions. Take advantage of this time to research your options and make an informed choice.

You can choose to enroll in Parts A and B (Original Medicare) only, or add on either Part C (Medicare Advantage Plan) or D. Original Medicare is run by the government and includes Medicare Part A, hospital insurance, and Medicare Part B, medical insurance. You can visit any doctor in the country who accepts Medicare. Enrollment is managed by Social Security.

If you enroll in Medicare Advantage, you’ll still have A and B, but you may be able to get additional benefits. These plans are managed by private health insurers and are similar to other private health plans. For example, these plans have networks of health care providers. Some also offer dental, hearing, vision, and prescription drug coverage.

As you decide the direction you want to take when you enroll in Medicare, consider Medicare Part D (prescription drug coverage) and Medigap. You cannot have Medicare Advantage, Part D, and Medigap at the same time. You’ll have to choose between Medicare Advantage only, Medigap only, Part D only, or Medigap and Part D.

Part D plans only provide prescription drug coverage. Medigap (or Medicare Supplement) plans help with out-of-pocket expenses (like copayments) from Original Medicare.

If you haven’t written a will yet, now’s a good time to do it. Include your wishes regarding medical treatment if you are on life support or in a coma. The will should also identify someone who will make medical and financial decisions on your behalf if you become unable to make them for yourself.

The rest of your will should set forth how you want your assets distributed. If you do not put your wishes into writing, your assets will be distributed according to state and federal laws.

While it can be intimidating to create a will, it’s important because it will lift decision-making burdens from your children and caretakers. You can use online resources to create your will yourself or go over it with an attorney. Reviewing it with an attorney can help you think through potential scenarios and plan for them.

Paying for Your Final Expenses

You also need to consider how your funeral and final costs will be paid. Funerals are expensive. The National Funeral Directors Association (NDFA) found that the median funeral costs with a viewing were $6,260 for cremation and $8,755 for burial in 2017.

If you have enough savings to pay for it yourself, you need to realize that probate will delay your beneficiaries’ access to those funds. Probate is the legal process for reviewing a will or applicable laws and disbursing everything out accordingly.

You do not want to put family and friends in a financial bind when planning your funeral.

You can buy a final expense or burial insurance policy.

If you know where you want to be buried and which funeral home you want to use, then it may be worth pre-paying for your funeral. Choose the funeral home wisely because if you prepay and the funeral home closes, you might be out of luck. You’ll also want to be sure that it’s a reputable funeral home.

Alternatively, you can buy a final expense or burial insurance policy. These policies are designed for seniors and are a kind of permanent life insurance policy. These permanent policies have lower coverage levels because they are meant to cover final expenses and funeral costs.

Once you have all these details taken care of, you’ll be able to stop worrying about problems you may encounter and how you’ll leave your loved ones. You’ll be able to maximize your time enjoying your golden years and cherish moments with family and friends.

Healthy Soups for Seniors

There are thousands of unique soup recipes out there on the internet. While soup may only be as healthy as the ingredients inside it, Eatingwell.com reports that soup-eaters have “higher intakes of fiber, vitamin A, magnesium, iron, and potassium, which are all important for a healthy diet, especially for aging seniors! Soups also tend to be relatively low in calories!

Granted, like everything else, you should enjoy soup in moderation. Soups also tend to be high in sodium, which can raise your blood pressure. The potassium content in many soups can even the sodium out, but it’s still not something you want to over-indulge in.

Healthiest Soups for Seniors

The way you prepare and consume a soup can determine whether or not it’s healthy for you. “Healthy” can also depend on your specific dietary needs.

However, the following soups can be deliciously healthy when prepared correctly!

Broth is made of bones and tissue usually derived from chicken, cows, or even fish. Broth can be rich in vitamins and minerals like calcium, magnesium, and phosphorous. MedicalNewsToday says that broth can strengthen your joints, fight osteoarthritis, reduce inflammation, support weight loss, and even aid sleep.

Osteoarthritis is one of the most common forms of arthritis, affecting millions each year. Arthritis can become a legitimate concern. Arthritis happens when your bones wear down from overuse, which can become more possible as you age.

Tomato-based Soups

Tomatoes are loaded with vitamin C and antioxidants and are sometimes considered a superfood. Uniquely, they also contain lycopene, a plant compound that gives tomatoes their red color and has been linked to prostate cancer prevention. Tomatoes are one of the few sources of lycopene. Tomatoes have also been proven to help maintain blood pressure, support heart health, improve insulin levels in diabetic people, reduce constipation, and improve skin and eye health.

Tomato Soup for Seniors

Lentil-based Soups

Lentils are high in fiber and nutrients like vitamin B, iron, magnesium, potassium, and zinc. They also contain phytochemicals, which protect against chronic diseases like heart disease and type 2 diabetes. Again, like everything, it’s important to only enjoy lentils in moderation. Uniquely, they contain “antinutrients,” which can reduce your intake of other nutrients. Thankfully, you would have to eat a lot of lentils for this to pose a real problem!

Healthy Canned Soup

In many cases, canned soups are not going to be nearly as healthy as a fresh, home-made batch. However, sometimes, you just don’t have the time or energy to make yourself some fresh soup! Canned soup can be very cheap at your local grocery store (and even online), and it’s not always terrible for you.

When looking for healthy canned soups, look at the nutrition label and look for low sodium content, less calories, and more vitamins and minerals. Additionally, canned soups tend to have high levels of BPA. Consider looking for soups packaged in “Tetra Pak” or other cardboard/BPA-free solutions.

We found this recipe for split-pea soup that serves six people from Epicurious! You could probably substitute out a different cut of pork (for example, if you have some leftover ham from Thanksgiving, throw that in there)!

Ingredients:

2 tbsp butter

1 chopped large onion

1 cup chopped celery

1 cup chopped peeled carrots

1 ½ pounds smoked pork hocks

2 tsp dried leaf marjoram

1 ½ cups green split peas

8 cups water

Directions:

Melt butter in large pot or dutch oven over medium-high heat

Add onion, celery, and carrots

Saute until vegetables soften (about eight minutes)

Add pork and marjoram; stir for one minute

Add peas, then water; bring to boil

Reduce heat to medium-low and partially cover pot

Simmer until pork and vegetables are tender and peas are falling apart; stir often (about 70 minutes)

Transfer hocks to a bowl

Puree five cups soup in batches in a blender; return to pot

What happens to your health insurance when you retire? Medicare and retirement can seem intimidating, but we’re here to ease some of your concerns and answer your questions.

There are currently an estimated 70 billion baby boomers who are nearing retirement. Planning for retirement is crucial to living a comfortable and healthy life. An annual estimate by Fidelity shows the average couple retiring at age 65 will need $280,000 to cover health-related costs. Fortunately, Medicare can help, but there is a set of guidelines and regulations regarding enrollment.

How Medicare and Retiree Coverage Work Together

Some employers may offer retiree health coverage, which can be a good option if you are not yet 65 and do not meet other Medicare eligibility requirements. If you are 65, it may be time to enroll in Medicare.

If you are already 65 when you retire and are interested in having both retiree coverage from your employer AND Medicare, the two can work together.

Your Medicare coverage will always come first. Your retiree coverage will work as extra coverage to backup your Medicare plan – kind of like a Medicare Supplement plan.

While retiree coverage is not a Medicare Supplement plan, it is very similar. It can cover things like copayments and deductibles, or even extra hospital stay days. All retiree plans are different, though, so look over your plan and call your insurance agent (or your former HR representative) to find out what it covers.

Do Retirees have to Pay for Medicare?

There are two parts to Original Medicare – Part A and B. If you have worked and paid Medicare taxes for at least 40 quarters (about 10 years), you can have premium-free Part A. If you did not work the 40 quarter minimum, then you will have to pay the Part A premium. For 2020, the Part A premium is $458 for 30+ quarters or $252 for 30-39 quarters.

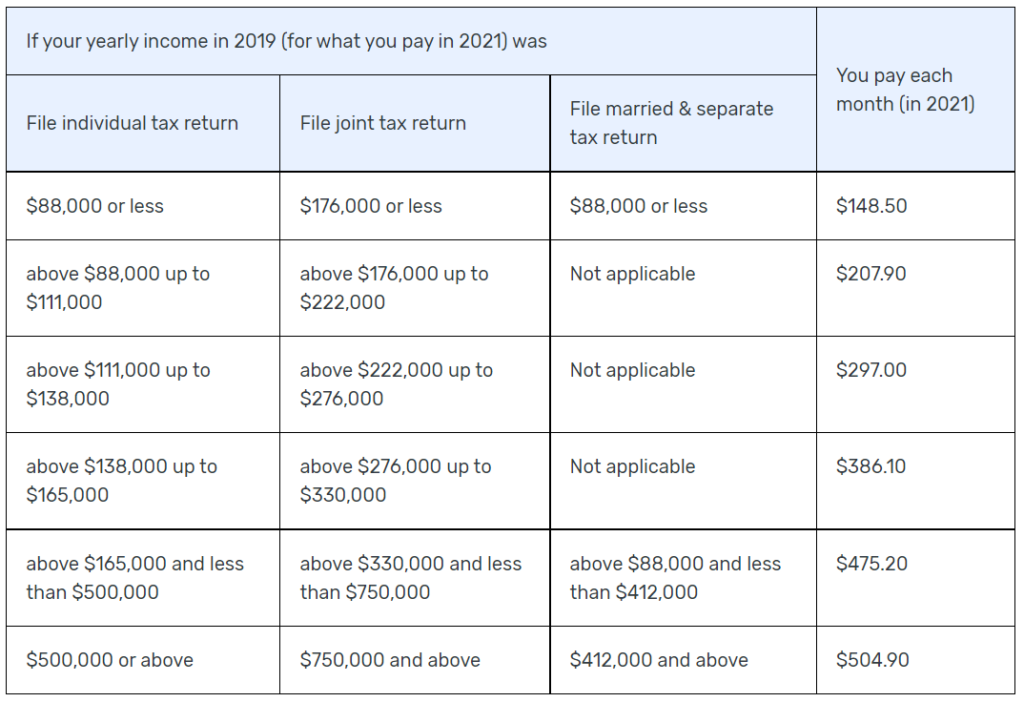

The standard Part B premium for 2020 is $144.60, but you may pay more or less based on your own set of circumstances. An estimated 3.5% of beneficiaries will have a lower premium due to the Social Security “hold harmless” provision which prevents premiums from exceeding Social Security benefits. Plus, if you make more than $87,000 a year, your monthly Part B premium will be adjusted based on your income. The income-based 2019 Part B premiums are as follows:

2020 Medicare Part B Premiums

Do you Automatically get Medicare When you Turn 65?

If you currently receive Social Security benefits, you will be automatically enrolled in Medicare Parts A and B the month you turn 65. However, if you do not receive Social Security benefits, you will need to enroll yourself. Medicare enrollment begins three months before your 65th birthday and will end three months after. This is called your initial enrollment period.

It’s important to act right away because delaying your enrollment can result in a 10% Part B premium increase for every year you’re eligible but don’t enroll. If you don’t select prescription drug coverage and later enroll, you may have a penalty of 1% the national base Medicare Part D monthly premium for each month you were not enrolled.

Health Insurance After Retirement Before Medicare (Early Retirement)

Should you keep working or retire early? Your decision may be influenced by your age, health, budget, Medicare eligibility, social security benefits, and employer coverage.

Employer Retiree Coverage

Some employers offer retiree coverage after you leave the company. However, retiree coverage and Medicare are not the same. Retiree coverage is health coverage that is provided to former employees of a company. This typically pays second to Medicare, which means you still need to enroll in Medicare to be fully covered. However, retiree coverage can help with health-related expenses if you retire before 65.

Not every employer offers retiree coverage. Since it isn’t required, your employer (or former employer) can cancel or change your retiree plan at any time. It’s safest for you to have Medicare as well. Plus, if you don’t enroll in Medicare when you first become eligible, you will face a penalty fee. Some retiree plans automatically stop when you turn 65 and become eligible for Medicare.

If your employer does not offer retiree coverage, retiring or losing your job gives you a SEP. A Special Enrollment Period means that you don’t have to wait for AEP, the Annual Enrollment Period, to buy coverage. You will have 60 days from your last day of work to enroll in a marketplace health plan. After those 60 days are over, you’ll have to wait until AEP (October 15 – December 7) to buy a marketplace plan, at which point you will be charged a penalty fee for having a lapse in coverage.

FERS/CSRS Retirement and Medicare

The CSRS, or Civil Service Retirement Act, became effective on August 1, 1920. It was replaced by the Federal Employees Retirement System (FERS) on January 1, 1987. Some people may still belong to CSRS. Both programs are for government employees only.

Both FERS and CSRS allow you to retire at age 62 if you have five or more years of service or at age 60 if you have 20 or more years of experience. Under FERS, you can retire between ages 55 and 57 (depending on your birth year) if you have 30 or more years of service.

Regardless of your FERS or CSRS status, if you’re 65, you’ll qualify for Medicare. You’ll also qualify for Medicare if you have a qualifying disability. If you are under 65 and do not qualify for Medicare, you can receive your FERS or CSRS benefits but will have to wait until you reach Medicare qualifying age.

Until then, you may qualify for the Federal Employees Health Benefits Program (FEHB). Once you do become eligible for Medicare, you may want to enroll in Part A anyway because there is no premium if you’ve worked for at least 40 quarters.

COBRA

When you leave your job, you’ll also have the option to enroll in COBRA. COBRA allows you to continue to belong to your employer’s group plan for a temporary period after you leave the company. The company can “kick you off” at any time, so this is not a permanent option. However, COBRA can help you out while you figure out what your other options are.

Ask your employer or your HR representative to find out what COBRA might look like for you.

Can you get Medicare at age 62?

It’s important to understand the differences between Social Security and Medicare. You can start to receive Social Security retirement benefits at the age of 62. This amount is typically reduced until you reach the age of 65. The average person does not qualify for Medicare until age 65, but there are exceptions.

You are automatically enrolled in Medicare once you have received Social Security benefits for two consecutive years. This means if you started receiving benefits at age 62, you will qualify for Medicare at age 64. Plus, you may qualify for Medicare before 65 if you have Lou Gehrig’s Disease (ALS) or End-Stage Renal Disease.

Importance of PlanningforRetirement

It’s never too early to start planning for retirement and Medicare. Our licensed agents can help explain your coverage options and answer all of your questions. Plus, they can provide bias-free assistance with a wide range of plan options because they are licensed with all major carriers in your state. Start planning now! Call us at 844-431-1832 or fill out this form to arrange a no-cost, no-obligation appointment.

This post was originally published on December 27, 2018, and was last updated on November 15, 2019.

$0 Premium Humana Honor Plans for Veterans

Humana is one of the biggest Medicare Advantage carriers, with over 8.4 million members across all 50 states (plus D.C. and Puerto Rico). They’ve been active for over three decades! New this year, Humana is providing a “Humana Honor” Medicare Advantage plan.

Uniquely, though it is “available to anyone eligible for Medicare” who lives in the service area, this Medicare Advantage plan is designed to complement VA (Veteran’s Affairs) coverage. Many veterans think they have no use for Medicare Advantage (or even Medicare at all) due to their VA coverage, but a plan like this could be a game-changer.

Do you Need Medicare if you have VA Coverage?

For some people, the VA may provide all the coverage you need. But, if you can get additional coverage at no extra cost, why not take it?

Plus, even though there are 1,921 VA facilities across the country, wait times can be a problem. You can use this tool to find out what your local wait times are, but you might not need to if you have additional coverage. If you also have Medicare (and if you have Medicare Advantage), your network can be expanded to many more local doctors and other medical facilities, where you may have an easier time getting an appointment.

Plus, the VA does not automatically provide dental coverage to all veterans. You can purchase it through the VADIP (VA Dental Insurance Program), but you might not need to. If it makes sense for you and if it is available in your area, you can instead enroll in a Humana Honor or other Medicare Advantage plan that includes a dental benefit.

Humana Honor is available as 17 different plans available in 28 states:

Alabama

Arizona

Arkansas

California

Colorado

Delaware

Florida

Georgia

Idaho

Illinois

Indiana

Kansas

Louisiana

Maryland

Michigan

Mississippi

Missouri

Nevada

New Mexico

New York

Ohio

Oklahoma

Oregon

Pennsylvania

South Carolina

Tennessee

Utah

Washington

How to get Humana Honor Medicare Advantage

There are a few ways you can enroll in Humana plans, but we recommend speaking with a licensed agent. An agent can help you sort through all your options and make sure that the plan you like is truly the best plan for you. It is free to speak with a licensed agent regarding your healthcare, so it can only help!

You can speak to a MedicarePlanFinder.com agent by calling 844-431-1832 during business hours or clicking here.

Humana Taking Care of Veterans

Humana has strong relationships with (and is the national Medicare plan carrier for) the VFW (Veterans of Foreign Wars) and AMVETS (American Veterans). Infact, Humana partnered with the VWF’s “Uniting to Combat Hunger” campaign and helped raise money for over 500,000 veteran meals.

Humana has also contributed over one million dollars to the Entrepreneurship Bootcamp for Veterans with Disabilities, an organization that serves post-9/11 veterans. They also sponsor the Washington, D.C. Rolling Thunder Motorcycle Run during Memorial Day weekend, as well as the Wounded Warrior’s “Warrior Games.”

Additionally, Humana’s administration has hired over 4,500 veterans and veteran spouses since 2011.

Whether you like Humana’s Medicare Advantage plans or not, you have to give them props for their work with veterans and veteran families!

We’re proud to offer Humana plans through our insurance brokers and are excited to be a part of providing veterans with the care they deserve.

Common Neurological Disorders in the Elderly

According to the World Health Organization, “neurological disorders are a common problem. For example, 50 million people have epilepsy.” Some common neurological disorders in the elderly like Alzheimer’s disease and Parkinson’s disease become more likely as you age, and there’s no sure-fire way to prevent those diseases. That makes having resources to get the proper healthcare such as health insurance and access to the right doctors extremely important.

Click on the Links Below to Learn More About Common Neurological Disorders in the Elderly

List of Neurological Disorders in Elderly Patients

Neurological disorders are diseases and conditions that affect the central nervous system (brain and spine). According to the US National Library of Medicine, there are more than 600 types of neurological disease. Here’s a list of common neurological disorders in the elderly:

Diseases caused by genetic factors, such as Huntington’s disease

Problems with the way the nervous system and/or skeletal system develops, such as spinal stenosis

Degenerative diseases, in which nerve cells are damaged or die, such as Parkinson’s disease and Alzheimer’s disease

Diseases of the blood vessels that supply oxygen and nutrients to the brain, such as stroke

Injuries to the brain and/or spinal cord

Seizure disorders, such as epilepsy

Brain cancer

Medicare Special Needs Coverage for Chronic Diseases

Original Medicare (Parts A and B) may cover many preventive services & screenings, diagnostic screenings, and treatment for neurological diseases. Some neurological conditions may make you eligible for a special type of Medicare plan called a Chronic Special Needs Plan (CSNP).

CSNPs are plans designed to fill the needs that a chronic disease like a neurological disorder may cause. For example, many CSNPs offer coverage for services not included with Original Medicare such as prescription drugs, meal delivery, and extended home health care services. They also feature coordination of care between your healthcare providers.

If you have a CSNP, you may be eligible for a Special Enrollment Period (SEP), which allows you to make changes to your coverage as your medical needs change, rather than at specific times of the year. Many Medicare enrollees have to wait until the Annual Enrollment Period (AEP), which is from October 15 to January 7.

All of the diseases on the above list may qualify you for a CSNP and a SEP.

Amyotrophic Lateral Sclerosis (ALS)

According to the ALS Association, “ALS, or amyotrophic lateral sclerosis, is a progressive neurodegenerative disease that affects nerve cells in the brain and the spinal cord.”

The most noticeable symptom is progressive muscle weakness, which may mean that you can’t firmly grasp a pen in ALS’ beginning stages Other early symptoms include tripping, muscle cramps, or bouts of uncontrollable laughing or crying may surface. As the disease progresses, you’ll lose muscle control including the muscles that enable you to walk.Eventually, the disease will cause the breathing muscles to stop working, and the lungs may collapse.

Medicare Coverage for ALS

ALS is one of two diseases that may make you eligible for Medicare before you turn 65. The other is ESRD. According to the ALS Association, your Medicare benefits start as soon as you become eligible for SSDI.

ALS is a chronic condition that may make you eligible for a CSNP, which may cover home care, meal delivery, and/or prescription drugs. Original Medicare may cover extended home care services, including:

Skilled nursing services (such as assistance with a feeding tube or ventilator) if you need them on an intermittent or part-‐time basis. Skilled nursing services are usually provided by a registered nurse (RN) or a licensed practical/vocational nurse (LPN/LVN).

Assistive (personal) care services (such as help with bathing or getting dressed) may be covered, but only when they are needed to support skilled nursing care, and only on an intermittent or part-time basis. Medicare does not cover assistive care if it is the only care that you need. Assistive care services may be provided by a home health aide (HHA) or certified nursing assistant (CNA).

Therapy services such as physical therapy, occupational therapy, and speech-‐ language pathology services when these services are necessary to help you maintain or regain the ability to move, perform everyday tasks for self-care, speak, or swallow safely. A licensed therapist must oversee the services in order for Medicare to cover them.

Medical social services (such as counseling) are covered by Medicare when your doctor orders them.

Medical supplies and durable medical equipment (DME). Disposable medical supplies are covered by Medicare when they are used as part of your care. Medicare also pays 80 percent of the cost for durable medical equipment (such as a hospital bed, walker, or wheelchair) when the doctor prescribes the equipment for in-home use.

Medicare may also cover a second opinion if you receive an ALS diagnosis.

Brain Cancer

Brain tumors — masses of cells that occur in your brain — may be cancerous (malignant) or not (benign). Tumors may start in the brain (primary brain tumors), or they may start in other parts of the body and spread to your brain (metastatic, or secondary brain tumors).

Brain Cancer Symptoms and Treatment

You should see a doctor if one or more of these symptoms become consistent and bothersome:

New onset of, or a change in headache patterns

Headaches that gradually become more frequent worse

Unexplained nausea or vomiting

Vision problems, such as blurred vision, double vision or peripheral vision loss

Gradual loss of sensation or movement in an arm or a leg

Difficulty balancing yourself

Speech difficulties

Confusion

Changes in personality or behavior

Seizures, especially if you don’t have a history of seizures

Hearing problems

Risk factors for brain tumors include family history and radiation exposure.

Neurological exams and imaging such as MRI are the most common methods to test for brain tumors. Your doctor may recommend a CT scan to look for cancer in other parts of the body.

Your doctor may recommend surgery, depending on the size and location of the tumor. Your doctor may also recommend chemotherapy, radiation, and/or targeted drug therapy. Rehabilitation therapies after your treatment may include occupational therapy, physical therapy, and speech pathology.

Dementia & Alzheimer’s Disease

Dementia is a term used to describe a syndrome with symptoms that include memory loss, difficulty with problem-solving, and struggling with language and processing thoughts.

There are over 100 types of dementia, and Alzheimer’s disease is one cause. Some forms of dementia can be temporary. Other types can be cured. Alzheimer’s disease is neither temporary nor curable.

Dementia Symptoms and Treatment

Dementia symptoms can be changes in cognitive ability or psychological changes.

Cognitive changes

Memory loss

Difficulty finding the right words during conversation

Getting lost while driving familiar routes

Difficulty with logical reasoning or problem-solving

Difficulty completing complex tasks

Difficulty planning and organizing daily activities

Difficulty with muscular coordination and motor functions, such as hand-eye coordination

Being confused or disoriented easily

Psychological changes

Changes in personality

Depression

Anxiety

Irrational, inappropriate, or out-of-the-ordinary behavior

Paranoia

Agitation

Hallucinations

Treatments for dementia include medication for memory such as cholinesterase inhibitors and memantine. Some doctors may prescribe antidepressants, anxiolytics, or antipsychotic medications in people who display drastic behaviors.

Some researchers believe that herbal remedies, dietary supplements, and certain foods can enhance memory and prevent Alzheimer’s. Some examples include coconut oil, coral calcium, and omega-3 fatty acids. Researchers also suggest that memory games and puzzles can help prevent dementia or slow its progression.

Medicare may cover testing for dementia and Alzheimer’s like cognitive tests during your Annual Wellness Visit.

Some nursing homes and assisted living facilities feature memory care services, which is a specific type of long-term care for dementia patients. Original Medicare does not cover room and board for assisted living or nursing homes, however, certain life insurance or long-term care insurance policies can. Medicare Part A and Part B may help pay for medical expenses while you live in a nursing home or assisted living facility.

According to NAEC, treatment for epilepsy has different levels of care: primary, neurologists, and epileptologists and epilepsy centers.

Primary Care: The first level of epilepsy care starts with an evaluation in an emergency room or at a primary care provider’s office. Treatment usually includes anti-epileptic medication. According to NAEC, the first medication prescribed will effectively control seizures without causing side-effects for many patients. If the doctor finds an effective way to control seizures, further specialized epilepsy evaluation may be unnecessary.

Neurologists: If a primary care provider can’t find a way to control seizures within three months, the primary care provider will refer the patient to a neurologist. A neurologist is a doctor who specializes in diseases of the brain and central nervous system. Once the seizures are under control, the patient can be transferred back to the primary care provider.

Epileptologists and Epilepsy Centers: If a patient continues to have persistent seizures or side effects may be transferred to an epileptologist, which is a doctor who specializes in epilepsy. Some patients may be transferred to a specialized epilepsy center. The third level of care aims to reduce the frequency of seizures and/or medication side effects for patients.

According to the Epilepsy Foundation, Medicare Part D and certain Medicare Advantage plans cover prescription drugs. The Epilepsy Foundation and NAEC are working to ensure that patients have access to the “therapies they need” because “epilepsy medications are not interchangeable.”

Some drugs may be too costly for patients, and low-income patients may qualify for LIS (Low Income Subsidy) or Extra Help. Eligibility is based on your income and/or assets and the Federal Poverty Level. Ask your agent to help you apply if you think you may qualify.

Symptoms usually appear between the ages of 30 and 50, and they worsen over a period of 10-25 years. Ultimately, the person “succumbs to pneumonia, heart failure, or other complications.”

According to HDSA, “Everyone has the gene that causes Huntington’s Disease.” However, only people who inherit the “expansion of the gene” will develop Huntington’s disease and they are more likely to pass the expanded gene to their children. Every person who inherits the expanded gene will develop Huntington’s disease. Eventually, the disease will affect the person’s “ability to reason, walk, and speak.”

Huntington’s Disease Symptoms and Treatment

Huntington’s disease symptoms include:

Changes to personality and mood swings

Depression

Forgetfulness

Impaired judgment

Irregular gait

Involuntary movements

Significant weight loss

Slurred speech

Difficulty swallowing

If you’re no longer able to work, Huntington’s disease may qualify you for SSDI. You may be eligible for Medicare if you’ve collected SSDI for at least 25 months, even if you’re younger than 65.

Medicare may cover the following tests for Huntington’s disease:

Genetic counseling and testing

Home health assessments

Motor assessments to examine eye movement, involuntary movements (chorea), gait, coordination and slowness in movement and stiffness

Neurocognitive testing

Neurological exam

Psychiatric consultation

There is no cure for Huntington’s disease, but Medicare may cover the following treatments:

Occupational therapy

Physical therapy

Psychotherapy

Speech therapy

Individual and family counseling

Palliative care

Medicare Part D or certain Medicare Advantage plans may cover the following medications:

Antidepressants

Antipsychotic medications

Involuntary movement medications

Mood-stabilizing medications

Multiple Sclerosis

Multiple sclerosis is another common neurological disorder in the elderly. According to the National Multiple Sclerosis Society, “multiple sclerosis (MS) is an unpredictable disease of the central nervous system” that interferes with the flow of information within the brain, and between the brain and the rest of the body.

Multiple Sclerosis Symptoms and Treatment

Symptoms of MS include:

Fatigue

Difficulty walking

Tingling or numbness

Weakness

Dizziness and vertigo

Pain and itching

Depression

Mood swings

Irritability

Spasticity (stiffness and muscle spasms)

Vision problems

Cognitive changes such as the inability to process and remember information

Testing for multiple sclerosis can include MRI, spinal fluid analysis, and blood tests to rule out any other medical conditions.

MS can cause damage to the myelin, which is a mixture of proteins that increases nerve impulse transmission speed. The damage blocks or slows nerve impulse transmission. If myelin is damaged, sometimes corticosteroids can help repair the damage.

A comprehensive MS treatment plan can include rehabilitation that focuses on function — meaning the treatment helps you improve your ability to perform safely and effectively at home or work. Other treatments include medications such as Avonex and Gilenya to help manage symptoms and/or modify the course of the disease.

Parkinson’s Disease

Parkinson’s disease affects the central nervous system. Over time, the disease affects movement and symptoms get worse. Symptoms of Parkinson’s start small, such as a barely noticeable tremor in one hand. Other symptoms include:

Slowed movement that can make simple tasks more difficult over time

Muscle stiffness

Quick, slurred, or soft speech

Changes to posture or balance such as slumping over when standing

Parkinson’s may be caused by genetic and/or environmental triggers. Rare genetic mutations may be associated with the disease. The mutations cause changes such as Lewy bodies, which are abnormal protein aggregates that form in nerve cells, and alpha-synuclein (a protein) in the Lewy bodies. Scientists believe that alpha-synuclein is the number one indicator of Parkinson’s.

Risk factors include a family history of Parkinson’s, age (most people who develop the disease are 60 or older), sex (men are more likely than women to develop the disease), and environmental factors including exposure to pesticides.

Parkinson’s causes are unknown, so there’s no proven way to prevent it. However, some research shows that regularexercise and caffeine may reduce the chances of developing Parkinson’s.

Testing for Parkinson’s includes analyzing tremors, movement, muscle stiffness, and balance. Your doctor may refer you to a movement disorder specialist for further diagnostic testing.

According to the US National Library of Medicine, paralysis is the loss of muscle function in part of your body. Most paralysis is due to spinal cord or neck injuries or stroke. Other causes include ALS or autoimmune diseases.

In order for paralysis to qualify you for a Special Needs Plan, your paralysis must be “extensive.” Qualifying paralysis includes:

Monoplegia: Paralysis that only affects only one arm or leg

Hemiplegia: Paralysis that affects one arm and one leg on the same side of your body

Paraplegia: Paralysis affects both legs

Quadriplegia or tetraplegia: Paralysis that affects both arms and both legs

If your paralysis makes it so you can’t work, you may qualify for SSDI. You may be eligible for Medicare after you receive SSDI for 25 months. You may also qualify for Medicare when you turn 65.

Medicare Part A may cover hospital services, skilled nursing care, home health care, and hospice care. Medicare Part B may cover occupational therapy and DME such as powered wheelchairs.

Polyneuropathy

Polyneuropathy is the most common type of peripheral neuropathy. The condition is a result of nerve damage outside of the brain and spinal cord. It can often cause weakness, numbness, and/or pain, usually in your hands and feet. Sometimes polyneuropathy can cause difficulty swallowing, breathing, and/or moving your eyes.

Polyneuropathy is most-commonly caused by diabetes. Less commonly, polyneuropathy develops due to hereditary causes. Sometimes the causes are unknown.

According to the Mayo Clinic, testing for polyneuropathy includes blood tests, imaging tests such as CT or MRI scans, and a neurological examination including EMG.

Treatments include medications such as pain relievers, anti-seizure medications such as Lyrica, topical treatments such as capsaicin cream, and antidepressants such as Pamelor and Silenor. Pain from diabetic polyneuropathy may be treated with Cymbalta.

Other treatments include nerve stimulation (TENS), plasma exchange and intravenous immunoglobulin, physical therapy, and/or surgery.

Spinal Stenosis

Spinal stenosis is when the spaces in your spine become more narrow. The narrowing can put pressure on the nerves within the spine. Sometimes, spinal stenosis doesn’t produce symptoms. Other people may experience pain, numbness, a tingling sensation, and/or muscle weakness. Symptoms can become worse over time.

Cervical stenosis is when the narrowing occurs in your neck, and lumbar stenosis occurs in the lower back. Both types of stenosis can cause numbness and tingling and/or weakness. Cervical stenosis can cause problems with balance and walking, neck pain, and/or bladder dysfunction. Lumbar stenosis can cause back pain and/or leg cramps or pain. According to the Mayo Clinic, you should see a doctor if you experience any of those symptoms.

An overgrowth of bone, herniated disks, tumors, spinal injuries, and/or thickened ligaments (tough cords that connect the vertebrae) can cause spinal stenosis. The condition mostly affects people over 50, but conditions such as trauma and genetic diseases may cause stenosis.

Your doctor may use spinal imaging tests such as MRI, X-rays, or CT to diagnose spinal stenosis and pinpoint the cause.

Treatment for Spinal Stenosis

Your doctor may prescribe over-the-counter pain relievers such as ibuprofen, prescription pain pills such as oxycodone, antidepressants, and/or anti-seizure drugs such as Neurontin. Other treatments can include physical therapy, corticosteroid injections, and/or a decompression procedure that uses “needle-like instruments to remove a portion of a thickened ligament in the back of the spinal column.”

Your doctor may also recommend surgery or alternative therapies such as chiropractic care and acupuncture.

Stroke-Related Neurologic Deficit

According to the Mayo Clinic, a stroke occurs when the blood supply to part of your brain is stopped or limited. The blockage deprives your brain of oxygen and nutrients, which causes brain cells to die. Strokes can cause a neurologic deficit, which is abnormal functioning of an area of the body. The deficit happens when the brain, spinal cord, muscles, or nerves have weaker functioning.

The most common cause of stroke is blood clots either in one of the arteries that supply the brain with blood (thrombotic stroke) or in an artery away from your brain (embolic stroke). Other causes of stroke include blood vessel ruptures or leaks (hemorrhagic stroke).

Risk factors for stroke include:

Hypertension

Smoking

Diabetes

Obesity

Alcoholism

Sedentary lifestyle

You can help prevent a stroke by watching your diet, quitting smoking, exercising regularly, and avoiding excess alcohol use.

Stroke Symptoms and Treatment

According to the American Stroke Association, you should use the acronym FAST to spot signs of a stroke and know when to call 9-1-1. FAST stands for:

Face drooping, which means one side of the face droops or it’s numb.

Arm weakness, which means that one arm feels weak or numb.

Speech difficulty, which can mean slurred speech.

Time to call 9-1-1. Call 9-1-1 if the person displays any of these symptoms, even if they’re temporary. These symptoms indicate an emergency, and the person needs to get to a hospital.

Other symptoms include sudden confusion, trouble seeing, walking, and/or a severe headache that doesn’t seem to have a cause.

According to Medicare.gov, “Medicare covers medical and rehabilitation services while you’re in a hospital or skilled nursing facility.” Medicare Part B may also help pay for physical therapy and occupational therapy.

Medicare preventive services for stroke include:

Cardiovascular disease screening such as blood cholesterol screening

Find Coverage for Common Neurological Disorders in the Elderly

Some of the most common neurological disorders in the elderly and other Medicare eligibles can be prevented, treated, and/or managed. The right health insurance plan can help. An agent with Medicare Plan Finder can see what’s available in your area and give you information. Our agents can assist you with finding a plan that meets your budget, medical, and lifestyle needs. Call 1-844-431-1832 or contact us here to set up a no-cost, no-obligation appointment today.

What is Medicare Part B Buy Back/Give Back?

Are Medicare Buy Back plans too good to be true?

No!

Can they really put money back into your social security check?

Yes, it’s offered through SOME Medicare Advantage plans but not all.

Here is how it works.

Some Medicare Advantage plans out there that can “buy back” your monthly Part B premiums, ultimately putting money back into your pocket. You’ve likely seen this on TV, but unfortunately it’s misleading as this specific benefit is narrowly used by a few plans across the country.

These plans are effectively paying you instead of the other way around! Let me explain.

Medicare Part B Premiums in 2022

In 2022, the standard Medicare Part B premium will be $148.50. Your premium may be a bit higher if you have a higher income. Below is a snap shot directly from Centers for Medicare and Medicaid about the current Part B premium scale.

The reason you have to keep paying this premium is because Medicare Part B is a paid program, unlike Medicare Part A which you earned during your working years by paying social security taxes. By default, everyone has to pay for Medicare Part B unless they get some kind of financial assistance.

While Medicare Part B is a part of original Medicare, Medicare Advantage plans are privately owned and offer additional benefits beyond original Medicare. In particular, Part B buy back is an additional benefit offered by some plans. This is sometimes confusing to many people, so bear with me.

To have Medicare Advantage, you must be enrolled in original Medicare Parts A and Parts B. In order to be enrolled in original Medicare, you must have worked 40 quarters (or 10 years) paying into social security to earn Part A, and then pay a monthly premium for Part B. To stay enrolled, you have to continue paying your premiums!

You can’t get a Medicare Advantage plan without having original Medicare.

What are Medicare Advantage Part B Buy Back Plans?

Medicare Advantage plans are additions to your existing Medicare coverage. They can vary greatly in coverage amounts and premium prices. Some Medicare Advantage plans can come with a $0 premium or a low premium in addition to a Part B buy back (or give back, as some plans call it).

If you pay your Part B premium automatically out of your Social Security check, this could feel like a bonus added to your monthly checks! You’ll start seeing a bit more coming in, which is nice, assuming the plan you choose has the buy back option.

Premium Give Back Plan? What’s the Catch?

You’re probably skeptical about the idea of an insurance company wanting to give YOU money.

However, there’s not really a catch. According to Quality Health Plans of New York, Medicare Advantage plans “may choose to use some of the funding it receives” to “reduce its members Medicare Part B premium.”

So, what these plans are doing is providing you an incentive to sign up for their plans.

Even if they give you some of that money back for your Part B premiums, they still get paid from your copayments, deductibles, etc.

As you’re looking into available Medicare Advantage plans that offer Part B buy back benefits in your area, be sure to consider what you might be giving up.

Remember, all plans are different, but it is possible that a plan with a Part B buy back option will have higher copayments and deductibles – which may not matter to you if you don’t spend a lot of time in the doctor’s office! The devil is in the details.

I guess you could say the only true “catch” to these plans is that you have to stay enrolled in Medicare parts A and B – but that’s true of any Medicare Advantage plan. You’ll have to continue paying your A and B premiums, even if you do get some of that money back.

Additionally, it may be a few months after you sign up for your premium give back plan before you receive your first Part B reimbursement.

How do I Get a Part B Buy Back (Give Back) Plan?

Great question! As you can imagine, these plans might be harder to find than more standard Medicare Advantage plans, and there may or may not be one available in your area.

Unfortunately, CMS (Centers for Medicare and Medicaid Services) does have certain rules in place that forbid us from sharing the plan details with you publically. However, we have licensed agents across the nation who can meet with you either in person or by phone to help you choose a plan.

If you’re interested, call us at 800-691-1832. Let us know that you’re interested in Part B buy back plans, and we’ll do all we can to help! You can also leave us a message here, and we’ll get back to you.